acf439 corporate finance: a student's handbook

TRANSCRIPT

International Business School Suzhou (IBSS)

学贯中西

兼善天下

Combining East and West

Creating a Better World

MODULE HANDBOOK

ACF439

Corporate Finance

Associate Professor Dr. Warren Wu

Semester 1

2015/2016

Page 2 of 17

SECTION A: BASIC INFORMATION

Brief Introduction to the Module

This module provides students with the knowledge of financial activities within a dynamic corporate setting

and develops the capabilities for them to skilfully engage relevant financial-management issues and

effectively make critical or strategic financial decisions. Students will learn about how to assess and

choose new investment or corporate-restructuring opportunities that are expected to earn returns higher

than the minimum rates of return required by the company’s fund-providers in a manner that reflects

embedded investment risks and its optimal funding mixes. Students will also learn how to analyse and

choose funding mixes between debt and equity that either maximise the values of existing

investments/assets or minimise the required rates of return of new investments/corporate structures in

order to increase the overall value of the company. It forms part of the curriculum of semester 1 of the

full-time MBA. As such, it provides (along with others) key knowledge and understanding of one of the

core functional areas and activities of advanced management practice.

Key Module Information

Module Name: Corporate Finance

Module Code: ACF439

Credit Value: 2.5 credit hours

Semester in Which the Module is Taught: Semester 1

Pre-requisites Needed for the Module: None

Programmes on Which the Module is Shared: None

Delivery Schedule

Lecture Room: BA209 (Monday) & BB123 (Thursday)

Lecture Time: 1100-1300 (Monday) & 0900-1100 (Thursday)

Tutorial Times: None

Module Leader and Contact Details

Name: Associate Professor Dr. Warren Wu

Email Address: [email protected]

Office Telephone: +86 (0)512 8816 7897

Room and Office Hours: BB338 Monday 1300-1500

Preferred Means of Contact: Email channel

Brief Biography:

Dr. Warren Wu is an Associate Professor of Finance with substantial experience in industry and university

teaching with positions in the US, Australia, New Zealand, Macao, and Thailand. As dean of a business

school in Thailand, he created coaching programs to support both CFA® and FRM® studies. As a Fulbright

Scholar in financial economics, he has taught a number of subject areas in finance but has specialized

expertise in financial modelling and creating risk analytic models for market VaR and credit risk modelling

for portfolio optimization. His industry experience started in the oil and gas industry and later became an

Economics Policy Researcher for the Finance Ministry of the Government of Thailand. Warren has

completed numerous consulting projects for banks and other institutions during this time as well and has

many publications, including two editions of his textbook on financial modelling and analysis (Pearson).

Page 3 of 17

SECTION B: WHAT YOU CAN EXPECT FROM THE MODULE

Educational Aims of the Module

1. To provide students with the knowledge about corporate finance and develops their capabilities to

skilfully manage financial resources and effectively make critical or strategic financial decisions;

2. To equip the students with appropriate analytical tools and decisional techniques to assessing and choose

new investment or corporate-restructuring opportunities; and

3. To enhance the student’s capability to analyse and choose funding mixes between debt and equity that

maximize the overall value of the company, and to evaluate the company’s overall performance and

choose the dividend-payout policies that maximize its shareholders’ value.

Learning Outcomes

Code Students completing the module successfully should be able to

A Apply appropriate techniques to assess investment and corporate-restructuring opportunities taking into

consideration the various factors affecting investment and corporate-restructuring decisions of a company.

B Identify funding requirements for existing assets, new investments, or corporate-structuring opportunities

whilst optimising and matching financing mixes that maximise a company’s overall value.

C Critically evaluate the choices of a company whether to continue funding its existing investments or return

cash to its shareholders in the most effective manner so as to maximise their wealth.

Assessment Details

Type Weight Assessment Topic

Individual

Assignment 80%

Analysis of company’s performance and prospect with value-enhancement implications

Critique of company’s performance and prospect with stakeholder-related implications

Group

Assignment 20%

How to create and enhance firm value from alternative processes of investing and raising

funds from diverse providers and returning funds to them amid internal and external

frictions.

Total 100% Please refer to these assignments on Pages 12 and 13 of this Module Handbook.

Methods of Learning and Teaching

A combination of inclusive teaching and active learning methods will be utilised. Essential concepts will be

presented and delivered in a weekly four-hour seminar that includes participatory discussions on current

issues as well as practical activities on case studies.

Syllabus & Teaching Plan

Syllabus

1. Investment Assessment and Decisions

Choosing investment or corporate-restructuring opportunities that deliver expected returns exceeding

minimum rates required by a company’s shareholders, including:

a. Determining how a required rate of return reflects the riskiness of an investment and the mix of

debt and equity being used to fund it

b. Assessing how an expected rate of return reflects the magnitude and timing of an investment’s cash

flow as well as all of its side effects.

c. Applying discounted-cash-flow methods and capital-budgeting techniques to choose among

competing or complementary investment opportunities.

Page 4 of 17

2. Financing Analysis and Decisions

Choosing funding mixes that maximises the company’s value while matching the funding mixes with

its assets’ dynamics, including:

a. Finding the right kind of funding sources for the company and the capital structure to fund its

ongoing operations and existing assets.

b. Analysing and optimising the funding mix between debt and equity that the company finances its

new investment or corporate-restructuring opportunities.

c. Matching changes in the company’s funding mix with those of its assets to maintain value

optimality.

3. Payout Evaluation and Decisions

Choosing dividend-payout policies that optimises investment-financing decisions between cash

distribution and share repurchase, including analyse of a dividend policy to determine the optimal cash

payout to the company’s shareholders, and evaluating and choosing among alternative ways of paying

out cash to the company’s shareholders.

Teaching Plan

Week Study Topic Chapter

Week 8

(Nov 2-6)

Introduction to the Module regarding its objectives, knowledge sources and contents, concept acquisition, skill and talent development, performance assessment, and expected outcomes.

Corporate Finance Decisions based on First Principles in how a firm’s value can be maximized amid different stakeholders’ interests and how such conflicting interests might be reconciled.

Chapters 1 & 2

Week 9

(Nov 9-13)

Capital Budgeting Decisions to drive a firm’s future growth, which require an analysis of relevant cash flows from new investments or corporate-restructuring and the capital-budgeting techniques.

Case Study #1: Capital Budgeting Case Study

Chapters

9 & 10

Week 10

(Nov 16-20)

Cost of Capital Determination to derive a firm’s present value, which requires an assessment of its risk-adjusted opportunity cost of capital (funding costs or hurdle rates) for discounting its cash flows.

Case Study #2: Cost of Capital Case Study

Chapter 7

Week 11

(Nov 23-27)

Capital Structure Decisions to lower a firm’s funding costs, which require a management of its capital structure (debt-equity mixes) through theories and practices on financial-leverage issues.

Case Study #3: Capital Structure Case Study

Chapters 18 & 19

Week 12

(Dec 1-4)

Long-term Financing Decisions to raise a firm’s external funds for its investment opportunities, which require an awareness of funding sources and an assessment of their benefits, costs, and risks.

Case Study #4: Long-term Financing Case Study

Chapters 16 & 20

Week 13

(Dec 7-11)

Dividend Policy Decisions to return a firm’s internal funds to its shareholders and retain its funds for future growth, which require an evaluation of dividend-payout and equity-financing options.

Case Study #5: Dividend Policy Case Study

Chapters 21 & 23

Week 14

(Dec 14-18)

Business Engagement with Guest Speaker: On Corporate Value Management Practices (tentative)

Individual Assignment Submission: Please see its details on Page 12 of this Module Handbook.

