digitie instant payment - online

TRANSCRIPT

DIGITIE INSTANT PAYMENTAN ANSWER TO 21ST CENTURY PAYMENT EXPECTATIONS? As smartphones and e-commerce become increasingly widespread, the digitalisation of the economy is resulting in a general acceleration of the payment process. Customers can make online purchases anywhere and at any time, even during evening classes and on weekends and public holidays - periods when most traditional electronic payment methods do not work. On the other hand, business and service providers expect a guarantee that they will receive the value of their goods or services.

The SCT Inst system meets these expectations by enabling pan-European transfers within ten seconds, so the amount transferred is immediately available on the beneficiary’s account.

We recommend using the DigiTie software solution’s SCT Inst Module (hereinafter: DigiTie SCT Inst) for connecting to any SCT Inst scheme based system, such as the TIPS (Target Instant Pay-ment System) or any local payment instant payment systems, as it can be easily integrated into the bank’s IT architecture. In addition to connecting to the payment system, the module also supports additional optional services that are already available in tandem with instant pay-ments in certain European countries, such as payment requests and the handling of secondary account identifiers. To ensure fast and seamless services, versions can be upgraded without any service interruptions.

The following provides a summary of the structure used by the SEPA Instant Credit Transfer, the system that has been developed to serve this connection, and the additional functions that can be added to such a system to ensure a higher level of customer service.

2

THE OBJECTIVE AND GUIDELINES OF THE SCT INST SCHEME

The groundwork for the SCT Inst system was laid by the EPC (European Payments Council). The EPC is a non-profit association whose role is to support and promote European payments integration and development, notably the SEPA (Single Euro Payments Area) as well as the SCT Inst scheme. It was established in 2002 as a result of a bank sector initiative and, although many of its goals are the same as those of the European Union, the EPC is not an EU institution. Its members are payment service providers or associations of such service providers.

SCT Inst targets:

• the development of a basic payment system that competes with cash payments in both speed and accessibility

• innovation• the harmonisation of payment solutions and the prevention of conflicting payment solutions.

The ten most important advantages of SCT Inst1:

1. The entire payment process takes just a few seconds (10 seconds as a general rule).2. Operation is continuous (24/7/365).3. Annually reviewed central maximum transaction limit (€15,000).4. Enables both national and cross-border payments.5. A digital payment method that also supports the use of new technologies.6. Helps company cash-flow management, as balances are available 24/7/365.7. Due to its ease of use, it is suitable for replacing cash and checks in many cases.8. Contributes to a single, harmonised euro payment environment and thus to the concept of a single

European market.9. Secure and compliant with consumer and data protection, fraud prevention, money laundering prevention,

and sanctioning regulations.10. Based on the long-running SEPA CT scheme, meaning implementation requires less effort than for an

entirely new system.

An important task and goal of the DigiTie system’s SCT Inst module is to ensure that the financial institutions using the services can maximise all the benefits of the scheme.

1 Source: https://www.europeanpaymentscouncil.eu/sites/default/files/kb/file/2018-11/EPC004-16%202019%20SCT%20Instant%20Rulebook%20v1.0.pdf

