2 3 cross-disciplinary economic theory

TRANSCRIPT

1 23

Journal of the Knowledge Economy ISSN 1868-7865 J Knowl EconDOI 10.1007/s13132-013-0163-6

Cross-Disciplinary Economic Theory

Frederick Betz

1 23

Your article is protected by copyright and all

rights are held exclusively by Springer Science

+Business Media New York. This e-offprint is

for personal use only and shall not be self-

archived in electronic repositories. If you wish

to self-archive your article, please use the

accepted manuscript version for posting on

your own website. You may further deposit

the accepted manuscript version in any

repository, provided it is only made publicly

available 12 months after official publication

or later and provided acknowledgement is

given to the original source of publication

and a link is inserted to the published article

on Springer's website. The link must be

accompanied by the following text: "The final

publication is available at link.springer.com”.

Cross-Disciplinary Economic Theory

Frederick Betz

Received: 14 November 2012 /Accepted: 9 June 2013# Springer Science+Business Media New York 2013

Abstract A knowledge economy still produces goods and services, although by theimportant use of knowledge. Therefore, economic models are relevant to understandinghow a knowledge economy should properly work, particularly the financial system in aknowledge economy. When finance fails, all knowledge stops. Cross-disciplinary ap-proaches to societal models of a knowledge economy are necessary and useful, becausesocieties are more complex than can be seen by any single social science discipline. Thiswas dramatically demonstrated in the first decade of the twenty-first century by the majorfailure of mainstream economic theory, as a basis for financial regulation. The surprisingthing was that the economic discipline as a whole did not take this empirical opportunity torethink economic theory, to build together a new and valid theory. Instead, the schools ofeconomics continued to argue with one another. We take this historical case of scholasticconflict to reexamine economic theory, but within a cross-disciplinary framework. Weuse the modeling that had been accomplished in the two conflicting economicschools—exogenous and endogenous schools. Each modeled parts of an economicsystem, production subsystem (exogenous school) and financial subsystem (endoge-nous school). But neither succeeded in modeling the whole of an economic system.Within a larger cross-disciplinary framework of societal dynamics theory, we show howto assemble these partial models into a more complete economic model.

Keywords Economic theory . Economic models . Cross disciplinary research

Introduction

Cross-disciplinary research is essential because policies based upon research shouldbe empirically valid. But research completely within the narrow bounds of a singlediscipline rarely results in valid theory, which realistically reflected the complexity ofa whole society. The Global Financial Crisis of 2007–2008 was a dramatic case of

J Knowl EconDOI 10.1007/s13132-013-0163-6

F. BetzKorea University, Seoul, South Korea

F. Betz (*)Portland State University, Portland, OR, USAe-mail: [email protected]

Author's personal copy

this, wherein mainstream economic policy failed to anticipate the crisis, while it hadbeen used to justify deregulation preceding the crisis. Policy failure in deregulation ofthe banking industry had been based upon an economic assumption that financialmarkets operated perfectly. Earlier, we analyzed this case in a cross-disciplinaryframework—seeing how that failure of the knowledge economy went beyond simpleexplanation by economic ideas—also requiring ideas from other disciplines, such associology, management science, and management of technology (Betz 2012). Thequestion we address here is not about the failure of a financial system but the failureof economic theory.

History—Division in Economic Theory in 2009–2012

Going back in time from 2012 to 2010 to 2009 (the recent years following thefinancial crisis of 2008), one can find the historical evidence of theory failure andalso of a continuing failure of the discipline to agree upon how to construct validtheory. In science, of course, when theory fails to explain empirical reality, thentheory is changed. But matters were not so straightforward in the recent history of theeconomics discipline. Instead of immediately rushing to change economic theory,there continued a contentious debate among economists. Was a market empiricallyperfect or only ideally perfect? Mainstream economic theory had constructed aneconomic model of supply–demand–price equilibrium, which was based upon theassumption of a perfect market. But fact was that the financial market had been farfrom perfect. For example in 2012, one economist, Howard Davies, then a professorat Sciences Po in Paris wrote: “In an exasperated outburst, just before he left thepresidency of the European Central Bank, Jean-Claude Trichet complained that: ‘as apolicymaker during the crisis. I found the available models of limited help; in fact, Iwould go further. In the face of the crisis, we felt abandoned by conventional tools.’”(Davies 2012).

Previously Davies had been the Director of the London School of Economics andearlier was the Chairman of Britain’s Financial Services Authority and even earlierthe Deputy Director of the Bank of England. Professionally as an economist, Davieswas both an economic academician and practiced as a banking authority. His viewabout the how contemporary economic theory had been useful to practice wasnegative: “Our approach to regulation in the past was based on the assumption thatfinancial markets could to a large extent be left to themselves, and that financialinstitution and their boards were best placed to control risk and defend their firms.These assumptions took a hard hit in the crisis, causing an abrupt shift to far moreintrusive regulation. Finding a new and stable relationship between the financialauthorities and private firms will depend crucially on a reworking of our intellectualmodels.” (Davies 2012).

Davies thought this required change in economics: Reworking economic modelsshould be based upon history: “… there should be more teaching of economichistory,… The study of economics should be set in a broader political context,…But it is not clear that a majority of the profession yet accepts even these modestproposals. The so-called ‘Chicago School’ has mounted a robust defense of itrational- expectations-based approach, rejecting the notion that a rethink is required.

J Knowl Econ

Author's personal copy

The Nobel laureate economist Robert Lucas has argued that the crisis was notpredicted because economic theory predicts that such events cannot be predicted.So all is well.’” (Davis 2012).

Earlier in 2010, Chris Giles had reported: “Many of the world’s top academiceconomists agreed on Friday (April 9, 2010) that the financial and economic crisishad exposed fatal flaws in their subject and ideas were urgently needed to keepeconomics relevant. While this represented an unusual consensus, the eminent eco-nomic brains lived up to their stereotype by disagreeing on what policies, if any,should be adopted to prevent a repetition.… The participants were speaking at theinaugural conference of the Institute for New Economic Thinking, a think-tanksponsored by George Soros, the billionaire financier. They included five Nobelprize-winners (in economics). Held at King’s College, Cambridge… the conferenceparticipants could neither agree on the cause of the crisis nor the necessary remedies.One disagreement hinged on whether asset price bubbles lay at the heart of the crisis.Those who thought so argued for tighter regulation… (Others, such as) MichaelGoldberg, of the University of New Hampshire, said it was wrong to suggest the priceswings were necessarily a bubble and that they were more likely to be fundamental tothe beneficial forces of capitalism.” (Giles 2010).

Another economist, Charles J. Whalen, had written: “The financial crisis that ranfrom late 2007 through early 2009 did more than traumatize the world economy; itdrew widespread attention to some major shortcomings of conventional economics.Paul Krugman pointed out those weaknesses in a number of public lectures and in thepages of The New York Times, but he was not alone. Forced to confront the reality ofthe Great Recession, a number of prominent scholars and policymakers also joinedthe chorus.” (Whalen 2012).

Back in 2009, Paul Krugman (a Noble prize economist) analyzed his discipline:“It’s hard to believe now, but not long ago economists were congratulating them-selves over the success of their field. Those successes—or so they believed—wereboth theoretical and practical, leading to a golden era for the profession. On thetheoretical side, they thought that they had resolved their internal disputes…. And inthe real world, economists believed they had things under control: the ‘centralproblem of depression-prevention has been solved’, declared Robert Lucas of theUniversity of Chicago in his 2003 presidential address to the American EconomicAssociation. In 2004, Ben Bernanke, a former Princeton professor who is now thechairman of the Federal Reserve Board, celebrated the Great Moderation in economicperformance over the previous two decades, which he attributed in part to improvedeconomic policy making. (But) last year (2008), everything came apart. … Feweconomists saw our current crisis coming, but this predictive failure was the least ofthe field’s problems. More important was the profession’s blindness to the verypossibility of catastrophic failures in a market economy. … During the golden years,financial economists came to believe that markets were inherently stable—indeed,that stocks and other assets were always priced just right. There was nothing in theprevailing models suggesting the possibility of the kind of collapse that happened lastyear in 2008.” (Krugman 2009).

