7eleven case-smu

TRANSCRIPT

7-ELEVEN, INC.

In mid-January, 2005, Jack Stout, the Asset ManagementPlanning Manager at 7-Eleven, Inc., met with a group of marketinginterns. The purpose of the meeting was to describe theirinternship project.

Mr. Stout's primary responsibility was to formulate thestrategy for where 7-Eleven, Inc. would open new conveniencestores and close existing stores. In 2005, 7-Eleven, Inc.intended to open around 100 to150 new stores in its present coreurban and suburban markets in the United States. Mr. Stoutthought that the marketing interns would welcome the opportunityto identify markets for new 7-Eleven convenience stores andrecommend specific store locations. Therefore, he proceeded togive an overview of 7-Eleven, Inc., the convenience storeindustry, and the internship assignment.

The Company

7-Eleven, Inc. is the world’s largest operator, franchiserand licensor of convenience stores with over 27,500 unitsworldwide. The company’s total revenues were about $12.2 billionin 2004 principally from retail sales of merchandise and gasolinein its U.S. and Canadian stores.

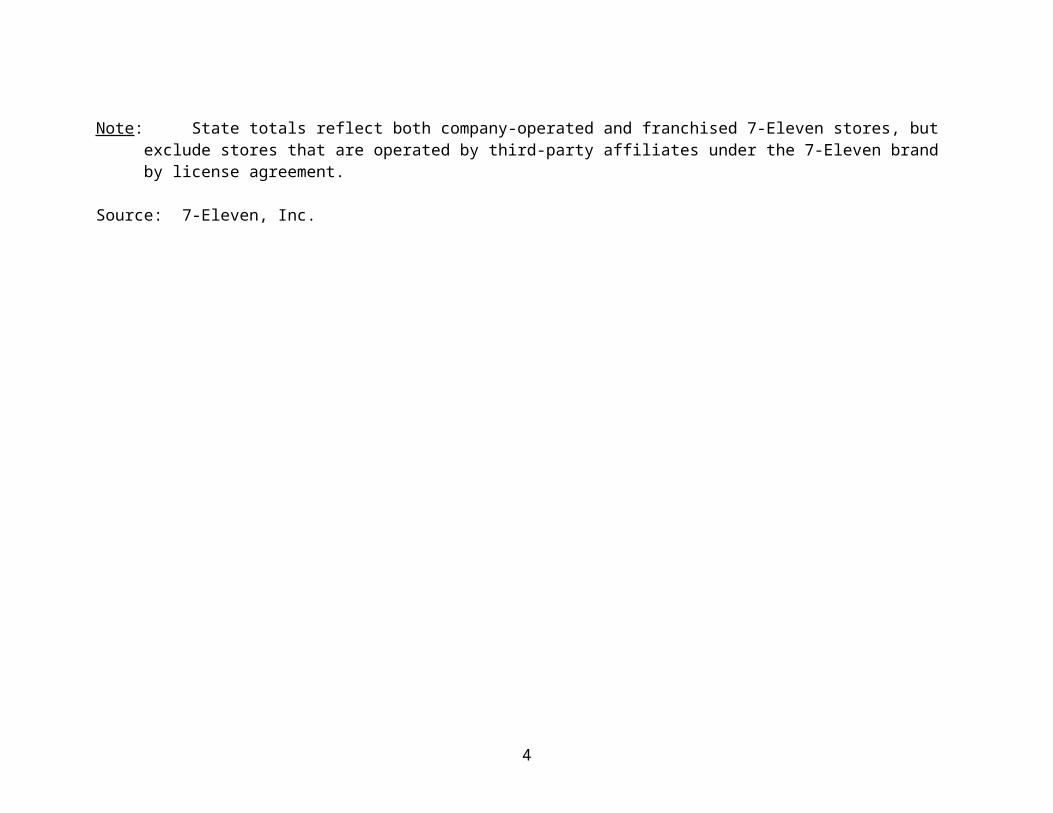

7-Eleven operates and franchises more than 5,300 stores inthe United States. About 60 percent of these stores are locatedin California, Florida, Maryland, New York, Texas, and Virginia.In addition, 7-Eleven operates and franchises about 500 stores inCanada. Area licensing agreements and joint ventures cover theoperation of around 500 stores in Mexico and more than 10,600

1

stores in Japan. Figure 1 shows the distribution of 7-Elevenstores in the contiguous United States.

