daily fx str europe 29 june 2011

TRANSCRIPT

8/6/2019 Daily FX Str Europe 29 June 2011

http://slidepdf.com/reader/full/daily-fx-str-europe-29-june-2011 1/8

Foreign Exchange London 08:00

FX Daily Strategist: Europe

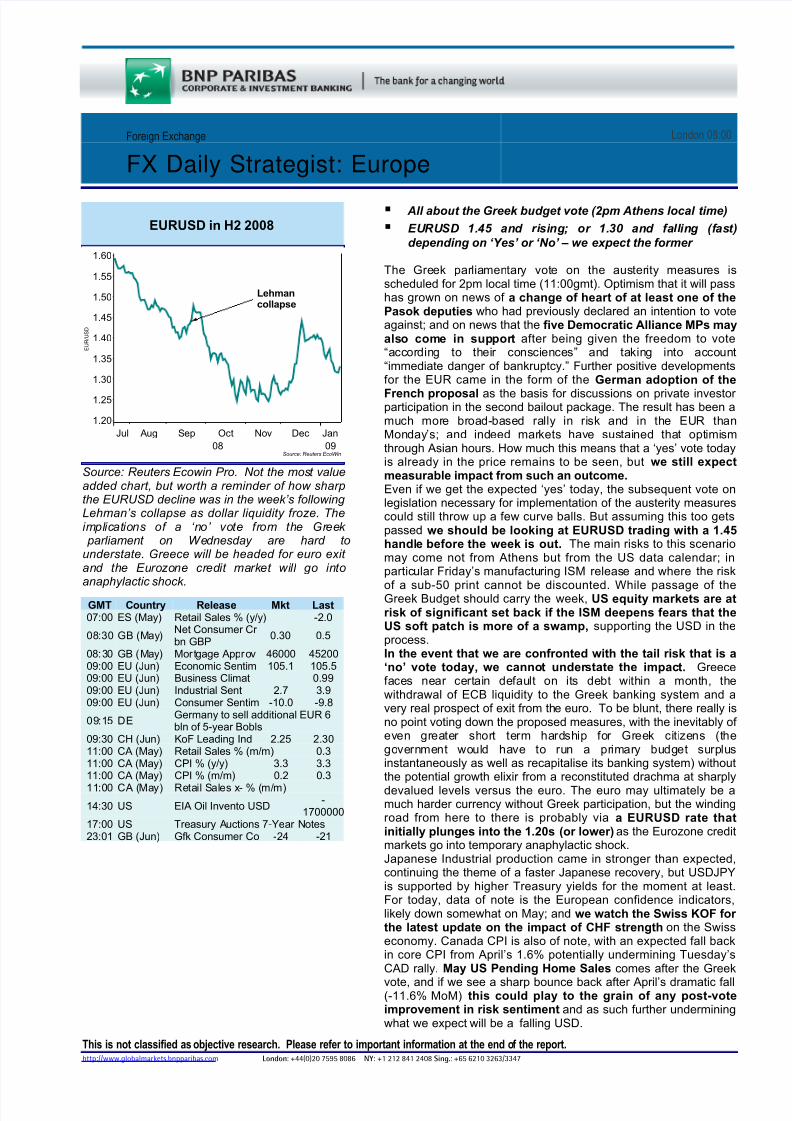

EURUSD in H2 2008

Source: Reuters EcoWin

Jul

08

Aug Sep Oct Nov Dec Jan

09

E U R / U S D

1.20

1.25

1.30

1.35

1.40

1.45

1.50

1.55

1.60

Lehmancollapse

Source: Reuters Ecowin Pro. Not the most valueadded chart, but worth a reminder of how sharpthe EURUSD decline was in the week’s following Lehman’s collapse as dollar liquidity froze. Theimplications of a ‘no’ vote from the Greek parliament on Wednesday are hard tounderstate. Greece will be headed for euro exit and the Eurozone credit market will go intoanaphylactic shock.

This is not classified as objective research. Please refer to important information at the end of the report.http://www.globalmarkets.bnpparibas.com London: +44(0)20 7595 8086 NY : +1 212 841 2408 Sing.: +65 6210 3263/3347

GMT Country Release Mkt Last07:00 ES (May) Retail Sales % (y/y) -2.0

08:30 GB (May)Net Consumer Cr bn GBP

0.30 0.5

08:30 GB (May) Mortgage Approv 46000 4520009:00 EU (Jun) Economic Sentim 105.1 105.509:00 EU (Jun) Business Climat 0.9909:00 EU (Jun) Industrial Sent 2.7 3.909:00 EU (Jun) Consumer Sentim -10.0 -9.8

09:15 DEGermany to sell additional EUR 6bln of 5-year Bobls

09:30 CH (Jun) KoF Leading Ind 2.25 2.3011:00 CA (May) Retail Sales % (m/m) 0.311:00 CA (May) CPI % (y/y) 3.3 3.311:00 CA (May) CPI % (m/m) 0.2 0.3

11:00 CA (May) Retail Sales x- % (m/m)

14:30 US EIA Oil Invento USD-

170000017:00 US Treasury Auctions 7-Year Notes23:01 GB (Jun) Gfk Consumer Co -24 -21

All about the Greek budget vote (2pm Athens local time)

