a project report on "depository system" in the subject financial services

TRANSCRIPT

A PROJECT REPORT

on

“DEPOSITORY SYSTEM”

in the subject Financial Services

Submitted to University of Mumbai

For IInd semester of M.Com.

BY

HEENA PARVEEN B. SHAIKHRoll No. 49

under the guidance of

Prof. SUNIL GUJARAN

2013 – 2014

A PROJECT REPORT

on

“DEPOSITORY SYSTEM”

in the subject Financial Services

Submitted to University of Mumbai

For IInd semester of M.Com.

BY

HEENA PARVEEN B. SHAIKHRoll No. 49

under the guidance of

Prof. SUNIL GUJARAN

2013 – 2014

C E R T I F I C A T E

This is to certify that the project entitled “DEPOSITORY

SYSTEM” submitted by Miss. Heena Parveen B. Shaikh Roll No.

49 student of M.Com. Banking & Finance (University of

Mumbai) (IInd Semester) examination has not been submitted

for any other examination and does not form a part of any

other course undergone by the candidate. It is further

certified that he has completed all required phases of the

project. This project is original to the best of our

knowledge and has been accepted for Internal Assessment.

Internal Examiner External Examiner

Co-ordinator Principal

College seal

DECLARATION BY THE STUDENT

I, Miss. Heena Parveen B. Shaikh student of M.Com. (Semester

– IInd) Banking & Finance, Roll No. 49 hereby declare that

the project for the Subject Financial Services titled,

“Depository System” submitted by me to University of Mumbai,

examination during the academic year 2013-2014, is based on

actual work carried by me under the guidance and supervision

of Prof. Sunil Gujaran.

I further state that this work is original and not submitted

anywhere else for any examination.

Heena Parveen B. Shaikh

Signature of student

ACKNOWLEDGEMENT

At the beginning, I would like to thank GOD for his shower

of blessing. The desire of completing this project was given

by my guide Prof. Sunil Gujaran. I am very much thankful to

him for the guidance, support and for sparing her / his

precious time from a busy schedule.

I would fail in my duty if I don’t thank my parents who are

pillars of my life. Finally I would express my gratitude to

all those who directly and indirectly helped me in

completing this project.

Heena Parveen B. Shaikh

EXECUTIVE SUMMARY:

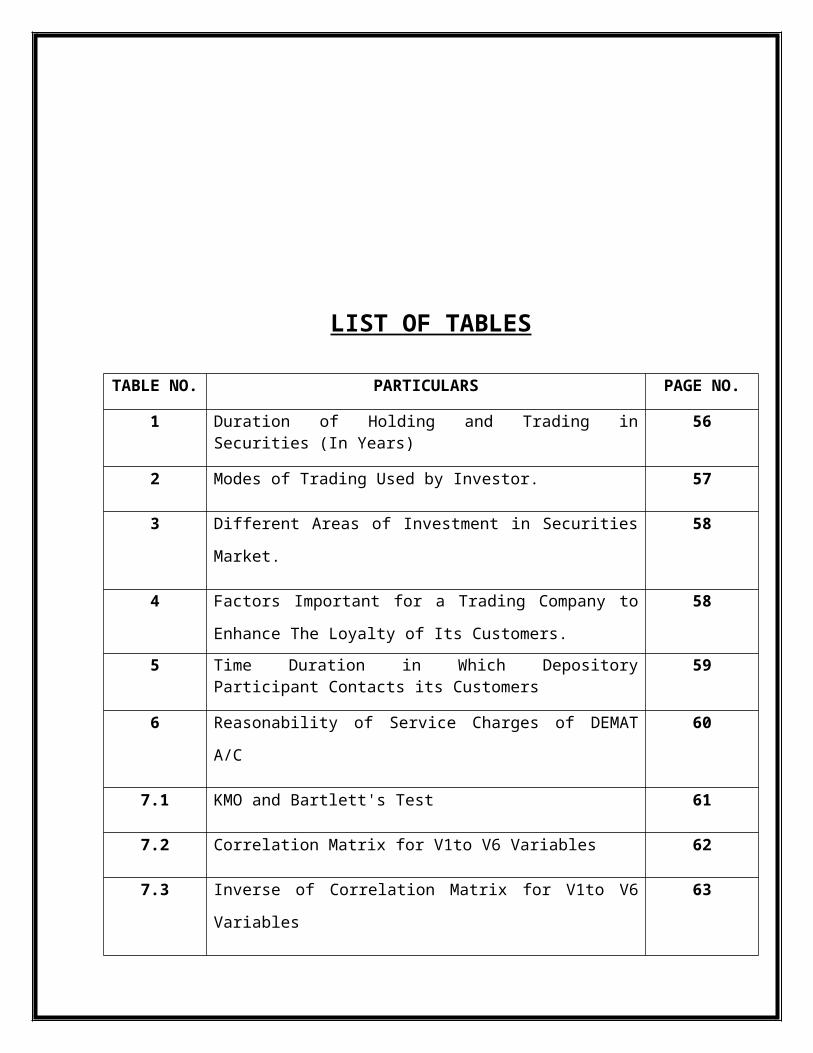

LIST OF TABLES

TABLE NO. PARTICULARS PAGE NO.

1 Duration of Holding and Trading inSecurities (In Years)

56

2 Modes of Trading Used by Investor. 57

3 Different Areas of Investment in Securities

Market.

58

4 Factors Important for a Trading Company to

Enhance The Loyalty of Its Customers.

58

5 Time Duration in Which DepositoryParticipant Contacts its Customers

59

6 Reasonability of Service Charges of DEMAT

A/C

60

7.1 KMO and Bartlett's Test 61

7.2 Correlation Matrix for V1to V6 Variables 62

7.3 Inverse of Correlation Matrix for V1to V6

Variables

63

7.4 Communalities Table 63

7.5 Total Variance Table 63

7.6 Rotated Component Matrix 65

7.7 Factors Influencing Different Functions and

Services that an Investor Should be Aware of

While Trading Through the DEMAT Account

65

8 Personal Details 66

Introduction:Depository system essentially aims at eliminating the

voluminous and cumbersome paper work involved in the scrip-

based system and offers scope for ‘paperless’ trading

through state-of-the-art technology. It is an institution

which maintains an electronic record of ownership or

securities. The storage and handling of certificates is

hence immediately eliminated which generates a reduction in

costs like back office cost for handling, transporting and

storing certificates.

Depositary participant is an institution akin to bank for

securities. When an investor hands over securities to a

depository participant, investor’s account is credited. The

investor’s depository system account will show their

holdings. His account is updated for his transactions of

sale and purchase but without physical movement of scripts

or transfer deeds. In depository system, share certificates

belonging to the investors are dematerialised (demats).

Dematerialisation or “Demat” is a process whereby investors’

securities like shares, debentures etc., are converted into

electronic data and stored in computers by a Depository.

Securities registered in investor’s name are surrendered to

depository participant (DP) and these are sent to the

respective companies who will cancel them after

“Dematerialization” and credit investor’s depository account

with the DP. The securities on Dematerialization appear as

balances in one’s depository account. These balances are

transferable like physical shares. If at a later date,

investors wish to have these “demat” securities converted

back into paper certificates, the Depository does this and

their names are entered in the records of depository as

beneficial owners. The beneficial ownership will be with investor but

legal ownership will be with the depository. Consequently, benefits

like interest, dividend, and rights: bonus and voting rights

will be with investors. Since depository is to get

securities transferred in its name, the depository name will

be registered in the ownership register maintained by the

company. Thus, instead of name of several owners, the name

of depository figures in the register of company.

