acca applied skills study text - kaplan publishing

TRANSCRIPT

ACCA

Applied Skills

Financial Reporting (FR)

Study Text

P.2 KAPLAN PUBLISHING

British Library Cataloguing-in-Publication Data A catalogue record for this book is available from the British Library.

Published by: Kaplan Publishing UK Unit 2 The Business Centre Molly Millar’s Lane Wokingham Berkshire RG41 2QZ

ISBN: 978-1-78740-392-5

© Kaplan Financial Limited, 2019

The text in this material and any others made available by any Kaplan Group company does not amount to advice on a particular matter and should not be taken as such. No reliance should be placed on the content as the basis for any investment or other decision or in connection with any advice given to third parties. Please consult your appropriate professional adviser as necessary. Kaplan Publishing Limited, all other Kaplan group companies, the International Accounting Standards Board, and the IFRS Foundation expressly disclaim all liability to any person in respect of any losses or other claims, whether direct, indirect, incidental, consequential or otherwise arising in relation to the use of such materials.

Printed and bound in Great Britain.

Acknowledgements

These materials are reviewed by the ACCA examining team. The objective of the review is to ensure that the material properly covers the syllabus and study guide outcomes, used by the examining team in setting the exams, in the appropriate breadth and depth. The review does not ensure that every eventuality, combination or application of examinable topics is addressed by the ACCA Approved Content. Nor does the review comprise a detailed technical check of the content as the Approved Content Provider has its own quality assurance processes in place in this respect.

This Product includes proprietary content of the International Accounting Standards Board which is overseen by the IFRS Foundation, and is used with the express permission of the IFRS Foundation under licence. All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without prior written permission of Kaplan Publishing and the IFRS Foundation.

The IFRS Foundation logo, the IASB logo, the IFRS for SMEs logo, the “Hexagon Device”, “IFRS Foundation”, “eIFRS”, “IAS”, “IASB”, “IFRS for SMEs”, “IFRS”, “IASs”, “IFRSs”, “International Accounting Standards” and “International Financial Reporting Standards”, “IFRIC” and “IFRS Taxonomy” are Trade Marks of the IFRS Foundation.

Trade Marks

The IFRS Foundation logo, the IASB logo, the IFRS for SMEs logo, the “Hexagon Device”, “IFRS Foundation”, “eIFRS”, “IAS”, “IASB”, “IFRS for SMEs”, “NIIF” IASs” “IFRS”, “IFRSs”, “International Accounting Standards”, “International Financial Reporting Standards”, “IFRIC”, “SIC” and “IFRS Taxonomy”.

Further details of the Trade Marks including details of countries where the Trade Marks are registered or applied for are available from the Foundation on request.

This product contains material that is ©Financial Reporting Council Ltd (FRC). Adapted and reproduced with the kind permission of the Financial Reporting Council. All rights reserved. For further information, please visit www.frc.org.uk or call +44 (0)20 7492 2300.

KAPLAN PUBLISHING P.3

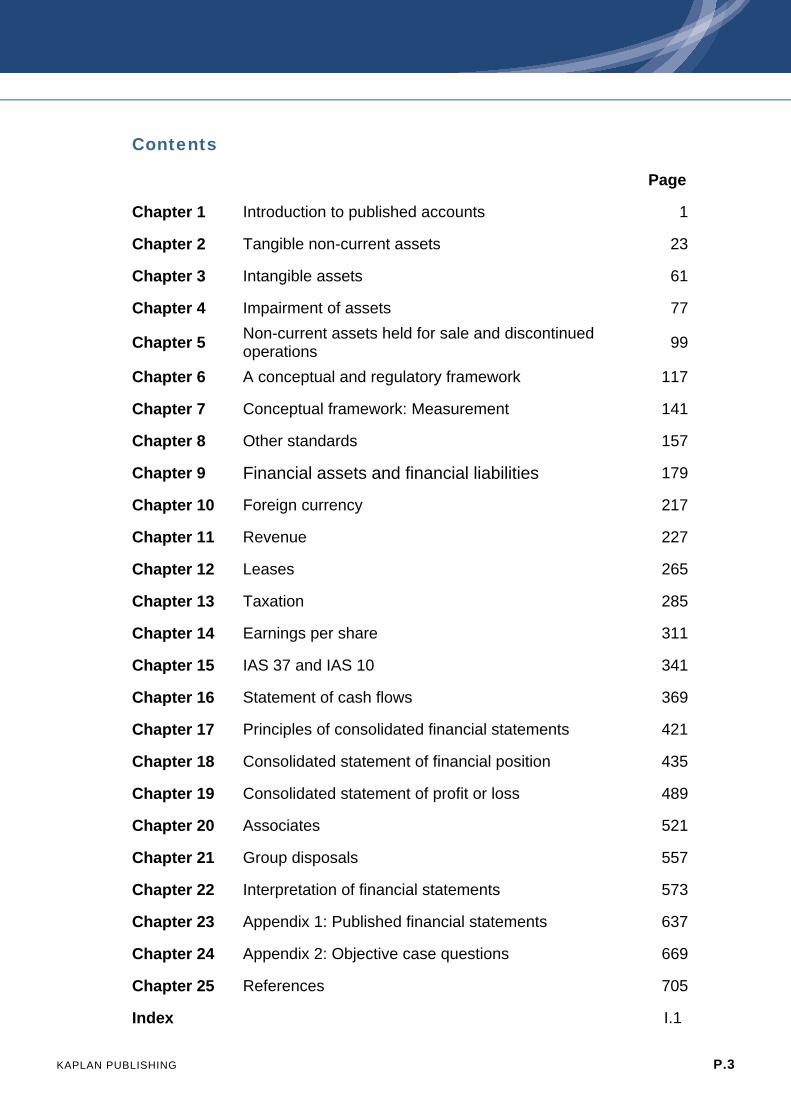

Contents

Page

Chapter 1 Introduction to published accounts 1

Chapter 2 Tangible non-current assets 23

Chapter 3 Intangible assets 61

Chapter 4 Impairment of assets 77

Chapter 5 Non-current assets held for sale and discontinued operations

99

Chapter 6 A conceptual and regulatory framework 117

Chapter 7 Conceptual framework: Measurement 141

Chapter 8 Other standards 157

Chapter 9 Financial assets and financial liabilities 179

Chapter 10 Foreign currency 217

Chapter 11 Revenue 227

Chapter 12 Leases 265

Chapter 13 Taxation 285

Chapter 14 Earnings per share 311

Chapter 15 IAS 37 and IAS 10 341

Chapter 16 Statement of cash flows 369

Chapter 17 Principles of consolidated financial statements 421

Chapter 18 Consolidated statement of financial position 435

Chapter 19 Consolidated statement of profit or loss 489

Chapter 20 Associates 521

Chapter 21 Group disposals 557

Chapter 22 Interpretation of financial statements 573

Chapter 23 Appendix 1: Published financial statements 637

Chapter 24 Appendix 2: Objective case questions 669

Chapter 25 References 705

Index I.1

KAPLAN PUBLISHING P.5

Introduction This document references IFRS® Standards and IAS® Standards, which are authored by the International Accounting Standards Board (the Board), and published in the 2018 IFRS Standards Red Book.

P.6 KAPLAN PUBLISHING

How to use the Materials These Kaplan Publishing learning materials have been carefully designed to make your learning experience as easy as possible and to give you the best chances of success in your examinations.

The product range contains a number of features to help you in the study process. They include:

1 Detailed study guide and syllabus objectives

2 Description of the examination

3 Study skills and revision guidance

4 Study text

5 Question practice

The sections on the study guide, the syllabus objectives, the examination and study skills should all be read before you commence your studies. They are designed to familiarise you with the nature and content of the examination and give you tips on how best to approach your learning.

The Study Text comprises the main learning materials and gives guidance as to the importance of topics and where other related resources can be found. Each chapter includes:

The learning objectives contained in each chapter, which have been carefully mapped to the examining body's own syllabus learning objectives or outcomes. You should use these to check you have a clear understanding of all the topics on which you might be assessed in the examination.

The chapter diagram provides a visual reference for the content in the chapter, giving an overview of the topics and how they link together.

The content for each topic area commences with a brief explanation or definition to put the topic into context before covering the topic in detail. You should follow your studying of the content with a review of the illustration/s. There are worked examples which will help you to better understand how to apply the content to the topic.

Test your understanding sections provide an opportunity to assess your understanding of the key topics by applying what you have learned to short questions. Answers can be found at the back of each chapter.

Summary diagrams complete each chapter to show the important links between topics and the overall content of the paper. These diagrams should be used to check that you have covered and understood the core topics before moving on.

KAPLAN PUBLISHING P.7

Quality and accuracy are of the utmost importance to us so if you spot an error in any of our products, please send an email to [email protected] with full details, or follow the link to the feedback form in MyKaplan.

Our Quality Coordinator will work with our technical team to verify the error and take action to ensure it is corrected in future editions.

Icon Explanations

Definition – Key definitions that you will need to learn from the core content.

Key point – Identifies topics that are key to success and are often examined.

Test your understanding – Exercises for you to complete to ensure that you have understood the topics just learned.

Illustration – Worked examples help you understand the core content better.

Supplementary reading – These sections will help to provide a deeper understanding of core areas. The supplementary reading is NOT optional reading. It is vital to provide you with the breadth of knowledge you will need to address the wide range of topics within your syllabus that could feature in an exam question. Reference to this text is vital when self-studying.

Tutorial note – Included to explain some of the technical points in more detail.

Footsteps – Helpful tutor tips.

P.8 KAPLAN PUBLISHING

On-line subscribers Our on-line resources are designed to increase the flexibility of your learning materials and provide you with immediate feedback on how your studies are progressing.

If you are subscribed to our on-line resources you will find:

1 On-line reference-ware: reproduces your Study Text on-line, giving you anytime/anywhere access.

2 On-line testing: provides you with additional on-line objective testing so you can practise what you have learned further.

3 On-line performance management: immediate access to your on-line testing results. Review your performance by key topics and chart your achievement through the course relative to your peer group.

Syllabus Core areas of the syllabus A conceptual framework for financial reporting.

A regulatory framework for financial reporting.

Financial statements.

Business combinations.

Analysing and interpreting financial statements.

ACCA Performance Objectives

In order to become a member of the ACCA, as a trainee accountant you will need to demonstrate that you have achieved nine performance objectives. Performance objectives are indicators of effective performance and set the minimum standard of work that trainees are expected to achieve and demonstrate in the workplace. They are divided into key areas of knowledge which are closely linked to the exam syllabus.

There are five Essential performance objectives and a choice of fifteen Technical performance objectives which are divided into five areas.

