dcmshriram nifty - narnolia.comcarbide and chlor ... fertilizer (urea) business:the company operates...

TRANSCRIPT

19-Dec-17

Key Highlights of the Report:

52wk Range H/L

Mkt Capital (Rs Cr)

Av. Volume (,000)

Financials/Valu

ation

FY15 FY16 FY17 FY18E FY19ENet Sales 5,639 5,841 6,117 7,349 8,144

EBITDA 399 505 771 1,289 1,437

EBIT 289 406 657 1,170 1,306

PAT 211 297 552 948 1,057

2QFY18 1QFY18 4QFY17 EPS (Rs) 13 18 34 58 65

Promoters 64 64 64 EPS growth (%) -13% 41% 86% 72% 11%

Public 34 34 34 ROE (%) 11% 14% 22% 28% 25%

Others 2 2 2 ROCE (%) 12% 13% 19% 27% 25%

Total 100 100 100 BV 114 129 156 207 266

P/B (X) 0.9 1.1 1.9 3.0 2.3

1Mn 3Mn 1Yr P/E (x) 8.3 7.7 8.6 10.0 9.0

Absolute 12 16 184

Rel.to Nifty 12 15 157 Recent Development

Current Sugar season has started and all company mills have started

crushing.The crushing period varies from region to region beginning in

October/ November and goes on till April/ May in all states except in

southern states like Tamil Nadu, Andhra Pradesh where it continues till

July/ August.

Input prices of Coal and Carbon material have risen over last year but

are stable sequentially. Better efficiencies and economies of scale post

completion of the expansion projects have mitigated part of the cost

increases emanating from increase in Coal pricesRitika [email protected]

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

239 Management expect a significant turnaround into the sugar industry due

to improving industry scenario along with supporting governmental

policies.Improvement in the return ratios

Keeping in mind near term headwind related to declining sugar prices

and sugarcane cost we maintain ACCUMULATE with a target price of

Rs. 695.

As on 10th November the board has given nod for additional investment

of Rs 838 crore for expansion projects.Out of this, Rs 500 crore is

estimated to be invested for expansion of its DSCL Sugar-Hariawan unit.

With the capacity enhancement, total sugar business capacity will

increase from 33,000 tonnes crushing per day (TCD) to 38,000 TCD.

