december 2013 strengthening and expanding our...

TRANSCRIPT

December 2013

Strengthening and Expanding our Platform – The Acquisition of General Chemical

2

Special Note Regarding Forward-looking Statements

This presentation contains certain statements which may constitute “forward-looking” statements within the meaning of certain securities laws, including the “safe harbour” provisions of the Securities Act (Ontario). The use of any of the words “anticipate”, “continue”, “estimate”, “expect”, “may”, “will”, “project”, “should”, “believe” and similar expressions are intended to identify forward-looking statements. This presentation contains forward-looking statements about the objectives, strategies, financial condition, results of operations and businesses of Chemtrade Logistics Income Fund. These statements are “forward-looking” as they are based on current expectations about our business and the markets we operate in, and on various estimates and assumptions. Forward-looking statements in this presentation describe our expectations as of the date of this presentation. Our actual results could be materially different from our expectations if known or unknown risks affect our business, or if our estimates or assumptions turn out to be inaccurate. As a result, we cannot guarantee that any forward-looking statement will materialize. Forward-looking statements do not take into account the effect that transactions or non-recurring items announced or occurring after the statements are made may have on our business. We disclaim any intention or obligation to update any forward-looking statement even if new information becomes available, as a result of future events or for any other reason. Risks that could cause our actual results to differ materially from our current expectations are discussed in the RISK FACTORS section of our Annual Information Form and the RISKS AND UNCERTAINTIES section of our most recent Management’s Discussion & Analysis. Further information can be found in the disclosure documents filed by Chemtrade Logistics Income Fund with the securities regulatory authorities, available on www.sedar.com.

Note: unless otherwise specified, all dollar amounts in this presentation are in Canadian dollars. This presentation contains non-IFRS financial measures and data, including, but not limited to, EBITDA, EBITDA margin, distributable cash, free cash flow conversion, payout ratio, leverage and General Chemical’s financial measures, which are prepared in accordance with US GAAP.

3

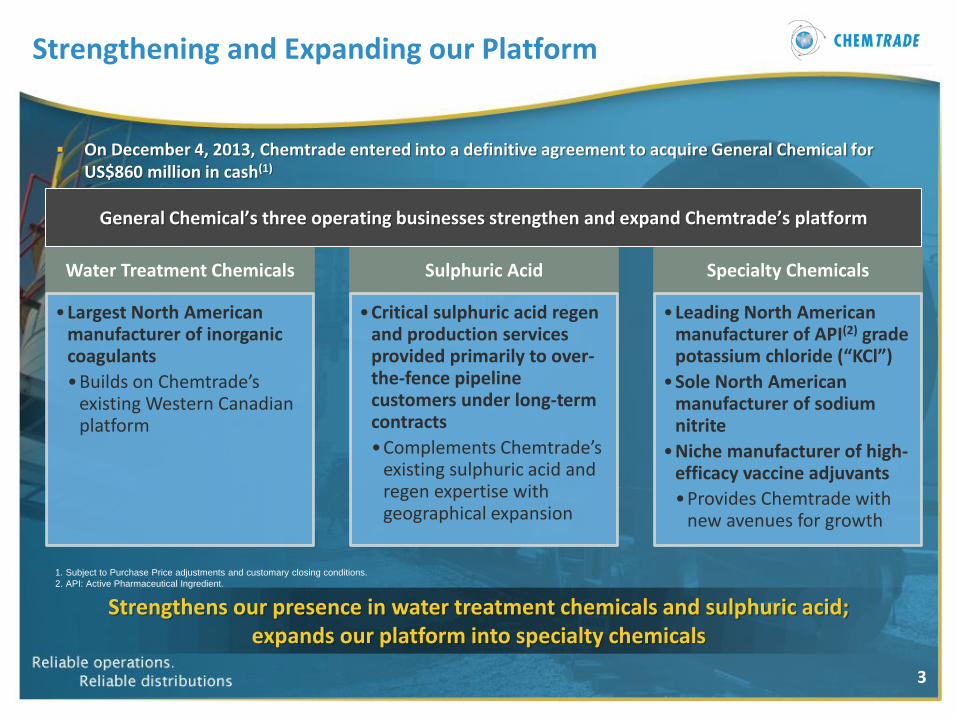

Strengthening and Expanding our Platform

Water Treatment Chemicals

•Largest North American manufacturer of inorganic coagulants

•Builds on Chemtrade’s existing Western Canadian platform

Sulphuric Acid

•Critical sulphuric acid regen and production services provided primarily to over-the-fence pipeline customers under long-term contracts

•Complements Chemtrade’s existing sulphuric acid and regen expertise with geographical expansion

Specialty Chemicals

•Leading North American manufacturer of API(2) grade potassium chloride (“KCl”)

•Sole North American manufacturer of sodium nitrite

•Niche manufacturer of high-efficacy vaccine adjuvants

•Provides Chemtrade with new avenues for growth

Strengthens our presence in water treatment chemicals and sulphuric acid; expands our platform into specialty chemicals

General Chemical’s three operating businesses strengthen and expand Chemtrade’s platform

On December 4, 2013, Chemtrade entered into a definitive agreement to acquire General Chemical for US$860 million in cash(1)

1. Subject to Purchase Price adjustments and customary closing conditions.

2. API: Active Pharmaceutical Ingredient.

4

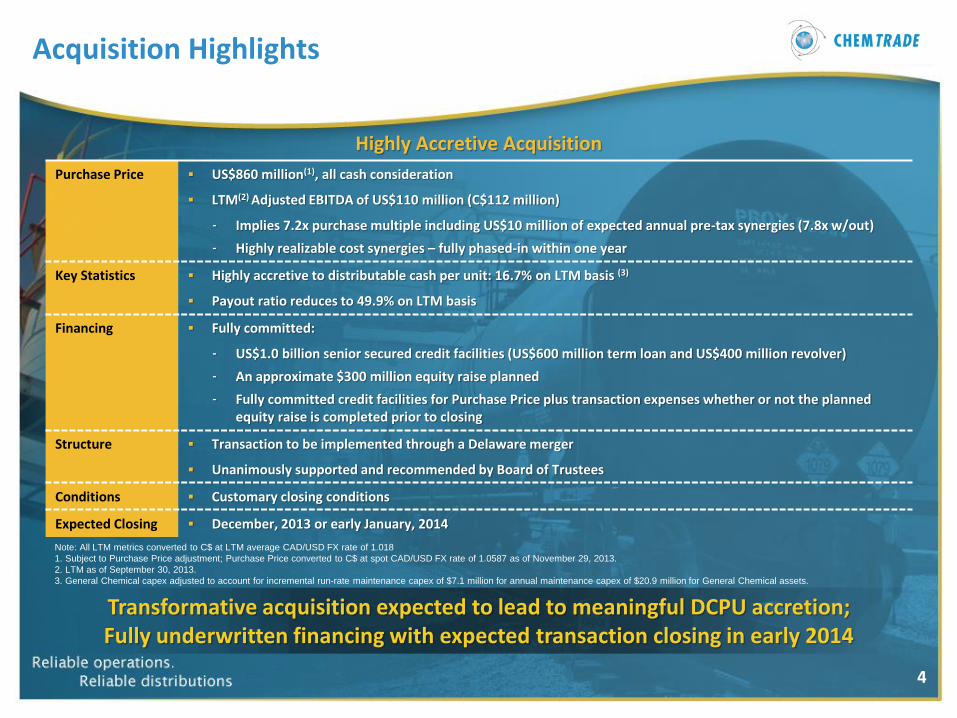

Acquisition Highlights

Highly Accretive Acquisition

Purchase Price US$860 million(1), all cash consideration

LTM(2) Adjusted EBITDA of US$110 million (C$112 million)