7-Eleven Business Model

The 7-Eleven business model consists of five key elements:

1. A differentiated merchandising strategy;2. Utilization of 7-Eleven’s retail information system;3. Managed distribution;4. Providing a convenient shopping environment; and5. A unique franchise model

The cooperation of 7-Eleven, Inc. in the preparation of this case is gratefullyacknowledged. This case was prepared by the JCPenney Center for Retail Excellence,Edwin L. Cox School of Business, Southern Methodist University, under the supervisionof Professor Roger A. Kerin.

2

Figure 1

3

7-Eleven Store Counts by State: January 2005

2

Note: State totals reflect both company-operated and franchised 7-Eleven stores, but exclude stores that are operated by third-party affiliates under the 7-Eleven brand by license agreement.

Source: 7-Eleven, Inc.

4

Differentiated merchandising strategy. 7-Eleven offers abroad array of products, including many not traditionallyavailable in convenience stores, to meet the needs of itscustomers. These products include high-quality fresh foods thatare delivered daily to stores. In addition, the company sells anumber of products that are developed specifically for itsstores, such as 7-Eleven Go-Go Taquitos®, crispy grilledtortillas with spicy Mexican filling. The company’s merchandiseassortment also features items specifically identified with 7-Eleven, including Slurpee® semi-frozen carbonated beverages, CaféSelect® coffee, Big Gulp® fountain beverages and Big Bite® hotdogs.

7-Eleven implements its merchandising strategy through avariety of means. It employs item-by-item inventory managementto keep top-selling items in-stock. In addition, the companypromotes new high-potential items. The company expects itsfranchisees and store managers to monitor customer buyingpatterns to maximize store sales by staying stocked on popularitems, managing product assortment and merchandising effectively.

7-Eleven sells gasoline at more than 2,400 stores. Almostall offer CITGO-branded gasoline. Because gasoline salescontribute to increased store traffic, 7-Eleven sells gasoline atits stores wherever practical. The company expects thatapproximately half of its new stores opening in the United Statesand Canada in the foreseeable future will sell gasoline.

Utilization of 7-Eleven’s retail information system. 7-Eleven was the first major convenience store chain in the UnitedStates to use an integrated set of retail information tools.Effective utilization of the system is the foundation of thecompany’s business model.

The 7-Eleven retail information system features:

A point-of-sale, touch-screen system withscanning and integrated credit, debit and stored

5

value card authorization, supported by acentralized price book;

Daily ordering, supported by five-dayforward-looking weather forecasts, merchandisemessages and historical sales information;

Category management and item level salesanalysis;

Integrated gasoline and “pay-at-the-pump”functionality;

Automated back-office functions, such assales and cash reporting, payroll, gasoline pricingand inventory control, which are connected directlyto the company accounting system; and

The ability to make delivery adjustments andperform write-offs on a hand-held unit.

Managed distribution. 7-Eleven works with its vendors and distributors to provide daily delivery of fresh food and other items to its stores, to lower the cost of delivery, and to shift deliveries to off-peak hours. Vendors include independently-owned and operated bakeries and commissaries that provide daily deliveries of fresh foods, such as sandwiches, salads, and baked goods, to its stores. In addition, the company uses 24 distribution centers in the United States and Canada to service approximately 4,900 of its stores. Each center serves about 200 stores, on average. These centers typically serve stores within a 90-minute drive. The distribution centers, which consolidate orders from multiple suppliers for daily distribution to individual stores, offer a number of advantages over other distribution systems, including:

More frequent deliveries of time-sensitive andperishable products such as milk, bread and fresh foods;

Off-peak, consolidated deliveries that allow storepersonnel to focus on store operations and reducecongestion in a typically small 7-Eleven store parkinglot during peak sales times;

6

More customized deliveries and improved in-stocklevels; and

Access to products that traditionally have notbeen available to individual convenience stores.