Group Assignment Submission: Please see its details on Page 13 of this Module Handbook.

Thu Dec 17

Study Topic Weighting

Capital Budgeting Decisions 20%

Cost of Capital Determination 20%

Capital Structure Decisions 20%

Long-term Financing Decisions 20%

Dividend Policy Decisions 20%

Page 5 of 17

Expected Learning Outcomes

Corporate Finance Decisions

Explain the general objectives of financial management, demonstrate the understanding of First Principles of

Corporate Finance, and describe the financial-strategy process for a business (i.e., investment, financing, payout,

corporate-governance, corporate-restructuring, and balance-sheet management strategies).

Describe the impact of financial markets and other external factors (e.g., government and society) on a business’s

financial strategy (market efficiency and externalities), using examples to illustrate the impacts.

Identify in the business and financial environment factors (i.e., risk exposures) that may affect financing for

investment in a different country (e.g., exchange rates, tax rates, and inflation rates).

Capital Budgeting & Opportunity Cost of Capital

Explain the investment decision-making process and apply various investment-appraisal techniques.

Select and justify appropriate discount (hurdle) rates and cash-flow values for use in selected

investment-appraisal techniques from information supplied, taking account of inflation and tax.

Demonstrate how the interpretation of results from the techniques can be influenced by an assessment of risk.

Recommend and justify a course of actions which is based upon the results of investment appraisal, the

consideration of relevant non-financial factors, and the limitation of the techniques being used.

Corporate Takeovers & Corporate Restructuring

Explain corporate takeovers (e.g., merger, consolidation, tender-offer, asset-purchase, leverage buyout, and

management buyout), the process of pricing an acquisition, and the steps in developing an acquisition strategy.

Explain corporate-restructuring strategies (e.g., stock-split, stock-dividend, divestiture, spin-off, split-off, split-up,

equity-carve-out, and tracking-stock), evaluate their characteristics, and choose from among them.

Capital Structure & Weighted-average Cost of Capital

Assess the suitability of different financing choices for a given business.

Explain, in non-technical terms with appropriate examples, the effect of capital gearing or financial leverage on

investors’ perception of risk and reward.

Compare the financing costs and benefits (including those that are not separately quantifiable) of various courses

of actions using appropriate financing-appraisal techniques.

Calculate the costs of different financing methods and the weighted average cost of capital (WACC).

Long-term Financing & Dividend Policy

Calculate a firm’s future requirements for capital, considering current and planned activities referring to levels of

uncertainty and making reasonable assumptions which are consistent with the situation.

Compare the features of different means of making returns to owners and lenders, explain their effects on the firm

and its stakeholders, and recommend options in a given scenario.

Draft a comprehensive investment-and-financing plan for a given business scenario of a firm and calculate its

fair corporate and equity values using alternative valuation approaches with appropriate sensitivity analyses.

Page 6 of 17

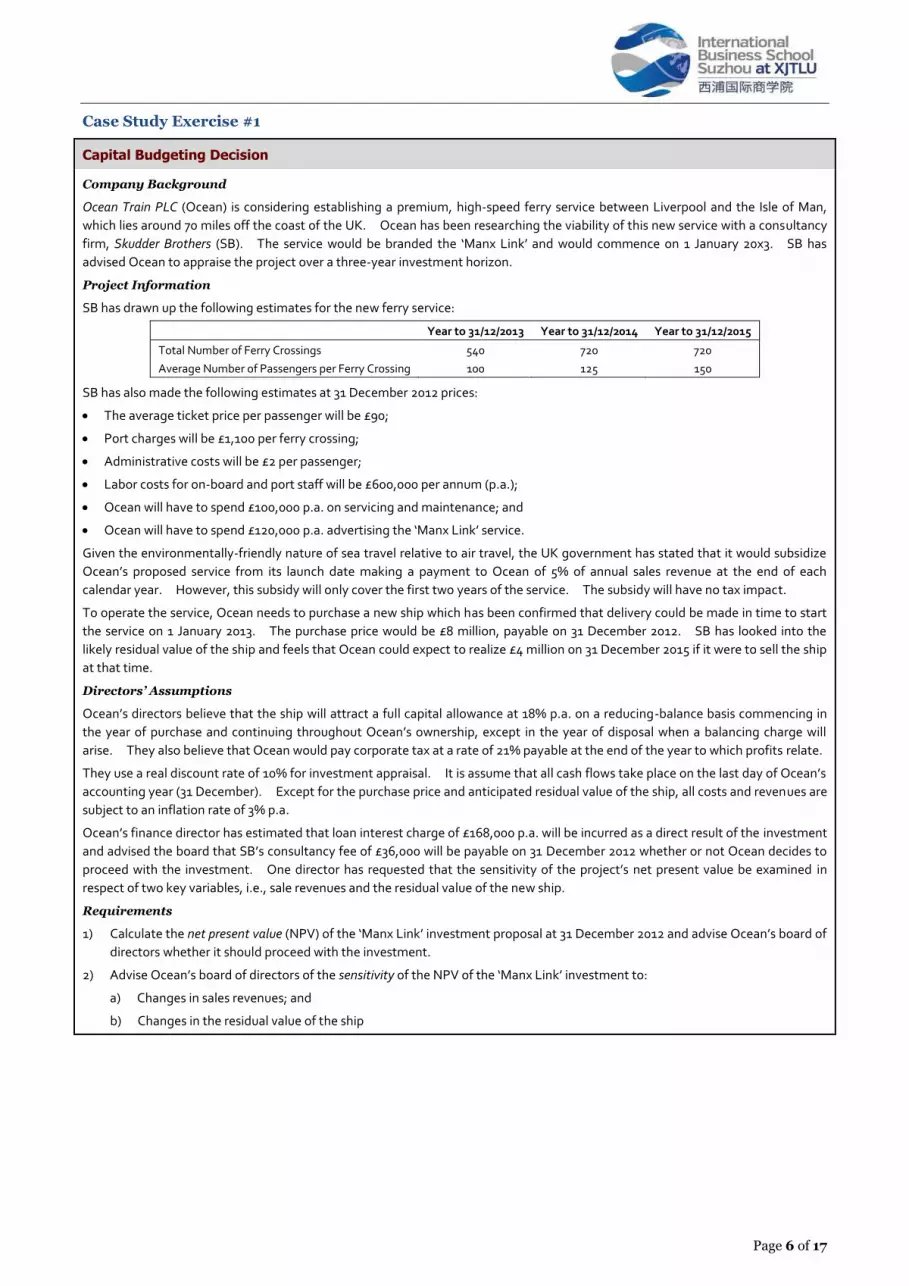

Case Study Exercise #1

Capital Budgeting Decision

Company Background

Ocean Train PLC (Ocean) is considering establishing a premium, high-speed ferry service between Liverpool and the Isle of Man,

which lies around 70 miles off the coast of the UK. Ocean has been researching the viability of this new service with a consultancy

firm, Skudder Brothers (SB). The service would be branded the ‘Manx Link’ and would commence on 1 January 20x3. SB has

advised Ocean to appraise the project over a three-year investment horizon.

Project Information

SB has drawn up the following estimates for the new ferry service:

Year to 31/12/2013 Year to 31/12/2014 Year to 31/12/2015

Total Number of Ferry Crossings 540 720 720

Average Number of Passengers per Ferry Crossing 100 125 150

SB has also made the following estimates at 31 December 2012 prices:

The average ticket price per passenger will be £90;

Port charges will be £1,100 per ferry crossing;

Administrative costs will be £2 per passenger;

Labor costs for on-board and port staff will be £600,000 per annum (p.a.);

Ocean will have to spend £100,000 p.a. on servicing and maintenance; and

Ocean will have to spend £120,000 p.a. advertising the ‘Manx Link’ service.