Upside 14% The captive power plant for chlor-alkali at Bharuch which was

comissioned in Q2FY17 (full in Q3FY17) sharply ramped its operations

and is now operating at capacity utilization of 90%. 625/196

10,100

NSE Code - DCMSHRIRAM

NIFTY - 10389

CMP 611 DCM Shriram has posted a sales of Rs 1605 Cr.The growth in the

revenue was largely driven by growth in the revenue of sugar segment

and chlor-Vinyl BusinessTarget Price 695

INDUSTRY - Diversified

BLOOMBERG- DCM IN

BSE Code - 523367

Company Data

Stock Performance %

Shareholding patterns %

80

100

120

140

160

180

200

220

De

c-1

6

Ja

n-1

7

Ja

n-1

7

Fe

b-1

7

Ma

r-1

7

Ma

r-1

7

Ap

r-1

7

Ma

y-1

7

Ma

y-1

7

Ju

n-1

7

Ju

l-1

7

Au

g-1

7

Au

g-1

7

Se

p-1

7

Oc

t-1

7

Oc

t-1

7

No

v-1

7

De

c-1

7

DCMSHRIRAM NIFTY

12%

15%

24%

14%

18%

22%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

FY15 FY16 FY17

ROE ROCE

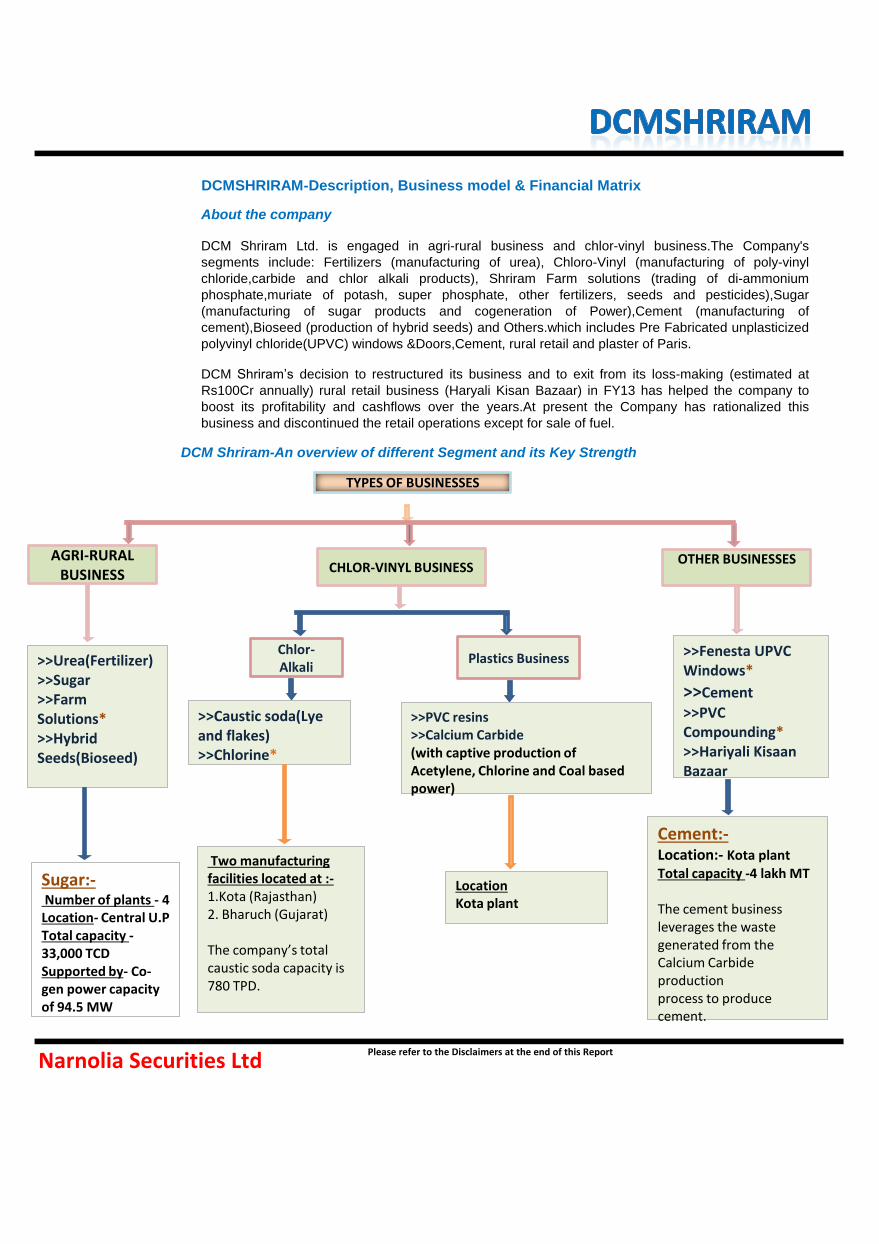

DCM Shriram-An overview of different Segment and its Key Strength

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

DCM Shriram Ltd. is engaged in agri-rural business and chlor-vinyl business.The Company's

segments include: Fertilizers (manufacturing of urea), Chloro-Vinyl (manufacturing of poly-vinyl

chloride,carbide and chlor alkali products), Shriram Farm solutions (trading of di-ammonium

phosphate,muriate of potash, super phosphate, other fertilizers, seeds and pesticides),Sugar

(manufacturing of sugar products and cogeneration of Power),Cement (manufacturing of

cement),Bioseed (production of hybrid seeds) and Others.which includes Pre Fabricated unplasticized

polyvinyl chloride(UPVC) windows &Doors,Cement, rural retail and plaster of Paris.

DCM Shriram’s decision to restructured its business and to exit from its loss-making (estimated at

Rs100Cr annually) rural retail business (Haryali Kisan Bazaar) in FY13 has helped the company to

boost its profitability and cashflows over the years.At present the Company has rationalized this

business and discontinued the retail operations except for sale of fuel.

DCMSHRIRAM-Description, Business model & Financial Matrix

About the company

TYPES OF BUSINESSES

AGRI-RURAL BUSINESS CHLOR-VINYL BUSINESS

OTHER BUSINESSES

>>Urea(Fertilizer) >>Sugar >>Farm Solutions* >>Hybrid Seeds(Bioseed)

Chlor- Alkali

Plastics Business >>Fenesta UPVC Windows*

>>Cement

>>PVC Compounding* >>Hariyali Kisaan Bazaar

Cement:- Location:- Kota plant Total capacity -4 lakh MT The cement business leverages the waste generated from the Calcium Carbide production process to produce cement.

Sugar:- Number of plants - 4 Location- Central U.P Total capacity - 33,000 TCD Supported by- Co-gen power capacity of 94.5 MW

>>Caustic soda(Lye and flakes) >>Chlorine*

>>PVC resins >>Calcium Carbide (with captive production of Acetylene, Chlorine and Coal based power)

Two manufacturing facilities located at :- 1.Kota (Rajasthan) 2. Bharuch (Gujarat) The company’s total caustic soda capacity is 780 TPD.

Location Kota plant

a)

b)

3.Agri-Input Business:

Agri-Input Businesses comprises of three segment namely Fertilizer Business,Shriram Farm

Solutions,and Bioseeds.

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

This business comprises 4 plants in Central U.P. with a total capacity of 33,000 TCD. The business is

supported by a Co-gen power capacity of 111MW(expanded in FY 17 from 94.5MWearlier). The company

has announced a new project of 150 KLD distillery at the Hariawan sugar plant, which is progesing as per

schedule and will be completed by Q4 FY 18.