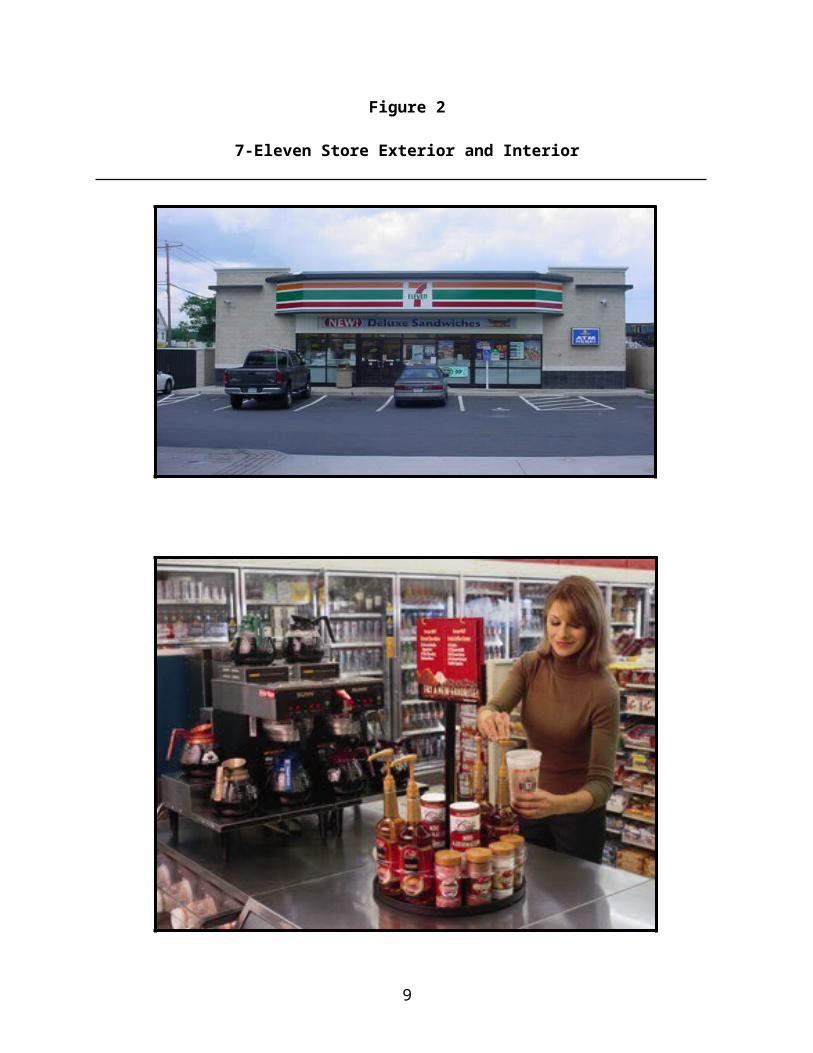

Providing a convenient shopping environment. 7-Eleven seeksto provide its customers with a convenient, safe and clean storeenvironment. The majority of 7-Eleven stores in the UnitedStates and Canada provide more than 6 million daily customerswith 24-hour convenience, seven days a week. Over the lastseveral years, the company has improved lighting inside andoutside its stores, modernized store signage and installedcanopies over the gasoline pumps. In 2004, around $80 millionwas spent for store maintenance and the replacement of storeequipment. Figure 2 shows the exterior and interior of a 7-Eleven store which typically range in size from 2,400 to 3,000square feet.

Unique franchise model. More than half of the 7-Elevenstores in the United States are operated by independentfranchisees. The company’s franchise model is different frommost others because 7-Eleven owns or leases the stores andequipment used by its franchisees. In addition, the ongoingroyalties that the company receives from its franchisees arebased upon a percentage of store gross profit. 7-Eleven believesthis model better aligns company interests with those of itsfranchisees and allows the company to provide consistency in thestore environment and shopping experience for its customers. 7-Eleven also provides more support to its franchisees than mostfranchisors, including financing, bookkeeping, advertising,business counseling and other services.

7-Eleven Growth Strategy

7-Eleven has identified four avenues for future growth. They are:

1. Increasing same-store merchandise sales.

7

2. Expanding in existing markets.3. Providing greater convenience to customers.4. Increasing the value of 7-Eleven licenses and expanding

internationally.

8

Figure 2

7-Eleven Store Exterior and Interior

9

Source: 7-Eleven, Inc.

10

Increasing same-store merchandise sales. 7-Eleven seeks to increase same-store sales1 by developing and introducing new products. By using proprietary inventory management and retail information systems, 7-Eleven’s merchandising team, franchisees, and store managers are better able to increase same-store sales by optimizing the product assortment in each store. Allowing individual store operators to manage product assortment is part of 7-Eleven's Retailer Initiative strategy. Store managers and franchisees are trained in the principles of item-by-item management – removing slow-selling items and introducing new items every day based on local preferences.