3

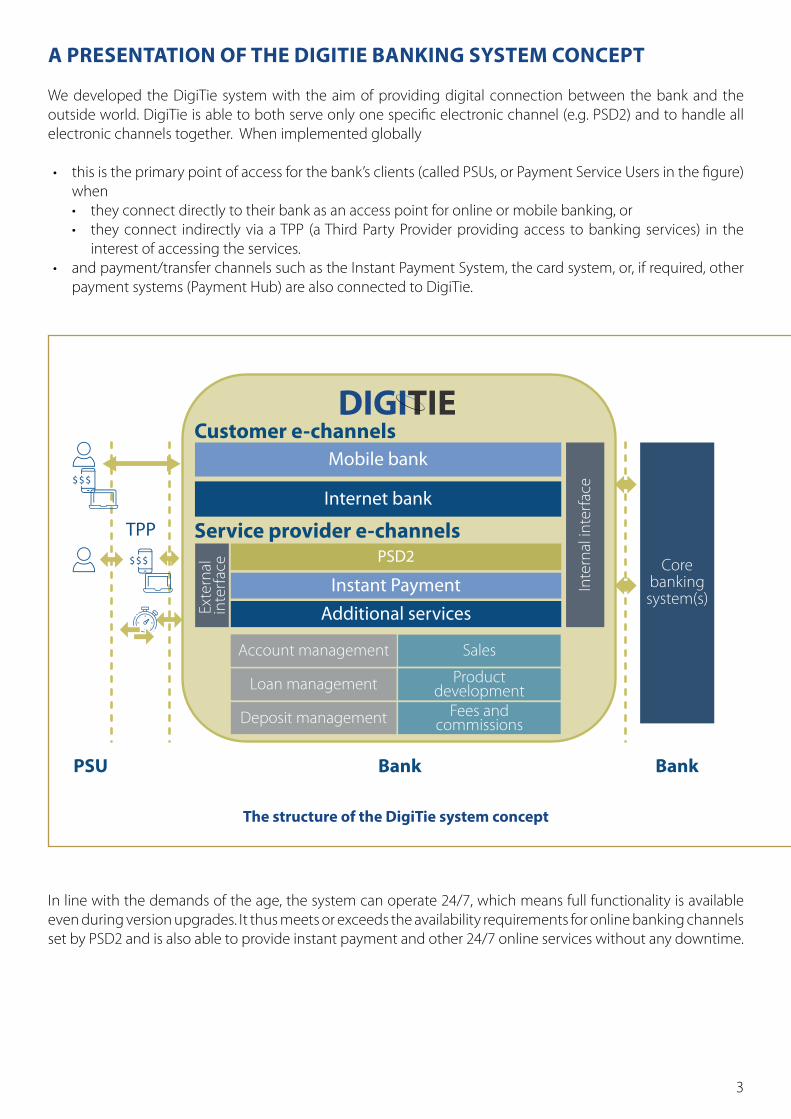

A PRESENTATION OF THE DIGITIE BANKING SYSTEM CONCEPT

We developed the DigiTie system with the aim of providing digital connection between the bank and the outside world. DigiTie is able to both serve only one specific electronic channel (e.g. PSD2) and to handle all electronic channels together. When implemented globally

• this is the primary point of access for the bank’s clients (called PSUs, or Payment Service Users in the figure) when • they connect directly to their bank as an access point for online or mobile banking, or • they connect indirectly via a TPP (a Third Party Provider providing access to banking services) in the

interest of accessing the services. • and payment/transfer channels such as the Instant Payment System, the card system, or, if required, other

payment systems (Payment Hub) are also connected to DigiTie.

The structure of the DigiTie system concept

In line with the demands of the age, the system can operate 24/7, which means full functionality is available even during version upgrades. It thus meets or exceeds the availability requirements for online banking channels set by PSD2 and is also able to provide instant payment and other 24/7 online services without any downtime.

Customer e-channelsMobile bank

Internet bank

Exte

rnal

in

terf

ace PSD2

Service provider e-channels

Instant Payment Inte

rnal

inte

rfac

e

Additional services

Account management

Loan management

Deposit management

Sales

Productdevelopment

Fees andcommissions

Corebankingsystem(s)

