critical issues facing takaful operators with special...

TRANSCRIPT

1

Critical Issues Facing

Takaful Operators with

Special Reference to

Malaysia

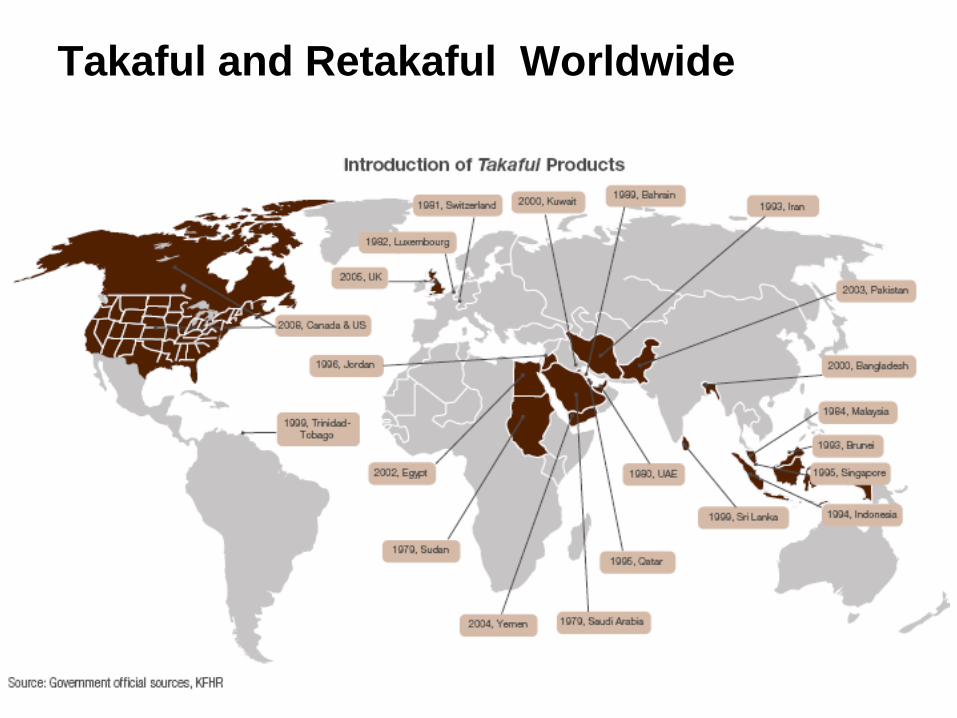

Takaful and Retakaful Worldwide

3

GCC Takaful & Retakaful Operators

(TO & RTO)

Saudi Arabia TO (11); RTO (2)

Kuwait TO (9); RTO (1)

UAE TO (9); RTO (2)

Qatar TO (5); RTO (1)

Bahrain TO (6); RTO (2)

Source: MEIR 2011, GIFF: Country and Business Guide: 2010, Labuan FSA

SEA Countries Takaful & Retakaful

Operators (TO & RTO)

Malaysia TO (11); RTO (19)

Indonesia TO (9); RTO (3)

Brunei TO (3)

Singapore TO (3); RTO (1)

African countries Takaful & Retakaful

Operators (TO & RTO)

Egypt TO (4)

Sudan TO (11); RTO (3)

Algeria TO (1)

Senegal TO (1)

Gambia TO (1)

Kenya TO (1)

Tunisia RTO (1)

Others Takaful & Retakaful Operators (TO

& RTO)

Pakistan TO (4)

Bangladesh TO (3)

Sri Lanka TO (2)

Luxembourg TO (1)

UK TO (2)

Estimated to be over 200 takaful companies

Takaful and Retakaful Worldwide

4

OUTLOOK:

Highest takaful contribution is expected to

come from Asia Pacific

PAST 6 YEARS TREND:

Highest global gross takaful contribution is

from the GCC region

Malaysia contributes ≥ 21% of its total contributions

Global takaful industry growth: 39% (2005-2008) vs 10.2% in conventional insurance