Expanding in existing markets. 7-Eleven’s store developmentefforts are focused on its existing markets to take advantage ofpopulation density and traffic. Typically, new stores areconcentrated around the distribution centers, commissaries andbakeries that allow the company to operate more efficiently.Company management believes that the potential exists forsignificant expansion in present core urban and suburban markets,and plans to open approximately 100 to150 new stores in theUnited States during 2005. A location analysis for new storesconsiders population density, demographics, traffic volume,visibility, ease of access, locations of other 7-Eleven stores,and economic and competitor activity in an area.

Providing greater convenience to customers. 7-Elevencontinually seeks ways to improve customer convenience throughinnovative merchandising programs. One such innovative programis Vcom®, which is 7-Eleven’s proprietary self-service kiosk thatoffers check-cashing, money order, money transfer, bill paymentand traditional ATM services and access to Verizon residentialtelephone services.

Increasing the value of 7-Eleven licenses and expandinginternationally. By continuing to develop its infrastructure, 7-Eleven offers an attractive financial opportunity to prospectivelicensees. Infrastructure development will also serve to1 Same-store merchandise sales refers to sales dollars generated only by thosestores that have been open more than one year and have historical sales data to compare the current year’s sales to the same time-frame the previous year.

11

strengthen the value of the 7-Eleven brand. 7-Eleven’s long-range plans include expanding into countries where it currentlydoes not have a presence. For example, an area licensingagreement for China was developed in early 2004.

7-Eleven Products and Services

7-Eleven stores offer a wide array of products and servicesbased on customer demands, sales potential, and profitability.Broadly speaking, 7-Eleven net sales are split between gasolineand merchandise (including services). Gasoline typicallyaccounts for about 30 percent of company net sales. Merchandise(including services) accounts for about 65 to 70 percent ofcompany net sales.