The performance objectives which link to this exam are:

1 Ethics and professionalism (Essential)

2 Stakeholder relationship management (Essential)

6 Record and process transactions and events (Technical)

7 Prepare external financial reports (Technical)

8 Analyse and interpret financial reports (Technical)

The following link provides an in-depth insight into all of the performance objectives:

https://www.accaglobal.com/content/dam/ACCA_Global/Students/per/PER-Performance-objectives-achieve.pdf

KAPLAN PUBLISHING P.9

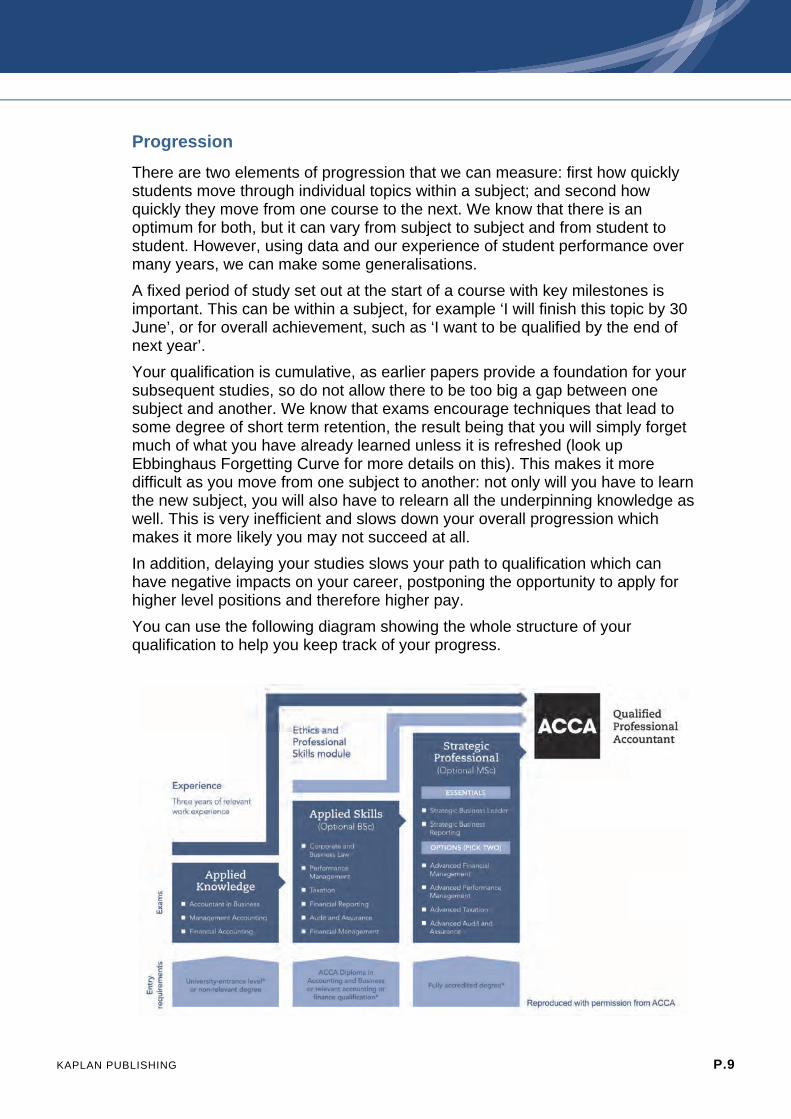

Progression

There are two elements of progression that we can measure: first how quickly students move through individual topics within a subject; and second how quickly they move from one course to the next. We know that there is an optimum for both, but it can vary from subject to subject and from student to student. However, using data and our experience of student performance over many years, we can make some generalisations.

A fixed period of study set out at the start of a course with key milestones is important. This can be within a subject, for example ‘I will finish this topic by 30 June’, or for overall achievement, such as ‘I want to be qualified by the end of next year’.

Your qualification is cumulative, as earlier papers provide a foundation for your subsequent studies, so do not allow there to be too big a gap between one subject and another. We know that exams encourage techniques that lead to some degree of short term retention, the result being that you will simply forget much of what you have already learned unless it is refreshed (look up Ebbinghaus Forgetting Curve for more details on this). This makes it more difficult as you move from one subject to another: not only will you have to learn the new subject, you will also have to relearn all the underpinning knowledge as well. This is very inefficient and slows down your overall progression which makes it more likely you may not succeed at all.

In addition, delaying your studies slows your path to qualification which can have negative impacts on your career, postponing the opportunity to apply for higher level positions and therefore higher pay.

You can use the following diagram showing the whole structure of your qualification to help you keep track of your progress.

P.20 KAPLAN PUBLISHING

Syllabus learning objective Chapter reference

(h) Explain and illustrate the effect of a disposal of a parent's investment in a subsidiary in the parent's individual financial statements and/or those of the group (restricted to disposals of the parent's entire investment in the subsidiary).

21

The numbers in square brackets indicate the intellectual depth at which the subject area could be assessed within the examination. Level 1 (knowledge and comprehension) broadly equates with the Knowledge module, Level 2 (application and analysis) with the Skills module and Level 3 (synthesis and evaluation) to the Professional level. However, lower level skills can continue to be assessed as you progress through each module and level.

The Examination

Examination format All questions are compulsory. The examination will contain both computational and discursive elements.

Some questions will adopt a scenario/case study approach.

Section A of the examination comprises 15 objective test (OT) questions of 2 marks each.

Section B of the examination comprises three objective case questions (OT cases) worth 10 marks each. Each case has five objective test questions of 2 marks each.

Section C of the examination comprises two constructed response (CR) questions, worth 20 marks each.

The 20 mark questions will examine the interpretation and preparation of financial statements for either a single entity or a group. The section A and section B questions can cover any areas of the syllabus.

An individual question may often involve elements that relate to different subject areas of the syllabus. For example, the preparation of an entity's financial statements could include matters relating to several accounting standards.

Questions may ask candidates to comment on the appropriateness or acceptability of management's opinion or chosen accounting treatment. An understanding of accounting principles and concepts and how these are applied to practical examples will be tested.

Questions on topic areas that are also included in Financial Accounting (FA) will be examined at an appropriately greater depth in this examination.

Candidates will be expected to have an appreciation of the need for specific accounting standards and why they have been issued. For detailed or complex standards, candidates need to be aware of their principles and key elements.

KAPLAN PUBLISHING P.21

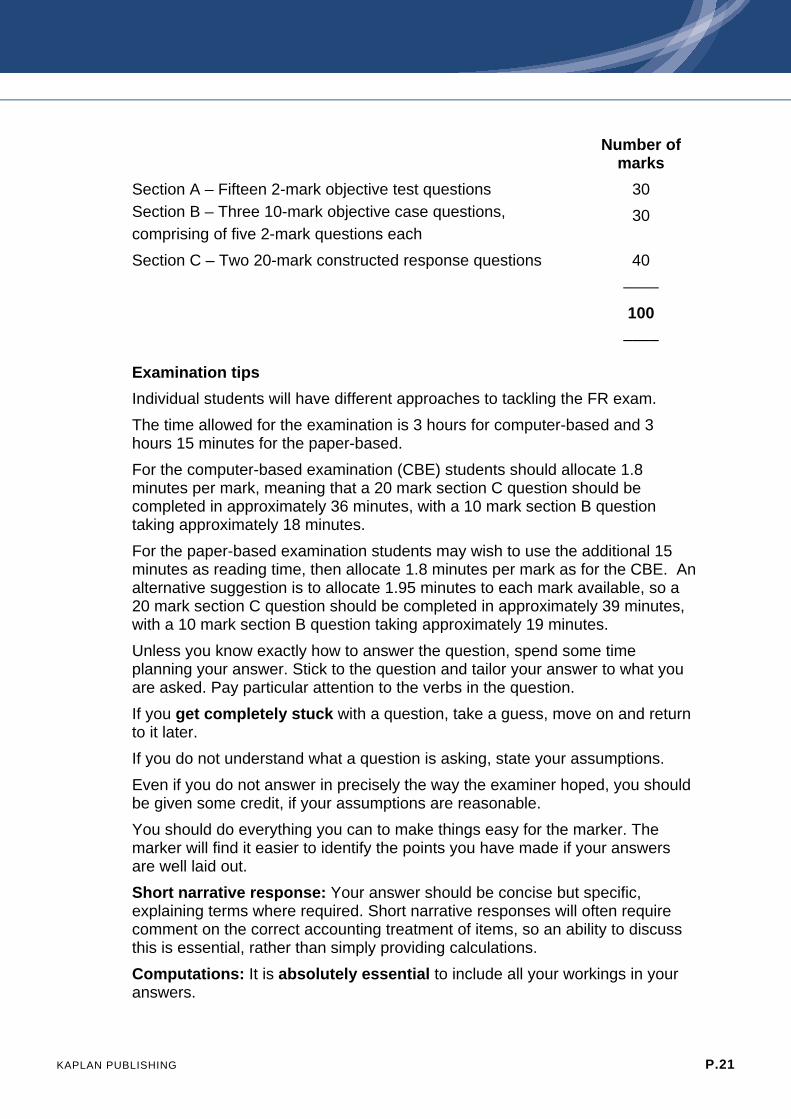

Number of marks

Section A – Fifteen 2-mark objective test questions 30

Section B – Three 10-mark objective case questions,

comprising of five 2-mark questions each 30

Section C – Two 20-mark constructed response questions 40

––––

100 ––––

Examination tips Individual students will have different approaches to tackling the FR exam.

The time allowed for the examination is 3 hours for computer-based and 3 hours 15 minutes for the paper-based.

For the computer-based examination (CBE) students should allocate 1.8 minutes per mark, meaning that a 20 mark section C question should be completed in approximately 36 minutes, with a 10 mark section B question taking approximately 18 minutes.

For the paper-based examination students may wish to use the additional 15 minutes as reading time, then allocate 1.8 minutes per mark as for the CBE. An alternative suggestion is to allocate 1.95 minutes to each mark available, so a 20 mark section C question should be completed in approximately 39 minutes, with a 10 mark section B question taking approximately 19 minutes.

Unless you know exactly how to answer the question, spend some time planning your answer. Stick to the question and tailor your answer to what you are asked. Pay particular attention to the verbs in the question.

If you get completely stuck with a question, take a guess, move on and return to it later.

If you do not understand what a question is asking, state your assumptions.

Even if you do not answer in precisely the way the examiner hoped, you should be given some credit, if your assumptions are reasonable.

You should do everything you can to make things easy for the marker. The marker will find it easier to identify the points you have made if your answers are well laid out.

Short narrative response: Your answer should be concise but specific, explaining terms where required. Short narrative responses will often require comment on the correct accounting treatment of items, so an ability to discuss this is essential, rather than simply providing calculations.

Computations: It is absolutely essential to include all your workings in your answers.

KAPLAN PUBLISHING 1

Introduction to published accounts

Chapter learning objectives

Upon completion of this chapter you will be able to:

prepare an entity’s financial statements in accordance with prescribed structure and content

prepare and explain the contents and purpose of the statement of changes in equity.

Chapter

1

PER

One of the PER performance objectives (PO7) is to prepare external financial reports. You take part in preparing and reviewing financial statements – and all accompanying information – and you do it in accordance with legal and regulatory requirements. Working though this chapter should help you understand how to demonstrate that objective.

Introduction to published accounts

2 KAPLAN PUBLISHING

Preparation of single entity financial statements could be examined as one of the constructed response questions in section C of the FR examination. This chapter will look at the techniques and principles behind the construction of this. It is important to note that Chapters 2 to 15 contain information on specific accounting standards, any of which could be included within the construction of single entity financial statements. Once you have worked through these chapters, Chapter 23 provides practice of single entity financial statements with those standards incorporated into them.