Still less than 1% of global insurance premiums

Source: GIFF 2010

Takaful and Retakaful Worldwide

5

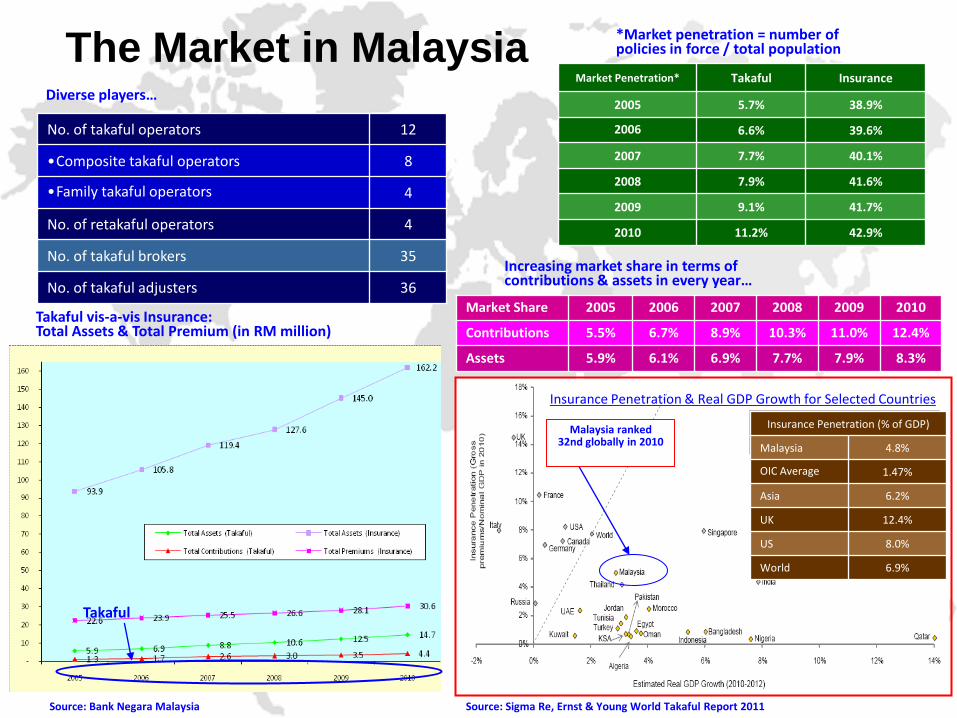

No. of takaful operators 12

•Composite takaful operators 8

•Family takaful operators 4

No. of retakaful operators 4

No. of takaful brokers 35

No. of takaful adjusters 36 Market Share 2005 2006 2007 2008 2009 2010

Contributions 5.5% 6.7% 8.9% 10.3% 11.0% 12.4%

Assets 5.9% 6.1% 6.9% 7.7% 7.9% 8.3%

Diverse players…

Increasing market share in terms of contributions & assets in every year…

Takaful vis-a-vis Insurance: Total Assets & Total Premium (in RM million)

Takaful

Market Penetration* Takaful Insurance

2005 5.7% 38.9%

2006 6.6% 39.6%

2007 7.7% 40.1%

2008 7.9% 41.6%

2009 9.1% 41.7%

2010 11.2% 42.9%

*Market penetration = number of policies in force / total population

Source: Bank Negara Malaysia Source: Sigma Re, Ernst & Young World Takaful Report 2011

Insurance Penetration & Real GDP Growth for Selected Countries

Insurance Penetration (% of GDP)

Malaysia 4.8%

OIC Average 1.47%

Asia 6.2%

UK 12.4%

US 8.0%

World 6.9%

Malaysia ranked 32nd globally in 2010

The Market in Malaysia

6

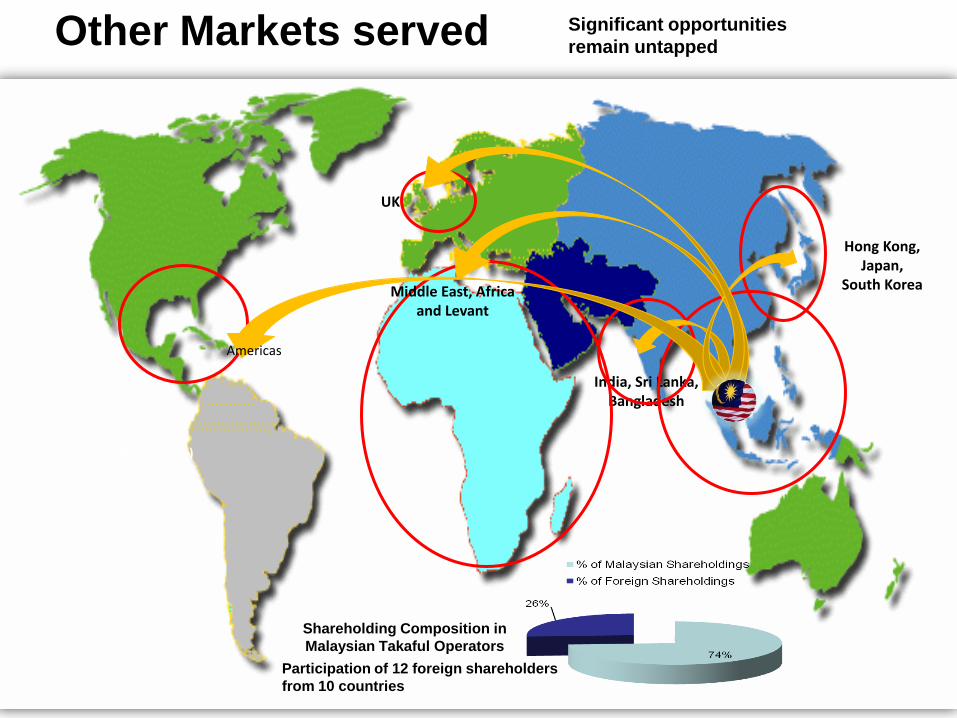

India, Sri Lanka, Bangladesh

Hong Kong, Japan,

South Korea

26% (RM 481.17 m)

