december 2014. former researcher and lecturer in energy and environmental economics, bocconi...

TRANSCRIPT

December 2014

• Former Researcher and Lecturer in Energy and Environmental Economics, Bocconi University, Milan

• Former Head of Gas Tariff Regulation, Italian Electricity and Gas Regulatory Authority

• Gas Advisor and Instructor, Florence School of Regulation• Consultant of the European Commission, of several energy

regulators (Lithuania, Czech Republic, Turkey, Ukraine, Egypt, Western Balkans), gas companies (ENI, EDF, E.On, ENEL, Gasunie, RWE, SNAM,EGAS…)

• Hired by PUA in 2012 to review Tamar gas contracts

Mr. Sergio AscariMr. Sergio Ascari

2

1. Gas has a significant impact on Israel’s economy and cost of living: within 5 years it will represent 6-8 billion NIS

2. Gas prices in Israel are higher than they need be, but costs could be reduced by 1 – 2 billion NIS each year

3. A cost based price control would be risky

4. This reduction can be achieved by linking prices to international markets, through an export parity approach

5. This price control will reduce regulatory uncertainty and foster the development of resources, starting with Leviathan and smaller fields

Main messagesMain messages

3

Production from Tamar provided a one percentage point boost to Israel's GDP in 2013 (CIA World Factbook)

Gas is going to affect about 25% of electricity tariff Electricity price is a significant factor affecting the CPI,

both directly and indirectly Gas reduces cost of energy for industrial customers by

50-60% Expected gas revenues to the Israeli Government are

in the order of 25-40 billion $ over the next 20 years

Economic macro impact of gasEconomic macro impact of gas

4

Since all new power plants will use gas, impact of gas on generation electricity competition is significant

• Every dollar/MMBtu in gas prices leads to 1.1 billion NIS paid by electricity consumers

• IPP’s are indifferent to their gas contracts and to their load curve, as the PUA is forced to cover the contract costs

• Price, take or pay obligation, gas consumption flexibility all have significant impact on generation competition

Macro impact of gas: the electricity marketMacro impact of gas: the electricity market

5

Problems in gas markets create higher financial barriers and

affect negatively the regulation set by PUA for IPPs and

consumers

Study in 2012 already found that:• Prices were well above any reasonable cost estimate• Indexation was not in line with international practice and not

related to market conditions• Any opening of the electricity market would be difficult under

such conditions, as gas monopolists would dominate the market Evolution since 2012:

• PUA waited for competition to develop, rather than intervening right away, after consultation with the Antitrust Authority

• Yet no new reservoirs appeared and the two main reservoirs (over 80% of resources) are now controlled by the same groups

• Export perspective became a reality• Both Tamar and Leviathan expected to sell to domestic market

and exports

Work done in 2012 for the PUA: findings and changes Work done in 2012 for the PUA: findings and changes sincesince

6

Israel will shortly be integrated with the world market

Israel gas prices increase constantlyIsrael gas prices increase constantlyLatest set of contracts is more Latest set of contracts is more

