credit risk management practices in banks: an appreciation

TRANSCRIPT

Credit Risk Management Practices in

Banks: An Appreciation

Md. Saidur Rahman∗∗∗∗

Abstract

The banks in Bangladesh have started undertaking a number of quantitative and qualitative

measures to understand the risks involve in credit or chance of default which may come from

the failure of counterparty or obligor (client) to fulfill his/her commitments as per agreed

terms and contractual agreement with the bank. Traditionally, a bank gives emphasis on

collateral in funding to the clients whereas in the concept of modern banking a bank keenly

feels to measure the business risk over the security risk for ensuring the timely repayment of

invested funds. Now-a-days a banker likes to adopt a number of sophisticated financial

techniques in credit appraisal process with a view to assessing the borrower’s business as

well as financial position rigorously. The use of sophisticated techniques for measuring the

financial, business and other risks is yet to be established in the banking operations very fast

due to the advent of computer based technologies. In some cases, the rate of adoption of

analyzing tools and techniques is highly remarkable in credit operation. This attitude of the

bankers has been changed by introducing quality training and reinforcing sophisticated

financial as well as risk grading techniques. A strong database is the demand of the day for

the proper application of the much-demanded credit risk management guidelines along with

effective risk grading system.

1. Introduction

Credit risk may be defined as the possibility that the potential client or counterparty

will fail to meet its obligations in accordance with the agreed terms with the bank. It

also signifies the risk of making credit to a risky customer for a risky venture which is

not likely to generate enough revenue to repay the money back to the bank. Credit

risk is the largest and most obvious source of risk in banking and it comes from a

bank’s credit portfolio. The credit portfolio of a bank usually consists of money

market portfolio, capital market portfolio and general credit portfolio. Here a bank is

highly exposed in the risks of capital market and general credit portfolio. In recent

times, the awareness among the bankers has grown regarding the need for managing

∗

The author is Joint Director (Training) and Faculty Member, Islami Bank Training and Research

Academy (IBTRA), Dhaka. The views expressed in this article are author’s own.

Journal of Islamic Economics, Banking and Finance, Vol. 7, No. 3, Jul– Sep 2011 38

perceived risks in credit related activities. One of the goals of credit risk management

in banks is to maximize a bank’s risk-adjusted rate of return by maintaining credit

risk exposure within the acceptable level. Hence, the credit risk assessment and

grading system are being applied to evaluate, identify, measure and monitor the level

or status of perceived risk associated with a credit proposal. A number of financial

and non-financial factors or parameters are used by the banks for these purposes. The

use of comprehensive credit risk assessment and grading techniques increasing very

rapidly in the banking sector in Bangladesh because of deterioration in the credit

standing of the clients, adoption of Basel accords, compliance of international

accounting standards (IAS) & international financial reporting standards (IFRS) and

the fast revolution of technologies that has made the bankers user friendly in the

adoption of these techniques.

From the findings of different studies, it can be noted that at the very outset the

banking sector in Bangladesh provided huge amount of soft debt facilities to trade,

industry and farming activities for enhancing overall economic growth of the country

and it was done as a part of social commitment of the nationalized sector. Therefore,

the bankers were more concerned to disburse credit to the clients and not to control

the credit flow. At that time, bankers used to take credit decisions mostly on the basis

of 5Cs consists of character, capacity, capital, collateral, condition and control for

safeguarding their credit and without requiring any information of much sophisticated

nature from the borrowers for using credit risk assessment for qualifying credit. Even

in many cases bankers were reluctant to apply very sophisticated financial techniques

in credit decision making if they were satisfied with the security or collateral supplied

by the borrowers. Thus the practice of sophisticated financial techniques as well as

credit risk assessment system for evaluating borrowers’ creditworthiness were more

or less absent in credit operations. But the bankers’ attitudes towards applying in-

depth financial analysis in credit decision making have been changed - particularly

after 1980s when they observed an alarming amount of default credit in their

portfolio. They started taking the whole financial scenario of the business of the

borrowers along with the security and collateral. They also started practicing the

techniques of financial analysis to evaluate the financial statements submitted by the

borrowers. But again the use of financial techniques was limited to the study of

income statement, balance sheet and cash flow statement only with the application of

some traditional financial ratios like current ratio, gross profit margin, debt service

coverage ratio, debt-equity ratio, break-even point analysis, net present worth, benefit

cost ratio, internal rate of return, etc.