1 Preparation of financial statements for companies

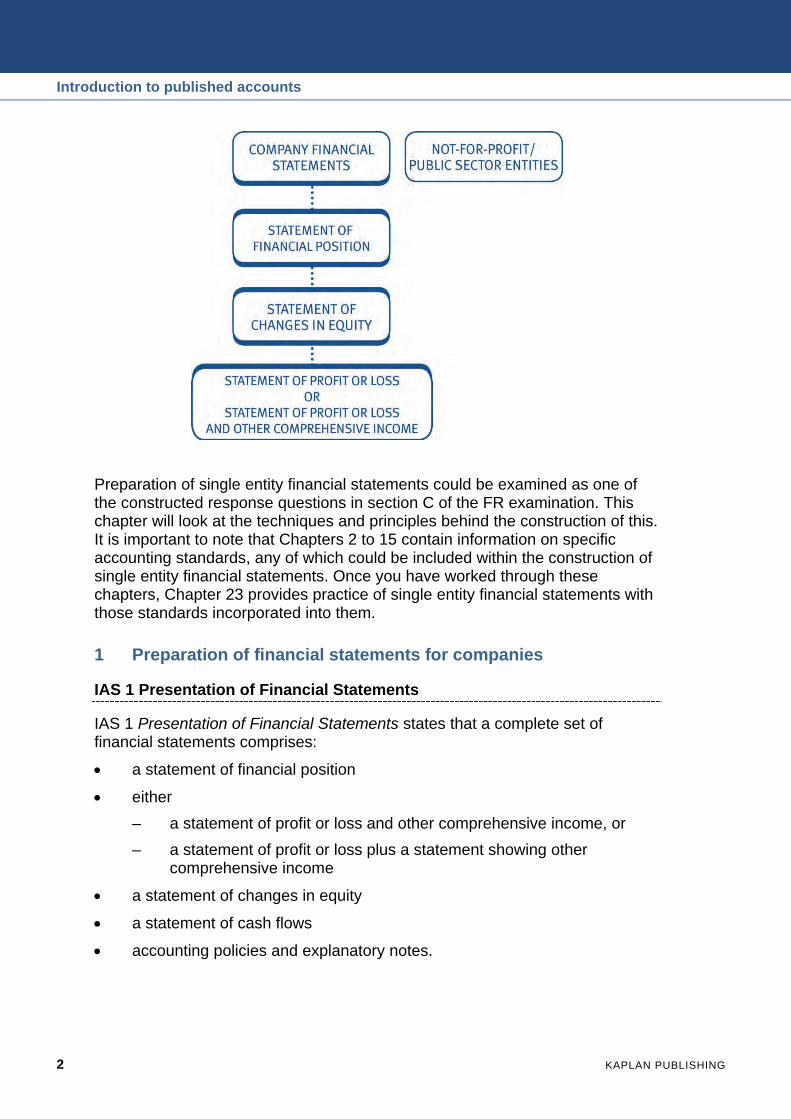

IAS 1 Presentation of Financial Statements

IAS 1 Presentation of Financial Statements states that a complete set of financial statements comprises:

a statement of financial position

either

– a statement of profit or loss and other comprehensive income, or

– a statement of profit or loss plus a statement showing other comprehensive income

a statement of changes in equity

a statement of cash flows

accounting policies and explanatory notes.

Chapter 1

KAPLAN PUBLISHING 3

IAS 1 (revised) does not require the above titles to be used by companies. It is likely in practice that many companies will continue to use the previous terms of balance sheet rather than statement of financial position, income statement instead of statement of profit or loss, and cash flow statement rather than statement of cash flows.

Exceptional items

Exceptional items is the name often given to material items of income and expense of such size, nature or incidence that disclosure is necessary in order to explain the performance of the entity.

The accounting treatment is to:

include the item in the standard statement of profit or loss line

disclose the nature and amount in the notes.

In some cases it may be more appropriate to show the item separately on the face of the statement of profit or loss.

Examples include:

write down of inventories to net realisable value (NRV)

impairment of property, plant and equipment

restructuring costs

gains/losses on disposal of non-current assets

discontinued operations

litigation settlements

reversals of provisions

Introduction to published accounts

4 KAPLAN PUBLISHING

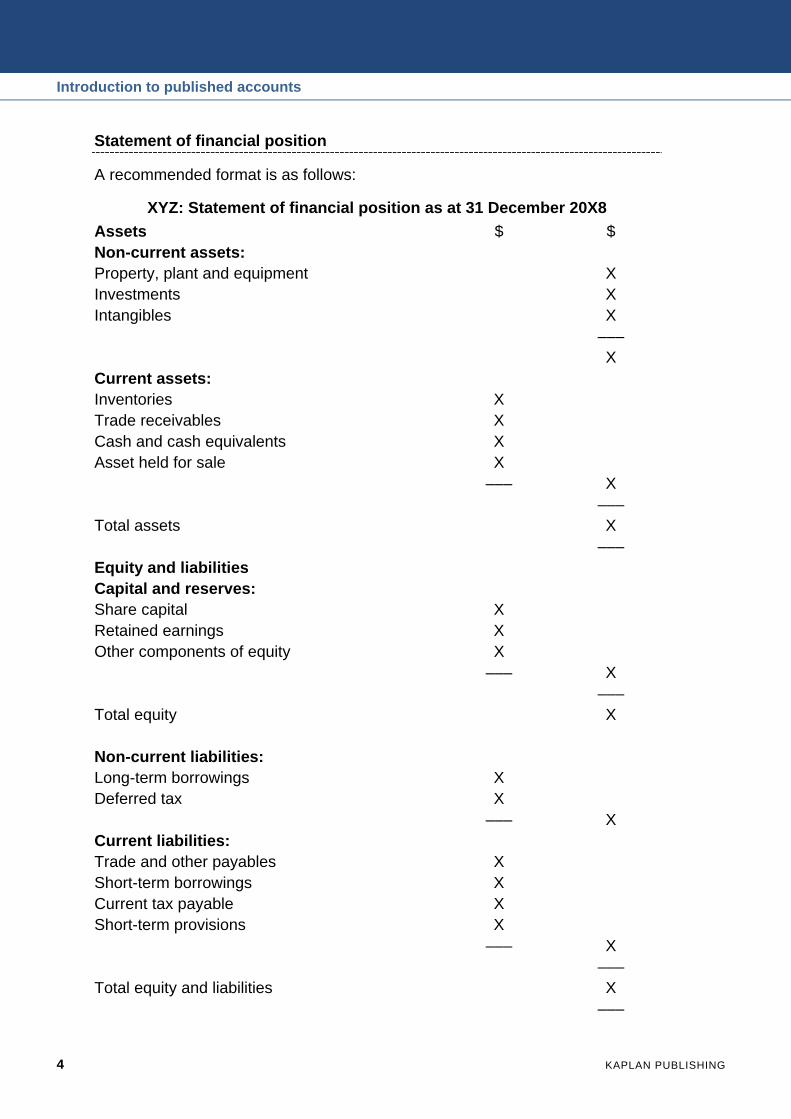

Statement of financial position

A recommended format is as follows:

XYZ: Statement of financial position as at 31 December 20X8 Assets $ $ Non-current assets: Property, plant and equipment X Investments X Intangibles X ––– X Current assets: Inventories X Trade receivables X Cash and cash equivalents X Asset held for sale X ––– X ––– Total assets X ––– Equity and liabilities Capital and reserves: Share capital X Retained earnings X Other components of equity X ––– X ––– Total equity X Non-current liabilities: Long-term borrowings X Deferred tax X ––– X Current liabilities: Trade and other payables X Short-term borrowings X Current tax payable X Short-term provisions X ––– X ––– Total equity and liabilities X –––

Chapter 1

KAPLAN PUBLISHING 5

Note that IAS 1 requires an asset or liability to be classified as current if:

it will be settled within 12 months of the reporting date, or

it is part of the entity's normal operating cycle.

Within the equity section of the statement of financial position, other components of equity include:

revaluation surplus

share premium

investment reserve (see financial instruments, Chapter 9).

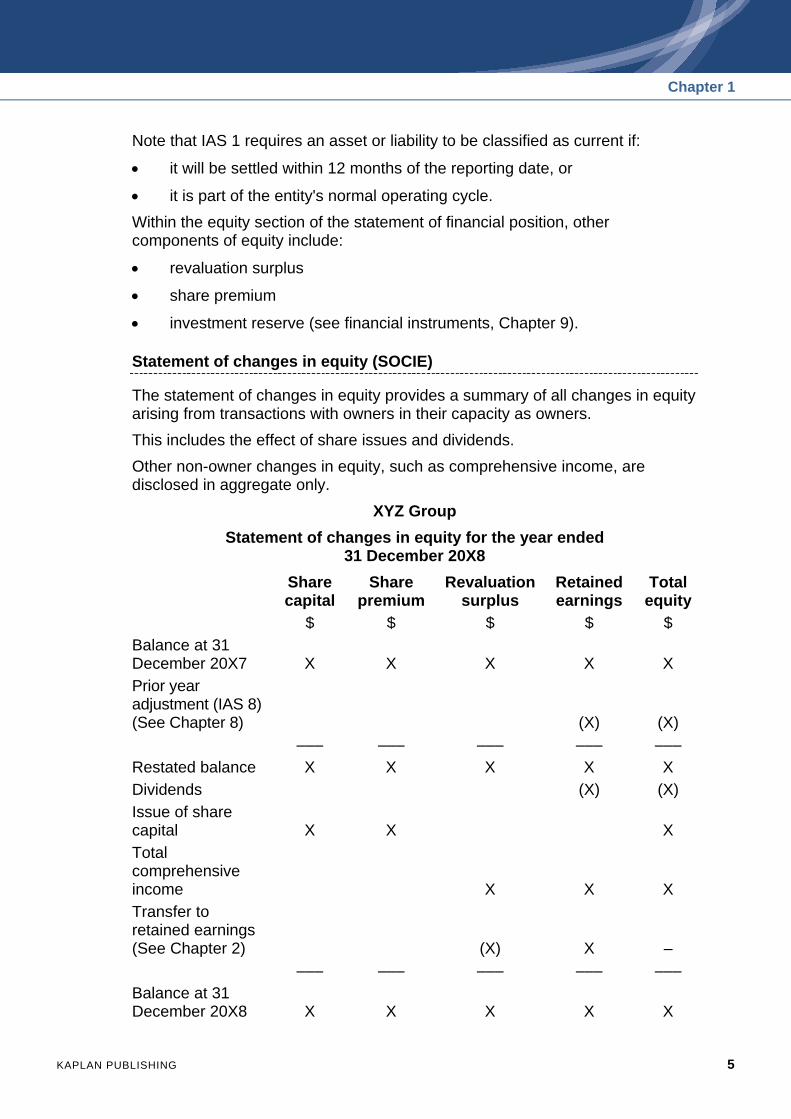

Statement of changes in equity (SOCIE)

The statement of changes in equity provides a summary of all changes in equity arising from transactions with owners in their capacity as owners.

This includes the effect of share issues and dividends.

Other non-owner changes in equity, such as comprehensive income, are disclosed in aggregate only.