Since transfer will be affected only in depository, register

of company need not be updated on every transactions of sale

or purchase of company’s share. It alleviates the hardships

currently faced by the investors and it also offers option

for converting the shares from electronic to physical or

paper form through a process of rematerialisation (remat).

Depository system is, indeed, time tested and long prevalent

in many advance countries and has been playing a significant

role in stock markets around the world.

The depository system comprises of:

1) Depository

2) Depository Participants (DPs)

3) Companies/issuer

4) Investors

The first depository was set up way back in 1947 in Germany.

In India it is a relatively new concept introduced in 1996

with the enactment of Depositories Act 1996. Their

operations are carried out in accordance with regulations

made by SEBI, bye-laws and rules of Depositories Act and

SEBI (Depositories and Participants) Regulations Act 1996.

Research Methodology:Although India adopted multi-depository system model to

provide competitive and healthy depository system for

surpass services to Investors. There is a chance to various

entities to enter into Depository system but only two

organizations National Securities Depository Ltd (NSDL) and

Central Depository Services Ltd (CDSL) are providing

depository services presently.

The data has been collected from the following sources:-

1. Primary data

2. Secondary data

Primary data:

In this study the questionnaire method have been used to

collect primary data.

Secondary data:

Secondary data is collected from the website of NSDL

(www.nsdl.co.in) and CDSL (www.cdsl.ac.in), website of

Indian central depository system (CDS), published reports of

NSDL and Govt. of India, Depository Act-1996, SEBI Act-1992,

and Capital Market Services, published books and printed

material on financial services or Intermediaries.

Objectives of the Study:

At Present the Indian stock exchanges are following screen

based trading and electronic settlement system. But

investors scattered at various distant places from trading

and settlement place. So there are some problems arising in

the settlement and transfer system. Thus, there is a need to

evaluate the effectiveness of Indian Depository system.

The Main objectives of the study are:

1) To evaluate the performance of the Depository system in

India with reference to NSDL.

2) To study the Organizational frame work, Operational

policies, Problems and Prospects and financial

performance of NSDL.

3) To present legislative measures of dematerialization

and to understand the present status of

dematerialization in India.

4) To analyze services rendered and quality among the DPs

and opinions of investors with regard to the

functioning of NSDL.

5) To identify the Investors expectations from the DP

companies and to exhibit the Investor’s perceptions on

the services offered by the DP companies .

6) To make appropriate and relevant recommendations to the

management of the organization under study.

Constituents of Depository System:1. Depository:

Depository functions like a securities bank, where the

dematerialized physical securities are traded and held in

custody. This facilitates faster risk free and low cost

settlement. Depository is much like a bank and performs many

activities that are similar to a bank depository:

Enables surrender and withdrawal of securities to and

from the depository through the process of ‘demat’ and

‘remat’,

maintains investors’ holdings in electronic form,

Effects settlement of securities traded in depository

mode on the stock exchanges,

carries out settlement of trades not done on the stock

exchanges (off market trades).

In India a depository has to be promoted as a corporate body

under Companies Act, 1956. It is also to be registered as a

depository with SEBI. It starts operations after obtaining a

certificate of commencement of business from SEBI. It has to

develop automatic data processing systems to protect against

unauthorised access. A network to link up with depository

participants, issuers and issuer’s agent has to be created.

Depository, operating in India, shall have a net worth of

rupees one hundred crore and instruments for which

depository mode is open need not be a security as defined in

the Securities Contract (Regulations) Act 1956. The

depository, holding securities, shall maintain ownership

records in the name of each participant. Despite the fact

that legal ownership is with depository, it does not have

any voting right against the securities held by it. Rights

are intact with investors.

There are two depositories in India at present i.e.

1. NSDL: National Securities Depository limited

2. CDSL: Central Depository Services (India) Limited

ii) Depository Participants (DP):

A DP is investors’ representative in the depository system

and as per the SEBI guidelines, financial

institutions/banks/custodians/stock brokers etc. can become

DPs provided they meet the necessary requirements prescribed

by SEBI. DP is also an agent of depository which functions

as a link between the depository and the beneficial owner of

the securities. DP has to get itself registered as such

under the SEBI Act. The relationship between the depository

and the DP will be of a principal and agent and their

relation will be governed by the bye-laws of the depository

and the agreement between them. Application for registration

as DP is to be submitted to a depository with which it wants

to be associated. The registration granted is valid for five

years and can be renewed. As depository holding the

securities shall maintain ownership records in the name of

each DP, DP in return as an agent of depository, shall

maintain ownership records of every beneficial owner

(investor) in book entry form.

A DP is the first point of contact with the investor and

serves as a link between the investor and the company

through depository in dematerialisation of shares and other

electronic transactions. A company is not allowed to

entertain a demat request from investors directly and

investors have to necessarily initiate the process through a

DP.

Eligibility criteria for depository participants:

The following entities are eligible for becoming depository

participant in accordance with

Regulation 19 of the SEBI (Depositories and Participants)

Regulations, 1996.

A public financial institution as defined in Section 4A

of the Companies Act, 1056.

A bank included in the second schedule of the Reserve

Bank of India Act, 1934.

A foreign bank, operating in India with the approval of

Reserve Bank of India.

A state financial corporation established under the

provisions of section 3 of the State Financial

Corporations Act, 1951.

An institution engaged in providing financial services,

promoted by any of the four institutions mentioned

above.

A custodian of securities, who has been granted a

certificate of registration by SEBI under Section

12(1A) of the SEBI Act, 1992.

A clearing corporation or a clearing house of a stock

exchange.

A stockbroker having a minimum net worth of rupees TWO

CRORES. The aggregate value of the portfolio of

securities, of the BOs, held in dematerialized form in

a depository through him, shall not exceed 100 times of

the net worth of the stockbroker. (Not applicable for

DPs whose net worth is Rs. ten crores). In case the

stockbroker seeks to act as a participant in more than

one depository, he shall comply with the net worth

criteria separately with each such depository.

A non-banking finance company, having a net worth of

not less than rupees fifty lakhs provided that such

company shall act as a participant only on behalf of

itself and not on behalf of any other person. Provided

further that a non-banking finance company may act as a

participant on behalf of any other entity, if it has a

net worth of Rs. fifty crores in addition to the net

worth specified by any other authority.

A registrar to an issue or share transfer agent who has

a minimum net worth of

Rupees ten crores and who has been granted a

certificate of registration by SEBI.

Characteristics of depository participant:

Acts as an Agent of Depository

Directly deal with customer

Functions like Securities Bank

Account opening

Facilitates dematerialization

Instant transfer on pay – out

Credits to investor in IPO, rights, bonus

Settles trades in electronic segment

iii) ISSUER / Companies:

The issuer is the co. which issues the securities. It

maintains a register for recording the names of the

registered owners of securities and the depositories. The

issuer sends a list of shareholders who opt for the

depository system. And only that co.’s can issue the

securities which are registered under stock exchanges

iv) BENEFICIAL OWNER/ INVESTOR:

Beneficial owner is a person whose name is recorded as such

with a depository. It means a person who is engaged in

buying and selling of securities issued by the companies and

is registered his/ her securities with the depository in the

form of book entry. And he/ she has all the rights and

liabilities associated with the securities

Facilities offered by depository system:

1) Dematerialization: It is a process of conversion of

physical share – certificate into electronic – form.