UK

Middle East, Africa and Levant

Americas

Significant opportunities

remain untapped Other Markets served

Shareholding Composition in

Malaysian Takaful Operators

Participation of 12 foreign shareholders

from 10 countries

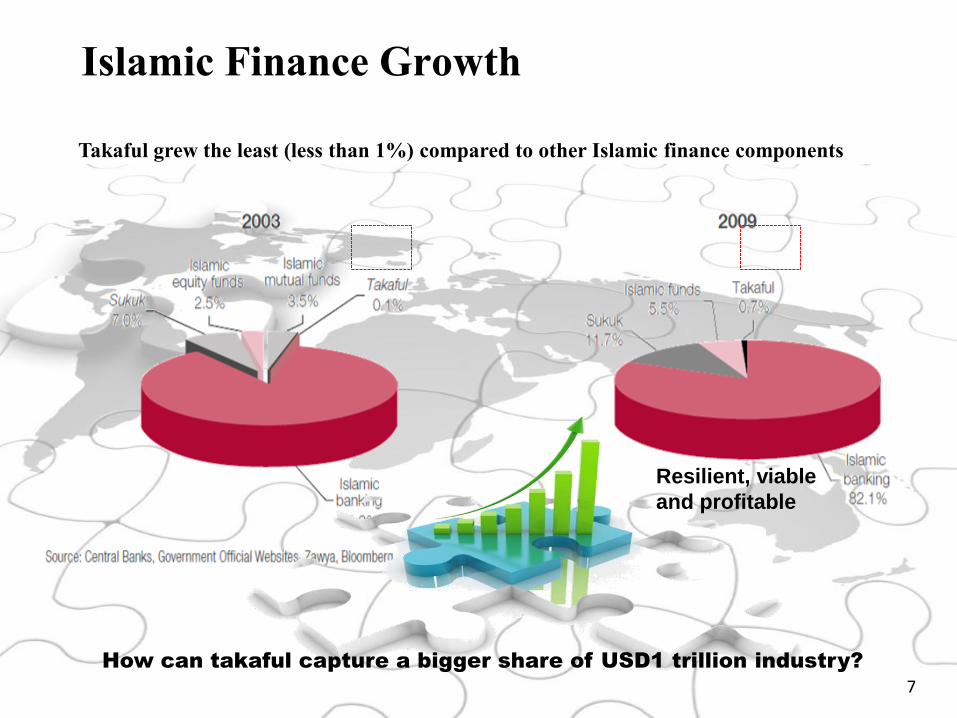

Islamic Finance Growth

7

How can takaful capture a bigger share of USD1 trillion industry?

Resilient, viable

and profitable

Takaful grew the least (less than 1%) compared to other Islamic finance components

8

Global Takaful Industry

Increasing Trend in Gross

Contributions

• GCC is expected to continue its

domination in global Takaful, to deliver

a gross contribution of USD6.4 billion

in 2010.

• This will be followed by South East

Asia with USD1.8billion, largely driven

by Malaysia.

• The projected growth of Takaful

worldwide is about 29%.

Different Preferences among

regions

• Family & Medical plan was the most

preferred plan in South East Asia.

• MENA in contrast saw higher

participation in General Takaful

Business compared to Family plans.

• Interestingly, the record shows the

upward trend in Family & Medical Plans

for both regions, suggesting potential of

the plans to be untapped by the players.