Given the environmentally-friendly nature of sea travel relative to air travel, the UK government has stated that it would subsidize

Ocean’s proposed service from its launch date making a payment to Ocean of 5% of annual sales revenue at the end of each

calendar year. However, this subsidy will only cover the first two years of the service. The subsidy will have no tax impact.

To operate the service, Ocean needs to purchase a new ship which has been confirmed that delivery could be made in time to start

the service on 1 January 2013. The purchase price would be £8 million, payable on 31 December 2012. SB has looked into the

likely residual value of the ship and feels that Ocean could expect to realize £4 million on 31 December 2015 if it were to sell the ship

at that time.

Directors’ Assumptions

Ocean’s directors believe that the ship will attract a full capital allowance at 18% p.a. on a reducing-balance basis commencing in

the year of purchase and continuing throughout Ocean’s ownership, except in the year of disposal when a balancing charge will

arise. They also believe that Ocean would pay corporate tax at a rate of 21% payable at the end of the year to which profits relate.

They use a real discount rate of 10% for investment appraisal. It is assume that all cash flows take place on the last day of Ocean’s

accounting year (31 December). Except for the purchase price and anticipated residual value of the ship, all costs and revenues are

subject to an inflation rate of 3% p.a.

Ocean’s finance director has estimated that loan interest charge of £168,000 p.a. will be incurred as a direct result of the investment

and advised the board that SB’s consultancy fee of £36,000 will be payable on 31 December 2012 whether or not Ocean decides to

proceed with the investment. One director has requested that the sensitivity of the project’s net present value be examined in

respect of two key variables, i.e., sale revenues and the residual value of the new ship.

Requirements

1) Calculate the net present value (NPV) of the ‘Manx Link’ investment proposal at 31 December 2012 and advise Ocean’s board of

directors whether it should proceed with the investment.

2) Advise Ocean’s board of directors of the sensitivity of the NPV of the ‘Manx Link’ investment to:

a) Changes in sales revenues; and

b) Changes in the residual value of the ship

Page 7 of 17

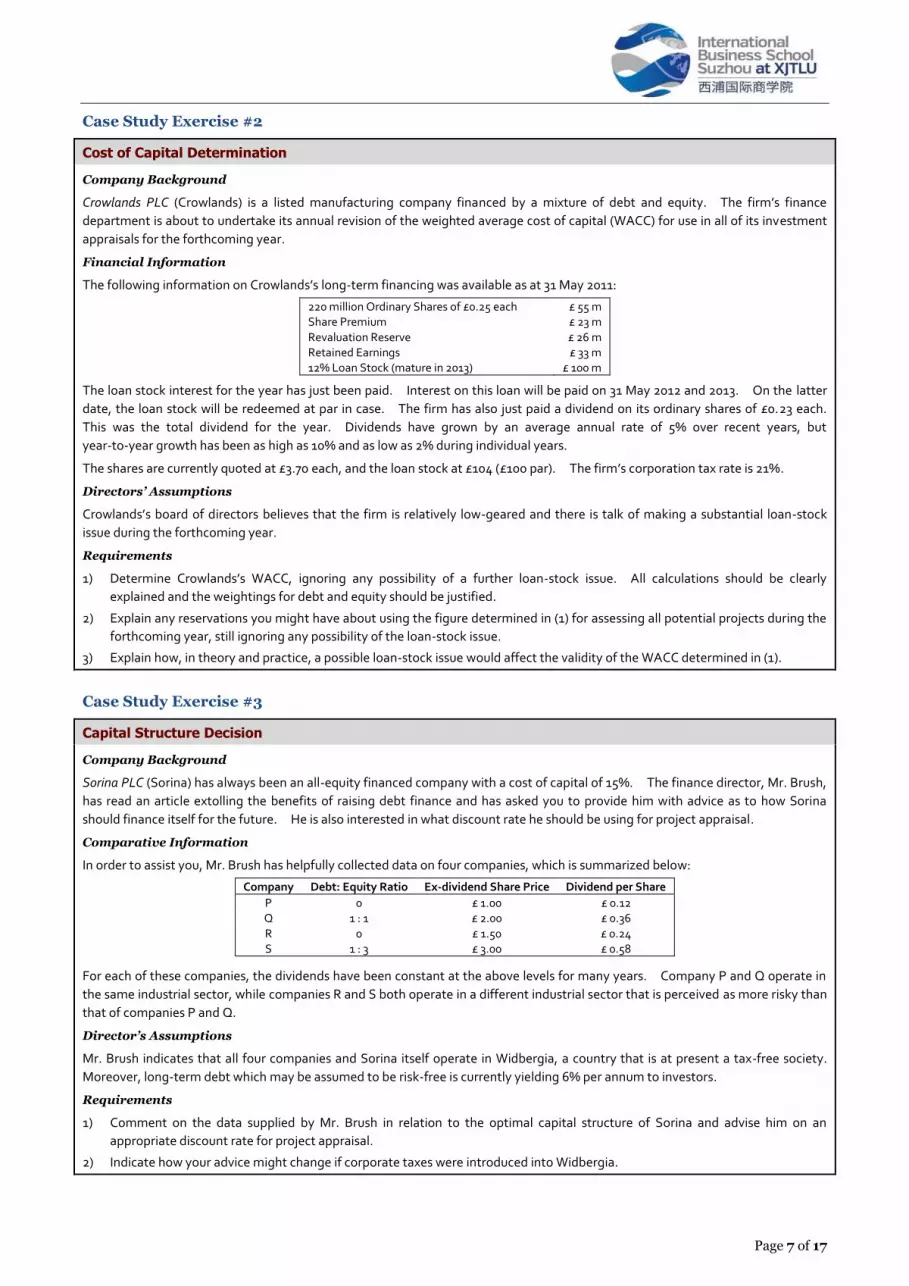

Case Study Exercise #2

Cost of Capital Determination

Company Background

Crowlands PLC (Crowlands) is a listed manufacturing company financed by a mixture of debt and equity. The firm’s finance

department is about to undertake its annual revision of the weighted average cost of capital (WACC) for use in all of its investment

appraisals for the forthcoming year.

Financial Information

The following information on Crowlands’s long-term financing was available as at 31 May 2011:

220 million Ordinary Shares of £0.25 each £ 55 m Share Premium £ 23 m

Revaluation Reserve £ 26 m Retained Earnings £ 33 m 12% Loan Stock (mature in 2013) £ 100 m

The loan stock interest for the year has just been paid. Interest on this loan will be paid on 31 May 2012 and 2013. On the latter

date, the loan stock will be redeemed at par in case. The firm has also just paid a dividend on its ordinary shares of £0.23 each.

This was the total dividend for the year. Dividends have grown by an average annual rate of 5% over recent years, but

year-to-year growth has been as high as 10% and as low as 2% during individual years.

The shares are currently quoted at £3.70 each, and the loan stock at £104 (£100 par). The firm’s corporation tax rate is 21%.

Directors’ Assumptions

Crowlands’s board of directors believes that the firm is relatively low-geared and there is talk of making a substantial loan-stock

issue during the forthcoming year.

Requirements

1) Determine Crowlands’s WACC, ignoring any possibility of a further loan-stock issue. All calculations should be clearly

explained and the weightings for debt and equity should be justified.

2) Explain any reservations you might have about using the figure determined in (1) for assessing all potential projects during the

forthcoming year, still ignoring any possibility of the loan-stock issue.