So, when a shareholder uses the dematerialization

facility, company take back the shares, through

depository – system and equal numbers of shares are

credited in his account in e-form.

2) Rematerialization: Rematerialization is the exact

reverse of Dematerialization. It refers to the process

of issuing physical securities in place of the

securities held electronically in book-entry form with

a depository.

Other Services:

a) Pledging Dematerialized Shares: Dematerialized shares

could be pledged; in fact, this is more advantageous as

compared to pledging share certificates. After loan is

repaid one can request for a closure of pledge by

instructing one’s DP through a standard format. The

pledgee on receiving the repayment as well as the

request for closure of pledge will instruct his DP

accordingly. Even the locked-in securities can be

pledged. The pledger continues to remain the

beneficiary holder of those securities even after the

securities are pledged.

b) Initial Public Offerings: Credits for public offers can

be directly received into demat account. In the public

issue application form of depository eligible

companies, there will be a provision to indicate the

manner in which securities should be allotted to the

applicant. One is to mention one’s client account

number and the name and identification number of DP.

All allotment due to investor will be credited into

required account.

c) Receipt of Cash/non-cash Benefits: When any corporate

event such as rights or bonus or dividend is announced

for a particular security, depository will give the

details of all the clients having electronic holdings

in that security as of the record date to the

registrar. The registrar will then calculate the

corporate benefits due to all the shareholders. The

disbursement of cash benefits such as dividend/

interest will be done directly by the registrar. In

case of non-cash benefits, depository will directly

credit the securities entitlements in the depository

accounts of all those clients who have opted for

electronic allotment based on the information provided

by the registrar.

d) Stock Lending and Borrowing: Through the depository

account securities in the demat form can be easily

lent/ borrowed. Securities can be lent or borrowed in

electronic form through an approved intermediary, who

has opened a special ‘intermediary’ account with a DP.

Instructions are to be given to DP through a standard

format (which is available with DP) to deposit

securities with the intermediary. Similarly to borrow

securities from the intermediary, one has to instruct

DP through a standard format (which is available with

your DP).

e) Transmission of Securities: Transmission of securities

due to death, lunacy, bankruptcy, insolvency or by any

other lawful means other than transfer is also possible

in the depository system. In the case of transmission,

the claimant will have to fill in a transmission

request form, (which is available with the DP)

supported by valid documents.

f) Freezing Account with DP: If at any time as a security

measure one wishes that no transaction should be

effected in one’s account, one may advise one’s DP

accordingly. DP will ensure that account of such

investor is totally frozen until further instructions

from him.

Benefits of Depository System:

1) This system will eliminate paper work as the book entry

system does not need physical movement of certificates

for transfer process.

2) The risk of bad deliveries, fraud and misplaced,

mutilated and lost share certificates will not exist.

3) The electronic media will shorten settlement time and

hence the investor can save time and increase the

velocity of security movement.

4) Investors will be able to change portfolio more

frequently.

5) The capital market will be more transparent as the

trading, clearing and settlement mechanism have to be

highly automated and interlinked with the depository

among them.

6) The market will be highly automated and efficient due

to the usage of computing and telecommunication

technology for the back office activities for all the

capital market players.

DEMATERIALISATION PROCESS:

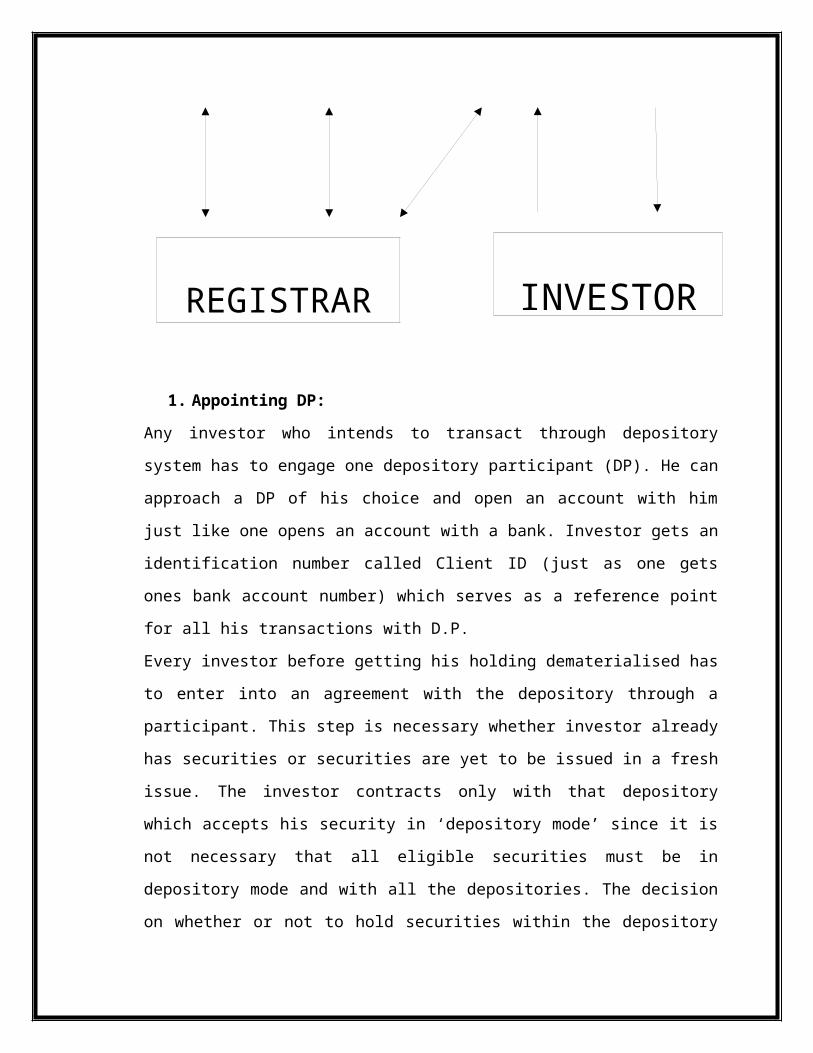

DepositoryparticipantNSDL

1. Appointing DP:

Any investor who intends to transact through depository

system has to engage one depository participant (DP). He can

approach a DP of his choice and open an account with him

just like one opens an account with a bank. Investor gets an

identification number called Client ID (just as one gets

ones bank account number) which serves as a reference point

for all his transactions with D.P.

Every investor before getting his holding dematerialised has

to enter into an agreement with the depository through a

participant. This step is necessary whether investor already

has securities or securities are yet to be issued in a fresh

issue. The investor contracts only with that depository

which accepts his security in ‘depository mode’ since it is

not necessary that all eligible securities must be in

depository mode and with all the depositories. The decision

on whether or not to hold securities within the depository

REGISTRAR INVESTOR

mode and if in depository mode, with which depository or

participants, would be entirely with the investor.