Gross Contributions by Continent

Product Mix : MENA vs South East Asia

9 9

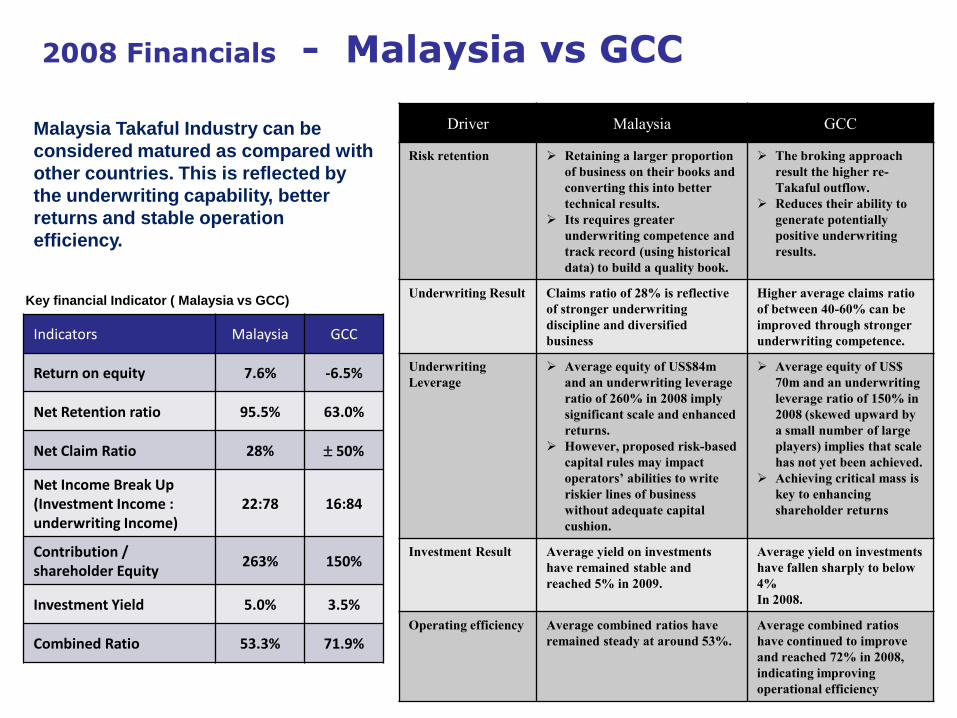

Indicators Malaysia GCC

Return on equity 7.6% -6.5%

Net Retention ratio 95.5% 63.0%

Net Claim Ratio 28% 50%

Net Income Break Up (Investment Income : underwriting Income)

22:78 16:84

Contribution / shareholder Equity

263% 150%

Investment Yield 5.0% 3.5%

Combined Ratio 53.3% 71.9%

2008 Financials - Malaysia vs GCC

Driver Malaysia GCC

Risk retention Retaining a larger proportion

of business on their books and

converting this into better

technical results.

Its requires greater

underwriting competence and

track record (using historical

data) to build a quality book.

The broking approach

result the higher re-

Takaful outflow.

Reduces their ability to

generate potentially

positive underwriting

results.

Underwriting Result Claims ratio of 28% is reflective

of stronger underwriting

discipline and diversified

business

Higher average claims ratio

of between 40-60% can be

improved through stronger

underwriting competence.

Underwriting

Leverage

Average equity of US$84m

and an underwriting leverage

ratio of 260% in 2008 imply

significant scale and enhanced

returns.

However, proposed risk-based

capital rules may impact

operators’ abilities to write

riskier lines of business

without adequate capital

cushion.

Average equity of US$

70m and an underwriting

leverage ratio of 150% in

2008 (skewed upward by

a small number of large

players) implies that scale

has not yet been achieved.

Achieving critical mass is

key to enhancing

shareholder returns

Investment Result Average yield on investments

have remained stable and

reached 5% in 2009.

Average yield on investments

have fallen sharply to below

4%

In 2008.

Operating efficiency Average combined ratios have

remained steady at around 53%.

Average combined ratios

have continued to improve

and reached 72% in 2008,

indicating improving

operational efficiency

Malaysia Takaful Industry can be

considered matured as compared with

other countries. This is reflected by

the underwriting capability, better

returns and stable operation

efficiency.

Key financial Indicator ( Malaysia vs GCC)