One exception had been the economist, Nouriel Roubini, who had forecast thehousing bubble and financial crisis. At the time, his warning was ignored, butafterwards, he became well-known and established a consultancy company. But the

J Knowl Econ

Author's personal copy

point is that the “mainstream” economic theorists had not anticipated financial crisesand could not explain them. The reason for this was in methodology—a split amongeconomists about how to explain economics. The mainstream economics school (calleda “Neo-Classical Synthesis” School) explained an economy principally as a productionsystem, perfectly balanced in supply and demand. The contending school called “Neo-Keynesians” (or “Post-Keynesians”) argued that a financial system was equally impor-tant with production systems in an economy, and that these two kinds of markets(commodity and financial) operated differently—and neither perfectly.

Krugman wrote about this division among economists: “Meanwhile, macroeconomists(remain) divided in their views. But the main division was between those who insisted thatfree-market economies never go astray and those who believed that economiesmay stray now and then (but that any major deviations from the path ofprosperity could and would be corrected by the all-powerful Fed). Neither sidewas prepared to cope with an economy that went off the rails despite the Fed’sbest efforts. … And in the wake of the crisis, the fault lines in the economicsprofession have yawned wider than ever.” (Krugman 2009).

Why did this fault line persist? Krugman explained this as due to “aesthetics”: “AsI (Krugman) see it, the economics profession went astray because economists, as agroup, mistook beauty, clad in impressive-looking mathematics, for truth. Until the(1930s) Great Depression, most economists clung to a vision of capitalism as aperfect or nearly perfect system. That vision wasn’t sustainable in the face of massunemployment. But as memories of the Depression faded, economists fell back inlove with the old, idealized vision of an economy in which rational individuals interactin perfect markets; this time gussied up with fancy equations. … Unfortunately, thisromanticized and sanitized vision of the economy led most economists to ignoreall the things that can go wrong. They turned a blind eye to the limitations of humanrationality that often lead to bubbles and busts; to the problems of institutions that runamok; to the imperfections ofmarkets—especially financial markets—that can cause theeconomy’s operating system to undergo sudden, unpredictable crashes; and to thedangers created when regulators don’t believe in regulation.” (Krugman 2009).

We briefly review the partial models of an economy by the two schools ofeconomics, Neo-Classical Synthesis and Neo-Keynesian

Neo-Classical Synthesis School

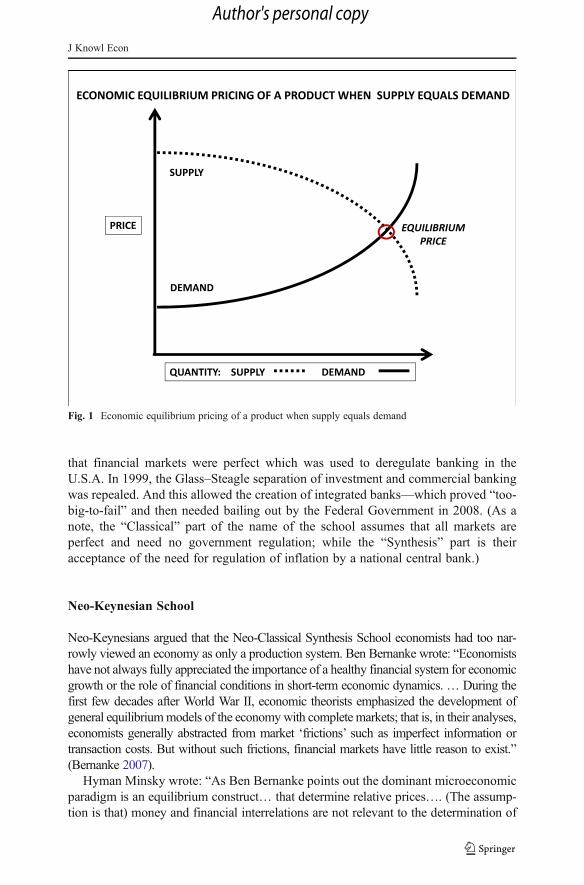

The central model in the Neo-Classical Synthesis School is the supply–demand curveof equilibrium pricing in an economy, as shown in Fig. 1.

When the price of a commodity is charted as the quantity of the supply of theproduct (dotted line) then the price will decrease in an economy as the supplyincreases. Because of business competition, more goods flooding a market will forceprices down. Also, if the demand for a product (solid line) increases, then the pricewill increase (as more consumers buy a limited amount of product). The optimalpricing of a product (commodity) in an economy will occur when supply equalsdemand. This is the equilibrium price, as supply and demand meet in quantity. If amarket behaves like this, it is perfect. No control over pricing is necessary, as asupply–demand equilibrium in the market sets the optimal price. This was the theory

J Knowl Econ

Author's personal copy

that financial markets were perfect which was used to deregulate banking in theU.S.A. In 1999, the Glass–Steagle separation of investment and commercial bankingwas repealed. And this allowed the creation of integrated banks—which proved “too-big-to-fail” and then needed bailing out by the Federal Government in 2008. (As anote, the “Classical” part of the name of the school assumes that all markets areperfect and need no government regulation; while the “Synthesis” part is theiracceptance of the need for regulation of inflation by a national central bank.)

Neo-Keynesian School

Neo-Keynesians argued that the Neo-Classical Synthesis School economists had too nar-rowly viewed an economy as only a production system. Ben Bernanke wrote: “Economistshave not always fully appreciated the importance of a healthy financial system for economicgrowth or the role of financial conditions in short-term economic dynamics.… During thefirst few decades after World War II, economic theorists emphasized the development ofgeneral equilibriummodels of the economywith complete markets; that is, in their analyses,economists generally abstracted from market ‘frictions’ such as imperfect information ortransaction costs. But without such frictions, financial markets have little reason to exist.”(Bernanke 2007).

Hyman Minsky wrote: “As Ben Bernanke points out the dominant microeconomicparadigm is an equilibrium construct… that determine relative prices…. (The assump-tion is that) money and financial interrelations are not relevant to the determination of

Fig. 1 Economic equilibrium pricing of a product when supply equals demand

J Knowl Econ

Author's personal copy

these equilibrium variables. … But if the basic microeconomic model is opened toinclude yesterdays, todays, and tomorrows—then (the only way that) … that equilibri-um exists, depends upon assuming that (economic) agents have perfect foresight.”(Minsky 1993). Minsky did not believe in “perfect foresight” of economic agents, thepeople who do economic transactions.

Minsky argued that a time dimension was important to a model of an economy. In1936, JohnMarnard Keynes had introduced a time dimension in an economy—in order toinclude “finance” as a part of the economicmodel. “In theGeneral Theory, Keynes soughtto create a model of the economy in which money is never neutral (to pricing). He did thisby creating a model… in which the price level of financial… assets is determined in(financial) markets where… the price of money… is an asset whose value is derived fromits liquidity. For Keynes, each capital and financial asset yields an income stream, (which)has carrying costs and possessing some degree of liquidity… The price level of assets isdetermined by the relative value… (of) income… and liquidity…” (Minsky 1993)

Time dependence in a Keynes model of a financial system lies in the concepts of: a“present-income” and a “future liquidity” of a “capital asset.” A capital asset is aninvestment which creates income and can later be sold. A capital asset produces anincome stream (present-income) but also can be sold in the future (future liquidity)(Minsky 1975). The time dimension is from (T1) of a present-income to (T2) of futureliquidity. This present-to-future (T1 to T2) temporal process occurs in a financialsystem as a transaction of “credit-debt.” Minsky wrote: “Every capitalist economy ischaracterized by a system of borrowing and lending… The fundamental borrowingand lending act… is an exchange of ‘money-now’ for ‘money-in-the-future’. Thisexchange takes place… in a negotiation in which the borrower demonstrates to thesatisfaction of the lender—that the money of the future part of the contract will beforthcoming…. The money in the future is to cover both the interest and therepayment of the principle of the contract.” (Minsky 1993).