- Implies 7.2x purchase multiple including US$10 million of expected annual pre-tax synergies (7.8x w/out)

- Highly realizable cost synergies – fully phased-in within one year

Key Statistics Highly accretive to distributable cash per unit: 16.7% on LTM basis (3)

Payout ratio reduces to 49.9% on LTM basis

Financing Fully committed:

- US$1.0 billion senior secured credit facilities (US$600 million term loan and US$400 million revolver)

- An approximate $300 million equity raise planned

- Fully committed credit facilities for Purchase Price plus transaction expenses whether or not the planned equity raise is completed prior to closing

Structure Transaction to be implemented through a Delaware merger

Unanimously supported and recommended by Board of Trustees

Conditions Customary closing conditions

Expected Closing December, 2013 or early January, 2014

Note: All LTM metrics converted to C$ at LTM average CAD/USD FX rate of 1.018

1. Subject to Purchase Price adjustment; Purchase Price converted to C$ at spot CAD/USD FX rate of 1.0587 as of November 29, 2013.

2. LTM as of September 30, 2013.

3. General Chemical capex adjusted to account for incremental run-rate maintenance capex of $7.1 million for annual maintenance capex of $20.9 million for General Chemical assets.

Transformative acquisition expected to lead to meaningful DCPU accretion; Fully underwritten financing with expected transaction closing in early 2014

5

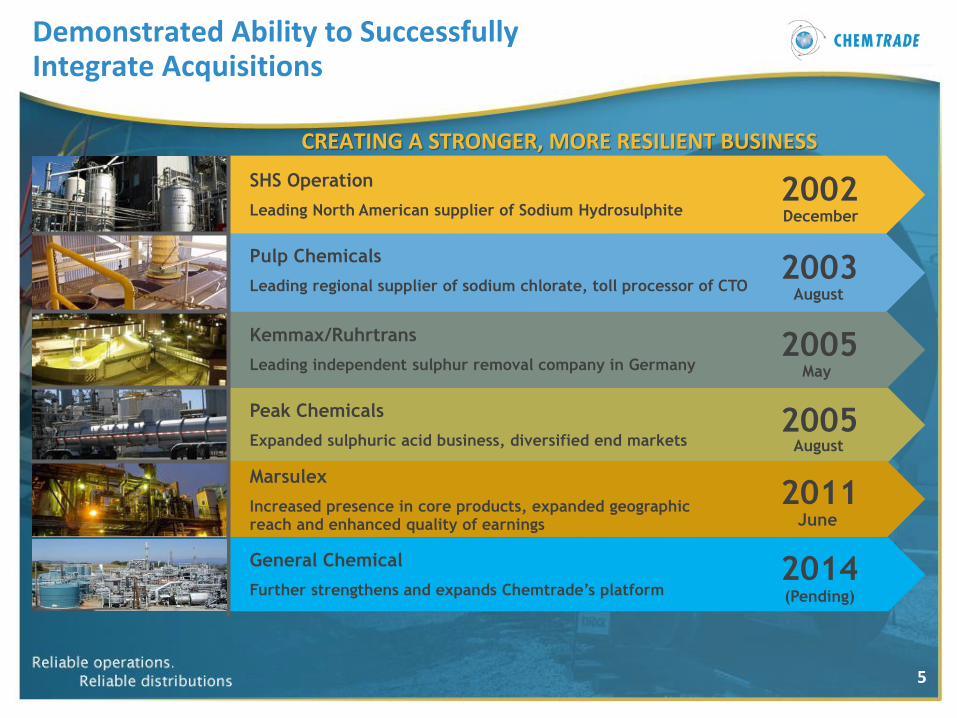

SHS Operation

Leading North American supplier of Sodium Hydrosulphite

Pulp Chemicals

Leading regional supplier of sodium chlorate, toll processor of CTO

Kemmax/Ruhrtrans

Leading independent sulphur removal company in Germany

Peak Chemicals

Expanded sulphuric acid business, diversified end markets

Marsulex

Increased presence in core products, expanded geographic reach and enhanced quality of earnings

General Chemical

Further strengthens and expands Chemtrade’s platform

2002 December

2003 August

2005 May

2005 August

2011 June

2014 (Pending)

CREATING A STRONGER, MORE RESILIENT BUSINESS

Demonstrated Ability to Successfully Integrate Acquisitions

6

$26

$44 $54 $59 $65 $69

$119

$81 $71

$115

$142 $143

$10

$112

$265

12.7%

15.1% 15.6%

13.9%

11.8% 12.6%

10.1%

14.8%

12.7% 13.0%

15.4%

21.2%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 Sept-13PF LTM

Chemtrade General Chemical Synergies EBITDA Margin

SHS Operation ($98 mm)

Pulp Chemicals($117 mm)

Kemmax/Ruhrtrans;

Peak($216 mm)

Marsulex($420 mm)

Transaction Continues Chemtrade’s Strong Growth Trajectory

1. Including pro forma annualized cost synergies of US$10 million, translated to Canadian dollars.

Continued expansion and strengthening of the Chemtrade platform

2002 to 2012 EBITDA CAGR of 18.3%

Pro forma EBITDA increases by 85%(1)

Industry-leading pro forma EBITDA margins

Track Record of Growth (EBITDA)

Nearly doubles LTM EBITDA and results in industry-leading margins

($ millions)