EURUSD 1.45 and rising; or 1.30 and falling (fast)

depending on ‘Yes’ or ‘No’ – we expect the former

The Greek parliamentary vote on the austerity measures isscheduled for 2pm local time (11:00gmt). Optimism that it will passhas grown on news of a change of heart of at least one of thePasok deputies who had previously declared an intention to voteagainst; and on news that the five Democratic Alliance MPs mayalso come in support after being given the freedom to vote“according to their consciences” and taking into account“immediate danger of bankruptcy.” Further positive developmentsfor the EUR came in the form of the German adoption of the

French proposal as the basis for discussions on private investor participation in the second bailout package. The result has been amuch more broad-based rally in risk and in the EUR thanMonday’s; and indeed markets have sustained that optimismthrough Asian hours. How much this means that a ‘yes’ vote todayis already in the price remains to be seen, but we still expectmeasurable impact from such an outcome.Even if we get the expected ‘yes’ today, the subsequent vote onlegislation necessary for implementation of the austerity measurescould still throw up a few curve balls. But assuming this too getspassed we should be looking at EURUSD trading with a 1.45handle before the week is out. The main risks to this scenariomay come not from Athens but from the US data calendar; inparticular Friday’s manufacturing ISM release and where the risk

of a sub-50 print cannot be discounted. While passage of theGreek Budget should carry the week, US equity markets are atrisk of significant set back if the ISM deepens fears that theUS soft patch is more of a swamp, supporting the USD in theprocess.In the event that we are confronted with the tail risk that is a‘no’ vote today, we cannot understate the impact. Greecefaces near certain default on its debt within a month, thewithdrawal of ECB liquidity to the Greek banking system and avery real prospect of exit from the euro. To be blunt, there really isno point voting down the proposed measures, with the inevitably of even greater short term hardship for Greek citizens (thegovernment would have to run a primary budget surplusinstantaneously as well as recapitalise its banking system) withoutthe potential growth elixir from a reconstituted drachma at sharply

devalued levels versus the euro. The euro may ultimately be amuch harder currency without Greek participation, but the windingroad from here to there is probably via a EURUSD rate thatinitially plunges into the 1.20s (or lower) as the Eurozone creditmarkets go into temporary anaphylactic shock.Japanese Industrial production came in stronger than expected,continuing the theme of a faster Japanese recovery, but USDJPYis supported by higher Treasury yields for the moment at least.For today, data of note is the European confidence indicators,likely down somewhat on May; and we watch the Swiss KOF for the latest update on the impact of CHF strength on the Swisseconomy. Canada CPI is also of note, with an expected fall backin core CPI from April’s 1.6% potentially undermining Tuesday’sCAD rally. May US Pending Home Sales comes after the Greek

vote, and if we see a sharp bounce back after April’s dramatic fall(-11.6% MoM) this could play to the grain of any post-voteimprovement in risk sentiment and as such further underminingwhat we expect will be a falling USD.

8/6/2019 Daily FX Str Europe 29 June 2011

http://slidepdf.com/reader/full/daily-fx-str-europe-29-june-2011 2/8

Market: Risk back in the ascendancy fro late yesterdayamid optimism that the Greek austerity package wouldpass in Wednesday's (2pm local time) vote. AUD andNOK were the best performing G10 currencies in NYC,both up just shy of 1%, followed by NZD +0.8% and EUR+0.6%. Yen the only currency to fall versus USD, -0.3%.In early Europe, USD is mixed versus G10 FX: AUD,CHF, NZD all 0.20-0.30% higher, CAD. JPY (+0.11%).EUR and GBP both flat at best, while the Scandies arethe underperformers (-0.15—0.28%). Asian FX all higher today, led by THB and KRW (+0.60% plus), MYR, INR,IDR (0.20-0.33%), others pretty flattish.

Asian equities also all in the green by over 1.10%(e.g. Japan +1.50% plus), but unfortunately China,Philippines and New Zealand are about 0.70% in thered. China’s losses are broad based, and especiallyconcentrated in financials (SHCOMP financials -1.03%).This after strong showing in the US: US equity indices

were all more than 1.20% stronger, NASDAQ +1,53%,S&P500 +1.29% and DJIA +1.21%.

Commodities stronger across the board except Brentcrude and gasoline

RECAP yesterday: European equities all stronger onaverage by 1% (Eurostoxx 50 +0.98%) late yesterday,led by CAC40 +1.5%. FTSE +0.78%. GIPS SOVspreads vs. Germany were all sharply tighter lateyesterday, led by Ireland (-63bp) Portugal (-48bp) andGreece (-34bps).

The Day Ahead (Via MNI news)

Greek vote today: While the Bloomberg calendar saythe Greek austerity measures vote roll call starts at 12:00GMT, MNI news says it will come after the market closearound 1830GMT, although that is subject to debate andevents.

European data: German DIW economic researchinstitute monthly economic barometer (time unknown),French 1Q detailed GDP (at 0630GMT), Spain May retailsales (at 0700GMT) then EMU June business climateindicator (0900GMT)

Germans weigh in through speeches: At 1115GMT,German FinMin Schaeuble gives a speech on financialmarket regulation, in Berlin, followed at 1230GMT byGerman Chancellor Merkel. At 1330GMT, ECB (Buba)Jens Weidmann gives a speech on financial marketregulation after the crisis, in Frankfurt

UK data: April Index of Services, BOE Lending toIndividuals, May BOE Final M4 and May BOE EffectiveRates (all at 0830GMT).

US data: MBA Mortgage Application Index (June 24week) at 1130GMT. At 1400GMT, the IMF releases itsannual Article IV review of US economy. At the sametime, May NAR Pending Home Sales June 11 Help-wanted Online data are released.

At 1600GMT, Fed Governor Raskin delivers a speechon rebuilding road to financial stability at the NewAmerican Foundation in Washington.