All the bankers were seen quite enthusiastic in the early 1990s when a broad based

Financial Sector Reforms Program (FSRP) was undertaken in the financial sector for

improving the efficiency of the banks. Under the said program, much emphasis were

Credit Risk Management Practices in Banks: An Appreciation 39

given in the process of selecting a credit proposal, risk analysis, credit pricing,

classification and provisioning thereof. In 1993, Bangladesh Bank made the first

regulatory move to introduce the best practices in this area through the introduction of

the Lending Risk Analysis (LRA) manual for all credit exposures undertaken by a

bank in excess of Tk.10 million. Bankers were asked to prepare Financial Spread

Sheet (FSS) to cover financial trend analysis through comparative and common-size

financial statements, cash and funds flow analysis, measuring credit scores like Z-

score and Y-score along with Lending Risk Analysis (LRA) for a particular amount

of credit. Under LRA, more emphasis was given to measure the business risk of the

clients. Henceforward, for the first time the bankers in Bangladesh started using

formal risk analysis techniques for measuring risk level of a credit proposal. The

concept of security in credit has been changed by adopting new techniques of credit

analysis. The bankers started understanding that the collateral or customer’s pledge

for credits is just one of the safety zones that a banker must keep for giving overall

protection against the funds which is given to the customers and the liquidate value of

the collateral or pledged goods must be equal or greater than the exposed risk value of

credit sanctioned. But from a number of studies it is found that the legal system in our

country sometimes makes it difficult for the bankers to repossess and sell out the

collateral taken against the credit. So it is clear that the income and cash flow from

business are to be the primary safety zones of a credit (Figure-1) and these are

actually preferred sources of ensuring repayment of credit.

Figure -1: Safety Zones Surrounding the Funds Credited by a Bank

Source: Rose, Peter S. (1996), “Banking Credit: Policies and Procedures,”

Commercial Bank Management ,3rd edition, Boston: Irwin-McGraw-Hill Publishing.

Personal guarantees and pledges made by the

owners of a business firm or by cosigners to a credit.

Resources on the customer’s balance sheet

and collateral pledged.

Customer’s expected profits, income

or cash flow.

Principal amount of credit

plus interest owed the bank.

Journal of Islamic Economics, Banking and Finance, Vol. 7, No. 3, Jul– Sep 2011 40

The most outer or remote safety zone of a credit is the guarantee from the borrowers

or cosigners where they pledged their personal assets to back the credit taken from the

bank. Before taking any personal guarantee, banker must have the idea about personal

net-worth of the person (s) which may help in mitigating risk.

Very recently the Focus Group on risk management has prepared an industry best

practice guidelines titled ‘Credit Risk Management Guidelines’ for the scheduled

banks in Bangladesh under the leadership of Bangladesh Bank with a view to

managing risk exposure effectively. To shed light this purpose and improving the

credit portfolio of the banks, the guidelines consists of some directional policy

frameworks and procedural methods like credit policy, credit risk assessment and risk

grading system, segregation of duties of approval authority, internal audit, preferred

organizational structure and responsibilities, approval process, credit administration,

credit monitoring and credit recovery. To supplement the policy frameworks another

manual on risk grading has also been prepared under the leadership of Bangladesh

Bank. Risk Grading Manual mainly deals with the credit risk grading process by

considering the principal risk components associated with the clients, early warning

signals (EWS), credit risk grading review, MIS on credit risk grading, financial

spread sheet (FSS), etc. It is expected that these guidelines along with the grading

system will improve the risk management culture, establish minimum standards for

segregation of duties and responsibilities, and will assist in the on going improvement

of the banking sector of Bangladesh.