7

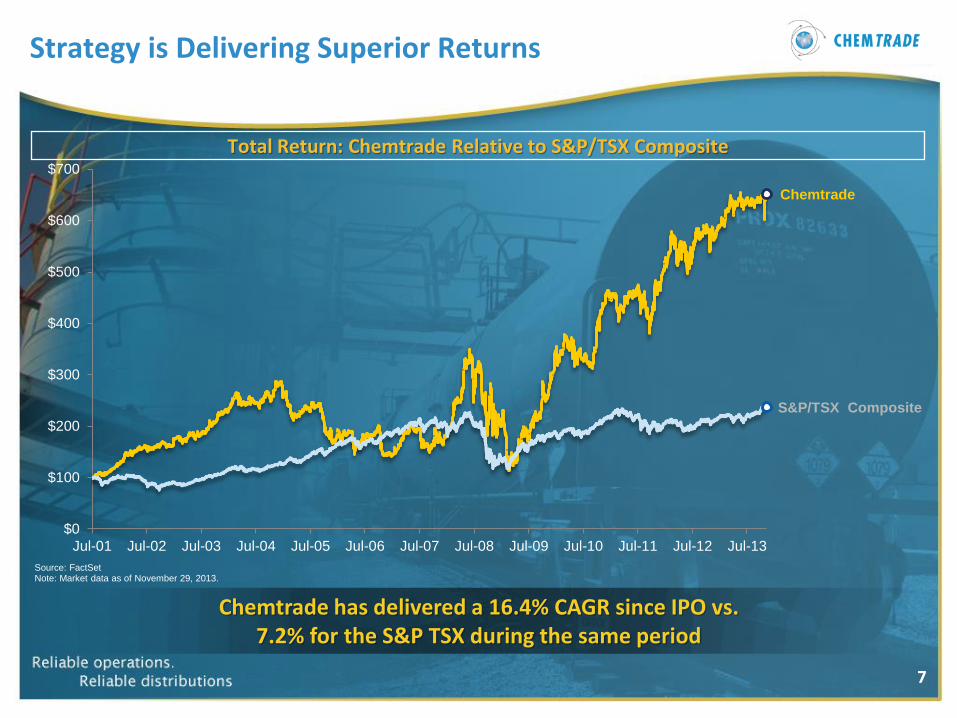

Strategy is Delivering Superior Returns

Source: FactSet Note: Market data as of November 29, 2013.

Chemtrade has delivered a 16.4% CAGR since IPO vs. 7.2% for the S&P TSX during the same period

Total Return: Chemtrade Relative to S&P/TSX Composite

Chemtrade

S&P/TSX Composite

$0

$100

$200

$300

$400

$500

$600

$700

Jul-01 Jul-02 Jul-03 Jul-04 Jul-05 Jul-06 Jul-07 Jul-08 Jul-09 Jul-10 Jul-11 Jul-12 Jul-13

8

Water Treatment Chemicals

$223 57%

Sulphuric Acid$93 24%

Speciality Chemicals

$69 18%

Corp/Other; $51%

General Chemical Business Overview

Water Treatment Chemicals

Largest North American manufacturer of inorganic coagulants used in water treatment process

- Products include Aluminum Sulphate, Other Aluminum Salts, Iron Salts, Alkali and Disinfectant

Sulphuric Acid

Regeneration and production services provided primarily to over-the-fence pipeline customers under long-term contracts

- Acid Regeneration, High Strength Sulphuric Acid, Merchant Acid and By-Products

Specialty Chemicals

Provides niche chemicals

- Products include Sodium Nitrite and High-Purity Potassium Chloride and Vaccine Adjuvants

Overview

Broad geographic scope and diverse product portfolio

LTM Revenue US$390 million

Note: LTM as of September 30, 2013

(US$ millions)

9

Products serve primarily municipal & industrial customers

Aluminum sulphate (“Alum”) and related blends – Most established coagulant used in water treatment

Other Aluminum Salts – Aluminum chlorohydrate ("ACH") and polyaluminum chloride ("PAC") used to remove impurities in water and manage pH

Iron Salts (ferric) – Can yield improved organic removal versus other coagulants

Disinfectant – Liquid aluminum sulphate used in distribution system disinfection

Strategically located facilities in close proximity to established, stable customer base to minimize freight costs

Water Treatment Overview

Product Offering Overview 39 Facilities Serving Diverse Customer Base

10

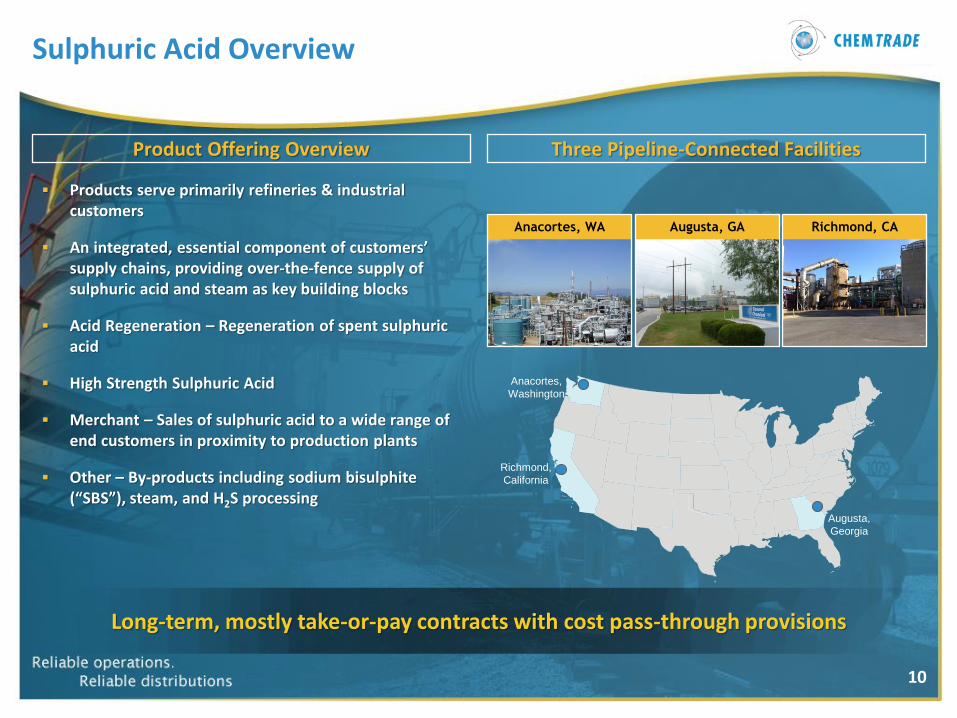

Product Offering Overview Three Pipeline-Connected Facilities

Richmond,

California

Anacortes,

Washington

Augusta,

Georgia

Sulphuric Acid Overview

Anacortes, WA Augusta, GA Richmond, CA

Products serve primarily refineries & industrial customers

An integrated, essential component of customers’ supply chains, providing over-the-fence supply of sulphuric acid and steam as key building blocks

Acid Regeneration – Regeneration of spent sulphuric acid

High Strength Sulphuric Acid

Merchant – Sales of sulphuric acid to a wide range of end customers in proximity to production plants

Other – By-products including sodium bisulphite (“SBS”), steam, and H2S processing

