debt sought to buy, refit manhattan trophy

TRANSCRIPT

See GRAPEVINE on Back Page

2 Hines Aims to Refi Conn. Offices

2 Loan Sought for Queens Condo Project

2 GE to Finance RXR Purchase in NY

4 Giliberto, Levy Plan Mezz-Loan Index

5 Cassin Hires 2 Attorneys, Seeks More

5 Eightfold Wins Auction for B-Piece

6 Refinancing Sought for Hotel Portfolio

7 Special-Servicing Rate Dips Under 7%

10 Guggenheim Backs Buyer of Offices

10 Mesa West Lends on Dallas Complex

12 Kroll Seeks Researcher, Analysts

13 INITIAL PRICINGS

Portfolio manager Toby Maitland Hudson recently left New York hedge fund Saba Capital, where his duties included han-dling B-piece investments and credit-default swaps tied to commercial MBS. There’s no word on his plans. Hudson joined Saba as a managing director in 2011 after six years at J.P. Morgan in New York and two years at Credit Suisse in London. He exited J.P. Morgan as the executive director in charge of propri-etary trading of CMBS derivatives.

Longtime trader Dylan Korpita resurfaced two weeks ago at Bay Crest Partners, two years after leaving the CMBS desk at Morgan Stanley in Manhattan. Korpita, now based in Deerfield, Mass., has joined the New York broker-dealer’s ongoing effort to raise its profile in the

Investors Scrutinize CMBS Loan ContributorsInvestors are pressuring the major banks that arrange conduit deals to limit the

percentage of loans contributed by nonbanks, especially small shops.Much of the pushback is being directed at Deutsche Bank and Wells Fargo, two

of the biggest conduit issuers. And there are signs that the bond buyers are being heard.

Deutsche is telling investors that going forward, it will shoot to contribute at least half of the collateral in conduit offerings floated via its COMM shelf entity. That would be up from an average of 37.1% last year — the lowest percentage among issuers.

Meanwhile, Wells in the past couple of months has found itself in a similar posi-tion, after losing RBS as a conduit partner when that bank pulled out of the market. Wells and RBS contributed a total of 63.4% of the collateral to their joint deals last year. But on the three deals Wells has since floated as a solo issuer, it supplied only

See INVESTORS on Page 8

Debt Sought to Buy, Refit Manhattan TrophyA General Growth Properties partnership is seeking $1.25 billion of debt to

finance its acquisition of a trophy retail/office property in Midtown Manhattan.The Chicago REIT is teaming up with New York investor Jeff Sutton to pur-

chase the Crown Building, at 730 Fifth Avenue, for about $1.8 billion. The 400,000-square-foot property is predominantly used as offices, but the greater part of its value is in the 35,000 sf of retail space, which the joint venture plans to expand.

General Growth and Sutton are looking for a mortgage with a term of 5-7 years. They’ll consider floating-rate quotes but would likely swap to a fixed rate. Eastdil Secured is marketing the lending assignment and brokering the trade for the seller, a local group including the Spitzer and Winter families.

Various banks and other debt shops are expected to compete for the assignment. But some may find the deal daunting because it’s largely a bet on the planned retail

See TROPHY on Page 12

Colony Sets $2 Billion Target for Debt FundColony Capital is soliciting $2 billion of equity for what would be its largest high-

yield debt fund yet.Like the three predecessor vehicles in the series, Colony Distressed Credit & Spe-

cial Situations Fund 4 will shoot for a 13-14% return by investing in subperforming or defaulted senior mortgages and mezzanine debt, and by originating loans for distressed property owners. But in a switch, it would seek to invest roughly 60% of its capital in Europe. The other funds primarily targeted the U.S.

The vehicle follows up the $1.2 billion Fund 3, which Colony began marketing in 2013 and closed five months ago. That is the largest vehicle to date in the fund series, which Colony launched in 2008. All told, the three funds raised close to $3 billion.

Investors in those funds include Louisiana Teachers, National Pension Service of South Korea, Koch Industries Employees, insurer ACE Group and California Endowment,

See COLONY on Page 6

THE GRAPEVINE

MARCH 6, 2015

Hines Aims to Refi Conn. OfficesThe owner of an office building in Greenwich, Conn., is in

the market for an $85 million mortgage.A partnership among Houston-based Hines, Warren Private

of Dublin and Willet Cos. of Rye, N.Y., wants to refinance the 128,000-square-foot property at 33 Benedict Place. The prefer-ence is for floating-rate debt with a term of five years. Eastdil Secured is pitching the assignment to lenders.

The request marks a change of course for the Hines team, which put the property up for sale in October. At the time it was expected to fetch about $140 million, or $1,094/sf, which would eclipse the local record for per-foot pricing. But no deal was struck. The partners will likely launch a fresh sales effort in a year or two, sources said.

Most of the proposed loan would go to retire $70 million of existing debt, which was originated by Greenwich Capital in 2005 and securitized in a $4.3 billion commercial MBS deal (GCCFC 2005-GG5). The interest-only loan has a 5.22% cou-pon and is set to mature in July. It can be prepaid without pen-alty beginning next month.

That loan helped finance the acquisition of the building for $87.5 million. The seller, Unilever, leased it back as its U.S. headquarters until 2007, then relocated.

The property is 95% occupied, with a weighted average remaining lease term of about seven years. The largest tenant, hedge fund manager AQR Capital, accounts for about 50% of the building — but never moved in and subleases its space. Other tenants include investment advisor Axiom International (21,000 sf until 2019). Net operating income was $8.3 million in 2013, the latest full-year figure available, and was on track for a slight increase in 2014.

The four-story building is at the corner of U.S. Route 1 North, near downtown Greenwich. It was developed in the 1970s for Chesebrough-Pond’s, which Unilever bought in 1998.

Loan Sought for Queens Condo ProjectA JK Equities partnership is looking for up to $200 million of

floating-rate debt to finance the construction of a long-stalled residential tower in Queens, N.Y.

The property would be built on the site of the shuttered RKO Keith’s Theater, on Northern Boulevard and Main Street in Flushing. That structure will be demolished, except for its landmarked lobby, which will be incorporated into the tower.

Previous developers had planned the project for several years, only to run into financial problems, and red tape related to the theater’s landmark status. JK Equities, of Port Washing-ton, N.Y., and its partners acquired the theater for $30 million in December 2013.

The permits call for a 17-story glass-and-steel building, with 357 luxury condominiums, 323 parking spots, 24,000 square feet of retail space and 15,000 sf of community space. But the JK Equities partnership is seeking approval from the local commu-nity board to amend the plan, according to the Queens Chronicle newspaper. It wants to reduce the number of units to 269 but

make them bigger, shave the number of parking spaces to 252, increase the building’s height by 15 feet and alter the facade.

Construction can’t begin without the board’s approval, but “the wheels are in motion,” said a person close to the process. The goal is to begin construction by June and finish by early 2018.

Mission Capital, the partnership’s advisor, is pitching the loan assignment to debt funds, banks, mortgage REITs and insurance companies.

The 3,000-seat theater opened in 1928 and booked vaude-ville acts and showed movies for decades. Its ornate “Mexican baroque” lobby was designated a New York City landmark and put on the National Register of Historic Places in 1984. But two years later, the theater closed for good, a victim of its immense size.

Since then, multiple developers came up with various plans to redevelop the site, only to be stymied. The JK Equities part-nership acquired the theater from developer Patrick Thompson, who had purchased it in 2010. The previous owner, New York developer Shaya Boymelgreen, had arranged the permits for the condo plan, but defaulted on a $20 million loan from Doral Bank.

The site is along Flushing’s primary retail corridor, one mile east of Citi Field, home of the New York Mets baseball team. It is a few blocks from Sky View Parc, a much larger condo com-plex set to begin its second phase of construction. The com-pleted first phase encompasses two towers with 448 units atop an 800,000-sf retail center. The developer, Onex Real Estate of Toronto, is seeking a $450 million loan to finance the construc-tion of three more towers with 805 units.

There is strong demand for condos in Flushing amid meager supply. Over one especially busy weekend in January, 150 units in Sky View Parc were presold.

GE to Finance RXR Purchase in NYAfter holding talks with two other lenders, RXR Realty has

gotten a commitment for about $325 million of debt from GE Capital to finance the purchase of the leasehold interest in the office building at 32 Old Slip in Lower Manhattan.

RXR is buying both the leasehold interest and the under-lying land from Boston fund shop Beacon Capital for $675 million. In a side deal, it will sell the land to a David Werner partnership for roughly $225 million.

RXR initially was in talks with HSBC and Helaba Bank for a $275 million floating-rate loan on the leasehold interest in the 1.1 million-square-foot building. But RXR changed course and gave the assignment to GE Capital, which offered more pro-ceeds, right around the amount RXR originally sought.

Werner, a New York investor, is teaming up with Melohn Properties of New York to buy the land. Morgan Stanley has agreed to provide a $176 million fixed-rate loan, with a 10-year term. RXR, of Uniondale, N.Y., will sign a 99-year lease on the ground.

The building, also known as One Financial Square, is on a block along the East River, bounded by Old Slip, Front Street, Gouverneur Lane and South Street.