2. Objectives, Scope and Methodology

The main objectives of this study is to make a thorough review of tools and

techniques of credit risk management practices in banks and financial institutions in

Bangladesh as suggested by the relevant bodies and experts under the leadership of

Bangladesh Bank and highlighting the key features in order to grow awareness of the

users about credit risk management practices and its proper implementation in the

credit decision making. Banks and financial institutions put their significant portion

of funds in the long-term financing along with other forms of advances to the public

and private sector programs. As a developing country a huge amount of credit flow is

very much needed both in public and private sector. But it is mentionable that the

credit operation involves risk of non-repayment from the counterparties or clients. In

order to manage the risk exposure which may come from such activities, the credit

risk management practices is one of the important aspects in bank management and it

must be proper and in systematic manner. This study is the result of consulting the

existing literature and is basically theoretical in nature on the subject. All the

discussions that have been included in this paper are the results of extensive study of

existing credit risk grading and risk management systems prevailing in this sector

which were issued by the central bank and international bodies time to time.

Credit Risk Management Practices in Banks: An Appreciation 41

3. Observations on Previous Practices

The Financial Sector Reform Program (FSRP) was introduced in the early nineties in

Bangladesh with a view to bringing about financial discipline by undertaking

appropriate reform measures in the financial sector. The program was undertaken by

the Government of Bangladesh (GoB) with combined support of the World Bank and

USAID under the ‘Structural Adjustment Program’. The program mainly covered the

banking institutions in the financial sector and suggested several reform measures.

Among the measures that FSRP recommended, the Lending Risk Analysis (LRA)

constitutes as an important measure. LRA was prescribed for taking sound credit

decision in consolidated form on the basis of analyzing risks involved in borrower’s

business and security. With a view to ensuring better credit risk management, the use

of LRA was made mandatory in case of sanctioning or renewing large credits until

the adoption of Credit Risk Grading (CRG) in 2003. At present LRA has been

replaced by the CRG.

Lending Risk Analysis (LRA) was involved in assessing the likelihood of non-

repayment of credits (mainly credit risk) from the borrowers as per credit agreement

by analyzing some sort of risks associated with the borrowers’ business and security.

Business risk, the prime component of credit risk, was viewed from two angles viz.

industry risk and company risk.

Table-1: Contents of Risk under LRA Manual

Business Risk Security Risk

1.Industry Risk

1.1 Supplies Risk

1.2 Sales Risk

2.Company Risk

2.1 Company Position Risk

� Performance Risk

� Resilience Risk

2.2 Management Risk

� Management Competence Risk

� Management Integrity Risk

1. Security Control Risk

2. Security Cover Risk

Source: FSRP Bangladesh, Credit Risk Analysis, June 1993.

Journal of Islamic Economics, Banking and Finance, Vol. 7, No. 3, Jul– Sep 2011 42

Again, industry risk was consisted with two types of risks viz. supplies risk and sales

risk. On the other hand, company risk was consisted with four types of risks like

performance risk and resilience risk under company position risk and management

competence risk and management integrity risk under management risk. Finally,

security risk was broken down into two segments like security control risk and

security cover risk. But in practice it limits the use in taking sound decision making

due to some reasons. Saha et al. (2001) conducted a study titled ‘LRA Practices in

Credit Decision in Banks’. The study mentioned that for the purpose of processing

term credit proposal, LRA is being used as a supplementary tool by the banks side-

by-side traditional approach. LRA helps to magnify the use of traditional approach of

credit analysis and there is no conflict between them no doubt. But LRA is not yet

used as a monitoring or follow-up tool in credit operation. However, banks are not

using the techniques of giving early warning signal on the basis of changing risk

status under LRA. More emphasis was given here for the subjective ranking. The

possibilities to reflect the individual’s own judgment and biasness are remained in

assessing credit risk through LRA. Single ‘Form’ for assessing varieties of credits and

ambiguities regarding some terms and concepts incorporated in the LRA Manual

makes it difficult to use a proper credit risk assessment tool. Keeping these limitations

in mind, the Lending Risk Analysis Manual (under RSRP) of Bangladesh Bank has

been amended, developed and re-produced in the name of ‘Credit Risk Grading

Manual’ (Bangladesh Bank: Credit Risk Grading Manual, November 2005). Under

the newly issued manual, the process of credit risk grading has been made more

effective and easier to use in credit decision. It has also been prepared in line with the

business complexities of banks and various processes and models followed by the

different countries and organizations in assessing credit risk.

Note that before adopting new practices under CRM Guidelines, the credit risk

management practices were confined to examine only the risk level for the larger

amount term credits and no attempt used to take to risk grading system for

unclassified accounts in subsequent stages.