Long-term, mostly take-or-pay contracts with cost pass-through provisions

11

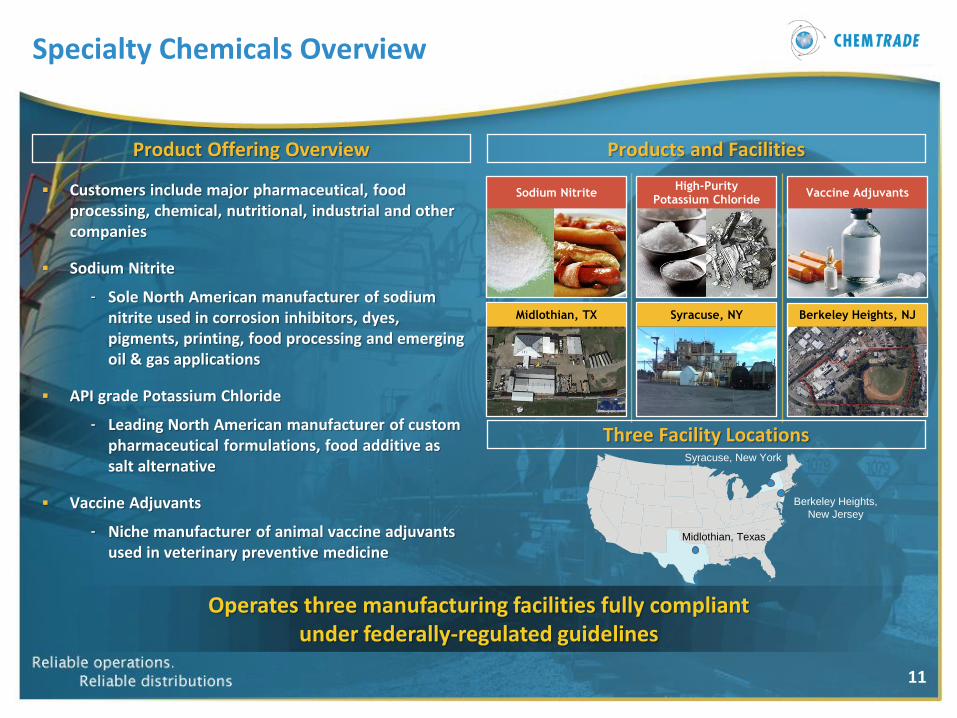

Product Offering Overview Products and Facilities

Specialty Chemicals Overview

Midlothian, Texas

Syracuse, New York

Berkeley Heights,

New Jersey

Sodium Nitrite High-Purity

Potassium Chloride Vaccine Adjuvants

Syracuse, NY Berkeley Heights, NJ Midlothian, TX

Three Facility Locations

Customers include major pharmaceutical, food processing, chemical, nutritional, industrial and other companies

Sodium Nitrite

- Sole North American manufacturer of sodium nitrite used in corrosion inhibitors, dyes, pigments, printing, food processing and emerging oil & gas applications

API grade Potassium Chloride

- Leading North American manufacturer of custom pharmaceutical formulations, food additive as salt alternative

Vaccine Adjuvants

- Niche manufacturer of animal vaccine adjuvants used in veterinary preventive medicine

Operates three manufacturing facilities fully compliant under federally-regulated guidelines

12

Industrial & Manufacturing

35%

Water Treatment34%

Pulp & Paper11%

Oil & Gas9%

Food / Pharma9%

Metals & Mining: 2.0%

Pulp & Paper

Chemicals (Toll-contract)

Plastics & Fibres

Paints & Dyes

Metal Treatment

Custom Pharmaceutical

Municipalities

Agriculture

Chemicals

Mining

Metals

Environmental

Rendering

Building Materials

General Chemical has Well-Balanced End-Market Exposure

Note: Based on 2012 revenue data

End-Market Exposure Detailed End-Market Exposure

Salt Alternative

Vitamin / Nutraceutical

Tantalum Refinement

Dialysis

Processed Meat

Custom Pharmaceutical

Detailed End-Market Exposure

Revenue base supported by a variety of complementary end-markets

Regen / Hydrogen sulfide (H2S) Processing

Metals & Mining

13

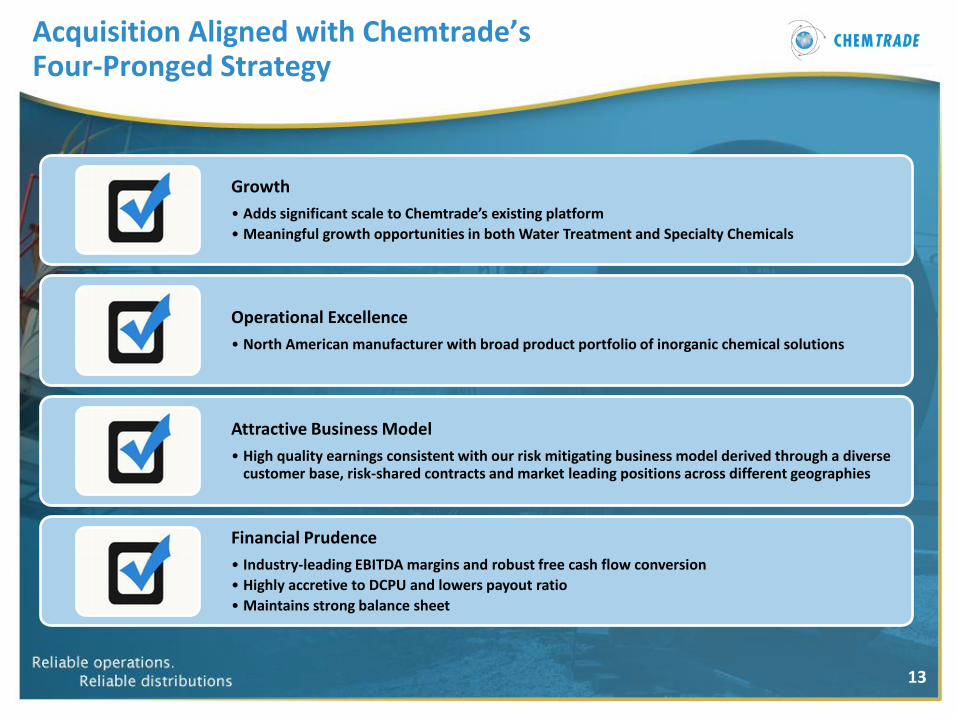

Acquisition Aligned with Chemtrade’s Four-Pronged Strategy

Growth

• Adds significant scale to Chemtrade’s existing platform

• Meaningful growth opportunities in both Water Treatment and Specialty Chemicals

Operational Excellence

• North American manufacturer with broad product portfolio of inorganic chemical solutions

Attractive Business Model

• High quality earnings consistent with our risk mitigating business model derived through a diverse customer base, risk-shared contracts and market leading positions across different geographies

Financial Prudence

• Industry-leading EBITDA margins and robust free cash flow conversion

• Highly accretive to DCPU and lowers payout ratio

• Maintains strong balance sheet

14

Water Treatment Chemicals Specialty Chemicals

Growth: Attractive Growth Opportunities

Proprietary licensed alkali technology – Lower maintenance pH corrector alternative to dry lime or caustic soda

- 10-year exclusivity for 43 states and Canada

- Allows General Chemical to provide efficient and non-hazardous alkali alternative

Demonstrated platform for bolt-on acquisitions

Other niche opportunities for further growth

Augments existing portfolio with products serving new end-markets with attractive growth profiles