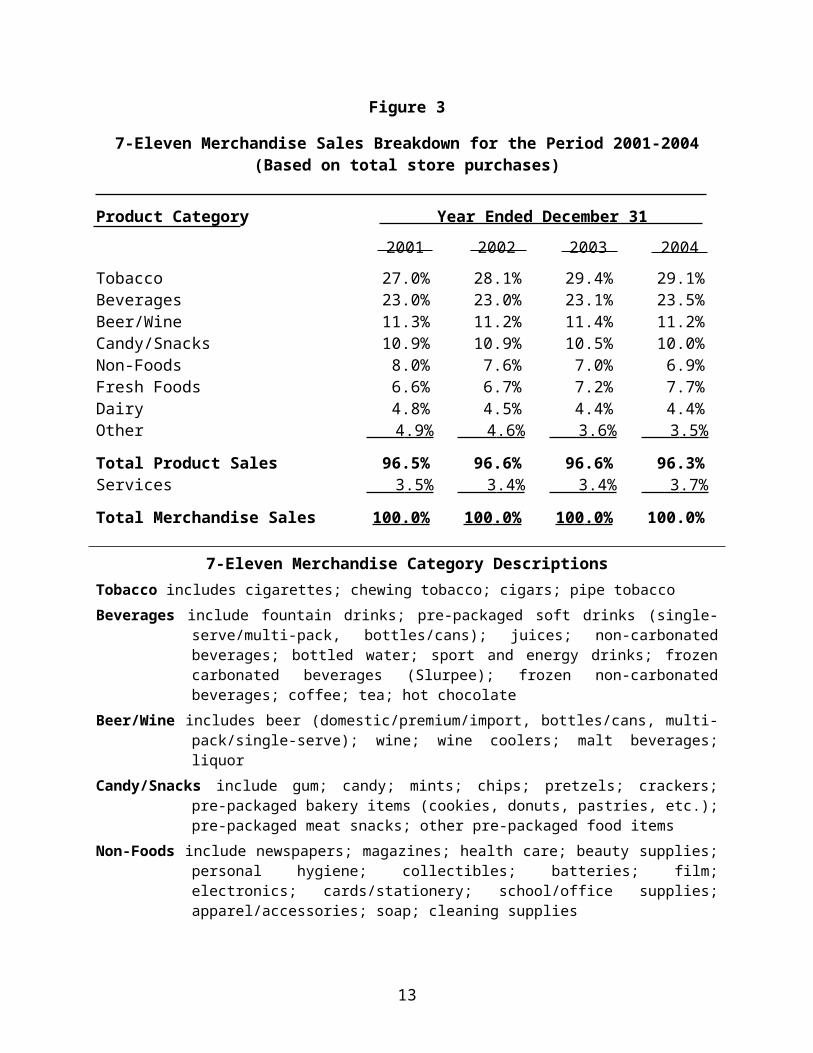

7-Eleven stores carry anywhere from 2,300 to 2,800merchandise items. These items fall into nine general productcategories. Figure 3 shows the merchandise (service) salesbreakdown for 7-Eleven stores in the United States and Canada byproduct category. Of all U.S. retailers, 7-Eleven sells the mostUSA Today newspapers, Sports Illustrated magazines, cold beer,cold single-serve bottled water, cold Gatorade, fresh-grilled hotdogs, single-serve snack chips and money orders. 7-Eleven alsohas the largest ATM network of any U.S. retailer.

12

Figure 3

7-Eleven Merchandise Sales Breakdown for the Period 2001-2004(Based on total store purchases)

Product Category Year Ended December 31

2001 2002 2003 2004Tobacco 27.0% 28.1% 29.4% 29.1%Beverages 23.0% 23.0% 23.1% 23.5%Beer/Wine 11.3% 11.2% 11.4% 11.2%Candy/Snacks 10.9% 10.9% 10.5% 10.0%Non-Foods 8.0% 7.6% 7.0% 6.9%Fresh Foods 6.6% 6.7% 7.2% 7.7%Dairy 4.8% 4.5% 4.4% 4.4%Other 4 .9% 4 .6% 3 .6% 3 .5%

Total Product Sales 96.5% 96.6% 96.6% 96.3%Services 3 .5% 3 .4% 3 .4% 3 .7%

Total Merchandise Sales 100 .0% 100 .0% 100 .0% 100.0%

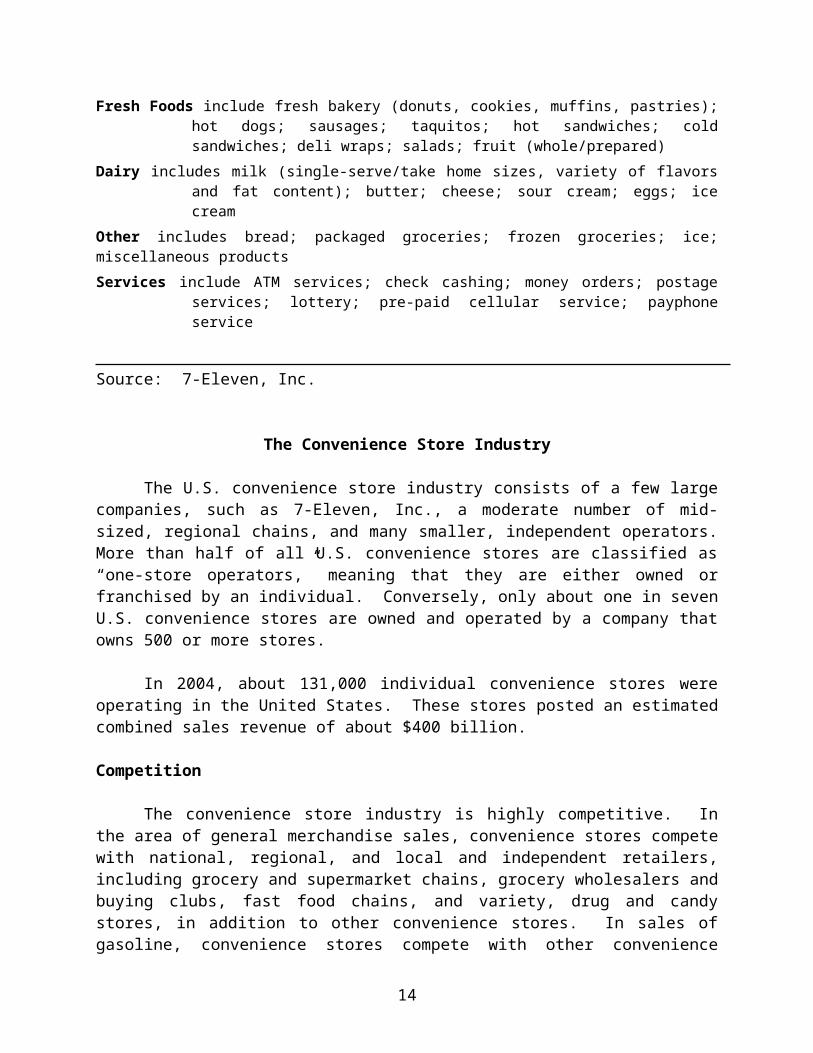

7-Eleven Merchandise Category DescriptionsTobacco includes cigarettes; chewing tobacco; cigars; pipe tobaccoBeverages include fountain drinks; pre-packaged soft drinks (single-