4. Findings and Observations on Recent Risk Management Practices in

Banks

Bangladesh Bank issued its BRPD Circular No. 17 dated October 07, 2003 advised

all the scheduled banks to put in place an effective risk management system by

December, 2003 based on the certain guidelines furnished to them. It appears from

the circular that the banking industry is completely different from other industries in

terms of the diversity and complexities of the risks they are exposed to. For

sustainable performance of the banks in view of the deregulation and globalization,

Credit Risk Management Practices in Banks: An Appreciation 43

the banks must be capable of managing their risks. Credit Risk Management

Guidelines involves in assessing and managing credit risks associated with the

selection process of a potential borrower, credit structuring (amount, duration,

purpose, repayment, and support), approval process of credit, credit documentation

(security and disbursement), credit administration, credit monitoring and recovery

functions of a bank or financial institution. At the selection stage, credit risk grading

is essential to keep the credit risk exposure at a tolerable level.

Table-2: Contents of CRM Guidelines

Policy Framework Organization Procedures

� Credit Guidelines

� Credit Assessment & Risk Grading

� Approval Authority

� Segregation of Duties

� Internal Audit

� Structure

� Key Responsibilities

� Approval Process

� Credit Administration

� Credit Monitoring

� Credit Recovery

Source: Bangladesh Bank (2003), Managing Core Risks in Banking: Credit Risk

Management, Dhaka: Bangladesh Bank, Head Office.

Bangladesh Bank, under its prudential regulatory guidelines, advised all the banks

and financial institutions in Bangladesh to follow a robust and structured framework

for risk management. In order to help them in building such type of effective risk

management system, it formed some ‘Focus Groups’ comprising the representatives

from Bangladesh Bank, SCBs, PCBs and FCBs to study the global ‘industry best

practices’ in banking and to recommend a suitable framework of the risk management

system. The present guidelines on core risks management are the outcome of such

types of exercise. The Focus Groups have identified some risk areas which are

associated with the banking operations like credit risk, asset-liability management

risk, foreign exchange risk, internal control and compliance risk, money laundering

risk and ICT risk. These risks are referred to collectively core risks in banking. The

credit risk is one of the major core risks faced by the banks. It is the possibility of

potential losses that may arise from the failure of counter party or obligor (client) to

meet its contractual agreement with the bank. Again, the failure may come from the

declining in financial condition, adverse situation in the industry or unfavorable

condition of the business, trouble in management, weak support due to inferior

quality of security, lack of ready succession and bad relationship with the bank of the

counterparty.

Journal of Islamic Economics, Banking and Finance, Vol. 7, No. 3, Jul– Sep 2011 44

The main feature of these guidelines is the flexibility in practice. Bangladesh Bank

has made the guidelines flexible for the banks in the sense that the respective banks

can design their own risk management system depending on their size and complexity

of business. Central bank, however, trained a good number of officers of the

scheduled banks who in turn may help their respective banks in building up the

capacity to adopt the risk management system. Other features of credit risk

management guidelines have been discussed below:

4.1 Centralization of Major Credit Related Activities

All the banks should have comprehensive credit risk management policies and

procedures to ensure earnings at acceptable level and minimize losses in their

portfolio. The policies will provide directional guidelines to perform credit related

activities properly and efficiently. Credit policy, credit assessment and risk grading

system, approval procedures, internal auditing system are the major areas of credit

risk management policy. Procedural guidelines consist of some set rules of activities

to conduct specific credit function effectively. Credit approval process, credit

administration, credit monitoring, and credit recovery are the part of procedural

guidelines. These policies and procedures should be approved and strictly enforced by

the managing director or chief executive officer and the board of directors. It is noted

that any credit activity which does not comply with the policy guidelines will require

approval from head of credit or managing director or chief executive officer and board

of directors. Security documents should be centralized at the head office or regional

office besides the copy of the same preserving in safe custody at branch level.

4.2 Establishing Own Credit Policy

For the purpose of performing credit activities in desired manner, each bank needs to

establish own credit policy in accordance with their business philosophy. The bank’s

credit philosophy – its general goals and objectives including the mission and vision

of the banks – are reflected in its credit policy. Thus industry and business segment

focus, types of credit facilities, single client or group limits, credit caps, discouraged

business types, credit facility parameters, system of approval etc. shall be

incorporated in the credit policy in black and white with a view to providing overall

framework of credit activities. However it should cover, at a minimum, what

constitutes proper credit support, risk based pricing and documentation of credit

for safety.