March 6, 2015 2Commercial Mortgage ALERT

EXPERIENCE • EXECUTION • EXCELLENCE

NATIONAL LEADER IN REAL ESTATE FINANCEOver $ Billion Loans Closed since 2010

Fixed I Floating I Bridge I Agency

www.ccre.com | 212.915.1700

NEW YORK • CHICAGO • ATLANTA • LOS ANGELES • NEWPORT BEACH DALLAS • MIAMI • SEATTLE • WASHINGTON, D.C. • SAN FRANCISCO

BOSTON • DETROIT • COLUMBUS • ST. LOUIS • NASHVILLE

March 6, 2015 4Commercial Mortgage ALERT

Giliberto, Levy Plan Mezz-Loan IndexJohn Levy and Michael Giliberto, who for 22 years have pro-

duced an index that measures commercial-mortgage perfor-mance, are now developing an index that tracks high-yield real estate loans.

The tool, which will likely be rolled out in the third quarter, will enable holders of high-yield debt to compare the perfor-mance of their investments with the market average. Potential users include fund managers, advisory shops, specialty finance firms, banks and insurers.

“We have always gotten inquiries from people who say,

‘What can you tell us about high-yield debt? We need a bench-mark for that,’ ” said Levy, who runs John B. Levy & Co., a bro-kerage and advisory shop in Richmond, Va.

The existing Giliberto-Levy Commercial Mortgage Perfor-mance Index, which Levy compiles with Giliberto, a Columbia University business professor and former J.P. Morgan strate-gist, tracks quarterly returns on fixed-rate senior commercial mortgages originated by balance-sheet lenders like insurers and pension funds. Users can break down the data in a vari-ety of ways, including loan duration, rate, loan-to-value ratio, interest-only component, property type and region.

Over time, some of those loans effectively became classi-fied as “high yield” because of declines in the collateral value or other credit quality issues. Levy said he would pass on data about such “accidental” high-yield loans in response to inquiries. “But now we’re getting more of these questions, and we’ve real-ized we can expand our platform to create a much bigger picture of the high-yield loan market.”

The new index will pool data on loans originated as mezzanine debt and on preferred equity. The data will be contributed by the index’s “founding members,” which Levy has already partly assembled.

“We are asking these folks for their input on how we should shape the index,” he said. “Those who join early on get the benefit of having more input into the process.”

Over time, the new index may be carved up into subsets, based on overall leverage load, and other criteria. “The people who want to know about lever-age that tops out at 75% are in a completely different group from those who can tolerate leverage up to 85%,” said Levy.

Levy and Giliberto are also looking to join forces with a marketing firm that will help promote the new product, which will be available by sub-scription.

The new index will be called the Giliberto-Levy Commercial Mortgage Performance Index 2, while the original one will add the number “1” to its name.

Value-Add, High-Traffi c Retail Center97,131 SF | Ontario, CA | 82% Leased

www.auction.com/w-vineyard

Non-Performing Note - Three NC Retail Centers

127,730 SF • Occupancy: 74% • Starting Bid: $1,250,000

Bid Online March 23-25 | www.auction.com/cma-ncretail

Two Performing Note Offerings | Bid Online March 24-26

Industrial Note in Pomona, CA • www.auction.com/cma-ca

Two-Note Portfolio* | $5MM UPB • www.auction.com/cma-mw

*TN retail and OH offi ce notes

FOR SALE

Non-Performing Retail Note near Chicago, IL

74,240 SF • Starting Bid: $1,750,000

Bid Online March 23-25 | www.auction.com/cma-homewood

Non-Performing Medical Offi ce Note in Tempe, AZ

22,845 SF • Occupancy: 62% • Starting Bid: $700,000

Bid Online March 23-25 | www.auction.com/cma-tempe

FOR SALE

Non-Performing Note - Three NC Retail Centers

127,730 SF • Occupancy: 74% • Starting Bid: $1,250,000

Bid Online March 23-25 |

Two Performing Note Offerings | Bid Online March 24-26

Industrial Note in Pomona, CA

Two-Note Portfolio* | $5MM UPB •

*TN retail and OH offi ce notes

FOR SALE

Non-Performing Retail Note near Chicago, IL

74,240 SF • Starting Bid: $1,750,000

Bid Online March 23-25 |

Non-Performing Medical Offi ce Note in Tempe, AZ

22,845 SF • Occupancy: 62% • Starting Bid: $700,000

Bid Online March 23-25 |

FOR SALE

TRANSACTIONSSPEAK LOUDERTHAN WORDS

SEARCH ASSETS AND SET ALERTS:

www.auction.com/cma-buy

INTERESTED IN SELLING?

www.auction.com/cma-sell

View licensing at www.auction.com/licensing

OVER $30 BILLION SOLD

WHERE REAL ESTATE IS MOVING™

FOR SALE

FOR SALE

March 6, 2015 5Commercial Mortgage ALERT

Cassin Hires 2 Attorneys, Seeks MoreThe law firm of Cassin & Cassin continues to expand its

commercial-mortgage group, whose roster of attorneys has nearly doubled over the last year.

The two latest additions are moving over from the real estate transaction group at Kasowitz Benson. On March 16, Steven Coury will join as a partner in Cassin’s Purchase, N.Y., office while Harrison Kaufman will start work as counsel in the firm’s New York headquarters.

They will bring to 30 the number of attorneys on the team, led by partners Michael Hurley and Dennis Mensi. The group has grown rapidly from about 16 lawyers a year ago. Plans call for adding more this year, but at a slower pace, said senior partner Joseph Cassin, who co-founded the firm in 1986.

The bulk of the group’s business involves originations of commercial MBS loans. The recent hiring spree reflects the firm’s efforts to bolster that practice, while expanding its client base among other types of lenders it serves, including insurers, banks and fund operators, Hurley said.

Cassin also wants to add two attorneys to its separate agency-lending group, preferably in Washington. Partner Caroline Blakely heads that 14-member team, which works with lenders that write Fannie Mae and Freddie Mac loans on multi-family properties.

The arrival of Coury and Kaufman from Kasowitz’s New York headquarters will boost Cassin’s overall staff count to 47 attorneys — about half in Manhattan and the rest split among its offices in Purchase, Dallas, Los Angeles and Wash-ington.

Coury has been a special counsel since joining Kasowitz three years ago. He worked at Skadden Arps for 13 years before that, moving up from associate to counsel in 2008.

Kaufman has been an associate at Kasowitz since 2010. He previously spent roughly two years at Thacher Proffitt and about a year as in-house counsel at Dillon Read Capital.

Eightfold Wins Auction for B-PieceEightfold Real Estate Capital has circled the junior portion of

an upcoming conduit issue from Goldman Sachs and Citigroup (CGCMT 2015-GC29).

That will be Eightfold’s third B-piece purchase this year. The Miami shop previously took down the subordinate pieces of COMM 2015-LC19 and WFCM 2015-C26.

The buzz is that Eightfold won the deal via a bidding auction that included several other firms. That has led some market play-ers to speculate that Eightfold plans to be more aggressive in auc-tions this year, after a relatively modest showing last year, when many of its purchases were made on a negotiated basis.

www.MCFiveMile.com | [email protected] | (212) 485 - 2580

Origination | Credit | Underwriting | Structuring | Capital Markets | Asset Management

Client Focused | Solution Oriented | Results Driven

$4,750,000Retail

Katy, TX

$10,100,000 e

Philadelphia, PA

$8,300,000 a a t ed i

elle ,

$19,000,000 t de t i

A ti , TX

$22,350,000 e

Pitt h, PA

$21,000,000 Retail

a ia ea h,

March 6, 2015 6Commercial Mortgage ALERT

Refinancing Sought for Hotel PortfolioA RockBridge Capital partnership is looking for an $85 mil-

lion mortgage to refinance a portfolio of mostly upper-upscale hotels.

The Columbus, Ohio, fund operator and its partner, Hospi-tality Ventures of Atlanta, prefer floating-rate debt with a term of 3-5 years. The loan-to-value ratio would be around 70%, indicating the 1,059-room package is worth about $121 mil-lion. Broker JLL is pitching the proposal mainly to banks.

The five properties are in Georgia, Kentucky, Michigan, Oklahoma and Texas. The RockBridge team acquired them in 2007, paying $86 million, or $81,209/room, to FelCor Lodging, a hotel REIT in Irving, Texas.

All the hotels carry Hilton-operated brands. Four have the upper-upscale Embassy Suites flag. Those are in Dallas (279 rooms), Troy, Mich. (251 rooms), Tulsa, Okla. (244 rooms) and Brunswick, Ga. (130 rooms). The fifth, a 155-room hotel in Lexington, Ky., flies the upscale DoubleTree flag.

Each hotel has meeting space, and the Lexington property, at 2601 Richmond Road, includes a 37,000-square-foot shop-ping center.

RockBridge operates funds that acquire hotels across the U.S. and originate senior and subordinate loans on such prop-erties. It held a final close last year on the $450 million Rock-Bridge Hospitality Fund 6, easily exceeding its $350 million

equity target. Hospitality Ventures invests in hotels and advises hotel operators.

Colony ... From Page 1

a statewide health foundation for underserved individuals and communities, according to Preqin.

The new fund could have roughly $3 billion of investment power when leveraged.