10

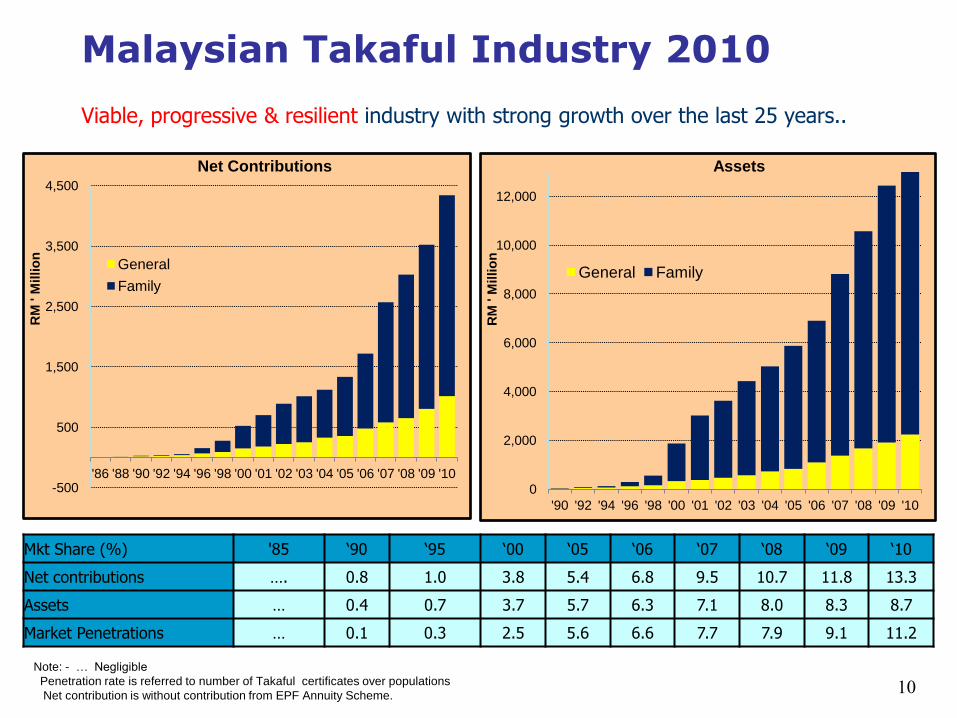

Note: - … Negligible

Penetration rate is referred to number of Takaful certificates over populations

Net contribution is without contribution from EPF Annuity Scheme.

Viable, progressive & resilient industry with strong growth over the last 25 years..

Malaysian Takaful Industry 2010

-500

500

1,500

2,500

3,500

4,500

'86 '88 '90 '92 '94 '96 '98 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10

RM

' M

illio

n

Net Contributions

General

Family

Mkt Share (%) '85 ‘90 ‘95 ‘00 ‘05 ‘06 ‘07 ‘08 ‘09 ‘10

Net contributions …. 0.8 1.0 3.8 5.4 6.8 9.5 10.7 11.8 13.3

Assets … 0.4 0.7 3.7 5.7 6.3 7.1 8.0 8.3 8.7

Market Penetrations … 0.1 0.3 2.5 5.6 6.6 7.7 7.9 9.1 11.2

0

2,000

4,000

6,000

8,000

10,000

12,000

'90 '92 '94 '96 '98 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 R

M ' M

illio

n

Assets

General Family

11

Malaysian Takaful Industry update

With greater diversity of players

8 Composite TOs 5 ICBUs

4 Family TOs

1 ITO

4 RTO 4 ICBU

Robust expansion

• experienced 5 year (2005-2010) compound average growth rate of

27% p.a. (net contributions);

20% p.a. (assets)

• achieved 12.4% market share (net contributions) of total insurance and takaful market in 2010

Net Contribution and Assets for Takaful

1.72.6 3.0 3.5

4.3

0.4

6.9

8.8

10.6

12.4

14.7 14.9

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

2006 2007 2008 2009 2010 Jan-11

Year

RM Billion

Net Contribution Assets

Growth of Net Contribution and Assets for Takaful

29.0

49.3

23.2

17.3

27.9

17.817.8

16.4

19.817.7

-

10.0

20.0

30.0

40.0

50.0

60.0

2006 2007 2008 2009 2010

Year

%

Net Contribution Assets

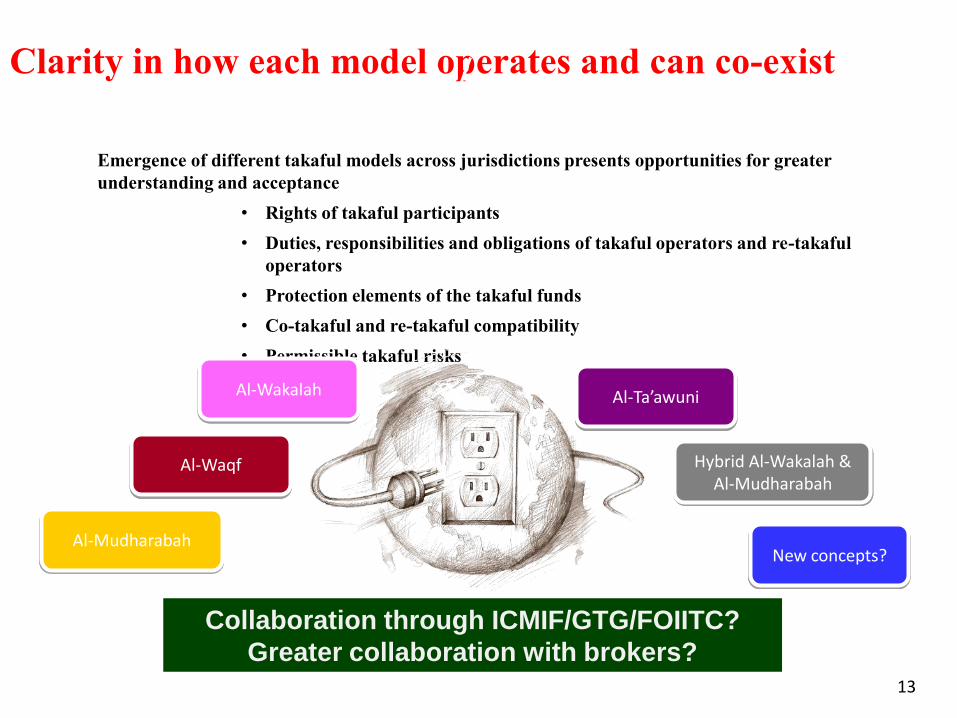

a) Clarity of takaful as a protection product

Issue 1 : International Connectivity in Takaful

Clarity in how each model operates and can co-exist

13

Takaful Funds

Emergence of different takaful models across jurisdictions presents opportunities for greater