Opportunities for new applications and end-market expansion

- Sodium Nitrite

Only FDA-approved provider for use in processed meat additives

Potential oil & gas opportunities

- Potassium Chloride

Pharma, vitamin and nutraceutical applications

Food additive as a salt alternative

15

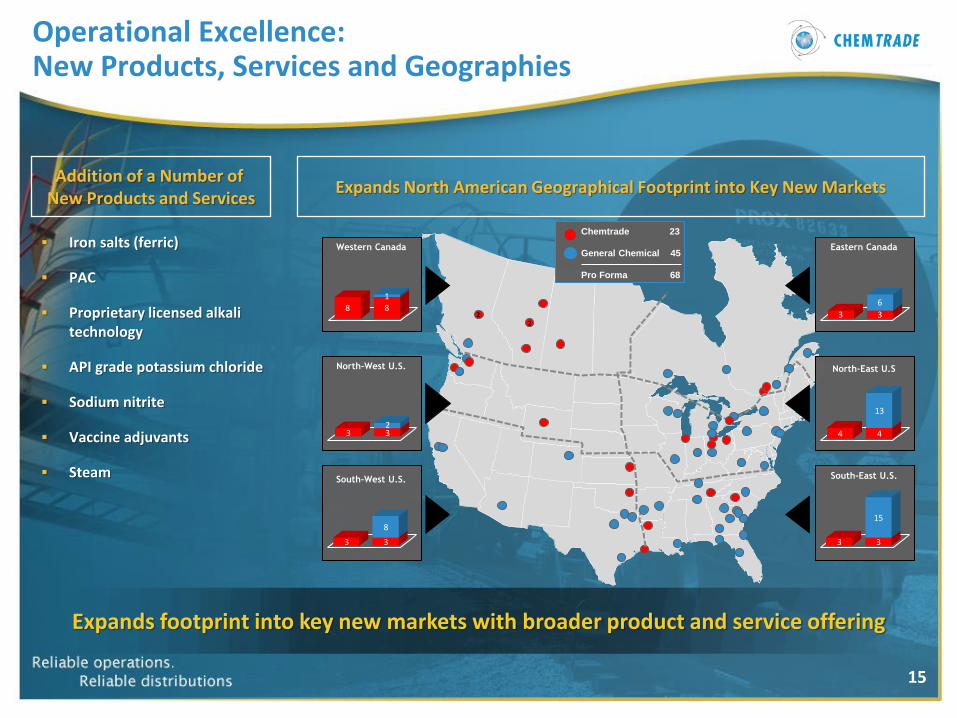

Operational Excellence: New Products, Services and Geographies

Iron salts (ferric)

PAC

Proprietary licensed alkali technology

API grade potassium chloride

Sodium nitrite

Vaccine adjuvants

Steam

Expands North American Geographical Footprint into Key New Markets Addition of a Number of

New Products and Services

Expands footprint into key new markets with broader product and service offering

Chemtrade 23

General Chemical 45

Pro Forma 68

2

2

Western Canada

North-West U.S.

South-West U.S.

Eastern Canada

North-East U.S

South-East U.S.

8 82 2 3 3 3 3 4 4 3 3

1

38 6

13 15

8 82 2 3 3 3 3 4 4 3 3

1

38 6

13 15

8 82 2 3 3 3 3 4 4 3 3

1

38 6

13 15

8 82 2 3 3 3 3 4 4 3 3

1

38 6

13 15

8 82 2 3 3 3 3 4 4 3 3

1

38 6

13 15

8 83 3 3 3 3 3 4 4 3 3

12

8 6

13 15

16

Industrial & Manufacturing

31%

Water Treatment

2% Pulp & Paper29%

Oil & Gas23%

Food / Pharma

2%

Metals & Mining

7%

Fertilizer6%

Industrial & Manufacturing

32%

Water Treatment

14%

Pulp & Paper 23%

Oil & Gas 18%

Food / Pharma

4%

Metals & Mining

6%

Fertilizer 4%

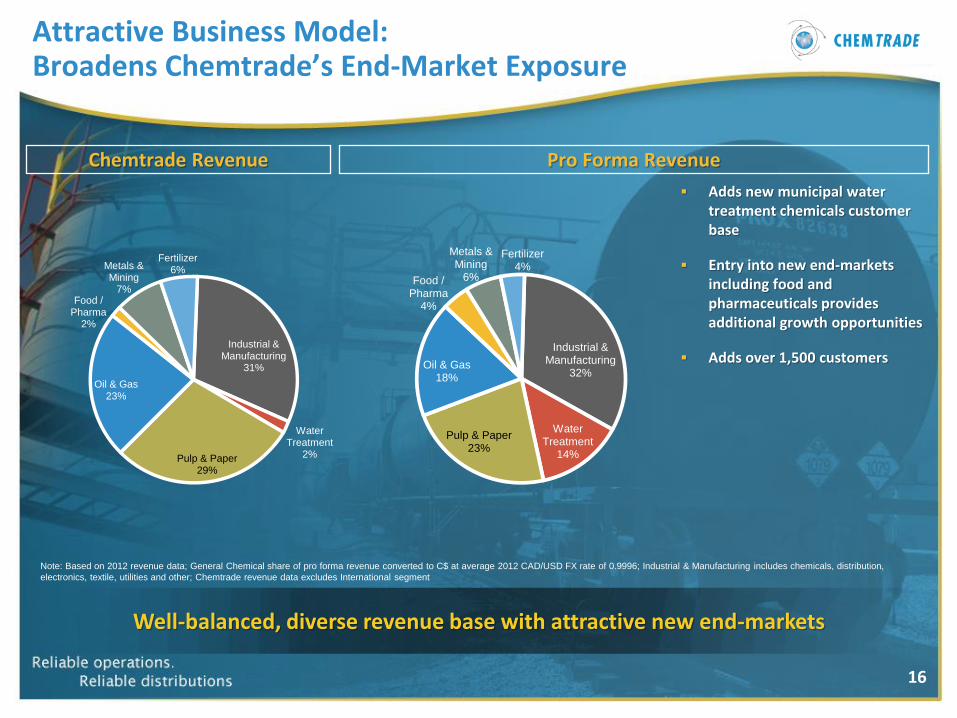

Attractive Business Model: Broadens Chemtrade’s End-Market Exposure

Adds new municipal water treatment chemicals customer base

Entry into new end-markets including food and pharmaceuticals provides additional growth opportunities

Adds over 1,500 customers

Pro Forma Revenue Chemtrade Revenue

Well-balanced, diverse revenue base with attractive new end-markets

Note: Based on 2012 revenue data; General Chemical share of pro forma revenue converted to C$ at average 2012 CAD/USD FX rate of 0.9996; Industrial & Manufacturing includes chemicals, distribution,

electronics, textile, utilities and other; Chemtrade revenue data excludes International segment

