crowding out and its critics - federal reserve bank … · crowding out and its crities* keith nj....

TRANSCRIPT

Crowding Out and Its Crities*KEITH NJ. CARLSON and ROGER W. SPENCER

OES Government spending displace a near equalamount of private spending? This notion, popularlyknown as the “crowding- out” effect of Governmentexpenditures, has recently gained wide-spread at-tention at two levels. Fii-st, at the policy level, publicofficials have expressed concern, that massive currentand projected Federal deficits will have a deleteriouseffect on private capital expenditures for some timeto come. Second, at the academic level, “crowdingout” is at least one of the issues which helps to dis-tinguish between followers of the t\vo major macro-economic schools of thought Keynesians andmonetarists.

This article focuses on “crowding out” from moreof an academic than a practical policy point of view.Policy implications can he drawn from this discus-sion, but, for the most part, the abstract economicmodels used in academic circles are not easily adapt-able to observable phenomena. Yet the origins of therecent crowding— out controversy at the academiclevel are traceable to certain empirical results basedon U.S. experience.

New research has been conducted in this area andsome old arguments have been revived.1 Many ofthe developments in the crowding-out controversy

°The authors acknowledge the helpful comments of JamesBarth, William Dewald, Dean Dutton, Thomas l-lavrilesky,Robert Rasehe, Paul Smith, Frank Steindi, and William Yohe,none of whom should be held responsible for remainingerrors.

I For a survey that includes a discussion of the views of theclassical economists on crowdmg out, Sec Roger \V. Spenceraad William P. Yohe, “The ‘Crowding Out’ of Private Ex-penditures by Fiscal Policy Actions,” this Review (October1970), pp. i2-24.

can be described in the context of the standardIS-LM analytic framework, In this framework, whichis the cornerstone of most macroeconomics coursestaught throughout the western world, the IS curverepresents the locus of points (pairs of interest ratesand real income) in \vhich the real sector of theeconomy is in equilibrium, and the LM curve repre-sents a similar locus of points for which the demandfor money equals the supply. The IS-Ui apparatushas distinct limitations, hut because of its widespreaduse as a pedagogical device, it serves a useful func-tion in highlighting the issues in the crowding-outcontroversy.2

The subject of crowding out is approached by firstinvestigating a number of separate “cases” which pro-vide various explanations of how crowding out mightoccur. Next, the role of stability considerations in thecontroversy is assessed. Finally, several econometricmodels~~treexamined to determine what empiricalimplications they have for the crowding-out issue.

To set the stage for the discussion, two mattersof a preliminary nature are taken up in this section.First, crowding out is defined for the purposes athand. Much of the recent discussion of crowding outhas been confusing simply because the term has notbeen carefully defined. Second, since the controversy

2For discussion of the limitations of the IS-LM framework,see Karl Brunner and Allan II. \ leltzer, “Monetanism ‘liePri ci pal Iss ties Areas of Agreei ient a 11(1 tllv Work Remain—aig.’’ \Jo tie tOitsoi, ed . 3 eroilie L, Stein, ( Ainsterdam NorthHollaiirl Publishing Co., forthcoming), and ‘Mr. Hicks andthe Monetarists, Ecoao,aica (Febmary 1973), pp. 44-59.

Page 2

FEDERAL RESERVE BANK OF ST. LOUIS DECEMBER 1975

has moved through several stages in recent years andhas oftentimes involved complex and subtle argu-ments, an overview is provided as a guide to thereader,

Crowding out generally refers to the economic ef-fects of expansionary fiscal actions. If an increase inGovernment demand, financed by either taxes ordebt issuance to the public, fails to stimulate totaleconomic activity, the private sector is said to havebeen ‘crowded out” by the Government action. Thepresumption of a constant money supply insures thatthe policy action accompanying the increase in Gov-ernment demand is fiscal and not monetary.

The analysis may be conducted in either real ornominal terms. The crowding-out hypothesis main-tains that if prices are held constant, as in typicalIS-LM fashion, an increase in real Government de-mand financed by real taxes or debt has no lastingeffect on real income. Alternatively, crowding outimplies that an increase in Government spending,given flexible prices and a constant money supply,has no lasting effect on nominal income. In otherwords, the steady state Government spending multi-plier, under the ahove conditions, is approximatelyzero.3

By approximately zero, we mean that increasedGovernment demand may crowd out exactly thesame amount of private demand, slightly less, orslightly more. There is complete crowding out if $1of Government demand displaces $1 of private de-mand, partial crowding out if $1 of Governmentdemand displaces less than $1 of private demand,and over crowding out if $1 of Government demanddisplaces more than $1 of private demand. The in-creased Government demand may increase aggregatedemand temporarily, permanently, or not at all, aswill be explained below.

The origins of the recent controversy are traceableprimarily to the empirical results published by Ander-sen and Jordan in 1968 and supporting studies byKeran in 1969 and 1970.~ These results indicated

3These definitional issues are explored in more tletail in theappendix.

~Leonall C. Andersen and Jerry L. Jordan, “Monetary andFiscal Actions: A Test of Their Relative Importance inEconomic Stabilization,” this Review (November 1968), pp.11-24; Michael W. Keran, “Monetary and Fiscal Influences

that nominal crowding out occurs; that is, a changein Federal spending financed by either horrowing ortaxes has only a negligible effect on GNP over aperiod of about a year, These studies did not suggestthat expansionary fiscal actions have no effect, butshowed instead that the initial effect, which is posi-tive, is followed in later quarters by an approximatelyoff-setting negative effect.

The response to these empirical results took placeat two levels — statistical and theoretical. At thestatistical level, the validity of the results was ques-tioned. Were proper statistical procedures followedin their derivation?5 On the theoretical level the ques-tion was whether or not the results were consistentwith what seemed to be the accumulated evidenceon certain theoretical propositions.°

Although all the returns regarding the validity ofthe Andersen-Jordan empirical procedures are notyet in, this article focuses on the theoretical argu-ments that have since evolved. The first theoreticalargument offered in response to the crowding outconcept was an alleged inconsistency between suchresults and the prevailing estimates of the interestelasticity of the demand for money.7 The criticscharged, on the basis of the IS-LM framework, thatin order for crowding out to occur, the proponentsof these results must be assuming that the demandfor money is nearly perfectly interest-inelastic, Thisallegation meant acceptance of the proposition thatthe LM curve is essentially vertical. According to thecritics, most empirical estimates do not support a zerointerest elasticity of money demand.

In answer to this charge of inconsistency, MiltonFriedman and others argued that the slope of theLM curve was largely irrelevant to the crowding out

on Economic Activity — The Historical Evidence,” this Re-view (November 1969), pp. 5-24, and “Monetary and FiscalJillluerices on Economic Activity: The Foreign Experience,”this Review (February 1970), pp. 16-28.

5See E. Gerald Corrigan, “The Measurement arid importanceof Fiscal Policy Changes,” Federal Reserve Bank of NewYork Monthly Rev-Jew (June 1970), pp. 133-45; Richard C.Davis, “How Much Does Money Matter? A Look at SomeRecent Evidence,” Federal Reserve Bank of New YorkMonthly Review (June 1969), pp. 111-31; and Edward M.(;raimi]ieh, “The Usefulness of Monetary and Fiscal Policyas Discretionary Stabilization Tools,” Journal of Money,Credit and Banking (May 1971), pp. 506-32.

6James Tobio, “Friedman’s Theoretical Framework,” Journalof Political Economy (September/October 1972), pp. 852-63;Warren L. Smith, “A Neo~KeynesianView of Monetary Pol-icy,” l”ederal Reserve Bank of Boston, Controlling MonetaryAggregates (June 1969), pp. 105-26; and Ronald L. Teigen,“A Critical Look at Monetarist Econonucs,” this Review(January 1972), pp. 10-25.Tobiii, “Friedman’s Theoretical Framework.”