XYZ Group Statement of changes in equity for the year ended

31 December 20X8

Share capital

Share premium

Revaluation surplus

Retained earnings

Total equity

$ $ $ $ $

Balance at 31 December 20X7 X X X X X

Prior year adjustment (IAS 8) (See Chapter 8) (X) (X)

––– ––– ––– ––– –––

Restated balance X X X X X

Dividends (X) (X)

Issue of share capital X X X

Total comprehensive income X X X

Transfer to retained earnings (See Chapter 2) (X) X –

––– ––– ––– ––– –––

Balance at 31 December 20X8 X X X X X

Introduction to published accounts

6 KAPLAN PUBLISHING

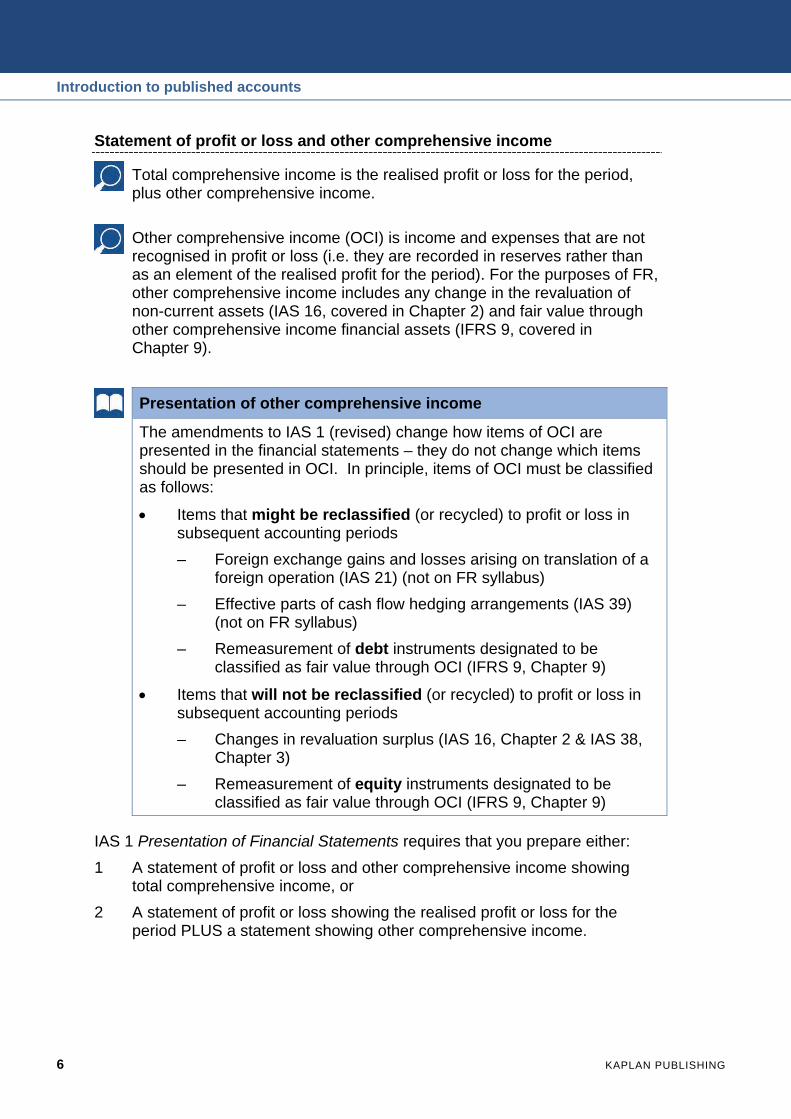

Statement of profit or loss and other comprehensive income

Total comprehensive income is the realised profit or loss for the period, plus other comprehensive income.

Other comprehensive income (OCI) is income and expenses that are not recognised in profit or loss (i.e. they are recorded in reserves rather than as an element of the realised profit for the period). For the purposes of FR, other comprehensive income includes any change in the revaluation of non-current assets (IAS 16, covered in Chapter 2) and fair value through other comprehensive income financial assets (IFRS 9, covered in Chapter 9).

Presentation of other comprehensive income

The amendments to IAS 1 (revised) change how items of OCI are presented in the financial statements – they do not change which items should be presented in OCI. In principle, items of OCI must be classified as follows:

Items that might be reclassified (or recycled) to profit or loss in subsequent accounting periods

– Foreign exchange gains and losses arising on translation of a foreign operation (IAS 21) (not on FR syllabus)

– Effective parts of cash flow hedging arrangements (IAS 39) (not on FR syllabus)

– Remeasurement of debt instruments designated to be classified as fair value through OCI (IFRS 9, Chapter 9)

Items that will not be reclassified (or recycled) to profit or loss in subsequent accounting periods

– Changes in revaluation surplus (IAS 16, Chapter 2 & IAS 38, Chapter 3)

– Remeasurement of equity instruments designated to be classified as fair value through OCI (IFRS 9, Chapter 9)

IAS 1 Presentation of Financial Statements requires that you prepare either:

1 A statement of profit or loss and other comprehensive income showing total comprehensive income, or

2 A statement of profit or loss showing the realised profit or loss for the period PLUS a statement showing other comprehensive income.

Chapter 1

KAPLAN PUBLISHING 7

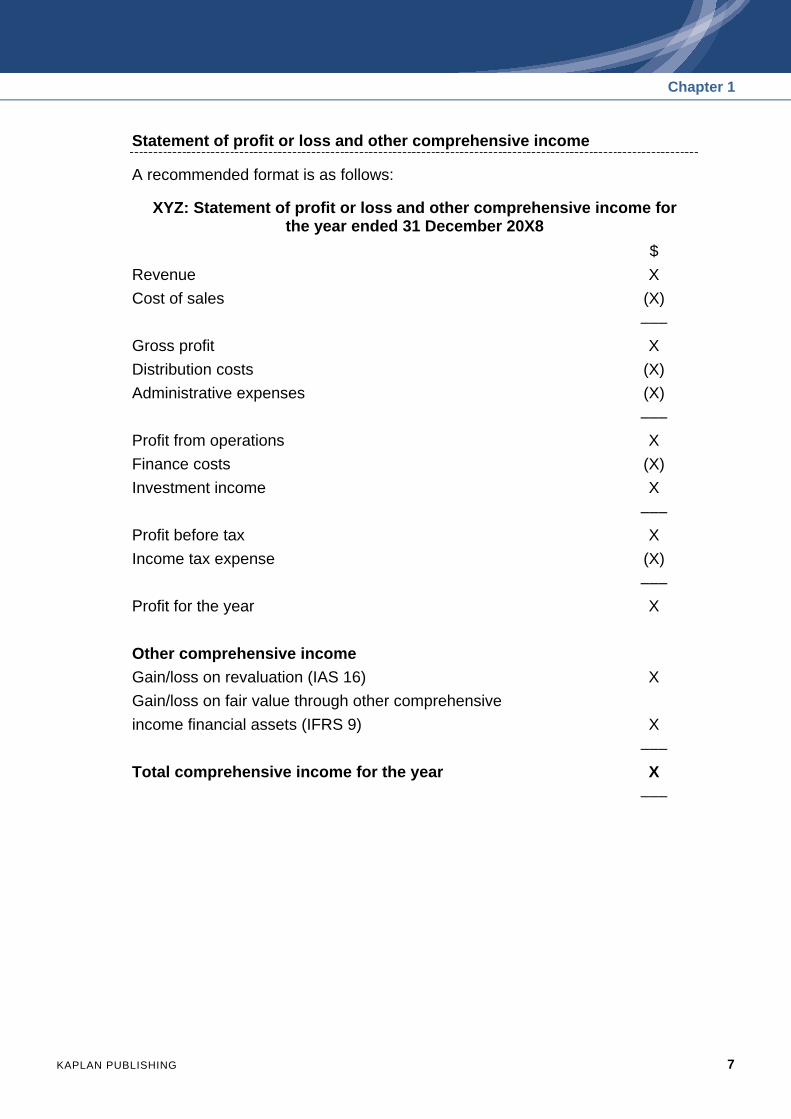

Statement of profit or loss and other comprehensive income

A recommended format is as follows:

XYZ: Statement of profit or loss and other comprehensive income for the year ended 31 December 20X8

$

Revenue X

Cost of sales (X)

–––

Gross profit X

Distribution costs (X)

Administrative expenses (X)

–––

Profit from operations X

Finance costs (X)

Investment income X

–––

Profit before tax X

Income tax expense (X)

–––

Profit for the year X

Other comprehensive income

Gain/loss on revaluation (IAS 16) X

Gain/loss on fair value through other comprehensive

income financial assets (IFRS 9) X

–––

Total comprehensive income for the year X –––

Introduction to published accounts

8 KAPLAN PUBLISHING

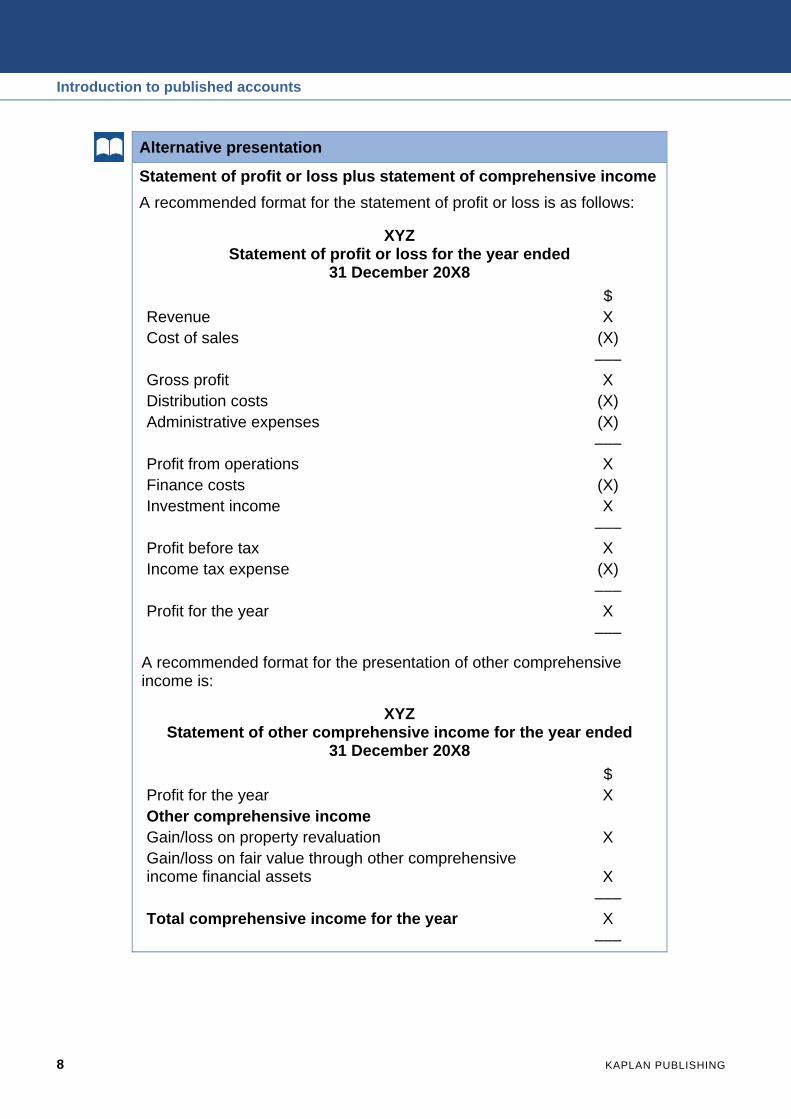

Alternative presentation

Statement of profit or loss plus statement of comprehensive income A recommended format for the statement of profit or loss is as follows:

XYZ Statement of profit or loss for the year ended

31 December 20X8 $ Revenue X Cost of sales (X) ––– Gross profit X Distribution costs (X) Administrative expenses (X) ––– Profit from operations X Finance costs (X) Investment income X ––– Profit before tax X Income tax expense (X) ––– Profit for the year X –––

A recommended format for the presentation of other comprehensive income is:

XYZ Statement of other comprehensive income for the year ended

31 December 20X8 $ Profit for the year X Other comprehensive income Gain/loss on property revaluation X Gain/loss on fair value through other comprehensive income financial assets X ––– Total comprehensive income for the year X –––

