decision-making. learning objectives the scope of decision-making the seven steps of the...

TRANSCRIPT

Decision-Making Decision-Making

learning objectives

the scope of decision-making

the seven steps of the decision-making process

relevant costs

examples of practical areas of decision-making

marginal costing and shutdown or continuation decisions

Session Summary (1) Session Summary (1)

make versus buy

product mix decisions and limiting factors

sales pricing

profit volume (PV) chart and contribution curve profit volume (PV) chart and contribution curve band

decision trees

example of a decision tree

Session Summary (2) Session Summary (2)

explain the scope and importance of decision-makingto an organisation

outline the decision-making process

explain the significance of the concept of relevant costs

apply marginal costing techniques to decision-making

Learning Objectives (1) Learning Objectives (1)

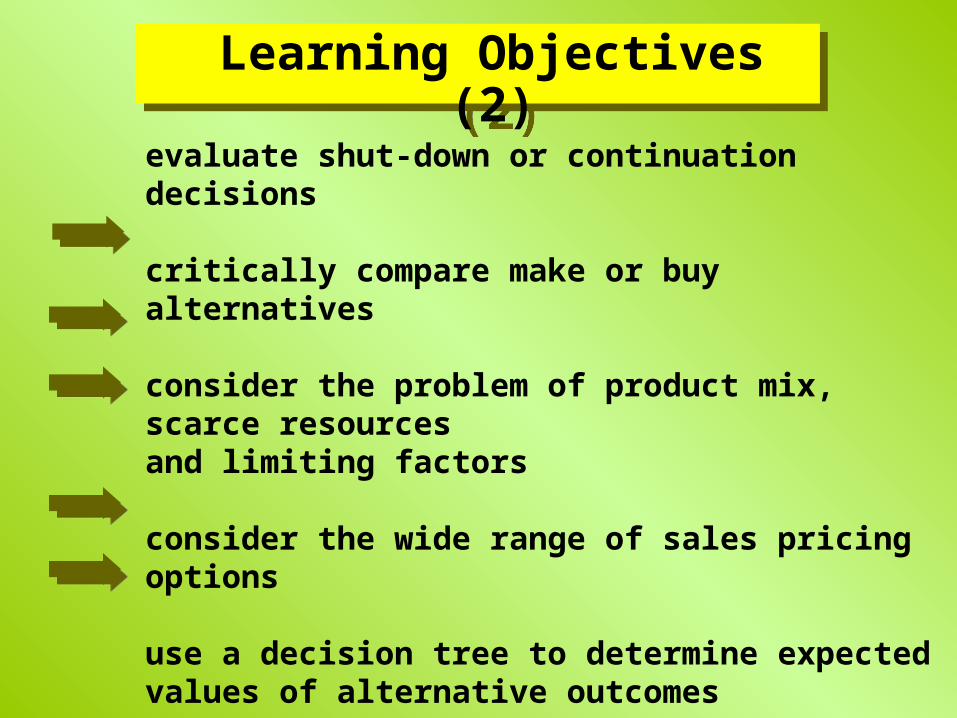

evaluate shut-down or continuation decisions

critically compare make or buy alternatives

consider the problem of product mix, scarce resourcesand limiting factors

consider the wide range of sales pricing options

use a decision tree to determine expected values of alternative outcomes

Learning Objectives (2) Learning Objectives (2)