3) Explain how, in theory and practice, a possible loan-stock issue would affect the validity of the WACC determined in (1).

Case Study Exercise #3

Capital Structure Decision

Company Background

Sorina PLC (Sorina) has always been an all-equity financed company with a cost of capital of 15%. The finance director, Mr. Brush,

has read an article extolling the benefits of raising debt finance and has asked you to provide him with advice as to how Sorina

should finance itself for the future. He is also interested in what discount rate he should be using for project appraisal.

Comparative Information

In order to assist you, Mr. Brush has helpfully collected data on four companies, which is summarized below:

Company Debt: Equity Ratio Ex-dividend Share Price Dividend per Share

P 0 £ 1.00 £ 0.12 Q 1 : 1 £ 2.00 £ 0.36

R 0 £ 1.50 £ 0.24 S 1 : 3 £ 3.00 £ 0.58

For each of these companies, the dividends have been constant at the above levels for many years. Company P and Q operate in

the same industrial sector, while companies R and S both operate in a different industrial sector that is perceived as more risky than

that of companies P and Q.

Director’s Assumptions

Mr. Brush indicates that all four companies and Sorina itself operate in Widbergia, a country that is at present a tax-free society.

Moreover, long-term debt which may be assumed to be risk-free is currently yielding 6% per annum to investors.

Requirements

1) Comment on the data supplied by Mr. Brush in relation to the optimal capital structure of Sorina and advise him on an

appropriate discount rate for project appraisal.

2) Indicate how your advice might change if corporate taxes were introduced into Widbergia.

Page 8 of 17

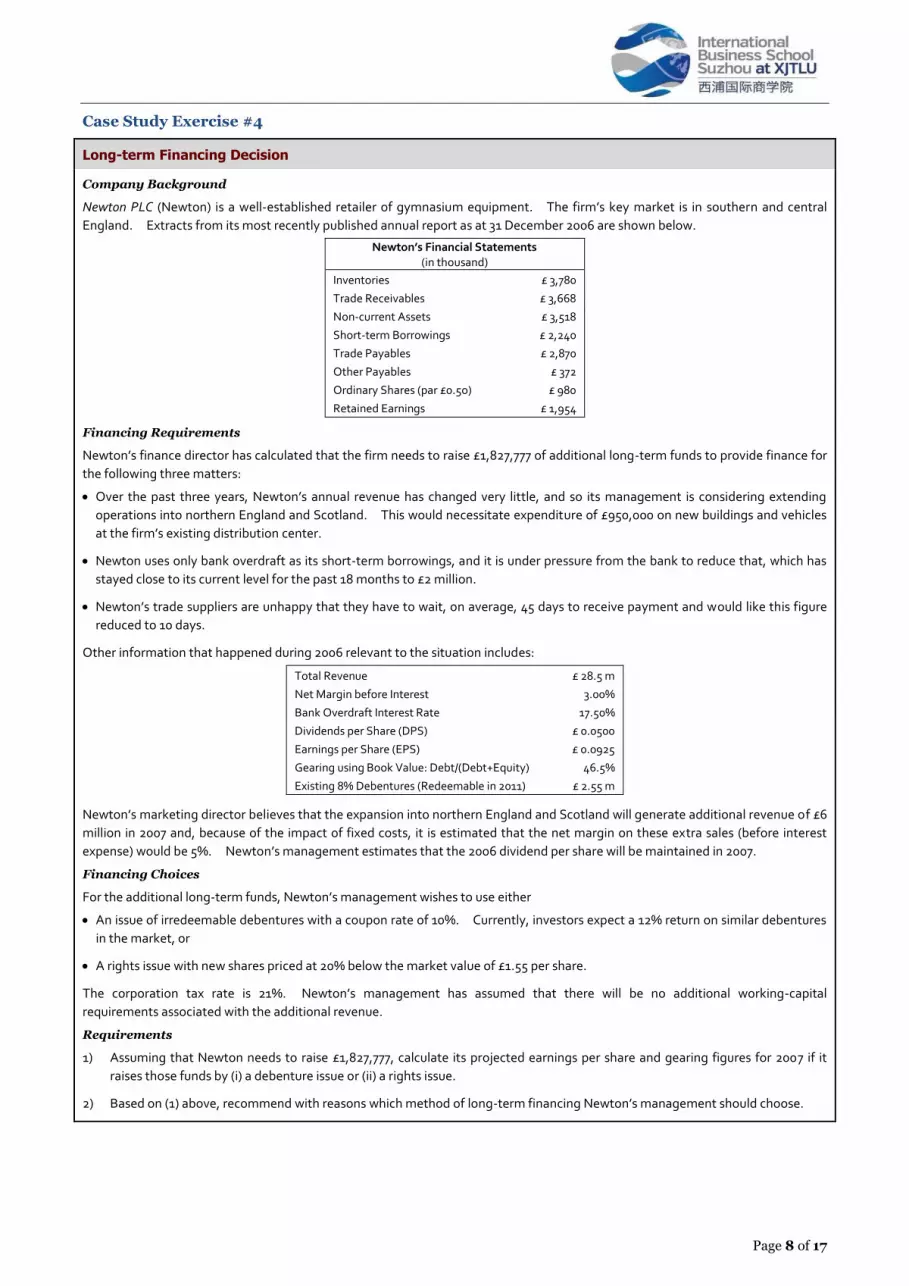

Case Study Exercise #4

Long-term Financing Decision

Company Background

Newton PLC (Newton) is a well-established retailer of gymnasium equipment. The firm’s key market is in southern and central

England. Extracts from its most recently published annual report as at 31 December 2006 are shown below.

Newton’s Financial Statements (in thousand)

Inventories £ 3,780

Trade Receivables £ 3,668

Non-current Assets £ 3,518

Short-term Borrowings £ 2,240

Trade Payables £ 2,870

Other Payables £ 372

Ordinary Shares (par £0.5o) £ 980

Retained Earnings £ 1,954

Financing Requirements

Newton’s finance director has calculated that the firm needs to raise £1,827,777 of additional long-term funds to provide finance for

the following three matters:

Over the past three years, Newton’s annual revenue has changed very little, and so its management is considering extending

operations into northern England and Scotland. This would necessitate expenditure of £950,000 on new buildings and vehicles

at the firm’s existing distribution center.

Newton uses only bank overdraft as its short-term borrowings, and it is under pressure from the bank to reduce that, which has

stayed close to its current level for the past 18 months to £2 million.

Newton’s trade suppliers are unhappy that they have to wait, on average, 45 days to receive payment and would like this figure

reduced to 10 days.

Other information that happened during 2006 relevant to the situation includes:

Total Revenue £ 28.5 m

Net Margin before Interest 3.00%

Bank Overdraft Interest Rate 17.50%

Dividends per Share (DPS) £ 0.0500

Earnings per Share (EPS) £ 0.0925

Gearing using Book Value: Debt/(Debt+Equity) 46.5%

Existing 8% Debentures (Redeemable in 2011) £ 2.55 m

Newton’s marketing director believes that the expansion into northern England and Scotland will generate additional revenue of £6

million in 2007 and, because of the impact of fixed costs, it is estimated that the net margin on these extra sales (before interest

expense) would be 5%. Newton’s management estimates that the 2006 dividend per share will be maintained in 2007.

Financing Choices

For the additional long-term funds, Newton’s management wishes to use either

An issue of irredeemable debentures with a coupon rate of 10%. Currently, investors expect a 12% return on similar debentures

in the market, or

A rights issue with new shares priced at 20% below the market value of £1.55 per share.

The corporation tax rate is 21%. Newton’s management has assumed that there will be no additional working-capital

requirements associated with the additional revenue.