Page 3

FEDERAL RESERVE DANK OF ST. LOUIS DECEMBER 1975

discussion.5 In particular, Friedman pointed out thenecessity of distinguishing between initial and subse-quent effects of fiscal actions. According to Friedman,an “expansionary” fiscal action might first be reflectedin a rise in output, but the financing of the deficitwould set in motion contractionary forces whichcould eventually offset the initial stimulative effectY

In response to the Friedman explanation, the crit-ics developed still another argument, again pointingout an alleged inconsistency. This time the criticsattempted to demonstrate that the Friedman argu-ment, which stemmed from explicit consideration ofthe Government’s financing requirements, is not con-sistent with generally accepted assumptions concern-ing stability of the economic system (as representedby the IS-LM apparatus).1° In particular, a debt-financed increase in Government spending in a worldwhere crowding out occurs does not set in motion aset of forces that will drive the IS-LM model to anew equilibrium once it is disturbed from an initialequilibrium.

All of these arguments are reviewed in some detailin this article, Several alternative explanations areoffered as to how crowding out might occur regard-less of the slope of the LM curve. A number ofshortcomings of the recently advanced argumentsbased on stability analysis arc discussed. Finally,returning to the empirical level, the results of somewell-known econometric models are examined to seewhat light they shed on the crowding-out controversy.

Until recently, it was suggested by a number ofanalysts that contemporary monetarists view the

8Milton Friedman, “Comments on the Critics,” Journal ofPolitical Economy (September/October 1972), pp. 906-50;and Karl Brunner and Allan H. Meltzer, “Money, Debt, andEconomic Activity,” Journal of Political Economy (Septem-ber/October 1972), pp. 951-77.

°For further discussion of the role of the Government financ-ing constraint, see Spencer and Yohe, “The ‘Crowding Out’of Private Expenditures;” Cad F. Christ, “A Short-Run Ag-gregate-Demand Model of the Interdependence and Effectsof Monetary and Fiscal Policies with Keynesian and ClassicalInterest Elasticities,” The American Economic Review (May1967), pp. 434-43, and “A Simple Macroeconomic Modelwith a Government Budget Restraint,” Journal of Politi-cal Economy (January/February 1968), pp. 53-67; and Wil-liam L. Sitber, “Fiscal Policy in JS-LM Analysis: A Correc-tion,” Journal of Money, Credit and Banking (November1970), pp. 461-72.

iOAlan S. Blinder and Robert M. Solow, “Does Fiscal PolicyMatter?” Journal of Public Economics (November 1973),pp. 319-37; and James Tobin and Willem Buiter, “Long

vertical LM curve as a requirement for the existenceof crowding out. James Tobin, for example, observedthat a vertical LM curve leads to the “characteristicmonetarist” proposition that “a shift of the IS locus,whether due to fiscal policy or to exogenous changein consumption and investment behavior, cannot alter~“,h1 William Branson, in his popular macroeconomicstextbook, noted that

The monetarist position is that the interest elastici-ties of the demand for and supply of money arezero, so that the LM curve is vertical, In this casefiscal policy changes the composition, but not thelevel of national output, while monetary policy, shift-ing a vertical LM curve, can change the level ofoutput. 12

Similar statements can be found in other texts.

This classical case of crowding out is examined insome detail because of its presumed importance inthe crowding-out discussion. Following discussion ofthis classical case, several alternative explanationsare offered as to how crowding out can occur in theIS-LM framework, even if the interest elasticity ofmoney demand is not zero.

In order for Government spending to stimulateeconomic activity, it must either foster increases inthe money stock (however defined) or increases inthe rate at which the existing money stock turns over.Because the former possibility does not involve netdebt purchases by the private sector or increases intaxes, there is no reason to think that private spend-ing would be crowded out. However, if the moneystock does not increase, Government spending mustbe financed by debt issuance or increased tax rev-enue, either of which could result in a reduction inprivate spending. If private spending is not curbedby such actions, total spending rises, which impliesa rise in velocity — the rate at which the money stockturns over.

Run Effects of Fiscal and Monetary Policy en AggregateDemand,” Cowles Foundation Discussion Paper No. 384(December 13, 1974).

IlTobin, “Friedman’s Theoretical Framework,” p, 853.

IOV/illiam H. Branson, Macroeconomic Thcory and Policy(New York: Harper & Row, Publishers, 1972), p. 281. It isof interest to note that Tobbi labels the case in which onlymonetary policy can affect income as characteristically mon-etarist arid the situation in which both monetary and fiscalpolicies can alter income as characteristically oeo-Keynesian.l3ranson symmetrically views the vertical LM case as“extreme” monetarist, and the vertical IS case as “extrememien—Keynesian (or “fiscalist” ).

Page 4

FEDERAL RESERVE BANK OF ST. LOUIS DECEMBER 1975

The LM curve is vertical (drawn for a given pricelevel, P,) in the classical case, reflecting a zero inter-est elasticity of the demand for (and supply of)money. Thus, an increase in Government spendingwhich shifts the IS curve to the right can only in-crease the interest rate, but does not stimulate veloc-ity. Consequently, aggregate demand, as shown inthe bottom half of Figure 1, does not shfft.ia One ormore components of private spending are crowdedout by an amount equal to the amount of the Govern-ment spending increase, As a result, with aggregatedemand failing to shift in response to the increasein Government spending, crowding out occnrs in bothreal and nominal terms.

JohnMaynard Keynes in 1936 provided the thrust for theproposition that Government spending does not crowdout private spending in his landmark book, The Gen-eral Theory of Employment, Interest and Money.14

It is ironic that certain passages in that book providestrong support for the opposite contention.

Keynes, throughout his General Theory, was muchconcerned with expectations and confidence. He didnot overlook the possibility, even in those times ofrelatively small budget deficits, that Government

l3Althomigh shown as a straight line, the true spirit of theclassical ease would be better preserved if aggregate de-mand were drawn as a rectangular hyperbola.

-iJulso Maynard Keynes, The General Theory of Employ—macnt, Interest and Money (New York: Hareourt, Brace andCompany, 1936), pp. 119-20.

Figure 1

Classical Case

xo

spending could adversely affect the confidence of theprivate sector in its economic future.

With the confused psychology which often prevails,the Government programme may, through its effecton ‘confidence’, increase liquidity-preference or di-minish the marginal efficiency of capital, which,again, may retard other investment unless measuresare taken to offset it.

15

An induced increase in liquidity preference, subse-quent to an increase in Government spending fromC to C1, is depicted in the IS-LM franiework (seeFigure 2) by a leftward shift of the LM curve, and adiminished marginal efficiency of investment scheduleis reflected by the subsequent backward shift of the

iSIbid., p. 120. For an algebraic analysis that takes into ac-count some of the relevant aspects of this Keynes case, seeRichard J. Cebula, “Deficit Spending, Expectations, andFiscal Policy Effectiveness,” Public Finance (3-4/1973), pp.362-70.

It is an axiom of classical economics that velocityis virtually constant and cannot be increased byGovernment actions. In particular, the rise in interestrates, which is associated with the issuance of Gov-ernment debt, does not induce the private sector toattempt to hold less money balances because thedemand for money is not sensitive to interest ratechanges. This idea can be illustrated graphicallywith the Hicksian IS-LM apparatus in Figure 1.

r

-IS (Gi)

p

Five cases are presented which represent eco-nomic situations conducive to Government displace-ment of private spending without the requirement ofa vertical LM curve. The architects of these frame-works range from such disparate figures as the Chi-cago economists, Frank Knight and Milton Friedman,to John Maynard Keynes.