Weekly EIA Crude Oil Stocks numbers are released at1430GMT.

NEWS

US

The Fed, amid the ongoing worries about Europe'ssovereign debt crisis, last week quietly approved theextension of a crisis-lending program that allows theECB to tap the U.S. for dollars, the WSJ reports. TheFed's dollar-lending agreements with the ECB - as wellas the central banks of England, Canada, Japan andSwitzerland - were scheduled to expire Aug 1. The Fed

and other central banks haven't yet disclosed renewal of the agreements, known as swap lines, the paper notes.

DATA RECAP: Case Schiller April composite homeprices -3.96% YoY as expected and vs. -3.61% in March.MoM -0.2%. Conference Board consumer confidence58.5 from 60.8 and 612.0 expected. Richmond Fedmanufacturing index +3 from -6 and vs. -3 expected

Europe

Greece politics: The Kathermerini website says thatboth the government and opposition are putting pressureon dissenters to vote along party lines. However, reading

between the lines of the article, it would appear thegovernment may have secured enough votes. Biut,eKathermerini warns that even if the government winsWednesday's vote it is not necessarily home free asThursday's vote - on a bill outlining the implementation of the measures set out in the first bill - must also besecured if the next tranche of rescue funding is to bereleased by the Troika and snap elections are to beaverted.

Greece CB Governor Provopoulos tells FT thatGreece will be committing "suicide" if its parliamentfails to back sweeping austerity measures aimed ataverting a catastrophic default, the Bank of Greece head

tells the FT. The warning by Provopoulos, further heightened the stakes ahead of a knife-edge vote onWednesday in the Greek parliament, the paper says.

Yesterday, Pasok lawmaker who previously stated hewould vote against the Greek austerity plans reportedsaying he would now support them

Christine Lagarde formally chosen to head IMF

Irish government thinks a French plan to allowGreece up to 30 years to repay some of its debts "isnot relevant to us", but analysts disagree, the IrishIndependent says. Although the Government here

disputes this, analysts say the deal needs to be closelywatched in Ireland, because it could well prove a modeldown the line for this country, the paper adds.

Foreign Exchange Strategy Wednesday, 29 June 2011

http://www.GlobalMarkets.bnpparibas.com 2

8/6/2019 Daily FX Str Europe 29 June 2011

http://slidepdf.com/reader/full/daily-fx-str-europe-29-june-2011 3/8

Ireland consumer sentiment weakened in June tolowest since February: The KBC Bank Ireland/ESRIConsumer Sentiment Index fell to 56.3 this month, from59.4 in May. In June 2010, the reading was 67.9.However, the index remains far above the all-time low of 39.6 that was recorded in July 2008, the paper notes.(Irish times)

Bank of Ireland has withdrawn a tough bondexchange offer that would have left a group of pensioners with just a fifth of the value of their original investment, the FT reports. The offer was partof a wider E 2.6bn deal on a series of junior bonds andpart of the bank's plans to raise E4.2bn in fresh capitalbefore a July 31 deadline, the paper says.

Yesterday, German preliminary Cost of Living 2.3%unchanged from May and as expected. EUHarmonized CPI unchanged at 2.4% and vs. 2.5%expected.

UK

The Government is set to claw back money frommore than a million people who unwittingly paid toolittle in tax over the past year because they were giventhe wrong tax codes, the Times says. HM Revenue &Customs revealed yesterday that 1.2 million taxpayersowed the Government an average of stg 600.

The storm engulfing retailers has put more than onein eight in "imminent danger" of closure, a leadinginsolvency practitioner said yesterday, the Times says.As a wave of store closures was announced yesterday,RSM Tenon said that about 67,000 companies were indanger of failing, the paper adds.

Switzerland/ Scandinavia

Swiss government's chief economist Aymo Brunetti sayscurrency has overshot in the recent past on safe havendemand. Says further significant appreciation would bevery problematic.

Denmark's Fjordbank Mors became the third regionalDanish lender since February to fail -- and the secondto burn senior bondholders, the Irish Independent

says. The Danish state will now step in after FjordbankMors declared that it had to close after Denmark'sregulators asked it to write down more bad loans, thepaper says. A request that the bank raise more moneybefore the end of the week forced the bank to close, thelender said.

China

The China Banking Regulatory Commission said itwarned commercial lenders about the risks of salesof high-yield wealth-management products. TheCBRC, at a meeting on June 24, urged banks to followthe rules when developing products, to control risk and to

be transparent, according to a text message sent to journalists yesterday evening. Banks sell the products toattract deposits at yields higher than the official depositrate of 3.25 percent. (Bloomberg)

Shanghai city government’s investment vehicle for property and highway construction, may not be ableto repay current loans from this month and has askedfor an extension of its repayment period, the Hong KongEconomic Journal reported today, citing unidentifiedpeople. (Bloomberg)

China Enters Shale Gas Era with Tender Offer:China’s search for natural gas passed a milestone thisweek as Beijing launched its first tender offer for four shale gas blocks in southern China to underline itsdetermination to move forward with developingunconventional gas resources. China is the world’slargest energy consumer and Beijing is increasinglylooking to natural gas to help power the country incoming decades. Shale gas, natural gas trapped in rockand extracted through a water-intensive process knownas “fracking”, is believed to be abundant in China,although it is not yet being extracted there. (FT)

The Shanghai Stock Exchange may move towardintroducing short-selling of exchange-traded fundsthis year, the China Business News reported, citing anunidentified official from the exchange’s productdevelopment department. The bourse is also consideringallowing the writing of options on ETFs, the newspaper reported, without saying where it got the information.(Bloomberg)

RECAP Europe and China: German Chancellor AngelaMerkel said at a meeting with Chinese Premier WenJiabao on Tuesday she expected trade between their twocountries to reach 200 billion euros in the next five years,f rom about 130 billion. Wen said at the beginning of the

first inter-governmental consultations between China andGermany in Berlin that he wanted trade volume betweenthe world's two biggest exporters to double over thesame period.