Colony, an investment manager in Santa Monica, Calif., also operates property funds, separate accounts for institutional investors, and vehicles that invest in foreclosed single-family homes. In addition, it runs a public mortgage REIT, Colony Financial.

Colony Capital is in the process of combining operations with Colony Financial. The merged company will be a public REIT operating as Colony Capital. Colony figures the maneu-ver will enable it to set up larger funds. The reason: By gaining access to public capital, Colony should be able to raise larger amounts of equity that it can contribute to its funds.

Colony Capital, which was founded in 1991 by chief execu-tive Tom Barrack, was among the earliest shops to invest in dis-tressed debt. It made a fortune from the S&L liquidations of the early 1990s, moved into lucrative European and Asian markets and then refocused in recent years on distressed debt in the U.S.

ATLANTA · NEW YORK · IRVINE · LONDON · AMSTERDAM

WORLD-CLASS PROJECTS.FROM START TO FINISH.

Over three decades, we've serviced thousands of complex construction loans of all shapes and sizes. This track record has earned us the highest possible Construction Servicer rating awarded by Standard & Poor's.

If you're ready to build, we're with you all the way.

CONSTRUCTION LOAN ADMINISTRATION IS A COMPLEX PROCESS. THAT'S WHERE WE COME IN.

March 6, 2015 7Commercial Mortgage ALERT

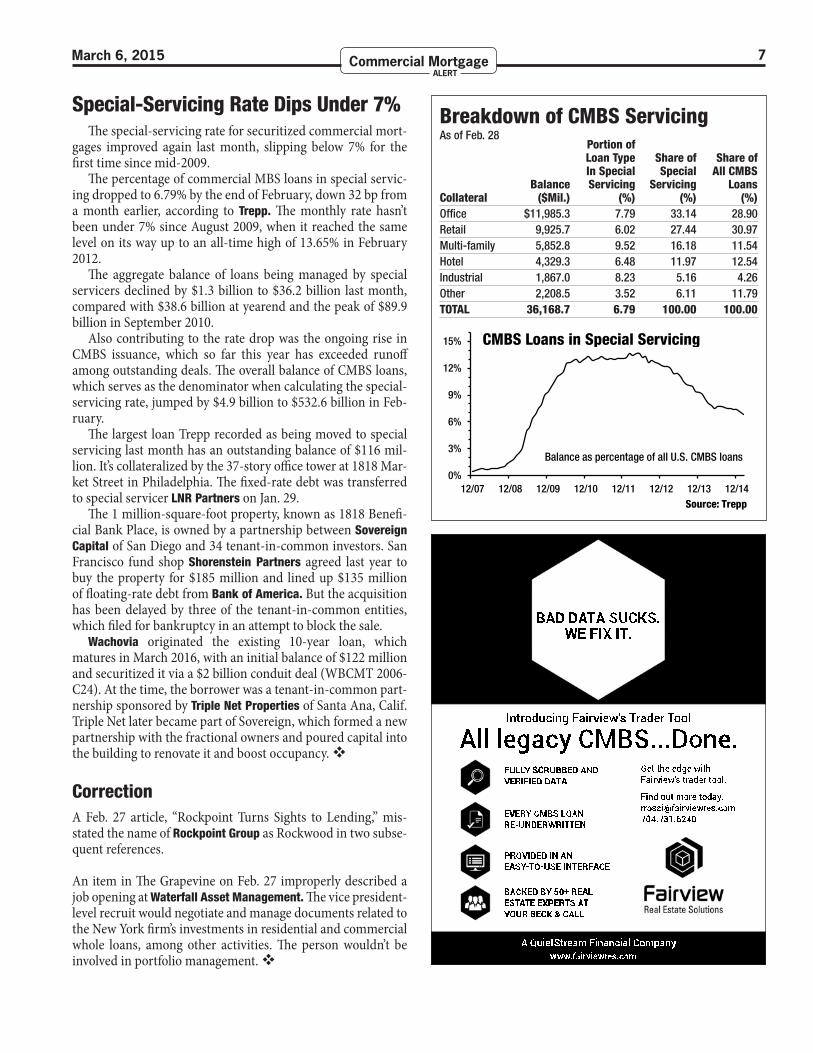

Special-Servicing Rate Dips Under 7%The special-servicing rate for securitized commercial mort-

gages improved again last month, slipping below 7% for the first time since mid-2009.

The percentage of commercial MBS loans in special servic-ing dropped to 6.79% by the end of February, down 32 bp from a month earlier, according to Trepp. The monthly rate hasn’t been under 7% since August 2009, when it reached the same level on its way up to an all-time high of 13.65% in February 2012.

The aggregate balance of loans being managed by special servicers declined by $1.3 billion to $36.2 billion last month, compared with $38.6 billion at yearend and the peak of $89.9 billion in September 2010.

Also contributing to the rate drop was the ongoing rise in CMBS issuance, which so far this year has exceeded runoff among outstanding deals. The overall balance of CMBS loans, which serves as the denominator when calculating the special-servicing rate, jumped by $4.9 billion to $532.6 billion in Feb-ruary.

The largest loan Trepp recorded as being moved to special servicing last month has an outstanding balance of $116 mil-lion. It’s collateralized by the 37-story office tower at 1818 Mar-ket Street in Philadelphia. The fixed-rate debt was transferred to special servicer LNR Partners on Jan. 29.

The 1 million-square-foot property, known as 1818 Benefi-cial Bank Place, is owned by a partnership between Sovereign Capital of San Diego and 34 tenant-in-common investors. San Francisco fund shop Shorenstein Partners agreed last year to buy the property for $185 million and lined up $135 million of floating-rate debt from Bank of America. But the acquisition has been delayed by three of the tenant-in-common entities, which filed for bankruptcy in an attempt to block the sale.

Wachovia originated the existing 10-year loan, which matures in March 2016, with an initial balance of $122 million and securitized it via a $2 billion conduit deal (WBCMT 2006-C24). At the time, the borrower was a tenant-in-common part-nership sponsored by Triple Net Properties of Santa Ana, Calif. Triple Net later became part of Sovereign, which formed a new partnership with the fractional owners and poured capital into the building to renovate it and boost occupancy.

CorrectionA Feb. 27 article, “Rockpoint Turns Sights to Lending,” mis-stated the name of Rockpoint Group as Rockwood in two subse-quent references.

An item in The Grapevine on Feb. 27 improperly described a job opening at Waterfall Asset Management. The vice president-level recruit would negotiate and manage documents related to the New York firm’s investments in residential and commercial whole loans, among other activities. The person wouldn’t be involved in portfolio management.

Breakdown of CMBS Servicing As of Feb. 28 Portion of Loan Type Share of Share of In Special Special All CMBS Balance Servicing Servicing LoansCollateral ($Mil.) (%) (%) (%)Office $11,985.3 7.79 33.14 28.90Retail 9,925.7 6.02 27.44 30.97Multi-family 5,852.8 9.52 16.18 11.54Hotel 4,329.3 6.48 11.97 12.54Industrial 1,867.0 8.23 5.16 4.26Other 2,208.5 3.52 6.11 11.79TOTAL 36,168.7 6.79 100.00 100.00

0%

3%

6%

9%

12%

15%

12/07 12/08 12/09 12/10 12/11 12/12 12/13 12/14 Source: Trepp

CMBS Loans in Special Servicing

Balance as percentage of all U.S. CMBS loans

March 6, 2015 8Commercial Mortgage ALERT

Investors ... From Page 1

40.3% of the pool balance.Market pros believe Wells is trying to line up a new partner.

Some think it will align with a bank that has a broker-dealer arm, enabling it to help distribute bonds. If so, Societe Generale is a logical candidate, because it hired 10 pros from the closed RBS operation in January to staff its new conduit program.

Some investors contend that finance shops and other non-banks are sometimes less rigorous about credit quality than the giant banks that put the transactions together and underwrite them. The investors acknowledge that their concerns aren’t neatly categorized. They emphasize that some nonbanks, includ-ing small shops, write quality loans, while some banks that aren’t issuers have suspect credit quality. In fact, one rating agency offi-cial said a list of the worst lenders would likely include a mix of banks and nonbanks, both big and small.

But by and large, there is a widespread perception among investors that the main source of poor-quality loans is nonbanks, especially small shops — often described as those that securitize less than $1 billion of mortgages a year. And lenders at banks and nonbanks alike agree the perception exists.

Whether that sentiment is true is hard to determine. Some market pros see little across-the-board differences between banks and nonbanks, and between big shops and small ones. But the complaint is widespread enough that issuers are sensitive to it.

While investors welcome the indications that their message is getting through, they remain dubious about how forcefully issuers will limit contributions from nonbanks, whose contin-ued involvement in the sector serves the issuers’ interests. For one thing, nonbanks help issuers achieve critical mass faster and crank out more transactions. They also tend to contribute more medium-size and small loans to collateral pools and thus bal-ance out the larger loans that the major banks tend to write. And they often finance their originations via warehouse credit lines provided by the issuers, generating fees for them.

The idea of curbing contributions from nonbanks — some-times referred to as “pool shaping” — drew lively comments from both investors and lenders at recent conferences sponsored by the Mortgage Bankers Association and Fitch. Deutsche execu-tives acknowledged the complaints and committed to supplying a larger percentage of the bank’s collateral, according to attendees.