AD

x

Page ~

FEDERAL RESERVE BANK OF ST. LOUIS DECEMBER 1975

r

P0

Figure 2

Keynes Case

xo

(G0)

IS (G1)IS (G0)

AD

x

x

IS curve to the position denoted as IS(G1), If theseshifts in the IS and LM curves result in 110 changein aggregate demand at the given price level P0, bothnominal and real crowding out will occur. Flowever,the actual shift in aggregate demand could be posi-tive, negative, or negligible, depending on the rela-tive shifts of the IS and LM curves.

A number of analysts have recently invoked theKeynes case to explain the sluggishness of capitalexpenditures in recent years. They, however, are notthe first since Keynes to attribute lackluster invest-mnent plans to stepped-up Government spending. Dc-scribing a situation with some similarities to thepresent, Daniel Throop Smnith observed (in 1939)that:

Page 6

A continued experience with deficits which do notproduce sustained recovery, as in this country, or arecent inflation and collapse, as in continental Eu-ropean countries, is likely to make a deficit a matterfor concern and anxiety. And, if there is disbelief inthe benefits of a deficit, then the new money spentby the government may well be more timan offset byadditional withdrawals of private money whichwould otherwise be spent. Likewise, if consumer in-comes do increase immediately as a result of the def-icit, business may anticipate that the increase is tem-porary and refrain from long-term commitments.t°

iPtr he-/’hi ( rn-,e: -~ Ij’-1’-tz~’teei /~(tic-,-,. TMscase is constructed on the basis of the writings ofFrank Knight,” The analysis does not do justice tothe complex theories of Knight, but is offered as beingroughly consistent with the spirit of his theory ofcapital and interest.18 Though Knight certainly didnot conduct his analysis within an IS-LM framework,an attempt is made to translate his ideas into suchterms.

According to Knight, we should expect no dimin-ishing returns from investment. One reason for anearly perfectly interest-elastic investment functionis that the quantity of capital is so large relative tothe additions to it that these additions should not beexpected to have much of an effect on the yield ofcapital.’9 Another reason, according to Knight, is

tm6Daniel Throop Smith, “Is Deficit Spending Practical?” lIar-

yard Business Reciew (Autumn 1939), p. 38.

“No attemnpt is made to cite all of Knight’s articles on in-terest and capital, but a sunimnary is contained in Frank H.Knight, “Capital and Interest,” in Readings in the Theoryof Income Distribution, The American Economnie Association(Philadelphia: The Blakiston Company, 1949), pp. 384-417. The Knight case was suggested to the authors by \Vil-ham Dewald of Ohio State University, hut he is absolvedof any responsibility for the particular analysis here.

‘~Thedifficulty of interpreting Knight’s writing is illustratedby Friedrich A. Lutz, The Theory of Interest (Chicago:Aldine Publishing Co., 1968), p. 104, where he intro-(luces his chapter on Knight as follows:

It is msot easy to give amm exposition of Kniglmt’s theoryof capital and interest. Over a numnber of years Knightdevoted misany papers to the subject; and, as ammyommewho ever attempted to wom-k his ‘vay through Knight’stheory knoivs. these writings have passages which arevery difficult to understammcl and also, either apparently’or really, cosmtradictory.

I °For a discussion of the relationship between stocks andflows in the market for capital goods, see James C. Witte,Jr., ‘‘The Microfoundations of the Social Investment Func-tion,” The Journal of Politico! Economy (October 1963),pp. 441-56.

To add to the confimsiomm relating to the interpretation ofKmught’s writings, it should he msoted tlmat Knight (lid notaccept the three—part division of resources into land, laborand capital. His interpretation, rather, was that anyone wholbs control over productive capacity will employ any’ or allsources in such a way as to mimaximiz.e the return for theiruse. For ami amialysis that preserves this broad interpretationof capital, see Milton Friedmamm, P-rice Theory: A ProcisionalTest (Chicago: Aldine Publishing Company, 1962), pp.244-63.

IM (G1)

P

FEDERAL RESERVE DANK OF ST. LOUIS DECEMBER 1975

that investment carries with it an investment inknowledge, including research and development. Asa result, a declining marginal product of capital isapproximately offset by technological advances sothat an aggregate investment curve is drawn as nearlyhorizontal with respect to the yield on capital.

When translated into an IS-LM frame of reference,the Knight ease introduces an interesting element tothe crowding-out controversy. A perfectly fiat IScurve (see Figure 3) means that fiscal actions areincapable of shifting the IS curve. An increase inGovernment spending, for example, absorbs savingand reduces the amount available for private invest-ment (any increase in Government spending showsup as a one-for-one displacement of private invest-ment). Combining the fiat IS curve with the LMcurve provides a case where monetary policy domin-ates the determination of output. Fiscal actionshave no effect on either output or the interest rate.2°It is of interest to note that monetary policy has noeffect on the interest rate either, an implicationwhich runs counter to some statements by Knight.2’But because fiscal actions do not shift aggregate de-mand for this so-called Knight case, the implicationis that both nominal and real crowding out occur.22

----Recently, Professors Paul David and John Scad-ding developed some arguments for crowding out thatare derived from an assumption of ultrarationality onthe part of households,23 The notion of ultraration-ality is based on the assumption that households re-gard the corporate and Government sectors as exten-sions of themselves — as instruments of their privateinterests. This fundamental behavorial assumption isofiered as an explanation for Denison’s Law — the

201t is surprising that this case has not received mnore atten-tion in the literature, because it is every bit as mnonetaristas tIme vertical LM ease. For an example of one writer wlmodoes mnention this case, see Martin Bronfenbrenner, IncomeDistribution Theory (Chicago: Aldine-Atherton, 1971), pp,339-40. However, Bronfemibrenner dismisses it as a long-m-uncase with little short—run significance.

2tSee Knight, “Capital and Interest,” p. 406.

~‘Though the Knight case has msot Iseen empirically tested, ithas implicatiomis which are consistemmt with the results ot anmnber of empirical studies. ‘The Andersen—lordan resultsrelating ehammges in CNP to -mnonetary and fiscal actions areconsistent with such a ease. The inability to find a stablerelationship between interest rates and various measures offiscal action is also consistemst. And finally, the stability ofreal interest rates over time — at least to the extent realrates have been nmeasured — provides indirect evidence insupport of the Knight model.

2tPaul A. David and John L. Seadding, “Private Savings:Ultrarationahity, Aggregation, amsd ‘Dcnisou’s Law,’ ‘‘ Journalof Political Economy (March/April 1974), pp. 225-49.

p0

Figure 3

Knight Case

AD

x0 x

observed stability of the ratio of gross private savingto GNP in tile United States.2’m

The David-Scadding article is of relevance to thecrowding-out controversy because of its fiscal policyimplications. The assumption of ultrarationality im-plies displacement effects of Government spendingwhich the authors call “cx ante crowding out.” Theyargue that stability of the gross private saving ratio

2~EdwardF. Denison, “A Note on Private Saving,” l’he Re-view of Economics and Statistics (Augsmst 1958), pp. 261-67.David and Scadding suggest that if Govemmnent and cor-porate activity simply substitute for, rather than augment,household activity, there should he virtually no change inmuch broad aggregates as the ratio of gross private savingto CNP.

rIM

IS

Px

Page 7

FEDERAL RESERVE DANK OF ST. LOWS DECEMBER 1975

in the face of substantial variation in the Governmentdeficit suggests that private debt and public debtare close substitutes. An extra dollar of Governmentdeficit displaces a dollar of private investment ex-penditure because deficit financing is viewed as pub-lic investment and substitutes for private investmentin that households tend to classify both in terms offuture consumption benefits. This case is shown inFigure 4, where an increase in Government spendingfinanced by borrowing induces an offsetting changein private investment so that the IS curve does notshift on balance.