expensiveexpensive

7

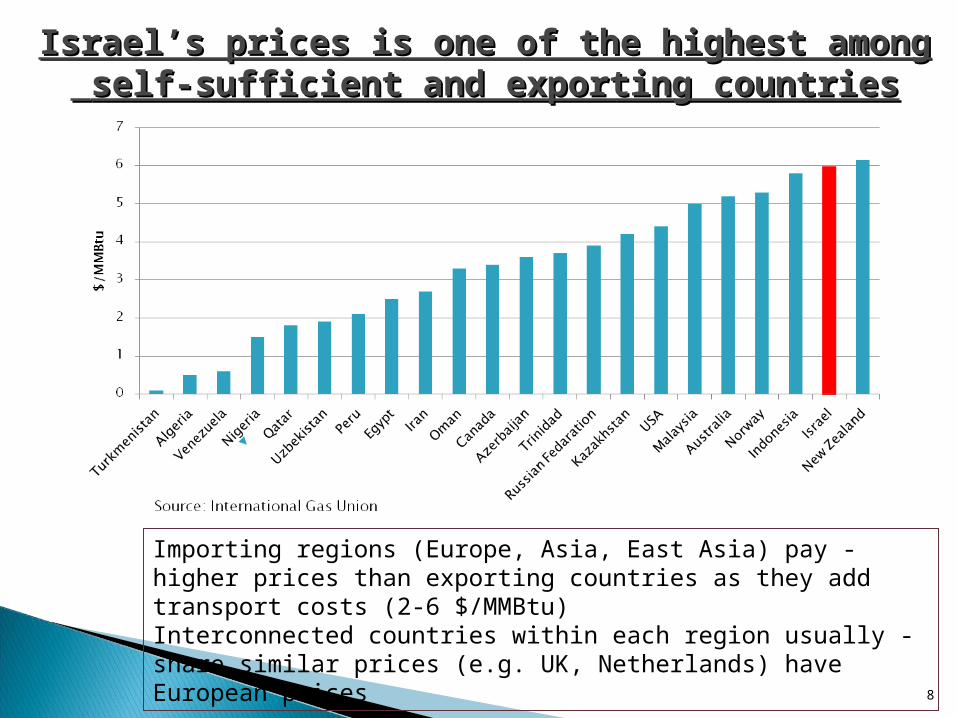

Israel’s prices is one of the highest among Israel’s prices is one of the highest among self-sufficient and exporting countriesself-sufficient and exporting countries

8

-Importing regions (Europe, Asia, East Asia) pay higher prices than exporting countries as they add transport costs (2-6 $/MMBtu)

-Interconnected countries within each region usually share similar prices (e.g. UK, Netherlands) have European prices

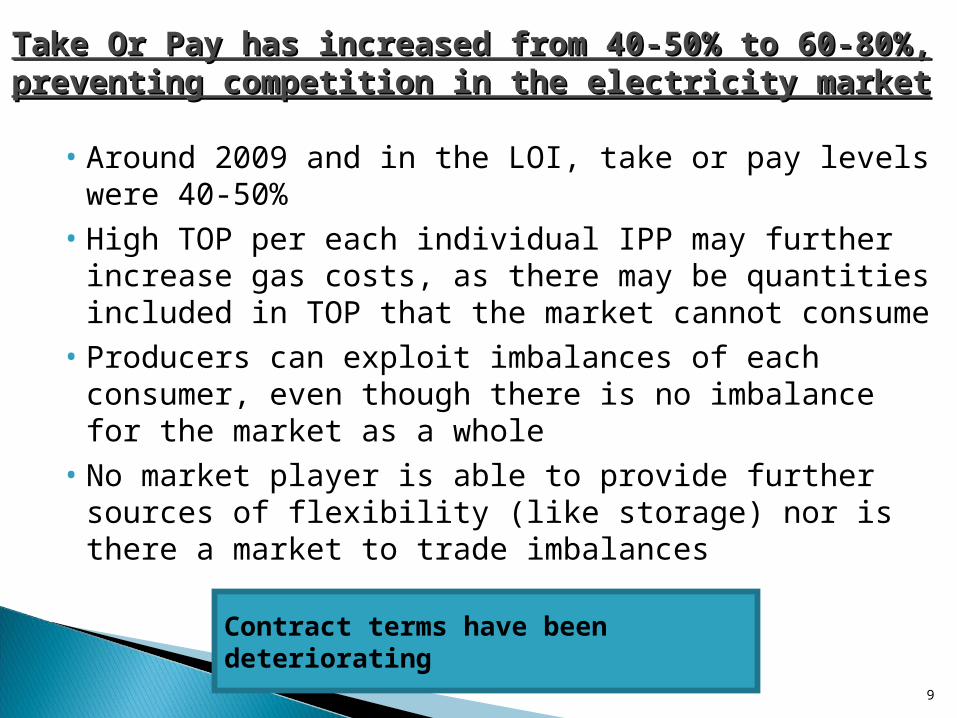

• Around 2009 and in the LOI, take or pay levels were 40-50%

• High TOP per each individual IPP may further increase gas costs, as there may be quantities included in TOP that the market cannot consume

• Producers can exploit imbalances of each consumer, even though there is no imbalance for the market as a whole

• No market player is able to provide further sources of flexibility (like storage) nor is there a market to trade imbalances

Take Or Pay has increased from 40-50% to 60-80%, Take Or Pay has increased from 40-50% to 60-80%, preventing competition in the electricity marketpreventing competition in the electricity market