Chapter 1

KAPLAN PUBLISHING 9

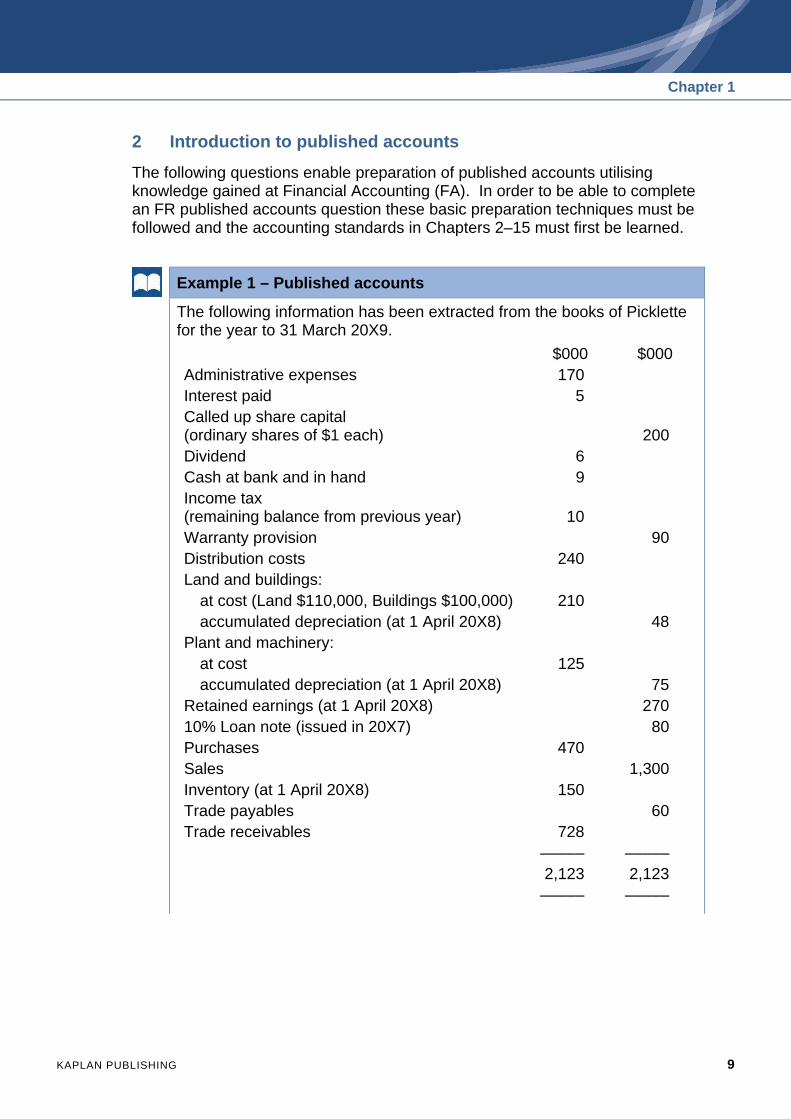

2 Introduction to published accounts

The following questions enable preparation of published accounts utilising knowledge gained at Financial Accounting (FA). In order to be able to complete an FR published accounts question these basic preparation techniques must be followed and the accounting standards in Chapters 2–15 must first be learned.

Example 1 – Published accounts

The following information has been extracted from the books of Picklette for the year to 31 March 20X9.

$000 $000 Administrative expenses 170 Interest paid 5 Called up share capital (ordinary shares of $1 each) 200 Dividend 6 Cash at bank and in hand 9 Income tax (remaining balance from previous year) 10 Warranty provision 90 Distribution costs 240 Land and buildings: at cost (Land $110,000, Buildings $100,000) 210 accumulated depreciation (at 1 April 20X8) 48 Plant and machinery: at cost 125 accumulated depreciation (at 1 April 20X8) 75 Retained earnings (at 1 April 20X8) 270 10% Loan note (issued in 20X7) 80 Purchases 470 Sales 1,300 Inventory (at 1 April 20X8) 150 Trade payables 60 Trade receivables 728 ––––– ––––– 2,123 2,123 ––––– –––––

Introduction to published accounts

10 KAPLAN PUBLISHING

Additional information 1 Inventory at 31 March 20X9 was valued at $250,000.

2 Buildings and plant and machinery are depreciated on a straight-line basis (assuming no residual value) at the following rates:

On cost: Buildings 5% Plant and machinery 20%

3 There were no purchases or sales of non-current assets during the year to 31 March 20X9.

4 The depreciation charges for the year to 31 March 20X9 are to be apportioned as follows:

Cost of sales 60% Distribution costs 20% Administrative expenses 20%

5 Income taxes for the year to 31 March 20X9 are estimated to be $135,000.

6 The 10% loan note was issued on 1 April 20X7 and is repayable five years from that date.

7 The year-end provision for warranty claims has been estimated at $75,000. Warranty costs are charged to administrative expenses.

Required: Prepare Picklette’s statement of profit or loss for the year to 31 March 20X9 and a statement of financial position as at that date.

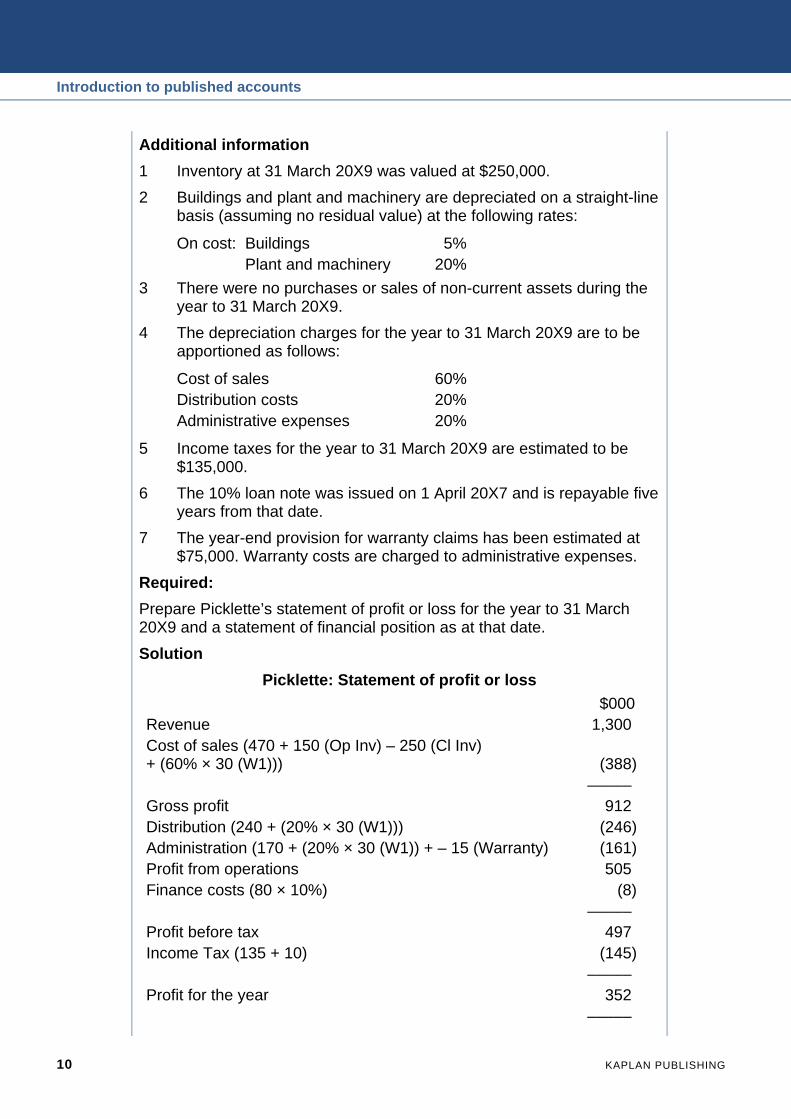

Solution Picklette: Statement of profit or loss

$000 Revenue 1,300 Cost of sales (470 + 150 (Op Inv) – 250 (Cl Inv) + (60% × 30 (W1))) (388) ––––– Gross profit 912 Distribution (240 + (20% × 30 (W1))) (246) Administration (170 + (20% × 30 (W1)) + – 15 (Warranty) (161) Profit from operations 505 Finance costs (80 × 10%) (8) ––––– Profit before tax 497 Income Tax (135 + 10) (145) ––––– Profit for the year 352 –––––

