directory of colonias located in texas - novoco.com of colonias located in texas ... 2009 counties...

TRANSCRIPT

Directory of Colonias Located in Texas This section features a comprehensive listing of all colonias located within Texas' border with Mexico. Colonias are listed alphabetically within the county in which it exists.

Brewster Hidalgo PresidioBrooks Hudspeth ReevesCameron Jeff Davis StarrCulberson Jim Hogg TerrellDimmit Kinney UvaldeDuvall La Salle Val VerdeEdwards Maverick WebbEl Paso Nueces WillacyFrio Pecos Zapata

2009 Counties Allowable for Evaporative Cooler Use

Andrews Garza Motley Armstrong Glasscock Nolan Bailey Gray Ochiltree Borden Hale Oldham Brewster Hall Parmer Briscoe Hansford Pecos Carson Hardeman Potter Castro Hartley Presidio Childress Haskell Randall Cochran Hemphill Reagan Coke Hockley Reeves Collinsworth Howard Roberts Concho Hudspeth Runnels Cottle Hutchinson Schleicher Crane Irion Scurry Crockett Jeff Davis Sherman Crosby Jones Sterling Culberson Kent Stonewall Dallam King Sutton Dawson Knox Swisher Deaf Smith Lamb Taylor Dickens Lipscomb Terry Donley Lubbock Tom Green Ector Loving Upton El Paso Lynn Val Verde Fisher Martin Ward Floyd Midland Wheeler Foard Mitchell Winkler Gaines Moore Yoakum

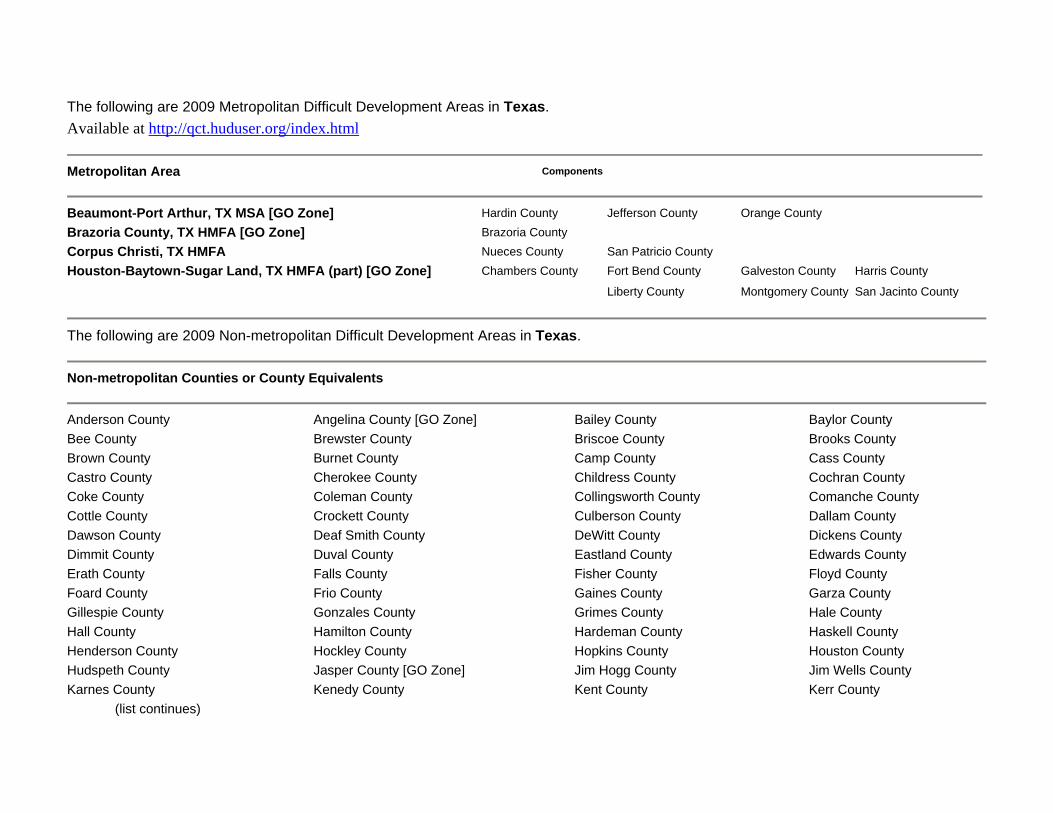

The following are 2009 Metropolitan Difficult Development Areas in Texas. Available at http://qct.huduser.org/index.html

Metropolitan Area Components

Beaumont-Port Arthur, TX MSA [GO Zone] Hardin County Jefferson County Orange County

Brazoria County, TX HMFA [GO Zone] Brazoria County Corpus Christi, TX HMFA Nueces County San Patricio County

Houston-Baytown-Sugar Land, TX HMFA (part) [GO Zone] Chambers County Fort Bend County Galveston County Harris County

Liberty County Montgomery County San Jacinto County

The following are 2009 Non-metropolitan Difficult Development Areas in Texas.

Non-metropolitan Counties or County Equivalents

Anderson County Angelina County [GO Zone] Bailey County Baylor County Bee County Brewster County Briscoe County Brooks County Brown County Burnet County Camp County Cass County Castro County Cherokee County Childress County Cochran County Coke County Coleman County Collingsworth County Comanche County Cottle County Crockett County Culberson County Dallam County Dawson County Deaf Smith County DeWitt County Dickens County Dimmit County Duval County Eastland County Edwards County Erath County Falls County Fisher County Floyd County Foard County Frio County Gaines County Garza County Gillespie County Gonzales County Grimes County Hale County Hall County Hamilton County Hardeman County Haskell County Henderson County Hockley County Hopkins County Houston County Hudspeth County Jasper County [GO Zone] Jim Hogg County Jim Wells County Karnes County Kenedy County

Kent County Kerr County

(list continues)

Kimble County Kinney County Kleberg County Knox County La Salle County Lamar County Lamb County Leon County Limestone County Llano County Lynn County Madison County Marion County Martin County Maverick County McCulloch County Menard County Mills County Mitchell County Montague County Morris County Motley County Nacogdoches County [GO Zone] Navarro County Newton County [GO Zone] Nolan County Palo Pinto County Parmer County Pecos County Polk County [GO Zone] Presidio County Real County Red River County Reeves County Refugio County Runnels County Sabine County [GO Zone] San Augustine County [GO Zone] San Saba County Shelby County [GO Zone] Starr County Stephens County Stonewall County Swisher County Terrell County Terry County Throckmorton County Titus County Trinity County [GO Zone] Tyler County [GO Zone] Uvalde County Val Verde County Walker County [GO Zone] Washington County Willacy County Winkler County Zapata County Zavala County

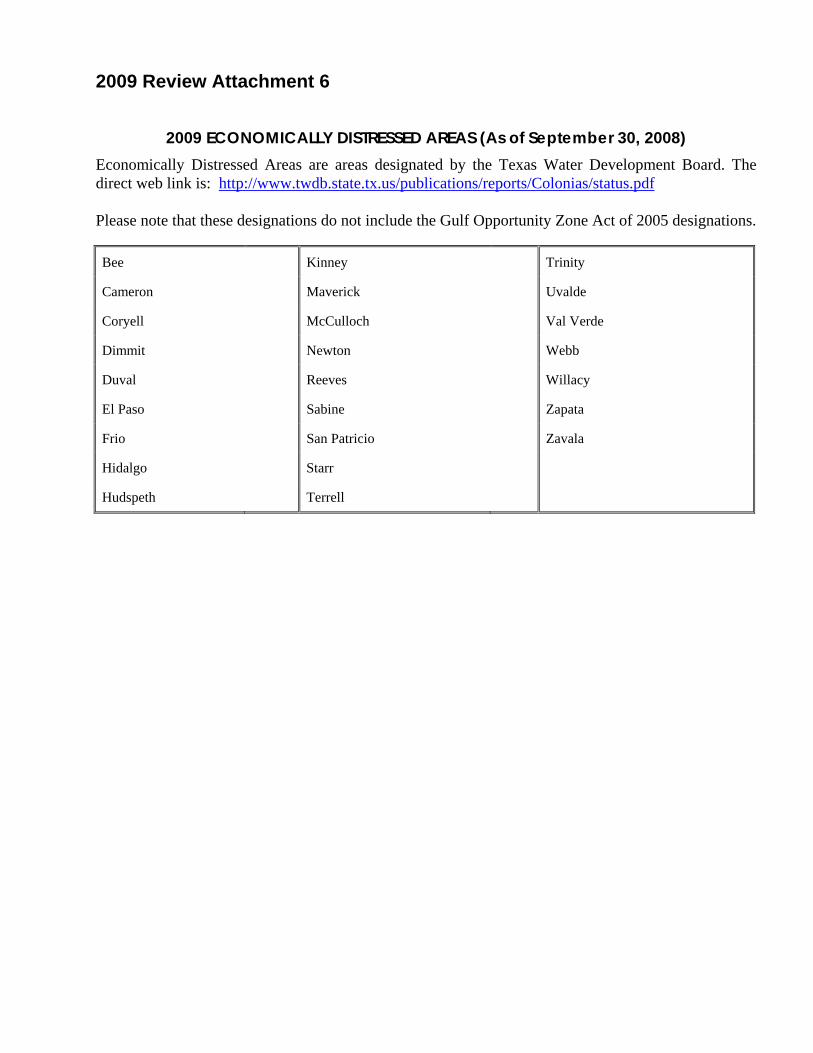

2009 Review Attachment 6

2009 ECONOMICALLY DISTRESSED AREAS (As of September 30, 2008) Economically Distressed Areas are areas designated by the Texas Water Development Board. The direct web link is: http://www.twdb.state.tx.us/publications/reports/Colonias/status.pdf Please note that these designations do not include the Gulf Opportunity Zone Act of 2005 designations.