17

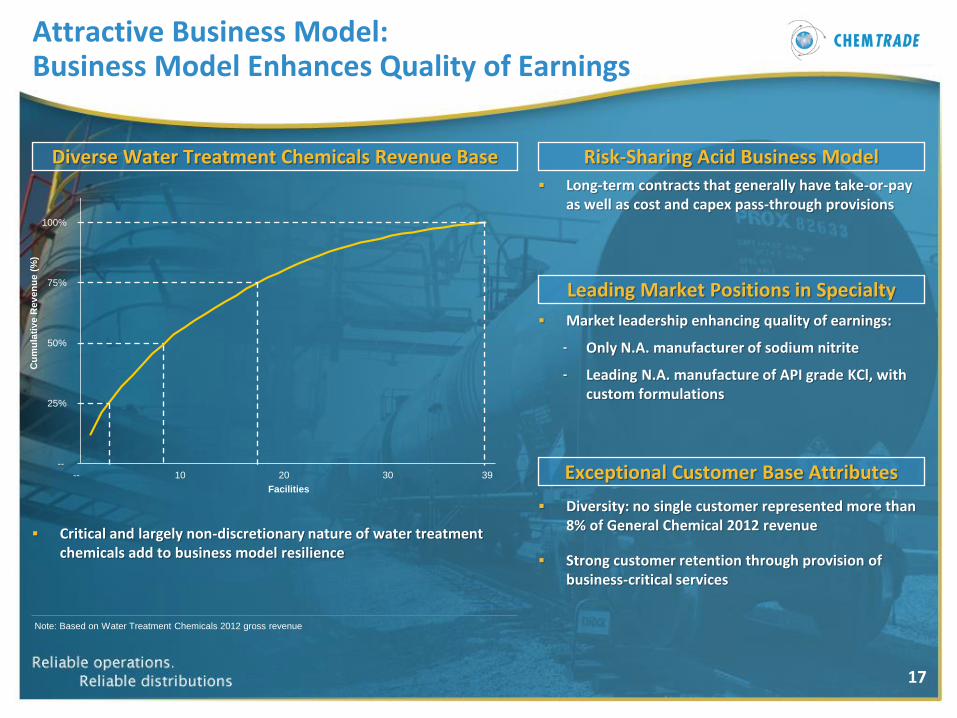

Diverse Water Treatment Chemicals Revenue Base

Note: Based on Water Treatment Chemicals 2012 gross revenue

Long-term contracts that generally have take-or-pay as well as cost and capex pass-through provisions

Attractive Business Model: Business Model Enhances Quality of Earnings

--

25%

50%

75%

100%

125%

-- 10 20 30 40

Cu

mu

lati

ve R

ev

en

ue (

%)

Facilities

39

Critical and largely non-discretionary nature of water treatment chemicals add to business model resilience

Risk-Sharing Acid Business Model

Market leadership enhancing quality of earnings:

- Only N.A. manufacturer of sodium nitrite

- Leading N.A. manufacture of API grade KCl, with custom formulations

Leading Market Positions in Specialty

Diversity: no single customer represented more than 8% of General Chemical 2012 revenue

Strong customer retention through provision of business-critical services

Exceptional Customer Base Attributes

18

Chemtrade General Chemical Pro Forma

Number of facilities

Canada | U.S. | Int.

27

10 | 13 | 4

45

7 | 38 | n.a.

72

17 | 51 | 4

Gross Revenue 2012 Split

Canada | U.S. | Int.28% | 43% | 29% 10% | 90% | n.a. 23% | 57% | 20%

Revenue (C$ millions) $858 $396 $1,254

EBITDA (C$ millions) $143 $112 $265

EBITDA Margin (%) 16.7% 28.2% 21.2%

Capex (C$ millions) $48 $21 $69

Free Cash Flow Conversion (%)(1) 66.3% 81.3% 73.9%

Distributable Cash (C$ millions) $86 n.a. $144

DCPU (C$) $2.06 n.a. $2.41

Operating

Profile

Financial

Profile

(LTM

Sep-30

2013)

1. Free cash flow conversion defined as (EBITDA – capex) / EBITDA.

2. General Chemical gross revenue split is based on location footprint.

3. Gross revenue.

(4)

(5)

(5)

(4)

(3)

4. Includes environmental liability payments; adjusted to account for incremental $7.1 million run-rate maintenance capex.

5. Includes pro forma annualized cost synergies.

(2) (2)

(4,5)

(4,5)

Financial Prudence: Highly Complementary Acquisition

19

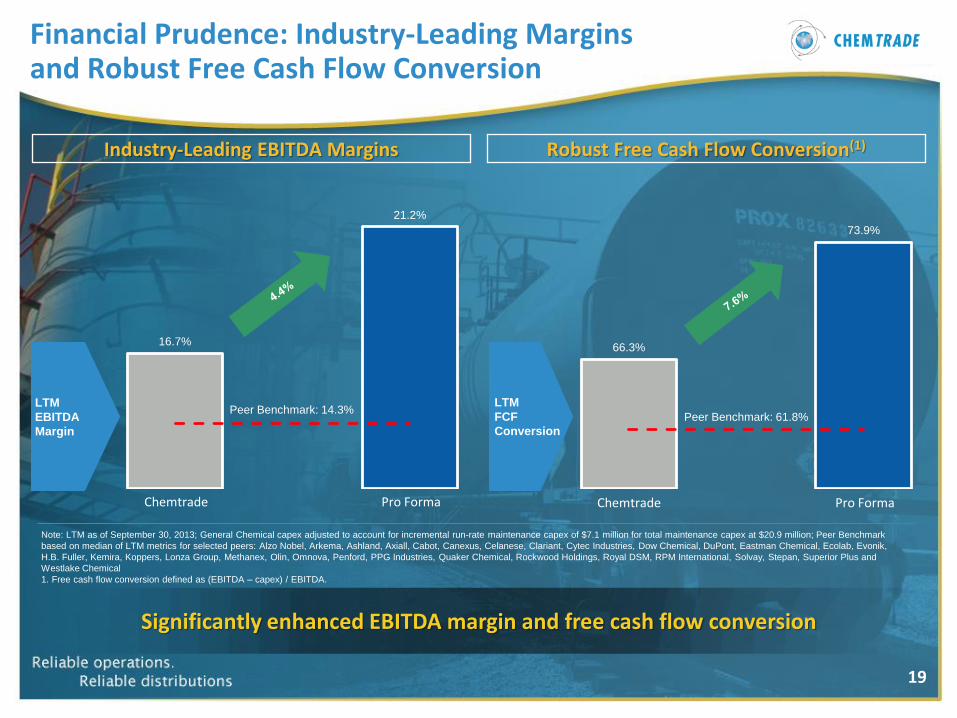

66.3%

73.9%

Chemtrade Pro Forma

Peer Benchmark: 61.8%

Financial Prudence: Industry-Leading Margins and Robust Free Cash Flow Conversion

Significantly enhanced EBITDA margin and free cash flow conversion

Industry-Leading EBITDA Margins Robust Free Cash Flow Conversion(1)

Note: LTM as of September 30, 2013; General Chemical capex adjusted to account for incremental run-rate maintenance capex of $7.1 million for total maintenance capex at $20.9 million; Peer Benchmark

based on median of LTM metrics for selected peers: Alzo Nobel, Arkema, Ashland, Axiall, Cabot, Canexus, Celanese, Clariant, Cytec Industries, Dow Chemical, DuPont, Eastman Chemical, Ecolab, Evonik,

H.B. Fuller, Kemira, Koppers, Lonza Group, Methanex, Olin, Omnova, Penford, PPG Industries, Quaker Chemical, Rockwood Holdings, Royal DSM, RPM International, Solvay, Stepan, Superior Plus and