Requirements

1) Assuming that Newton needs to raise £1,827,777, calculate its projected earnings per share and gearing figures for 2007 if it

raises those funds by (i) a debenture issue or (ii) a rights issue.

2) Based on (1) above, recommend with reasons which method of long-term financing Newton’s management should choose.

Page 9 of 17

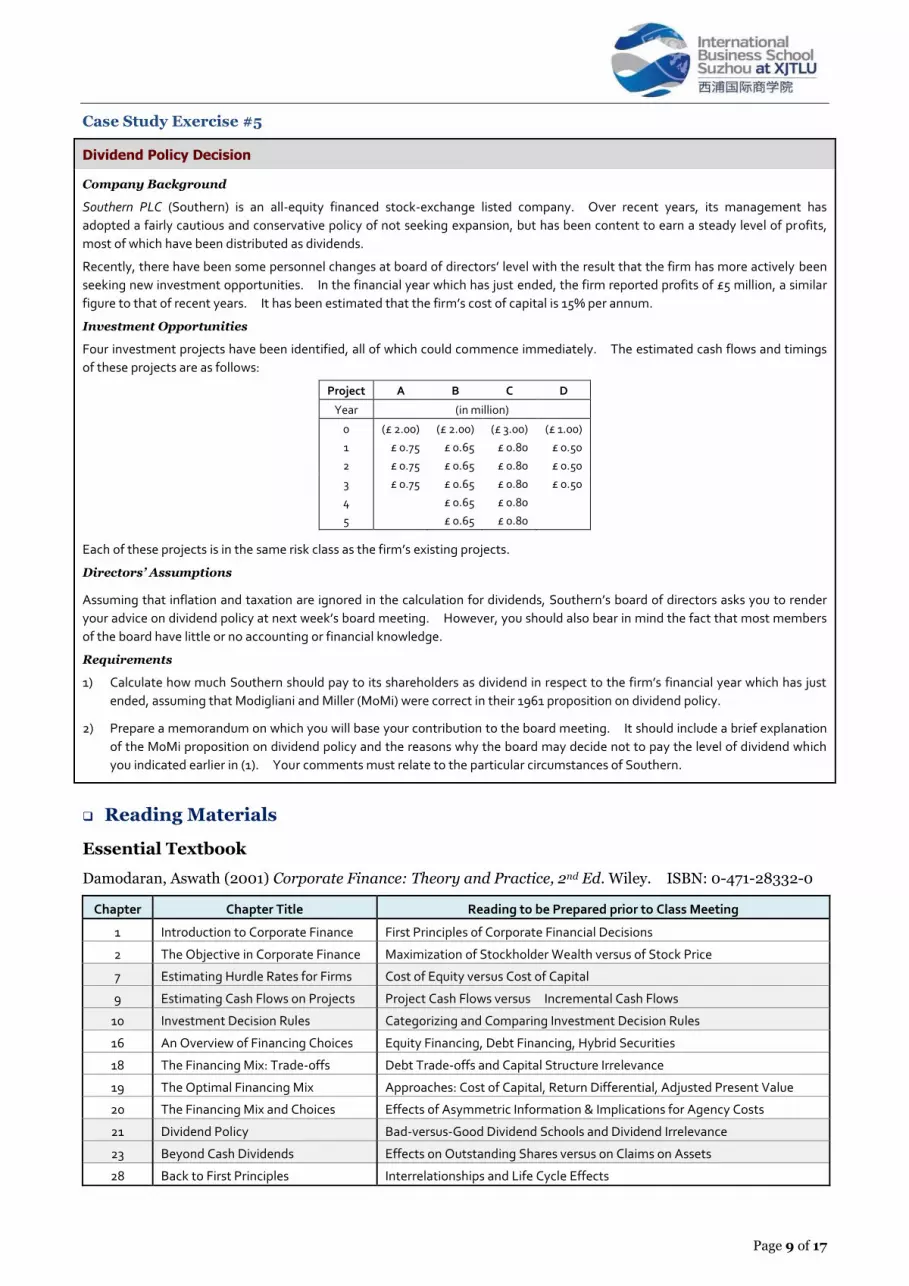

Case Study Exercise #5

Dividend Policy Decision

Company Background

Southern PLC (Southern) is an all-equity financed stock-exchange listed company. Over recent years, its management has

adopted a fairly cautious and conservative policy of not seeking expansion, but has been content to earn a steady level of profits,

most of which have been distributed as dividends.

Recently, there have been some personnel changes at board of directors’ level with the result that the firm has more actively been

seeking new investment opportunities. In the financial year which has just ended, the firm reported profits of £5 million, a similar

figure to that of recent years. It has been estimated that the firm’s cost of capital is 15% per annum.

Investment Opportunities

Four investment projects have been identified, all of which could commence immediately. The estimated cash flows and timings

of these projects are as follows:

Project A B C D

Year (in million)

0 (£ 2.00) (£ 2.00) (£ 3.00) (£ 1.00)

1 £ 0.75 £ 0.65 £ 0.80 £ 0.50

2 £ 0.75 £ 0.65 £ 0.80 £ 0.50

3 £ 0.75 £ 0.65 £ 0.80 £ 0.50

4 £ 0.65 £ 0.80

5 £ 0.65 £ 0.80

Each of these projects is in the same risk class as the firm’s existing projects.

Directors’ Assumptions

Assuming that inflation and taxation are ignored in the calculation for dividends, Southern’s board of directors asks you to render

your advice on dividend policy at next week’s board meeting. However, you should also bear in mind the fact that most members

of the board have little or no accounting or financial knowledge.

Requirements

1) Calculate how much Southern should pay to its shareholders as dividend in respect to the firm’s financial year which has just

ended, assuming that Modigliani and Miller (MoMi) were correct in their 1961 proposition on dividend policy.

2) Prepare a memorandum on which you will base your contribution to the board meeting. It should include a brief explanation

of the MoMi proposition on dividend policy and the reasons why the board may decide not to pay the level of dividend which

you indicated earlier in (1). Your comments must relate to the particular circumstances of Southern.

Reading Materials

Essential Textbook

Damodaran, Aswath (2001) Corporate Finance: Theory and Practice, 2nd Ed. Wiley. ISBN: 0-471-28332-0

Chapter Chapter Title Reading to be Prepared prior to Class Meeting

1 Introduction to Corporate Finance First Principles of Corporate Financial Decisions

2 The Objective in Corporate Finance Maximization of Stockholder Wealth versus of Stock Price

7 Estimating Hurdle Rates for Firms Cost of Equity versus Cost of Capital

9 Estimating Cash Flows on Projects Project Cash Flows versus Incremental Cash Flows

10 Investment Decision Rules Categorizing and Comparing Investment Decision Rules

16 An Overview of Financing Choices Equity Financing, Debt Financing, Hybrid Securities

18 The Financing Mix: Trade-offs Debt Trade-offs and Capital Structure Irrelevance

19 The Optimal Financing Mix Approaches: Cost of Capital, Return Differential, Adjusted Present Value

20 The Financing Mix and Choices Effects of Asymmetric Information & Implications for Agency Costs

21 Dividend Policy Bad-versus-Good Dividend Schools and Dividend Irrelevance

23 Beyond Cash Dividends Effects on Outstanding Shares versus on Claims on Assets

28 Back to First Principles Interrelationships and Life Cycle Effects

Page 10 of 17

Recommended Readings

Damodaran, Aswath (1996). Investment Valuation: Tools and Techniques for Determining the Value of

Any Asset, University Edition. John Wiley & Sons. ISBN: 0-471-13393-0

Ross, Stephen A., Westerfield, Randolph W., and Jaffe, Jeffrey (2010). Corporate Finance, International