Bee Kinney Trinity

Cameron Maverick Uvalde

Coryell McCulloch Val Verde

Dimmit Newton Webb

Duval Reeves Willacy

El Paso Sabine Zapata

Frio San Patricio Zavala

Hidalgo Starr

Hudspeth Terrell

2009 List of Counties Eligible for Points Pursuant to §49.9(i)(10) of the 2009 QAP, Declared Disaster Areas

Anderson Collingsworth Glasscock Kaufman Moore Somervell Andrews Colorado Goliad Kendall Morris Starr Angelina Comal Gonzales Kenedy Motley Stephens Aransas Comanche Gray Kent Nacogdoches Sterling Archer Concho Grayson Kerr Navarro Stonewall Armstrong Cooke Gregg Kimble Newton Sutton Atascosa Coryell Grimes King Nolan Swisher Austin Cottle Guadalupe Kinney Nueces Tarrant Bailey Crane Hale Kleberg Ochiltree Taylor Bandera Crockett Hall Knox Oldham Terrell Bastrop Crosby Hamilton La Salle Orange Terry Baylor Culberson Hansford Lamar Palo Pinto ThrockmortonBee Dallam Hardeman Lamb Panola Titus Bell Dallas Hardin Lampasas Parker Tom Green Bexar Dawson Harris Lavaca Parmer Travis Blanco Deaf Smith Harrison Lee Pecos Trinity Borden Delta Hartley Leon Polk Tyler Bosque Denton Haskell Liberty Potter Upshur Bowie DeWitt Hays Limestone Presidio Upton Brazoria Dickens Hemphill Lipscomb Rains Uvalde Brazos Dimmit Henderson Live Oak Randall Val Verde Brewster Donley Hidalgo Llano Reagan Van Zandt Briscoe Duval Hill Loving Real Victoria Brooks Eastland Hockley Lubbock Red River Walker Brown Ector Hood Lynn Reeves Waller Burleson Edwards Hopkins Madison Refugio Ward Burnet El Paso Houston Marion Roberts Washington Caldwell Ellis Howard Martin Robertson Webb Calhoun Erath Hudspeth Mason Rockwall Wharton Callahan Falls Hunt Matagorda Runnels Wheeler Cameron Fannin Hutchinson Maverick Rusk Wichita Camp Fayette Irion McCulloch Sabine Wilbarger Carson Fisher Jack McLennan San Augustine Willacy Cass Floyd Jackson McMullen San Jacinto Williamson Castro Foard Jasper Medina San Patricio Wilson Chambers Fort Bend Jeff Davis Menard San Saba Winkler Cherokee Franklin Jefferson Midland Schleicher Wise Childress Freestone Jim Hogg Milam Scurry Wood Clay Frio Jim Wells Mills Shackelford Yoakum Cochran Gaines Johnson Mitchell Shelby Young Coke Galveston Jones Montague Sherman Zapata Coleman Garza Karnes Montgomery Smith Zavala Collin Gillespie

Previously Approved Local Political Subdivisions (Governmental Instrumentalities) Pursuant to §49.9(i)(5) of the 2009 QAP

Amarillo HFC Arlington Housing Finance Corporation Austin HFC Bexar County HFC Borger Economic Development Corporation Brownsville HFC Brownsville Housing Authority Cameron County Housing Authority Capital Area HFC City of Alton Development Corporation City of San Juan Housing Authority Cross Plains EDC Dallas Housing Authority Deep East Texas Council of Governments (for Nacogdoches and Jasper) East Texas HFC (for Cherokee County) El Paso Housing Finance Corporation El Paso PHA Fort Bend Community Development Corporation Fort Bend County HFC Fort Worth HFC Georgetown Housing Authority Harris County HFC Heart of Texas HFC Hidalgo County UCP Housing Authority of Odessa Housing Authority of the County of Hidalgo, Texas Houston HFC Jasper Economic Development Corporation Jefferson County HFC Kerrville Economic Improvement Corporation Kingsville PHA Lubbock PHA McAllen Housing Authority Mercedes Housing Authority Mesquite Housing Finance Corporation Montgomery County Community Development Nacogdoches PHA Nortex HFC Northeast Texas Housing Finance Pampa Economic Development

Panhandle Region HFC Pharr Housing Authority San Antonio Housing Authority San Marcos Housing Authority Southeast Texas HFC Tarrant County Community Development Corporation Tarrant County HFC Temple EDC Texas City Housing Authority Travis County Housing Authority Victoria Housing Authority Weslaco Housing Authority

2009 IRS SECTION 42(d)(5)(B) QUALIFIED CENSUS TRACTS (2000 Census Data; OMB Metropolitan Area Definitions, December 5, 2005)

Available at http://qct.huduser.org/index.html

STATE: Texas COUNTY OR COUNTY EQUIVALENT TRACT TRACT TRACT

TRACT

TRACT

TRACT

TRACT

TRACT

TRACT

TRACT

TRACT

TRACT

Anderson County 9505.00 9507.00

Angelina County 5.00 6.00

Atascosa County 9605.00

Bee County 9504.00 9505.00 9506.00

Bell County 207.01 207.02 208.00 209.00 216.02 235.00

Bexar County 1101.00 1102.00 1103.00 1105.00 1106.00 1107.00 1108.00 1109.00 1110.00 1202.00 1205.02 1214.04

1301.00 1302.00 1303.00 1304.00 1305.00 1306.00 1307.00 1308.00 1309.00 1311.00 1312.00 1402.00

1410.00 1411.00 1501.00 1503.00 1504.00 1505.01 1505.02 1507.00 1508.00 1511.00 1514.00 1519.00

1520.00 1601.00 1605.00 1606.00 1607.01 1607.02 1609.00 1610.00 1613.01 1613.02 1615.01 1616.00

1701.01 1701.02 1702.00 1703.00 1704.01 1704.02 1705.00 1707.00 1708.00 1709.00 1710.00 1711.00

1712.00 1713.00 1714.00 1715.00 1716.00 1804.00 1805.01 1805.04 1808.00 1818.06 1901.00 1903.00

1905.02 1907.00 1910.04

Bowie County 104.00 105.00 106.00 108.00

Brazoria County 6643.00

Brazos County 13.01 13.03 14.00 15.00 16.03 16.04 17.00

Brewster County 9504.00

Brooks County 9502.00

Brown County 9506.00 9507.00 9508.00

Caldwell County 9602.00 9607.00

Cameron County 109.00 119.03 123.03 124.03 126.09 126.10 131.06 132.03 132.06 132.07 133.07 134.01

134.02 137.00 138.01 138.02 139.01 139.02 139.03 140.01 140.02

Camp County 9502.00

Cherokee County 9504.00 9505.00 9507.00

Cochran County 9501.00

Collin County 309.00 319.00

Cooke County 9904.00 9905.00

Crosby County 9503.00

Culberson County 9502.00

Dallas County 4.01 4.03 4.05 6.01 9.00 12.04 14.00 15.02 15.03 15.04 16.00 20.00

21.00 22.00 24.00 25.00 27.01 27.02 29.00 32.01 33.00 34.00 35.00 37.00

38.00 39.01 39.02 40.00 41.00 43.00 46.00 47.00 48.00 49.00 50.00 52.00

55.00 56.00 57.00 59.02 60.01 60.02 64.00 67.00 69.00 72.01 72.02 78.15

78.18 78.19 84.00 86.03 86.04 87.01 87.03 87.04 87.05 88.01 88.02 89.00

90.00 91.03 91.05 92.02 93.01 93.03 93.04 96.10 98.02 98.04 99.00 100.00

101.01 101.02 102.00 104.00 105.00 106.01 106.02 107.01 107.04 108.01 108.02 109.01

109.02 111.05 114.01 114.02 115.00 118.00 120.00 122.08 122.10 122.11 123.02 137.13

146.02 149.01 155.00 159.00 161.00 166.05 169.01 182.04 190.13 192.09 199.00 Deaf Smith County 9505.00

Delta County 9502.00

Denton County 206.01 207.00 208.00 209.00 210.00 211.00 212.00

DeWitt County 9702.00

Dimmit County 9501.00 9502.00 9503.00

Duval County 9501.00 9503.00 9504.00

Ector County 3.00 7.00 12.00 14.00 15.00 18.00 19.00

Edwards County 9501.00

Ellis County 604.00

El Paso County 2.05 3.01 4.04 8.00 12.03 14.00 16.00 17.00 18.00 19.00 20.00 21.00

22.01 22.02 28.00 29.00 30.00 32.00 35.02 36.02 37.02 39.01 39.02 39.03

41.03 41.05 104.03 105.01 105.02 105.03 105.04

Falls County 9903.00 9904.00

Floyd County 9506.00

Fort Bend County 6749.00 6750.00

Frio County 9502.00 9503.00

Galveston County 7222.00 7224.00 7240.00 7243.00 7244.00 7245.00 7246.00 7247.00 7251.00 7252.00 7254.00 Gonzales County 9903.00

Gray County 9506.00 9507.00 9508.00

Grayson County 2.00 16.01

Gregg County 11.00 12.00 13.00 14.00 15.00

Hale County 9501.00 9502.00

Hall County 9504.00

Harris County 1000.00 2102.00 2103.00 2104.00 2105.00 2107.00 2108.00 2109.00 2110.00 2111.00 2112.00 2113.00

2114.00 2115.00 2116.00 2117.00 2118.00 2119.00 2120.00 2121.00 2201.00 2202.00 2203.00 2204.00

2205.00 2206.00 2207.00 2208.00 2209.00 2210.00 2213.00 2214.00 2215.00 2218.00 2219.00 2220.00

2221.00 2225.00 2226.00 2227.00 2230.00 2301.00 2302.00 2303.00 2304.00 2305.00 2306.00 2307.00

2308.00 2309.00 2310.00 2311.00 2312.00 2313.00 2315.00 2317.00 2319.00 2327.00 2331.00 2336.00

2337.00 2401.00 2402.00 2405.00 2406.00 2545.00 3101.00 3102.00 3104.00 3105.00 3106.00 3107.00