Similarly, tax-financed expenditures have a dis-placement effect on private consumption since theyare viewed in terms of their present consumptionbenefits and substitute perfectly for private con-sumption. With an increase in Government spendingfor consumption financed by increased taxes, the in-crease in taxes reduces private consumption with noeffect on private saving. As a result, there is a shiftin the composition of output from the private sectorto the Government, but there is no shift in aggregatedemand.

Consequently, \vith tax-financed Government ex-penditures displacing private consumption and Gov-ernment bond issues (deficit financing) displacingprivate debt issues dollar for dollar, there is no waythat fiscal actions can affect total demand for goodsand services. In the parlance of the IS-LM framework,fiscal actions (defined as either tax- or debt-financedGovernment expenditures) have no net effect on theIS curve or on aggregate demand, which implies bothnominal and real crowding out. Also, for this case,fiscal actions have no influence on interest rates,

Whether the David-Scadding ultrarational case isto be taken as a serious explanation of crowding outis an open question. Yet it is important to note theimplications of this model, because it represents adeparture from the severe restrictions implicit in theIS-LM model, In particular, tile IS-LM model allowsfor no substitution between private spending andpublic spending; David-Scadding have shown thatmoving away from these restrictive assumptionsacts in the direction of reducing the fiscal policymultipliers. Furthermore, by way of Denison’s Law,they conclude that the evidence leans more towardthe extreme of ultrarationality than the extreme ofthe IS-LM model.

~ f:~c-~ Allcases discussed thus far have not presented any con-flicts with respect to the nominal versus real crowding

r

ro

p

p0

l~i

out issue, because aggregate demand typically doesnot shift. There is, however, another way in whichcrowding out might occur, reflecting a response ofthe price level to a step-sip in Government spending.This case argtres that crowding out is possible evenwithout tile assumption that aggregate demand doesnot shift. Tile implication for nominal versus realcrowding out is ambiguous for this case, however,

Robert Rasche constructed a sophisticated versionof the IS-LM apparatus which was based primarilyon the textbook presentation of Robert Grouch.2°

25Rohert H. Rasehe, ‘‘A Commmparative Static Analysis of Soame\lonetarist Propositions,” this Review (December 1973), pp.15-23; and Robert L. Crouelm Macroeconomics ( New York:Harcoort Brace Jovammovich, Time., 1972)

Figure 4

liltrarational CaseLM

IS (G0}IS (Ga)

x

AD

xo x

Page 8

FEDERAL RESERVE BANK OF ST. LOUIS

The model included wealth in the consumption andmoney demand functions, a Government budget con-straint, and a labor sector, as well as an endogenousprice level. According to Rasche’s analysis, an in-crease in real Government purchases, financed eitherby taxes or debt issuance, increases aggregate de-mand, and, consequently, the commodity price level.Although there may also be a rise in consumptionowing to a presumed positive effect of debt issuanceon wealth, there is an offsetting increase in thedemand for money associated with such wealth gains(see Figure 5). The rise in the price level reducesprivate consumption as well as the real supply ofmoney. Together with a decline in the amount ofprivate investment owing to an increase in interestrates, these factors tend to crowd out an amount ofreal private expenditures equivalent to the increasein Government purchases. Crowding out occurs in thismodel in real terms, but with a higher price level,crowding out is not likely to occur in nominal terms.

These results lead Rasehe to conclude that nominalcrowding out requires “extreme” assumptions aboutthe interest elasticity and the wealth elasticity of thedemand for real cash balances. It should he pointedout, however, that Rasche, in his manipulation of themodel, did not ailow for a Keynes expectation effect,an ultrarational direct substitution effect, or a Knighteffect, all of which may leave the aggregate demandcurve unmoved in response to an initial increase inGovernment spending.

Milton Friedman’s role in the crowding-out con-troversy was established in a series of articles pub-lished in the Journal of Political Economy over theperiod 1970 to 1972.20 Friedman did not rely solelyon the IS-LM model as a framework for his analysis,hut most of his ideas can be summarized in such acontext. Friedman denied emphatically that the mone-tarist propositions rested on the shape of the LMlocus. Instead, Friedman stressed the continuing ef-fects of deficit finance, and a fundamental distinctionbetween stocks and flows.

Friedman dealt with a large number of complexissues in his reply to the critics, and it is difficult todetermine to what extent he supported the notion offiscal crowding out. 1-lis chief point seems to have

~0Friedmnan, “Comnmnents on tile Critics”; “A TheoreticalFramework for Monetary Asmalysis,” Journal of PoliticalEconomy (March/April 1970), pp. 193-238; and “A Mone-tary Theory of Nomnirmal Income,” Journal of PoliticalEconomy (March/April 1971), pp. 323-37

r

DECEMBER 1975

Figure 5

Extended IS-LM CaseLM (01,P1)

IS (G1FPQ]

IS (G11P1)

been that the power of monetary actions far surpassesthat of fiscal actions, which is similar to but not quitethe same as declaring a belief in crowding out. Never-theless, he concluded that the expansionary effect ofarm increase in Government spending by borrowingis likely to be minor.

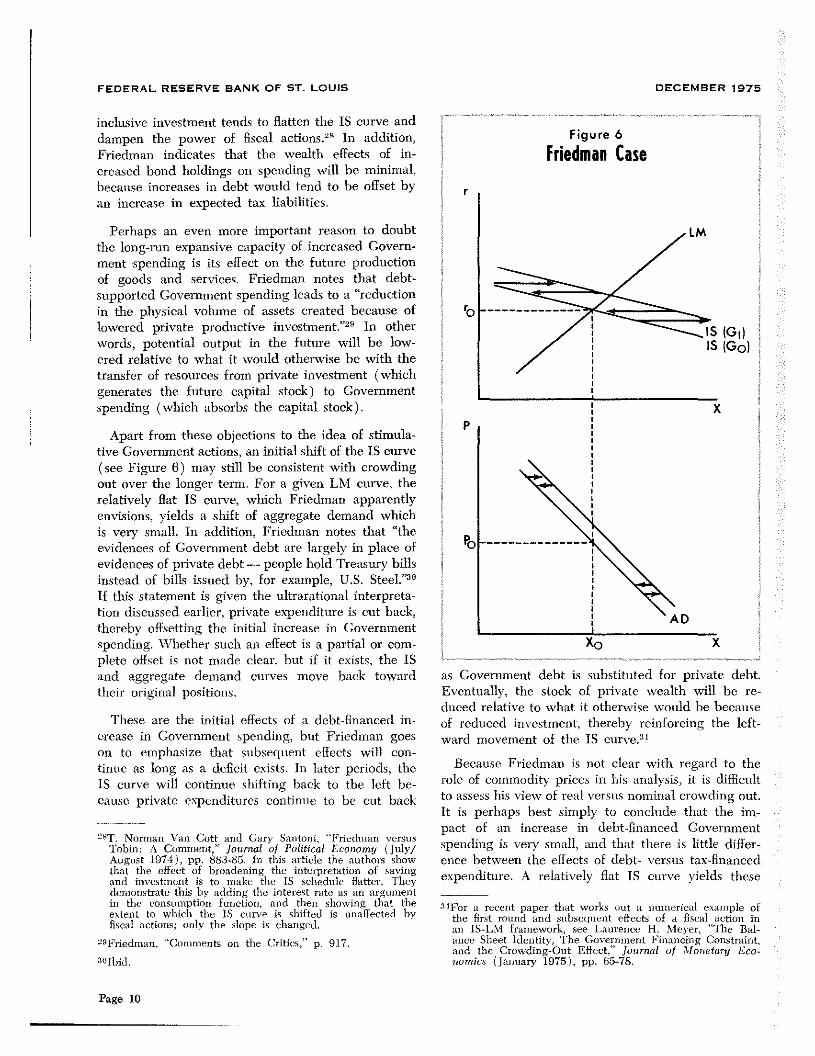

To illustrate the Friedman case, consider Figure 6.The IS curve is drawn quite flat, reflecting Friedman’sstatement that “‘saving’ and ‘investment’ have to beinterpreted much more broadly than neo-Keynesianstend to interpret it,...”27 Though Friedman doesnot emphasize it, this interpretation puts him close tothe Knight case, because the implication of more

2iFriedmnan, “Comments 0mm the Critics,” pp. 915.