Chlor- Alkali:DCM Shriram's Chlor-Alkali (Chemicals) business comprises Caustic Soda (Lye and

flakes), Chlorine and associated chemicals including Hydrochloric acid, Stable Bleaching powder,

Compressed Hydrogen and Sodium Hypochlorite.

The Company has two manufacturing facilities located at Kota (Rajasthan) and Bharuch (Gujarat) with

full coal based captive power. The company completed capacity expansion at the Bharuch plant in FY

17 taking the total caustic soda capacity to 1343 TPD from 780 TPD.

Plastics Business:A highly integrated business, located at the Kota plant, it involves manufacturing of

PVC resins and Calcium Carbide with captive production of Acetylene, Chlorine and Coal based

power.PVC Resin is a widely used raw material owing to its safe,healthy,convenient and aesthetical

advantage for applications in urban infrastructure,Electronic products,Consumer products,Irrigation etc.It

is a thermoplastic with 57% chlorine and 43% carbon,making it excellent fire resistant material.More

than70% of PVC resins are used for producing PVC .

2. Sugar:

DCM Shriram-Segment Wise business Overview

1.Chloro-Vinyl Businesses:

Product

Caustic soda

Chlorine

Calcium Carbide

PVC

Calcium Carbide is used in manufacturing

many other chemicals and also used steel

making

Industry size is estimated at 2.5 mn

mt.Domestic production estimated at 1.5mn

mt and balance is imported

Industry dynamics DCM's advantage Captive use

Fully integrated plant with coal based

captive power provides cost advantage

Used as intermediates which improves

margins

Chemical Segment Dynamics

Industry size is estimated at 3.2mn capacity

however production is estimated at 2.5 mn mt

due to lower utilisation

Chlorine is used mainly as intermediatery for

the manufacturing of other chemical products

PVC resins is further integrated into

manufacturing of PVC compounds

Chlorine - which is a by product of caustic

soda is used for captive purpose

35-40% is used captive for making PVC

70% of total production is used captiveDCM is the only company to use Calcium

Carbide in PVC manufacturing

35% of PVC Resins is used captive for making

PVC compounds

a)

b)

c)

Fertilizer (Urea) Business:The Company operates the dual feed naphtha/LNG based Urea plant

with a capacity of 3.79 lakh MT per annum, at its integrated manufacturing facility at Kota.The company

markets its products under the “Shriram Urea” brand. “Shriram Urea” a trusted name and enjoys high brand

equity amongst the farmers. The Company has an extensive distribution network over the entire Northern and

Central India

Bioseeds:Bioseed business is present across the entire Seeds value chain, i.e. Research,

Production, Processing, Extension activities and Marketing with established significant presence in India,

Philippines, Vietnam and Indonesia. The Company is present in both Field and Vegetable Crops in India. The

key crops in India comprises of BT cotton, Corn, Paddy, Vegetables among others.In Philippines, Vietnam and

Indonesia the business is present primarily in Corn.

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

3.Agri-Input Business:

Shriram Farm Solutions:This business provides a complete basket of Agri-inputs, viz. Hybrid seeds,

Pesticides, Bulk fertilizers, Micro-nutrients and other Value added inputs, through its broad distribution

network. The business also provides high quality agronomy services aimed at increasing farmer

productivity.

Segment

Seeds

Crop cares

Specialty nutrients

Bulk Fertiliser

Farm solutions business segment

Products sold

DAP, MOP, SSP etc

These fertilisers are imported and help

company to improve its product basket

Margins and returns

Enjoys margins of 15-20%. May some time lead to high

inventory risks

Margins in this segment ranges from 5-10%

Margins in this segment ranges from 10-40%Margins are very thin of 2-3% and requires high working

capital due to subsidies

Business dynamics

Includes selling of its own seeds as well as

purchased

These are purchased pesticides and

marketed by DCM under their brand.

These specialty products are traded and sold

through DCM's distribution network.

Insecticides, Fungicides, Herbicides

and plant growth regulators

GM seeds, hybrid seeds and

Varietal seeds

Water Soluble Fertilizers, Micro-

Nutrients etc

Country Field Crops

India

Vietnam

Philippines

Thailand

Indonesia

Bioseeds Presence by country-crop

Tomato, ridge gourd, okra, cabbage,hot pepper, cauliflower,sweet

pepper,coriander, eggplant, carrot, bittergourd, cucumber, pumpkin,

watermelon, bottle gourd,sponge gourd,musk melon

Vegetable Crops

Water melon, tomato

Corn, rice, sorghum,

sunflower,millet,

pigeon pea, cotton

Corn, rice

Corn, rice

Corn

Corn

a)

b)

c)