BankBankPSU

$$$

$$$

TPP

4

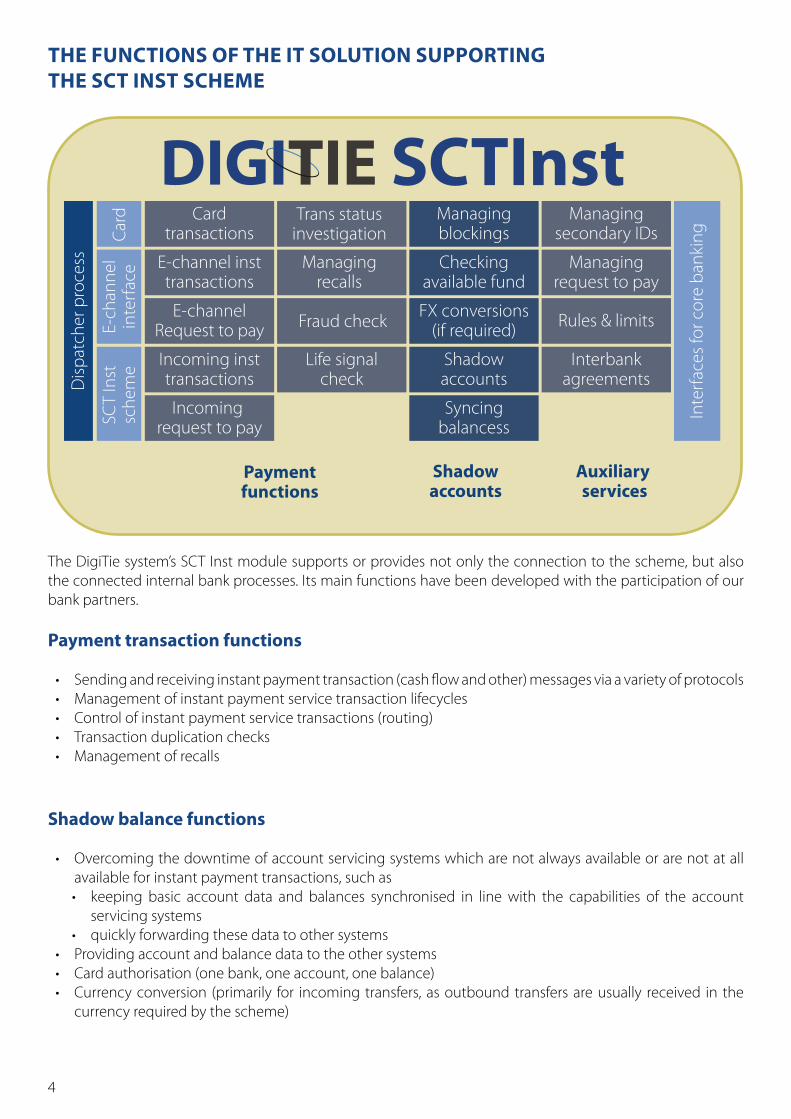

THE FUNCTIONS OF THE IT SOLUTION SUPPORTING THE SCT INST SCHEME

The DigiTie system’s SCT Inst module supports or provides not only the connection to the scheme, but also the connected internal bank processes. Its main functions have been developed with the participation of our bank partners.

Payment transaction functions

• Sending and receiving instant payment transaction (cash flow and other) messages via a variety of protocols• Management of instant payment service transaction lifecycles• Control of instant payment service transactions (routing)• Transaction duplication checks• Management of recalls

Shadow balance functions

• Overcoming the downtime of account servicing systems which are not always available or are not at all available for instant payment transactions, such as • keeping basic account data and balances synchronised in line with the capabilities of the account

servicing systems• quickly forwarding these data to other systems

• Providing account and balance data to the other systems• Card authorisation (one bank, one account, one balance)• Currency conversion (primarily for incoming transfers, as outbound transfers are usually received in the

currency required by the scheme)

SCTInstD

ispa

tche

r pro

cess

Card

E-ch

anne

lin

terf

ace

SCT

Inst

sche

me

Cardtransactions

E-channel insttransactions

E-channelRequest to pay

Incoming insttransactions

Incoming request to pay

Trans statusinvestigation

Managingrecalls

Fraud check

Life signalcheck

Managingblockings

Checkingavailable fund

FX conversions(if required)

Shadowaccounts

Syncingbalancess

Managingsecondary IDs

Managingrequest to pay

Rules & limits

Interbankagreements

Inte

rfac

es fo

r cor

e ba

nkin

g

Paymentfunctions

Shadowaccounts

Auxiliary services

5

Additional functions

• Handles agreements and limits between banks (and countries)• Supports the use of secondary account identifiers

• Registration, record, and lifecycle management • Annual confirmation• Data processing statements• Allows other bank systems (e.g. Internet Bank, Mobile Bank, Core) to access the functions