serve/multi-pack, bottles/cans); juices; non-carbonatedbeverages; bottled water; sport and energy drinks; frozencarbonated beverages (Slurpee); frozen non-carbonatedbeverages; coffee; tea; hot chocolate

Beer/Wine includes beer (domestic/premium/import, bottles/cans, multi-pack/single-serve); wine; wine coolers; malt beverages;liquor

Candy/Snacks include gum; candy; mints; chips; pretzels; crackers;pre-packaged bakery items (cookies, donuts, pastries, etc.);pre-packaged meat snacks; other pre-packaged food items

Non-Foods include newspapers; magazines; health care; beauty supplies;personal hygiene; collectibles; batteries; film;electronics; cards/stationery; school/office supplies;apparel/accessories; soap; cleaning supplies

13

Fresh Foods include fresh bakery (donuts, cookies, muffins, pastries);hot dogs; sausages; taquitos; hot sandwiches; coldsandwiches; deli wraps; salads; fruit (whole/prepared)

Dairy includes milk (single-serve/take home sizes, variety of flavorsand fat content); butter; cheese; sour cream; eggs; icecream

Other includes bread; packaged groceries; frozen groceries; ice;miscellaneous productsServices include ATM services; check cashing; money orders; postage

services; lottery; pre-paid cellular service; payphoneservice

Source: 7-Eleven, Inc.

The Convenience Store Industry

The U.S. convenience store industry consists of a few largecompanies, such as 7-Eleven, Inc., a moderate number of mid-sized, regional chains, and many smaller, independent operators.More than half of all U.S. convenience stores are classified as“one-store operators,” meaning that they are either owned orfranchised by an individual. Conversely, only about one in sevenU.S. convenience stores are owned and operated by a company thatowns 500 or more stores.

In 2004, about 131,000 individual convenience stores wereoperating in the United States. These stores posted an estimatedcombined sales revenue of about $400 billion.

Competition

The convenience store industry is highly competitive. Inthe area of general merchandise sales, convenience stores competewith national, regional, and local and independent retailers,including grocery and supermarket chains, grocery wholesalers andbuying clubs, fast food chains, and variety, drug and candystores, in addition to other convenience stores. In sales ofgasoline, convenience stores compete with other convenience

14

stores, food stores, service stations and increasinglysupermarket chains, hyper-marts and other discount retailers.The rapid growth in the numbers of convenience-type stores openedby oil companies over the past several years has also intensifiedcompetition.

Customers

About 90 percent of U.S. adults (18 years or older) visit aconvenience store at least once a year. The average number ofvisits per week for a 7-Eleven customer is 3.5. Twenty percentof customers visit a 7-Eleven store more than five times perweek.