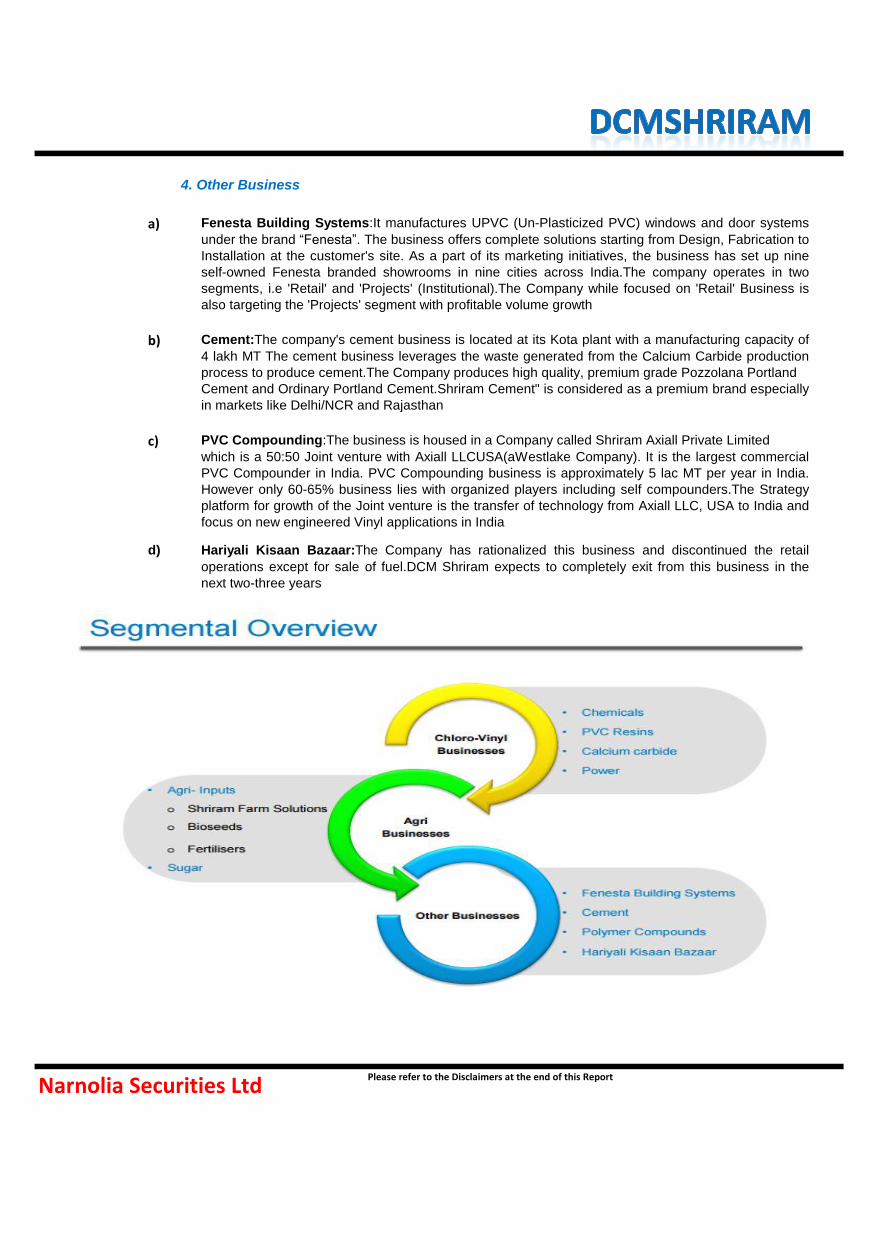

d) Hariyali Kisaan Bazaar:The Company has rationalized this business and discontinued the retail

operations except for sale of fuel.DCM Shriram expects to completely exit from this business in the

next two-three years

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

PVC Compounding:The business is housed in a Company called Shriram Axiall Private Limited

which is a 50:50 Joint venture with Axiall LLCUSA(aWestlake Company). It is the largest commercial

PVC Compounder in India. PVC Compounding business is approximately 5 lac MT per year in India.

However only 60-65% business lies with organized players including self compounders.The Strategy

platform for growth of the Joint venture is the transfer of technology from Axiall LLC, USA to India and

focus on new engineered Vinyl applications in India

4. Other Business

Fenesta Building Systems:It manufactures UPVC (Un-Plasticized PVC) windows and door systems

under the brand “Fenesta”. The business offers complete solutions starting from Design, Fabrication to

Installation at the customer's site. As a part of its marketing initiatives, the business has set up nine

self-owned Fenesta branded showrooms in nine cities across India.The company operates in two

segments, i.e 'Retail' and 'Projects' (Institutional).The Company while focused on 'Retail' Business is

also targeting the 'Projects' segment with profitable volume growth

Cement:The company's cement business is located at its Kota plant with a manufacturing capacity of

4 lakh MT The cement business leverages the waste generated from the Calcium Carbide production

process to produce cement.The Company produces high quality, premium grade Pozzolana Portland