Chapter 1

KAPLAN PUBLISHING 11

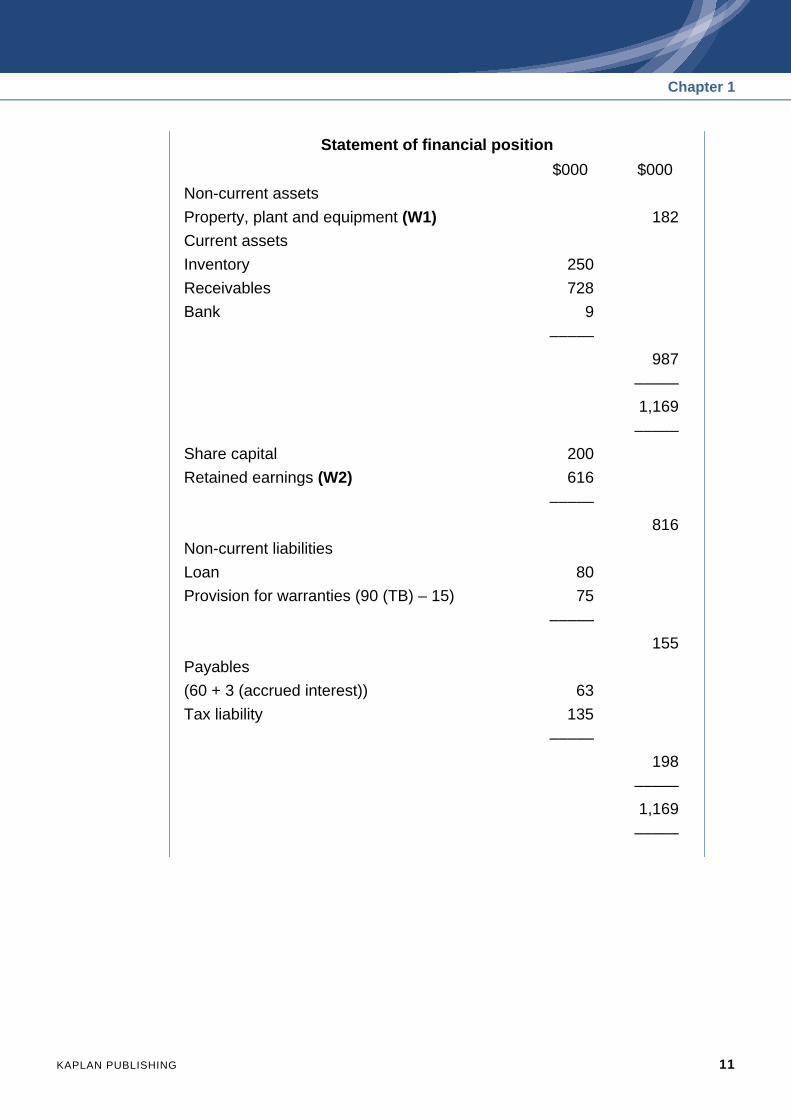

Statement of financial position $000 $000

Non-current assets

Property, plant and equipment (W1) 182

Current assets

Inventory 250

Receivables 728

Bank 9

–––––

987

–––––

1,169

–––––

Share capital 200

Retained earnings (W2) 616

–––––

816

Non-current liabilities

Loan 80

Provision for warranties (90 (TB) – 15) 75

–––––

155

Payables

(60 + 3 (accrued interest)) 63

Tax liability 135

–––––

198

–––––

1,169

–––––

Introduction to published accounts

12 KAPLAN PUBLISHING

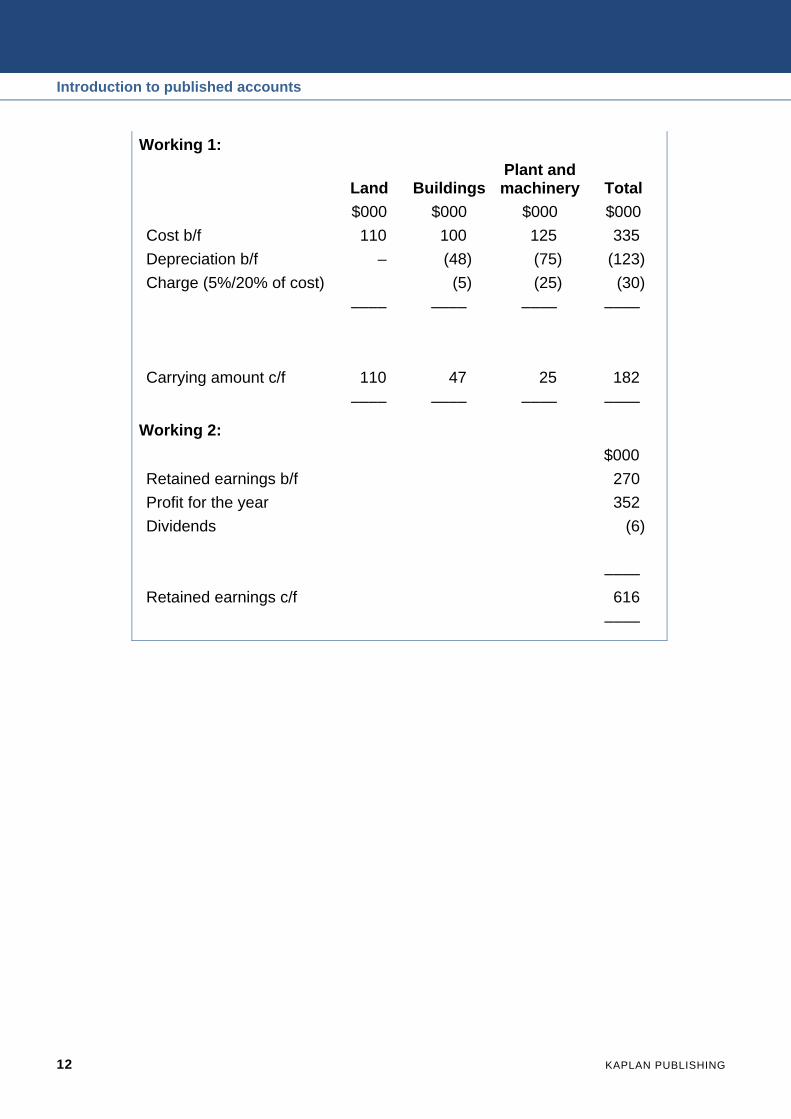

Working 1:

Land Buildings Plant and machinery Total

$000 $000 $000 $000

Cost b/f 110 100 125 335

Depreciation b/f – (48) (75) (123)

Charge (5%/20% of cost) (5) (25) (30)

–––– –––– –––– ––––

Carrying amount c/f 110 47 25 182

–––– –––– –––– ––––

Working 2: $000

Retained earnings b/f 270

Profit for the year 352

Dividends (6)

––––

Retained earnings c/f 616

––––

Chapter 1

KAPLAN PUBLISHING 13

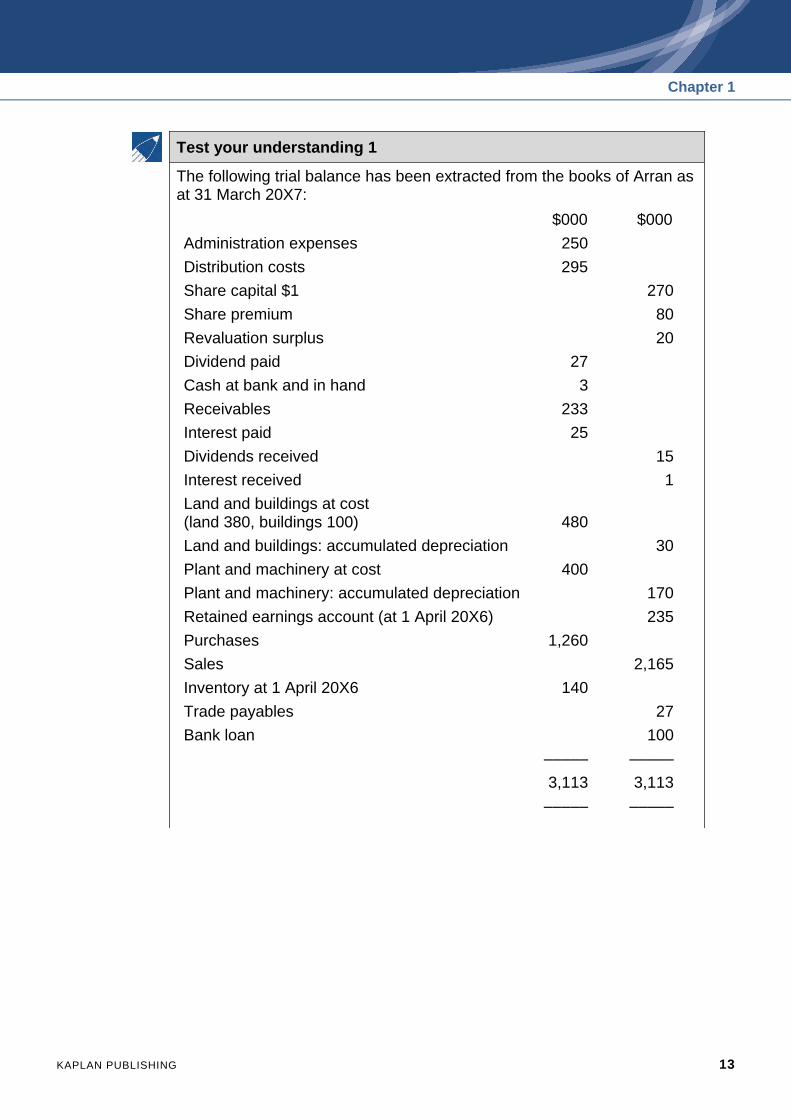

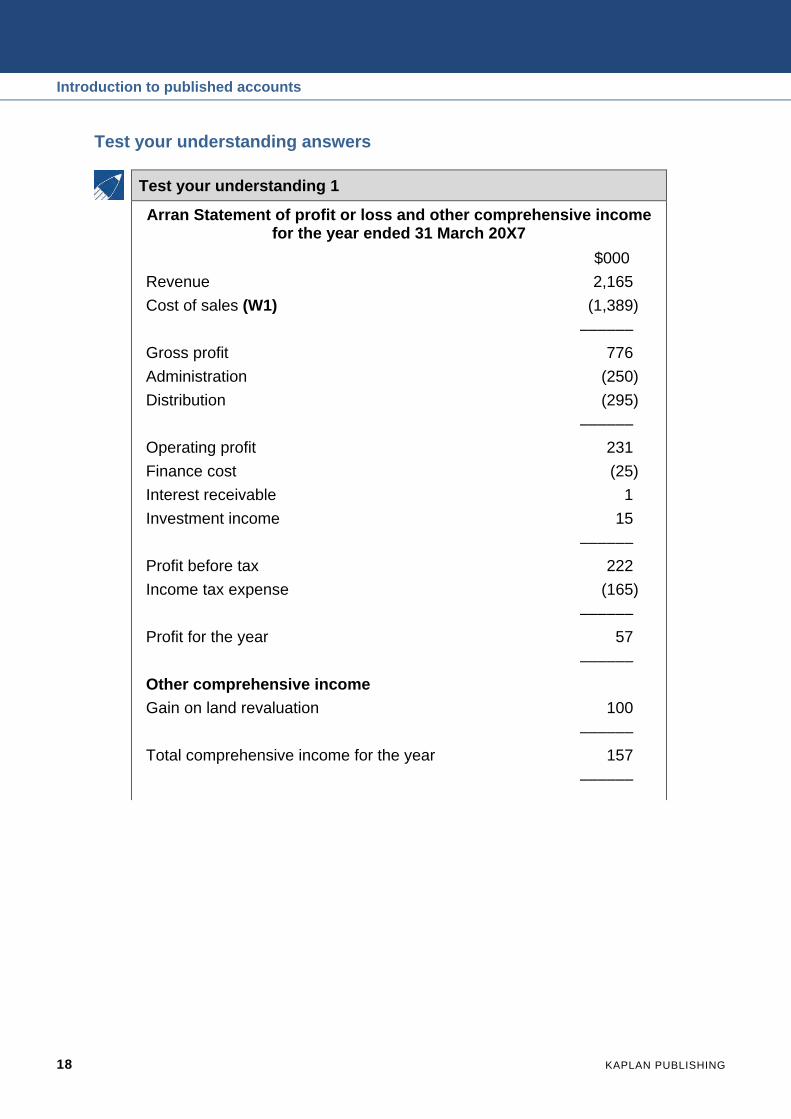

Test your understanding 1

The following trial balance has been extracted from the books of Arran as at 31 March 20X7:

$000 $000

Administration expenses 250

Distribution costs 295

Share capital $1 270

Share premium 80

Revaluation surplus 20

Dividend paid 27

Cash at bank and in hand 3

Receivables 233

Interest paid 25

Dividends received 15

Interest received 1

Land and buildings at cost (land 380, buildings 100) 480

Land and buildings: accumulated depreciation 30

Plant and machinery at cost 400

Plant and machinery: accumulated depreciation 170

Retained earnings account (at 1 April 20X6) 235

Purchases 1,260

Sales 2,165

Inventory at 1 April 20X6 140

Trade payables 27

Bank loan 100

––––– –––––

3,113 3,113

––––– –––––

Introduction to published accounts

14 KAPLAN PUBLISHING

Additional information 1 Inventory at 31 March 20X7 was valued at a cost of $95,000.

Included in this balance were goods that had cost $15,000. These goods had become damaged during the year and it is considered that the goods could be sold for $5,000, after paying commission of $500.

2 Depreciation for the year to 31 March 20X7 is to be charged against cost of sales as follows:

Buildings 5% on cost (straight line) Plant and machinery 30% on carrying amount (reducing balance)

3 Land is to be revalued upwards by $100,000.

4 Income tax of $165,000 is to be provided for the year to 31 March 20X7.

5 The bank loan is repayable in five years' time.

Prepare the statement of profit or loss and other comprehensive income, statement of changes in equity and statement of financial position for year ended 31 March 20X7. Note: Show all workings, notes are not required.

3 Not-for-profit and public sector entities

Not-for-profit and public sector entities

Comparison of aims

The main aims of not-for-profit and public sector entities are very different to those of profit-orientated entities:

Profit-orientated sector Not-for-profit/public sector Financial aim is to make profit and increase shareholder wealth.

Financial aim is to achieve value for money/provide service.

Directors are accountable to shareholders.

Managers are accountable to trustees/government/public.

External finance freely available in the form of loans and share capital.

Finance generally limited to donations/ government subsidies.