2. Request for ‘Demat’:

After any agreement is entered for getting securities

dematerialised and his account is opened, the investor makes

an application to depository participants in form called

‘Dematerialisation Request Form’ (DRF) to be provided by the

DP and hands over his share certificates duly cancelled by

writing’ surrendered for dematerialisation’ to them for

demat. The DP will accept certificates registered only in

investor’s name.

The request for dematerialisation with the depository

participants is sent to the depository through depository

network with which DP is connected.

Simultaneously DP submits the securities certificates to the

issuer company or it’s Registrar of transfer.

3. Approach the Company or Registrar of Transfer

The depository will electronically intimate the issuer or

its ‘Registrar and transfer agent’ of the dematerialisation

request. The issuer or the ‘Registrar and transfer

Agent’ has to verify the validity of the security

certificates as well as the fact that the DRF has been made

by the person recorded as a member in its Register of

Members. If the issuer or its Registrar is satisfied, it

dematerialises the scrip and updates its record.

4. Confirmation of Demat

The Registrar to transfer or the concerned company when

satisfied with the case of demat has to inform the

depository of the completion of dematerialisation

authorising an electronic credit for that security in favour

of the investor.

5. Crediting the Client’s Account

DP credits investor’s account with the number of shares so

dematerialised and thereafter investor hold the securities

in electronic form. If there is rejection of demat request

then such credit is not given. After crediting the account,

the client is sending the necessary information in form of a

statement like we get bank statement after bank

transactions.

Demat Account:Demat account is a safe and convenient means of holding

securities just like a bank account is for funds. Today,

practically 99.9% settlement (of shares) takes place on

demat mode only. Thus, it is advisable to have a Beneficiary

Owner (BO) account to trade at the exchanges.

Benefits Of Demat Account:

A safe and convenient way of holding securities (equity

and debt instruments both).

Transactions involving physical securities are costlier

than those involving dematerialised securities (just

like the transactions through a bank teller are

costlier than ATM transactions). Therefore, charges

applicable to an investor are lesser for each

transaction.

Securities can be transferred at an instruction

immediately.

Increased liquidity, as securities can be sold at any

time during the trading hours (between 9:55 AM to 3:30

PM on all working days), and payment can be received in

a very short period of time.

No stamp duty charges.

Risks like forgery, thefts, bad delivery, delays in

transfer etc., associated with physical certificates,

are eliminated.

Pledging of securities in a short period of time.

Reduced paper work and transaction cost.

Odd-lot shares can also be traded (can be even 1

share).

Nomination facility available.

Any change in address or bank account details can be

electronically intimated to all companies in which

investor holds any securities, without having to inform

each of them separately.

Securities are transferred by the DP itself, so no need

to correspond with the companies.

Shares arising out of bonus, split, consolidation,

merger etc. are automatically credited into the demat

account of the investor.

Shares allotted in public issues are directly credited

into demat account of the applicants in quick time.

Opening a Demat Account:

To start dealing in securities in electronic form, one needs

to open a demat account with a DP of his choice. An investor

already having shares in physical form should ensure that he

gets the account opened in the same set of names as

appearing on the share certificate; otherwise a new account

can be opened in any desired pattern by the investor.

Opening a Demat Account

Getting started

1. Choose a DP

2. Fill up an account

opening form provided by

DP, and sign an

Documents to be attached

1. Passport size

photographs

2. Proof of residence (POR)

- Any one of Photo

agreement with DP in a

standard format

prescribed by the

depository.

3. DP provides the investor

with a copy of the

agreement and schedule

of charges for his

future reference.

4. DP opens the account and

provides the investor

with a unique account

number, also known as

Beneficiary Owner

Identification Number

(BO ID).

Ration Card with DOB /

Photo Driving License

with DOB / Passport copy

/ Electricity bill /

Telephone bill

3. Proof of identity (POI)

- Any one of Passport

copy / Photo Driving

License with DOB /

Voters ID Card / PAN

Card / Photo Ration Card

with DOB

4. PAN card

Note:

The agreement required to be signed by the investor

details the rights and duties of the investor and DP.

DP may revise the charges by giving a 30 days prior

notice. SEBI has rationalized the cost structure for

isation by removing account opening charges,

transaction charges for credit of securities and

custody charges, effective from January 28, 2005.

Re materialisation process:

Rematerialisation is a process of converting electronic

holdings of investor back into share certificates in

paper form. The process of rematerialisation is also

carried out through DP and the process has to be

completed within a period of 30 days. Thus, once security

is dematerialised it is not necessary that investor is to

continue in depository mode for all times to come. He can

switch over to remat whereby he gets back physical

possession of security scripts. The client of DP has to

submit a request for remat. This request is forwarded for

necessary action to depository. The depository confirms

the rematerialisation request to the Registrar and

Transfer Agents. The Registrar updates the accounts and

prints the desired certificate. The depository is

informed by Registrar and certificate is sent to the

investor. The depository updates its records and

communicates to DP to incorporate necessary changes in

the account of the client.

National Securities Depository Limited:In a span of about nine years, investors have switched over

to electronic [demat] settlement and National Securities

Depository Limited (NSDL) stands at the centre of this

change. In order to provide quality service to the users of

depository, NSDL launched a certification programme in

depository operations in May 1999. This certification is

conducted using NCFM infrastructure created by NSE and is

called "NSDL - Depository Operations Module". The programme

is aimed at certifying whether an individual has adequate

knowledge of depository operations, to be able to service

investors. Depository Participants are required to appoint

at least one person who has qualified in the certification

programme at each of their service centres. This handbook is

meant to help the candidates in their preparation for the

certification programme.

National Securities Depository Limited is the first

depository to be set-up in India. It was incorporated on

December 12, 1995. The Industrial Development Bank of India

(IDBI) - the largest development bank in India, Unit Trust

of India (UTI) - the largest Indian mutual fund and the

National Stock Exchange (NSE) - the largest stock exchange

in India, sponsored the setting up of NSDL and subscribed to

the initial capital. NSDL commenced operations on November

8, 1996.

Ownership

NSDL is a public limited company incorporated under the

Companies Act, 1956. NSDL had a paidup equity capital of Rs.

105 crore. The paid up capital has been reduced to Rs. 80

crore since NSDL has bought back its shares of the face

value of Rs. 25 crore in the year 2000. However, its net

worth is above the Rs. 100 crore, as required by SEBI

regulations.

The following organisations are shareholders of NSDL as on

March 31, 2005.

1. Industrial Development Bank of India

2. Administrator of the Specified Undertaking of the Unit

Trust of India - DRF

3. National Stock Exchange

4. State Bank of India

5. Oriental Bank of Commerce

6. Citibank N.A.

7. Standard Chartered Bank

8. HDFC Bank Limited

9. The Hongkong and Shanghai Banking Corporation Limited

10. Deutsche Bank A.G.

11. Dena Bank

12. Canara Bank

Management of NSDL:

NSDL is a public limited company managed by a professional

Board of Directors. The day-today operations are conducted

by the Chairman & Managing Director (CMD). To assist the CMD

in his functions, the Board appoints an Executive Committee

(EC) of not more than 15 members. The eligibility criteria

and period of nomination, etc. are governed by the Bye-Laws

of NSDL in this regard.

Bye-Laws of NSDL:

Bye-Laws of National Securities Depository Limited have been

framed under powers conferred under section 26 of the

Depositories Act, 1996 and approved by Securities and

Exchange Board of India. The Bye-Laws contain fourteen

chapters and pertain to the areas listed below:

1. Short title and commencement

2. Definitions

3. Board of Directors

4. Executive Committee

5. Business Rules

6. Participants

7. Safeguards to protect interest of clients and

participants.