This is the time dimension of any financial system—the yesterday of credit, thetoday of interest payment, and the tomorrow of paying off the debt. Credit and debt asa financial process is essentially temporal; and this is why models of economicsystems must have a time dimension for Keynesians.And a financial market providesliquidity through valuing capital assets: “In the General Theory, Keynes… created amodel… in which the price level of financial… assets is determined in (financial)markets… where … the price of money… is an asset whose value is derived from itsliquidity… For Keynes, each capital and financial asset yields an income stream,(which) has carrying costs and possessing some degree of liquidity… The price levelof assets is determined by the relative value… (of) income in the future and liquiditynow.” (Minsky 1993). A financial market makes the credit-debt contracts sellable inthe future, as future liquidity. A capital asset must have two temporal features of acurrent-income and a future liquidity. A financial market provides the capability offuture liquidity for a capital asset.

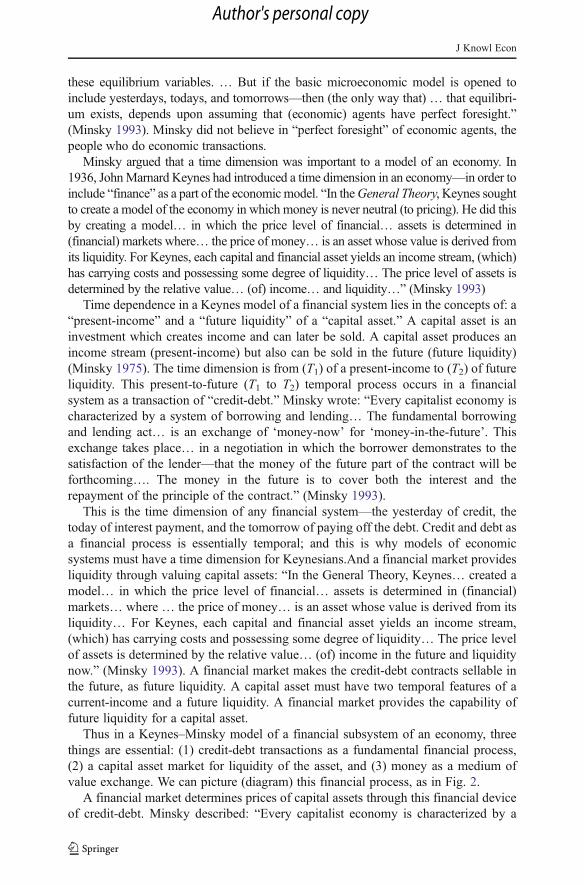

Thus in a Keynes–Minsky model of a financial subsystem of an economy, threethings are essential: (1) credit-debt transactions as a fundamental financial process,(2) a capital asset market for liquidity of the asset, and (3) money as a medium ofvalue exchange. We can picture (diagram) this financial process, as in Fig. 2.

A financial market determines prices of capital assets through this financial deviceof credit-debt. Minsky described: “Every capitalist economy is characterized by a

J Knowl Econ

Author's personal copy

system of borrowing and lending based upon margins of safety. The fundamentalborrowing and lending act… is an exchange of ‘money-now’ for ‘money-in-the-future’. This exchange takes place… in a negotiation in which the borrower demon-strates to the satisfaction of the lender—that the money of the future part of thecontract will be forthcoming… The money in the future is to cover both the interestand the repayment of the principle of the contract.” (Minsky 1993). Keynes andMinsky argued that an economic system must have both production markets (whichdetermine equilibrium prices of commodities) and also financial markets (whichdetermine prices of capital assets).

Their key point was that commodity and financial markets operated differently:“… the prices of current output (production) and capital assets (finance) are deter-mined in quite different markets.” (Minsky 1993). Commodity markets operatetoward a supply–demand equilibrium of prices. In contrast, financial markets (ofcredit-debt) operate dynamically toward a price disequilibrium (financial booms andbusts); and this disequilibrium pricing occurs in financial market because of thepractice of financial leverage.

About debt, another important concept is “leverage.” For profit, a financial systemuses debt to finance the purchase of capital assets; and profits can be increased throughfinancial leverage. Financial leverage is an increased-debt-in-the-present to optimizelarger-wealth-in-the-future. This is the financial rational of “leverage”—more “present-debt” toward greater “future wealth.” However, when present-debt is too large, toohighly leveraged, it might not create future wealth but bankruptcy. Excessive “leverage”increases the risk toward bankruptcy and not future wealth. Irving Fisher had called this

Fig. 2 Keynes/Minsky financial process

J Knowl Econ

Author's personal copy

state in a financial system of excessive leverage as “debt deflation” (Fisher 1933). LaterHyman Minsky called it “Ponzi finance” (Minsky 1986).

Although leverage is basic to financial systems, excessive leverage can break asystem. Paul McCulley nicely expressed this: “At its core, capitalism is all about risktaking. One form of risk taking is leverage. Indeed, without leverage, capitalismcould not prosper… And it is grand while the ever-larger application of leverage putsupward pressure on asset prices. There is nothing like a bull market to make geniusesout of levered dunces. … call it the Forward Minsky Journey, where stability begetsever riskier debt arrangements, until they have produced a bubble in asset prices.Then the bubble bursts…” (McCulley 2009). Leveraged “present-debt” can increase“future wealth”; but excessive leverage can lead to bankruptcy.

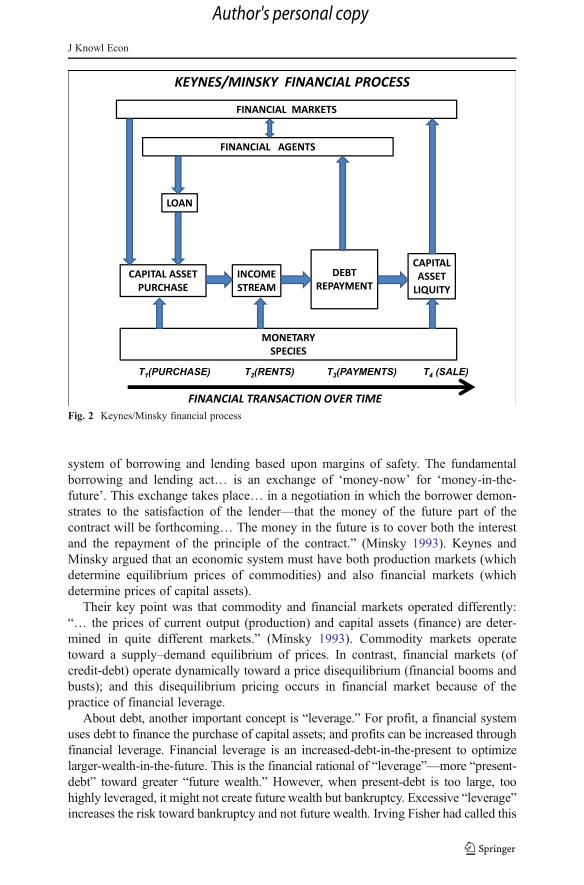

The first cross-disciplinary step in reconciling the Neo-Classical Synthesis Schoolwith the Neo-Keynesian School is, for a capital asset market, to explicitly introduce atime dimension into its supply–demand equilibrium model as shown in Fig. 3.Therein the dotted line describes how the price of a capital asset can increase overtime due to speculative investment in the assets. At time T1, an equilibrium price ofthe capital asset occurred when present-supply-equaled-present-demand. But at thistime, speculators anticipated a future increase of the price of the capital assets andbegan buying capital assets at higher prices—taking the present price to a higherfuture price, away from the equilibrium price—as time unfolded from T1 toward T2.

As time progresses, speculators continue to bid capital asset prices higher andhigher, until a financial bubble occurs. Then the financial bubble bursts at time T2.Through speculation, a financial system can move the equilibrium price of an assettoward higher and higher prices in the future as the bubble builds.