Cement and Ordinary Portland Cement.Shriram Cement" is considered as a premium brand especially

in markets like Delhi/NCR and Rajasthan

DCM SHRIRAM Milestone & Key Events Over the Years

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

DCM SHRIRAM -Strong Manufacturing Capabilities

DCM SHRIRAM-Promoter & Promoter Group

DCM SHRIRAM--Institutional Investors

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

DCM SHRIRAM-Shareholding Pattern

# Promoter and Promoter Group Shares % Stake

SUMANT INVESTMENTS PRIVATE LIMITED 98282284 60.51

Individuals/Hindu undivided Family 5472500 3.37

Total 103754784 63.88

Institutional Investors Shares % Stake

1 Foreign Portfolio Investors 3462160 2.13

2 LIFE INSURANCE CORPORATION OF INDIA 12863749 7.92

3 Other Insurance Companies 2070591 1.28

Total 18396500 11.33

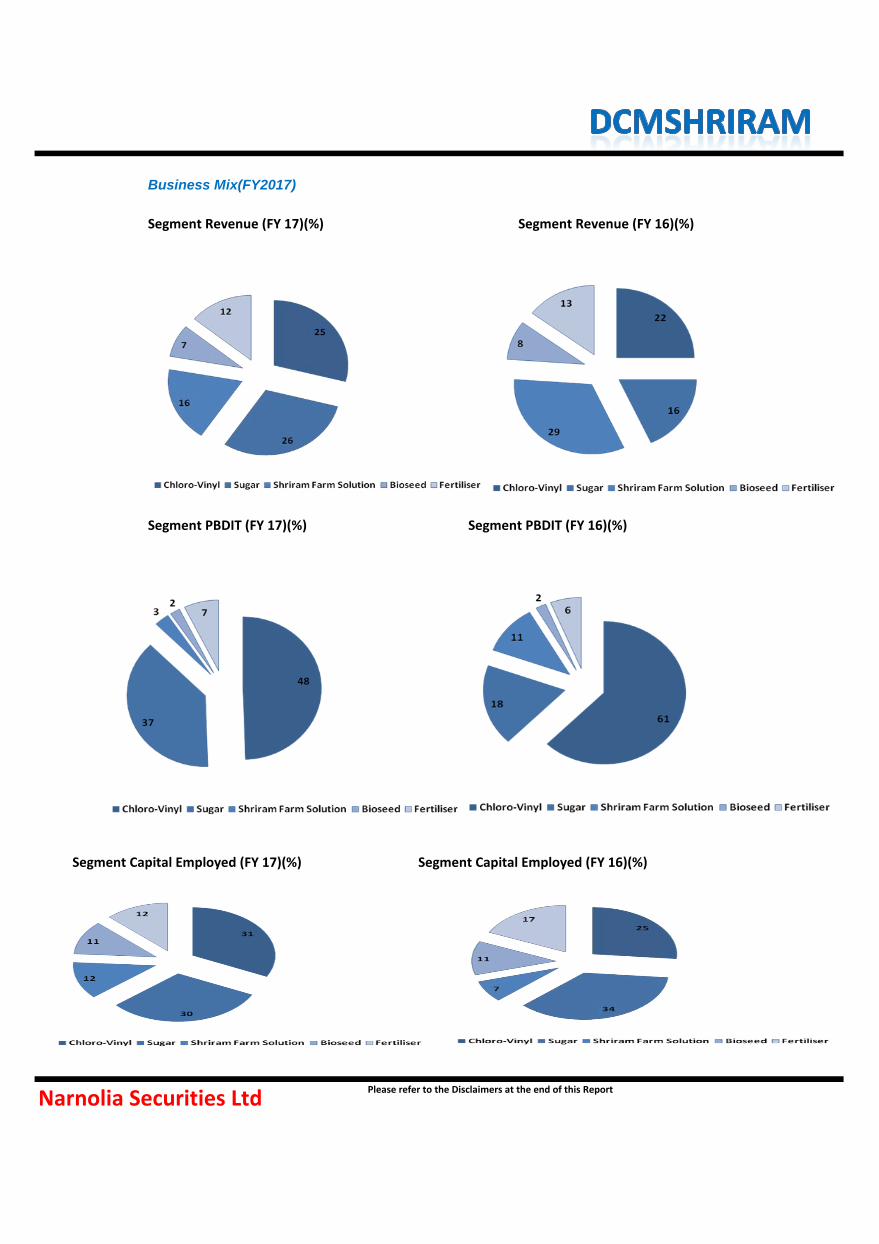

Segment Revenue (FY 17)(%) Segment Revenue (FY 16)(%)

Segment PBDIT (FY 17)(%) Segment PBDIT (FY 16)(%)

Segment Capital Employed (FY 17)(%) Segment Capital Employed (FY 16)(%)

Business Mix(FY2017)