8. Securities

9. Accounts/transactions by book entry

10. Reconciliation, accounts and audit

11. Disciplinary action

12. Appeals

13. Conciliation

ArbitrationAmendments to NSDL Bye-Laws require the approval

of the Board of Directors of NSDL and SEBI.

Business Rules of NSDL

Amendments to NSDL Business Rules require the approval of

NSDL Executive Committee andfiling of the same with SEBI at

least a day before the effective date for the amendments.

Functions:

NSDL performs the following functions through

depository participants:

Enables the surrender and withdrawal of securities to

and from the depository (dematerialisation and

rematerialisation).

Maintains investor holdings in the electronic form.

Effects settlement of securities traded on the

exchanges.

Carries out settlement of trades not done on the stock

exchange (off-market trades).

Transfer of securities.

Pledging/hypothecation of dematerialised securities.

Electronic credit in public offerings of companies or

corporate actions.

Receipt of non-cash corporate benefits like bonus

rights, etc. in electronic form.

Stock Lending and Borrowing.

Services Offered by NSDL:

NSDL offers a host of services to the investors through its

network of DPs:

Maintenance of beneficiary holdings through DPs

Dematerialisation

Off-market Trades

Settlement in dematerialised securities

Receipt of allotment in the dematerialised form

Distribution of corporate benefits

Rematerialisation

Pledging and hypothecation facilities

Freezing/locking of investor's account

Stock lending and borrowing facilities

Fee Structure of NSDL

NSDL charges the DPs and not the investors directly. These

charges are fixed. The DPs in turn, are free to charge their

clients, i.e., the investors for their services. Thus, there

is a two tier fee structure.

Inspection, Accounting and Internal Audit

NSDL obtains audited financial reports from all its DPs once

every year. NSDL also carries out periodic visits to the

offices of its constituents - R&T agents, DPs and clearing

corporations – to review the operating procedures, systems

maintenance and compliance with the Bye-Laws, Business Rules

and SEBI Regulations.

Additionally, DPs are required to submit to NSDL, internal

audit reports every quarter. Internal audit has to be

conducted by a chartered accountant or a company secretary

in practice.

The Board of Directors appoints a Disciplinary Action

Committee (DAC) to deal with any matter relating to DPs

clients, Issuers and R&T agents. The DAC is empowered to

suspend or expel a DP, declare a security as ineligible on

the NSDL system, freeze a DP account and conduct inspection

or call for records and issue notices.

If a DP is aggrieved by the action of the DAC, it has the

right to appeal to the EC against the action of the DAC.

This has to be done within 30 days of the action by DAC. The

EC has to hear the appeal within two months from the date of

filing the appeal. The EC has the power to stay the

operation of the orders passed by the DAC. The information

on all such actions has to be furnished to SEBI.

Settlement of Disputes:

All disputes, differences and claims arising out of any

dealings on the NSDL, irrespective of whether NSDL is a

party to it or not, have to be settled under the Arbitration

and Conciliation Act 1996.

Technology and Connectivity in NSDL

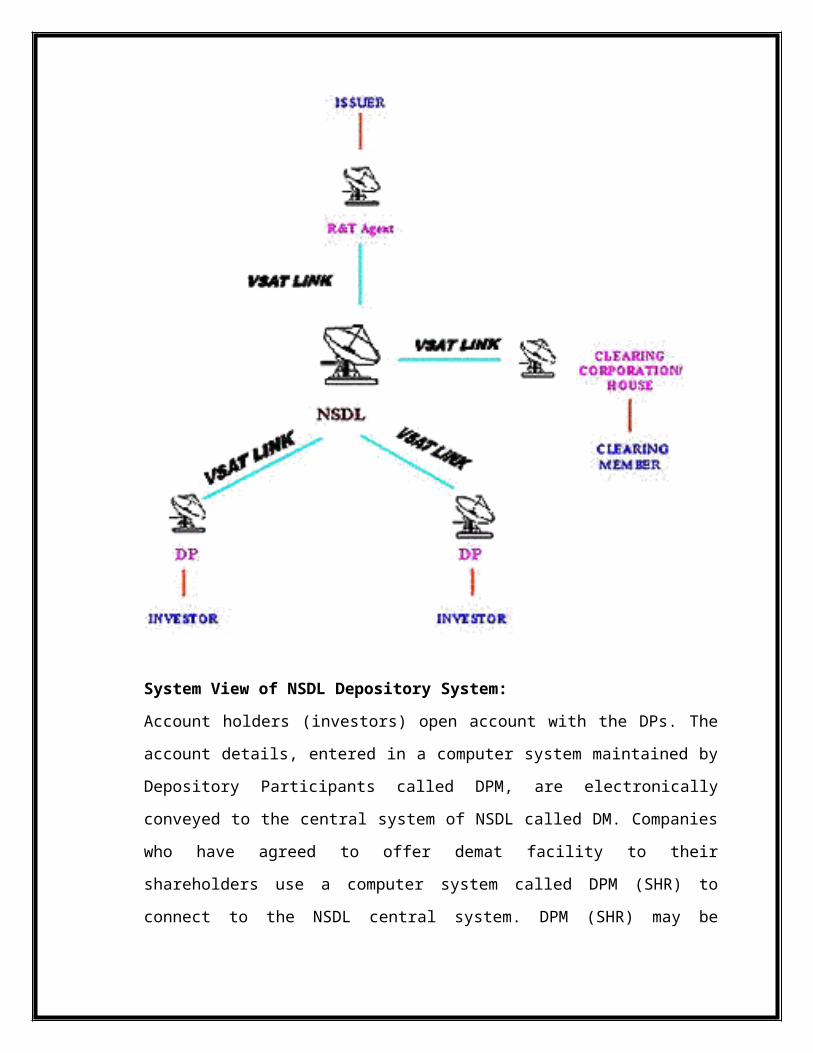

System View of NSDL Depository System:

Account holders (investors) open account with the DPs. The

account details, entered in a computer system maintained by

Depository Participants called DPM, are electronically

conveyed to the central system of NSDL called DM. Companies

who have agreed to offer demat facility to their

shareholders use a computer system called DPM (SHR) to

connect to the NSDL central system. DPM (SHR) may be

installed by the company itself or through its R&T Agent.

This system is used to electronically receive demat

requests, confirm such requests or to receive beneficial

owner data (Benpos) from the depository. Stock exchanges

receive pay-in (receiving securities against sales made by

brokers) or to payout (giving securities to brokers against

their purchases) using a computer system connected to NSDL

called DPM (CC).

All the computer systems installed by DPs (DPM-DP),

companies (DPM-SHRs), and stock exchanges (DPM-CC) are

connected to NSDL central system (DM) through V-SAT (very

small aperture terminal) or leased lines. These are

collectively called Business Partner Systems. Any

transaction conducted by any computer system in the NSDL

depository system which is targetted to reach any other

computer system first gets recorded in DM and then will

reach the target. No two business partners' systems can

communicate to each other without passing through the DM.

Maintenance of Accounts at the Central System:

The NSDL central system known as DM maintains accounts of

all account holders in the depository system. All the

transactions entered at any point in the computer system

connected to it are first effected in the central system and

subsequently at these computers. Thus, the central system of

NSDL has the records of all details of every transaction

conducted in the depository system.