HP Deepens Commitment to China: HP todayannounced a series of new initiatives designed toaccelerate growth and investment in China and to deliver seamless, secure, context-aware experiences for aconnected world. (Business Wire)

Meyer Burger successfully signs new contract withGCL in China worth more than CHF 200mn (Reuters)

Japan

Data showed that the 5.7% rise m/m (5.5% expected) inMay industrial output, the second largest on recordafter +7.9% marked in March 1953, was led by arecovery in production of passenger cars and trucks aswell as higher output of general machinery. y/y down to-6.9% y/y vs. -13.6% y/y in April. METI Forecast Index:Japan June Output +5.3% M/M, July +0.5%, and METIUpgrades View: Japan Output Recovering From QuakeImpact

Japan's trade balance for the first 10 days of Juneshowed a deficit worth Y165.5 billion, compared with a

surplus of Y50.9 billion a year earlier, as exports fell1.3% y/y while imports rose 10.2%, data from theMinistry of Finance show.

Foreign Exchange Strategy Wednesday, 29 June 2011

http://www.GlobalMarkets.bnpparibas.com 3

8/6/2019 Daily FX Str Europe 29 June 2011

http://slidepdf.com/reader/full/daily-fx-str-europe-29-june-2011 4/8

Russia will call on Japan to jointly develop oil andnatural gas resources near northern islands that Japanclaims as its own, the Nikkei reports. Reserves there areequivalent to 350 million tons of oil, the report says.

Australia/ New Zealand/Canada

Australia: Internet Vacancy Index (IVI), a measure of thedemand for skills and labor in Australia, rose 0.3% inMay, with 5 of the 8 occupational groups registering anincrease. On an on-year basis, IVI rose 12% with 7 of the8 occupational groups increasing. All states, except,Tasmania registered an increase in the last 12 months.

CORP/M&A: Another iron ore project in Australia suffersfrom cost blowout, as Gildalbie Metals announces a 30%increase is construction cost estimate for its Karara IronOre project in Western Australia. The company flaggedsuch an increase in March and is now estimating totalcost at A$2.57 bln, up 30% from A$1.97 bln

Other Asia

S. Korea government will step up cooperation toprovide coordinated policy measures in its ongoinganti-inflation efforts, Yonhap news reports citing thefinance minister. "Not just the finance ministry but alsoother related ministries will join hands and come up withreasonable measures, if needed, by closely analyzingprice trends of major items that show price instability,"Finance Minister Bahk Jae-wan told an economic policycoordination meeting.

S. Korea’s export growth is likely to slow sharply inH2 due mainly to unfavorable market conditions inelectronics parts and rising competition from China,Yonhap News reports citing state-run Korea Trade-Investment Promotion Agency (KOTRA) report.

North Korea has threatened to launch "a retaliatorysacred war" against South Korea for "slandering" theNorth, as the two sides prepared to hold rare talks ontheir troubled joint tour project in the isolated country,Yonhap News reports.

Philippines Net inflow foreign portfolio investmentshave tripled. Hot money posted a net inflow of $2.2

billion as of June 10, more than thrice the $698.9 millionrecorded a year ago, latest BSP data show.

Singapore said on Tuesday it will make its bankshold higher capital levels than those set out under the new Basel III regulations, imposing some of thetoughest new banking rules unveiled so far across theglobe. With effect from 1 January 2013, Singaporebanks have to meet a minimum common equity tier-1(CET1) of 4.5% and tier 1 ratio of 6%. (Reuters)

Foreign Exchange Strategy Wednesday, 29 June 2011

http://www.GlobalMarkets.bnpparibas.com 4

8/6/2019 Daily FX Str Europe 29 June 2011

http://slidepdf.com/reader/full/daily-fx-str-europe-29-june-2011 5/8

Why We like being Short CableWe have long been Sterling bears, further convinced of our view when leading indicators for growth startedrolling over around May. And now, with Q1 GDP data –and revised Q4 data – showing a sorry current account

picture over the past 6 months, our bearish GBP stancestill holds.

We have been watching the recent uptick in UKSovereign CDS rates, which coincides with a rolling over of leading growth indicators. This suggests that thecredibility of the Government’s fiscal consolidation plan isunder threat. Recall how credit markets late last year showed their appreciation for the fiscal consolidationplan, leading to a fall in 5Y UK CDS rates and arebounding GBP. However, it seems that the plan wasbased on overly optimistic growth forecasts, in turnexplaining the turnaround in UK sovereign CDS. Whilethis in itself should be of concern for Sterling, Q1 data

released yesterday showed that the current accountdeficit failed to narrow nearly as much as thought (GBP9.4bn deficit) with a 2.5bn downward revision to the Q4deficit to -13bnt. This implies that the hole to be filled bythe financial account is even bigger than initially thought.FDI inflows (which come to under GBP 2bn on a four-quarter basis) make up only a small part of shortfall.