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

Financials 2QFY17 3QFY17 4QFY17 1QFY18 2QFY18 YoY % QoQ% FY16 FY17 YoY %

Net Sales 1366 1448 1709 2052 1605 18% -22% 5841 6117 5%

Other Income 10 12 14 13 16 241% 22% 39 47 21%

COGS 799 662 804 1113 820 3% -26% 3453 3043 -12%

Employee Cost 128 137 141 146 145 13% -1% 494 533 8%

Other Expenses 111 165 247 139 137 23% -1% 1389 1442 4%

EBITDA 122 189 222 329 290 139% -12% 505 771 53%

Depreciation 27 31 32 32 36 33% 13% 99 114 15%

Interest 13 17 22 24 20 56% -18% 86 71 -17%

PBT 92 152 183 287 250 173% -13% 359 633 76%

Tax 1 16 25 53 78 14406% 48% 62 80 30%

PAT 91 136 156 233 172 88% -26% 297 552 86%

Bioseeds an agri input Segment revenue increased by 21% YoY to Rs 80 Cr on the back of

higher demand in Cotton and Corn.

Fertilisers (Urea) an agri input Segment revenue increased by 13% YoY to Rs 196 Cr due to healthy

volume growth and increased production.

Others segment which includes primarily Fenesta, Cement, Hariyali and PVC compounding that is

under a 50:50 JV reported a overall decline of 5% YoY revenue to Rs189Cr due to lower volume of

traded cement and slowdown in the order bookin in Fenesta.

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

Sriram Farm Solutions an agri input Segment revenue declined by 37% YoY to Rs 152 Cr

Quarterly Performance

Q2FY18 Result Update:

Chlor-alkali revenue increased by 29% YoY to Rs 485 Cr, as the capacity utilization at newly

commissioned facility increased to 90% from 80% in Q1FY18.

Sugar Segment revenue increased by 30% YoY to Rs 516 Cr,due to the Growth in volume of cane

crushed and sustained high sugar price.

Sugar volume increased by 35% yoy to 1.32mn quintal compared to 0.98mn quintal in Q2FY17.

17

86

14

15

12

57

13

07

14

36

13

59

14

42

16

97

20

47

15

98

123

62 60 55

167

91

136156

233

172

0

500

1000

1500

2000

2500

Net Sales PAT

Margin % 2QFY17 3QFY17 4QFY17 1QFY18 2QFY18 YoY(+/-) QoQ(+/-) FY16 FY17 YoY(+/-)

Gross Margin 42% 54% 53% 46% 49% 7% 3% 41% 50% 9%

EBITDA Margin 9% 13% 13% 16% 18% 9% 2% 9% 13% 4%

PAT Margin 7% 9% 9% 11% 11% 4% -1% 5% 9% 4%

Chloro-Vinyl:Capacity expansion of Chlor-alkali at Kota (84TPD) and Bharuch (146TPD) at an

investment of Rs98Cr. Bharuch expansion is expected to be completed by Q1FY20 and Kota by

Q2FY20.The company expects to sustain / improve on the ~90% capacity utilization achieved by the

end of Q2FY18 at Bharuch.

Sugar:As per the management distillery plant with 150 KLPD capacity is progesing as per schedule

and will be commissioned in Q4FY18.The company has also approved expansion of Sugar capacity by

5,000TCD, which includes a distillery of 100KLD and power Co-gen (34MW) at an investment of

~Rs500Cr. These Projects are likely to be completed by Q3FY19 and Distillery by Q3FY20.

Power:To replace the old 50MW plant a new 66MW Power plant at Kota, is coming on stream at an

investment of Rs240Cr and is expected to be completed by Q3FY20.

In chemical segment new 60TPD ‘Anhydrous Aluminum Chloride’ facility at an investment of Rs43Cr

at Bharuch Chemicals complex expected to be completed by Q2FY19.

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

Company Expansion Projects in different sectors

Gross margin declined by ~600 bps YoY to 26% aided by decrease in the input prices of raw material

cost.

EBITDA margin improved by ~920 bps to 18.1% YoY driven by by the increase in Chlor-alkali volume

and higher realization in the Chloro-Vinyl business.

PAT margin improved by ~400 bps YoY and PAT remained Rs 172 Cr for this quarter led by lower

interest cost and strong growth at operating level.

Investment Arguments:

Improvement in the Debt Equity Ratio Improvement in the EBITDA Margin YoY

Key Risks:

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

Increase in Raw MaterialCost(Prices of Coal and carbon) and power cost for Chlor Vinyl

business:Rising energy costs as a result of rising international and domestic coal prices, freight,

duties and levies, is increasing the cost of production which will impact the margin adversely.

Normal Monsoon will have significant impact on the revenue stream of Agri-Input

business:Company has a high dependence on monsoon as over 50% of the revenue comes from agri

input business which comprises of Fertlizer,Shriram Food Solutions,and Bioseeds.The Agri-Input

businesses,accounted for about 51% of revenue in FY17.

Strong Debt-To-Equity Ratio:Going ahead generation of strong cashflow will help the company to

reduce debt gradually in FY18 and FY19.