3108.00 3109.00 3110.00 3111.00 3112.00 3114.00 3115.00 3116.00 3117.00 3118.00 3119.00 3120.00

3122.00 3123.00 3124.00 3125.00 3127.00 3128.00 3129.00 3130.00 3133.00 3134.00 3135.00 3136.00

3137.00 3138.00 3202.00 3203.00 3206.00 3215.00 3220.00 3221.00 3223.00 3225.00 3230.00 3231.00

3235.00 3239.00 3311.00 3312.00 3313.00 3314.00 3316.00 3317.00 3318.00 3319.00 3320.00 3321.00

3322.00 3323.00 3328.00 3329.00 3334.00 4101.00 4201.00 4205.00 4212.00 4213.00 4214.00 4215.00

4216.00 4222.00 4231.00 4327.00 4328.00 4330.00 4331.00 4335.00 4526.00 4531.00 4532.00 5101.00

5102.00 5105.00 5106.00 5109.00 5206.00 5211.00 5212.00 5214.00 5216.00 5301.00 5303.00 5304.00

5305.00 5306.00 5307.00 5308.00 5318.00 5319.00 5320.00 5332.00 5333.00 5334.00 5501.00 Harrison County 204.01 204.02

Haskell County 9503.00

Hays County 102.00 103.01 103.02 105.00 107.00

Henderson County 9510.00 9512.00

Hidalgo County 205.01 207.23 211.00 213.03 219.01 222.02 225.01 226.00 231.01 237.00 241.01 241.02

241.03 241.04 242.01 245.00

Hill County 9609.00 9610.00

Hockley County 9504.00

Houston County 9503.00 9504.00

Howard County 9503.00 9504.00 9505.00

Hudspeth County 9501.00

Hunt County 9605.00 9606.00 9608.00 9609.00

Hutchinson County 9507.00

Jasper County 9503.00 9506.00

Jefferson County 1.03 6.00 7.00 9.00 10.00 12.00 16.00 19.00 20.00 22.00 23.00 24.00

25.00 26.00 51.00 53.00 54.00 59.00 61.00 62.00 63.00 64.00 66.00 70.01

101.00

Jim Hogg County 9504.00

Jim Wells County 9502.00 9505.00 9506.00 9507.00

Johnson County 1308.00 1309.00

Karnes County 9703.00 9704.00

Kaufman County 505.00

Kleberg County 202.00 203.00

Knox County 9502.00

Lamar County 5.00 6.00 8.00

La Salle County 9501.00 9502.00

Liberty County 7002.00 7006.00

Limestone County 9701.00 9704.00

Lubbock County 2.02 3.01 3.02 6.03 6.05 6.07 9.00 10.00 12.00 13.00 17.03 24.00

McLennan County 1.00 2.00 3.00 4.00 7.00 10.00 12.00 14.00 15.00 19.00 33.00 Marion County 9503.00 9504.00

Matagorda County 7301.00 7304.00

Maverick County 9501.00 9502.01 9502.02 9502.03 9503.00 9504.00 9505.00 9506.01 9506.02

Menard County 9502.00

Midland County 9.00 14.00 15.00 16.00 17.00

Montgomery County 6931.00 6934.00

Nacogdoches County 9506.00 9507.00 9508.00 9509.00 9510.00

Navarro County 9708.00

Newton County 9503.00

Nolan County 9503.00 9504.00

Nueces County 3.00 4.00 5.00 7.00 8.00 9.00 10.00 11.00 12.00 13.00 15.00 16.01

16.02 17.00 50.00 56.02 59.00

Orange County 202.00

Palo Pinto County 9808.00 9809.00

Pecos County 9503.00

Potter County 103.00 106.00 111.00 120.00 122.00 128.00 130.00 139.00 146.00 148.00 153.00 Presidio County 9502.00

Reeves County 9501.00 9502.00 9503.00 9505.00

Runnels County 9502.00

San Patricio County 108.00 113.00

Smith County 1.00 2.01 2.02 3.00 4.00 5.00 7.00

Starr County 9501.01 9501.02 9501.03 9502.01 9502.02 9504.00 9505.00 9506.00 9507.01 9507.02

Tarrant County 1002.02 1003.00 1004.00 1005.01 1009.00 1010.00 1011.00 1014.02 1014.03 1016.00 1017.00 1018.00

1020.00 1025.00 1029.00 1030.00 1031.00 1033.00 1034.00 1035.00 1036.01 1036.02 1037.01 1037.02

1038.00 1039.00 1040.00 1045.02 1045.03 1045.05 1046.01 1046.02 1046.03 1046.04 1047.00 1048.02

1052.05 1058.00 1059.00 1061.02 1062.01 1062.02 1063.00 1065.15 1065.16 1217.03 1217.04 1219.02

1222.00 1223.00 1224.00 1228.00

Taylor County 101.00 102.00 103.00 104.00 108.00 110.00 117.00 119.00 121.00

Terrell County 9501.00

Terry County 9504.00

Titus County 9506.00

Tom Green County 4.00 5.00 6.00 7.00 9.00

Travis County 2.03 3.02 4.01 4.02 5.00 6.01 6.03 6.04 7.00 8.02 8.03 8.04

9.01 9.02 10.00 18.04 18.05 18.06 18.11 18.12 21.05 21.07 21.09 21.10

21.11 21.12 22.02 23.04 23.07 23.08 23.10 23.11 23.12 23.14 23.15 23.16

24.13

Uvalde County 9505.00

Val Verde County 9502.02 9503.00 9504.00 9506.01 9506.02 9507.00

Victoria County 3.01

Walker County 7906.00 7907.00 7908.00

Waller County 6804.00

Washington County 1701.00

Webb County 3.00 4.00 5.00 6.00 9.02 12.00 13.00 18.05

Wharton County 7403.00 7407.00 Wichita County 101.00 102.00 104.00 111.00 112.00 130.00 Wilbarger County 9505.00 Willacy County 9503.00 9504.00 9505.00 9507.00 Williamson County 210.00 214.02 Zapata County 9502.00 9503.00 Zavala County 9501.00 9502.00 9503.01 9503.02

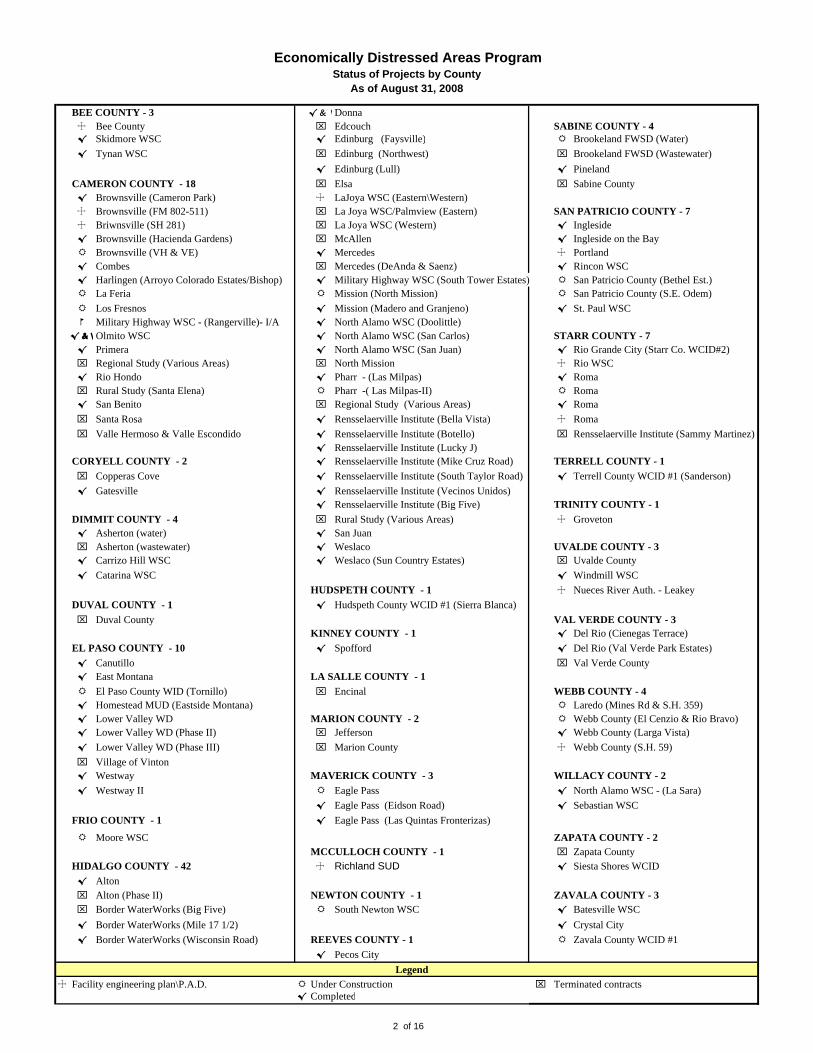

Economically Distressed Areas Program August 31, 2008

Counties with EDAP Projects in Progress or Completed: 24

Table of Contents Page Project Status Summary 2

Financial Summary 3 Project with Committed

Construction Funding By County 4

Project in Facility Planning Phase 12 Facility Plans Approved 14 Terminated Contracts 14

Economically Distressed Areas Program Status of Projects by County

As of August 31, 2008

BEE COUNTY - 3 √ & \ Donna \ Bee County ⌧ Edcouch SABINE COUNTY - 4 √ Skidmore WSC √ Edinburg (Faysville) 5 Brookeland FWSD (Water) √ Tynan WSC ⌧ Edinburg (Northwest) ⌧ Brookeland FWSD (Wastewater)

√ Edinburg (Lull) √ Pineland CAMERON COUNTY - 18 ⌧ Elsa ⌧ Sabine County √ Brownsville (Cameron Park) \ LaJoya WSC (Eastern\Western)