Distributed Database:

Each of the computer systems connected to NSDL system has

its own database relating to its clients. This helps in

giving prompt and accurate service to the clients. However

each of the databases is reconciled with the data at the

central system everyday in order to ensure that the data in

the distributed database tallies with the central database.

Common Software:

NSDL develops software required by depository participants,

companies, R&T Agents and clearing corporations for

conducting depository operations. Thus, the computer systems

used by all the entities will have common software given by

NSDL. However, depending on the business potential, branch

networks and any other specific features, DPs may develop

software of their own for co-ordination, communication and

control and provide service to their clients. Such exclusive

software is called "back office software". DPM system given

by NSDL gives "export and import" facility to take out the

transaction details to be used by back office software and

to feed in transaction details generated from the back

office software.

Connectivity:

The computer system used by DPs, companies, R&T Agents and

stock exchanges may be connected to NSDL central system

through V-SAT network or leased line network. NSDL uses

NSE's V-SAT network for the connectivity purposes. Thus, V-

SATs used by NSE brokers can connect to NSDL if the software

supplied by NSDL is used. V-SAT uses satellites for

communication purposes. Some business partners may connect

using leased lines provided by MTNL/ BSNL. V-SAT or leased

line connections are called primary connectivity. If primary

connectivity fails for any reason, BPs must have the ability

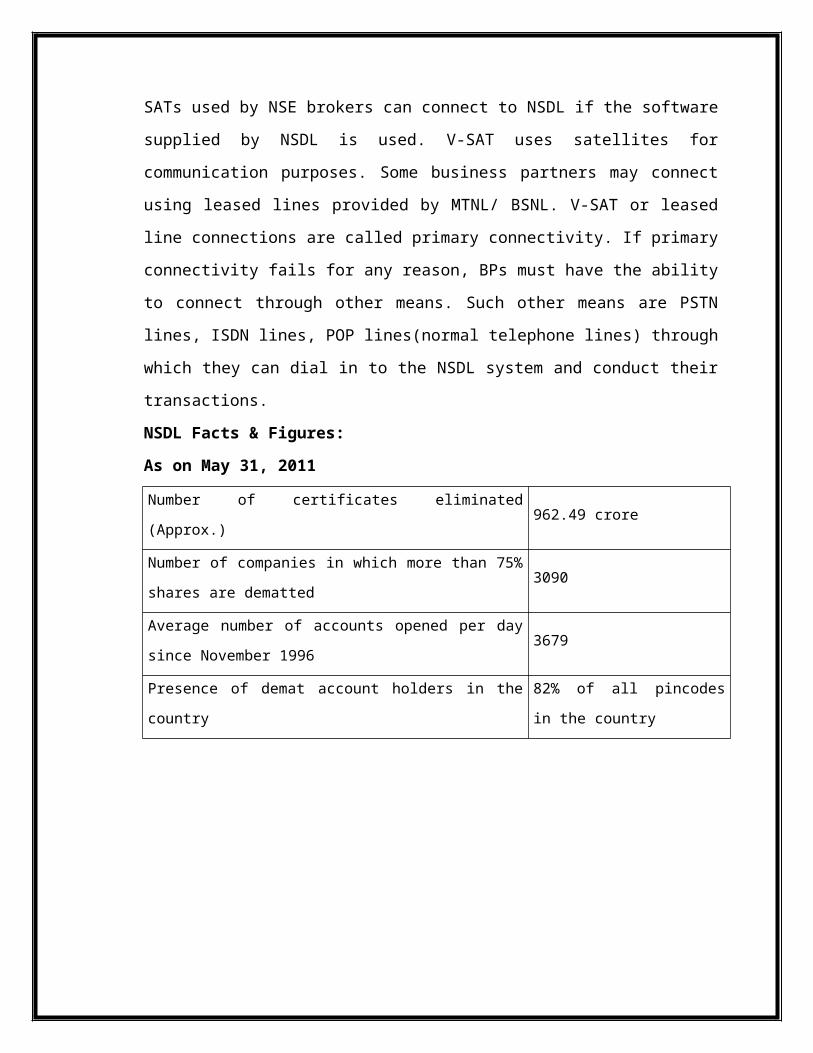

to connect through other means. Such other means are PSTN

lines, ISDN lines, POP lines(normal telephone lines) through

which they can dial in to the NSDL system and conduct their

transactions.

NSDL Facts & Figures:

As on May 31, 2011

Number of certificates eliminated

(Approx.)962.49 crore

Number of companies in which more than 75%

shares are dematted3090

Average number of accounts opened per day

since November 19963679

Presence of demat account holders in the

country

82% of all pincodes

in the country

Central Depositary Securities Limited:A Depository facilitates holding of securities in the

electronic form and enables securities transactions to be

processed by book entry by a Depository Participant (DP),

who as an agent of the depository, offers depository

services to investors. According to SEBI guidelines,

financial institutions, banks, custodians, stockbrokers,

etc. are eligible to act as DPs. The investor who is known

as beneficial owner (BO) has to open a demat account through

any DP for dematerialisation of his holdings and

transferring securities.

The balances in the investors account recorded and

maintained with CDSL can be obtained through the DP. The DP

is required to provide the investor, at regular intervals, a

statement of account which gives the details of the

securities holdings and transactions. The depository system

has effectively eliminated paper-based certificates which

were prone to be fake, forged, counterfeit resulting in bad

deliveries. CDSL offers an efficient and instantaneous

transfer of securities.

CDSL was promoted by Bombay Stock Exchange Limited (BSE)

jointly with leading banks such as State Bank of India, Bank

of India, Bank of Baroda, HDFC Bank, Standard Chartered

Bank, Union Bank of India and Centurion Bank.

CDSL was set up with the objective of providing convenient,

dependable and secure depository services at affordable cost

to all market participants. Some of the important milestones

of CDSL system are:

CDSL received the certificate of commencement of business

from SEBI in February, 1999

Honourable Union Finance Minister, Shri Yashwant Sinha

flagged off the operations of CDSL on july 15,1999.

Settlement of trades in the demat mode through BOI

Shareholding Limited, the clearing house of BSE,

started in july 1999.

All leading stock exchanges like the National Stock

Exchange, Calcutta Stock Exchange, Delhi stock

Exchange, The Stock Exchange, Ahmedabad, etc have

established connectivity with CDSL.

As at the end of Dec 2007, over 5000 issuers have

admitted their securities (equities, bonds, debentures,

commercial papers), units of mutual funds, certificate

of deposits etc. into the CDSL system.