Chapter 1

KAPLAN PUBLISHING 15

Accounting standards and not-for-profit and public sector entities

Accounting standards are designed to:

measure financial performance accurately and consistently

report the financial position accurately and consistently

account for the directors' stewardship of resources and assets.

Not-for-profit and public sector organisations:

do not aim to achieve a profit but have to account for their income and costs

have to account for their effectiveness, economy and efficiency

do not have to produce financial statements for the public (but in many cases may do so).

Some measurement accounting standards will be relevant such as those relating to inventory, non-current assets, leasing, etc. Others relating purely to reporting such as earnings per share (eps) will not be so relevant.

Introduction to published accounts

16 KAPLAN PUBLISHING

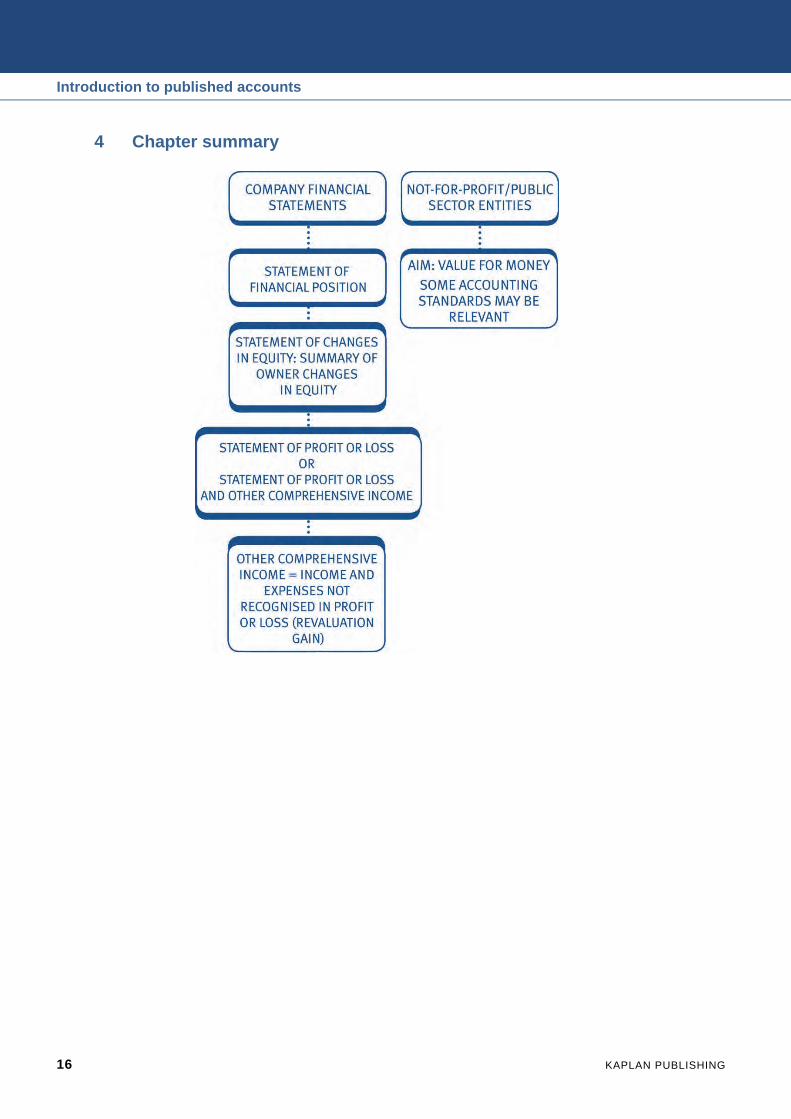

4 Chapter summary

Chapter 1

KAPLAN PUBLISHING 17

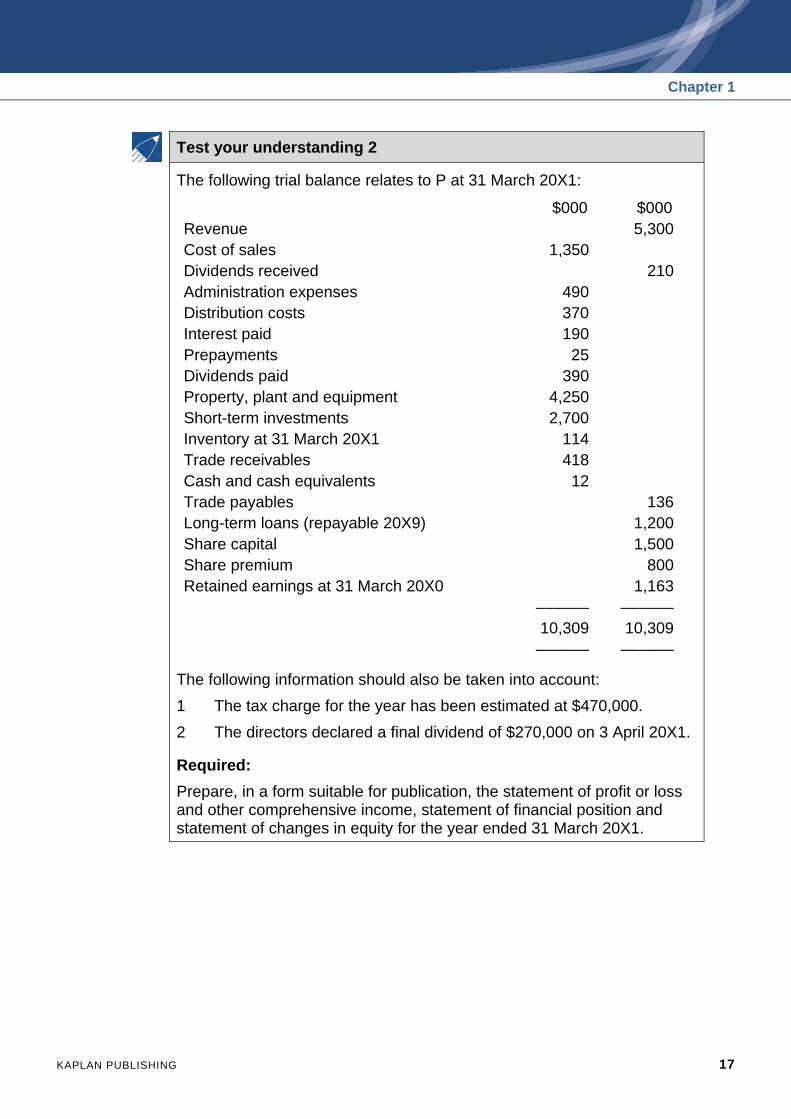

Test your understanding 2

The following trial balance relates to P at 31 March 20X1:

$000 $000 Revenue 5,300 Cost of sales 1,350 Dividends received 210 Administration expenses 490 Distribution costs 370 Interest paid 190 Prepayments 25 Dividends paid 390 Property, plant and equipment 4,250 Short-term investments 2,700 Inventory at 31 March 20X1 114 Trade receivables 418 Cash and cash equivalents 12 Trade payables 136 Long-term loans (repayable 20X9) 1,200 Share capital 1,500 Share premium 800 Retained earnings at 31 March 20X0 1,163 –––––– –––––– 10,309 10,309 –––––– ––––––

The following information should also be taken into account:

1 The tax charge for the year has been estimated at $470,000.

2 The directors declared a final dividend of $270,000 on 3 April 20X1.

Required: Prepare, in a form suitable for publication, the statement of profit or loss and other comprehensive income, statement of financial position and statement of changes in equity for the year ended 31 March 20X1.

Introduction to published accounts

18 KAPLAN PUBLISHING

Test your understanding answers

Test your understanding 1

Arran Statement of profit or loss and other comprehensive income for the year ended 31 March 20X7

$000

Revenue 2,165

Cost of sales (W1) (1,389)

––––––

Gross profit 776

Administration (250)

Distribution (295)

––––––

Operating profit 231

Finance cost (25)

Interest receivable 1

Investment income 15

––––––

Profit before tax 222

Income tax expense (165)

––––––

Profit for the year 57

––––––

Other comprehensive income

Gain on land revaluation 100

––––––

Total comprehensive income for the year 157

––––––

Chapter 1

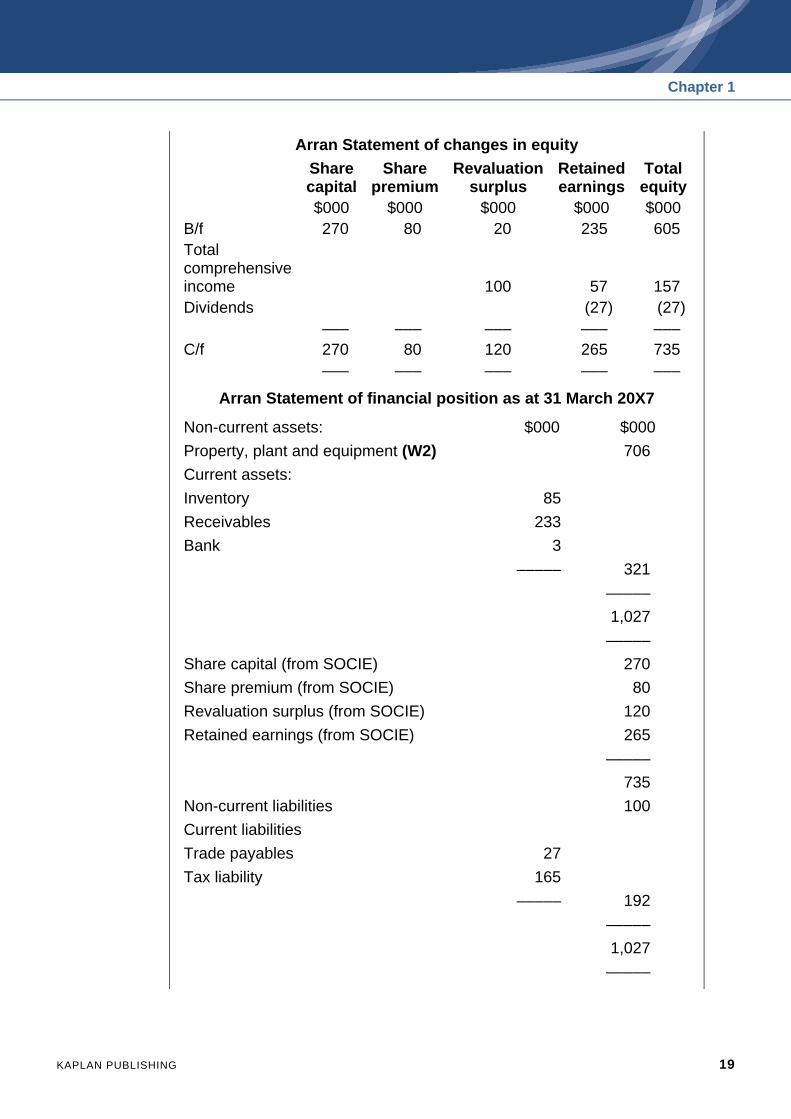

KAPLAN PUBLISHING 19

Arran Statement of changes in equity Share

capital Share

premium Revaluation

surplus Retained earnings

Total equity

$000 $000 $000 $000 $000 B/f 270 80 20 235 605 Total comprehensive income 100 57 157 Dividends (27) (27) ––– ––– ––– ––– ––– C/f 270 80 120 265 735 ––– ––– ––– ––– –––

Arran Statement of financial position as at 31 March 20X7

Non-current assets: $000 $000

Property, plant and equipment (W2) 706

Current assets:

Inventory 85

Receivables 233

Bank 3

––––– 321

–––––

1,027

–––––

Share capital (from SOCIE) 270

Share premium (from SOCIE) 80

Revaluation surplus (from SOCIE) 120

Retained earnings (from SOCIE) 265

–––––

735

Non-current liabilities 100

Current liabilities

Trade payables 27

Tax liability 165

––––– 192

–––––

1,027

–––––

Introduction to published accounts

20 KAPLAN PUBLISHING

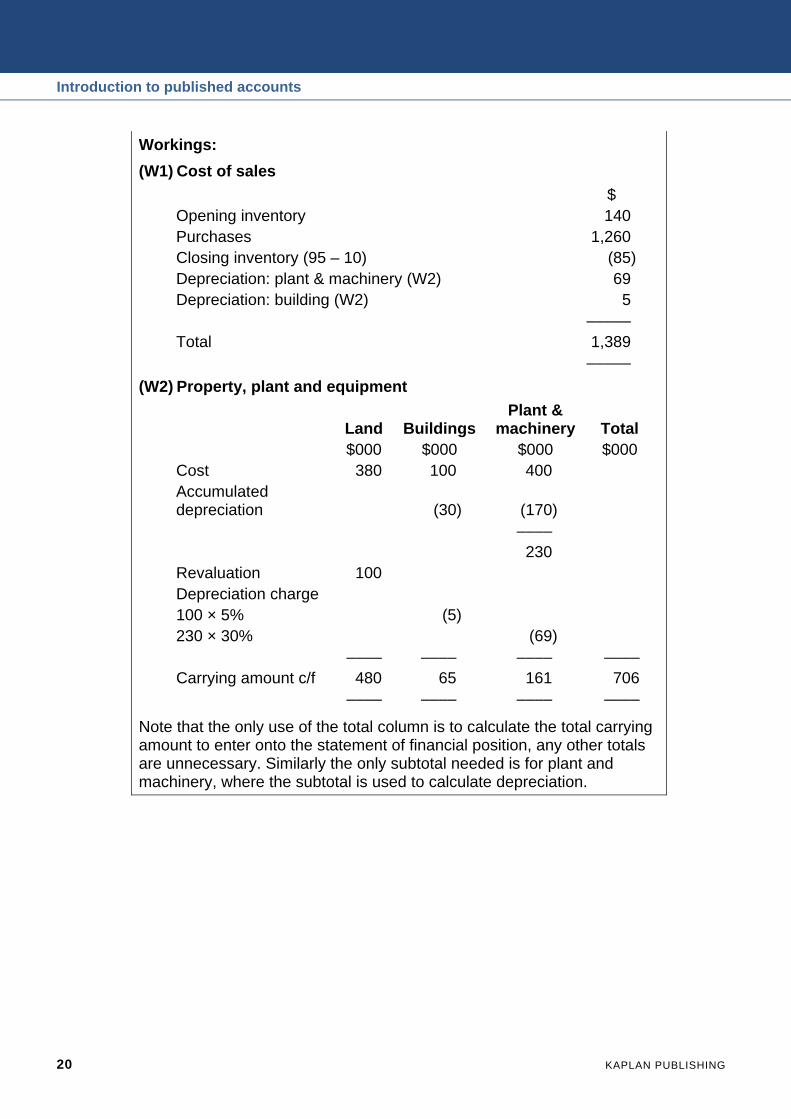

Workings: (W1) Cost of sales

$ Opening inventory 140 Purchases 1,260 Closing inventory (95 – 10) (85) Depreciation: plant & machinery (W2) 69 Depreciation: building (W2) 5 ––––– Total 1,389 –––––

(W2) Property, plant and equipment

Land Buildings Plant &

machinery Total $000 $000 $000 $000 Cost 380 100 400 Accumulated depreciation (30) (170) –––– 230 Revaluation 100 Depreciation charge 100 × 5% (5) 230 × 30% (69) –––– –––– –––– –––– Carrying amount c/f 480 65 161 706 –––– –––– –––– ––––

Note that the only use of the total column is to calculate the total carrying amount to enter onto the statement of financial position, any other totals are unnecessary. Similarly the only subtotal needed is for plant and machinery, where the subtotal is used to calculate depreciation.

Chapter 1

KAPLAN PUBLISHING 21

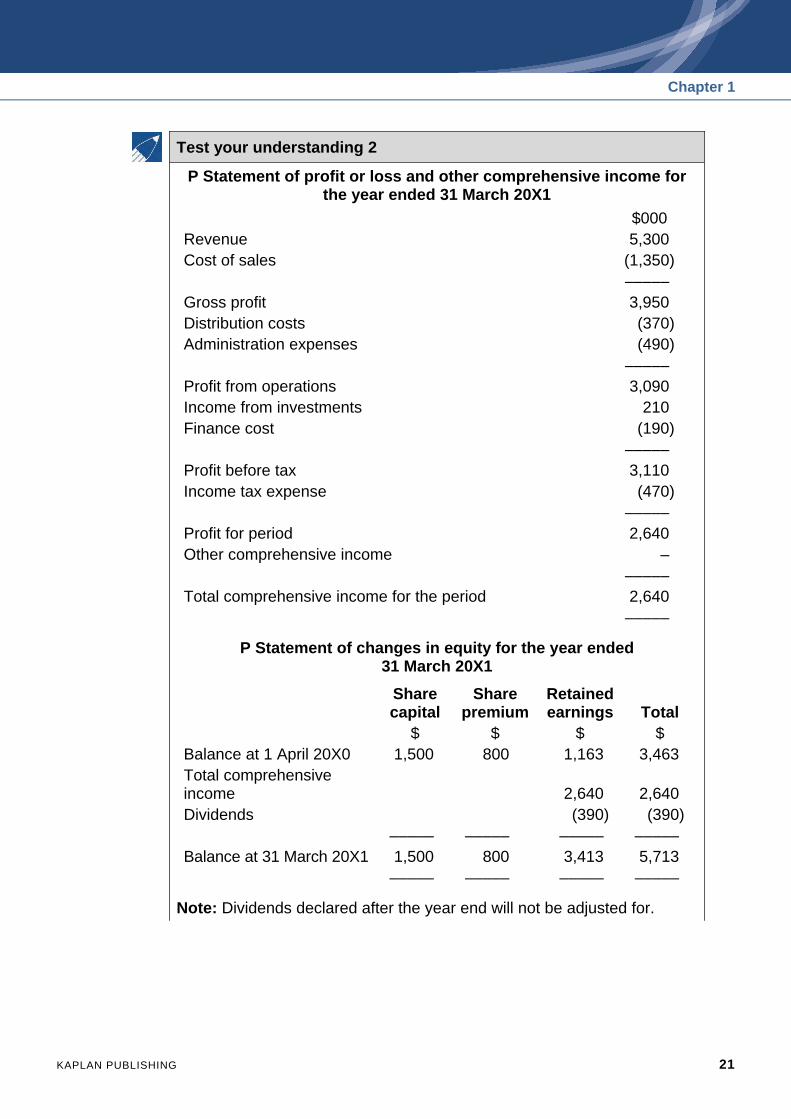

Test your understanding 2

P Statement of profit or loss and other comprehensive income for the year ended 31 March 20X1

$000 Revenue 5,300 Cost of sales (1,350) ––––– Gross profit 3,950 Distribution costs (370) Administration expenses (490) ––––– Profit from operations 3,090 Income from investments 210 Finance cost (190) ––––– Profit before tax 3,110 Income tax expense (470) ––––– Profit for period 2,640 Other comprehensive income – ––––– Total comprehensive income for the period 2,640 –––––

P Statement of changes in equity for the year ended 31 March 20X1

Share capital

Share premium

Retained earnings Total

$ $ $ $ Balance at 1 April 20X0 1,500 800 1,163 3,463 Total comprehensive income 2,640 2,640 Dividends (390) (390) ––––– ––––– ––––– ––––– Balance at 31 March 20X1 1,500 800 3,413 5,713 ––––– ––––– ––––– –––––

Note: Dividends declared after the year end will not be adjusted for.

Introduction to published accounts

22 KAPLAN PUBLISHING

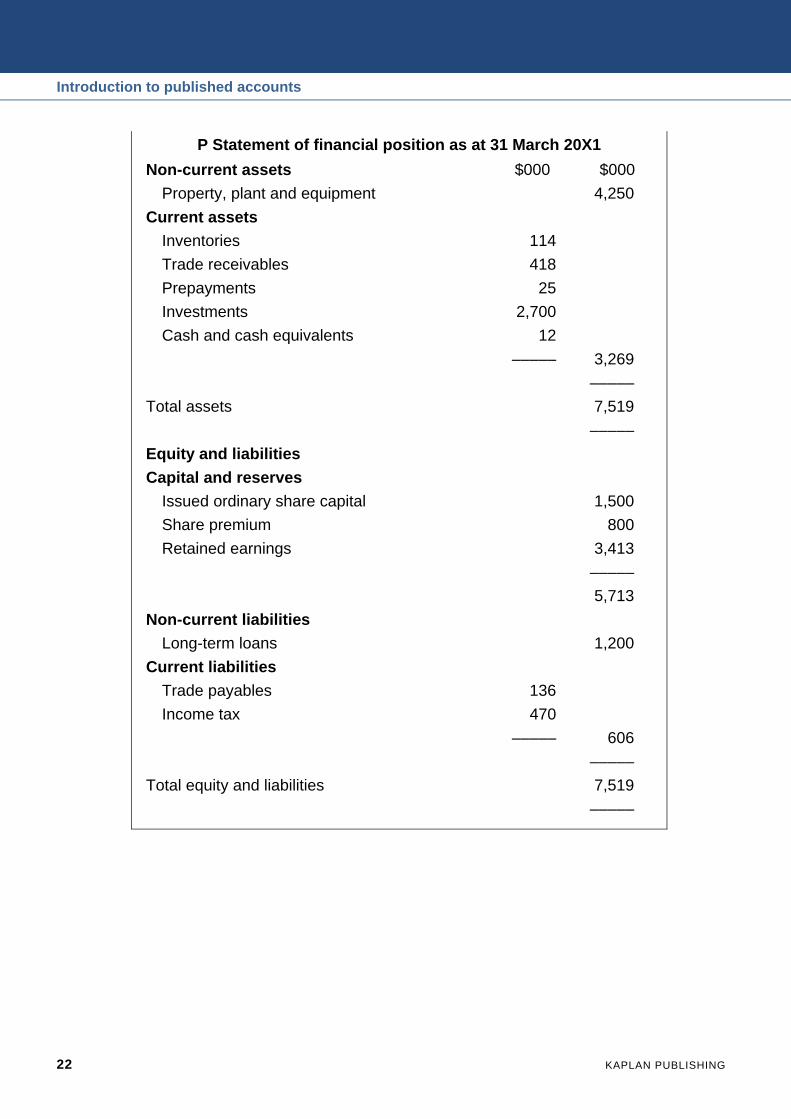

P Statement of financial position as at 31 March 20X1 Non-current assets $000 $000

Property, plant and equipment 4,250

Current assets

Inventories 114

Trade receivables 418

Prepayments 25

Investments 2,700

Cash and cash equivalents 12

––––– 3,269

–––––

Total assets 7,519

–––––

Equity and liabilities

Capital and reserves

Issued ordinary share capital 1,500

Share premium 800

Retained earnings 3,413

–––––

5,713

Non-current liabilities

Long-term loans 1,200

Current liabilities

Trade payables 136

Income tax 470

––––– 606

–––––

Total equity and liabilities 7,519

–––––