New Distillery project at Hariawan to aid growth in the sugar segment:As per the management

distillery plant with 150 KLPD capacity is progesing as per schedule and will be commissioned in

Q4FY18, which will lead to further improvement of profitability of Sugar business, in case of cyclical

downturn in the Sugar business.

Divestment of loss making Hariyali Kisan Bazar business will lead to improvement in the return

ratios (ROE/RoCE improvement):DCM Shriram’s Hariyali Kisan Bazar were rationalised in 2013. The

company is focused on the sale of remaining properties, which progressed slowly in FY17 and is

expected to take another 2-3 years.Moreover, the sale of properties under this segment will make it

further asset light, releasing cash.This will lead to further improvement in the overall RoCE profile of

the company.The segment had been making huge losses for the past several years.

Dependency on rainfall: As company has a direct impact of rainfall so unseasonal rains could impact

Agri Input Business which would impact the company’s sales.So Timely and normal rainfall is essential

for agrochemical companies to post good performance.

Capacity addition in the high margin Chloro Vinyl will boost margin significantly: The capacity

utilization at newly commissioned facility at Bharuch increased to 90% from 80% in Q1FY18 due to

which EBITDA margin expanded by 920bps yoy to 18%.The company is increasing the high margin

Chlor Alkali capacity at Kota (84TPD) and Bharuch (146TPD) at an investment of Rs98Cr. Bharuch

expansion to be completed by Q1FY20 and Kota by Q2FY20 and the management expects it to run at

optimum capacity utilization immediately

0.8

0.4

0.2

0.5

0.3

0

0.2

0.4

0.6

0.8

1

FY13 FY14 FY15 FY16 FY17

Net Debt/ Equity

1)

Global and Indian Caustic Soda Segment Breakup (%)

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

Industry Overview:

Chlor- Alkali industry:The Chlor- Alkali industry in India has 35 operating units with a combined

installed capacity of 3.7 million Tons per annum of Caustic Soda.Globally, 40% of the chlorine

produced is used by the vinyl industry whereas only 7.8% of the chlorine produced in India is used.

This is due to lack of expansion in PVC production capacity in India. As a consequence, the chlor-

alkali industry in India is a caustic driven industry unlike the rest of the world, where it is a chlorine

driven industry

Global and Indian Chlorine Segment Breakup (%)

2)

Domestic manufacturers and capacities (kT)

3)

Domestic Sugar Price: Trend reversal

Sugar:The Indian Sugar Industry is the second largest producer after Brazil and the largest consumer

of sugar in the world.This year, Indian sugar industry witnessed a revival from the preceding

depressed years. Central as well as State Governments are to be credited for this success for the

initiatives undertaken in the preceding years along with the rationale policies adopted in sugar season

2016-17. A balanced demand supply situation in India also supported the initiative and ensured that

sugar prices remained reasonable at around 35 Rs/kg to 37 Rs/kg throughout the year.

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

Plastics:India's PVC resin installed capacity currently stands at around 1.4 million Metric Ton per

annum(MTPA).As against this,domestic demand has been growing steadily and has reached~2.95MTPA

in FY17,up 9.3% over last year.The gap in demand and supply,which currently stands at 54.5% of total

demand,is being met by the import of PVC resin.Reliance Industries accounts for roughly 50% of the

country’s PVC production spread across three plants in Gujarat, followed by Chemplast (19%) and

Finolex Industries (17%). DCM Shriram has a market share of 5% in the PVC segment Indian PVC

demand is expected to grow at 8 to 10% CAGR for the next 4-5 years.

Income Statement Rs in Crores Key Ratios

Y/E March FY16 FY17 FY18E FY19E Y/E March FY16 FY17 FY18E FY19ERevenue from Operation 5,841 6,117 7,349 8,144 ROE 14% 22% 28% 25%

Change (%) 4% 5% 20% 11% ROCE 13% 19% 27% 25%

EBITDA 505 771 1,289 1,437 Asset Turnover 1.2 1.1 1.1 1.1

Change (%) 27% 53% 67% 11% Debtor Days 80 60 50 48

Margin (%) 9% 13% 18% 18% Inventory Days 82 96 90 92

Dep & Amortization 99 114 119 131 Payable Days 72 70 65 65

EBIT 406 657 1,170 1,306 Interest Coverage 4.73 9.20 15.90 18.15

Interest & other finance cost 86 71 74 72 P/E 8 9 10 9

Other Income 39 47 60 63 Price / Book Value 1.1 1.9 3.0 2.3

EBT 359 633 1,156 1,297 EV/EBITDA

Exceptional Item - - - - FCF per Share (18) 19 24 23

Tax 62 80 208 240 Dividend Yield 0.15 0.17 0.17 0.17

Minority Int & P/L share of Ass. - - - -

Reported PAT 297 552 948 1,057

Adjusted PAT 297 552 948 1,057

Change (%) 41% 86% 72% 11%

Margin(%) 5% 9% 13% 13%

Balance Sheet Rs in Crores Cash Flow Statement Rs in Crores

Y/E March FY16 FY17 FY18E FY19E Y/E March FY16 FY17 FY18E FY19EShare Capital 33 33 33 33 PBT 359 552 1,156 1,297