Fig. 3 Three-dimensional (price, quantity, time) supply–demand–price-equilibrium chart—over time

J Knowl Econ

Author's personal copy

While production systems can operate toward equilibrium pricing of commodities,financial systems, in contrast, can operate toward disequilibrium pricing of capitalassets, financial bubbles. A time dimension in a capital asset supply–demand curvecan describe how disequilibrium prices can occur over time, diverging from equilibriumprices during a financial bubble. Because of the phenomena of financial bubbles,economic instability is seen by Neo-Keynesians as inherent to economic models ofproduction. For this reason, the Neo-Keynesian School has also been called an “endog-enous school of economics,” as they argued that financial system as indigenous toeconomic dynamics, inherently introducing instability through disequilibrium pricing infinancial bubble. They called the Neo-Classical Synthesis School an “exogenous”school of economics because they believed all instability was external to an economicsystem (of perfect markets).

Cross-Disciplinary Model of an Economic System

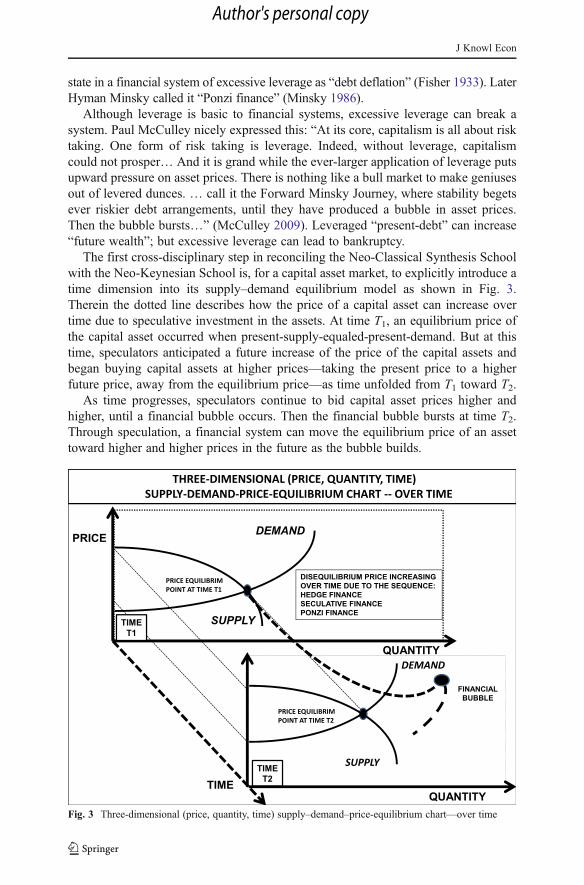

The Neo-Classical Synthesis School focused upon the production subsystem; in whichthe present price of a commodity is the key factor of control in a production subsystem.The Neo-Keynesian School focused upon a financial subsystem, in which future price ofa capital asset is the key factor of control in a financial subsystem. The modelingchallenge is to use both these economic models (theories) in a complementary frame-work. For this, one can methodologically use a “meta-framework,” such as in societaldynamics theory. In the meta-framework for economic system modeling, we use atopological systemsmodel of a society, in which an economy is an economic subsystem;and in the economic subsystem are production and financial sub-subsystems. The devel-opment of this societal systems model can be found in (Betz 2011).

In a societal dynamics topological model of the stasis of a society, the majorsystems in an industrialized society can be classified into four kinds of subsystems(economic, cultural, political, and technological; and these can be topologicallypresented as stacked planes, as in Fig. 4). Also traditionally in economics, an economyis composed of production, distribution, and consumption of goods and services.The production subsystem produces the goods and services from material/energyresources and financed by a financial system. These goods/services are con-sumed within a market. Thus any economic system can be partitioned into four sub-systems of production, market, finance, and resources. Therein, we can now placethe exogenous school’s model of an economy (as a production system) withinthis larger societal context—as the production subsystem of the economic system. Also,one can place the endogenous school’s model of an economy (as a financialsystem) within this larger societal context—as the financial subsystem of theeconomic plane.

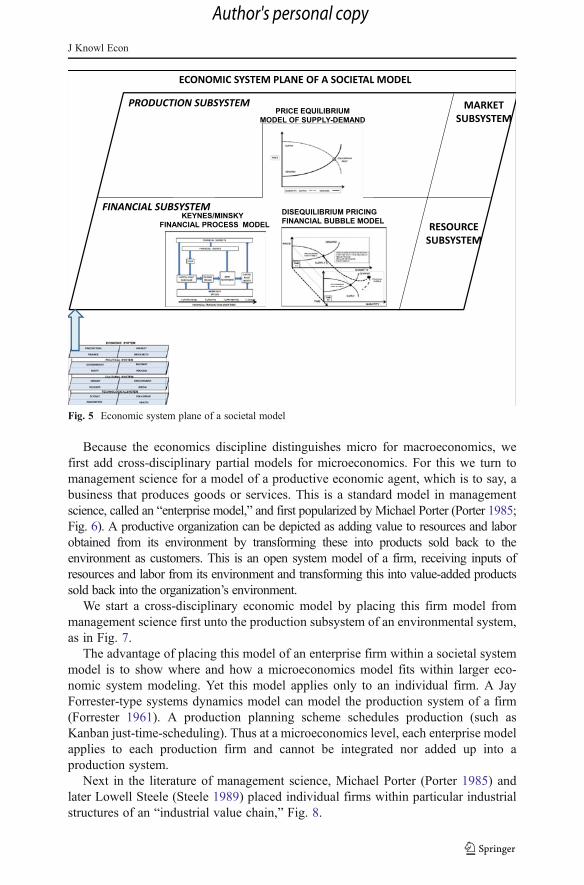

The cross-disciplinary meta-framework of societal dynamics facilitates seeing theeconomic theories (models) of two schools of economics—exogenous (Neo-ClassicalSynthesis) and endogenous (Neo-Keynesian)—as complementary within the largercontext of a societal system. Next, one can place the economic models from theeconomics literature within this societal meta-framework as Fig. 5.

What this topological meta-framework shows is how the models from the two schoolsof economics, exogenous and endogenous, relate to each other as complementary models

J Knowl Econ

Author's personal copy

of production and financial subsystems, both in the framework of a society’s economicsubsystem.

What still needs to be discussed is how data is fed into the models and whatinformation results and how information can be transmitted from one model toanother. For this, it is important to note that we are not trying to construct oneintegrated model of a whole economy. The models from the economics disciplinaryliterature do not permit this because, as we have just reviewed, some of the econo-mists themselves (particularly the Neo-Keynesian) see their models of an economy as“partial” models: (1) as modeling pricing equilibrium in commodity-productionprocesses and (2) as modeling pricing disequilibrium pricing in financial processes.What this meta-framework approach to relating models provides is an effective wayto use different partial models of several processes—without having to try to createone tightly-integrated and complete model of a situation with a complex set ofprocesses.

A modeling meta-framework assists relating partial models in a complex societalsituation.

Cross-disciplinary Model of a Production Subsystem of an Economy

To understand how to connect the partial economic models from the endogenous andexogenous schools, we will next draw upon other models from other social sciencedisciplines, aiming toward a connectable model of a societal economic subsystem—across-disciplinary economic system.