Edition. McGraw-Hill Irwin. ISBN: 0-077-33762-x

Brealey, Richard A., Myers, Stewart C., and Allen, Franklin (2011). Principles of Corporate Finance,

Global Edition. McGraw-Hill Irwin. ISBN: 0-073-53073-5

Clayman, Michelle R., Fridson, Martin S., and Troughton, George H. (2012). Corporate Finance: A

Practical Approach, 2nd Edition. The CFA Institute. ISBN: 978-1-11810-537-5

Clayman, Michelle R., Fridson, Martin S., and Troughton, George H. (2012). Corporate Finance

Workbook: A Practical Approach, 2nd Edition. The CFA Institute. ISBN: 978-1-11811-197-4

Institute of Charted Accountants of England and Wales (ICAEW) (2014). ACA Professional Level –

Financial Management: Study Manual. ICAEW. ISBN: 978-0-85760-808-6

Institute of Charted Accountants of England and Wales (ICAEW) (2014). ACA Professional Level –

Financial Management: Revision Question Bank. ICAEW. ISBN: 978-0-85760-803-1

SECTION C: FURTHER INFORMATION

Student Feedback

The University requires student feedback to be obtained and evaluated by Departments for each module

in every session. It is University policy that the preferred way of achieving this is by means of an Online

Module Evaluation Questionnaire Survey. Students will be invited to complete the questionnaire survey

for this module at the end of the semester.

Plagiarism, Cheating, and Fabrication of Data.

Offences of this type can result in attendance at a University-level committee and penalties being

imposed. You need to be familiar with the rules. Please see the “Policy for Dealing with Plagiarism,

Collusion and Data Fabrication” document available on e-Bridge in the Student Academic Services

section under the heading ‘Policies and Regulations’.

Rules of submission for assessed coursework

The School has detailed rules and procedures governing the submission of assessed coursework. You

need to be familiar with them. Details can be found in the “Code of Practice for Assessment” document

available on e-Bridge in the Student Academic Services section under the heading ‘Policies and

Regulations’.

Late Submission of Assessed Coursework

The University attaches penalties to the late submission of assessed coursework. You need to be

familiar with the University’s rules. Details can be found in the “Code of Practice for Assessment”

document available on e-Bridge in the Student Academic Services section under the heading ‘Policies

and Regulations’.

Page 11 of 17

Mitigating Circumstances

The University is able to take into account mitigating circumstances such as illness or personal

circumstances which may have adversely affected student performance on a module. It is the student’s

responsibility to keep their Academic Adviser, Programme Director or Head of Department informed of

illness and other factors affecting their progress during the year and especially during the examination

period. Students who believe that their performance on a examination or assessed coursework may have

been impaired by illness, or other exceptional circumstances should follow the procedures set out in the

Mitigating Circumstances Policy, which can be found on e-Bridge in the Student Academic Services

section under the heading ‘Policies and Regulations’.

Interactive Communication Environment (ICE)

Copies of lecture notes and other materials are available electronically through ICE, the University’s

virtual learning environment.

Page 12 of 17

ACF439 Corporate Finance

Semester 1 of 2015-16

Individual Assignment (80% of Grade)

An Analysis of company’s performance and prospect with value-creation/enhancement implications A Critique of company’s performance and prospect with stakeholder-related conflict implications

Introduction

This module deals principally with a corporate financial decision-making process of a firm that involves investing,

fundraising, dividend-paying, agency-governing, and strategic-resource management activities amid various challenges

and opportunities. The learning-outcome objective of this Individual Assignment is to develop or enhance each

student’s proven capabilities to 1) practically undertake quantitative analysis and 2) critically provide qualitative

synthesis on a given firm based on its case-study information.

Instructions

Each student shall receive the same set of questions from the lecturer on Friday December 11, 2015 for her/him to

perform this Individual Assignment uncontrolled yet unassisted within five days (see details below). The following

components are expected to be included in the report:

1. Detailed Calculations Workout: As there will be several numerical derivation works involved in a company’s

value analysis, you should be prepared to present your detailed calculations that lead to either the interim or the

final results required by the questions.

2. Financial Statement Analysis: At least three standard pro forma financial-statement reports are to be

constructed from the given input variable and presented using a spreadsheet model (based on or extended from the

case studies discussed and practiced in class), namely the income statement, the balance sheet, and the cash flow

statement, over a certain expected duration. You are required to prepare a complete calculation procedure and

provide its resultant outcomes.

3. Discounted Cash Flow Analysis: Since one of the alternative valuation methods is the discounted cash flow

(DCF), you are required to identify an appropriate type of cash flow and its corresponding discount rate, plus any

other relevant side-effect adjustment, at this stage of analysis after which you shall derive a net present value.

4. Alternative Valuation Methods Assessment: Based on different approaches, you are required to provide a

detailed assessment for each valuation method by weighing its advantages against its disadvantages in order to

allow you to provide a decision-maker your objective recommendations about firm valuation.

5. Value Creation Strategies Criticism: There are many sets of value creation or enhancement strategies from

which a firm can draw to fit its specific circumstances. You are required to provide your own critical and/or

creative comments categorically regarding such strategies that are deemed appropriate for the given firm.

6. Corporate Governance Issues Criticism: There are several groups of stakeholders with different interests and

opinions on a firm’s value-creating or enhancing activities. You are required to provide your own critical and/or

creative comments regarding ways to address those conflict-of-interest issues via effective corporate-governance

system without undermining firm value.

7. Professional Report Preparation: Write your report by addressing all the questions’ requirements. Ensure

that you do not plagiarize from somebody else’s works or sources as plagiarism is considered a serious academic

offense. Also inspect and clear your report through Turn-it-in plagiarism detection software before you submit it.

8. There is neither minimum nor maximum limit imposed on page number of your report that uses a 12-point Times

New Roman font and a 1.5 line spacing, excluding tables, charts, appendices, citations, or references.

Duration

Each student is allowed to perform on this Individual Assignment within a window of five (5) days from December 12

through 16, 2015 after the question set has been provided by the lecturer.

Submission

The deadline for submitting your Individual Assignment report is Thursday December 17, 2015. Please use the

Submission Cover Sheet provided on ICE.

Page 13 of 17

ACF439 Corporate Finance

Semester 1 of 2015-16

Group Assignment (20% of Grade)

How to create and enhance firm value from alternative processes of investing and raising funds

from diverse providers and returning funds to them amid internal and external frictions

Introduction

The learning-outcome goal of this Group Assignment, complementary with that of the Individual Assignment, is to allow

a team of three (3) students to collaborate in exploring alternative ideas to create maximum firm value from the

perspectives of different stakeholders, both internal and external, who are able to contribute or influence the firm’s

corporate financial decisions. The team is encouraged to utilize actual internal (accounting) and external (market)

information from an existing company of its own choice along with necessary hypothetical data and assumptions.

Instructions

Based on the four guides outlined in the Appendix to this Module Handbook, additional library-research, and

Internet-survey works from an online database, you are required to perform the following group-learning tasks:

1. Industry-level Analysis: Choose one industry in which your team is MOST interested and look closely at its

average financial performance and value indicators relative to its own historical track record (time series) and across

other similar industries (cross section), e.g., air transport versus train and marine, renewable energy versus

traditional ones, e-commerce versus wholesale and retail, digital banking versus conventional ones, etc.

2. Firm-level Analysis: Select one company within the industry your team just chose and scrutinize its average

financial performance and all related value indicators relative to its own historical track record (growth rate) and its

peers within the same industry (competitiveness).