• Supports payment requests• Allows requests to be launched from bank interfaces or via an API, as required• Forwards received requests to client interfaces• Received request management function and the management of instant payments launched on the

basis of approved requests• Manages anti-fraud and money laundering checks in regard to instant payments• Interface to transaction monitoring and data warehouse systems

THE PLACE OF THE MODULE WITHIN THE BANK

SCTInst

Dis

patc

her p

roce

ss

Card

E-ch

anne

lin

terf

ace

SCT

Inst

sche

me

Cardtransactions

E-channel insttransactions

E-channelRequest to pay

Incoming insttransactions

Incoming request to pay

Trans statusinvestigation

Managingrecalls

Fraud check

Life signalcheck

Managingblockings

Checkingavailable fund

FX conversions(if required)

Shadowaccounts

Syncingbalances

Managingsecondary IDs

Managingrequest to pay

Rules & limits

Interbankagreements

Inte

rfac

es fo

r cor

e ba

nkin

g

Paymentfunctions

Shadowaccounts

Auxiliary services

Core bankingsystem (s)

...

Datawarehouse

Datawarehouse

Transactionmonitoring

Cardschemes

Internet banking

PSD2

E-channels

SCT Inst

Mobile banking

TPP

$$$

$$$

$

SCT Inst

6

The above figure clearly illustrates that the message types under the ISO 20022 XML standard cover the entire spectrum necessary for instant payment and thus also provide the perfect basis for the SCT Inst scheme. A number of European, non-euro based payment systems are based on SCT Inst (e.g. Hungarian and Croatian systems), which use the same types with only slight differences and country-specific solutions.

In addition to defining the interbank area, an important element of the scheme is the provision of guidelines for the messages used for communication between banks and customers, helping to further the idea of a single European market.

COMMUNICATION WITH THE INSTANT PAYMENT SYSTEM

The scheme uses communication based on instant messages to operate the payment process and the connected functions; the format of the messages is primarily based on the ISO 20022 standard. The use of both SOAP and REST-based HTTPS web services are common in such types of communication. Accordingly, DigiTie supports schemes implemented according to both, can operate both simultaneously, and can communicate synchronously and asynchronously through these.

ISO 20022 message types in instant payment2

2 Source: https://www.iso20022.org/sites/default/files/documents/general/RealTimePaymentsandISO20022_v3.pdf

Overlay Services

PayerPain.001Pain.002

Pain.013/Pain.014Camt.052/053/054

Camt.056/029Remt.001/002

Interbank messagingPacs.008Pacs.002

Pacs.004Pain.013/Pain.014

Camt.052/053/054Camt.056/029Remt.001/002

PayeePain.013/Pain.014

CAmt.052/053/054Remt.001/002

SettlementPacs.009

Pacs.0010Pacs.002

’Core' paymentmessage

Optional usage and drive by system design and market requirement

7

The main message types3:

Message type (data set) Message purpose / content

pain.001 (DS-01) Transfer/payment initiation (customer à bank)

pain.002 (based on DS-03)Payment status report (bank à customer)Rejection, or negative or positive confirmation

pacs.008 (DS-02) Transfer/payment initiation (bank à bank)

pacs.002 (DS-03)Final status report (bank à bank)Positive (ACCP) or negative (RJCT) confirmation

camt.056 (DS-05 or DS-08) Instant payment message recall initiation (bank à bank)

pain.004 (DS-06) Positive answer to a recall (bank à bank)

camt.029 (DS-06) Negative answer to a recall (bank à bank)

pacs.028 (DS-07)Instant payment status investigation message (bank à bank)Request for status update on a request for recall (bank à bank)

ENSURING 24/7/365 OPERATION

A critical requirement for instant payment systems is that they must ensure full operation with practically no downtime. This is expected by the banks that wish to use the channel for interbank transfers as well as by clients who expect the system to be available every day of the week, and even throughout the night, as the main competitors of instant payment, cash and cards, are both able to meet these demands.