\ Brownsville (FM 802-511) ⌧ La Joya WSC/Palmview (Eastern) SAN PATRICIO COUNTY - 7 \ Briwnsville (SH 281) ⌧ La Joya WSC (Western) √ Ingleside √ Brownsville (Hacienda Gardens) ⌧ McAllen √ Ingleside on the Bay 5 Brownsville (VH & VE) √ Mercedes \ Portland √ Combes ⌧ Mercedes (DeAnda & Saenz) √ Rincon WSC √ Harlingen (Arroyo Colorado Estates/Bishop) √ Military Highway WSC (South Tower Estates) 5 San Patricio County (Bethel Est.) 5 La Feria 5 Mission (North Mission) 5 San Patricio County (S.E. Odem) 5 Los Fresnos √ Mission (Madero and Granjeno) √ St. Paul WSC b Military Highway WSC - (Rangerville)- I/A √ North Alamo WSC (Doolittle)

√ & \ Olmito WSC √ North Alamo WSC (San Carlos) STARR COUNTY - 7 √ Primera √ North Alamo WSC (San Juan) √ Rio Grande City (Starr Co. WCID#2) ⌧ Regional Study (Various Areas) ⌧ North Mission \ Rio WSC √ Rio Hondo √ Pharr - (Las Milpas) √ Roma ⌧ Rural Study (Santa Elena) 5 Pharr -( Las Milpas-II) 5 Roma √ San Benito ⌧ Regional Study (Various Areas) √ Roma ⌧ Santa Rosa √ Rensselaerville Institute (Bella Vista) \ Roma ⌧ Valle Hermoso & Valle Escondido √ Rensselaerville Institute (Botello) ⌧ Rensselaerville Institute (Sammy Martinez)

√ Rensselaerville Institute (Lucky J) CORYELL COUNTY - 2 √ Rensselaerville Institute (Mike Cruz Road) TERRELL COUNTY - 1 ⌧ Copperas Cove √ Rensselaerville Institute (South Taylor Road) √ Terrell County WCID #1 (Sanderson) √ Gatesville √ Rensselaerville Institute (Vecinos Unidos)

√ Rensselaerville Institute (Big Five) TRINITY COUNTY - 1 DIMMIT COUNTY - 4 ⌧ Rural Study (Various Areas) \ Groveton √ Asherton (water) √ San Juan ⌧ Asherton (wastewater) √ Weslaco UVALDE COUNTY - 3 √ Carrizo Hill WSC √ Weslaco (Sun Country Estates) ⌧ Uvalde County √ Catarina WSC √ Windmill WSC

HUDSPETH COUNTY - 1 \ Nueces River Auth. - Leakey DUVAL COUNTY - 1 √ Hudspeth County WCID #1 (Sierra Blanca) ⌧ Duval County VAL VERDE COUNTY - 3

KINNEY COUNTY - 1 √ Del Rio (Cienegas Terrace) EL PASO COUNTY - 10 √ Spofford √ Del Rio (Val Verde Park Estates) √ Canutillo ⌧ Val Verde County √ East Montana LA SALLE COUNTY - 1 5 El Paso County WID (Tornillo) ⌧ Encinal WEBB COUNTY - 4 √ Homestead MUD (Eastside Montana) 5 Laredo (Mines Rd & S.H. 359) √ Lower Valley WD MARION COUNTY - 2 5 Webb County (El Cenzio & Rio Bravo) √ Lower Valley WD (Phase II) ⌧ Jefferson √ Webb County (Larga Vista) √ Lower Valley WD (Phase III) ⌧ Marion County \ Webb County (S.H. 59) ⌧ Village of Vinton √ Westway MAVERICK COUNTY - 3 WILLACY COUNTY - 2 √ Westway II 5 Eagle Pass √ North Alamo WSC - (La Sara)

√ Eagle Pass (Eidson Road) √ Sebastian WSC FRIO COUNTY - 1 √ Eagle Pass (Las Quintas Fronterizas)

5 Moore WSC ZAPATA COUNTY - 2 MCCULLOCH COUNTY - 1 ⌧ Zapata County

HIDALGO COUNTY - 42 \ Richland SUD √ Siesta Shores WCID √ Alton ⌧ Alton (Phase II) NEWTON COUNTY - 1 ZAVALA COUNTY - 3 ⌧ Border WaterWorks (Big Five) 5 South Newton WSC √ Batesville WSC √ Border WaterWorks (Mile 17 1/2) √ Crystal City √ Border WaterWorks (Wisconsin Road) REEVES COUNTY - 1 5 Zavala County WCID #1

√ Pecos City Legend

\ Facility engineering plan\P.A.D. 5 Under Construction ⌧ Terminated contracts √ Completed

2 of 16

Code of Federal Regulations Title 24, Volume 1

Revised as of April 1, 2001 From the U.S. Government Printing Office via GPO Access

CITE: 24CFR8Page 134-141

TITLE 24--HOUSING AND URBAN DEVELOPMENT

PART 8--NONDISCRIMINATION BASED ON HANDICAP IN FEDERALLY ASSISTED PROGRAMS AND ACTIVITIES OF THE DEPARTMENT OF HOUSING AND URBAN DEVELOPMENT Table of Contents

Subpart C--Program Accessibility

Sec. 8.20 General requirement concerning program accessibility.

Except as otherwise provided in Secs. 8.21(c)(1), 8.24(a), 8.25, and 8.31, no qualified individual with handicaps shall, because a recipient's facilities are inaccessible to or unusable by individuals with handicaps, be denied the benefits of, be excluded from participation in, or otherwise be subjected to discrimination under any program or activity that receives Federal financial assistance.

Sec. 8.21 Non-housing facilities.

(a) New construction. New non-housing facilities shall be designed and constructed to be readily accessible to and usable by individuals with handicaps.

(b) Alterations to facilities. Alterations to existing non-housing facilities shall, to the maximum extent feasible, be made to be readily accessible to and usable by individuals with handicaps. For purposes of this paragraph, the phrase to the maximum extent feasible shall not be interpreted as requiring that a recipient make a non-housing facility, or element thereof, accessible if doing so would impose undue financial and administrative burdens on the operation of the recipient's program or activity.

(c) Existing non-housing facilities--(1) General. A recipient shall operate each non-housing program or activity receiving Federal financial assistance so that the program or activity, when viewed in its entirety, is readily accessible to and usable by individuals with handicaps. This paragraph does not-

(i) Necessarily require a recipient to make each of its existing non-housing facilities accessible to and usable by individuals with handicaps;

(ii) In the case of historic preservation programs or activities, require the recipient to take any action that would result in a substantial impairment of significant historic features of an historic property; or

(iii) Require a recipient to take any action that it can demonstrate would result in a fundamental alteration in the nature of its program or activity or in undue financial and administrative burdens. If an action would result in such an alteration or such burdens, the recipient shall take any action that would not result in such an alteration or such burdens but would nevertheless ensure that individuals with handicaps receive the benefits and services of the program or activity.

(2) Methods--(i) General. A recipient may comply with the requirements of this section in its programs and activities receiving Federal financial assistance through such means as location of programs or services to accessible facilities or accessible portions of facilities, assignment of aides to beneficiaries, home visits, the addition or redesign of equipment (e.g., appliances or furnishings) changes in management policies or procedures, acquisition or construction of additional facilities, or alterations to existing facilities on a selective basis, or any other methods that result in making its program or activity accessible to individuals with handicaps. A recipient is not required to make structural changes in existing facilities where other methods are effective in achieving compliance with this section. In choosing among available methods for meeting the requirements of this section, the recipient shall give priority to those methods that offer programs and activities to qualified individuals with handicaps in the most integrated setting appropriate.

ACCESSIBILITY STANDARDS UNDER 24 CFR PART 8, SUBPART C

(ii) Historic preservation programs or activities. In meeting the requirements of Sec. 8.21(c) in historic preservation programs or activities, a recipient shall give priority to methods that provide physical access to individuals with handicaps. In cases where a physical alteration to an historic property is not required because of Sec. 8.21(c)(1)(ii) or (iii), alternative methods of achieving program accessibility include using audio-visual materials and devices to depict those portions of an historic property that cannot otherwise be made accessible; assigning persons to guide individuals with handicaps into or through portions of historic properties that cannot otherwise be made accessible; or adopting other innovative methods.

(3) Time period for compliance. The recipient shall comply with the obligations established under this section within sixty days of July 11, 1988, except that where structural changes in facilities are undertaken, such changes shall be made within three years of July 11, 1988, but in any event as expeditiously as possible.

(4) Transition plan. If structural changes to non-housing facilities will be undertaken to achieve program accessibility, a recipient shall develop, within six months of July 11, 1988, a transition plan setting forth the steps necessary to complete such changes. The plan shall be developed with the assistance of interested persons, including individuals with handicaps or organizations representing individuals with handicaps. A copy of the transition plan shall be made available for public inspection. The plan shall, at a minimum-

(i) Identify physical obstacles in the recipient's facilities that limit the accessibility of its programs or activities to individuals with handicaps;

(ii) Describe in details the methods that will be used to make the facilities accessible; (iii) Specify the schedule for taking the steps necessary to achieve compliance with this section and, if the

time period of the transition plan is longer than one year, identify steps that will be taken during each year of the transition period;

(iv) Indicate the official responsible for implementation of the plan; and (v) Identify the persons or groups with whose assistance the plan was prepared.

(Approved by the Office of Management and Budget under control number 2529-0034) [53 FR 20233, June 2, 1988; 53 FR 28115, July 26, 1988, as amended at 54 FR 37645, Sept. 12, 1989]

Sec. 8.22 New construction--housing facilities.

(a) New multifamily housing projects (including public housing and Indian housing projects as required by Sec. 8.25) shall be designed and constructed to be readily accessible to and usable by individuals with handicaps.

(b) Subject to paragraph (c) of this section, a minimum of five percent of the total dwelling units or at least one unit in a multifamily housing project, whichever is greater, shall be made accessible for persons with mobility impairments. A unit that is on an accessible route and is adaptable and otherwise in compliance with the standards set forth in Sec. 8.32 is accessible for purposes of this section. An additional two percent of the units (but not less than one unit) in such a project shall be accessible for persons with hearing or vision impairments.