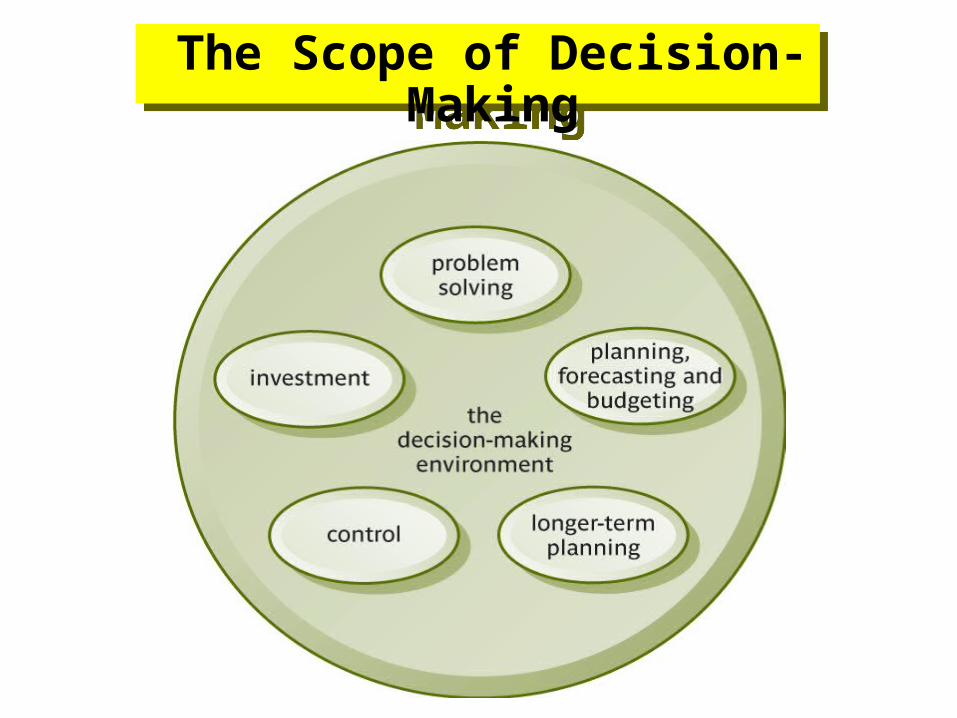

The Scope of Decision-Making

The Scope of Decision-Making

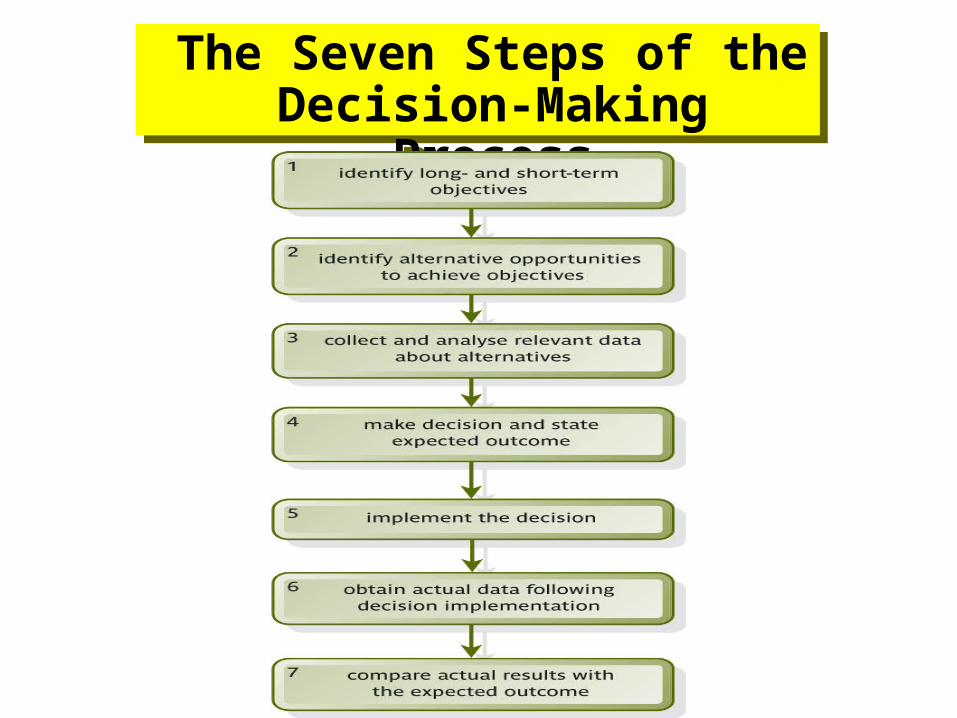

The Seven Steps of the Decision-Making

Process

The Seven Steps of the Decision-Making

Process

the decision-making process includes

identification of relevant costs, and starts

with the identification of objectives