9

Contract terms have been deteriorating

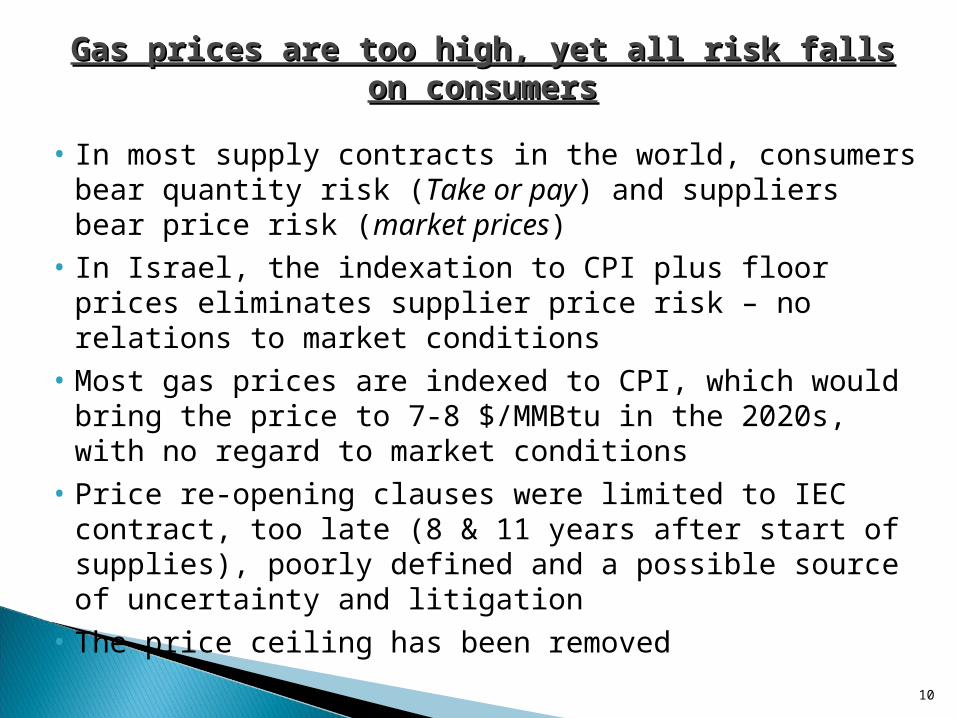

• In most supply contracts in the world, consumers bear quantity risk (Take or pay) and suppliers bear price risk (market prices)

• In Israel, the indexation to CPI plus floor prices eliminates supplier price risk – no relations to market conditions

• Most gas prices are indexed to CPI, which would bring the price to 7-8 $/MMBtu in the 2020s, with no regard to market conditions

• Price re-opening clauses were limited to IEC contract, too late (8 & 11 years after start of supplies), poorly defined and a possible source of uncertainty and litigation

• The price ceiling has been removed

Gas prices are too high, yet all risk falls on Gas prices are too high, yet all risk falls on consumersconsumers

10

Average profitability of Tamar expected at 22-23%, much higher than 8-10% of the oil & gas industry in the world and 12-17% of simulations considered by the Shishinsky Committee

The dominance of the Tamar-Leviathan Consortium could discourage entry by other potential suppliers, as it would be too hard to beat them

Since investors know that gas is overpriced, they still fear that price controls may come, hence uncertainty that may limit entry by other investors

Producer returns Producer returns are too high, leaving few are too high, leaving few hopes for newcomershopes for newcomers