Chart 1 shows the sum of portfolio investment plus“other” investment in green (the two big ticket items seenfrom UK financial account data) set against GBPUSD.The recent data showed this sum rolling over further intothe deficit. Rising credit risks against the backdrop of aneven bigger current account deficit - with the financialaccount already in deficit – begs the question of where

the inflows can come from. The implication is one thatspells trouble for Sterling.The second point worth noting from the weak externalbalance data is the indirect implication for monetarypolicy, which in turn feeds into views about the futureGBP exchange rate. If one assumes that the UK’s fiscaltightening programme is kept on track, then for analready weak economy not to go into a tailspin wouldrequire overall monetary conditions to remain easy or even easier. This implies a need for one or both of thefollowing: (a) easing monetary policy by lowering bondyields further (QE); (b) encouraging a weaker GBP in thehope of improving export-led growth prospects. Inpractise, these are two sides of the same coin. With

policy rates effectively at the zero bound, a weaker GBPwould need to be the result of either lower longer termrates or higher inflation expectations – one or other of which is achievable with more QE. In this context, itshould not be surprising that we have now have moreMPC members talking about the potential need for moreQE down the road. While our economists currentlyforecast unchanged policy through 2012, having already-negative UK yields becoming even more negative willsurely hurt GBP even more.

Chart 2 shows that bond market implied inflationexpectations may have already begun to price a greater potential for UK QE relative to US QE. It compares the

US-UK 10Y bond implied inflation expectations spreadset against GBPUSD. We assume that one side-effect of extraordinary easing measures is to promote higher

Foreign Exchange Strategy Wednesday, 29 June 2011

http://www.GlobalMarkets.bnpparibas.com 5

Chart 1: Financial Account vs. GBPUSD

99 00 01 02 03 04 05 06 07 08 09 10

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

b i l l i o n s

-75

-50

-25

0

25

50

75

100

UK Financial Account

GBPUSD (RHS)

Source: Reuters Ecowin Pro. The Financial Account (sum of Portfolio Investments and other Investments) isstarting to turn south, consistent with GBP weakness.

Chart 2: Inflation expectations have in partexplained the GBPUSD post crisis

Source: Bloomberg, BNP Paribas

inflation expectations. The chart shows that GBPUSDgains in recent months have coincided with the US beingmore successful in engineering a rise in inflationexpectations. We note that this is the reverse of themechanism seen over the 2004-2006 period, when

higher inflation expectations in the UK relative to the USimplied a higher GBPUSD (via the anticipated monetarypolicy response)). This overplayed relationship reversedpost the financial crisis, and now falling US inflationexpectations forewarns of a stronger USD relative to theGBP.Strategy: Last week we recommended a short Cableposition in our medium term recommendations on abreak of 1.5930 targeting 1.5350 with a stop at 1.6285.While a EUR led USD sell off may support GBP in theweeks ahead, we remain comfortable being shortGBPUSD.

8/6/2019 Daily FX Str Europe 29 June 2011

http://slidepdf.com/reader/full/daily-fx-str-europe-29-june-2011 6/8

Daily Currency SummaryG3

EURUSD

Ahead of the vote on the Greek austerity plans currently scheduled for 2pm local time on Wednesday, the news flowfrom Athens was positive, in particular reported comments from one of the Greek Pasok party deputies that havingdeclared his intent to vote against the budget he would now support it. Euro peripheral spread narrowing on the eveof the vote indicates growing confidence that the austerity plans will pass this major hurdle Wednesday, pendingfurther debate and vote Thursday on the implementation of the Budget and which could throw up a few curved balls.Whereas Monday’s EUR run up was seen to have driven by one very lumpy flow, Wednesday’s rally was more broadbased. While this suggests that the upside relief rally on a 'Yes' vote may be muted, we still expect significant upwardprogress in the days ahead (to 1.45+) if this is indeed the outcome.

USDJPY

USDJPY didn’t fall much when Treasury yields were languishing beneath 3% at 10yrs but — co-incidentally or otherwise — popped higher alongside a return to a 3% handle on Tuesday. After USDJPY broke above initialIchimoku cloud resistance at 81.06, exporters came in to limit the topside. However, with prospect of Fed extendingcrisis lending measures (swap lines post August) USDJPY downside becomes vulnerable once again. Stronger Industrial production data (5.7% m/m vs. 5.5 expected) with METI upgrading their view on production only play to abearish USDJPY view. This goes to BoJ Governor Shirakawa’s economic judgment that “all is well” even post the

earthquake/tsunami, in turn ruling out JPY weakening QE prospects.

JPY Crosses

EURJPY is now facing significant upside risk have taken out 50-dma at 116.59 just as things start looking a little lessscary on Greek politics. Assuming things turn out well for the EUR, a EURUSD rally today along with some modestslippage in USDJPY (stronger Japan IP, Fed extending crisis lending measures) suggests that the path of leastresistance is to the topside. This is the opposite to our beginning of the week sense that EURJPY looked vulnerableto the downside.

EUR Bloc

EURGBP

Mixed comments from BoE MPC members in the past 24 hours, Posen laying into the BIS´s suggestion that the BoEneeded to move away from the zero rates environment describing it a nonsense but Paul Tucker quickly to putPosen down. Much worse than expected Q1 (and revised Q4) Current account data reminds us that a weak poundhas done more to boost prices than it has net exports but this is not going to deter the majority of the MPC from theview that a weak pound is anything other than welcome. EURGBP should rally alongside any further gains in

EURUSD, while GBPUSD is likely to head lower still in anything other than an outright USD bearish environment.Plenty of data Wednesday but none of it top draw — Services PMI on Friday is important.