following the implementation of decisions,

the process ends with the comparison of

actual results with expected outcomes

relevant costs, or incremental or

differential costs, arise as direct

consequence of a decision, which may differ

between alternative options

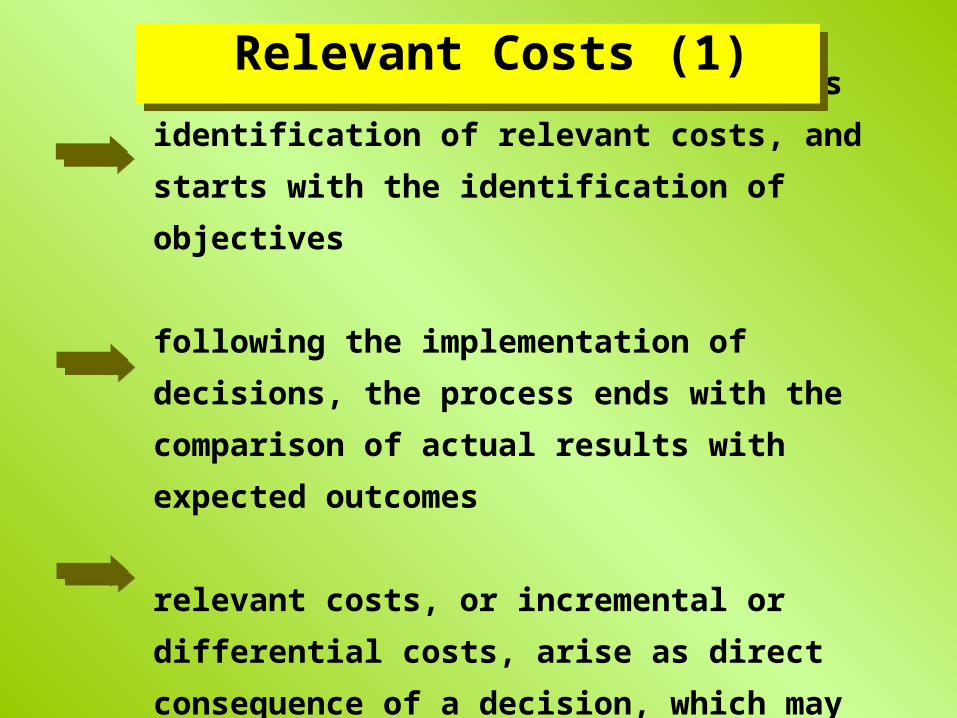

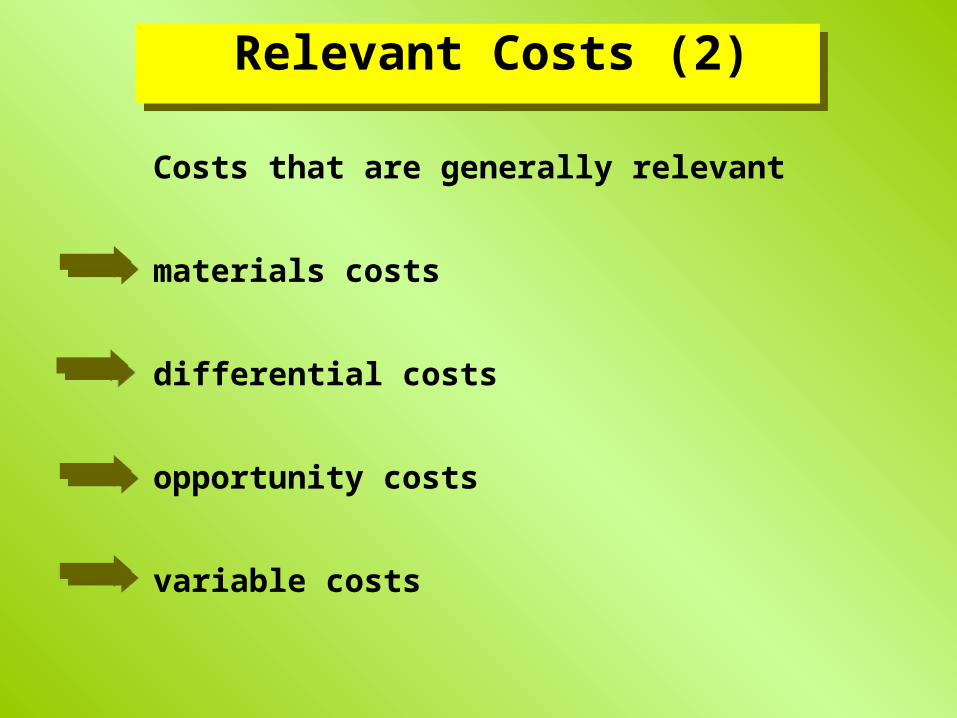

Relevant Costs (1) Relevant Costs (1)