Fig. 4 Topological model of society as interacting systems of economy, politics, culture, and technology

J Knowl Econ

Author's personal copy

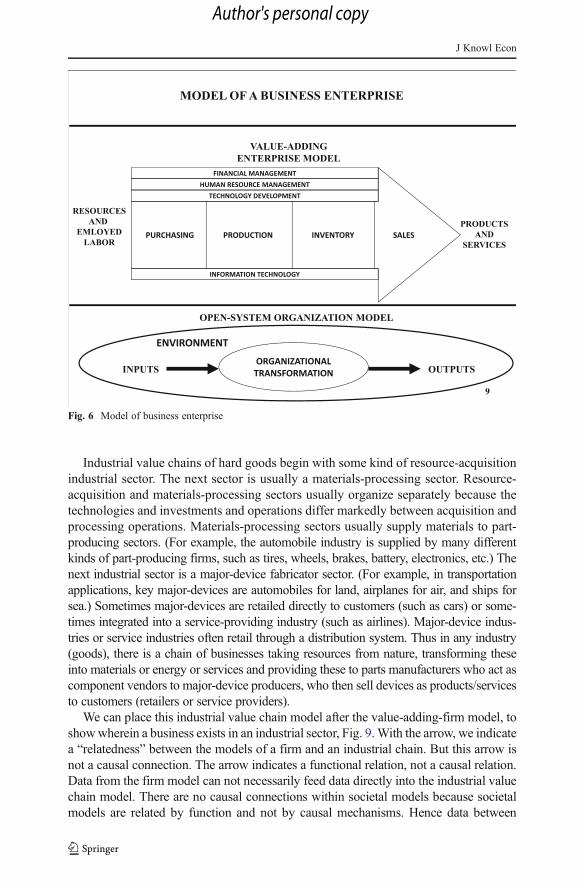

Because the economics discipline distinguishes micro for macroeconomics, wefirst add cross-disciplinary partial models for microeconomics. For this we turn tomanagement science for a model of a productive economic agent, which is to say, abusiness that produces goods or services. This is a standard model in managementscience, called an “enterprise model,” and first popularized by Michael Porter (Porter 1985;Fig. 6). A productive organization can be depicted as adding value to resources and laborobtained from its environment by transforming these into products sold back to theenvironment as customers. This is an open system model of a firm, receiving inputs ofresources and labor from its environment and transforming this into value-added productssold back into the organization’s environment.

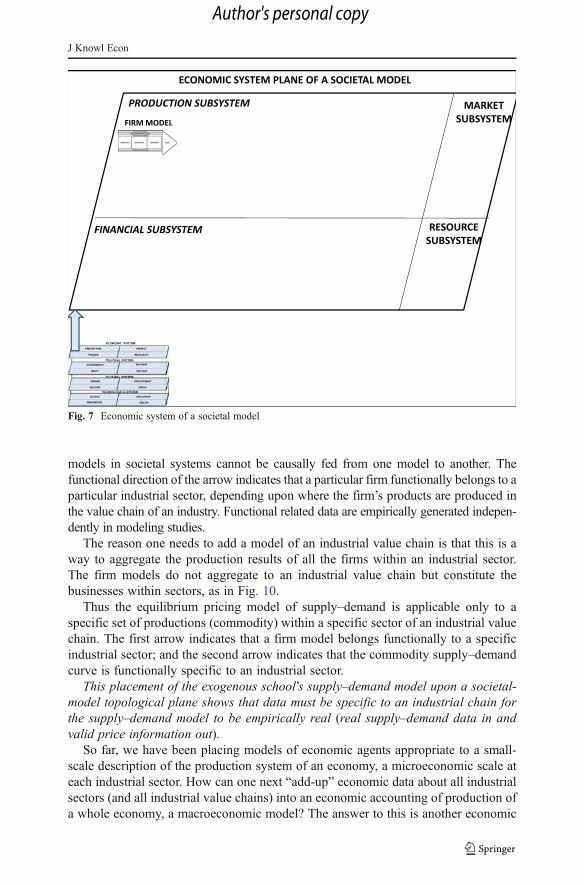

We start a cross-disciplinary economic model by placing this firm model frommanagement science first unto the production subsystem of an environmental system,as in Fig. 7.

The advantage of placing this model of an enterprise firm within a societal systemmodel is to show where and how a microeconomics model fits within larger eco-nomic system modeling. Yet this model applies only to an individual firm. A JayForrester-type systems dynamics model can model the production system of a firm(Forrester 1961). A production planning scheme schedules production (such asKanban just-time-scheduling). Thus at a microeconomics level, each enterprise modelapplies to each production firm and cannot be integrated nor added up into aproduction system.

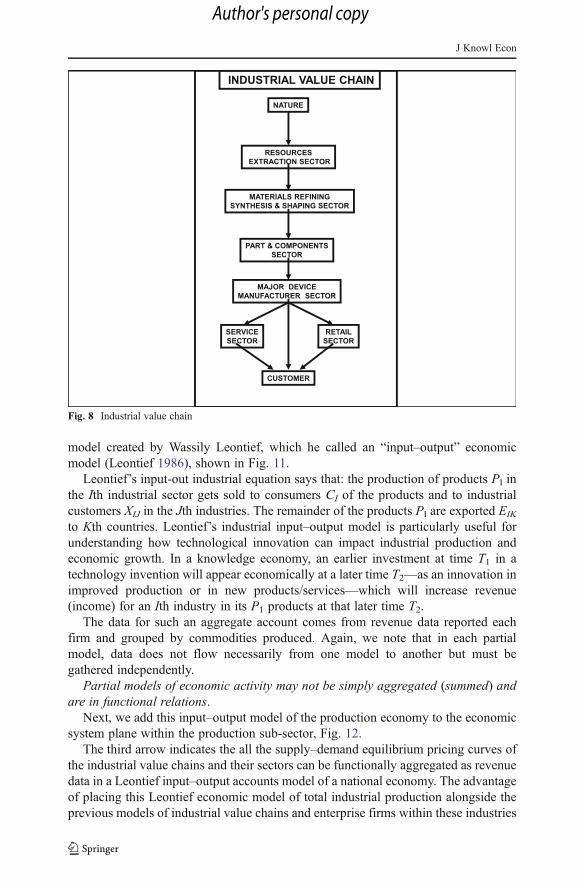

Next in the literature of management science, Michael Porter (Porter 1985) andlater Lowell Steele (Steele 1989) placed individual firms within particular industrialstructures of an “industrial value chain,” Fig. 8.

Fig. 5 Economic system plane of a societal model

J Knowl Econ

Author's personal copy

Industrial value chains of hard goods begin with some kind of resource-acquisitionindustrial sector. The next sector is usually a materials-processing sector. Resource-acquisition and materials-processing sectors usually organize separately because thetechnologies and investments and operations differ markedly between acquisition andprocessing operations. Materials-processing sectors usually supply materials to part-producing sectors. (For example, the automobile industry is supplied by many differentkinds of part-producing firms, such as tires, wheels, brakes, battery, electronics, etc.) Thenext industrial sector is a major-device fabricator sector. (For example, in transportationapplications, key major-devices are automobiles for land, airplanes for air, and ships forsea.) Sometimes major-devices are retailed directly to customers (such as cars) or some-times integrated into a service-providing industry (such as airlines). Major-device indus-tries or service industries often retail through a distribution system. Thus in any industry(goods), there is a chain of businesses taking resources from nature, transforming theseinto materials or energy or services and providing these to parts manufacturers who act ascomponent vendors to major-device producers, who then sell devices as products/servicesto customers (retailers or service providers).

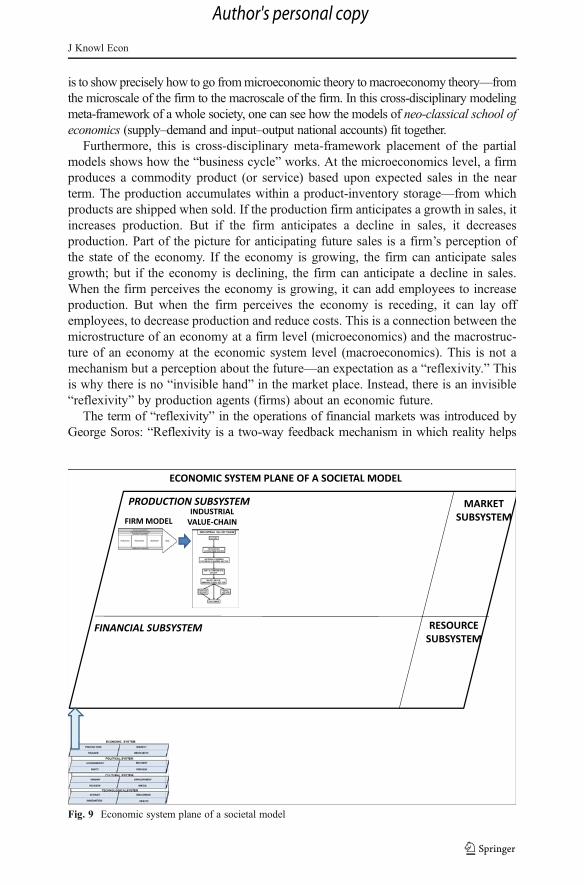

We can place this industrial value chain model after the value-adding-firm model, toshowwherein a business exists in an industrial sector, Fig. 9.With the arrow, we indicatea “relatedness” between the models of a firm and an industrial chain. But this arrow isnot a causal connection. The arrow indicates a functional relation, not a causal relation.Data from the firm model can not necessarily feed data directly into the industrial valuechain model. There are no causal connections within societal models because societalmodels are related by function and not by causal mechanisms. Hence data between

Fig. 6 Model of business enterprise

J Knowl Econ

Author's personal copy

models in societal systems cannot be causally fed from one model to another. Thefunctional direction of the arrow indicates that a particular firm functionally belongs to aparticular industrial sector, depending upon where the firm’s products are produced inthe value chain of an industry. Functional related data are empirically generated indepen-dently in modeling studies.