11

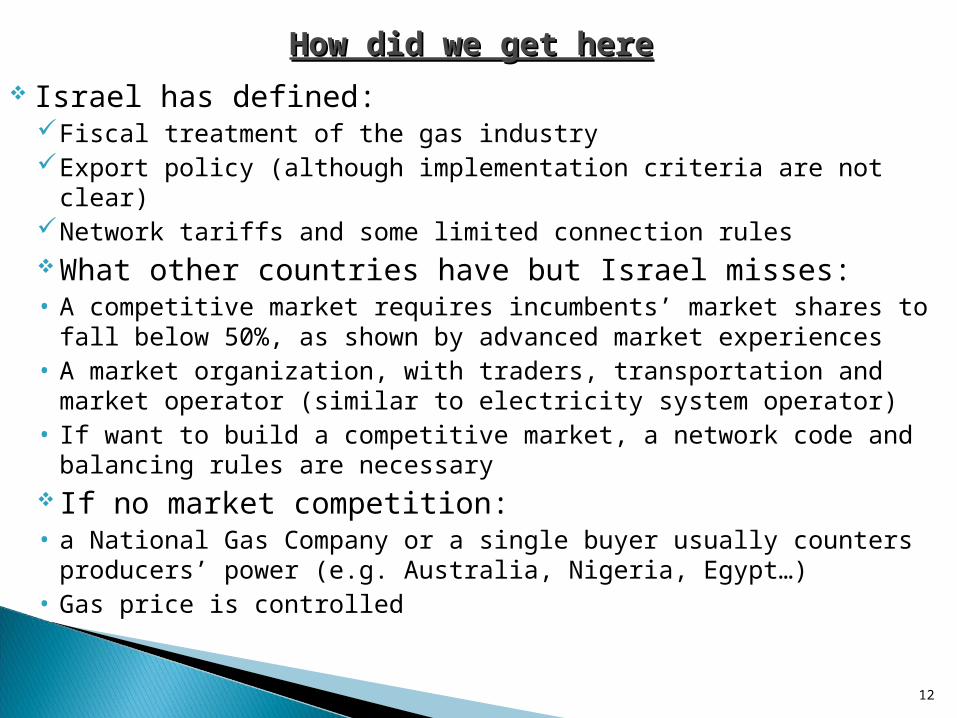

Israel has defined:Fiscal treatment of the gas industry Export policy (although implementation criteria are not clear)Network tariffs and some limited connection rulesWhat other countries have but Israel misses:• A competitive market requires incumbents’ market shares to fall

below 50%, as shown by advanced market experiences• A market organization, with traders, transportation and market

operator (similar to electricity system operator) • If want to build a competitive market, a network code and

balancing rules are necessary If no market competition:• a National Gas Company or a single buyer usually counters

producers’ power (e.g. Australia, Nigeria, Egypt…)• Gas price is controlled

How did we get hereHow did we get here

12

• New study has undertaken a survey of countries and their price regulatory practices, as well as indexation and ancillary conditions

• Covering: USA, EU overview, France, Italy, Netherlands (until 1995), Russia, China, India, Brazil, Argentina, New Zealand (mostly until 2002), Nigeria, Algeria, Egypt (over 50% of world market)

• Main Lessons: All countries have or had regulated gas prices until a working

competitive market started Price control is normally lifted only after competition is found

working Most countries control market also by means of National

Companies, sometimes by Single Buyers, to counteract the market power of monopolies or big international companies

All countries have either a competitive market or a All countries have either a competitive market or a price control. Israel has noneprice control. Israel has none

13

Gas prices are forward looking rather than cost-based Hard to define proper depreciation or depletion rates of natural

resources In advanced markets with high rule of law standards (e.g. USA,

New Zealand), this approach led to burdensome procedures and contributed to slowing investment, triggered a shortage

Cost based price controls are found in less transparent countries, usually negotiated by national companies (e.g. taxes, exploration efforts, royalties) – e.g. China, India, Argentina, Algeria, Nigeria, Egypt

If prices are not market related, they are always “wrong” except by chance• If too high, consumers would pay too much• If too low, producers would be tempted to postpone production

by any means (e.g. reduced maintenance or development of new wells)

Cost based price control is risky in natural gasCost based price control is risky in natural gas