Costs that are generally relevant

materials costs

differential costs

opportunity costs

variable costs

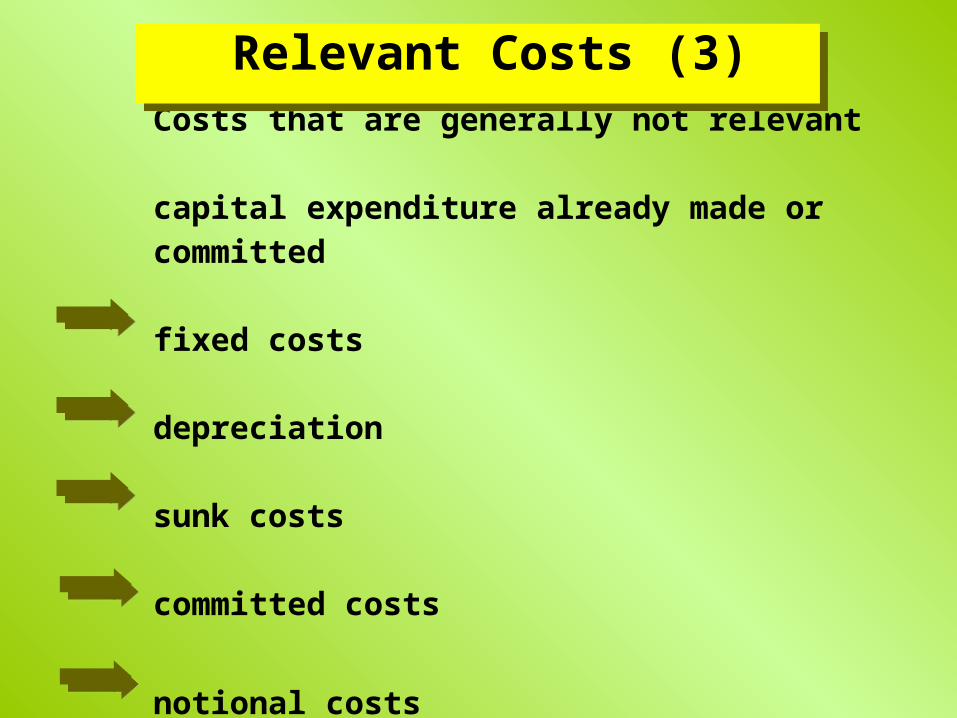

Relevant Costs (2) Relevant Costs (2)

Costs that are generally not relevant

capital expenditure already made or committed

fixed costs

depreciation

sunk costs

committed costs

notional costs

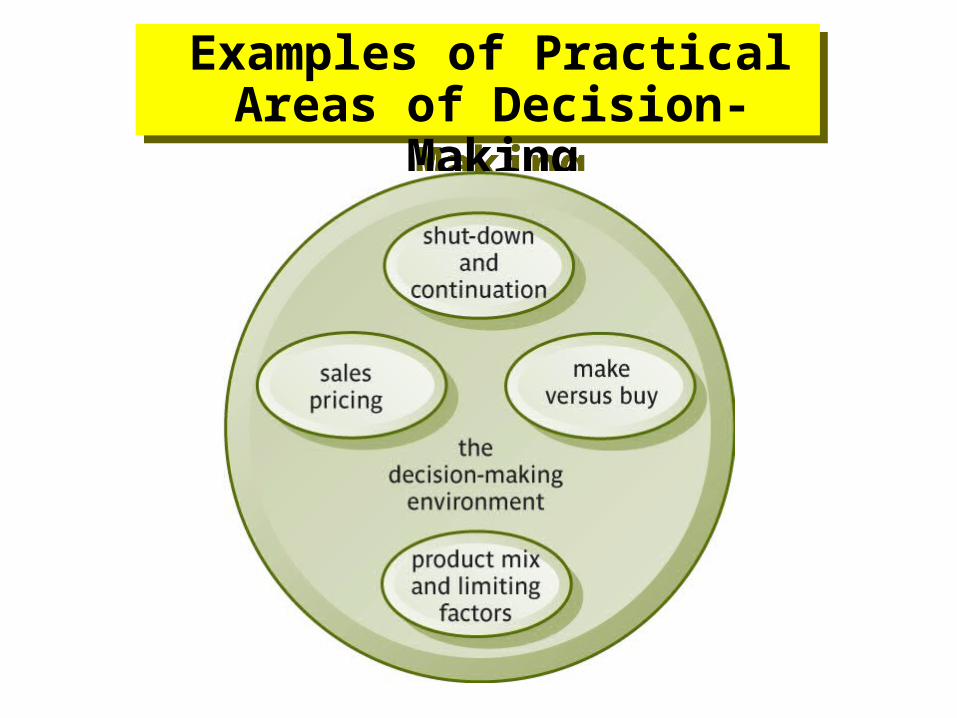

Relevant Costs (3) Relevant Costs (3)