3. Value Sources Analysis: Identify and describe that company’s value sources from its operating, investing,

financing, governing, and strategic activities in terms of their current strengths and weaknesses as well as their

future opportunities and challenges. Your team can combine a set of quantitative analyses of the firm’s financial

information with another set of qualitative assessments of the firm’s value implications.

4. Value Drivers & Enhancers: Choose one set of the company’s value drivers and enhancers that your team

believes is the most compelling, distinctive, and sustainable on which to expand your alternative ideas of firm-value

creation. Your team can approach the analysis of your chosen set of value drivers and enhancers from various

stakeholders’ perspectives to see how any friction to value creation can be effectively minimized.

5. Value-creating Implications: Critically synthesize your stepwise recommendations on how the company should

pursue and proceed in order to achieve its targeted or desired value-creating outcomes. Your team can reconcile

diverging ideas from different stakeholders’ perspectives in order to come up with a unified approach to firm-value

creation specifically applicable to your chosen company.

6. Professional Report Preparation: Write your group report outlining, detailing, analyzing, criticizing, and

synthesizing the above items in their sequential order. Please ascertain that your team does not plagiarize from

somebody else’s works or sources as plagiarism is considered a serious academic offense. Please make sure you

inspect and clear your report through Turn-it-in plagiarism detection software before you submit it. Your report

will be evaluated based on the following assessment criteria:

(a) Demonstration of learned theories and relevant concepts (35%)

(b) Completeness of explanations, examples, and citations (30%)

(c) Accuracy of definitions, arguments, and calculations (35%)

7. There is no minimum number of pages in your report, but its upper limit is NOT to exceed 20 pages using a 12-point

Times New Roman font and a 1.5 line spacing, excluding tables, charts, appendices, citations, or references.

Duration

Each team is allowed to perform on this Group Assignment uncontrolled yet unassisted between Week 1 (starting on

September 7, 2015) and Week 14 (ending on December 11, 2015) of the semester.

Submission

The deadline for submitting your Group Assignment report is Thursday December 17, 2015. Please use the

Submission Cover Sheet provided on ICE.

Page 14 of 17

‒ Appendix ‒

A Guide to Capital Budgeting Decisions & Cost of Capital Determination

Project Cash Flows, Hurdle Rates, Investment Decision Rules Analysis

Objectives:

1) To estimate earnings and cash flows on a typical project for a firm.

2) To develop a risk profile for a project and estimate its appropriate hurdle rate.

3) To decide which decision rule the firm should be using in investment analysis.

Key Questions:

1) Does the firm have a typical investment? If so, can the firm estimate the earnings and cash flow on that investment?

2) What are the different businesses that the firm is involved in? What are the differences in their risk exposures?

3) What are the cost of equity and cost of capital for each of the businesses that the firm is involved in?

4) What investment decision rule does the firm use in analyzing its projects?

5) What investment decision rule should the firm use to analyze investments?

Analytical Framework:

1) Typical Investments

- Does the firm take a few or several investment each year?

- Do those investments have much in common? If so, what is their commonality? If not, how are they different?

2) Earnings and Cash Flows

- What is the typical life of an investment made by the firm?

- What is the pattern of earnings and of cash flows on such an investment?

- Based on the firm’s aggregate numbers, can its earnings and cash flows be estimated on a hypothetical investment?

3) Business Division Risk Analysis

- Estimate a bottom-up unlevered beta for each business division or project in the firm.

- If historical accounting earnings by business division are available, estimate its accounting beta as a check.

- Examine the reasons for the differences in betas across business divisions by looking at differences in their business

risk and operating leverage.

4) Estimating Business Division’s Cost of Equity

- If business divisions do not carry their own debt, use the debt/equity ratio for the firm to estimate bottom-up levered

betas by division. Use the bottom-up levered beta to estimate divisional cost of equity.

- If business divisions do carry their own debt or debt can be assigned to them on a reasonable basis, use division-specific

debt/equity ratios and bottom-up levered betas to estimate divisional costs of equity.

5) Estimating Business Division’s Cost of Capital

- If business divisions do not carry their own debt, use the firm’s debt/capital ratio and the firm’s cost of debt to estimate

divisional cost of capital.

- If business divisions do carry their own debt or debt can be assigned to them on a reasonable basis, use division-specific

debt/capital ratios and costs of debt to estimate divisional costs of capital.

6) Investment Decision Rules Used

- What investment decision rule does the firm use to decide on investments?

- If the firm has a stated objective, is the investment decision rule consistent with that objective?

7) Correct Investment Decision Rule

- Are the earnings and cash flows on the firm’s investments likely to be very different? Are there significant non-cash

charges and working-capital needs?

- Does the firm face any capital-rationing constraints?

Information Sources:

1) Firms describe their investments in their annual reports, though not in significant detail. The statement of cash flows will

provide some breakdown, as will the footnotes to the financial statements.

2) To estimate costs of capital for each of the firm’s different businesses, begin by identifying the businesses in its

comprehensive annual report. Then, find comparable firms in each of those businesses and estimate the average beta and

debt/equity ratio for those firms. Use the unlevered beta for each business to estimate a levered beta and cost of equity.

Use the same debt ratio and the cost of debt for the firm to estimate a cost of capital for the business division.

3) Firms sometimes specify their objectives (e.g., double revenues within x years, increase return on equity by x%, etc.) in their

annual reports. They almost never specify investment decision rules, though managers may sometimes mention them in

the context of explaining why they made a specific investment.

Page 15 of 17

A Guide to Capital Structure Decisions

Capital Structure Choices & Optimal Financing Mix Analysis

Objectives:

1) To analyze the tradeoff between debt and equity for a firm and to examine whether it favors the use of debt.

2) To estimate the optimal mix of debt and equity for a firm and to evaluate the effect on firm value of moving to that mix.

Key Questions:

1) How large, in qualitative or quantitative terms, are the advantages and disadvantages to the firm from using debt?

2) From the qualitative tradeoff, does the firm seem to have too much or too little debt?

3) Based on the cost-of-capital approach, what is the optimal debt ratio for the firm?

4) Bringing reasonable constraints into the decision process, what would be the recommended debt ratio for the firm?

5) Quantitatively, does the firm have too much or too little debt relative to (a) its industry and (b) the market?

Analytical Framework:

1) Benefit of Debt

- What marginal tax rate does the firm face, and how does this rate measure up to the marginal tax rates of other firms?

- Does the firm have other tax deductions (e.g., depreciation) that reduce the tax liability?

- Does the firm have high free cash flows (e.g., EBITDA/firm value)? Has it taken good investment projects?

- How responsive are managers to stockholders?

- Would there be any advantage to the use of debt by the firm as a way of keeping managers in line, or do other cheaper

mechanisms exist?

2) Cost of Debt

- How high are the current cash flows of the firm to service its debt, and how stable are those cash flows?

- How easy is it for bondholders to observe what stockholders are doing? Are the assets tangible or intangible? If they

are intangible, what are the costs of monitoring stockholders or bond covenants?

- How well can the firm forecast its future investment opportunities and needs? How much does it value flexibility?

3) Cost of Capital

- What is the current cost of capital for the firm?

- What happens to the cost of capital when the debt ratio is changed?

- At what debt ratio is the cost of capital minimized and firm value maximized? If they are different, explain why.

- What will happen to the firm value if the firm moves to its optimal debt ratio?

- What will happen to the stock price if the firm moves to its optimal debt ratio and if stockholders are rational?

4) Building Constraints into the Process

- What rating does the firm have at the optimal debt ratio? If a rating constraint were imposed, what would it be?