EURCHF

Some signs of EURCHF finding a base but the downtrend channel is till very much in place. The cross moves upform here on a Greek ´yes´ vote, and (very) sharply lower on a ´No´. No follow-through Tuesday to the reportssuggesting left-leaning Swiss parliamentarians were pressing fro the SNB to re-peg the CHF to the EUR. In additionto the obvious impact on the CHF safe haven bid from the Greek vote, Wednesday´s KoF index is going to beimportant as a fresh read on how the economy is coping with latest CHF strength.

EURNOK

The NOKSEK dip yesterday proved limited and spot is looking bid having carved out a fresh 10-month high at1.1882. Was interesting to see Norway Trade Minister come out against NOK bulls and noting that the "NOK is notthe CHF" as a safe haven in the face of Greek sorrows as much of Norway´s exports go to Europe. However, it iscertainly a better haven relative to the SEK- which is also exposed to the global IP cycle. Expect NOKSEK tocontinue to remain bid even as EURNOK remains stuck in an effective 7.75-7.90 range.

EURSEK

EURSEK has broken higher to a fresh 7-month high above 9.2400. The SEK is not only underperforming the EUR,but also the USD with USDSEK still well bid above 6.40 even though persistently dogged of late by 200-dma at6.5240. Much weaker retail sales in May (-1.1% y/y vs. +2.0% tipped, 5.6% y/y in April) may have played a part, inaddition to the fact that the SEK is one of the most exposed (small open economy) to a global IP slowdown. A softer US ISM as European PMI´s are rolling down won’t help either.

USD Bloc

USDCAD

USDCAD testing but not convincingly breaking its 200dma on Monday and falling back deeper into the 0.97-0.99range on Tuesday. Stronger oil and improved risk sentiment evident in global equity markets is an irresistiblecombination for CAD and repels risk of a test of parity on USDCAD from below. But if CPI on Wednesday iscomforting as expected (fall in annual rate from April's 1.6%) we would look for some renewed underperformance byCAD on various crosses.

AUDUSD

Some excitement at the break below 1.0410 AUDUSD Monday but the pair has since recovered its poise. AUDUSDis still within a channel down trend and we need to break above about 1.06 to get more bullish here. Suffice to say aGreek ´yes´ vote that improve risk sentiment generally may do just that. AUD specific event risk comes form the

official China PMI due on Thursday. If this has at least a 51 handle and given signs China may be preparing toloosen the monetary breaks to support growth, AUD could start going better.

NZDUSDNBNZ business survey first think Thursday morning next domestic focus and in the meantime AUDNZD likely toremain volatile but within a 1.2950-1.3050 range.

Foreign Exchange Strategy Wednesday, 29 June 2011

http://www.GlobalMarkets.bnpparibas.com 6

8/6/2019 Daily FX Str Europe 29 June 2011

http://slidepdf.com/reader/full/daily-fx-str-europe-29-june-2011 7/8

FX Forecasts*USD Bloc Q2 '11 Q3 '11 Q4 '11 Q1 '12 Q2 '12 Q3 '12 Q4 '12 Q1 '13 Q2 '13 Q3 '13 Q4 '13

EUR/USD 1.45 1.50 1.55 1.45 1.40 1.35 1.35 1.30 1.30 1.30 1.30

USD/JPY 80 78 83 85 90 95 95 95 95 95 95

USD/CHF 0.84 0.83 0.83 0.90 0.93 1.00 1.00 1.04 1.04 1.04 1.04

GBP/USD 1.63 1.65 1.68 1.59 1.56 1.53 1.53 1.53 1.53 1.53 1.53

USD/CAD 0.97 0.98 0.93 0.95 0.97 1.01 1.01 1.04 1.04 1.04 1.04

AUD/USD 1.07 1.09 1.13 1.07 1.04 0.99 0.99 0.96 0.96 0.96 0.96

NZD/USD 0.84 0.82 0.84 0.81 0.80 0.76 0.76 0.74 0.74 0.74 0.74

USD/SEK 6.28 5.93 5.48 5.93 6.21 6.67 6.67 6.92 6.92 6.92 6.92

USD/NOK 5.36 4.98 4.77 5.07 5.26 5.56 5.56 5.77 5.77 5.77 5.77

EUR Bloc Q2 '11 Q3 '11 Q4 '11 Q1 '12 Q2 '12 Q3 '12 Q4 '12 Q1 '13 Q2 '13 Q3 '13 Q4 '13

EUR/JPY 116 117 129 123 126 128 128 124 124 124 124

EUR/GBP 0.89 0.91 0.92 0.91 0.90 0.88 0.88 0.85 0.85 0.85 0.85

EUR/CHF 1.22 1.25 1.28 1.30 1.30 1.35 1.35 1.35 1.35 1.35 1.35

EUR/SEK 9.10 8.90 8.50 8.60 8.70 9.00 9.00 9.00 9.00 9.00 9.00EUR/NOK 7.77 7.47 7.40 7.35 7.37 7.50 7.50 7.50 7.50 7.50 7.50

EUR/DKK 7.46 7.46 7.46 7.46 7.46 7.46 7.46 7.46 7.46 7.46 7.46

Central Europe Q2 '11 Q3 '11 Q4 '11 Q1 '12 Q2 '12 Q3 '12 Q4 '12 Q1 '13 Q2 '13 Q3 '13 Q4 '13