understanding and acceptance

• Rights of takaful participants

• Duties, responsibilities and obligations of takaful operators and re-takaful

operators

• Protection elements of the takaful funds

• Co-takaful and re-takaful compatibility

• Permissible takaful risks

Al-Mudharabah

Al-Waqf

Al-Ta’awuni

Hybrid Al-Wakalah & Al-Mudharabah

New concepts?

Al-Wakalah

Collaboration through ICMIF/GTG/FOIITC?

Greater collaboration with brokers?

Covers operational processes relating to takaful and shareholders’ fund, include the requirements relating to:

• Establish operational model that based on the contract and approved by Shariah Committee

• Setting up fund

Segregate shareholders’ fund and takaful fund

• Management of takaful operations

Adequate tabarru’ allocation into PRF to cover risk and obligations associated with takaful contract

Establish written policy on the management of surplus that are approved by Shariah Committee and Board

• Management of operating costs and income of takaful operators

• Management of assets, liabilities and surplus

• Rectification of deficiency of takaful fund

• Establish written policy on mechanism to rectify deficit and/or loss in PRF that are approved by the Board

Guidelines of Takaful

Operational Framework

Key Requirements:

Purpose:

• Ensure business activities and innovations are within TO’s risk management capacity and do not compromise prudence

• Ensure long term business sustainability and safeguard interest of stakeholders via comprehensive internal controls

Snapshot of Malaysian TOF

15

b) Mutual recognition of Shariah

interpretation and enforcement

Issue 1 : International Connectivity in Takaful

16

Mutual recognition of Shariah interpretation and enforcement:

Two main issues

Addressing “leakages” of

business and investments

Seizing a more sizeable

share of Shariah compliant

investible universe

17

c) Intensify development of

international best practices

Issue 1 : International Connectivity in Takaful

19

A good start but more needed in augmenting the uniqueness yet comparability of

takaful as a mainstream protection product which co-exists alongside insurance (eg risk-based capital for takaful and impact of Solvency II requirements on takaful)

Facilitates rating of takaful operators

Regulatory Challenges - IFSB implementation Issues

1. Do the existing law and legal systems adequately address insolvency issues arising from

Takaful operations?

2. Clarity from Shariah standpoint on the treatment of “outstanding” Qard (i.e. that has

been made but not repaid) in the case where a PR F enters into an insolvent winding-up.

IFSB recommends that:

• Any outstanding Qard would rank pari passu with participants’ claims, so that the deficiency

would be shared pro rata;

• Participants’ claims would rank above any outstanding Qard.

3. Clarity on earmarking concept from Shariah standpoint, accounting etc

4. How to determine sufficient level of the Qard draw-down to provide reasonable

assurance those adequate resources will be available within the PRF to meet any

obligations arising in the process of run-off before a PRF be allowed to be run off?

5. Should TOs failed to meet of solvency requirement, required to disclose to the public?

Accountability vs market confident

21

Issue 2 : Market Penetration

•Family takaful product mix heavily concentrated in mortgage-related products;

•Health, endowment & annuity underserved in takaful

Endowment products: Average Size of Annual Premium

2008 2009 2010

RM RM RM

Takaful 802 863 923

Insurance 1,338 1,536 1,764

•Less innovation in family takaful compared to life insurance

- In 2010, on average a life insurer launched 4 times more new basic (ordinary & IL) product and double the number of riders launched by a family takaful player

•Average size of contributions and sum assured still lower than insurance, although gradually increasing

•Need to develop capability to serve all consumer segments including higher income range

Distribution of New Business for Family Takaful and Life Insurance for Dec 2010

13.2

37.0

51.5

10.2

9.1

7.7

2.0

5.4

15.6

31.5

0 20 40 60 80 100

Family Takaful

Life Insurance

Business

%

Endowment & Whole Life*

Mortgage

Medical & health

Other plans

Riders

Annuity

Investment-linked (IL)

Issue 3 : Family Takaful not as competitive

TOs need to improve investment performance…

• Investment yields of family takaful fund consistently underperform life insurance, although gap narrowing