Reserves 2,058 2,495 3,333 4,280 (inc)/Dec in Working Capital (265) 123 10 (94)

Networth 2,091 2,528 3,366 4,313 Non Cash Op Exp 99 114 119 131

Debt 985 980 1,008 999 Interest Paid (+) 86 71 74 72

Other Non Current Liab 172 189 210 231 Tax Paid (83) (147) (208) (240)

Total Capital Employed 3,076 3,508 4,374 5,312 others (28) (30) - -

Net Fixed Assets (incl CWIP) 1,793 2,086 2,736 3,402 CF from Op. Activities 182 772 1,151 1,166

Non Current Investments - - - - (inc)/Dec in FA & CWIP (466) (459) (769) (798)

Other Non Current Assets 116 77 77 77 Free Cashflow (285) 313 382 367

Non Current Assets 1,994 2,317 2,966 3,632 (Pur)/Sale of Investment (0) (6) - -

Inventory 1,320 1,616 1,812 2,053 others 59 35 - -

Debtors 1,287 1,004 1,007 1,071 CF from Inv. Activities (407) (426) (768) (798)

Cash & Bank 40 212 152 22 inc/(dec) in NW - - - -

Other Current Assets 183 259 311 345 inc/(dec) in Debt 311 (61) 27 (9)

Current Assets 2,895 3,135 3,334 3,549 Interest Paid (87) (67) (74) (72)

Creditors 1,149 1,176 1,309 1,450 Dividend Paid (inc tax) (55) (113) (110) (110)

Provisions 29 40 48 54 others (3) 71 - -

Other Current Liabilities 318 454 522 578 CF from Fin. Activities 166 (171) (156) (191)

Curr Liabilities 1,750 1,867 2,115 2,344 Inc(Dec) in Cash (60) 176 226 177

Net Current Assets 1,145 1,268 1,219 1,205 Add: Opening Balance 86 23 212 152

Total Assets 5,007 5,574 6,423 7,305 Closing Balance 26 199 438 329

Financials Snap Shot

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

Narnolia Securities LtdPlease refer to the Disclaimers at the end of this Report

Going forward, the company's continuous focus on improving cost efficiency to mitigate the

impact of rising input cost will ensure stability in EBITDA Margin. Chlorine market demand is

expected to remain strong due to increased penetration in the Western and Northern regions

of the Country while growth in the alumina industry is expected to propel the demand for

caustic soda in times to come, thus benefiting the market for chemicals segment in the long

run. Declining sugar price makes us cautious about near term revenue visibility of the

company. Also any significant increase in cane cost going forward could adversely impact the

financial performance and cash generation potential of the company. Keeping in mind near

term headwind related to declining sugar prices and sugarcane cost we maintain

ACCUMULATE with a target price of Rs. 695.

Outlook & Valuation

DCM Shriram has reported sales of Rs 1605 Cr, in line with our estimates. Sales grew by

17.5% YOY on account of growth in revenues from the Sugar business (sustained high sugar

price) as well as capacity ramp-up of new Chloro-Vinyl plant. Margin improvement was driven

by the increase in Chlor-alkali volume and higher realization in the Chloro-Vinyl business.

Good monsoon season had a positive impact on the demand for the company’s products and

are evident from the growth in revenues in the last two quarters.

Narnolia Securities Ltd201 | 2nd Floor | Marble Arch Build ing | 236B-AJC Bose

Road | Kolkata-700 020 , Ph : 033-40501500

email: [email protected],

website : www.narnolia.com

Risk Disclosure & Disclaimer: This report/message is for the personal information of

the authorized recipient and does not construe to be any investment, legal or taxation

advice to you. Narnolia Securities Ltd. (Hereinafter referred as NSL) is not soliciting any

action based upon it. This report/message is not for public distribution and has been

furnished to you solely for your information and should not be reproduced or

redistributed to any other person in any from. The report/message is based upon publicly

available information, findings of our research wing “East wind” & information that we

consider reliable, but we do not represent that it is accurate or complete and we do not

provide any express or implied warranty of any kind, and also these are subject to change

without notice. The recipients of this report should rely on their own investigations,

should use their own judgment for taking any investment decisions keeping in mind that

past performance is not necessarily a guide to future performance & that the the value of

any investment or income are subject to market and other risks. Further it will be safe to

assume that NSL and /or its Group or associate Companies, their Directors, affiliates

and/or employees may have interests/ positions, financial or otherwise, individually or

otherwise in the recommended/mentioned securities/mutual funds/ model funds and

other investment products which may be added or disposed including & other mentioned

in this report/message.