Examples of Practical Areas of Decision-

Making

Examples of Practical Areas of Decision-

Making

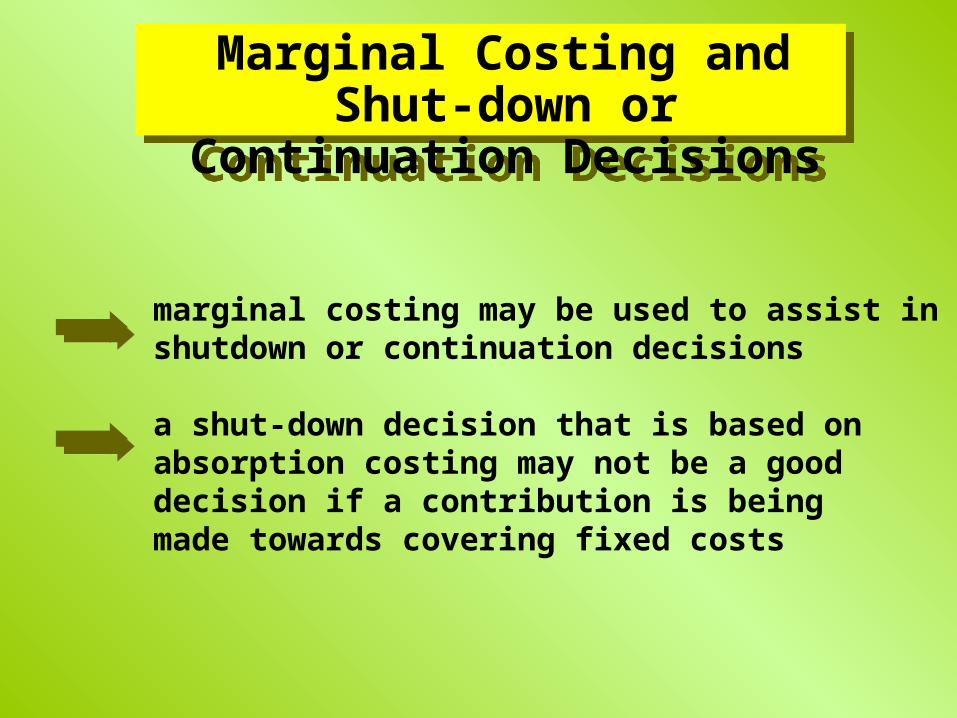

marginal costing may be used to assist in shutdown or continuation decisions

a shut-down decision that is based on absorption costing may not be a good decision if a contribution is beingmade towards covering fixed costs

Marginal Costing and Shut-down or

Continuation Decisions

Marginal Costing and Shut-down or

Continuation Decisions

make versus buy decisions involve

consideration of a wider range of factors

than simply the differences in the basic

cost, for example:

cost price sensitivity

accuracy of data

reliability of bought-in materials

supplier switching costs

delivery reliability

financial stability

cost price stability

opportunity costs

Make versus Buy Make versus Buy

organisations do not have access to unlimited supplies of resources, for example

labour hours

levels of labour skills

machine capacity

time

market demand

components and raw materials

cash

Product Mix Decisions and Limiting Factors

(1)

Product Mix Decisions and Limiting Factors

(1)

a limiting factor is the lack of any resource which limits the activity of the organisation product mix decisions are influenced by the scarcity of resources and the availability of limiting factors

Product Mix Decisions and Limiting Factors

(2)

Product Mix Decisions and Limiting Factors

(2)

sales pricing policy is just one of the four categories of decision included in the marketing mix of

price

product

place

promotion

Sales Pricing (1) Sales Pricing (1)

there is a variety of methods that may be used to determine selling prices, which may be included under the general headings of:

cost plus pricing

pricing based on demand and using market data

sales pricing policy is based on cost and market factors that influence demand for the product

Sales Pricing (2) Sales Pricing (2)