4.3 Customization of Credit Policy Based on Changing Circumstances

Now in a deregulated environment, banks are no longer considered as passive takers.

Therefore after the introduction of prudential credit policy, the banks must stand

Credit Risk Management Practices in Banks: An Appreciation 45

ready to meet all the legitimate demands for credit facilities at all the times by

customizing their credit policy. While looking into the matter of customizing credit

policy, the changes in economic outlook and the evolution of bank’s credit portfolio

should be taken into account. The credit policy can also be modified and tuned to

match the changing credit related rules and regulations of the country and all the

modifications and changes must be approved by the managing director or chief

executive officer and board of directors.

4.4 Introduction of Credit Risk Grading (CRG) System in Credit Operations

The risks associated with the borrower or counter-party need to be carefully and

critically analyzed before funding to the client’s business. To quantify the risk

exposure, it should be graded as per credit risk score sheet by the individual banks in

line with the guidelines of CRG Manual. Risk grading is a key measurement of a

bank’s asset quality and it is a robust process. Therefore borrower’s risk grade should

be clearly stated on the credit application form for using credit decision making

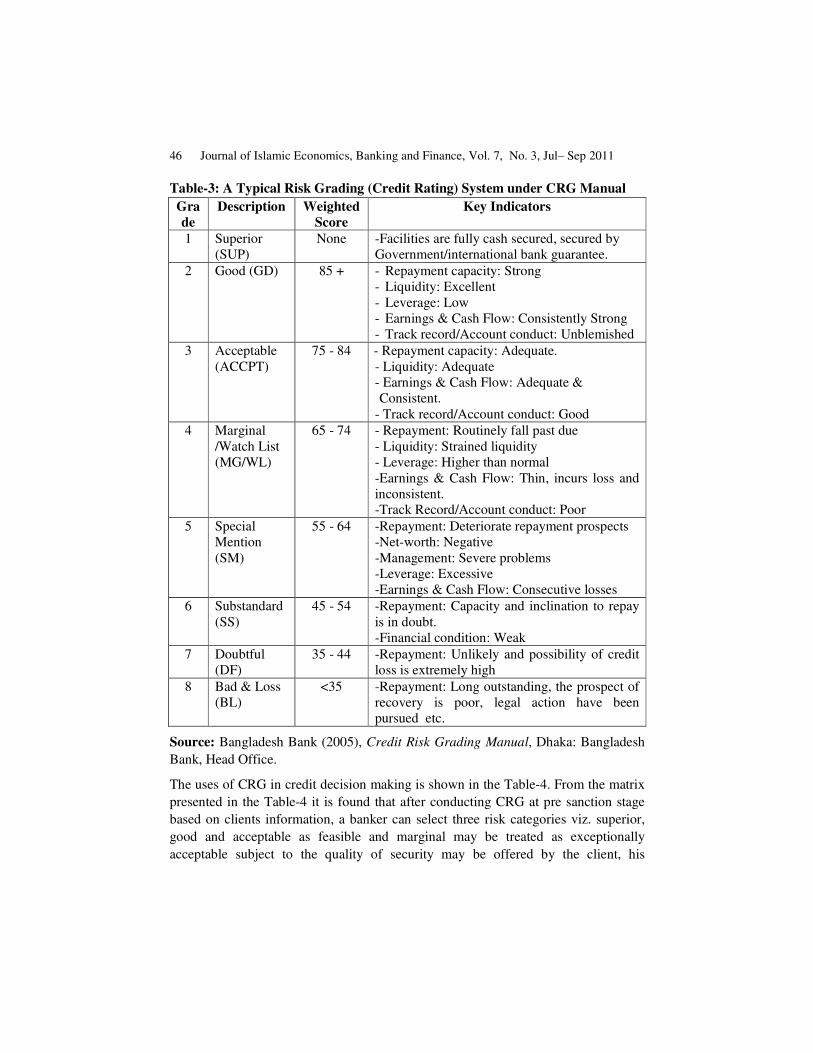

process. In CRG Manual, five risk components viz. financial risk, industry/business