(c) HUD may prescribe a higher percentage or number than that prescribed in paragraph (b) of this section for any area upon request therefor by any affected recipient or by any State or local government or agency thereof based upon demonstration to the reasonable satisfaction of HUD of a need for a higher percentage or number, based on census data or other available current data (including a currently effective Housing Assistance Plan or Comprehensive Homeless Assistance Plan), or in response to evidence of a need for a higher percentage or number received in any other manner. In reviewing such request or otherwise assessing the existence of such needs, HUD shall take into account the expected needs of eligible persons with and without handicaps.

[53 FR 20233, June 2, 1988, as amended at 56 FR 920, Jan. 9, 1991]

ACCESSIBILITY STANDARDS UNDER 24 CFR PART 8, SUBPART C

Sec. 8.23 Alterations of existing housing facilities.

(a) Substantial alteration. If alterations are undertaken to a project (including a public housing project as required by Sec. 8.25(a)(2)) that has 15 or more units and the cost of the alterations is 75 percent or more of the replacement cost of the completed facility, then the provisions of Sec. 8.22 shall apply.

(b) Other alterations. (1) Subject to paragraph (b)(2) of this section, alterations to dwelling units in a multifamily housing project (including public housing) shall, to the maximum extent feasible, be made to be readily accessible to and usable by individuals with handicaps. If alterations of single elements or spaces of a dwelling unit, when considered together, amount to an alteration of a dwelling unit, the entire dwelling unit shall be made accessible. Once five percent of the dwelling units in a project are readily accessible to and usable by individuals with mobility impairments, then no additional elements of dwelling units, or entire dwelling units, are required to be accessible under this paragraph. Alterations to common areas or parts of facilities that affect accessibility of existing housing facilities shall, to the maximum extent feasible, be made to be accessible to and usable by individuals with handicaps. For purposes of this paragraph, the phrase to the maximum extent feasible shall not be interpreted as requiring that a recipient (including a PHA) make a dwelling unit, common area, facility or element thereof accessible if doing so would impose undue financial and administrative burdens on the operation of the multifamily housing project.

(2) HUD may prescribe a higher percentage or number than that prescribed in paragraph (b)(1) of this section for any area upon request therefor by any affected recipient or by any State or local government or agency thereof based upon demonstration to the reasonable satisfaction of HUD of a need for a higher percentage or number, based on census data or other available current data (including a currently effective Housing Assistance Plan or Comprehensive Homeless Assistance Plan), or in response to evidence of a need for a higher percentage or number received in any other manner. In reviewing such request or otherwise assessing the existence of such needs, HUD shall take into account the expected needs of eligible persons with and without handicaps.

Sec. 8.24 Existing housing programs.

(a) General. A recipient shall operate each existing housing program or activity receiving Federal financial assistance so that the program or activity, when viewed in its entirety, is readily accessible to and usable by individuals with handicaps. This paragraph does not--

(1) Necessarily require a recipient to make each of its existing facilities accessible to and usable by individuals with handicaps;

(2) Require a recipient to take any action that it can demonstrate would result in a fundamental alteration in the nature of its program or activity or in undue financial and administrative burdens. If an action would result in such an alteration or such burdens, the recipient shall take any action that would not result in such an alteration or such burdens but would nevertheless ensure that individuals with handicaps receive the benefits and services of the program or activity.

(b) Methods. A recipient may comply with the requirements of this section through such means as reassignment of services to accessible buildings, assignment of aides to beneficiaries, provision of housing or related services at alternate accessible sites, alteration of existing facilities and construction of new facilities, or any other methods that result in making its programs or activities readily accessible to and usable by individuals with handicaps. A recipient is not required to make structural changes in existing housing facilities where other methods are effective in achieving compliance with this section or to provide supportive services that are not part of the program. In choosing among available methods for meeting the requirements of this section, the recipient shall give priority to those methods that offer programs and activities to qualified individuals with handicaps in the most integrated setting appropriate.

(c) Time period for compliance. The recipient shall comply with the obligations established under this section within sixty days of July 11, 1988 except that-

(1) In a public housing program where structural changes in facilities are undertaken, such changes shall be made within the timeframes established in Sec. 8.25(c).

(2) In other housing programs, where structural changes in facilities are undertaken, such changes shall be made within three years of July 11, 1988, but in any event as expeditiously as possible.

ACCESSIBILITY STANDARDS UNDER 24 CFR PART 8, SUBPART C

(d) Transition plan and time period for structural changes. Except as provided in Sec. 8.25(c), in the event that structural changes to facilities will be undertaken to achieve program accessibility, a recipient shall develop, within six months of July 11, 1988, a transition plan setting forth the steps necessary to complete such changes. The plan shall be developed with the assistance of interested persons, including individuals with handicaps or organizations representing individuals with handicaps. A copy of the transition plan shall be made available for public inspection. The plan shall, at a minimum-

(1) Identify physical obstacles in the recipient's facilities that limit the accessibility of its programs or activities to individuals with handicaps;

(2) Describe in detail the methods that will be used to make the facilities accessible; (3) Specify the schedule for taking the steps necessary to achieve compliance with this section and, if the time

period of the transition plan is longer than one year, identify steps that will be taken during each year of the transition period;

(4) Indicate the official responsible for implementation of the plan; and (5) Identify the persons or groups with whose assistance the plan was prepared.

(Approved by the Office of Management and Budget under control number 2529-0034) [53 FR 20233, June 2, 1988; 53 FR 28115, July 26, 1988, as amended at 54 FR 37645, Sept. 12, 1989]

Sec. 8.25 Public housing and multi-family Indian housing.

(a) Development and alteration of public housing and multi-family Indian housing. (1) The requirements of Sec. 8.22 shall apply to all newly constructed public housing and multi-family Indian housing.

(2) The requirements of Sec. 8.23 shall apply to public housing and multi-family Indian housing developed through rehabilitation and to the alteration of public housing and multi-family Indian housing.

(3) In developing public housing and multi-family Indian housing through the purchase of existing properties PHAs and IHAs shall give priority to facilities which are readily accessible to and usable by individuals with handicaps.

(b) Existing public housing and multi-family Indian housing--general. The requirements of Sec. 8.24(a) shall apply to public housing and multi-family Indian housing programs.

(c) Existing public housing and multi-family Indian housing--needs assessment and transition plan. As soon as possible, each PHA (for the purpose of this paragraph, this includes an Indian Housing Authority) shall assess, on a PHA-wide basis, the needs of current tenants and applicants on its waiting list for accessible units and the extent to which such needs have not been met or cannot reasonably be met within four years through development, alterations otherwise contemplated, or other programs administered by the PHA (e.g., Section 8 Moderate Rehabilitation or Section 8 Existing Housing or Housing Vouchers). If the PHA currently has no accessible units or if the PHA or HUD determines that information regarding the availability of accessible units has not been communicated sufficiently so that, as a result, the number of eligible qualified individuals with handicaps on the waiting list is not fairly representative of the number of such persons in the area, the PHA's assessment shall include the needs of eligible qualified individuals with handicaps in the area. If the PHA determines, on the basis of such assessment, that there is no need for additional accessible dwelling units or that the need is being or will be met within four years through other means, such as new construction, Section 8 or alterations otherwise contemplated, no further action is required by the PHA under this paragraph. If the PHA determines, on the basis of its needs assessment, that alterations to make additional units accessible must be made so that the needs of eligible qualified individuals with handicaps may be accommodated proportionally to the needs of non-handicapped individuals in the same categories, then the PHA shall develop a transition plan to achieve program accessibility. The PHA shall complete the needs assessment and transition plan, if one is necessary, as expeditiously as possible, but in any event no later than two years after July 11, 1988. The PHA shall complete structural changes necessary to achieve program accessibility as soon as possible but in any event no later than four years after July 11, 1988. The Assistant Secretary for Fair Housing and Equal Opportunity and the Assistant Secretary for Public and Indian Housing may extend the four year period for a period not to exceed two years, on a case-by-case determination that compliance within that period would impose undue financial and administrative burdens on the operation of the recipient's public housing and multi-family Indian housing program. The Secretary or the Undersecretary may further extend this time period in extraordinary circumstances, for a period not to exceed one year. The plan shall be developed with the assistance of interested

ACCESSIBILITY STANDARDS UNDER 24 CFR PART 8, SUBPART C

persons including individuals with handicaps or organizations representing individuals with handicaps. A copy of the needs assessment and transition plan shall be made available for public inspection. The transition plan shall, at a minimum-

(1) Identify physical obstacles in the PHA's facilities (e.g., dwelling units and common areas) that limit the accessibility of its programs or activities to individuals with handicaps;

(2) Describe in detail the methods that will be used to make the PHA's facilities accessible. A PHA may, if necessary, provide in its plan that it will seek HUD approval, under 24 CFR part 968, of a comprehensive modernization program to meet the needs of eligible individuals with handicaps;

(3) Specify the schedule for taking the steps necessary to achieve compliance with this section and, if the time of the transition plan is longer than one year, identify steps that will be taken during each year of the transition period;

(4) Indicate the official responsible for implementation of the plan; and (5) Identify the persons or groups with whose assistance the plan was prepared.

(Approved by the Office of Management and Budget under control number 2529-0034) [53 FR 20233, June 2, 1988, as amended at 54 FR 37645, Sept. 12, 1989; 56 FR 920, Jan. 9, 1991]

Sec. 8.26 Distribution of accessible dwelling units.

Accessible dwelling units required by Sec. 8.22, 8.23, 8.24 or 8.25 shall, to the maximum extent feasible and subject to reasonable health and safety requirements, be distributed throughout projects and sites and shall be available in a sufficient range of sizes and amenities so that a qualified individual with handicaps' choice of living arrangements is, as a whole, comparable to that of other persons eligible for housing assistance under the same program. This provision shall not be construed to require provision of an elevator in any multifamily housing project solely for the purpose of permitting location of accessible units above or below the accessible grade level.