Operate more efficiently

•Takaful industry currently less cost-efficient than insurance

- Underlying trend reflects consistently higher expense ratio

•Cost containment vital to enhance attractiveness of takaful products

- Avoid consumer perception that takaful an expensive option

Investment yield with capital gain

9.4

4.8 4.45.7

4.7 5.24.8

6.5 6.55.8 6.15.6

0.0

2.0

4.0

6.0

8.0

10.0

2005 2006 2007 2008 2009 2010

Year

%

Family Takaful Fund Life Insurance Fund

Incurred management expense ratio

8.4

12.3

10.7

12.1

10.9

9.7

11.6

8.38.27.57.3

6.7

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

2005 2006 2007 2008 2009 2010

Year

%

Takaful Insurance

Incurred Agency Remuneration Ratio

20.3

14.8

20.5

16.4

14.4 14.8

0.0

5.0

10.0

15.0

20.0

25.0

2008 2009 2010

Year

%

Takaful Insurance

And improve productivity

•Based on benchmarking, takaful agents consistently getting higher remuneration for producing much less business than insurance agents

-Takaful average new contributions per agent of RM17,185 vs insurance’s RM38,325 (Q4 2009)

• Increasing trend of retakaful ceded to conventional players despite growing retakaful capacity in the market

• Genuine and progressive efforts to reduce leakage vital for maintaining credibility of takaful and Islamic financial system

Distribution of Retakaful Ceded

-

10

20

30

40

50

60

70

80

2008 2009 2010

Year

%

Insurance/Reinsurance companies Takaful/Retakaful companies

RM 170 m

RM 150 m

RM 187 m

RM 71 m

RM 318 m

RM 105 m

Net Contribution for Retakaful Business (Dec 2010)

49%51%

Local business Foreign business

• Encouraging progress achieved, but some retakaful operators still domestic-focused

• Need to capitalise more on growth opportunities arising from enlarging global takaful market

Leakage to conventional players Domestic focused

Issue 4 : Retakaful Sector

Recent benchmarking exercises reveal

• Higher surrender rate in family takaful than life insurance

• Longer turnaround time for settling family takaful claims from intimation date - 46 days vs 20 days (life insurance) in Q4 2009 - 36 days vs 17 days (life insurance) in Q2 2010

• Lower customer retention in motor takaful than insurance - Only 28% certificates renewal vs insurance’s 48% in Q2 2010

Common areas of takaful consumer complaints to BNM:

• Mis-selling: exaggeration of benefits, no explanation on product exclusion

• Use of scare tactics & intimidation – merely using halal/haram argument as selling point

Issue 5 : Takaful Industry underperforming

Issue 6 : Readiness to comply with new Regulations

Contribute to..

• Enhanced industry readiness in implementation

• Pragmatic and orderly industry growth and development.

• Takaful operators to keep up-to-date with regulatory developments & ensure capacity towards effective implementation

• MTA to play effective role in providing balanced views that reflects industry consensus on issues for the greater good and benefit of industry as a whole

Takaful regulatory framework

BNM Guidelines Effective date

Takaful Operational Framework 1 Oct 2011

Valuation Basis for Liabilities of Family Takaful

Business

FYE beginning on or

after 1 July 2011

Valuation Basis for Liabilities of General Takaful

Business

FYE beginning on or

after 1 July 2011

Shariah Governance Framework 1 Oct 2011

Investment-linked Business 15 April 2010

Internal Audit Function of Licensed Institutions 20 July 2010

Product Transparency and Disclosure Various

Introduction of New Products 1 July 2009

IFSB’s international standards & best practices Issued date

IFSB-8: Guiding Principles on Governance For Takaful

(Islamic Insurance) Undertakings

Dec 2009

IFSB-9: Guiding Principles on Conduct of Business for

Institutions Offering Islamic Financial Services

Dec 2009

IFSB-10: Guiding Principles on Shariah Governance

Systems for Institutions Offering Islamic Financial

Services

Dec 2009

IFSB-11: Standard on Solvency Requirements for

Takaful Undertakings

Dec 2010

Domestic and international regulatory framework for takaful is evolving :

Issue 7 : Human Capital Development

• More concerted action required from all key stakeholders – MTA, takaful operators and training providers

- Talent development as a strategic focus area under a permanent committee of MTA

- Industry to leverage more on INCEIF, IBFIM & ISRA as dedicated education and training solution providers for Islamic finance

INCEIF: Out of 1710 students (2006-2010), only 27 students or less than 2% from takaful industry; all sponsored by only 1 TO

Support INCEIF, IBFIM & ISRA’s capability building agenda

• Harness closer industry – academia/training providers partnership to create synergies for mutual benefits

- Industry to define required skill-set to better integrate industry needs into programs on offer

- Collaborative internship – provide real involvement with industry that allows students to gain valuable practical experience

• Ensure no duplication of efforts or competing objectives to optimise limited resources available

• Review Agency distribution training needs - 20% of agents producing 80% results

• Develop right-mind set and sales skills

• Provide sales tools and harness technology for ‘ease-of-doing business with’