risk, management risk, security risk and relationship risk have been identified which

are responsible of failing to meet the obligations by the borrowers. These risk

components are rated based on the some basic parameters. Note that there are twenty

parameters under the five risk components to reflect the risk exposure. Financial risk

comes from the financial distress of the counterparty. It includes identification of

extent of leverage through debt-equity ratio, liquidity of the borrower through current

ratio, profitability performance through operating profit margin and coverage through

debt-service coverage ratio. Business/Industry risk arises due to adverse change in

business or industry situation. In order to assess the borrower’s business/industry risk

the size of borrower’s business in terms of annual sales volume, age of business,

industry growth, market competition and entry & exit barriers are to be assessed.

Management risk is conducted in assessing the competence and risk taking propensity

of the management. It covers the parameters like experience, second line/succession

plan and team work of the management. Security risk is assessed by analyzing the

primary security, collateral security and support. Relationship risk is considered under

CRG by assessing the account conduct, utilization of limit, compliance of covenants

and balance of personal deposits. There is a wide range of risk exposure or grading

system in the present practices where superior is the top position and bad & loss is the

worst position. In between superior and bad & loss there are six types of risk

exposures say, good, acceptable, marginal/watch list, special mention, substandard

and doubtful (Table-3).

Journal of Islamic Economics, Banking and Finance, Vol. 7, No. 3, Jul– Sep 2011 46

Table-3: A Typical Risk Grading (Credit Rating) System under CRG Manual

Gra

de

Description Weighted

Score

Key Indicators

1 Superior

(SUP)

None -Facilities are fully cash secured, secured by

Government/international bank guarantee.

2 Good (GD) 85 + - Repayment capacity: Strong

- Liquidity: Excellent

- Leverage: Low

- Earnings & Cash Flow: Consistently Strong

- Track record/Account conduct: Unblemished

3 Acceptable

(ACCPT)

75 - 84 - Repayment capacity: Adequate.

- Liquidity: Adequate

- Earnings & Cash Flow: Adequate &

Consistent.

- Track record/Account conduct: Good

4 Marginal

/Watch List

(MG/WL)

65 - 74 - Repayment: Routinely fall past due

- Liquidity: Strained liquidity

- Leverage: Higher than normal

-Earnings & Cash Flow: Thin, incurs loss and

inconsistent. -Track Record/Account conduct: Poor

5 Special

Mention

(SM)

55 - 64 -Repayment: Deteriorate repayment prospects

-Net-worth: Negative

-Management: Severe problems

-Leverage: Excessive

-Earnings & Cash Flow: Consecutive losses

6 Substandard

(SS)

45 - 54 -Repayment: Capacity and inclination to repay

is in doubt.

-Financial condition: Weak

7 Doubtful

(DF)

35 - 44 -Repayment: Unlikely and possibility of credit

loss is extremely high

8 Bad & Loss

(BL)

<35 -Repayment: Long outstanding, the prospect of

recovery is poor, legal action have been

pursued etc.

Source: Bangladesh Bank (2005), Credit Risk Grading Manual, Dhaka: Bangladesh

Bank, Head Office.

The uses of CRG in credit decision making is shown in the Table-4. From the matrix

presented in the Table-4 it is found that after conducting CRG at pre sanction stage

based on clients information, a banker can select three risk categories viz. superior,

good and acceptable as feasible and marginal may be treated as exceptionally

acceptable subject to the quality of security may be offered by the client, his

Credit Risk Management Practices in Banks: An Appreciation 47

reputation etc. However, a borrower with special mentions, sub-standard, doubtful

and bad/loss rating at pre-sanction stage will be treated as not-feasible. A borrower

with superior, good and acceptable rating at post-sanction stage is a performing one.

Borrower who is beginning to demonstrate above average risk i.e. marginal/watch list

or special mention at post-sanction stage will require banker’s attention because it has

become as early alert (warning) account. Rest of the ratings of a borrower at the post-

sanction stage exhibit as non-performing or classified status.