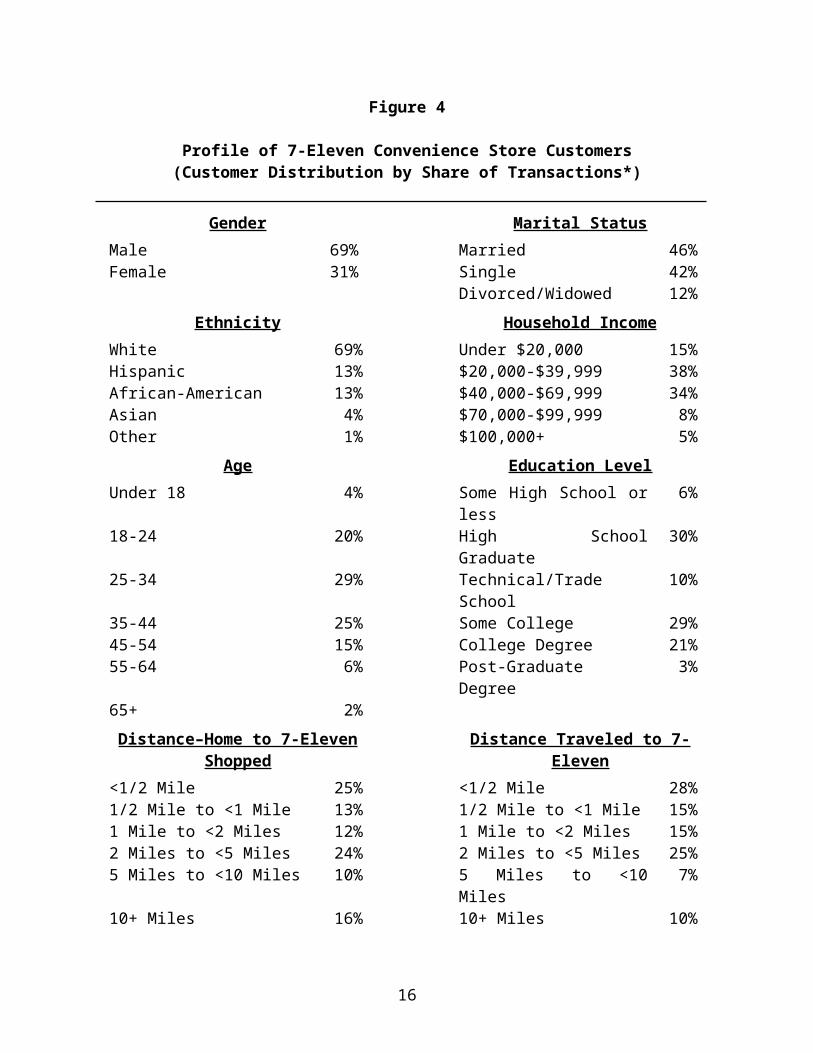

7-Eleven management believes that the characteristics of itscustomers are representative of convenience store customers as awhole. Figure 4 shows the profile of 7-Eleven convenience storecustomers. Almost 7 in 10 (69%) customers are male and white. Amajority of customers (54%) are unmarried; 54 percent fall intothe 25 to 44 age group; and 53 percent have attended or completedcollege. Almost three-quarters (72%) of 7-Eleven customers havean annual household income between $20,000 and $70,000.