14

LNG Terminal

1pipeline

LNG SHIP

LNG SHIPLNG SHIP

Pipeline 2

Pipeline 3

LNG Terminal

LNG SHIP

Pipeline 3

LNG SHIP

LNG SHIP

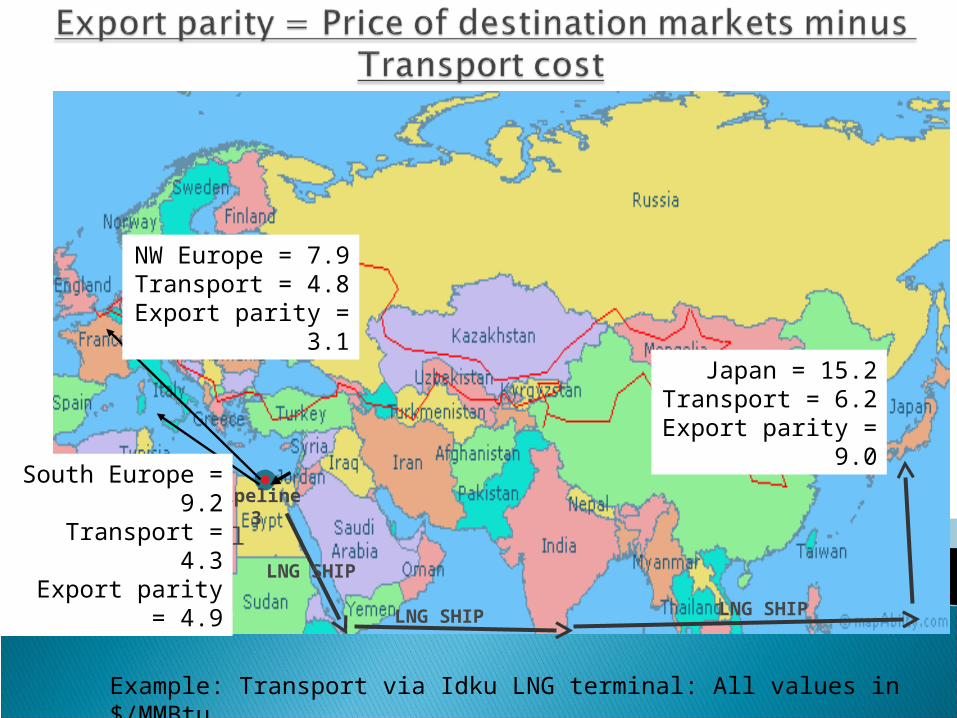

NW Europe = 7.9Transport = 4.8

Export parity = 3.1

Example: Transport via Idku LNG terminal: All values in $/MMBtu

South Europe = 9.2Transport = 4.3

Export parity = 4.9

Japan = 15.2Transport = 6.2

Export parity = 9.0

1. The domestic wholesale prices in Israel should be the same for all fields or other gas sources

2. Equal to prices of destination markets for potential Israeli exports, minus transportation costs

3. Based on competitive and liquid markets that cannot be influenced by suppliers (like small neighboring markets: Jordan, Cyprus, Palestinian Authority)

4. Preliminary estimations are presented, based on the routes Israel Egyptian LNG terminals South Europe (1/3), North-West Europe (1/3), Japan (1/3)

◦ A pipeline route via Turkey-Greece would yield similar results to Europe

◦ An LNG terminal on Israeli or Cyprus coasts (or a floating one) would yield higher transportation costs, due to recent gas liquefaction cost inflation, and hence lower prices in Israel

How to define an export parity price for Israel (1)How to define an export parity price for Israel (1)

16

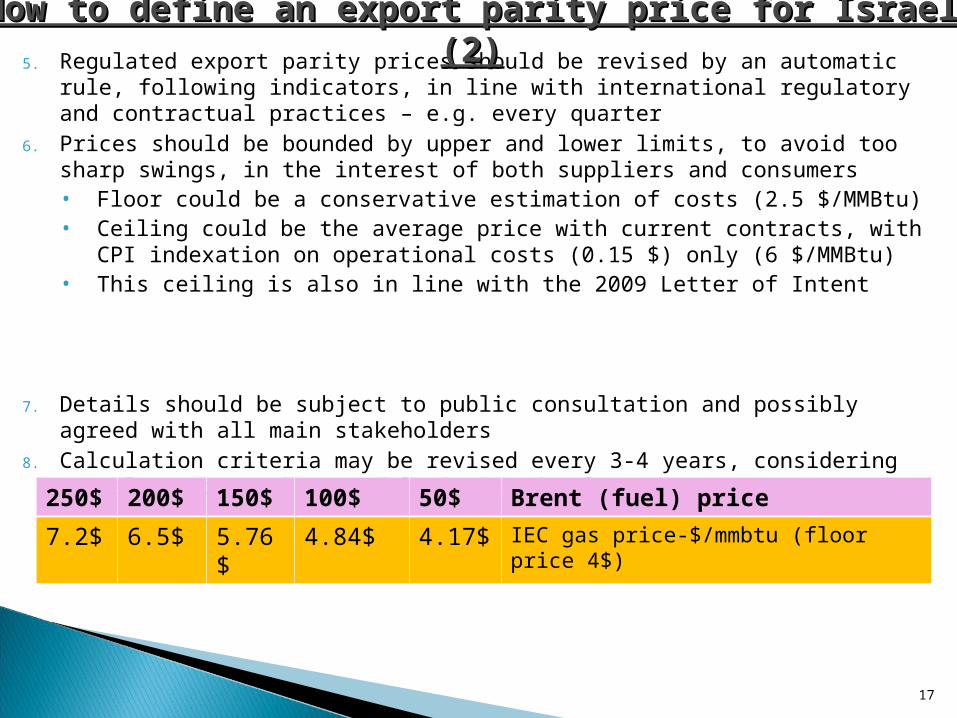

5. Regulated export parity prices should be revised by an automatic rule, following indicators, in line with international regulatory and contractual practices – e.g. every quarter