LM (G0,P0)

P

IS (G01P0)

AS

x

P

p0

AD (G1)

x0 x

Page 9

FEDERAL RESERVE BANK OF ST. LOUIS DECEMBER 1975

inclusive investment tends to flatten the IS curve anddampen the power of fiscal actions.

25 In addition,Friedman indicates that the wealth effects of in-creased bond holdings on spending will be minimal,because increases in debt would tend to be offset byan increase in expected tax liabilities.

Perhaps an even more important reason to doubtthe long-run expansive capacity of increased Govern-ment spending is its effect on the future productionof goods and services. Friedman notes that debt-supported Government spending leads to a “reductionin the physical volume of assets created because oflowered private productive investment.”29 In otherwords, potential output in the future will be low-ered relative to what it would otherwise be with thetransfer of resources from private investment (whichgenerates the future capital stock) to Governmentspending (which absorbs the capital stock).

Apart from these objections to the idea of stimula-tive Government actions, an initial shift of the IS curve(see Figure 6) may still be consistent with crowdingout over the longer term, For a given LM curve, therelatively flat IS curve, svhieh Friedman apparentlyenvisions, yields a shift of aggregate demand whichis very small. In addition, Friedman notes that “theevidences of Government debt are largely in place ofevidences of private debt — people hold Treasury billsinstead of bills issued by, for example, U.S. Steel.”3°If this statement is given the ultrarational interpreta-tion discussed earlier, private expenditure is cut back,thereby offsetting the initial increase in Governmentspending. Whether such an effect is a partial or com-plete offset is not made clear, hut if it exists, the ISand aggregate demand curves move hack towardtheir original positions.

These are the initial effects of a debt-financed in-crease in Government spending, but Friedman goeson to emphasize that subsequent effects will con-tinue as long as a deficit exists. In later periods, theIS curve will continue shifting hack to the left be-cause private expenditures continue to he cut back

28T. Norman Van Cott and Gary Sammtoni, ‘‘Friedman versusTobin: A Comment,” Journal of Political Economy (July!August 1974), pp. 883-85, In this article the authors showthat the effect of broadening the interpretation of savingand investment is to make the IS schedule flatter. Theydemonstrate this by adding the interest rate asan argumentin the consumption function, and then showing that theextent to which the IS curve is shifted is smnaffeeted byfiscal actions; only the slope is changed.

29Friedman, “Comments on the Critics,’ p. 917.

3~Ibid,

as Government debt is substituted for private debt.Eventually, the stock of private wealth will be re-duced relative to what it otherwise would be becauseof reduced investment, thereby reinforcing the left-

ward movement of the IS curve.31

Because Friedman is not clear with regard to therole of commodity prices in his analysis, it is difficultto assess his view of real versus nominal crowding out.It is perhaps best simply to conclude that the im-pact of an increase in debt-financed Governmentspending is very small, and that there is little differ-ence between the effects of debt- versus tax-financedexpenditure. A relatively flat IS curve yields these

.tmFor a recent paper that works Out a numerical example ofthe first round and subsequent effects of a fiscal action inan lS-LM framework, see Laurence H. Meyer, “The Bal-ance Sheet Identity, The Government Financing Constraint,and the Crowding-Out Effect,” Journal of Monetary Eco-nomics (January 1975), pp. 65-78.

Figure 6Friedman Case

r

IM

ISIS

(G~)(Go)

px

x0 x

Page 10

FEDERAL RESERVE BANK OF ST. LOUIS DECEMBER 1975

results, and any ultrarational effects would reinforcethem.

:wJ(~ fifld

The Friedman emphasis on the longer-run effectsof monetary and fiscal actions prompted two majorpapers (one by Alan Blinder and Robert Solow andthe other by James Tobin and Willem Buiter) thatattempted to demonstrate that the crowding-out ef-fect of fiscal actions is not consistent with the assump-tion of stability of the economic system, as repre-sented by the IS-LM model.52 Both of these papersare discussed in this section along with a third — by

Karl Brunner and Allan Meltzer — which actuallyantedates the other two.33 All three models essentiallyemploy comparative static tools to examine a dynamicphenomenon.

Ide .1. lid Ud. ~

Blind’ nnd dsinn: Recently, Blinder and Solowdeveloped a rigorous theoretical attack on the cro\vd-ing-out thesis.3~They envisioned three possible levelsof crowding out:

1) The Government undertakes activities whichwould otherwise be provided, on a one-for-one basis,by the private sector. They point out that this sort ofcrowding out (to time extemlt it exists) would occurregardless of 110w the Government spending wasfinanced;

2) Debt issues floated by the Government to fi-nance its spending drive up interest rates and crowdout private horrowing;

3) Increases in wealth, derived from the issuanceof Govermnent bonds, increase money demand, thatis, shift the LM curve leftward sufficiently to negatethe rightward shifts of the IS curve.

Blinder-Solow constructed an extended version ofthe IS-LM framework which incorporated consump-

~ii3lismder aimd Solow, ‘‘Does Fiscal Policy Matter?” and Tohiuand Baiter, ‘Lommg Run Effects.”

:nsl3mjmner and Meitzer, “Money, Debt, mmmd EconomicActivity,”tm4For papers criticizing the Blinder-Solow analysis, see AlbertAndo, ‘Ssmme Aspects of Stalsilization Policies, The Mone—tarist Controversy, and time MPS Model,” International Eco-nomic Reciew (October 1974), pp . 541—71; Paul E, Ssnith,‘‘Time Covem’nment Budget Constraismt, Crowding Out, andStability of Equilibrium,” unpublished (May 1975); andames it, Barth, Jammmes T, Benmiett, and Richard H. Sines,

‘‘Fiscal Policy and Macroeeomsomnic Activity,’ ( Paper pre—seuted at tIme Meetings (mf the Sontherms Econonmie Associa—tiomm, New Orleans, Louisiana, November 14, 1.975).

tion and money demand as functions of wealth, anda Government budget constraint providing for Gov-ernment debt interest payments. They adhered to theusual IS-LM customs of treating the price level asfixed and of ignoring the existence of a bankingsystem.

Blinder-Solow then attempted to discern the likeli-hood of crowding-out phenomena occurring by in-vestigating the stabihty properties of the model. Theyderived the following theoretical conclusions:

1) if Government spending financed by bond issu-ance is confractionary, as (according to Blinder-Solow)monetarists claim, the IS-LM model is unstable;

2) if Government spending financed by bond issu-ance is expansive, as neo-Keynesians claim, but lessexpansive than Governnient spending financed bymoney creation, the model is unstable;

3) if Government spending financed by bond issu-ance is more expansive than Government spendingfinanced by money creation, the model is stable.

The unusual result that theoretical stability condi-tions imply that bond-financed Government spendingis more stimulative than money-financed Governmentspending comes about because of the inclusion ofinterest payments on outstanding debt in the Gov-ernment budget constraint. For the model to be stable,the budget must be in balance in the long run toensure unchanging stocks of money and debt. In or-der for the budget gap to close after the initial shockof fiscal stimulus, income must rise by a larger amountin the bond-financed case than in the money-financedcase. This result follows because higher tax receiptsmust be induced to offset the increased interest pay-muents on the Government debt.