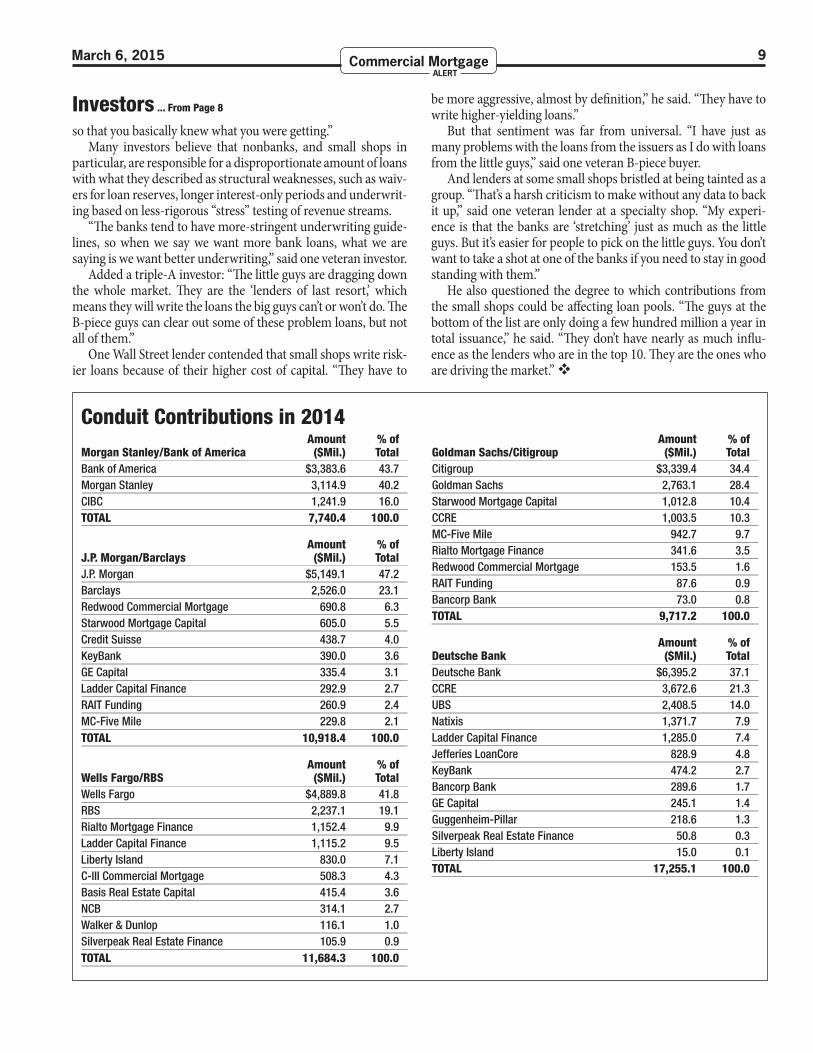

There are five major conduit issuers: Deutsche; Wells (for-merly Wells/RBS); the team of Goldman Sachs and Citigroup; the team of J.P. Morgan and Barclays; and the team of Morgan Stanley and Bank of America. Each issuer sells bonds via its own shelf entity.

Last year, those issuers floated 49 of the 50 conduit deals, which totaled $57.5 billion. All told, 31 conduit shops contrib-uted collateral to those transactions. The nine banks that made up the issuing entities supplied $33.8 billion of the collateral, or 59%, with individual contributions ranging from $6.4 billion by Deutsche to $2.2 billion by RBS. Fifteen lenders securitized less than $1 billion each.

The Morgan Stanley/BofA team was the dominant issuer con-tributor, accounting for 84% of the collateral in its deals last year.

Next came J.P. Morgan/Barclays (70.3%), Goldman/Citi (62.8%), Wells/RBS and Wells solo (61.0%) and Deutsche (37.1%).

If Deutsche, Wells and other issuers supply larger percentages of the collateral for their deals, that could limit the ability of small shops to find an outlet for their originations and could theoreti-cally drive some out of the sector.

It could also constrain those issuers’ deal volume and cut into the credit they are awarded in bookrunner rankings. Deutsche and Wells have boosted their bookrunner volume by aligning with lenders that either don’t have bond-underwriting affiliates or don’t care about league-table credit.

For example, Deutsche last year was the top underwriter, snaring a 26.1% share of conduit bookrunner volume, but con-tributed only 11.1% of the total collateral. Deutsche’s COMM deals have included contributions from a rotating list of conduit shops, including two top-10 lenders — CCRE and Ladder Capital.

Likewise, Wells finished third among bookrunners, with a 17% market share, but supplied only 8.5% of the collateral itself. Wells is believed to be the biggest provider of warehouse-financ-ing facilities to small conduit lenders, and those shops contrib-ute their loans to Wells’ transactions. As a result, those deals can have an unusually large number of contributors — as many as eight in one offering last year.

By contrast, the gap between bookrunner and loan-contrib-utor market shares was much smaller for the other issuers.

The degree to which investors actually penalize deals with significant loan contributions from nonbanks — if at all — is impossible to say because that’s only one of many variables that factor into pricing. But Deutsche, for one, must think it is a drag, because it is moving to address the concern.

Deutsche’s plan to contribute half of the collateral in its deals was generally welcomed by investors interviewed for this story. But many said there is no magic percentage that would allay their concerns, adding that they saw that as a proxy for getting better-quality loans into collateral pools on a consistent basis.

Some investors said that having a regular lineup of loan con-tributors is more important than the issuer’s contribution level. “It’s about having a consistent set of originators, so that you don’t have to scratch your head every time a deal comes out, and ask, ‘Who are these people?’ ” said one bond buyer. “The old ‘TOP’ shelf, for instance, that had Morgan Stanley, Wells, Principal Financial and Bear Stearns, developed a track record over time,

See INVESTORS on Page 9

Conduit Issuers in 2014 Issuer No. of Amount Contrib. Issues ($Bil.) (%)Morgan Stanley/Bank of America 6 $7,740.4 84.0J.P. Morgan/Barclays 9 10,918.4 70.3Goldman Sachs/Citigroup 9 9,717.2 62.8Wells Fargo/RBS 10 11,684.3 61.0Deutsche Bank 15 17,255.1 37.1TOTAL 49 57,315.5

March 6, 2015 9Commercial Mortgage ALERT

Investors ... From Page 8

so that you basically knew what you were getting.”Many investors believe that nonbanks, and small shops in

particular, are responsible for a disproportionate amount of loans with what they described as structural weaknesses, such as waiv-ers for loan reserves, longer interest-only periods and underwrit-ing based on less-rigorous “stress” testing of revenue streams.

“The banks tend to have more-stringent underwriting guide-lines, so when we say we want more bank loans, what we are saying is we want better underwriting,” said one veteran investor.

Added a triple-A investor: “The little guys are dragging down the whole market. They are the ‘lenders of last resort,’ which means they will write the loans the big guys can’t or won’t do. The B-piece guys can clear out some of these problem loans, but not all of them.”

One Wall Street lender contended that small shops write risk-ier loans because of their higher cost of capital. “They have to

be more aggressive, almost by definition,” he said. “They have to write higher-yielding loans.”

But that sentiment was far from universal. “I have just as many problems with the loans from the issuers as I do with loans from the little guys,” said one veteran B-piece buyer.

And lenders at some small shops bristled at being tainted as a group. “That’s a harsh criticism to make without any data to back it up,” said one veteran lender at a specialty shop. “My experi-ence is that the banks are ‘stretching’ just as much as the little guys. But it’s easier for people to pick on the little guys. You don’t want to take a shot at one of the banks if you need to stay in good standing with them.”

He also questioned the degree to which contributions from the small shops could be affecting loan pools. “The guys at the bottom of the list are only doing a few hundred million a year in total issuance,” he said. “They don’t have nearly as much influ-ence as the lenders who are in the top 10. They are the ones who are driving the market.”