Westlake Chemical

1. Free cash flow conversion defined as (EBITDA – capex) / EBITDA.

LTM

EBITDA

Margin

LTM

FCF

Conversion

16.7%

21.2%

Chemtrade Pro Forma

Peer Benchmark: 14.3%

20

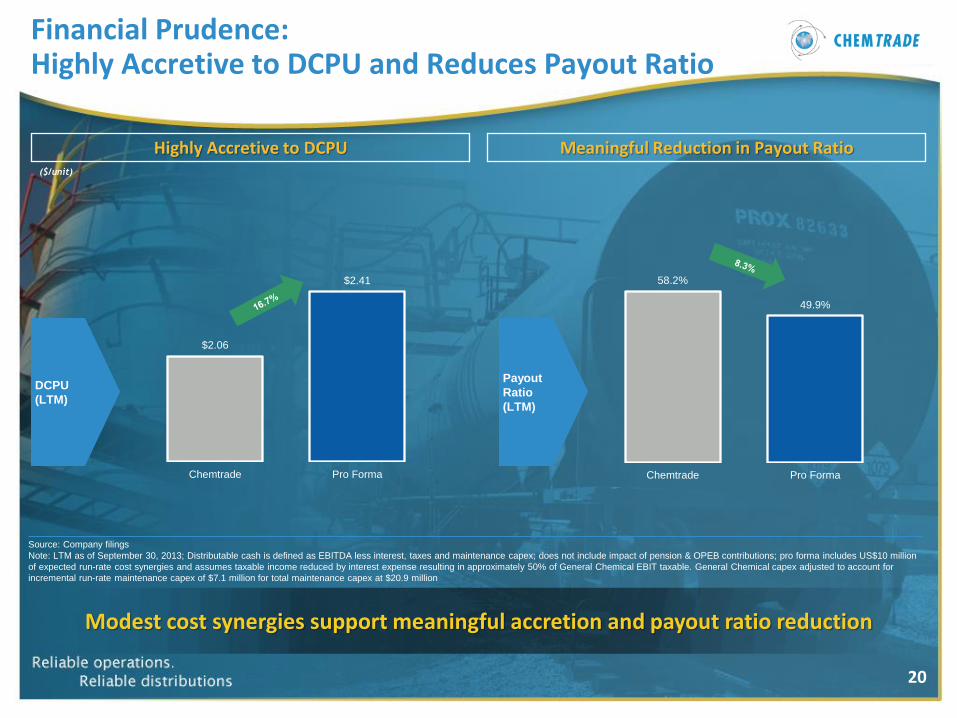

58.2%

49.9%

Chemtrade Pro Forma

$2.06

$2.41

Chemtrade Pro Forma

Highly Accretive to DCPU

Financial Prudence: Highly Accretive to DCPU and Reduces Payout Ratio

Source: Company filings

Note: LTM as of September 30, 2013; Distributable cash is defined as EBITDA less interest, taxes and maintenance capex; does not include impact of pension & OPEB contributions; pro forma includes US$10 million

of expected run-rate cost synergies and assumes taxable income reduced by interest expense resulting in approximately 50% of General Chemical EBIT taxable. General Chemical capex adjusted to account for

incremental run-rate maintenance capex of $7.1 million for total maintenance capex at $20.9 million

DCPU

(LTM)

($/unit)

Payout

Ratio

(LTM)

Modest cost synergies support meaningful accretion and payout ratio reduction

Meaningful Reduction in Payout Ratio

21

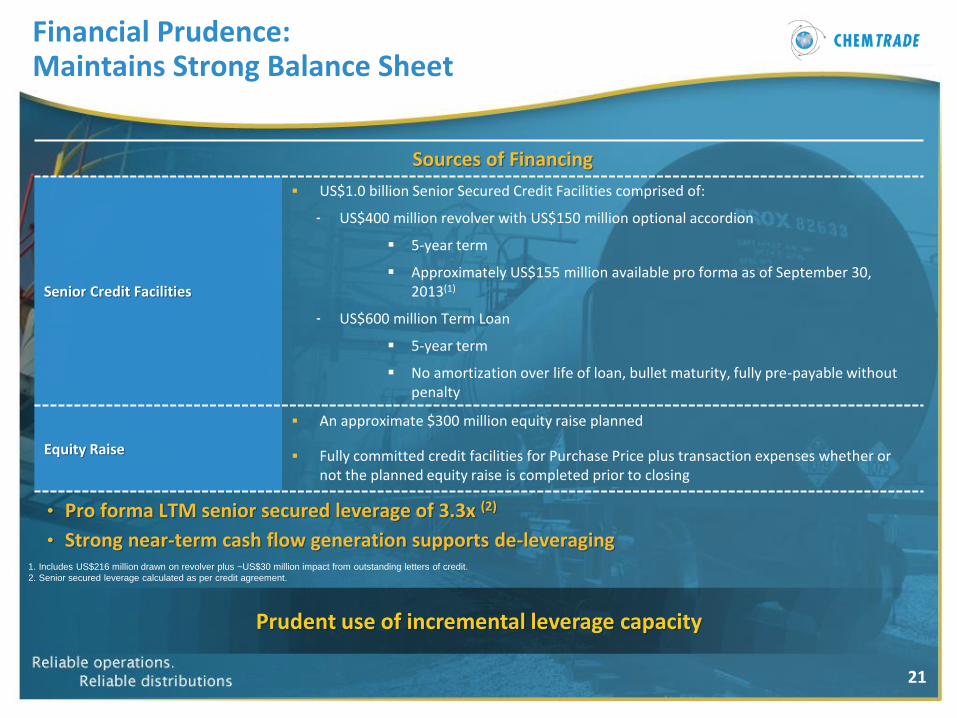

Financial Prudence: Maintains Strong Balance Sheet

Prudent use of incremental leverage capacity

Sources of Financing

Senior Credit Facilities

US$1.0 billion Senior Secured Credit Facilities comprised of:

- US$400 million revolver with US$150 million optional accordion

5-year term

Approximately US$155 million available pro forma as of September 30, 2013(1)

- US$600 million Term Loan

5-year term

No amortization over life of loan, bullet maturity, fully pre-payable without penalty

Equity Raise

An approximate $300 million equity raise planned

Fully committed credit facilities for Purchase Price plus transaction expenses whether or not the planned equity raise is completed prior to closing

• Pro forma LTM senior secured leverage of 3.3x (2)

• Strong near-term cash flow generation supports de-leveraging 1. Includes US$216 million drawn on revolver plus ~US$30 million impact from outstanding letters of credit.