The reason one needs to add a model of an industrial value chain is that this is away to aggregate the production results of all the firms within an industrial sector.The firm models do not aggregate to an industrial value chain but constitute thebusinesses within sectors, as in Fig. 10.

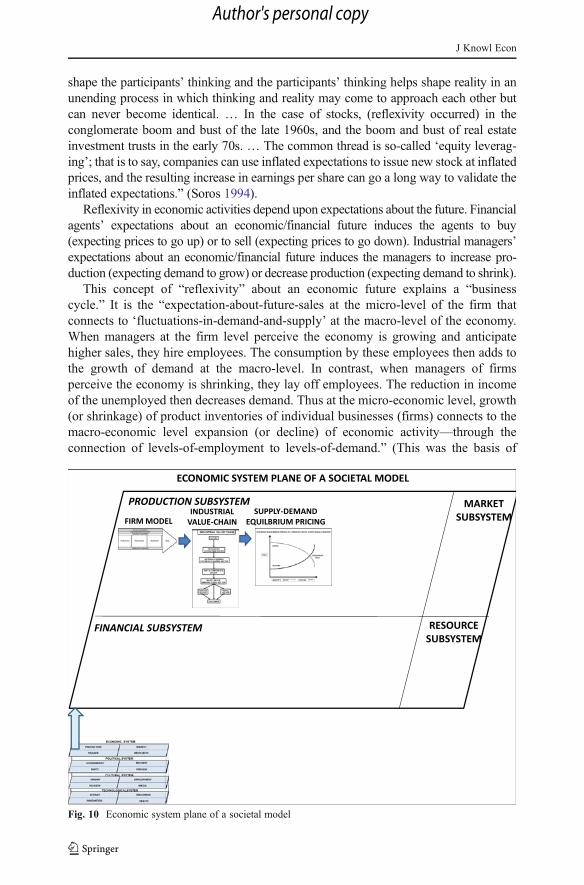

Thus the equilibrium pricing model of supply–demand is applicable only to aspecific set of productions (commodity) within a specific sector of an industrial valuechain. The first arrow indicates that a firm model belongs functionally to a specificindustrial sector; and the second arrow indicates that the commodity supply–demandcurve is functionally specific to an industrial sector.

This placement of the exogenous school’s supply–demand model upon a societal-model topological plane shows that data must be specific to an industrial chain forthe supply–demand model to be empirically real (real supply–demand data in andvalid price information out).

So far, we have been placing models of economic agents appropriate to a small-scale description of the production system of an economy, a microeconomic scale ateach industrial sector. How can one next “add-up” economic data about all industrialsectors (and all industrial value chains) into an economic accounting of production ofa whole economy, a macroeconomic model? The answer to this is another economic

Fig. 7 Economic system of a societal model

J Knowl Econ

Author's personal copy

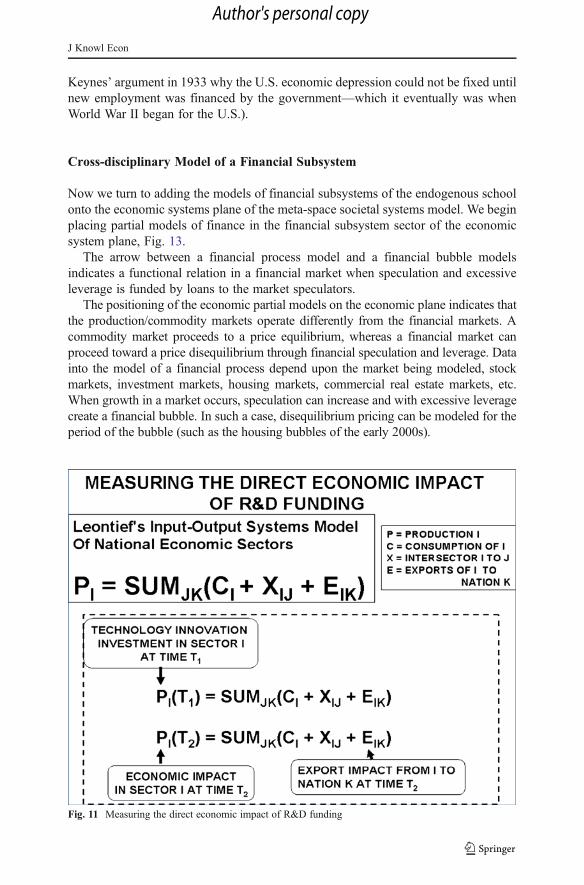

model created by Wassily Leontief, which he called an “input–output” economicmodel (Leontief 1986), shown in Fig. 11.

Leontief’s input-out industrial equation says that: the production of products PI inthe Ith industrial sector gets sold to consumers CI of the products and to industrialcustomers XIJ in the Jth industries. The remainder of the products PI are exported EIK

to Kth countries. Leontief’s industrial input–output model is particularly useful forunderstanding how technological innovation can impact industrial production andeconomic growth. In a knowledge economy, an earlier investment at time T1 in atechnology invention will appear economically at a later time T2—as an innovation inimproved production or in new products/services—which will increase revenue(income) for an Ith industry in its P1 products at that later time T2.

The data for such an aggregate account comes from revenue data reported eachfirm and grouped by commodities produced. Again, we note that in each partialmodel, data does not flow necessarily from one model to another but must begathered independently.

Partial models of economic activity may not be simply aggregated (summed) andare in functional relations.

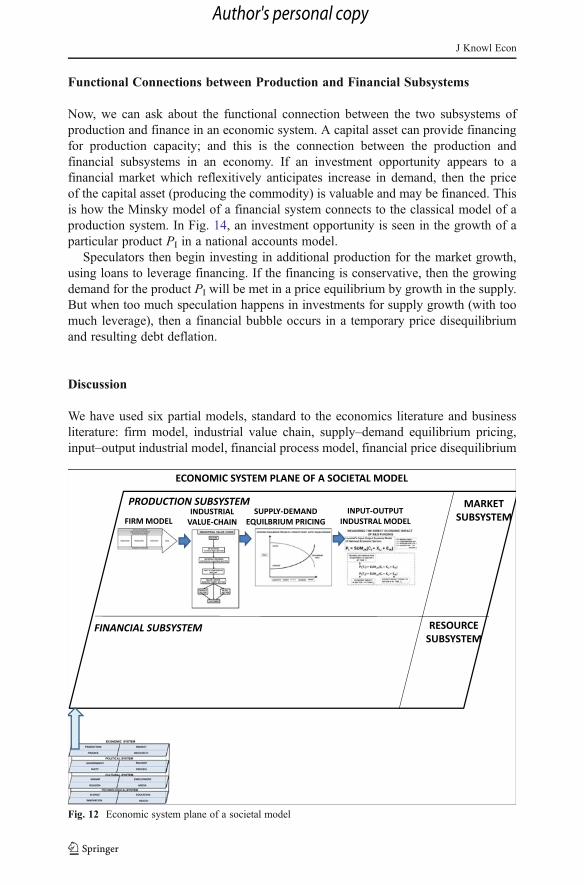

Next, we add this input–output model of the production economy to the economicsystem plane within the production sub-sector, Fig. 12.