Amount % ofMorgan Stanley/Bank of America ($Mil.) TotalBank of America $3,383.6 43.7Morgan Stanley 3,114.9 40.2CIBC 1,241.9 16.0TOTAL 7,740.4 100.0

Amount % ofJ.P. Morgan/Barclays ($Mil.) TotalJ.P. Morgan $5,149.1 47.2Barclays 2,526.0 23.1Redwood Commercial Mortgage 690.8 6.3Starwood Mortgage Capital 605.0 5.5Credit Suisse 438.7 4.0KeyBank 390.0 3.6GE Capital 335.4 3.1Ladder Capital Finance 292.9 2.7RAIT Funding 260.9 2.4MC-Five Mile 229.8 2.1TOTAL 10,918.4 100.0

Amount % ofWells Fargo/RBS ($Mil.) TotalWells Fargo $4,889.8 41.8RBS 2,237.1 19.1Rialto Mortgage Finance 1,152.4 9.9Ladder Capital Finance 1,115.2 9.5Liberty Island 830.0 7.1C-III Commercial Mortgage 508.3 4.3Basis Real Estate Capital 415.4 3.6NCB 314.1 2.7Walker & Dunlop 116.1 1.0Silverpeak Real Estate Finance 105.9 0.9TOTAL 11,684.3 100.0

Amount % ofGoldman Sachs/Citigroup ($Mil.) TotalCitigroup $3,339.4 34.4Goldman Sachs 2,763.1 28.4Starwood Mortgage Capital 1,012.8 10.4CCRE 1,003.5 10.3MC-Five Mile 942.7 9.7Rialto Mortgage Finance 341.6 3.5Redwood Commercial Mortgage 153.5 1.6RAIT Funding 87.6 0.9Bancorp Bank 73.0 0.8TOTAL 9,717.2 100.0

Amount % ofDeutsche Bank ($Mil.) TotalDeutsche Bank $6,395.2 37.1CCRE 3,672.6 21.3UBS 2,408.5 14.0Natixis 1,371.7 7.9Ladder Capital Finance 1,285.0 7.4Jefferies LoanCore 828.9 4.8KeyBank 474.2 2.7Bancorp Bank 289.6 1.7GE Capital 245.1 1.4Guggenheim-Pillar 218.6 1.3Silverpeak Real Estate Finance 50.8 0.3Liberty Island 15.0 0.1TOTAL 17,255.1 100.0

Conduit Contributions in 2014

March 6, 2015 10Commercial Mortgage ALERT

Guggenheim Backs Buyer of OfficesGuggenheim Partners has written a $95 million fixed-rate

loan to finance the acquisition of five office properties in the Southeast that are fully leased to Wells Fargo.

The 10-year mortgage is backed by 1.6 million square feet in Georgia, North Carolina, South Carolina and Virginia. Wells’ triple-net lease on all the space runs until 2024. The loan-to-value ratio is 65%, pegging the value of the portfolio at $146 million.

Guggenheim plans to securitize the loan, which has an interest-only period and then amortizes on a 30-year schedule. CBRE brokered the financing for a trust created by the family of Samuel Klein, founder of a large appliance-store chain in Brazil.

The Klein trust acquired the portfolio in two stages from a partnership between Los Angeles-based Oaktree Capital and National Financial Realty of Torrance, Calif. The buyer paid cash for a 336,000-sf building at 3579-3585 Atlanta Avenue in Atlanta, then arranged the financing, which closed two weeks ago along with the purchase of the other four properties. All five collateralize the loan from Chicago-based Guggenheim.

The largest property, with 443,000 sf, is in Roanoke, Va., at 7711 Plantation Road. Two are in Winston-Salem, N.C., at 809 West 4 1/2 Street (343,000 sf) and 401 Linden Street (211,000 sf). The fifth is at 101 Greystone Boulevard in Columbia, S.C. (241,000 sf).

The properties were part of a 3.4 million-sf portfolio that the

Oaktree partnership acquired in March 2013 from KBS Realty of Newport Beach, Calif., for $240 million. In September of that year it put 15 of the properties, or 2.2 million sf, up for sale. The Klein purchase accounts for the lion’s share of that package. The disposition of the other properties is unclear.

Polish-born Samuel Klein, who died in November, was a Holocaust survivor who eventually made his way to Brazil. In 1957 he started Casas Bahia, which he built into one of the country’s largest retailers before selling it in 2009.

Mesa West Lends on Dallas ComplexMesa West Capital has written a $65.6 million floating-rate

loan for the buyer of a Dallas office/retail property that plans extensive renovations.

The borrower, a Quadrant Investment Properties partner-ship, purchased the 391,000-square-foot Centrum in Decem-ber, paying cash. The price is unknown. The property, at 3102 Oak Lawn Avenue, also contains separately owned residential condominiums that weren’t part of the deal.

The five-year loan, brokered by JLL, closed on Monday. Dal-las-based Quadrant and its partner, Angelo Gordon & Co. of New York, are expected to use some of the proceeds to reposition the office and retail components and lift the 71% occupancy rate. Los Angeles-based Mesa typically writes loans represent-ing leverage of 65-70%, which would indicate a valuation of $94 million to $100 million.

The Centrum is a 19-story tower, with a distinctive stair-step design, rising from a two-story base that fills most of a block in the Uptown/Turtle Creek submarket. The office and retail space is on the lower 11 floors, and the condos are on the upper stories.

The granite-and-glass building was developed in 1987. It has yet to undergo a major renovation. The Quadrant partnership plans to begin work this year that will include construction of a new lobby, courtyards and rooftop decks, along with upgrades to other common areas and the underground garage.

The property’s leasing rate is well below the submarket’s 87.6% level and the 81.1% rate for the overall Dallas office mar-ket at yearend, according to CBRE.

The Centrum’s largest tenant, law firm Baron & Budd, leases 147,000 sf across eight floors until 2017. Other tenants include Fitness Evolution Centrum (31,000 sf until 2018) and Compass Health Group (24,000 sf under two leases, maturing in 2017 and 2018). Mattito’s restaurant signed a lease in 2013 for 6,500 sf, and more restaurants are planned as part of the reposition-ing.

Call: 1-212-901-0542 www.imn.org/cfowest15 | Email: [email protected]

Don’t Forget To Mention Discount Code “HSP” For 10% Savings

Unless your company holds a multi-user license, it is a violation of U.S. copyright law to photocopy or reproduce any part of this publication, or forward it electronically, without first obtaining permission from Commercial Mortgage Alert. For details about licenses, contact JoAnn Tassie at 201-234-3980 or [email protected].

MBA.ORG/CREFST1514719

MBA’S COMMERCIAL�/� MULTIFAMILY SERVICING AND TECHNOLOGY CONFERENCE 2015

MAY 3–6SHERATON

BOSTON HOTEL

AdvanceMBA’s Commercial�/�Multifamily Servicing and Technology Conference 2015 can help you advance your business and professional performance in the year ahead. Join us for a dynamic conference packed with networking opportunities and much more, including:

• State of the Industry Sessions

• Hands-on Peer Workshops

• Expert Discussion Panels

• Technology Sessions

Make your plans today to network and learn from the most important and influential commercial�/�multifamily real estate leaders in our industry!

Early registration savings end March 31.

Register today by going to mba.org/CREFST15.

March 6, 2015 12Commercial Mortgage ALERT

Kroll Seeks Researcher, AnalystsKroll is recruiting three staffers for its commercial MBS

team.The rating agency is looking to replace a departing senior

researcher and fill two newly created posts, said senior man-aging director Eric Thompson, who runs the CMBS group. The positions are based at Kroll’s New York headquarters.

The vacancy stems from the resignation of senior director and head of CMBS research Terri Magnani, whose last day is today. She is joining Barclays as a director on the CMBS trading desk in New York, reporting to managing director Chris Haid. Magnani, who starts March 23, will be a “desk strategist” focus-ing on new-issue distribution and secondary-market trading in the U.S.

At Kroll, Magnani conducted research for internal use by analysts and prepared public reports. The company is seek-ing to hire a seasoned research pro, preferably someone with pre-crash experience in the commercial real estate industry at another rating agency or Wall Street shop.

Before joining Kroll in mid-2013, Magnani spent eight years at New York fund shop Tricadia Capital. From 2008 on, her duties there included co-managing a pool of CMBS and other commercial real estate debt investments for a private account. She previously worked at Merrill Lynch Investment Managers for 13 years.

Kroll, which has been growing steadily since it started rat-ing commercial MBS issues four years ago, also is seeking to add two staffers to its 35-member team that rates CMBS deals at issuance. The more-senior position, at the associate level, requires 4-7 years of experience. A similar background of 1-3 years is needed for the other opening, as an analyst or senior analyst. Both staffers would report to managing director Yee Cent Wong.

To apply for any of the openings, go to [email protected].

Trophy ... From Page 1

expansion.The 26-story building stands on the southwest corner of

57th Street, at the head of the prime Fifth Avenue shopping corridor, where retail rents are among the highest in the world. The property’s ground-level storefronts, whose tenants include luxury retailers Bulgari, Mikimoto and Piaget, account for at least 60% of its revenue, market pros say.

General Growth has said that once the acquisition is com-plete, its 50/50 joint venture with Sutton will convert addi-tional floors to retail space, increasing that component by up to 125,000 sf — then carve off and sell the office portion. Some $100 million of the loan proceeds would go into the reconfigu-ration, which would take about a year. The partnership is ask-ing lenders to provide those construction funds up-front.

Emptying some of the existing office space for conversion would trim revenue. Combined with the full funding of the loan, that would bring the initial debt yield down to a scant 2%. Potential lenders are being told that the income from the retail component would increase by 400% once it was built out and leased, and that the debt yield — net operating income as a percentage of the loan — would rise above 10%.

Lenders will weigh the construction and leasing risk, and the proposed 70% leverage, against Sutton’s track record as a specialist in converting and upgrading properties into high-end retail space. “He actively seeks out that pretty steep lever-age. But if you talk to him, he is absolutely convinced that he will perform on the rents,” one originator said. “And he’s proven it out time and time again.”

That pro noted that the proposal doesn’t fit the formulas lenders typically use to evaluate a deal — for example, the loan-per-foot metric for an office property. In this case, that would be an astronomical $3,125/sf. But while it currently accounts for more than 90% of the property, “the office [space] doesn’t matter,” he said. “You can get top-of-the-market rents and it doesn’t even turn the dial.”