6. Prices should be bounded by upper and lower limits, to avoid too sharp swings, in the interest of both suppliers and consumers• Floor could be a conservative estimation of costs (2.5 $/MMBtu)• Ceiling could be the average price with current contracts, with

CPI indexation on operational costs (0.15 $) only (6 $/MMBtu) • This ceiling is also in line with the 2009 Letter of Intent

7. Details should be subject to public consultation and possibly agreed with all main stakeholders

8. Calculation criteria may be revised every 3-4 years, considering actual export markets and logistics developments

How to define an export parity price for Israel (2)How to define an export parity price for Israel (2)

17

Brent (fuel) price50$100$150$200$250$

IEC gas price-$/mmbtu (floor price 4$)4.17$4.84$5.76$6.5$7.2$

Simulation of bounded export parity (based on Simulation of bounded export parity (based on 2008-14 prices; average of NW Europe, Italy, Japan; 2008-14 prices; average of NW Europe, Italy, Japan;

$/MMBtu)$/MMBtu)

18

Average = 4.4 $/MMBtu

Simulation of impacts of different pricing criteria on Simulation of impacts of different pricing criteria on producers, consumers and Treasury (Nominal NIS producers, consumers and Treasury (Nominal NIS

billion, 2013-30)billion, 2013-30)

19

In the next 16 years, with export parity, Israeli consumers would save almost 50 billion NIS. Israeli citizens (as consumers and taxpayers) would save over 20 billion NIS.

Export parity price would bring Israel back to Export parity price would bring Israel back to price levels of self sufficient and exporting price levels of self sufficient and exporting

countriescountries

20

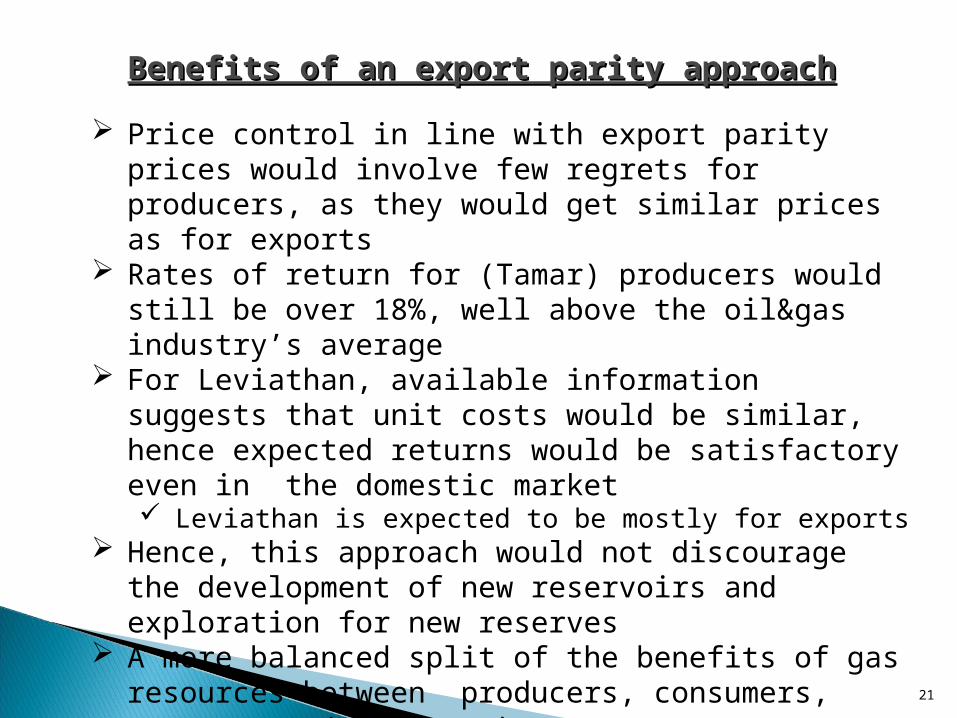

Benefits of an export parity approachBenefits of an export parity approach

21

Price control in line with export parity prices would involve few regrets for producers, as they would get similar prices as for exports