Sec. 8.27 Occupancy of accessible dwelling units.

(a) Owners and managers of multifamily housing projects having accessible units shall adopt suitable means to assure that information regarding the availability of accessible units reaches eligible individuals with handicaps, and shall take reasonable nondiscriminatory steps to maximize the utilization of such units by eligible individuals whose disability requires the accessibility features of the particular unit. To this end, when an accessible unit becomes vacant, the owner or manager before offering such units to a non-handicapped applicant shall offer such unit:

(1) First, to a current occupant of another unit of the same project, or comparable projects under common control, having handicaps requiring the accessibility features of the vacant unit and occupying a unit not having such features, or, if no such occupant exists, then

(2) Second, to an eligible qualified applicant on the waiting list having a handicap requiring the accessibility features of the vacant unit.

(b) When offering an accessible unit to an applicant not having handicaps requiring the accessibility features of the unit, the owner or manager may require the applicant to agree (and may incorporate this agreement in the lease) to move to a non-accessible unit when available.

Sec. 8.28 Housing certificate and housing voucher programs.

(a) In carrying out the requirements of this subpart, a recipient administering a Section 8 Existing Housing Certificate program or a housing voucher program shall:

(1) In providing notice of the availability and nature of housing assistance for low-income families under program requirements, adopt suitable means to assure that the notice reaches eligible individuals with handicaps;

(2) In its activities to encourage participation by owners, include encouragement of participation by owners having accessible units;

ACCESSIBILITY STANDARDS UNDER 24 CFR PART 8, SUBPART C

(3) When issuing a Housing Certificate or Housing Voucher to a family which includes an individual with handicaps include a current listing of available accessible units known to the PHA and, if necessary, otherwise assist the family in locating an available accessible dwelling unit;

(4) Take into account the special problem of ability to locate an accessible unit when considering requests by eligible individuals with handicaps for extensions of Housing Certificates or Housing Vouchers; and

(5) If necessary as a reasonable accommodation for a person with disabilities, approve a family request for an exception rent under Sec. 982.504(b)(2) for a regular tenancy under the Section 8 certificate program so that the program is readily accessible to and usable by persons with disabilities.

(b) In order to ensure that participating owners do not discriminate in the recipient's federally assisted program, a recipient shall enter into a HUD-approved contract with participating owners, which contract shall include necessary assurances of nondiscrimination.

[53 FR 20233, June 2, 1988, as amended at 63 FR 23853, Apr. 30, 1998]

Sec. 8.29 Homeownership programs (sections 235(i) and 235(j), Turnkey III and Indian housing mutual self-help programs).

Any housing units newly constructed or rehabilitated for purchase or single family (including semi-attached and attached) units to be constructed or rehabilitated in a program or activity receiving Federal financial assistance shall be made accessible upon request of the prospective buyer if the nature of the handicap of an expected occupant so requires. In such case, the buyer shall consult with the seller or builder/sponsor regarding the specific design features to be provided. If accessibility features selected at the option of the homebuyer are ones covered by the standards prescribed by Sec. 8.32, those features shall comply with the standards prescribed in Sec. 8.32. The buyer shall be permitted to depart from particular specifications of these standards in order to accommodate his or her specific handicap. The cost of making a facility accessible under this paragraph may be included in the mortgage amount within the allowable mortgage limits, where applicable. To the extent such costs exceed allowable mortgage limits, they may be passed on to the prospective homebuyer, subject to maximum sales price limitations (see 24 CFR 235.320.)

Sec. 8.30 Rental rehabilitation program.

Each grantee or state recipient in the rental rehabilitation program shall, subject to the priority in 24 CFR 511.10(l) and in accordance with other requirements in 24 CFR part 511, give priority to the selection of projects that will result in dwelling units being made readily accessible to and usable by individuals with handicaps.

[53 FR 20233, June 2, 1988; 53 FR 28115, July 26, 1988]

Sec. 8.31 Historic properties.

If historic properties become subject to alterations to which this part applies the requirements of Sec. 4.1.7 of the standards of Sec. 8.32 of this part shall apply, except in the case of the Urban Development Action Grant (UDAG) program. In the UDAG program the requirements of 36 CFR part 801 shall apply. Accessibility to historic properties subject to alterations need not be provided if such accessibility would substantially impair the significant historic features of the property or result in undue financial and administrative burdens.

Sec. 8.32 Accessibility standards.

(a) Effective as of July 11, 1988, design, construction, or alteration of buildings in conformance with sections 3-8 of the Uniform Federal Accessibility Standards (UFAS) shall be deemed to comply with the requirements of Secs. 8.21, 8.22, 8.23, and 8.25 with respect to those buildings. Departures from particular technical and scoping requirements of the UFAS by the use of other methods are permitted where substantially equivalent or greater access to and usability of the building is provided. The alteration of housing facilities shall also be in

ACCESSIBILITY STANDARDS UNDER 24 CFR PART 8, SUBPART C

conformance with additional scoping requirements contained in this part. Persons interested in obtaining a copy of the UFAS are directed to Sec. 40.7 of this title.

(b) For purposes of this section, section 4.1.6(1)(g) of UFAS shall be interpreted to exempt from the requirements of UFAS only mechanical rooms and other spaces that, because of their intended use, will not require accessibility to the public or beneficiaries or result in the employment or residence therein of individuals with physical handicaps.

(c) This section does not require recipients to make building alterations that have little likelihood of being accomplished without removing or altering a load-bearing structural member.

(d) For purposes of this section, section 4.1.4(11) of UFAS may not be used to waive or lower the minimum of five percent accessible units required by Sec. 8.22(b) or to apply the minimum only to projects of 15 or more dwelling units.

(e) Except as otherwise provided in this paragraph, the provisions of Secs. 8.21 (a) and (b), 8.22 (a) and (b), 8.23, 8.25(a) (1) and (2), and 8.29 shall apply to facilities that are designed, constructed or altered after July 11, 1988. If the design of a facility was commenced before July 11, 1988, the provisions shall be followed to the maximum extent practicable, as determined by the Department. For purposes of this paragraph, the date a facility is constructed or altered shall be deemed to be the date bids for the construction or alteration of the facility are solicited. For purposes of the Urban Development Action Grant (UDAG) program, the provisions shall apply to the construction or alteration of facilities that are funded under applications submitted after July 11, 1988. If the UDAG application was submitted before July 11, 1988, the provisions shall apply, to the maximum extent practicable, as determined by the Department.

[53 FR 20233, June 2, 1988, as amended at 61 FR 5203, Feb. 9, 1996]

Sec. 8.33 Housing adjustments.

A recipient shall modify its housing policies and practices to ensure that these policies and practices do not discriminate, on the basis of handicap, against a qualified individual with handicaps. The recipient may not impose upon individuals with handicaps other policies, such as the prohibition of assistive devices, auxiliary alarms, or guides in housing facilities, that have the effect of limiting the participation of tenants with handicaps in the recipient's federally assisted housing program or activity in violation of this part. Housing policies that the recipient can demonstrate are essential to the housing program or activity will not be regarded as discriminatory within the meaning of this section if modifications to them would result in a fundamental alteration in the nature of the program or activity or undue financial and administrative burdens.

ACCESSIBILITY STANDARDS UNDER 24 CFR PART 8, SUBPART C

END OF SECTION

IRC SECTION 42

IRC SECTION 42

SUBTITLE A. INCOME TAXES CHAPTER 1. NORMAL TAXES AND SURTAXES SUBCHAPTER A. Determination of Tax Liability

PART IV. CREDITS AGAINST TAX SUBPART D. Business Related Credits

(a) In general. For purposes of section 38, the amount of the low-income housing credit determined under this section for any taxable year in the credit period shall be an amount equal to--

(1) the applicable percentage of (2) the qualified basis of each qualified low-income

building. (b) Applicable percentage: 70 percent present value

credit for certain new buildings; 30 percent present value credit for certain other buildings. For purposes of this section--

(1) Building placed in service during 1987. In the case of any qualified low-income building placed in service by the taxpayer during 1987, the term "applicable percentage" means--

(A) 9 percent for new buildings which are not federally subsidized for the taxable year, or

(B) 4 percent for--(i) new buildings which are federally subsidized

for the taxable year, and (ii) existing buildings.

(2) Buildings placed in service after 1987. (A) In general. In the case of any qualified

low-income building placed in service by the taxpayer after 1987, the term "applicable percentage" means the appropriate percentage prescribed by the Secretary for the earlier of--

(i) the month in which such building is placed in service, or

(ii) at the election of the taxpayer-- (I) the month in which the taxpayer and the

housing credit agency enter into an agreement with respect to such building (which is binding on such agency, the taxpayer, and all successors in interest) as to the housing credit dollar amount to be allocated to such building, or

(II) in the case of any building to which subsection (h)(4)(B) applies, the month in which the tax-exempt obligations are issued.

A month may be elected under clause (ii) only if the election is made not later than the 5th day after the close of such month. Such an election, once made, shall be irrevocable.

(B) Method of prescribing percentages. The percentages prescribed by the Secretary for any month shall be percentages which will yield over a 10-year period amounts of credit under subsection (a) which have a present value equal to--

(i) 70 percent of the qualified basis of a building described in paragraph (1)(A), and

(ii) 30 percent of the qualified basis of a building described in paragraph (1)(B). (C) Method of discounting. The present value under

subparagraph (B) shall be determined--(i) as of the last day of the 1st year of the 10-year

period referred to in subparagraph (B), (ii) by using a discount rate equal to 72 percent

of the average of the annual Federal mid-term rate and the annual Federal long-term rate applicable under section 1274(d)(1) to the month applicable under clause (i) or (ii) of subparagraph (A) and compounded annually, and

(iii) by assuming that the credit allowable under this section for any year is received on the last day of such year.

(3) Cross references. (A) For treatment of certain rehabilitation

expenditures as separate new buildings, see subsection (e).