The third arrow indicates the all the supply–demand equilibrium pricing curves ofthe industrial value chains and their sectors can be functionally aggregated as revenuedata in a Leontief input–output accounts model of a national economy. The advantageof placing this Leontief economic model of total industrial production alongside theprevious models of industrial value chains and enterprise firms within these industries

Fig. 8 Industrial value chain

J Knowl Econ

Author's personal copy

is to show precisely how to go frommicroeconomic theory tomacroeconomy theory—fromthe microscale of the firm to the macroscale of the firm. In this cross-disciplinary modelingmeta-framework of a whole society, one can see how the models of neo-classical school ofeconomics (supply–demand and input–output national accounts) fit together.

Furthermore, this is cross-disciplinary meta-framework placement of the partialmodels shows how the “business cycle” works. At the microeconomics level, a firmproduces a commodity product (or service) based upon expected sales in the nearterm. The production accumulates within a product-inventory storage—from whichproducts are shipped when sold. If the production firm anticipates a growth in sales, itincreases production. But if the firm anticipates a decline in sales, it decreasesproduction. Part of the picture for anticipating future sales is a firm’s perception ofthe state of the economy. If the economy is growing, the firm can anticipate salesgrowth; but if the economy is declining, the firm can anticipate a decline in sales.When the firm perceives the economy is growing, it can add employees to increaseproduction. But when the firm perceives the economy is receding, it can lay offemployees, to decrease production and reduce costs. This is a connection between themicrostructure of an economy at a firm level (microeconomics) and the macrostruc-ture of an economy at the economic system level (macroeconomics). This is not amechanism but a perception about the future—an expectation as a “reflexivity.” Thisis why there is no “invisible hand” in the market place. Instead, there is an invisible“reflexivity” by production agents (firms) about an economic future.

The term of “reflexivity” in the operations of financial markets was introduced byGeorge Soros: “Reflexivity is a two-way feedback mechanism in which reality helps

Fig. 9 Economic system plane of a societal model

J Knowl Econ

Author's personal copy

shape the participants’ thinking and the participants’ thinking helps shape reality in anunending process in which thinking and reality may come to approach each other butcan never become identical. … In the case of stocks, (reflexivity occurred) in theconglomerate boom and bust of the late 1960s, and the boom and bust of real estateinvestment trusts in the early 70s. … The common thread is so-called ‘equity leverag-ing’; that is to say, companies can use inflated expectations to issue new stock at inflatedprices, and the resulting increase in earnings per share can go a long way to validate theinflated expectations.” (Soros 1994).

Reflexivity in economic activities depend upon expectations about the future. Financialagents’ expectations about an economic/financial future induces the agents to buy(expecting prices to go up) or to sell (expecting prices to go down). Industrial managers’expectations about an economic/financial future induces the managers to increase pro-duction (expecting demand to grow) or decrease production (expecting demand to shrink).

This concept of “reflexivity” about an economic future explains a “businesscycle.” It is the “expectation-about-future-sales at the micro-level of the firm thatconnects to ‘fluctuations-in-demand-and-supply’ at the macro-level of the economy.When managers at the firm level perceive the economy is growing and anticipatehigher sales, they hire employees. The consumption by these employees then adds tothe growth of demand at the macro-level. In contrast, when managers of firmsperceive the economy is shrinking, they lay off employees. The reduction in incomeof the unemployed then decreases demand. Thus at the micro-economic level, growth(or shrinkage) of product inventories of individual businesses (firms) connects to themacro-economic level expansion (or decline) of economic activity—through theconnection of levels-of-employment to levels-of-demand.” (This was the basis of

Fig. 10 Economic system plane of a societal model

J Knowl Econ

Author's personal copy

Keynes’ argument in 1933 why the U.S. economic depression could not be fixed untilnew employment was financed by the government—which it eventually was whenWorld War II began for the U.S.).

Cross-disciplinary Model of a Financial Subsystem

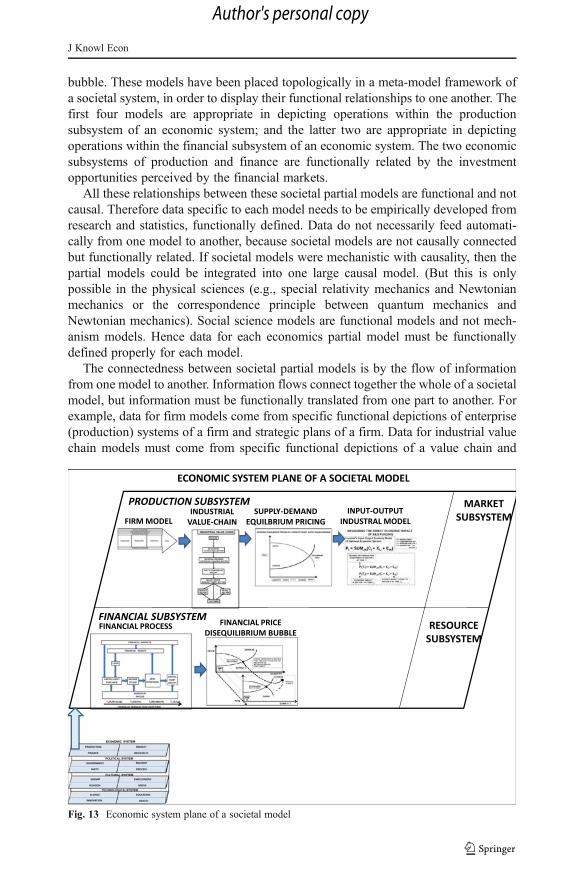

Now we turn to adding the models of financial subsystems of the endogenous schoolonto the economic systems plane of the meta-space societal systems model. We beginplacing partial models of finance in the financial subsystem sector of the economicsystem plane, Fig. 13.

The arrow between a financial process model and a financial bubble modelsindicates a functional relation in a financial market when speculation and excessiveleverage is funded by loans to the market speculators.

The positioning of the economic partial models on the economic plane indicates thatthe production/commodity markets operate differently from the financial markets. Acommodity market proceeds to a price equilibrium, whereas a financial market canproceed toward a price disequilibrium through financial speculation and leverage. Datainto the model of a financial process depend upon the market being modeled, stockmarkets, investment markets, housing markets, commercial real estate markets, etc.When growth in a market occurs, speculation can increase and with excessive leveragecreate a financial bubble. In such a case, disequilibrium pricing can be modeled for theperiod of the bubble (such as the housing bubbles of the early 2000s).

Fig. 11 Measuring the direct economic impact of R&D funding

J Knowl Econ

Author's personal copy

Functional Connections between Production and Financial Subsystems

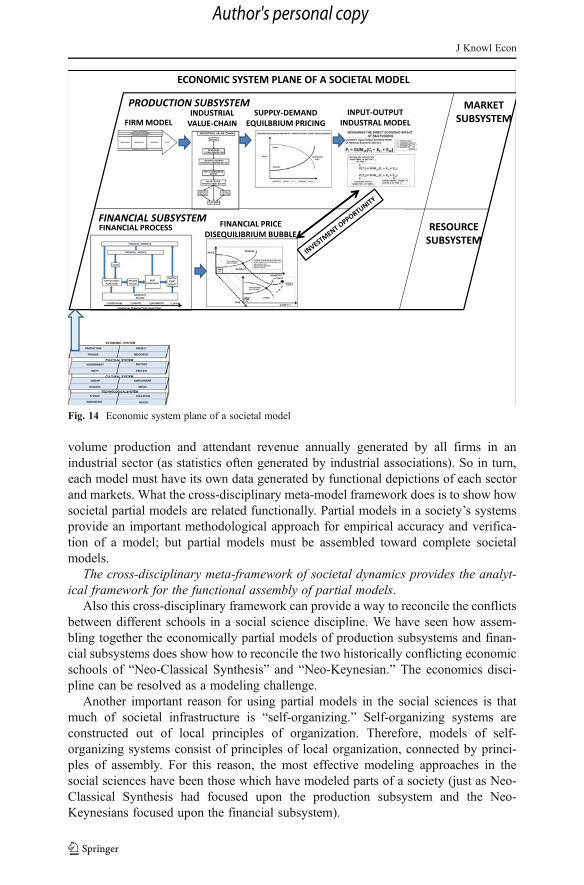

Now, we can ask about the functional connection between the two subsystems ofproduction and finance in an economic system. A capital asset can provide financingfor production capacity; and this is the connection between the production andfinancial subsystems in an economy. If an investment opportunity appears to afinancial market which reflexitively anticipates increase in demand, then the priceof the capital asset (producing the commodity) is valuable and may be financed. Thisis how the Minsky model of a financial system connects to the classical model of aproduction system. In Fig. 14, an investment opportunity is seen in the growth of aparticular product PI in a national accounts model.