Bndr~ Recently Tobin and Buiter alsoformulated an IS-LM model for the purpose of ex-amining the crowding-out thesis. Although some ofthe eqnations differ from those employed by Blinder-Solow, the basic assumptions, such as a constant pricelevel, and the methodology, which is marked by thestability requirement of a balanced budget process,are virtually the same.3° Like Blinder-Solow, Tobin-Buiter utilized more than one variation of the basicIS-LM model, and like Blinder-Solow, they arrived atthe conclusion that the stability considerations inher-ent in the balanced budget requirement generate a

~~Altlmommghthe bulk of their analysis assuumes a constant pricelevel, as does nml earlier smmodel on which their paper wasi,ased, Tohin—Buiter present one version of the model whichemmmploys a variable price level.

Page 11

FEDERAL RESERVE BANK OF ST. LOUIS DECEMBER 1975

positive Government spending multiplier. Tohin-Buiter emphasized that the analysis is conducted forperiods in which the economy is less than fully em-ployed. Furthermore, that crowding out occurs atfull employment is, for them, not a foregone con-clusion, in view of a positive fiscal multiplier in theirfull-employment model.

‘ , H’. ‘ Another model has recentlybeen developed which is adaptable to analysis of thecrowding-out question. Brunner and Meltzer con-sfructed a model of the economy which differs sig-nificantly in orientation from the standard IS-LMmodel. The Brunner-Meltzer model contains marketsfor real assets, financial assets, and current output, andpermits wealth owners to choose among money, bonds,real capital and current expenditures. In contrastwith the Blinder-Solow and basic Tobin-Buiter mod-els, the Brunner-Meltzer model permits the pricelevel to be determined endogenously and includes abanking sector. The analysis also features, as do theother models, stability considerations and a Govern-ment sector which issues interest-bearing debt.

Apparently, these common elements of the modelsare the elements which lead to the unusual resultsalready noted in the Blinder-Solow model, and whichalso emerge in the Brunner-Meltzer model. In par-ticular, Brunner-Meltzer find that Government spend-ing financed by debt issuance is more stimulative thanGovernment spending accompanied by expansionarymonetary actions. Such a result is again dictated bythe requirement of a balanced budget for long-runequilibrium. Once disturbed by, say, an increase inGovernment spending, the budget is required to re-turn to balance, and the presence of interest pay-ments in the budget constraint means that a largerincrease in income is required for bond-financingthan for money financimmg.

Brunner-Meltzer recognized this obvious discrep-ancy between their model results and the historicalevidence, particularly as interpreted by monetarists,They note, that their model results imply “that infla-tion or deflation can occur without any change in B[the monetary base, which is the prime determinantof the money supp1y].’~~Bnmnner and Meltzer takea markedly different view of the causes of inflationoutside their model construct and in the context ofobservable phenomena: “Our analysis of inflation, pre-sented at the Universities-National Bureau Gonfer-ence on Secular Inflation, analyzes the issue in more

36Bmnner amid Meitzer, “Money, Deht, amid Economic Activ-ity,” p. 973 (bracketed words supplied).

detail and explains why most inflations or deflationshave resulted from changes in money.”37

One must bear in mind that the results of theBrunner-Meltzer model are predicated on: (1) theabsence of money illusion (in the usual sense), butthe existence of a possible wealth illusion by way ofincomplete, discounting of future tax liabilities; (2)the requirement of a balanced budget; (3) a fixedcapital stock (Blinder-Solow, in contrast, present avariation of their model in which the capital stock ispermitted to grow); (4) no labor sector (to facilitatechanges in output in lieu of the absence of a changingcapital stock); and (5) the presumption that assetprices respond more strongly to an increase in Govern-ment debt than to an increase in the monetary base.~~

The recent attack on the crowding-out thesis byway of stability analysis introduces a new elementinto the controversy. There are several reasons toto question the implications of these models of theeconomy which indicate that crowding out is not con-sistent with model stability.

B ~“ ‘:,‘,~ i~nn’~:”~’ The Blinder-

Solow model and the basic Tobin-Buiter model, whichare somewhat sophisticated versions of the standardIS-LM apparatus, pci-mit no role for price levelchanges.~°Considering world-wide economic devel-opments over the past decade, one must question therelevance of so-called “structural” models which omitthe existence of inflationary pressures and inflationaryexpectations. Moreover, an important channel throughwhich crowding out might occur is closed off whenprice level changes are forbidden to emerge.

Blinder-Solow recognized this deficiency of theirmodel to some extent, as indicated by their acknowl-edgement that the fiscal policy multiplier would belowered in several ways by the inclusion of an en-dogenously-determined price level: (1) higher priceslower the real value of the money stock and shift the

~~Ihid.

Page 12

3tm

The last—nmemmtiormed itesmi is particularly critical for timeiirunmmer-Meltzer results. \Vhereas asset prices can he ex-pectedl to respond imi a positive maminer to increases in themosmetary base, there is’amnbiguity in the respoimse of assetprices to the issuance of Covernmnermt debt, A positivewealth effect ( givems immeommmplete diseountimmg of future taxliai,ihties ) mnust outweigh a mmegative suhstitutiomm effect(caused hy (kmvernnment debt cosnpeting ism asset marketswith private debt) for time Bnmjmner-Moitzer results to hold.

:sOThe Brunner-Meltzer mnodel permits price level flexibility,hut excludes a labor sector, which presumnahly plays animportant part in realistic attemupts to capture time econonmicstructure.

FEDERAL RESERVE SANK OF ST. LOUIS DECEMBER 1975

LM curve to the left; (2) higher prices reduce realwealth, and thus consumption, shifting the IS curveto the left; (3) progressive taxes combined with in-flation increase the real yield of the tax system, whichalso tends to shift the IS curve leftward; (4) a risingprice level depresses exports and induces imports inan open economy, which again pushes the IS curveto the left.4°

Blinder-Solow maintained that although the fiscalmultiplier will be less than before with the inclusionof price level changes, the sign of the multiplier willremain positive. Because it is their view that thecrowding-out hypothesis requires the fiscal multiplierto be negative, the authors considered only the signof the coefficient to be at issue. This, however, is agross exaggeration. To our knowledge, there have beenno claims that the crowding-out hypothesis requiresthat a dollar of Government spending, unsupportedby monetary expansion, must reduce private spend-ing by ‘more than a dollar, which is the implicationof a negative fiscal policy multiplier,41 Crowding outof the private sector occurs not only when $1 of Gov-ernment spending reduces private spending by $1(a multiplier of zero), but when $1 of Governmentspending reduces private spending by 50 cents (amultiplier of 0.50). Crowding out, then, is a matterof degree rather than of absolute magnitudes. Anegative multiplier is not a necessary condition forcrowding out. And the omission of changing pricelevels in various IS-LM models contributes to thelikelihood that crowding out tendencies will notemerge.

The three modelsunder consideration show that in order for the budgetto be balanced, and for the model to be in long-runequilibrium, the fiscal policy multiplier must be posi-tive, A full equilibrium requires that the levels ofstocks and flows be unchanging. But the question re-mains, how does such a formal analysis contribute toan explanation of the empirical results that implycrowding out occurs?

Tobin-Buiter made two significant points in thisconnection, First, they questioned the ability of eco-nomic analysis — presumably, as incorporated in ab-stract models — to track changing economic variablesto some logical end. “The trouble with such discus-

40Blinder-Soiow added this final price effect in “AnalyticalFommndations of Fiscal Policy,” in Alan S. Blinder, RobertM. Solow, et ai., The Economics of Public Finance (Wash-ington, D.C.: The Brookings Institution, 1974), p. 47.