(B) For determination of applicable percentage for increases in qualified basis after the 1st year of the credit period, see subsection (f)(3).

(C) For authority of housing credit agency to limit applicable percentage and qualified basis which may be taken into account under this section with respect to any building, see subsection (h)(7).

(c) Qualified basis; qualified low-income building. For purposes of this section--

(1) Qualified basis. (A) Determination. The qualified basis of any

qualified low-income building for any taxable year is an amount equal to--

(i) the applicable fraction (determined as of the close of such taxable year) of

(ii) the eligible basis of such building (determined under subsection (d)(5)). (B) Applicable fraction. For purposes of

subparagraph (A), the term "applicable fraction" means the smaller of the unit fraction or the floor space fraction.

(C) Unit fraction. For purposes of subparagraph (B), the term "unit fraction" means the fraction--

(i) the numerator of which is the number of low-income units in the building, and

(ii) the denominator of which is the number of residential rental units (whether or not occupied) in such building.

IRC SECTION 42

(D) Floor space fraction. For purposes of subparagraph (B), the term "floor space fraction" means the fraction--

(i) the numerator of which is the total floor space of the low-income units in such building, and

(ii) the denominator of which is the total floor space of the residential rental units (whether or not occupied) in such building. (E) Qualified basis to include portion of building

used to provide supportive services for homeless. In the case of a qualified low-income building described in subsection (i)(3)(B)(iii), the qualified basis of such building for any taxable year shall be increased by the lesser of--

(i) so much of the eligible basis of such building as is used throughout the year to provide supportive services designed to assist tenants in locating and retaining permanent housing, or

(ii) 20 percent of the qualified basis of such building (determined without regard to this subparagraph).

(2) Qualified low-income building. The term "qualified low-income building" means any building--

(A) which is part of a qualified low-income housing project at all times during the period--

(i) beginning on the 1st day in the compliance period on which such building is part of such a project, and

(ii) ending on the last day of the compliance period with respect to such building, and (B) to which the amendments made by section

201(a) of the Tax Reform Act of 1986 apply. Such term does not include any building with respect

to which moderate rehabilitation assistance is provided, at any time during the compliance period, under section 8(e)(2) of the United States Housing Act of 1937 (other than assistance under the Stewart B. McKinney Homeless Assistance Act of 1988 (as in effect on the date of the enactment of this sentence)).

(d) Eligible basis. For purposes of this section-- (1) New buildings. The eligible basis of a new building

is its adjusted basis as of the close of the 1st taxable year of the credit period.

(2) Existing buildings. (A) In general. The eligible basis of an existing

building is--(i) in the case of a building which meets the

requirements of subparagraph (B), its adjusted basis as of the close of the 1st taxable year of the credit period, and

(ii) zero in any other case. (B) Requirements. A building meets the

requirements of this subparagraph if--(i) the building is acquired by purchase (as

defined in section 179(d)(2)),

(ii) there is a period of at least 10 years between the date of its acquisition by the taxpayer and the later of--

(I) the date the building was last placed in service, or

(II) the date of the most recent nonqualified substantial improvement of the building, (iii) the building was not previously placed in

service by the taxpayer or by any person who was a related person with respect to the taxpayer as of the time previously placed in service, and

(iv) except as provided in subsection (f)(5), a credit is allowable under subsection (a) by reason of subsection (e) with respect to the building. (C) Adjusted basis. For purposes of subparagraph

(A), the adjusted basis of any building shall not include so much of the basis of such building as is determined by reference to the basis of other property held at any time by the person acquiring the building.

(D) Special rules for subparagraph (B). (i) Nonqualified substantial improvement. For

purposes of subparagraph (B)(ii)--(I) In general. The term "nonqualified

substantial improvement" means any substantial improvement if section 167(k) (as in effect on the day before the date of enactment of the Revenue Reconciliation Act of 1990 [11/5/90] ) was elected with respect to such improvement or section 168 (as in effect on the day before the date of the enactment of the Tax Reform Act of 1986) applied to such improvement.

(II) Date of substantial improvement. The date of a substantial improvement is the last day of the 24-month period referred to in subclause (III).

(III) Substantial improvement. The term "substantial improvement" means the improvements added to capital account with respect to the building during any 24-month period, but only if the sum of the amounts added to such account during such period equals or exceeds 25 percent of the adjusted basis of the building (determined without regard to paragraphs (2) and (3) of section 1016(a)) as of the 1st day of such period. (ii) Special rules for certain transfers. For

purposes of determining under subparagraph (B)(ii) when a building was last placed in service, there shall not be taken into account any placement in service--

(I) in connection with the acquisition of the building in a transaction in which the basis of the building in the hands of the person acquiring it is determined in whole or in part by reference to the adjusted basis of such building in the hands of the person from whom acquired,

IRC SECTION 42

(II) by a person whose basis in such building is determined under section 1014(a) (relating to property acquired from a decedent),

(III) by any governmental unit or qualified nonprofit organization (as defined in subsection (h)(5)) if the requirements of subparagraph (B)(ii) are met with respect to the placement in service by such unit or organization and all the income from such property is exempt from Federal income taxation,

(IV) by any person who acquired such building by foreclosure (or by instrument in lieu of foreclosure) of any purchase-money security interest held by such person if the requirements of subparagraph (B)(ii) are met with respect to the placement in service by such person and such building is resold within 12 months after the date such building is placed in service by such person after such foreclosure, or

(V) of a single-family residence by any individual who owned and used such residence for no other purpose than as his principal residence. (iii) Related person, etc.

(I) Application of section 179. For purposes of subparagraph (B)(i), section 179(d) shall be applied by substituting "10 percent" for "50 percent" in section 267(b) and 707(b) and in section 179(b)(7).

(II) Related person. For purposes of subparagraph (B)(iii), a person (hereinafter in this subclause referred to as the "related person") is related to any person if the related person bears a relationship to such person specified in section 267(b) or 707(b)(1), or the related person and such person are engaged in trades or businesses under common control (within the meaning of subsections (a) and (b) of section 52). For purposes of the preceding sentence, in applying section 267(b) or 707(b)(1), "10 percent" shall be substituted for "50 percent".

(3) Eligible basis reduced where disproportionate standards for units.

(A) In general. Except as provided in subparagraph (B), the eligible basis of any building shall be reduced by an amount equal to the portion of the adjusted basis of the building which is attributable to residential rental units in the building which are not low-income units and which are above the average quality standard of the low-income units in the building.

(B) Exception where taxpayer elects to exclude excess costs.

(i) In general. Subparagraph (A) shall not apply with respect to a residential rental unit in a building which is not a low-income unit if--

(I) the excess described in clause (ii) with respect to such unit is not greater than 15 percent of the cost described in clause (ii)(II), and

(II) the taxpayer elects to exclude from the eligible basis of such building the excess described in clause (ii) with respect to such unit. (ii) Excess. The excess described in this clause

with respect to any unit is the excess of-- (I) the cost of such unit, over (II) the amount which would be the cost of

such unit if the average cost per square foot of low-income units in the building were substituted for the cost per square foot of such unit.

The Secretary may by regulation provide for the determination of the excess under this clause on a basis other than square foot costs.

(4) Special rules relating to determination of adjusted basis. For purposes of this subsection--

(A) In general. Except as provided in subparagraphs (B) and (C), the adjusted basis of any building shall be determined without regard to the adjusted basis of any property which is not residential rental property.

(B) Basis of property in common areas, etc., included. The adjusted basis of any building shall be determined by taking into account the adjusted basis of property (of a character subject to the allowance for depreciation) used in common areas or provided as comparable amenities to all residential rental units in such building.

(C) INCLUSION OF BASIS OF PROPERTY USED TO PROVIDE SERVICES FOR CERTAIN NONTENANTS. -

(i) IN GENERAL.-The adjusted basis of any building located in a qualified census tract (as defined in paragraph (5) (C)) shall be determined by taking into account the adjusted basis of property (of a character subject to the allowance for depreciation and not otherwise taken into account) used throughout the taxable year in providing any community service facility.

(ii) LIMITATION.- The increase in the adjusted basis of any building which is taken in to account by reason of clause (i) shall not exceed 10 percent of the eligible basis of the qualified low-income housing project of which it is a part. For purposes of the preceding sentence, all community service facilities which are part of the same qualified low-income housing project shall be treated as one facility.

(iii) COMMUNITY SERVICE FACILITY.- For purposes of this subparagraph, the term ‘community service facility’ means any facility designed to serve primarily individuals whose income is 60 percent or less of area median income (within the meaning of subsection (g) (1) (B)).

IRC SECTION 42

(D) No reduction for depreciation. The adjusted basis of any building shall be determined without regard to paragraphs (2) and (3) of section 1016(a). (5) Special rules for determining eligible basis.

(A) Eligible basis reduced by federal grants. If, during any taxable year of the compliance period, a grant is made with respect to any building or the operation thereof and any portion of such grant is funded with Federal funds (whether or not includible in gross income), the eligible basis of such building for such taxable year and all succeeding taxable years shall be reduced by the portion of such grant which is so funded.

(B) Eligible basis not to include expenditures where section 167(k) (as in effect on the day before the date of enactment of the Revenue Reconciliation Act of 1990 [11/5/90] ) elected. The eligible basis of any building shall not include any portion of its adjusted basis which is attributable to amounts with respect to which an election is made under section 167(k) (as in effect on the day before the date of enactment of the Revenue Reconciliation Act of 1990 [11/5/90]).

(C) Increase in credit for buildings in high cost areas. (i) In general. In the case of any building located

in a qualified census tract or difficult development area which is designated for purposes of this subparagraph--

(I) in the case of a new building, the eligible basis of such building shall be 130 percent of such basis determined without regard to this subparagraph, and

(II) in the case of an existing building, the rehabilitation expenditures taken into account under subsection (e) shall be 130 percent of such expenditures determined without regard to this subparagraph. (ii) Qualified census tract.