The Crown Building was built in 1921. Its facade includes gilded details, and its roofline has a crown-like appearance that’s particularly distinctive when illuminated at night. The Spitzer partnership acquired the property for $93.6 million at a foreclosure auction in 1991, when it was 50% vacant.

The building is 97.8% leased, according to CoStar. The larg-est office tenants include talent agency ICM Partners (52,000 sf) and Apollo Management (43,000 sf).

Start your free trial at CMAlert.com or call 201-659-1700.

Plugged in?Commercial Mortgage Alert, the weekly newsletter that tips you off to opportunities inreal estate finance and securitization you won’t see anywhere else.

March 6, 2015 13Commercial Mortgage ALERT

INITIAL PRICINGSINITIAL PRICINGS

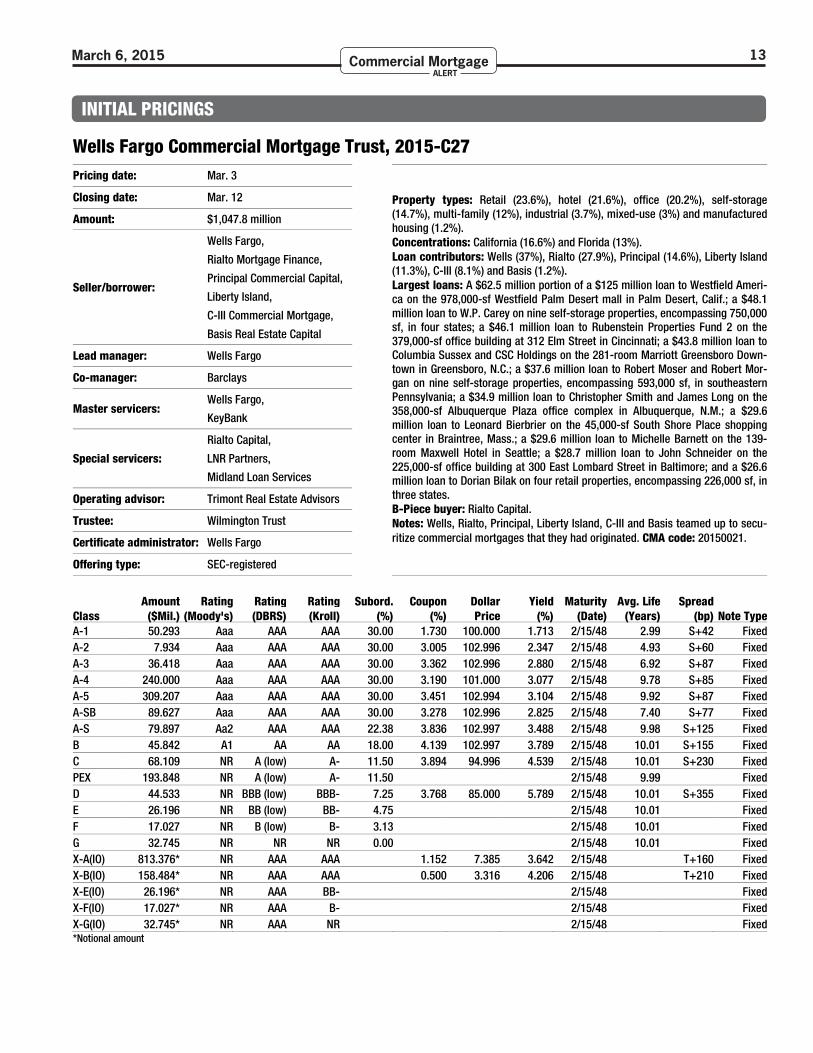

Wells Fargo Commercial Mortgage Trust, 2015-C27 Pricing date: Mar. 3

Property types: Retail (23.6%), hotel (21.6%), office (20.2%), self-storage (14.7%), multi-family (12%), industrial (3.7%), mixed-use (3%) and manufactured housing (1.2%). Concentrations: California (16.6%) and Florida (13%). Loan contributors: Wells (37%), Rialto (27.9%), Principal (14.6%), Liberty Island (11.3%), C-III (8.1%) and Basis (1.2%). Largest loans: A $62.5 million portion of a $125 million loan to Westfield Ameri-ca on the 978,000-sf Westfield Palm Desert mall in Palm Desert, Calif.; a $48.1 million loan to W.P. Carey on nine self-storage properties, encompassing 750,000 sf, in four states; a $46.1 million loan to Rubenstein Properties Fund 2 on the 379,000-sf office building at 312 Elm Street in Cincinnati; a $43.8 million loan to Columbia Sussex and CSC Holdings on the 281-room Marriott Greensboro Down-town in Greensboro, N.C.; a $37.6 million loan to Robert Moser and Robert Mor-gan on nine self-storage properties, encompassing 593,000 sf, in southeastern Pennsylvania; a $34.9 million loan to Christopher Smith and James Long on the 358,000-sf Albuquerque Plaza office complex in Albuquerque, N.M.; a $29.6 million loan to Leonard Bierbrier on the 45,000-sf South Shore Place shopping center in Braintree, Mass.; a $29.6 million loan to Michelle Barnett on the 139-room Maxwell Hotel in Seattle; a $28.7 million loan to John Schneider on the 225,000-sf office building at 300 East Lombard Street in Baltimore; and a $26.6 million loan to Dorian Bilak on four retail properties, encompassing 226,000 sf, in three states. B-Piece buyer: Rialto Capital. Notes: Wells, Rialto, Principal, Liberty Island, C-III and Basis teamed up to secu-ritize commercial mortgages that they had originated. CMA code: 20150021.

Closing date: Mar. 12

Amount: $1,047.8 million

Seller/borrower:

Wells Fargo,

Rialto Mortgage Finance,

Principal Commercial Capital,

Liberty Island,

C-III Commercial Mortgage,

Basis Real Estate Capital

Lead manager: Wells Fargo

Co-manager: Barclays

Master servicers: Wells Fargo,

KeyBank

Special servicers:

Rialto Capital,

LNR Partners,

Midland Loan Services

Operating advisor: Trimont Real Estate Advisors

Trustee: Wilmington Trust

Certificate administrator: Wells Fargo

Offering type: SEC-registered

Amount Rating Rating Rating Subord. Coupon Dollar Yield Maturity Avg. Life Spread Class ($Mil.) (Moody's) (DBRS) (Kroll) (%) (%) Price (%) (Date) (Years) (bp) Note Type A-1 50.293 Aaa AAA AAA 30.00 1.730 100.000 1.713 2/15/48 2.99 S+42 Fixed A-2 7.934 Aaa AAA AAA 30.00 3.005 102.996 2.347 2/15/48 4.93 S+60 Fixed A-3 36.418 Aaa AAA AAA 30.00 3.362 102.996 2.880 2/15/48 6.92 S+87 Fixed A-4 240.000 Aaa AAA AAA 30.00 3.190 101.000 3.077 2/15/48 9.78 S+85 Fixed A-5 309.207 Aaa AAA AAA 30.00 3.451 102.994 3.104 2/15/48 9.92 S+87 Fixed A-SB 89.627 Aaa AAA AAA 30.00 3.278 102.996 2.825 2/15/48 7.40 S+77 Fixed A-S 79.897 Aa2 AAA AAA 22.38 3.836 102.997 3.488 2/15/48 9.98 S+125 Fixed B 45.842 A1 AA AA 18.00 4.139 102.997 3.789 2/15/48 10.01 S+155 Fixed C 68.109 NR A (low) A- 11.50 3.894 94.996 4.539 2/15/48 10.01 S+230 Fixed PEX 193.848 NR A (low) A- 11.50 2/15/48 9.99 Fixed D 44.533 NR BBB (low) BBB- 7.25 3.768 85.000 5.789 2/15/48 10.01 S+355 Fixed E 26.196 NR BB (low) BB- 4.75 2/15/48 10.01 Fixed F 17.027 NR B (low) B- 3.13 2/15/48 10.01 Fixed G 32.745 NR NR NR 0.00 2/15/48 10.01 Fixed X-A(IO) 813.376* NR AAA AAA 1.152 7.385 3.642 2/15/48 T+160 Fixed X-B(IO) 158.484* NR AAA AAA 0.500 3.316 4.206 2/15/48 T+210 Fixed X-E(IO) 26.196* NR AAA BB- 2/15/48 Fixed X-F(IO) 17.027* NR AAA B- 2/15/48 Fixed X-G(IO) 32.745* NR AAA NR 2/15/48 Fixed *Notional amount