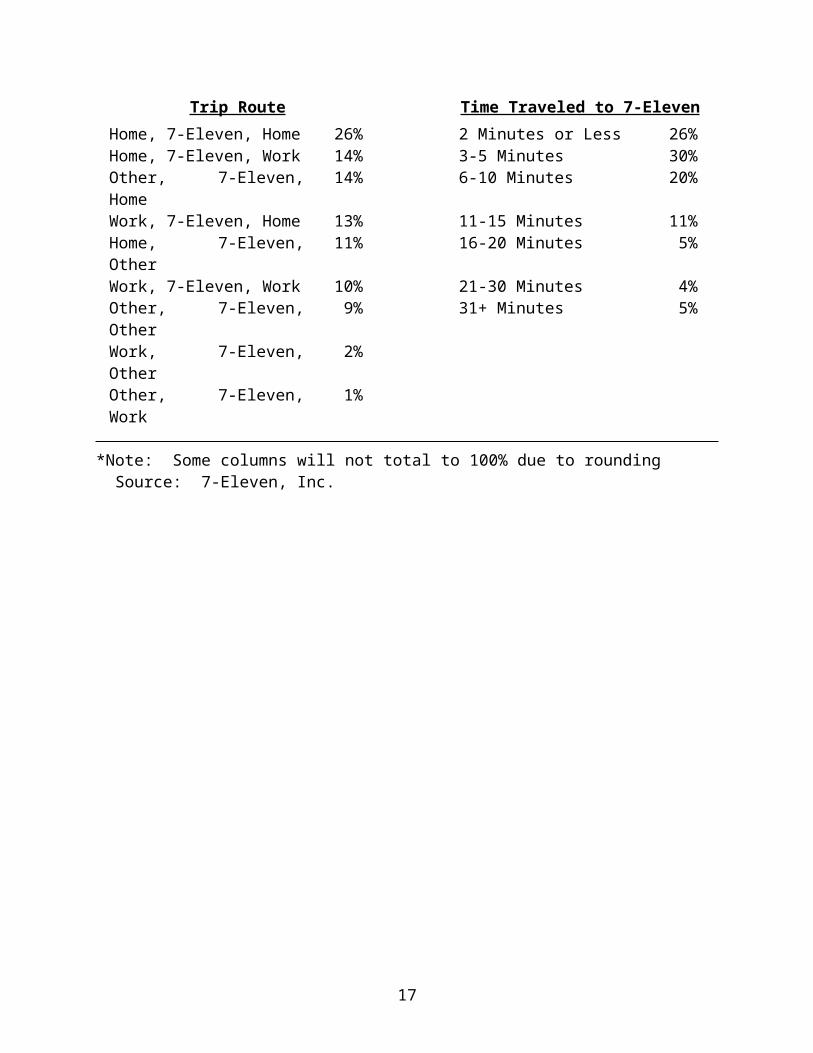

Almost 8 in 10 (78%) 7-Eleven store trip visits have acustomer’s residence as the origin or destination. The distancefrom a customer’s residence to the 7-Eleven store visited isunder 10 miles for 84 percent of customers. Nine in 10 customerstravel less than 10 miles to a 7-Eleven store. The time traveledto a 7-Eleven store is 10 minutes or less for 76 percent ofcustomers.

15

Figure 4

Profile of 7-Eleven Convenience Store Customers(Customer Distribution by Share of Transactions*)

Gender Marital Status

Male 69% Married 46%Female 31% Single 42%

Divorced/Widowed 12%Ethnicity Household Income

White 69% Under $20,000 15%Hispanic 13% $20,000-$39,999 38%African-American 13% $40,000-$69,999 34%Asian 4% $70,000-$99,999 8%Other 1% $100,000+ 5%

Age Education LevelUnder 18 4% Some High School or

less6%

18-24 20% High SchoolGraduate

30%

25-34 29% Technical/TradeSchool

10%

35-44 25% Some College 29%45-54 15% College Degree 21%55-64 6% Post-Graduate

Degree3%

65+ 2%Distance–Home to 7-Eleven

ShoppedDistance Traveled to 7-

Eleven<1/2 Mile 25% <1/2 Mile 28%1/2 Mile to <1 Mile 13% 1/2 Mile to <1 Mile 15%1 Mile to <2 Miles 12% 1 Mile to <2 Miles 15%2 Miles to <5 Miles 24% 2 Miles to <5 Miles 25%5 Miles to <10 Miles 10% 5 Miles to <10

Miles7%

10+ Miles 16% 10+ Miles 10%

16

Trip Route Time Traveled to 7-ElevenHome, 7-Eleven, Home 26% 2 Minutes or Less 26%Home, 7-Eleven, Work 14% 3-5 Minutes 30%Other, 7-Eleven,Home

14% 6-10 Minutes 20%

Work, 7-Eleven, Home 13% 11-15 Minutes 11%Home, 7-Eleven,Other

11% 16-20 Minutes 5%

Work, 7-Eleven, Work 10% 21-30 Minutes 4%Other, 7-Eleven,Other

9% 31+ Minutes 5%

Work, 7-Eleven,Other

2%

Other, 7-Eleven,Work

1%

*Note: Some columns will not total to 100% due to rounding Source: 7-Eleven, Inc.

17

The Assignment (Report and Presentation Due Tue. April 19)

Following the overview of 7-Eleven, Inc. and the conveniencestore industry, Mr. Stout outlined the assignment for the MBA’s.The assignment was to employ the SimmonsLocal® Market Servicedatabase and Microsoft MapPoint® software to examine selected 7-Eleven markets and recommend specific locations for new 7-Elevenconvenience stores. Mr. Stout was particularly interested instore location opportunities in Austin, Texas, where there arecurrently 36 stores.

Mr. Stout expected the students to prepare a detailed reportthat would:

1. Identify a specific location in the Austin market wherea 7-Eleven store should be opened and explain thereasons for the selection. The location should be aspecific street intersection.

2. Describe the socio-economic profile of the likelycustomers at the specific locations. Compare andcontrast this profile with that of convenience storecustomers.

3. Recommend at least one new product category or servicethat the specified store locations should provide, inaddition the product assortment typically carried by a7-Eleven store. Explain the reasons for thisrecommendation.

In preparing their report, the students could assume that the newstore locations would offer CITGO-branded gasoline and beserviced by a 7-Eleven distribution center and independently-owned bakeries and commissaries.

The text portion of the report should not exceed 15 double-spaced pages using one inch margins and a 12-point type fontsize. Only those tables and figures used to summarize datarelevant to the analysis and recommendations should be submittedwith the report. They should be properly titled, clearlyreferenced in the text, and attached to the end of the report.

18