Shareholders of CDSL:

CDSL was promoted by Bombay Stock Exchange Limited (BSE) in

association with Bank of India, Bank of Baroda, State Bank

of India and HDFC Bank. BSE has been involved with this

venture right from the inception and has contributed

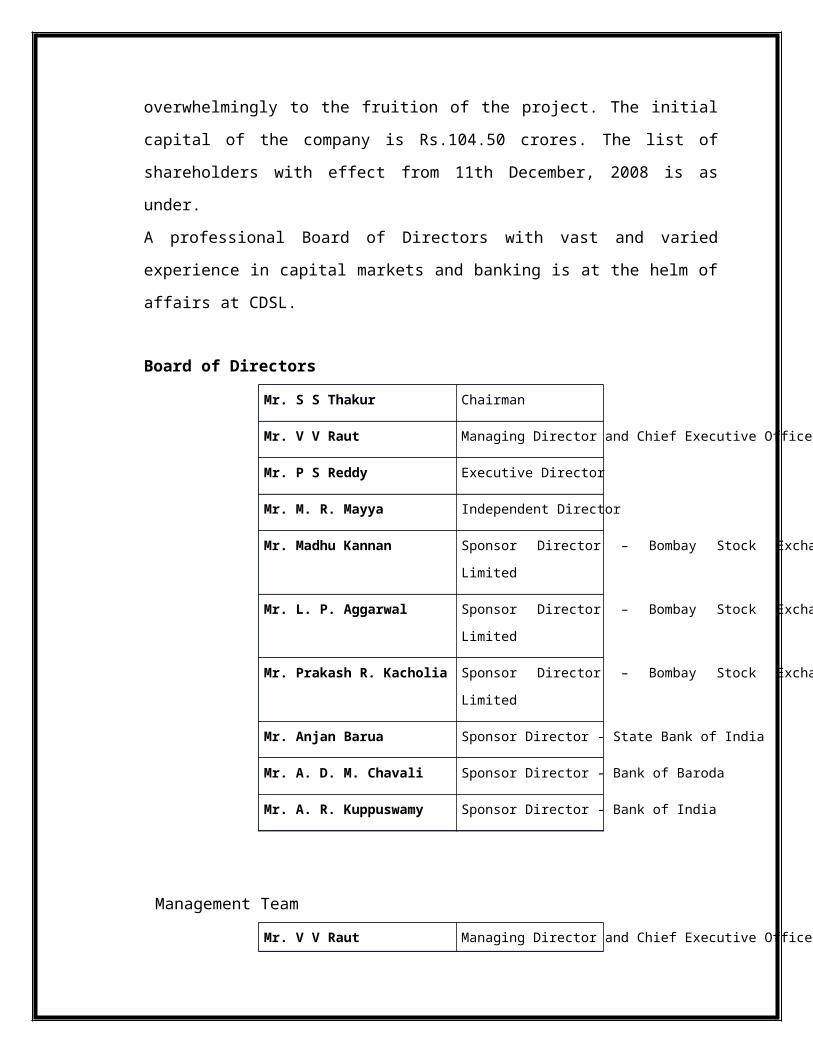

overwhelmingly to the fruition of the project. The initial

capital of the company is Rs.104.50 crores. The list of

shareholders with effect from 11th December, 2008 is as

under.

A professional Board of Directors with vast and varied

experience in capital markets and banking is at the helm of

affairs at CDSL.

Board of Directors

Mr. S S Thakur Chairman

Mr. V V Raut Managing Director and Chief Executive Officer

Mr. P S Reddy Executive Director

Mr. M. R. Mayya Independent Director

Mr. Madhu Kannan Sponsor Director – Bombay Stock Exchange

Limited

Mr. L. P. Aggarwal Sponsor Director – Bombay Stock Exchange

Limited

Mr. Prakash R. Kacholia Sponsor Director – Bombay Stock Exchange

Limited

Mr. Anjan Barua Sponsor Director - State Bank of India

Mr. A. D. M. Chavali Sponsor Director - Bank of Baroda

Mr. A. R. Kuppuswamy Sponsor Director - Bank of India

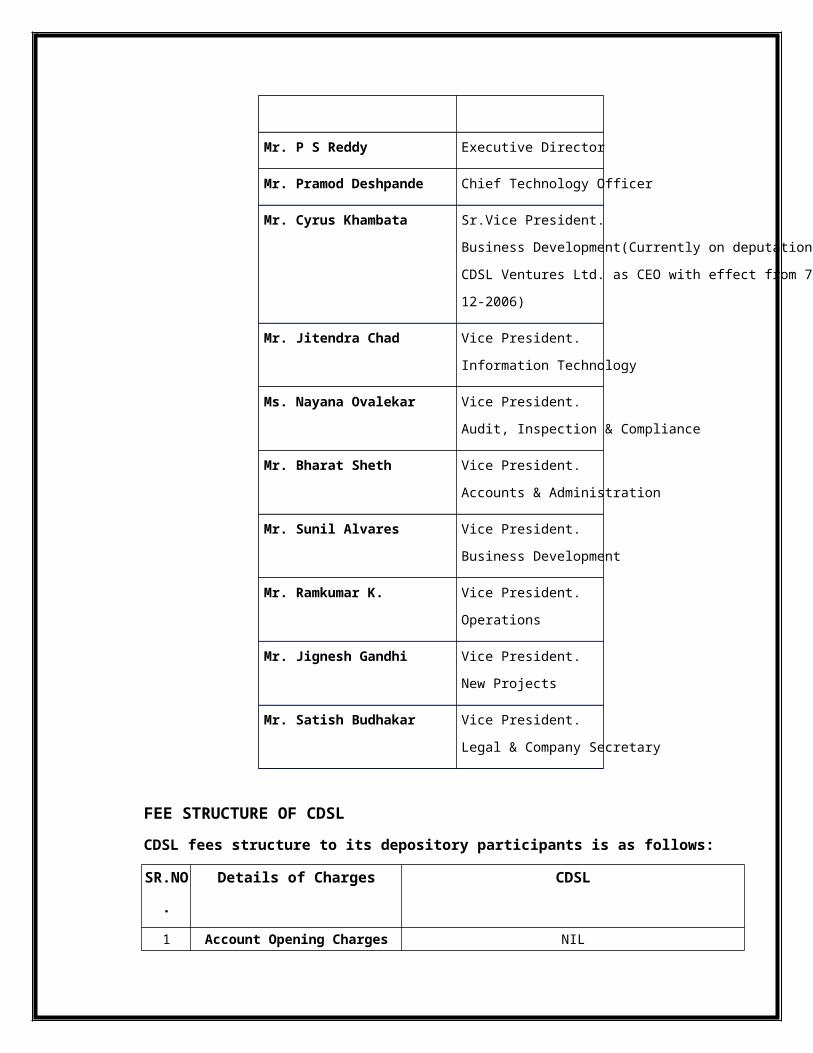

Management Team

Mr. V V Raut Managing Director and Chief Executive Officer

Mr. P S Reddy Executive Director

Mr. Pramod Deshpande Chief Technology Officer

Mr. Cyrus Khambata Sr.Vice President.

Business Development(Currently on deputation to

CDSL Ventures Ltd. as CEO with effect from 7-

12-2006)

Mr. Jitendra Chad Vice President.

Information Technology

Ms. Nayana Ovalekar Vice President.

Audit, Inspection & Compliance

Mr. Bharat Sheth Vice President.

Accounts & Administration

Mr. Sunil Alvares Vice President.

Business Development

Mr. Ramkumar K. Vice President.

Operations

Mr. Jignesh Gandhi Vice President.

New Projects

Mr. Satish Budhakar Vice President.