• Improve agency management skills and discipline

• Recruitment, training, sales, logistics

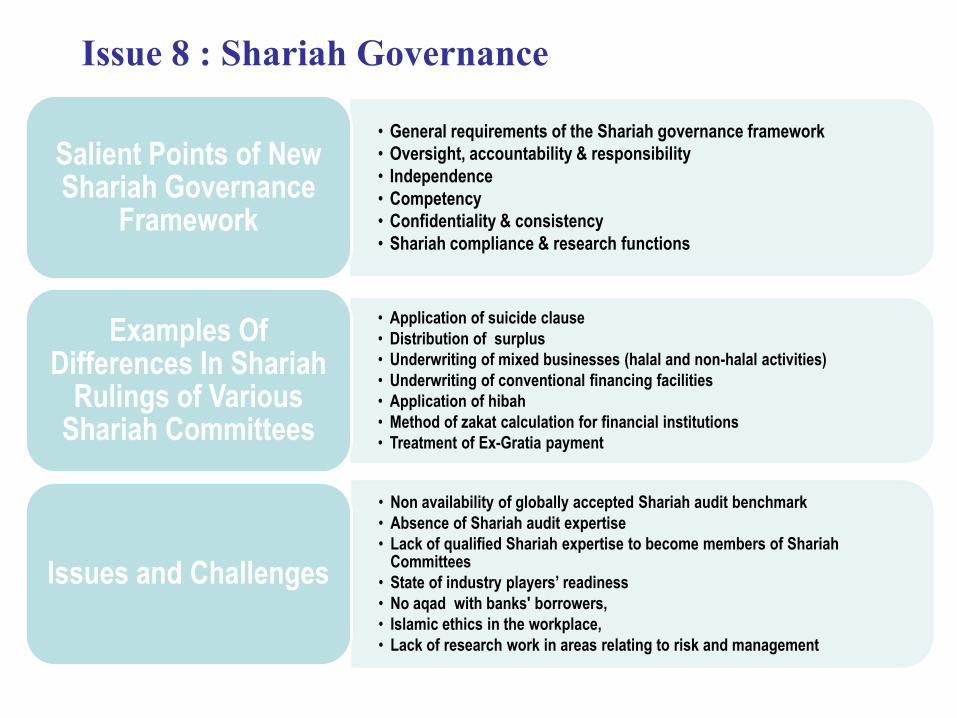

Issue 8 : Shariah Governance

• General requirements of the Shariah governance framework

• Oversight, accountability & responsibility

• Independence

• Competency

• Confidentiality & consistency

• Shariah compliance & research functions

Salient Points of New Shariah Governance

Framework

• Application of suicide clause

• Distribution of surplus

• Underwriting of mixed businesses (halal and non-halal activities)

• Underwriting of conventional financing facilities

• Application of hibah

• Method of zakat calculation for financial institutions

• Treatment of Ex-Gratia payment

Examples Of Differences In Shariah

Rulings of Various Shariah Committees

• Non availability of globally accepted Shariah audit benchmark

• Absence of Shariah audit expertise

• Lack of qualified Shariah expertise to become members of Shariah Committees

• State of industry players’ readiness

• No aqad with banks' borrowers,

• Islamic ethics in the workplace,

• Lack of research work in areas relating to risk and management

Issues and Challenges

Malaysian Takaful Industry: Way Forward

Product Development

Attractive portfolios of product & services that meets current market standards, yet highly

differentiated

Distribution reach

Wide, efficient channel network adapted to

customers’ preferences

Strong underwriting capabilities

Strong underwriting capabilities, skills in

asset allocation & access to

retakafulcapacity

Branding & marketing

Strong reputation as legitimate

takafuloperators & generate goodwill &

trust from customers*

• Standardised to

customised products

• Value-added activities:

white-labelling,

outsourcing centre

• Technical ability to

underwrite LSR,

mega-projects, micro-

Takaful

• Supported by

comprehensive &

efficient data-mining &

advanced analytics

tools

• Operational

excellence

• Cost-efficiency

• Multi-

channelling &

partnership

• Brand leadership

attained from

superior service

quality &

professionalism

that command

customer loyalty

To develop a new blueprint for significant expansion of the financial system, emphasis on the

development of a vibrant regional financial market that can support the expansion in trade and

investment activities within the region.

Conclusion : Key Priorities for M’sian Takaful Operators

1. Sharpen business focus & competitiveness to increase market share, increase takaful penetration and strengthen takaful ecosystem

2. Ensure well-planned transition process towards pricing deregulation of motor insurance and takaful

3. Strengthen operational efficiency and market conduct to attain clear ethical leadership and competitive advantage

4. Ensure readiness for effective implementation of domestic regulatory framework & international best practices

5. Secure success through continuous focus in human capital development

6. Enhance Shariah governance to earn public trust, enhance awareness and facilitate braanding

31

Thank you.