DigiTie meets this requirement even when undergoing version upgrades by using the system running the old version for messaging until the new version has been fully installed. After installation is complete, messaging is redirected to the new version.

However, it should be noted that no matter how tolerant the software solution is, its running environment also has to be given special attention. In the course of implementation both on-premise and on a central server (private cloud/SaaS: should the European regulatory environment develop accordingly, even a public cloud), suitable preparations have to be made including sizing and DR plans, the designs for both of which are always included in our offer.

3 Sources:– C2B: https://www.europeanpaymentscouncil.eu/document-library/implementation-guidelines/sepa-instant-

credit-transfer-scheme-customer-bank-0 – Interbank: https://www.europeanpaymentscouncil.eu/document-library/implementation-guidelines/sepa-

instant-credit-transfer-scheme-interbank-3

8

POSSIBLE DEVIATIONS FROM THE EUROPEAN SCT INST SCHEME

The DigiTie SCT Inst module does not support only instant payment solutions under the SCT Inst scheme, but also supports individual, national solutions that have been implemented in line with local requirements and expectations. For example, an instant payment solution prepared for the Hungarian market contains exactly such deviations, which, among others, includes the following individual elements:

Character set The use of Hungarian accented characters

Currency The use of Hungarian forint (HUF)

Limit valueNot checked by the central system; defined by law and bilateral or multilateral agreements

Time limit for uniqueness

Under the scheme, unique identifiers have to remain unique for 7 calendar days

Error codes The support of error codes different than those defined by ISO 20022

Recalls and answersThe rules of the scheme require 30 day time limits for initiating recalls and for providing answers

Accuracy of time measurement

The time stamp required to determine the execution time must be specified with millisecond accuracy; its time is either the time of client authentication or receipt by the payment service provider, whichever is later

Indication of secondary identifier

In the case of both transfers and payment requests, the use of a secondary identifier has to be indicated and included in the message

Linking the payment request and the connected payment

The EndToEndIdentification of the two transactions have to be identical, and the appropriate field must indicate that the payment is for the fulfilment of a payment request

Type of payment situation

The type of payment situation (e.g. physical purchase, online purchase, invoice payment, P2P transfer) can be indicated with the use of standard ISO 20022 or unique codes

For all markets these requirements may differ and we are happy to tailor our solution to your requirements and are happy also to work on discovering new possible directions for evolution. Having a trustable core payment processing software is just a brick in the wall, you have to provide your customers with the related service offerings as well.

DigiTie was created with evolution in mind and is able to provide for the requirements of any instant payment system and is also perfectly capable to provide additional services in similarly high quality, including traditionally paper-heavy personal matters like depositing and loan distribution in line with the local regulatory possibilities. By providing more and more services 24/7 in the digital world the new age of banking can become a reality.

9

REQUEST TO PAY

Built on the possibilities of the quick messaging nature of instant payment a new type of service is setting foot across Europe alongside it. Request to pay (RTP for short) is a new option to get payed quickly and conveniently for businesses and people alike.

When using this service, all you need to do is specify how much money you need and from who and this message is sent to the payer, usually through the central infrastructure of instant payment. On the payer side this appears as a notification, that a payment has been requested and it is up to the receiver to decide what to do with it.

It is important to note though, that this type of message is not considered payment and therefore is not regulated like one in most countries. Thus, this type of service can be provided for example by a PISP and can initiate the payments under the rules of PSD2 based on the approval of the payer quickly and conveniently.

RTP USE CASES

Use cases can include the followings, all of which provide an improved user experience compared to current options, among other benefits:

Buy in-store The payment request is accepted on the mobile phone in a physical store.

Shop onlineThe payment request is accepted on the mobile phone in the checkout process of a purchase on the internet.

Split the bill Someone pays and sends the requests to the others to pay their shares.

Pay utility billThe request of paying a utility bill is shown on the mobile phone and the payment can be scheduled for the due date.

Pay invoiceThe request of paying an invoice is shown on the mobile phone and the payment can be scheduled for the due date.

Set up monthly payment

Monthly request is shown on the mobile phone and the customer can pay immediately, schedule for later, ignore or cancel (e.g. insurance fee).