Legal & Company Secretary

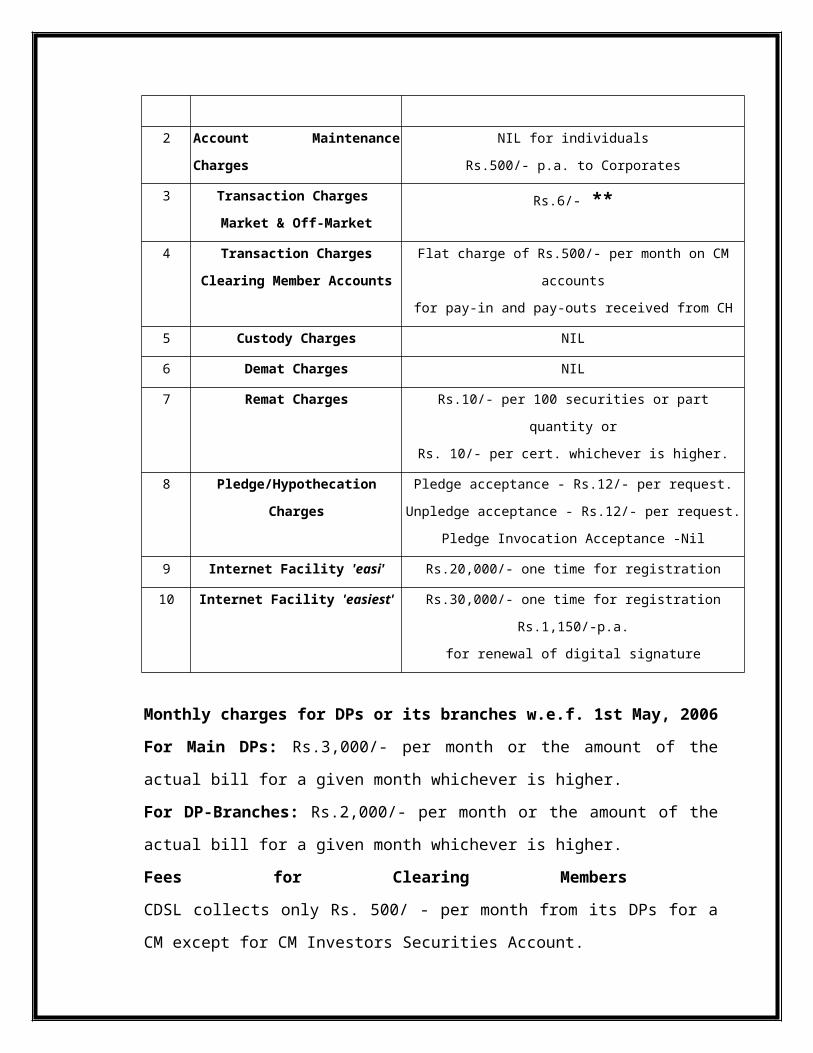

FEE STRUCTURE OF CDSLCDSL fees structure to its depository participants is as follows:

SR.NO

.

Details of Charges CDSL

1 Account Opening Charges NIL

2 Account Maintenance

Charges

NIL for individuals

Rs.500/- p.a. to Corporates

3 Transaction Charges

Market & Off-Market Rs.6/- **

4 Transaction Charges

Clearing Member Accounts

Flat charge of Rs.500/- per month on CM

accounts

for pay-in and pay-outs received from CH

5 Custody Charges NIL

6 Demat Charges NIL

7 Remat Charges Rs.10/- per 100 securities or part

quantity or

Rs. 10/- per cert. whichever is higher.

8 Pledge/Hypothecation

Charges

Pledge acceptance - Rs.12/- per request.

Unpledge acceptance - Rs.12/- per request.

Pledge Invocation Acceptance -Nil

9 Internet Facility 'easi' Rs.20,000/- one time for registration

10 Internet Facility 'easiest' Rs.30,000/- one time for registration

Rs.1,150/-p.a.

for renewal of digital signature

Monthly charges for DPs or its branches w.e.f. 1st May, 2006

For Main DPs: Rs.3,000/- per month or the amount of the

actual bill for a given month whichever is higher.

For DP-Branches: Rs.2,000/- per month or the amount of the

actual bill for a given month whichever is higher.

Fees for Clearing Members

CDSL collects only Rs. 500/ - per month from its DPs for a

CM except for CM Investors Securities Account.

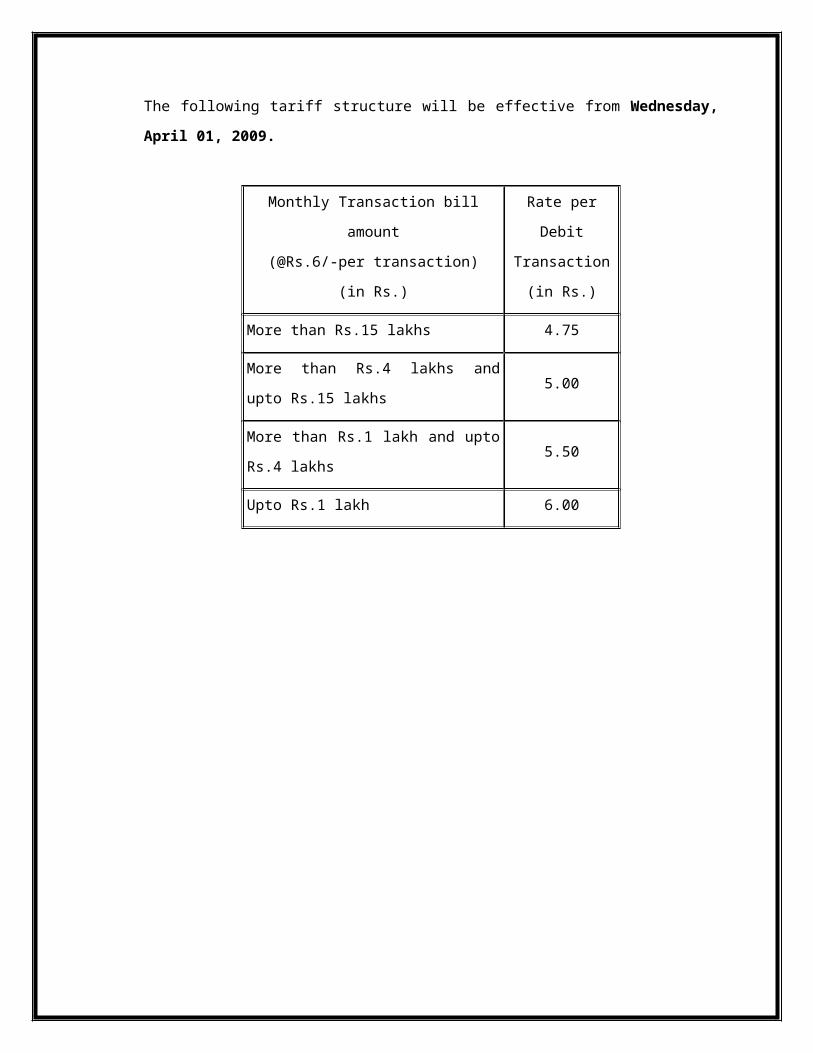

The following tariff structure will be effective from Wednesday,

April 01, 2009.

Monthly Transaction bill

amount

(@Rs.6/-per transaction)

(in Rs.)

Rate per

Debit

Transaction

(in Rs.)

More than Rs.15 lakhs 4.75

More than Rs.4 lakhs and

upto Rs.15 lakhs5.00

More than Rs.1 lakh and upto

Rs.4 lakhs5.50

Upto Rs.1 lakh 6.00