USD/PLN 2.72 2.60 2.48 2.69 2.75 2.81 2.78 2.85 2.77 2.85 2.85

EUR/CZK 24.5 24.3 24.5 24.1 23.9 23.8 23.5 23.7 24.0 23.5 23.3

EUR/HUF 280 275 275 269 265 265 260 260 255 260 260

USD/ZAR 6.90 6.80 6.60 6.55 6.60 6.50 6.50 7.20 7.10 7.00 6.90

USD/TRY 1.59 1.52 1.50 1.56 1.59 1.63 1.65 1.65 1.67 1.69 1.69

EUR/RON 4.25 4.20 4.15 4.20 4.25 4.15 4.10 4.20 4.20 4.10 3.95

USD/RUB 27.86 27.51 27.25 27.86 27.97 28.08 27.65 28.19 27.75 29.07 27.75

EUR/PLN 3.95 3.90 3.85 3.90 3.85 3.80 3.75 3.70 3.60 3.70 3.70

USD/UAH 7.9 7.8 7.8 7.5 7.5 7.5 7.5 7.5 7.5 7.5 7.3

EUR/RSD 102 100 100 98 97 96 95 93 92 91 90

Asia Bloc Q2 '11 Q3 '11 Q4 '11 Q1 '12 Q2 '12 Q3 '12 Q4 '12 Q1 '13 Q2 '13 Q3 '13 Q4 '13

USD/SGD 1.23 1.22 1.21 1.21 1.20 1.19 1.18 1.17 1.16 1.15 1.14

USD/MYR 3.00 2.95 2.90 2.87 2.85 2.83 2.80 2.77 2.75 2.73 2.70

USD/IDR 8600 8500 8400 8300 8200 8100 8000 7900 7800 7800 7800

USD/THB 30.00 29.80 29.50 29.30 29.00 28.70 28.50 28.30 28.00 28.00 28.00

USD/PHP 43.00 42.50 42.00 41.50 41.00 40.50 40.00 39.50 39.00 39.00 39.00

USD/HKD 7.80 7.80 7.80 7.80 7.80 7.80 7.80 7.80 7.80 7.80 7.80

USD/RMB 6.47 6.40 6.31 6.25 6.21 6.17 6.13 6.23 6.20 6.17 6.15

USD/TWD 28.50 28.00 27.50 27.00 26.70 26.50 26.00 26.00 26.00 26.00 26.00

USD/KRW 1070 1060 1050 1040 1030 1020 1010 1000 1000 1000 1000

USD/INR 45.00 45.50 45.00 44.50 44.00 43.50 43.00 43.00 42.50 42.50 42.00

USD/VND 20500 20500 20000 20000 20000 20000 20000 20000 20000 20000 20000

LATAM Bloc Q2 '11 Q3 '11 Q4 '11 Q1 '12 Q2 '12 Q3 '12 Q4 '12 Q1 '13 Q2 '13 Q3 '13 Q4 '13

USD/ARS 4.10 4.18 4.25 4.34 4.43 4.51 4.60 4.69 4.78 4.86 4.95

USD/BRL 1.60 1.58 1.55 1.53 1.55 1.56 1.58 1.59 1.60 1.61 1.62

USD/CLP 465 450 435 425 430 435 440 442 445 447 450

USD/MXN 11.70 11.40 11.10 11.00 10.90 11.00 11.10 11.10 11.17 11.25 11.30

USD/COP 1770 1730 1690 1690 1700 1710 1720 1725 1730 1740 1750

USD/VEF 4.29 4.29 4.29 4.29 4.29 4.29 4.29 8.80 8.80 8.80 8.80

USD/PEN 2.75 2.70 2.65 2.63 2.63 2.64 2.66 2.67 2.68 2.69 2.70

Others Q2 '11 Q3 '11 Q4 '11 Q1 '12 Q2 '12 Q3 '12 Q4 '12 Q1 '13 Q2 '13 Q3 '13 Q4 '13

USD Index 74.21 72.30 70.76 74.87 77.62 80.72 80.72 82.99 82.99 82.99 82.99

*End Quarter

Foreign Exchange Strategy Wednesday, 29 June 2011

http://www.GlobalMarkets.bnpparibas.com 7

8/6/2019 Daily FX Str Europe 29 June 2011

http://slidepdf.com/reader/full/daily-fx-str-europe-29-june-2011 8/8

FX - Global Strategy Contacts

Foreign Exchange

Ray Attrill Senior Currency Strategist New York 1 212 841 2492 [email protected] Hellawell Quantitative Strategist London 44 20 7595 8485 [email protected] Kowshik Currency Strategist London 44 20 7595 1495 [email protected] Nicola Currency Strategist New York 1 212 841 2492 [email protected]

Emerging Markets FX & IR StrategyDrew Brick Head of FX & IR Strategy Asia Singapore 65 6210 3262 [email protected] Loo Thio FX & IR Asia Strategist Singapore 65 6210 3263 [email protected] Ryan FX & IR Asia Strategist Singapore 65 6210 3314 [email protected] Poh FX & IR Asia Strategist Singapore 65 6210 3418 [email protected] Qi FX & IR Asia Strategist Shanghai 86 21 2896 2876 [email protected] Pawlowski Head of FX & IR Strategy CEEMEA London 44 20 7595 8195 [email protected] Donadio FX & IR Latin America Strategist São Paulo 55 11 3841 3421 diego.donadio@@br.bnpparibas.com

Production and Distribution, please contact :

Roshan Kholil, Foreign Exchange, London. Tel: 44 20 7595 8486, Email: [email protected]