(I) In general. The term "qualified census tract" means any census tract which is designated by the Secretary of Housing and Urban Development and, for the most recent year for which census data are available on household income in such tract, either in which 50 percent or more of the households have an income which is less than 60 percent of the area median gross income for such year or which has a poverty rate of at least 25 percent. If the Secretary of Housing and Urban Development determines that sufficient data for any period are not available to apply this clause on the basis of census tracts, such Secretary shall apply this clause for such period on the basis of enumeration districts.

(II) Limit on MSA's designated. The portion of a metropolitan statistical area which may be designated for purposes of this subparagraph shall not exceed an area having 20 percent of the population of such metropolitan statistical area.

(III) Determination of areas. For purposes of this clause, each metropolitan statistical area shall be treated as a separate area and all nonmetropolitan areas in a State shall be treated as 1 area. (iii) Difficult development areas.

(I) In general. The term "difficult development areas" means any area designated by the Secretary of Housing and Urban Development as an area which has high construction, land, and utility costs relative to area median gross income.

(II) Limit on areas designated. The portions of metropolitan statistical areas which may be designated for purposes of this subparagraph shall not exceed an aggregate area having 20 percent of the population of such metropolitan statistical areas. A comparable rule shall apply to nonmetropolitan areas. (iv) Special rules and definitions. For purposes of

this subparagraph--(I) population shall be determined on the

basis of the most recent decennial census for which data are available,

(II) area median gross income shall be determined in accordance with subsection (g)(4),

(III) the term "metropolitan statistical area" has the same meaning as when used in section 143(k)(2)(B), and

(IV) the term "nonmetropolitan area" means any county (or portion thereof) which is not within a metropolitan statistical area.

(6) Credit allowable for certain federally-assisted buildings acquired during 10-year period described in paragraph (2)(B)(ii).

(A) In general. On application by the taxpayer, the Secretary (after consultation with the appropriate Federal official) may waive paragraph (2)(B)(ii) with respect to any federally-assisted building if the Secretary determines that such waiver is necessary--

(i) to avert an assignment of the mortgage secured by property in the project (of which such building is a part) to the Department of Housing and Urban Development or the Farmers Home Administration, or

(ii) to avert a claim against a Federal mortgage insurance fund (or such Department or Administration) with respect to a mortgage which is so secured. The preceding sentence shall not apply to any

building described in paragraph (7)(B). (B) Federally-assisted building. For purposes of

subparagraph (A), the term "federally-assisted building" means any building which is substantially assisted, financed, or operated under--

(i) section 8 of the United States Housing Act of 1937,

IRC SECTION 42

(ii) section 221(d)(3) or 236 of the National Housing Act, or

(iii) section 515 of the Housing Act of 1949, as such Acts are in effect on the date of the

enactment of the Tax Reform Act of 1986. (C) Low-income buildings where mortgage may be

prepaid. A waiver may be granted under subparagraph (A) (without regard to any clause thereof) with respect to a federally-assisted building described in clause (ii) or (iii) of subparagraph (B) if--

(i) the mortgage on such building is eligible for prepayment under subtitle B of the Emergency Low Income Housing Preservation Act of 1987 or under section 502(c) of the Housing Act of 1949 at any time within 1 year after the date of the application for such a waiver,

(ii) the appropriate Federal official certifies to the Secretary that it is reasonable to expect that, if the waiver is not granted, such building will cease complying with its low-income occupancy requirements, and

(iii) the eligibility to prepay such mortgage without the approval of the appropriate Federal official is waived by all persons who are so eligible and such waiver is binding on all successors of such persons. (D) Buildings acquired from insured depository

institutions in default. A waiver may be granted under subparagraph (A) (without regard to any clause thereof) with respect to any building acquired from an insured depository institution in default (as defined in section 3 of the Federal Deposit Insurance Act) or from a receiver or conservator of such an institution.

(E) Appropriate federal official. For purposes of subparagraph (A), the term "appropriate Federal official" means--

(i) the Secretary of Housing and Urban Development in the case of any building described in subparagraph (B) by reason of clause (i) or (ii) thereof, and

(ii) the Secretary of Agriculture in the case of any building described in subparagraph (B) by reason of clause (iii) thereof.

(7) Acquisition of building before end of prior compliance period.

(A) In general. Under regulations prescribed by the Secretary, in the case of a building described in subparagraph (B) (or interest therein) which is acquired by the taxpayer--

(i) paragraph (2)(B) shall not apply, but (ii) the credit allowable by reason of subsection

(a) to the taxpayer for any period after such acquisition shall be equal to the amount of credit which would have been allowable under subsection (a) for such period to the prior owner referred to in subparagraph (B) had such owner not disposed of the building.

(B) Description of building. A building is described in this subparagraph if--

(i) a credit was allowed by reason of subsection (a) to any prior owner of such building, and

(ii) the taxpayer acquired such building before the end of the compliance period for such building with respect to such prior owner (determined without regard to any disposition by such prior owner).

(e) Rehabilitation expenditures treated as separate new building.

(1) In general. Rehabilitation expenditures paid or incurred by the taxpayer with respect to any building shall be treated for purposes of this section as a separate new building.

(2) Rehabilitation expenditures. For purposes of paragraph (1)--

(A) In general. The term "rehabilitation expenditures" means amounts chargeable to capital account and incurred for property (or additions or improvements to property) of a character subject to the allowance for depreciation in connection with the rehabilitation of a building.

(B) Cost of acquisition, etc., not included. Such term does not include the cost of acquiring any building (or interest therein) or any amount not permitted to be taken into account under paragraph (3) or (4) of subsection (d). (3) Minimum expenditures to qualify.

(A) In general. Paragraph (1) shall apply to rehabilitation expenditures with respect to any building only if--

(i) the expenditures are allocable to 1 or more low-income units or substantially benefit such units, and

(ii) the amount of such expenditures during any 24-month period meets the requirements of whichever of the following subclauses requires the greater amount of such expenditures:

(I) The requirement of this subclause is met if such amount is not less than 10 percent of the adjusted basis of the building (determined as of the 1st day of such period and without regard to paragraphs (2) and (3) of section 1016(a)).

(II) The requirement of this subclause is met if the qualified basis attributable to such amount, when divided by the number of low-income units in the building, is $ 3,000 or more.

(B) Exception from 10 percent rehabilitation. In the case of a building acquired by the taxpayer from a governmental unit, at the election of the taxpayer, subparagraph (A)(ii)(I) shall not apply and the credit under this section for such rehabilitation expenditures shall be determined using the percentage applicable under subsection (b)(2)(B)(ii).

(C) Date of determination. The determination under subparagraph (A) shall be made as of the close of the 1st taxable year in the credit period with respect to such expenditures.

IRC SECTION 42

(4) Special rules. For purposes of applying this section with respect to expenditures which are treated as a separate building by reason of this subsection--

(A) such expenditures shall be treated as placed in service at the close of the 24-month period referred to in paragraph (3)(A), and

(B) the applicable fraction under subsection (c)(1) shall be the applicable fraction for the building (without regard to paragraph (1)) with respect to which the expenditures were incurred.

Nothing in subsection (d)(2) shall prevent a credit from being allowed by reason of this subsection. (5) No double counting. Rehabilitation expenditures

may, at the election of the taxpayer, be taken into account under this subsection or subsection (d)(2)(A)(i) but not under both such subsections.

(6) Regulations to apply subsection with respect to group of units in building. The Secretary may prescribe regulations, consistent with the purposes of this subsection, treating a group of units with respect to which rehabilitation expenditures are incurred as a separate new building. (f) Definition and special rules relating to credit period.

(1) Credit period defined. For purposes of this section, the term "credit period" means, with respect to any building, the period of 10 taxable years beginning with--

(A) the taxable year in which the building is placed in service, or

(B) at the election of the taxpayer, the succeeding taxable year, but only if the building is a qualified low-income

building as of the close of the 1st year of such period. The election under subparagraph (B), once made, shall be irrevocable.

(2) Special rule for 1st year of credit period. (A) In general. The credit allowable under

subsection (a) with respect to any building for the 1st taxable year of the credit period shall be determined by substituting for the applicable fraction under subsection (c)(1) the fraction--

(i) the numerator of which is the sum of the applicable fractions determined under subsection (c)(1) as of the close of each full month of such year during which such building was in service, and

(ii) the denominator of which is 12. (B) Disallowed 1st year credit allowed in 11th year.

Any reduction by reason of subparagraph (A) in the credit allowable (without regard to subparagraph (A)) for the 1st taxable year of the credit period shall be allowable under subsection (a) for the 1st taxable year following the credit period. (3) Determination of applicable percentage with respect

to increases in qualified basis after 1st year of credit period. (A) In general. In the case of any building which was

a qualified low-income building as of the close of the 1st year of the credit period, if--

(i) as of the close of any taxable year in the compliance period (after the 1st year of the credit period) the qualified basis of such building exceeds

(ii) the qualified basis of such building as of the close of the 1st year of the credit period,

the applicable percentage which shall apply under subsection (a) for the taxable year to such excess shall be the percentage equal to 2/3 of the applicable percentage which (after the application of subsection (h)) would but for this paragraph apply to such basis. (B) 1st year computation applies. A rule similar to

the rule of paragraph (2)(A) shall apply to any increase in qualified basis to which subparagraph (A) applies for the 1st year of such increase. (4) Dispositions of property. If a building (or an interest

therein) is disposed of during any year for which credit is allowable under subsection (a), such credit shall be allocated between the parties on the basis of the number of days during such year the building (or interest) was held by each. In any such case, proper adjustments shall be made in the application of subsection (j).

(5) Credit period for existing buildings not to begin before rehabilitation credit allowed.

(A) In general. The credit period for an existing building shall not begin before the 1st taxable year of the credit period for rehabilitation expenditures with respect to the building.

(B) Acquisition credit allowed for certain buildings not allowed a rehabilitation credit.

(i) In general. In the case of a building described in clause (ii)--

(I) subsection (d)(2)(B)(iv) shall not apply, and