~Ut should be pointed out that various econometric modelsindeed have uncovered negative fiscal mnultipliers (see p.14of this article).

sions, including this one, is that a long run constructedto track the ultimate consequences of anything is anever-never land. For that abstraction we apologizein advance.”42 If one is really interested in trackingchanges in economic variables over time, the betterapproach would be to construct dynamic modelsrather than comparative static models.

Second, Tobin-Buiter questioned the stability re-quirements (including a balanced budget) associatedwith the IS-LM investigations into the crowding-outcontroversy. Their concluding remarks were:

Finally, we observe again that it is disturbing thatthe qualitative properties of models — the signs ofimportant system-wide multipliers, the stability ofequilibria — can turn on relatively small changes ofspecification or on small differences in values ofcoefficients. We do not feel entitled to use the‘correspondence principle’ assumption of stability toderive restrictions on structural equations and pa-rameters. There is no divine guarantee that theeconomic system is stable,43

The economic system may be stable in the sensethat the U.S. economy has not exploded, but it is along jump from that sort of stability to one whichrequires stock-flow equilibrium including a balancedbudget. Indeed, the budget of the U.S. Governmenthas been in deficit in eleven of the past fifteen years.

The stock-flow equilibrium models discussed here,then, are basically empty of empirical content. Al-though there may have been periods in which someof the relevant flows were approximately in balance,one would be hard pressed to uncover data pointscorresponding to periods of unchanging stocks. With-out the necessary data and a translation of the ab-stract models in a form which is testable, it is impos-sible to confirm or refute the hypotheses associatedwith these stock-flow equilibrium models.

The underlying as-

sumptions and stability requirements of the modelsin question combine to produce a most curious result:Government spending financed by debt issuance ismore expansionary than Government spending ac-companied by money creation, The expansionary ef-fect is summarized in terms of real output in theBlinder-Solow model and prices in the Brunner-Melt-zer model,

These theoretical implications run contrary to vir-tually every investigation conducted into the impactsof fiscal and monetary policy actions on economic

42Tobin and Buiter, “Long Run Effects,” p. 1.

~~Ibid., p. 42 (italics supplied).

Page 13

FEDERAL RESERVE BANK OF ST. LOUIS DECEMBER 1975

activity. None of the architects of these models at-tempted to reconcile the model implications with themass of empirical studies contradicting them.

Brunner and Meltzer acknowledged this discrep-ancy. Hlowever, they offered no explanation for thefact that even though their model implies that bond-financed Government spending is more inflationarythan money-financed spending, their own empiricalstudies indicate just the opposite.44 One is led toconclude that manipulation of these theoretical mod-els constitutes an interesting academic exercise, hutcontributes little of practical significance to the crowd-ing out controversy. With empirical considerationscoming to the fore, the discussion now turns to theeconometric literature to determine what evidencethat approach lmas brought to bear on the issue ofcrowding out.

~ i.~’Li,.),’t,’t~~1B~.

In a recent study of a number of econometricmodels, Gary Fromm and Lawrence Klein publishedsimulation results showing the implied Governmentexpenditure and tax mulitpliers for these models.45

The results showed long-run Government spendingmultipliers ranging from about 1 to 5 when measuredin terms of impact on current dollar GNP.4° How-ever, the majority of the large models surveyed re-vealed that crowding out did occur in real terms overtime. Some indicated $1 of Government spending forgoods and services crowded out even more than $1 ofprivate spending.

For example. the Wharton Mark III Model yieldeda multiplier of minus 3 after forty quarters, and theBureau of Economic Analysis (U.S. Department ofComn’merce) Model gave a real Government spending

Karl Bm’uoaer, Miehele Fratianoi, Jerry L. Jordan, Allan II.Meitzer, and Manfred J, Neumarmn, “Fiscal and MonetaryPolicies in Moderate inflation: Case Stuches of Three Coumm—tries,” Journal of Money, Credit and Banking (February1973), pp. 313-53.

45Cary Fromm and Lawrence R. Klein, “A Comparisomm ofF:leven Econoimietrie Models of the United States,” TheAmerican Ecoimomic Review (May 1973j, pp. 385-93, Thesemodels, unlike the IS-LM abstractions discussed earlier,~vere not forced to a fuli stock—flow equilibrium.

4 °Bliimdem—Solow cited these results as attesting to the absenceof crowding out in large incoimie—expendittmre oodels. Ac-knowledging the imonexisteoce of Covernmnent hudget eon—straiimts in the msmodels, they added that despite this de-fieiermcy, “All we can do now is render a verdict orm thebasis of the evidemmce already in.” They ignored the realcrowding—out results implied by the econometric smiodels,which is smmrpnisimmg, in that their own mmmodei emmmphasized thecrowding-out issue in real terms. See Blinder and Solo’v,“Analytical Foundations,” p. 78.

multiplier over the same time period of minus 23.These results go well beyond monetarists’ contentionsthat complete crowding out gives a multiplier of ap-proximately zero, though these results are less thanclear on the issue of nominal crowding out.

The Fromm-Klein survey of the empirical resultssuggested that crowding out typically occurred be-cause of a rising price level, capacity constraints, andrising nominal interest rates. These results are con-sistent with those implied by the extended IS-LMcase described above, and do not necessarily cor-roborate crowding out of the nonshifting aggregatedemand variety, that is, those cases which implythat crowding out occurs because fiscal actions are off-set by other components of aggregate demand.

However, Fromm-Klein recognized that the modelsimulations produced evidence not in accord with theusual standard Keynesian presumption of positiveGovernment spending multipliers:

Conventional textbook expositions generally depictreal expendittmre mncmltipliers approaching positiveasymptotes. In fact, most of the models here showsuch mnultipliers reaching a peak in two or three yearsand then declining thereafter in fluctuating paths.At the end of five to ten years, some of the modelsshow that eontirnmed sustained fiscal stimulus hasever-increasing perverse impacts.47

Klein suggested elsewhere that perlmaps these newestimates of the fiscal multiplier are not as damagingto the Keynesian position as they initially appear.48

After all, it takes a considerable length of time insome of the models for the Government spendingmnultiplier to approach zero or turn negative, andpolieymakers historically have shown little concernfor the long run. We would only add that this argu-nient reflects ~he progression of the debate on crowd-ing out from “Does it exist?” to “What is the timeperiod?”

As far as small niodels are concerned, the monetaristmodel of the Federal Reserve Bank of St. Louis setoff much of the current controversy. Fiscal crowdingout emerges in the reduced form equations publishedin the St. Louis Review only after a period of time,even though it is a much shorter period of time thanthat of the large income-expenditure models, and it

occurs in nominal terms rather than in just real terms.(;ovci~mentspending, as measured by high-employ-ment expenditures, exercises a relatively strong in-

‘mT

Frt,nim and Klein, “A Comnparisoim,’’ p. 393 (italics suppheci45

See La’vremmce R. Klein, “Conlmentarv on ‘1’he State of theMouetanist Debate,’” this Review (September 1873), pp.9-12.

Page 14

FEDERAL RESERVE DANK OF ST. LOUIS DECEMBER 1975

fluence on GNP (assuming a constant change in themoney supply) in the current quarter and the nextquarter, hut is approximately offset within a year’stime.

These results, which are confirmed by regressionanalysis employing data through mid-1975, should notbe interpreted to suggest that “Government spendingdoesn’t matter”; it matters very much over a certainperiod. Moreover, if Government spending were toaccelerate or decelerate rapidly rather than be heldto a steady rate of change, the impact on GNP wouldbe considerable,

The chief reason that these reduced form resultsare of interest is that they do not follow from astructural model that constrains the channels of trans-mission from fiscal actions to economic activity. Gov-ernment expenditures cover a wide range of activities,some of which substitute for private consumption andinvestment, and others which serve as substitutes orcomplements to private factors of production.4°Withsuch diverse effects, any model which restricts thetransmission of fiscal actions to income and/or interestrate channels, runs the risk of missing the full effectsof Government interaction with the private sector.°°Time St. Louis results certainly do not do justice to themeasurement of the effects of the complexities of theGovernment spending process, but they serve thefunction of questioning the results from models whichrestrict the operation of fiscal actions via fixedchannels.