- What is the optimal debt ratio with the rating constraint?

- How volatile is the firm’s operating income? What is the “normalized” operating income of the firm? What is the

optimal debt ratio of the firm at that level of normalized operating income?

5) Relative Analysis

- Does it have too much or too little debt relative to the industry in which the firm operates?

- Does it have too much or too little debt relative to the rest of the firms in the market?

6) Financial Market Concerns

- How many analysts follow the firm?

- How much trading volume is there on the firm’s stock?

7) Societal Constraints

- What does the firm say about its social responsibilities?

- Does the firm have a good or bad reputation as a corporate citizen? If so, how has it earned that reputation?

- If the firm has been a recent target of social criticism, how has it responded?

Information Sources:

1) To find out what types of securities and financing the firm has outstanding, check the footnote in the comprehensive annual

report of a company’s financial performance filed with the Securities and Exchange Commission (SEC), known in the US as

the 10-K report. To get the other inputs needed for the analysis, check the historical financials on the firm.

2) To get the input needed to estimate the optimal capital structure, examine the 10-K report or the annual report. The

ratings and interest coverage ratios can be obtained from the rating agencies such as S&P and Moody’s and default spreads

can be estimated by finding traded bonds in each rating class. Value Line also provides information on other firms in the

industry individually in its database.

Page 16 of 17

A Guide to Long-term Financing Decisions

Long-term Financing Choices & Financial Transitions Analysis

Objectives:

1) To examine a firm’s current financing choices and to categorize them into long-term debt and equity.

2) To analyze the firm’s place in the growth cycle and any financial transitions that it has or will be making soon.

Key Questions:

1) Where and how does the firm get its current financing?

2) Would these financing choices be classified as debt, equity, or hybrid securities?

3) Where in the growth cycle is the firm? What types of financing would it expect to use?

4) If it is using a different kind of financing than would be expected, what might be some of the reasons for the deviation?

5) What financial transitions has the firm already made, and what are the transitions it would make in the future?

Analytical Framework:

1) Assessing Current Financing

- How does the firm raise equity? If it is a publicly traded firm, it can raise equity from common stock and warrants or

options. If it is a private firm, the equity can come from personal savings and venture capital.

- How, if at all, does the firm borrow money? If it is a public firm, it can raise debt from bank loans or corporate bonds.

- Does the firm use hybrid securities to raising fund, which combine some of the features of deb and some of equity?

Examples include preferred stock, convertible bonds, and bonds with warrants attached to them.

2) Detailed Description of Current Financing

- If the firm raises equity from warrants or convertibles, what are the characteristics of the options (e.g., exercise price,

maturity, etc.)?

- If the firm has borrowed money, what are the characteristics of the debt (e.g., maturity, coupon or stated interest rate,

call features, fixed or floating rate, secured or unsecured, and currency)?

- If the firm has hybrid securities, what are their special or unique features?

3) Breakdown into Debt and Equity

- If the firm has financing with debt and equity components (e.g., convertible bonds), how much of the value can be

attributed to debt and how much to equity?

- Given the coupon rate and maturity of the non-traded debt, what is the current estimated market value of that debt?

- What is the market value of equity that the firm has outstanding?

4) Stage in the Growth Cycle

- How fast are the firm’s revenues growing? How fast are earnings growing?

- How much is the firm reinvesting in new investments?

- How much do the firm’s existing investments generate in cash flows?

- Given this information, at what stage in the life cycle would the firm be placed?

5) Predicted versus Actual Financing

- Given where the firm is in the life cycle, what types of financing would it expect to use?

- What is the financing that the firm is currently using?

- If the actual financing is different from the expected financing, what might be some of the reasons?

6) Financial Transitions

- If the firm recently had an initial public offering (IPOs), what were the details of the offering, i.e., who was the

investment banker, what was the offering price, what happened to the stock price after the offering?

- If the firm recently had a seasoned equity offering, what were the terms of the offering?

- If the firm recently had a seasoned bond offering, what were the terms of the offering?

Information Sources:

1) Almost all the information about current financing choices can be extracted from the financial statements. The balance

sheet should provide a summary of the book values of the various financing choices made by the firm, though hybrids are

usually categorized into debt (if they are debt hybrids) and equity (if they are equity hybrids). The description of warrants

outstanding as well as the details of the borrowing that the firm has should be available in the footnotes to the balance

sheets. In particular, the maturity dates for different components of borrowing, the coupon rates, and information on any

other special features should be available in the footnotes.

2) The information on a firm’s current revenue and earnings growth can be obtained from the financial statements. The

information on recent security offerings (equity as well as debt) can be obtained from the filings made by the firm with the

SEC. Firms that are planning to make IPOs or have just made public offering have to file registration statements with the

SEC. There are a number of services that track forthcoming IPOs as well as seasoned offerings.

Page 17 of 17

A Guide to Dividend Policy Decisions

Dividend Policy Trade-off & Dividends Analysis

Objectives:

1) To examine how much cash a firm has returned to its stockholders and in what forms (dividends or stock buybacks), and to

evaluate whether the tradeoff favors returning more or less.

2) To determine whether the firm should change its dividend policy based upon an analysis of its investment opportunities and

comparable firms.

Key Questions:

1) How has the firm returned cash to its owners? Has it paid dividends, bought back stock, or spun off assets?

2) How would the firm be recommended to return cash to stockholders (assuming that it has excess cash) given its

characteristics today?

3) How much could the firm have returned to its stockholders over the last few years? How much did it actually return?

4) Would the firm be pushed to change its dividend policy (i.e., return more or less cash to its stockholders) given its current

cash balance?

5) How does the firm’s dividend policy compare to those of its peer group and to the rest of the market?

Analytical Framework:

1) Historical Dividend Policy

- How much has the firm paid as cash dividends each year over the last few years?

- How much stock has the firm bought back each year over the last few years?

- Cumulatively, how much cash has been returned to stockholders each year for the last few years?

2) Firm Characteristics

- How easily can the firm convey information to financial markets, i.e., how necessary is it for the firm to use dividend

policy as signal?

- Who are the marginal stockholders in the firm? Do they like dividends, or would they prefer stock buybacks?

- How well can the firm forecast its future financing needs? How valuable is preserving flexibility to this firm?

- Are there bond covenants that restrict the firm’s dividend policy?

- How does the firm’s dividend policy compare to that of other firms in the same industry?

3) Affordable Dividends

- What were the free cash flows to equity that the firm had over the last few years?

- What is the current cash balance for the firm?

4) Management Trust

- How well have the managers of the firm picked investments, historically?

- Is there any reason to believe that future investments of the firm will be different from the historical record?

5) Changing Dividend Policy

- Given the relationship between dividends and free cash flows to equity, and the trust the stockholders have in the

management of the firm, should the firm change its dividend policy?

6) Comparing to Industry and Market

- Relative to the industry in which it operates, does the firm pay too much or too little in dividends? (Do regression, if

necessary)

- Relative to the rest of the firms in the market, does the firm pay too much or too little in dividends? (Use the market

regression, if necessary)

Information Sources:

1) Information about dividends paid and stock bought back over time can be obtained from the financial statements of the

firm. (The statement of changes in cash flows is usually the best source of both.) To find typical dividend payout ratios

and yields for the industrial sector in which the firm operates, examine the data set on industry average on the textbook

author’s web site at http://www.stern.nyu.edu/~adamodar/cfin2E/project/data.htm.

2) Information needed to estimate free cash flows to equity and returns on equity can be found from the past

financial-statement analysis, e.g., an equity beta and a debt ratio. Data on stock returns and the returns on a market index

over the period of dividend analysis are also required.