March 6, 2015 14Commercial Mortgage ALERT

INITIAL PRICINGSINITIAL PRICINGS

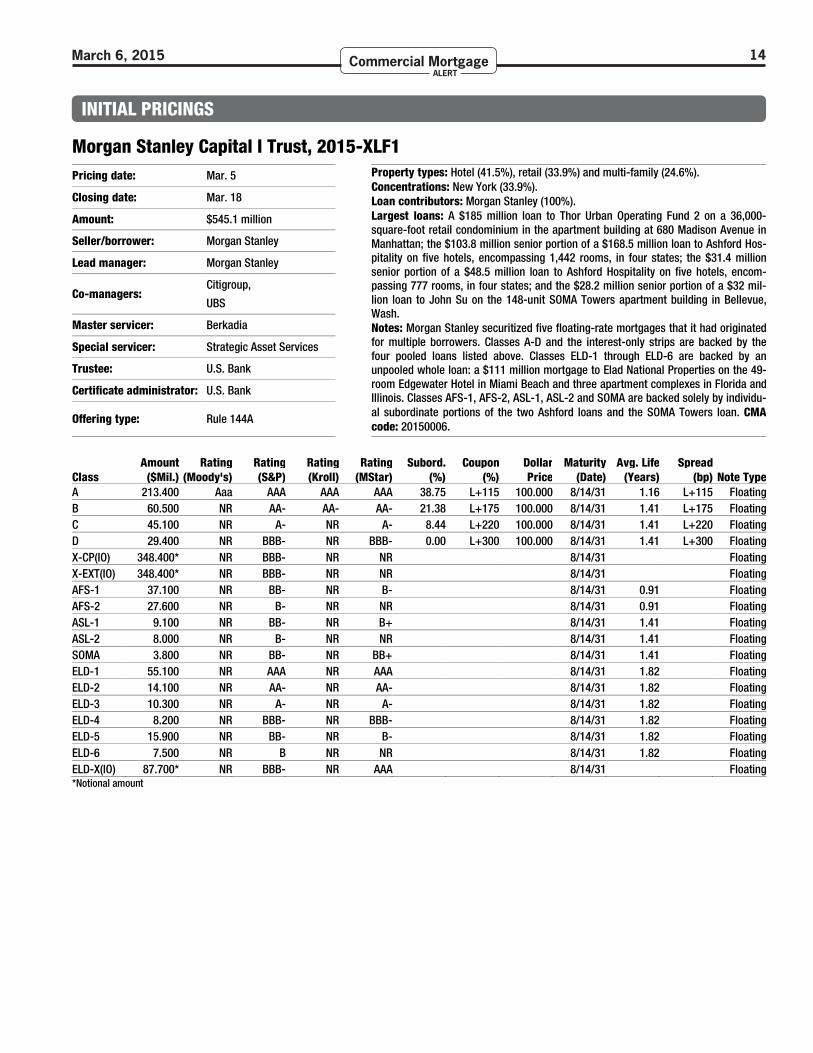

Morgan Stanley Capital I Trust, 2015-XLF1 Pricing date: Mar. 5

Property types: Hotel (41.5%), retail (33.9%) and multi-family (24.6%). Concentrations: New York (33.9%). Loan contributors: Morgan Stanley (100%). Largest loans: A $185 million loan to Thor Urban Operating Fund 2 on a 36,000-square-foot retail condominium in the apartment building at 680 Madison Avenue in Manhattan; the $103.8 million senior portion of a $168.5 million loan to Ashford Hos-pitality on five hotels, encompassing 1,442 rooms, in four states; the $31.4 million senior portion of a $48.5 million loan to Ashford Hospitality on five hotels, encom-passing 777 rooms, in four states; and the $28.2 million senior portion of a $32 mil-lion loan to John Su on the 148-unit SOMA Towers apartment building in Bellevue, Wash. Notes: Morgan Stanley securitized five floating-rate mortgages that it had originated for multiple borrowers. Classes A-D and the interest-only strips are backed by the four pooled loans listed above. Classes ELD-1 through ELD-6 are backed by an unpooled whole loan: a $111 million mortgage to Elad National Properties on the 49-room Edgewater Hotel in Miami Beach and three apartment complexes in Florida and Illinois. Classes AFS-1, AFS-2, ASL-1, ASL-2 and SOMA are backed solely by individu-al subordinate portions of the two Ashford loans and the SOMA Towers loan. CMA code: 20150006.

Closing date: Mar. 18

Amount: $545.1 million

Seller/borrower: Morgan Stanley

Lead manager: Morgan Stanley

Co-managers: Citigroup,

UBS

Master servicer: Berkadia

Special servicer: Strategic Asset Services

Trustee: U.S. Bank

Certificate administrator: U.S. Bank

Offering type: Rule 144A

Amount Rating Rating Rating Rating Subord. Coupon Dollar Maturity Avg. Life Spread Class ($Mil.) (Moody's) (S&P) (Kroll) (MStar) (%) (%) Price (Date) (Years) (bp) Note Type A 213.400 Aaa AAA AAA AAA 38.75 L+115 100.000 8/14/31 1.16 L+115 Floating B 60.500 NR AA- AA- AA- 21.38 L+175 100.000 8/14/31 1.41 L+175 Floating C 45.100 NR A- NR A- 8.44 L+220 100.000 8/14/31 1.41 L+220 Floating D 29.400 NR BBB- NR BBB- 0.00 L+300 100.000 8/14/31 1.41 L+300 Floating X-CP(IO) 348.400* NR BBB- NR NR 8/14/31 Floating X-EXT(IO) 348.400* NR BBB- NR NR 8/14/31 Floating AFS-1 37.100 NR BB- NR B- 8/14/31 0.91 Floating AFS-2 27.600 NR B- NR NR 8/14/31 0.91 Floating ASL-1 9.100 NR BB- NR B+ 8/14/31 1.41 Floating ASL-2 8.000 NR B- NR NR 8/14/31 1.41 Floating SOMA 3.800 NR BB- NR BB+ 8/14/31 1.41 Floating ELD-1 55.100 NR AAA NR AAA 8/14/31 1.82 Floating ELD-2 14.100 NR AA- NR AA- 8/14/31 1.82 Floating ELD-3 10.300 NR A- NR A- 8/14/31 1.82 Floating ELD-4 8.200 NR BBB- NR BBB- 8/14/31 1.82 Floating ELD-5 15.900 NR BB- NR B- 8/14/31 1.82 Floating ELD-6 7.500 NR B NR NR 8/14/31 1.82 Floating ELD-X(IO) 87.700* NR BBB- NR AAA 8/14/31 Floating *Notional amount

March 6, 2015 15Commercial Mortgage ALERT

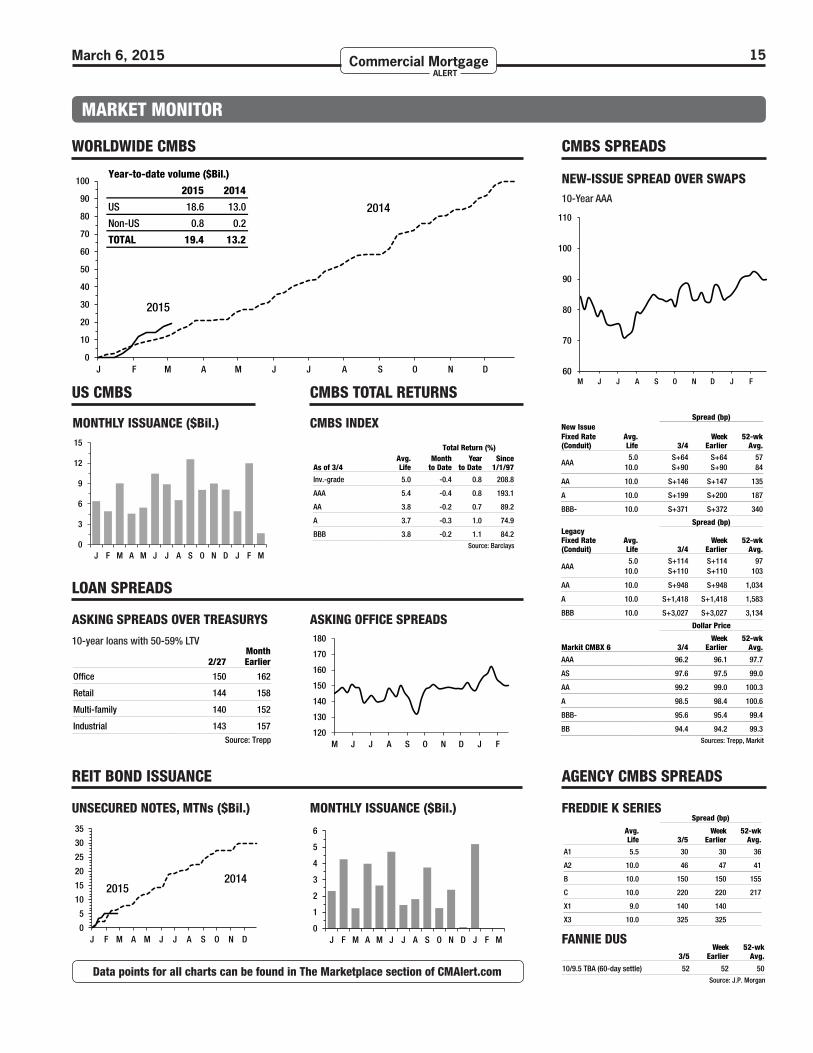

WORLDWIDE CMBS

US CMBS

LOAN SPREADS

ASKING SPREADS OVER TREASURYS ASKING OFFICE SPREADS

REIT BOND ISSUANCE

UNSECURED NOTES, MTNs ($Bil.) MONTHLY ISSUANCE ($Bil.)

Data points for all charts can be found in The Marketplace section of CMAlert.com

0

10

20

30

40

50

60

70

80

90

100

J F M A M J J A S O N D

2014

2015

MONTHLY ISSUANCE ($Bil.)