Speculators then begin investing in additional production for the market growth,using loans to leverage financing. If the financing is conservative, then the growingdemand for the product PI will be met in a price equilibrium by growth in the supply.But when too much speculation happens in investments for supply growth (with toomuch leverage), then a financial bubble occurs in a temporary price disequilibriumand resulting debt deflation.

Discussion

We have used six partial models, standard to the economics literature and businessliterature: firm model, industrial value chain, supply–demand equilibrium pricing,input–output industrial model, financial process model, financial price disequilibrium

Fig. 12 Economic system plane of a societal model

J Knowl Econ

Author's personal copy

bubble. These models have been placed topologically in a meta-model framework ofa societal system, in order to display their functional relationships to one another. Thefirst four models are appropriate in depicting operations within the productionsubsystem of an economic system; and the latter two are appropriate in depictingoperations within the financial subsystem of an economic system. The two economicsubsystems of production and finance are functionally related by the investmentopportunities perceived by the financial markets.

All these relationships between these societal partial models are functional and notcausal. Therefore data specific to each model needs to be empirically developed fromresearch and statistics, functionally defined. Data do not necessarily feed automati-cally from one model to another, because societal models are not causally connectedbut functionally related. If societal models were mechanistic with causality, then thepartial models could be integrated into one large causal model. (But this is onlypossible in the physical sciences (e.g., special relativity mechanics and Newtonianmechanics or the correspondence principle between quantum mechanics andNewtonian mechanics). Social science models are functional models and not mech-anism models. Hence data for each economics partial model must be functionallydefined properly for each model.

The connectedness between societal partial models is by the flow of informationfrom one model to another. Information flows connect together the whole of a societalmodel, but information must be functionally translated from one part to another. Forexample, data for firm models come from specific functional depictions of enterprise(production) systems of a firm and strategic plans of a firm. Data for industrial valuechain models must come from specific functional depictions of a value chain and

Fig. 13 Economic system plane of a societal model

J Knowl Econ

Author's personal copy

volume production and attendant revenue annually generated by all firms in anindustrial sector (as statistics often generated by industrial associations). So in turn,each model must have its own data generated by functional depictions of each sectorand markets. What the cross-disciplinary meta-model framework does is to show howsocietal partial models are related functionally. Partial models in a society’s systemsprovide an important methodological approach for empirical accuracy and verifica-tion of a model; but partial models must be assembled toward complete societalmodels.

The cross-disciplinary meta-framework of societal dynamics provides the analyt-ical framework for the functional assembly of partial models.

Also this cross-disciplinary framework can provide a way to reconcile the conflictsbetween different schools in a social science discipline. We have seen how assem-bling together the economically partial models of production subsystems and finan-cial subsystems does show how to reconcile the two historically conflicting economicschools of “Neo-Classical Synthesis” and “Neo-Keynesian.” The economics disci-pline can be resolved as a modeling challenge.

Another important reason for using partial models in the social sciences is thatmuch of societal infrastructure is “self-organizing.” Self-organizing systems areconstructed out of local principles of organization. Therefore, models of self-organizing systems consist of principles of local organization, connected by princi-ples of assembly. For this reason, the most effective modeling approaches in thesocial sciences have been those which have modeled parts of a society (just as Neo-Classical Synthesis had focused upon the production subsystem and the Neo-Keynesians focused upon the financial subsystem).

Fig. 14 Economic system plane of a societal model

J Knowl Econ

Author's personal copy

And of course, all scientific theory must be grounded in experience. The use ofsocietal dynamics theory as an analytic framework for historical studies can enablethe direct comparison between economic history (the empiricism of economics) andeconomic theory (the rationalism of economics). By looking at history of the theo-retical conflict in economics, we have shown how societal dynamics can provide ameta-framework for historical studies.

We note that for the meta-framework of economic modeling, we have placed modelsonto a topological framework, using the mathematical topic of topology, connectivity.Quantitative expression in economics has made significant progress using calculus, butnot in necessarily as much progress in expressing institutional insights about economicprocesses. The use of topology, in addition to calculus, expands the mathematical powerof economic theory. Again, we emphasize that the application of topology to socialscience theory is functional connectivity and not geometric connectivity.

The limit of this research has been to rely upon standard theories and modelsdeveloped within the economics discipline, supplemented by some models from thebusiness literature. The objective was to show how to relate together these modelswithin a larger societal modeling framework. It is hoped that a larger cross-disciplinary meta-framework (societal dynamics) may stimulate more cross-disciplinaryresearch across the social sciences, so that partial models better fit reality. And to avoid inthe future, having financial reality distorted to fit the disciplinary convenience of someregulators—as did happen in the global financial collapse of 2007–2008.

References

Bernanke, B. S. (2007). “Regulation and Financial Innovation”, 2007 Financial Markets Conference, SeaIsland, Georgia, May 15. Federal Reserve Bank of Atlanta (Bernanke, 2007).

Betz, F. (2011). Societal dynamics. New York: Springer.Betz, F. (2012). Control in knowledge economies. Journal of Knowledge Economy. doi:10.1007/s13132-012-0100-0.Davies, H. ( 2012). Economics i Denial About Its Academic Merit. The Korea Herald, August 27.Fisher, I. (1933). The debt-deflation theory of the great depression. Econometrica, October 1933.Forrester, J. (1961). Industrial dynamics. Waltham: Pegasus Communications.Giles, C. (2010). Financial crisis exposed flaws in economics. Financial Times, April 10.Krugman, P. (2009). The B Word. The New York Times, March 17.Leontief, W. (1986). Input–output economics (2nd ed.). New York: Oxford University Press.McCulley, P. (2009). “ Global Central Bank Focus”, Comments Before the Money Marketeers Club, April,

“Comments Before the Money Marketeers Club”, PIMCO http://web.archive.org/web/20100206185224/http://www.pimco.com/LeftNav/Featured+Market+Commentary/FF/2009/Global+Central+Bank+Focus+April+2009+Money+Marketeers+Solitaire+McCulley.htm. Accessed 2012.

Minsky, H. P. (1975). John Maynard Keynes, McGraw Hill (reprint 2000, originally published by ColumbiaUniversity Press in 1975).

Minsky, H. P. (1986). Stabilizing on unstable economy. New York: McGraw-Hill.Minsky, H. (1993). “Comment on Ben Bernanke, ‘Credit in the Macro-economy’” Hyman P. Minsky

Archive, Paper 361 (http://digitalcommons.bard.edu/hm_archive/361)Porter, M. (1985). Competitive strategy. New York: The Free Press.Steele, L. W. (1989). Managing technology. New York: McGraw-Hill.Soros, G. (1994). The theory of reflexivity. Speech delivered April 26, 1994 to the MIT Department of

Economics World Economy Laboratory Conference Washington, D.C.Whalen, C. J. (2012). Post-Keynesian institutionalism after the great recession. Working Paper No. 724,

Levy Economics Institute of Bard College (http://www.leveyinstitute.org).

J Knowl Econ

Author's personal copy