Rates of return for (Tamar) producers would still be over 18%, well above the oil&gas industry’s average

For Leviathan, available information suggests that unit costs would be similar, hence expected returns would be satisfactory even in the domestic market Leviathan is expected to be mostly for exports

Hence, this approach would not discourage the development of new reservoirs and exploration for new reserves

A more balanced split of the benefits of gas resources between producers, consumers, government (taxpayers)

Price risks would fall on both producers and consumers, but would be reduced by the ceiling and floor limits

• The current situation does not reflect a balanced resource and risk allocation between producers and consumers

• The better way to overcome the gas market abuse is by creating a significantly competitive market

• Until that happens there is a need for price control, as done everywhere in the world

• A market based price control is preferred over a cost based one, as implemented in North America and a few European countries (for small customers)

• Without regulatory intervention, damage to Israeli economy and public good is likely to worsen

Final ConclusionsFinal Conclusions

22

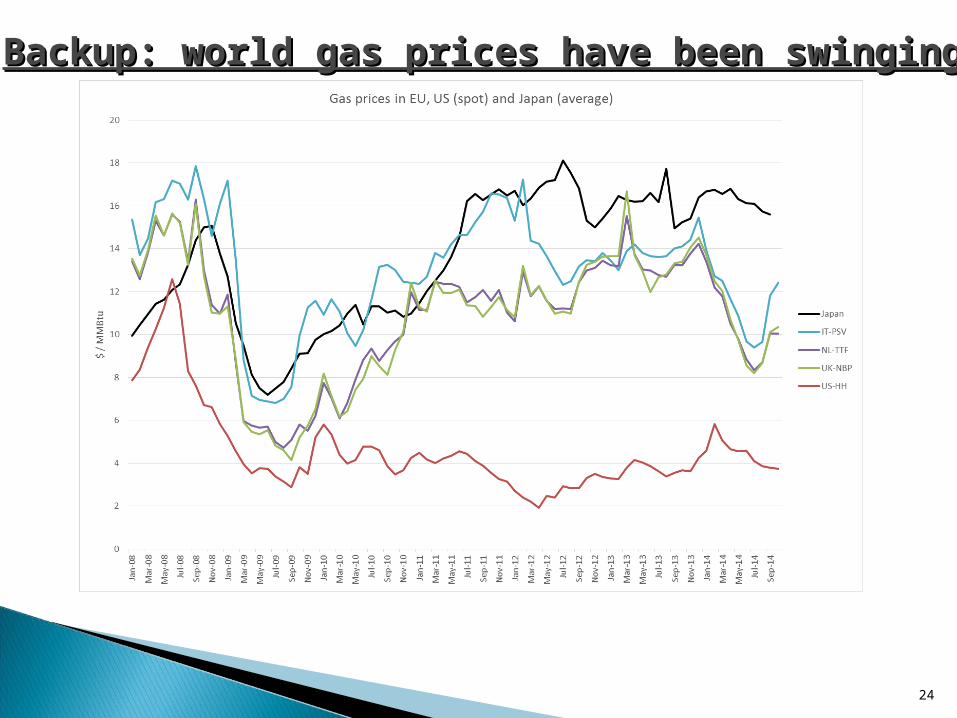

Backup: world gas prices have been swingingBackup: world gas prices have been swinging

24

• In US, Central Europe, market competition has been achieved by pooling the markets of several countries, so that national dominant companies have to compete with each other

• This requires an interconnected transportation network, with clear and friendly access rules

• In UK, Italy, Spain, Turkey (then rather isolated markets), “gas release” programs were undertaken, which led to gas supply contracts of volumes transferred to other suppliers

• In all cases, competition became significant only after dominant suppliers’ market share in the “relevant” (integrated) market fell below 50%

Backup: Developing a competitive marketBackup: Developing a competitive market

25

• Ancillary conditions (e.g. take or pay, flexibility, duration of contracts, destination clauses) depend on availability of alternative fuels, demand characteristics – often not public

• Little information from the international survey• No take or pay level as such is “high” or “low”• The price control could foresee higher prices for lower

flexibility, in line with higher costs of lowering take or pay levels

Backup: Proposal for Take or payBackup: Proposal for Take or pay

26