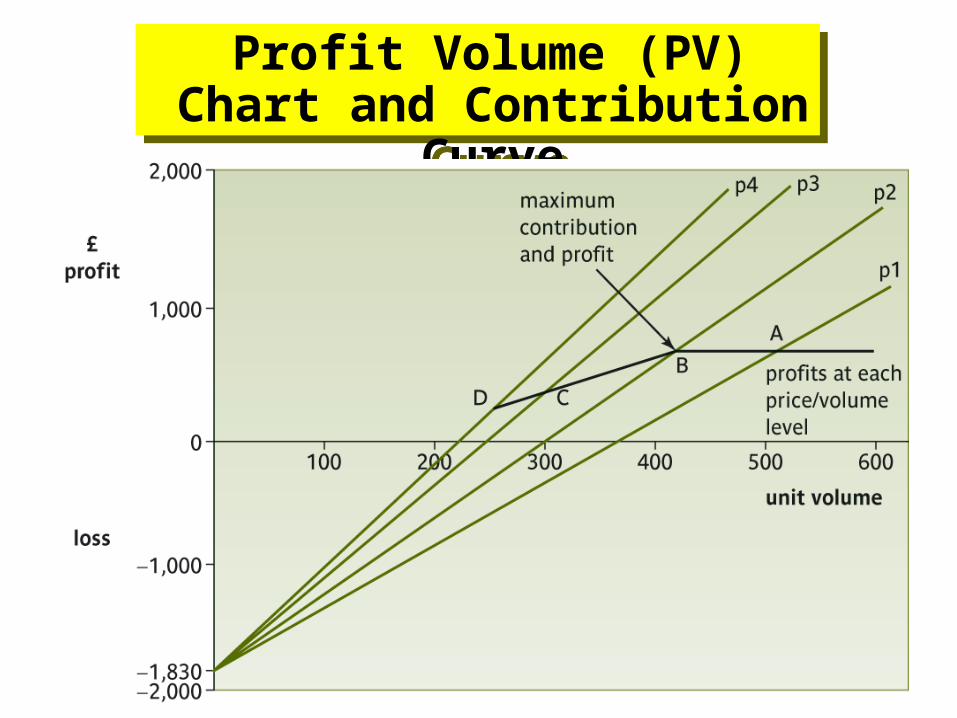

Profit Volume (PV) Chart and Contribution

Curve

Profit Volume (PV) Chart and Contribution

Curve

Profit Volume (PV) Chart and Contribution

Curve Band

Profit Volume (PV) Chart and Contribution

Curve Band

decision trees enable a sequence of interrelated decisions, and their expected outcomes, to be reported pictorially

Decision Trees

Decision Trees

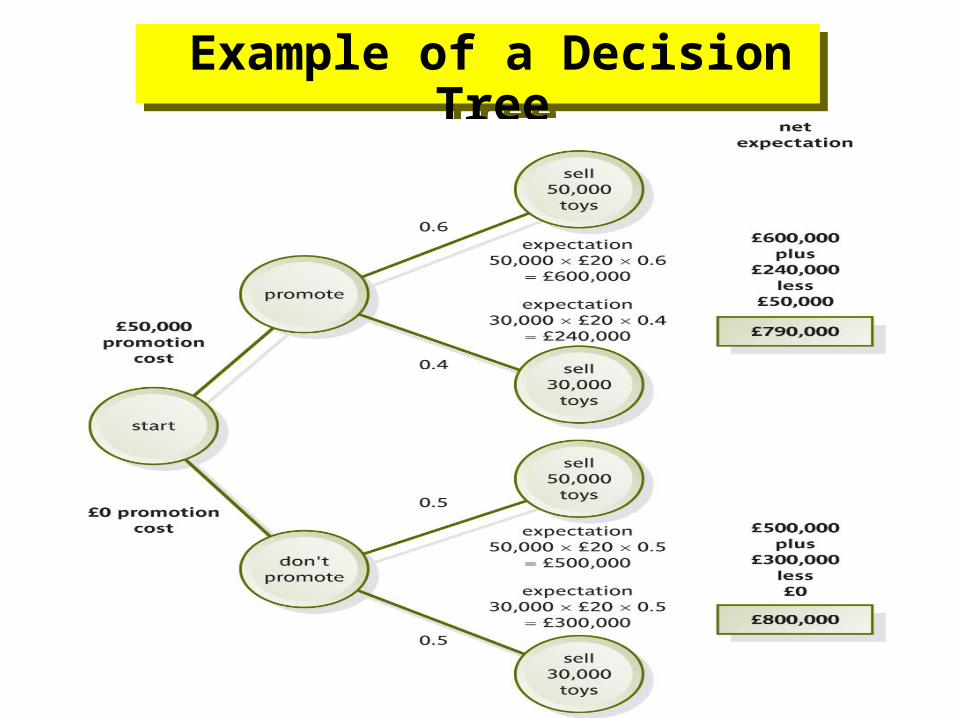

Example of a Decision Tree

Example of a Decision Tree