Important DisclosuresThis report has been written by our strategy teams. Such reports do not purport to be an exhaustive analysis and may be subject to conflicts of interest resultingfrom their interaction with sales and trading which could affect the objectivity of this report. (Please see further important disclosures in the text of this report).This report is a marketing communication. It is not independent investment research. It has not been prepared in accordance with legal requirements designedto provide the independence of investment research, and is not subject to any prohibition on dealing ahead of the dissemination of investment research. Theinformation and opinions contained in this report have been obtained from, or are based on, public sources believed to be reliable, but no representation or warranty, express or implied, is made that such information is accurate, complete or up to date and it should not be relied upon as such. This report does notconstitute a prospectus or other offering document or an offer or solicitation to buy or sell any securities or other investment. Information and opinions containedin the report are published for the assistance of recipients, but are not to be relied upon as authoritative or taken in substitution for the exercise of judgement byany recipient, are subject to change without notice and not intended to provide the sole basis of any evaluation of the instruments discussed herein. Anyreference to past performance should not be taken as an indication of future performance. To the fullest extent permitted by law, no BNP Paribas groupcompany accepts any liability whatsoever (including in negligence) for any direct or consequential loss arising from any use of or reliance on material containedin this report. All estimates and opinions included in this report are made as of the date of this report. Unless otherwise indicated in this report there is nointention to update this report. BNP Paribas SA and its affiliates (collectively “BNP Paribas”) may make a market in, or may, as principal or agent, buy or sellsecurities of the issuers mentioned in this report or derivatives thereon. BNP Paribas may have a financial interest in the issuers mentioned in this report,including a long or short position in their securities and/or options, futures or other derivative instruments based thereon, or vice versa. BNP Paribas, includingits officers and employees may serve or have served as an officer, director or in an advisory capacity for any issuer mentioned in this report. BNP Paribas may,

from time to time, solicit, perform or have performed investment banking, underwriting or other services (including acting as adviser, manager, underwriter or lender) within the last 12 months for any issuer referred to in this report. BNP Paribas may be a party to any agreement with the issuer relating to theproduction of this report. BNP Paribas, may to the extent permitted by law, have acted upon or used the information contained herein, or the research or analysis on which it was based, before its publication. BNP Paribas may receive or intend to seek compensation for investment banking services in the nextthree months from or in relation to an issuer mentioned in this report. Any issuer mentioned in this report may have been provided with sections of this reportprior to its publication in order to verify its factual accuracy.BNP Paribas is incorporated in France with limited liability. Registered Office 16 Boulevard des Italiens, 75009 Paris. This report was produced by a BNPParibas group company. This report is for the use of intended recipients and may not be reproduced (in whole or in part) or delivered or transmitted to any other person without the prior written consent of BNP Paribas. By accepting this document you agree to be bound by the foregoing limitations.

Certain countries within the European Economic AreaThis report is solely prepared for professional clients. It is not intended for retail clients and should not be passed on to any such persons. This report has beenapproved for publication in the United Kingdom by BNP Paribas London Branch, a branch of BNP Paribas, 10 Harewood Avenue, London NW1 6AA, which isregulated by the Financial Services Authority for the conduct of its investment business in the United Kingdom and registered in England & Wales under No.FC13447. This report has been approved for publication in France by BNP Paribas, a credit institution licensed as an investment services provider by theCECEI and the AMF, whose head office is 16, Boulevard des Italiens 75009 Paris, France.This report is being distributed in Germany either by BNP Paribas London Branch, or by BNP Paribas Niederlassung Frankfurt am Main, regulated by theBundesanstalt für Finanzdienstleistungsaufsicht (BaFin).United States: This report is being distributed to US persons by BNP Paribas Securities Corp., or by a subsidiary or affiliate of BNP Paribas that is not registered

as a US broker-dealer to US major institutional investors only. BNP Paribas Securities Corp., a subsidiary of BNP Paribas, is a broker-dealer registered with theSecurities and Exchange Commission and a member of the National Association of Securities Dealers, the New York Stock Exchange and other principalexchanges. BNP Paribas Securities Corp. accepts responsibility for the content of a report prepared by another non-US affiliate only when distributed to USpersons by BNP Paribas Securities Corp.Japan: This report is being distributed to Japanese based firms by BNP Paribas Securities (Japan) Limited, Tokyo Branch, or by a subsidiary or affiliate of BNPParibas not registered as a financial instruments firm in Japan, to certain financial institutions defined by article 17-3, item 1 of the Financial Instruments andExchange Law Enforcement Order. BNP Paribas Securities (Japan) Limited, Tokyo Branch, a subsidiary of BNP Paribas, is a financial instruments firmregistered according to the Financial Instruments and Exchange Law of Japan and a member of the Japan Securities Dealers Association. BNP ParibasSecurities (Japan) Limited, Tokyo Branch accepts responsibility for the content of a report prepared by another non-Japan affiliate only when distributed toJapanese based firms by BNP Paribas Securities (Japan) Limited, Tokyo Branch. Some of the foreign securities stated on this report are not disclosedaccording to the Financial Instruments and Exchange Law of Japan.Hong Kong: This report is being distributed in Hong Kong by BNP Paribas Hong Kong Branch, a branch of BNP Paribas whose head office is in Paris, France.BNP Paribas Hong Kong Branch is regulated as a Registered Institution by Hong Kong Monetary Authority for the conduct of Advising on Securities [RegulatedActivity Type 4] under the Securities and Futures Ordinance.

© BNP Paribas (2011). All rights reserved.

Foreign Exchange Strategy Wednesday, 29 June 2011

http://www.GlobalMarkets.bnpparibas.com 8