/

This article has surveyed the recent literature onthe subject of the crowding-out effect of fiscal actions.Crowding out was defined as a steady state Govern-ment spending multiplier of near zero, a definitionwhich was extended to differentiate the terms “nom-inal” and “real” crowding out.

~°We, like most other anaiysts, have had littie to say aboutthe effect of fiscal actions on aggregate supply. For anattempt to enrich standard macroeconomic analysis withsuch considerations, see Kenneth J. An’ow arid MordeeaiKurz, Public Investment, the Rate of Return, and OptimalFiscal Policy (Baltimore: The Johmms Hopkins Press, 1970);and Lowell E. Galloway ammd Pamml F. Smith, ‘The Covenm-ment Budget Constraint and Aggregate Supply,” (Paperpresented at the Meetings of the Southern Economnie Asso—eiatioxm, New Om’leans, Lomn’sinmia, November 14, 1975).

5°See II. 1,. llasmann, ‘‘Remarks Concerning the Applieatiommof Exact Firmite Sample Distrihution Functions for CCLEstimators in Eccmnonmetrie Statistical inference,” Journalof the American Statistical Association (December 1963),p. 944, where he says:

the entire burden of statistical inference in econo-metric simultaneosms equatiomms models falls on the un—

This survey indicates that the controversy has takenplace on two fronts — theoretical and empirical. First,the theoretical literature has developed primarily withreference to the IS-LM model or modifications thereof,Several cases were examined which serve as candi-dates providing theoretical support for the crowding-out hypothesis. In addition, the role of stability con-ditions in the crowding-out controversy was examined.In general, the conclusion was that stability considera-tions are of limited relevance with respect to the ac-ceptance or rejection of the crowding-out hypothesis.

The empirical literature, on the other hand, hastaken the form of simulations of Government actionsand has yielded results that show signs of being con-sistent with the crowding-out hypothesis. This crowd-ing out tends to be very slow in developing, however,and occurs in real rather than nominal terms. The St.Louis results still stand out relative to the largeeconometric models in that crowding out occurs morequickly and also in nominal terms.

As a result of this survey, it is clear that thecrowding-out controversy continues to exist. Appar-ently these issues will not approach resolution untiladditional structural models are developed and tested,The Keynesians have developed many models, butthese models have not been tested as interdependentunits.51 Monetarists, on the other hand, have not of-fered structural models to go along with their reducedform results,52 Such a turn toward hypothesis testingcould lead toward a resolution of the issues in thecrowding-out controversy. Although the controversyhas been explored in this article primarily on a theo-retical level, the implications of these issues for practi-cal matters of stabilization policy are of greatsignificance,

constrained estimates and test statistics associated withthe m’edueed-fonmm, at least, if empinicah confirmatiosmof the underlying economic postulates is the goal aimedat. Whenever the tmnconstnained reduced-fonn statisticsare judged to he in good agreement with the propo-sitions (theorems ) dedcmeed fromn the umlderlying ceo—nouue postulates, then do the structural estimatesemerge as sound nmmd comivenient summaries of thatpart of the sample statistical information which isrelevant to the numerical values of stnmetural pa-rameters, but generally not othenvise.

amSee Keith M. Carlson, ‘‘Monetary ammd Fiscal Actions inMacroeconomic Models,” this Review (January 1974), pp.8-18, A suggested testing of mnodels as interdependentimmmits requires that the muodel be specified in structural formn,but the testing of the model should focus on the reducedform. For further discussion of this approach, see James L.Murphy, Introductory Econometrics ( Hom~mewood, illinois:Richard 1). Irwin, Inc., 1973).

52For recent efforts in this direction, however, see LeonallC. Ammdersen, “A Monetary Model of Nominal IncomeDetermnination,” this Review (Jumie 1975), pp. 9-19.

Page 15

FEDERAL RESERVE BANK OF ST, LOUIS DECEMBER 1975

4/,,

For purposes of definition consider the accompanyingFigure, panel (A), which is a representation of themarket for total output of goods and services. Theintersection of aggregate supply (AS0) and demand(ADo) determine the equilibriimm level of output, Xo,and the price. Po. at which it will be sold. Label thisintersection as point A and interpret it as an initialequilibrium. Now, introduce an expansionary fiscalaction like increased Government demand for goodsand services financed by sales of Government debtto time public.

Assume that the net effect of increased Governmentdemand and the issuance of debt is an increased de-mand for goods and services, as indicated by the shiftof the demand curve to ADm. Further, suppose thatthe expanded Government sector adversely affectsefficiency and productive capacity, resulting in a shiftof the simpply curve to AS. If the new equilibriumoccurs’ anywhere on the vertical line through point A,say at poiimt B, we say that real crowding out hasocetmrred. That is, increased real Government spendinghas been completely offset by a decline in real privatespending.

Consider no’v Panel (B) in the Figure. The curvedline drawn through point A is a rectangular hyperbolaindicating that P times X, which is defined as thenominal value of total onmtput (that is, GNP) , is con-stant and equal to Po Xo. In other words, there is aninfimmite iumimmber of combinations of P and X, besides Poand Xo, which would give the same dollar x-alue oftotal output as at point A. Suppose that in responseto an expansionary fiscal actiomi, aggregate demandammd aggregate supply shift in various directions (de-pending on the assumptions made) and the newequilibriunm settles on the curved hue, say at point Bor C. Under these conditions, nominal crowding outis said to occur. That is, an increase in Co’ernmentspemlding has been offset by a decline in time dollaramount of spending by the private sector,

This distinction between nominal and real crowd-ing out is important because eleamiy one does not im-ply the other. This is shown, in Panel (C) whicheombines the definitions of real and nominal crowd-ing out from Panel (A) and (B). The solid lines are notdemamld and supply curves, but are the loei of pointsdefining neal and nominal crosvding out.

Note that the lines are now drawn as the midpointof a shaded band. This is done to reflect the crowding-out hypothesis; that is, an increase in Governmentdemand, not supported by monetary expansion, re-sults in a steady state income multiplier of approxi-mately zero. The middle of these bands representsthose points at which $1 of Government spendingcrowds out exactly $1 of private spending. The shad-imlg to the right of either line describes that area inwhich partial crowding out (a multiplier between 0and +1) occurs; the shading to the left of either linedescribes that area in which over crowding out (amultiplier between 0 and —1) occurs, Of course, it ispossible that a dollar of Government spending mightcrowd out more than two dollars of private spending,resulting in a multiplier of less than —1 and an equilib-riunl point to the left of either of the bands.

Various combinations of real and nominal crowd-ing out are possible, given an expansionary fiscal ac-tioml. For example, at point A, there is partial nominalammd partial real crowding out. At point B, there ispartial mmominal, but over real crowding out and so onfor other eomhimlations imi’oimnd the intersection of thetwo bands. At some point outside this area, such aspoint E, there is partial real crowding out, hut a com-plete absence of any sort of nominal crowding (lilt. Itis clear that a complete analysis of the fiscal processrequires amm assessnment uf both the demand and sup-ply factors involved in order to describe accuratelythe extent to which nominal and real crowding outmight occur.

Page 16

FEDERAL RESERVE BANK OF ST. LOUIS DECEMBER 197$

Definitions of Crowding Out

(A)Real Crowding Out

AD0

x

P

P0

(B)Nominal Crowding Out

NominalCrowding OUt

PAS1

AD1

P0

•AS1

AD

AS2

Px=POxO

(C)

PSummary

RealCrowding Out

C

A

Page 17