Set up regular donation

Request is displayed on donor’s mobile phone every month to decide about.

Make a donation to volunteer on street

One-time donation request appears on mobile phone.

The use cases generally start with the customer showing interest to pay for a service or product and the merchant/provider sends an RTP message to the customer. The request can be addressed to an account number or to a secondary ID. This seemingly minor change allows the customer to provide just this ID to initiate an RTP and all the other necessary data is automatically filled by the merchant upon RTP initiation and the customer’s bank on RTP acceptance.

10

The process is usually like this in the context of a purchase at a merchant:

1. The customer places the order at the merchant and provides any valid account ID for payment2. The merchant sends the RTP to the provided account ID3. The customer receives the RTP at their device or internet banking software4. The customer authenticates towards the bank and can authorise the payment 5. The instant payment is initiated towards the merchant who can get instant confirmation and can provide

the service or product immediately without getting a delayed payment

THE BENEFITS OF RTP

The new request to pay service has many possibilities and we are still just exploring the potential use cases, which can range from person-to-person payments for splitting the bill to utility companies issuing RTP-s for their customers as a method of paying for the services.

ReachRTP can reach more users than cards or wallets, e.g. businesses, as it uses the ordinary bank account.

Low costAs the basic cost is just the messaging and the providers may value the data more than the direct revenue, prices can be very low.

Low risk, high control

The user authenticates and authorizes for every transaction which results in lower fraud, chargeback and even payment decline rates.

Real time settlement

There is no longer a waiting time of 2-3 days for payments with the use of instant payment.

Secondary IDs

In several RTP systems you can use proxy IDs for customers (e-mail, phone number) which enables much smoother customer registration and is a relief for merchants, businesses as well. Also reduces the risks of data breach risks as account details are not disclosed.

Reduction in late payments

The system enables B2B payments to be much easier and much faster thus reducing Days Sales Outstanding (DSO).

Less cashThe time stamp required to determine the execution time must be specified with millisecond accuracy; its time is either the time of client authentication or receipt by the payment service provider, whichever is later.

Choice Pay from any funding source.

Request to pay is one of the first widespread use cases of the newly appeared instant messaging type instant payment networks with a very big potential. More and more regulators, financial institutions and service providers are building on it, we can help you be a part of it.

DigiTie SCT Inst enables you to join the RTP network to fully utilize all of the its benefits and provide value to your users.

If you are interested in any of the above, please contact us, we are happy to provide additional materials.

11

ABOUT ONLINE BUSINESS TECHNOLOGIES

We are an innovative IT development company specialized in banking technology since 1989.

We provide a wide spectrum of highly flexible solutions necessary for banks to go digital, including modules to join FinTech ecosystems (e.g. PSD2, open APIs, instant payments), e-channel solutions, and state-of-the-art core banking modules to support front- and back-office operations (including account management, credits, deposit, GL etc.)

Our modules can be combined freely, we are able to deliver a standalone solution for a specific task (e.g. PSD2), or a series of modules covering the complete value chain (e.g. credit processes).

Our operations in numbers:

• Nearly 2500 years of banking, financial software development experience• Our solutions are used by more than 8000 users• Our solutions are used in more than 1000 branches by our customers• Our partners serve more than 3 million customers with our solutions

OUR VALUES

UNIQUE COMPETENCE Our experience and professional knowledge in the field of credit institutions and finance is unique among IT providers.

CUSTOMIZED SYSTEMS With the help of our unique development and version management technology, our modules can be customized and implemented rapidly. We also have extensive experience in realizing unique functionality.

HIGH QUALITY Owing to the quality control system covering all of our activities and to the controlled development processes, our systems are of high quality and reliability.

QUICK RETURN Fast launching of developments that save customer resources, increased efficiency in management, flexible response to market trends – these all result in our customers gaining advantage in the rapidly changing financial market.

For more information check out our website: www.online.hu and contact us!

Online Business Technologies H-1032 Budapest, Vályog street 3. | +36 -1 437-0700 | https://www.online.hu/contact