0

3

6

9

12

15

J F M A M J J A S O N D J F M

Spread (bp) New Issue

Fixed Rate Avg. Week 52-wk (Conduit) Life 3/4 Earlier Avg.

AAA 5.0

10.0 S+64

S+90 S+64 S+90

57 84

AA 10.0 S+146 S+147 135

A 10.0 S+199 S+200 187

BBB- 10.0 S+371 S+372 340 Spread (bp) Legacy Fixed Rate Avg. Week 52-wk (Conduit) Life 3/4 Earlier Avg.

AAA 5.0

10.0 S+114

S+110 S+114 S+110

97 103

AA 10.0 S+948 S+948 1,034

A 10.0 S+1,418 S+1,418 1,583

BBB 10.0 S+3,027 S+3,027 3,134 Dollar Price Week 52-wk Markit CMBX 6 3/4 Earlier Avg.

AAA 96.2 96.1 97.7

AS 97.6 97.5 99.0

AA 99.2 99.0 100.3

A 98.5 98.4 100.6

BBB- 95.6 95.4 99.4

BB 94.4 94.2 99.3 Sources: Trepp, Markit

Month 2/27 Earlier

Office 150 162

Retail 144 158

Multi-family 140 152

Industrial 143 157 Source: Trepp

120

130

140

150

160

170

180

M J J A S O N D J F

10-year loans with 50-59% LTV

CMBS TOTAL RETURNS

CMBS INDEX Total Return (%)

Avg. Month Year Since As of 3/4 Life to Date to Date 1/1/97

Inv.-grade 5.0 -0.4 0.8 208.8

AAA 5.4 -0.4 0.8 193.1

AA 3.8 -0.2 0.7 89.2

A 3.7 -0.3 1.0 74.9

BBB 3.8 -0.2 1.1 84.2 Source: Barclays

0

5

10

15

20

25

30

35

J F M A M J J A S O N D

2015 2014

0

1

2

3

4

5

6

J F M A M J J A S O N D J F M

60

70

80

90

100

110

M J J A S O N D J F

NEW-ISSUE SPREAD OVER SWAPS

CMBS SPREADS

10-Year AAA

WORLDWIDE CMBS ISSUANCE ($Bil.)2014 2015

01/06/00 J 0.0 0.0 Year-to-date volume ($Bil.)

01/13/00 1.6 0.0 2015 2014

01/20/00 2.1 0.2 US 18.6 13.0

01/27/00 4.2 2.5 Non-US 0.8 0.2

02/03/00 F 6.4 5.5 TOTAL 19.4 13.2

02/10/00 7.9 11.902/17/00 8.9 14.002/24/00 10.0 14.203/02/00 M 11.5 17.703/09/00 13.2 19.403/16/00 16.103/23/00 17.603/30/00 20.904/06/00 A 20.904/13/00 21.104/20/00 21.304/27/00 21.405/04/00 25.705/11/00 M 27.005/18/00 27.305/25/00 30.306/01/00 30.906/08/00 36.006/15/00 J 37.006/22/00 40.206/29/00 42.207/06/00 43.507/13/00 J 44.207/20/00 48.907/27/00 50.208/03/00 52.408/10/00 A 55.708/17/00 58.108/24/00 58.408/31/00 58.409/07/00 58.609/14/00 S 61.509/21/00 69.409/28/00 70.810/05/00 71.910/12/00 76.010/19/00 O 76.210/26/00 80.011/02/00 80.711/09/00 83.711/16/00 84.211/23/00 N 85.711/30/00 90.312/07/00 91.812/14/00 97.6

MARKET MONITOR

xxx 1Commercial Mortgage ALERT

AGENCY CMBS SPREADS

FREDDIE K SERIES Spread (bp)

Avg. Week 52-wk Life 3/5 Earlier Avg.

A1 5.5 30 30 36

A2 10.0 46 47 41

B 10.0 150 150 155

C 10.0 220 220 217

X1 9.0 140 140

X3 10.0 325 325 Week 52-wk 3/5 Earlier Avg.

10/9.5 TBA (60-day settle) 52 52 50 Source: J.P. Morgan

FANNIE DUS

Spread (bp)

Avg. Week 52-wk Life 3/5 Earlier Avg.

A1 5.5 30 30 36

A2 10.0 46 47 41

B 10.0 150 150 155

C 10.0 220 220 217

X1 9.0 140 140

X3 10.0 325 325 Week 52-wk 3/5 Earlier Avg.

10/9.5 TBA (60-day settle) 52 52 50 Source: J.P. Morgan

TO SUBSCRIBE

Signature:

COMMERCIAL MORTGAGE ALERT www.CMAlert.com

THE GRAPEVINE... From Page 1

Telephone: 201-659-1700 Fax: 201-659-4141 Email: [email protected]

Donna Knipp Managing Editor 201-234-3967 [email protected] Mura Senior Writer 201-234-3978 [email protected] Weihrauch Senior Writer 201-234-3988 [email protected] Friedman Senior Writer 201-234-3970 [email protected] Quinn Senior Writer 201-234-3997 [email protected]

Andrew Albert Publisher 201-234-3960 [email protected] Cowles General Manager 201-234-3963 [email protected] J. Ferris Editor 201-234-3972 [email protected] Murphy Deputy Editor 201-234-3975 [email protected] Lebowitz Operations Director 201-234-3977 [email protected] Grauer Database Director 201-234-3987 [email protected] E. Romano Advertising Director 201-234-3968 [email protected] Albert Advertising Manager 201-234-3999 [email protected] Renee Selnick Layout Editor 201-234-3962 [email protected] Eannace Marketing Director 201-234-3981 [email protected] Tassie Customer Service 201-659-1700 [email protected]

Commercial Mortgage Alert (ISSN: 1520-3697), Copyright 2015, is published weekly by Harrison Scott Publications Inc., 5 Marine View Plaza, Suite 400, Hoboken, NJ 07030-5795. It is a violation of federal law to photocopy or distribute any part of this publication (either inside or outside your company) without first obtaining permission from Commercial Mort-gage Alert. We routinely monitor forwarding of the publication by employing email-tracking technology such as ReadNotify.com. Subscription rate: $4,997 per year. Information on multi-user license options is available upon request.

YES! Sign me up for a one-year subscription to Commercial Mortgage Alert at a cost of $4,997. I understand I can cancel at any time and receive a full refund for the unused portion of my 46-issue license.

DELIVERY (check one): q Email. q Mail.

PAYMENT (check one): q Check enclosed, payable to Commercial

Mortgage Alert. q Bill me. q American Express. q Mastercard.

q Visa.

Account #:

Exp. date:

Name:

Company:

Address:

City/ST/Zip:

Phone:

E-mail:

MAIL TO: Commercial Mortgage Alert www.CMAlert.com 5 Marine View Plaza #400 FAX: 201-659-4141 Hoboken NJ 07030-5795 CALL: 201-659-1700

March 6, 2015 16Commercial Mortgage ALERT

structured-products market. He’ll be working closely with Jesse Kwon, who runs trading of such instruments, and Kyle Wilson, who oversees sales in that area. Korpita joined Morgan Stanley in 2008 after four years at Sorin Capital, where he managed a CMBS portfolio. Last year, he ran unsuccessfully for the Massachusetts House of Representatives on the Republican ticket.

Todd Moore joined Dallas-based Hart Advisors late last month as chief operating officer, a new position. He reports to chief executive Tanya Little. Hart advises borrowers on CMBS loan restructurings and assumptions. Moore will help guide the firm as it expands into additional markets, including Miami and Orange County, Calif., and keeps up with growing demand for its services. Moore was formerly a managing director at Pre-sidium Asset Solutions, where he over-saw liquidations and modifications of

assets in a $1 billion commercial loan servicing portfolio.

After six years as an associate at Weil, attorney Elizabeth Alibhai jumped to Dechert last month. She remains in London, as counsel in the Philadelphia-based firm’s global finance and real estate practice, which is led by partner Rick Jones. Alibhai advises clients on commercial real estate finance and other types of transactions, including acquisitions and sale-leasebacks. Before joining Weil, she worked at London-based Boodle Hatfield.

Attorneys Chad Baum, Matt Fischer and David Lingard joined Sidley Austin in New York over the last two weeks, as associates in the CMBS group led by partner Kevin Blauch. Two made the jump to Chicago-based Sidley from the New York office of Quinn Emanuel, where Baum was a staff attorney and Lingard was an associate. Fischer was an associ-ate at Dechert, also in New York.

Hunt Mortgage has added attorney Tracy Dennis as a managing director and

head of transaction management in its New York headquarters. Dennis, who started last week, will oversee all of the company’s transactions and closings. She reports to chief operating officer Nicholas Hoffer. Dennis previously spent more than two years at First American Title, where she was senior underwrit-ing counsel. Before that, she worked for five years at Credit Suisse, where she was a director.

DebtX wants to add one senior and one junior loan trader at its Boston headquarters. Candidates for the more-senior vice president/director position should have 5-10 years of loan acquisition, origination or similar experience. Duties would include extensive contact with buysiders at banks, funds and other investment shops, loan pricing and negotiations for the sale of performing and non-performing debt. Applicants for the junior post must be fluent in Spanish and will deal in Latin American and European markets. DebtX will provide training. Contact Liz Morini at [email protected].