2. Senior secured leverage calculated as per credit agreement.

22

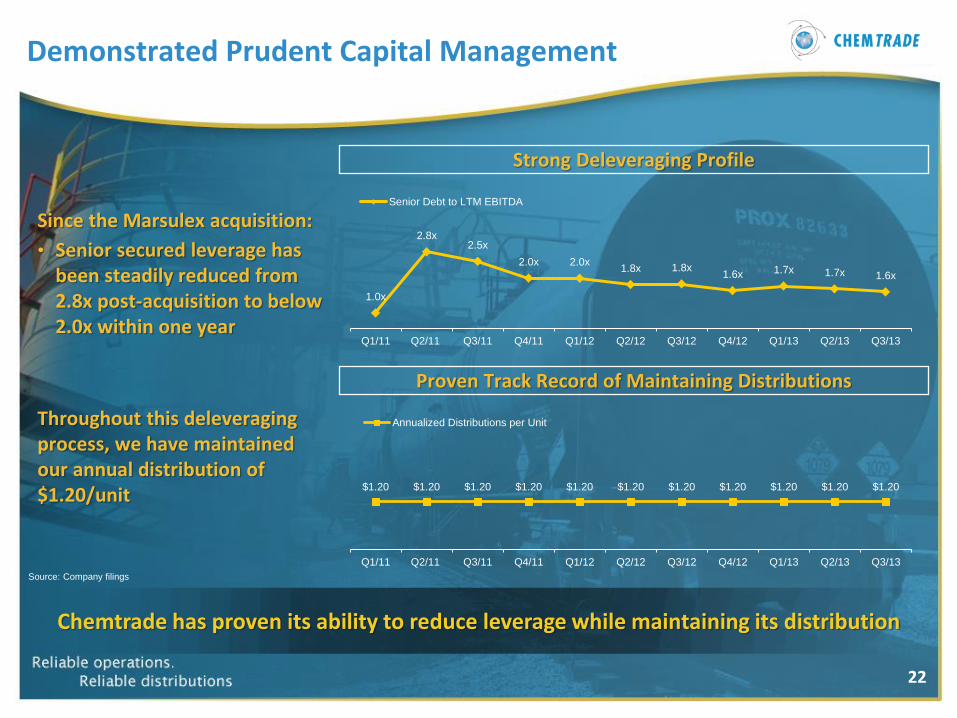

Demonstrated Prudent Capital Management

Proven Track Record of Maintaining Distributions

Chemtrade has proven its ability to reduce leverage while maintaining its distribution

1.0x

2.8x 2.5x

2.0x 2.0x 1.8x 1.8x

1.6x 1.7x 1.7x 1.6x

Q1/11 Q2/11 Q3/11 Q4/11 Q1/12 Q2/12 Q3/12 Q4/12 Q1/13 Q2/13 Q3/13

Senior Debt to LTM EBITDA

Since the Marsulex acquisition:

• Senior secured leverage has been steadily reduced from 2.8x post-acquisition to below 2.0x within one year

Strong Deleveraging Profile

$1.20 $1.20 $1.20 $1.20 $1.20 $1.20 $1.20 $1.20 $1.20 $1.20 $1.20

Q1/11 Q2/11 Q3/11 Q4/11 Q1/12 Q2/12 Q3/12 Q4/12 Q1/13 Q2/13 Q3/13

Annualized Distributions per UnitThroughout this deleveraging process, we have maintained our annual distribution of $1.20/unit

Source: Company filings

23

Executing on our Four-Pronged Strategy

Growth

Operational Excellence

Business Model

Financial Prudence

The acquisition of General Chemical strengthens and expands our platform

24

Appendix

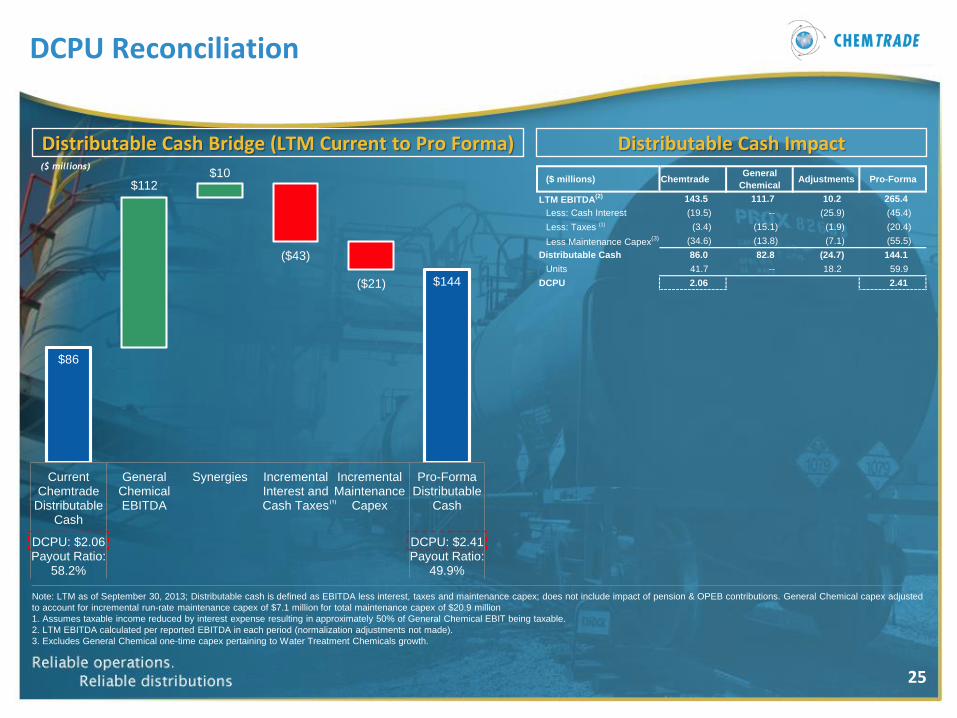

25

$86

$144

$112$10

($43)

($21)

CurrentChemtrade

DistributableCash

GeneralChemicalEBITDA

Synergies IncrementalInterest andCash Taxes

IncrementalMaintenance

Capex

Pro-FormaDistributable

Cash

DCPU: $2.06Payout Ratio:

58.2%

DCPU: $2.41Payout Ratio:

49.9%

(1)

Distributable Cash Bridge (LTM Current to Pro Forma)

DCPU Reconciliation

Note: LTM as of September 30, 2013; Distributable cash is defined as EBITDA less interest, taxes and maintenance capex; does not include impact of pension & OPEB contributions. General Chemical capex adjusted

to account for incremental run-rate maintenance capex of $7.1 million for total maintenance capex of $20.9 million

1. Assumes taxable income reduced by interest expense resulting in approximately 50% of General Chemical EBIT being taxable.

2. LTM EBITDA calculated per reported EBITDA in each period (normalization adjustments not made).

3. Excludes General Chemical one-time capex pertaining to Water Treatment Chemicals growth.

($ millions)

Distributable Cash Impact

($ millions) ChemtradeGeneral

Chemical Adjustments Pro-Forma

LTM EBITDA(2) 143.5 111.7 10.2 265.4

Less: Cash Interest (19.5) -- (25.9) (45.4)

Less: Taxes (1) (3.4) (15.1) (1.9) (20.4)

Less Maintenance Capex(3) (34.6) (13.8) (7.1) (55.5)

Distributable Cash 86.0 82.8 (24.7) 144.1

Units 41.7 -- 18.2 59.9

DCPU 2.06 2.41