Table-4: Decision Matrix of CRG

Pre-Sanction Stage Grading Status Post-Sanction

Stage

Superior

Good

(1) F

easib

le

Acceptable

(1)

Perfo

rm

ing

(2) Conditional/ Exceptionally

Acceptable

Marginal/Watchlist

Special Mention

(2) Early

Warning

Account

Sub-standard

Doubtful

(3) N

ot -F

easib

le Bad/Loss

(3)

No

n-

Perfo

rmin

g

4.5 Use of Classification and Provisioning Rules in determining Credit Risk

Grading

Out of the eight categories of risk exposures mentioned under the guidelines, four risk

exposures or grading are determined as per the prevailing loan classification and

provisioning rules of the central bank. Therefore, central bank’s rules for credit

classification shall be applied irrespective of risk rating under CRG sheet in case of

risk exposures like special mention, sub-standard, doubtful and bad & loss.

4.6 More Emphasis has been given on the Financial Risk of the Borrowers under

the New Guidelines

Five major risk components are considered to quantify the risk status of a potential

client before funding like financial risk (50%), business/industry risk (18%),

Journal of Islamic Economics, Banking and Finance, Vol. 7, No. 3, Jul– Sep 2011 48

management risk (12%), security risk (10%) and relationship risk (10%). It is to be

mentioned that according to the importance of risk profile, the highest weightage (i.e.

50% out of 100%) has been assigned against the financial risk and the rest weightages

are assigned for the rest principal risk components.

4.7 Introduction of Credit Assessment System

Besides credit risk grading, a thorough credit assessment should also be done before

sanctioning any credit facility in line with the credit risk management guidelines. The

task of credit assessment will cover analysis of borrower, its guarantors, suppliers,

buyers, etc. To supplement such assessment all banks must have well equipped

‘Know Your Customer (KYC)’ form. Credit assessment starts with some summaries

results from the credit application of the borrower like the amount and types of credit

facility proposed, purpose of the credit, its structure, security arrangement, etc. In

addition, some risk areas viz. borrower analysis, industry analysis, supplier/buyer

analysis, historical financial analysis, projected financial analysis where term

facilities require more than one year tenor, account conduct, adherence to credit

guidelines, mitigating factors, security and name credit are to be addressed here.

4.8 Segregation of Major Credit Functions

With a view to improving the knowledge levels and expertise in various functional

areas of credit, to impose controls over the disbursement of authorized credit facilities

and to obtain an objective and independent judgment of credit proposal it is advised

to segregate the credit functions into Credit Approval, Relationship

Management/Marketing and Credit Administration. Moreover, it is advised to make

separate approval function from the marketing function.

4.9 Suggestions for Delegating Approval Authority to Individual Executive not

to Committees

To ensure the accountability in the approval process, the authority to approve or

sanction facilities must be delegated to the senior credit executive not to the

committees based on his/her knowledge and experiences. Approving authorities

should have at least 5 years experience working in corporate/commercial banking as a

relationship manager or account executive, training and experience in financial

statement analysis, financial reporting and full disclosure, cash flow, projections,

trade cycle, risk analysis, credit structuring and documentation, a thorough working

knowledge of accounting, local industry and market dynamics, etc.

4.10 Suggestions for using Computer Based Forms and Templates

Credit risk management is a comprehensive and robust process. It calls for various

sorts of analysis, preservation of results of the analysis and communicating the same

Credit Risk Management Practices in Banks: An Appreciation 49

among the parties involved with the process. It has been advised that banks should

create and use some computer based forms and templates to perform the credit risk

related activities to ensure the accuracy and easy access of information.

4.11 Preferred Organizational Structure

Like all businesses, banks have a hierarchy of command and a division of

responsibility in different functional areas. Credit activity is one of them and it is also

a subject of large dimension. Therefore, within the credit function the banks need to

establish organizational structure and it must be in place to ensure the objectivity and

accountability in credit risk management. As per the proposed organizational

structure of CRM guidelines, below the position of MD or CEO there should be the

Head of CRM and the Head of Corporate/Commercial Banking. Other direct reports

say, internal audit may also belong to the position of MD/CEO. The credit

administration, credit approval and credit monitoring/recovery function may come

under the Head of CRM. On the other hand, relationship management/marketing and

business development may come under the Head of Corporate/Commercial Banking.

4.12 Introduction of Internal Audit System

Credit audit is an important yardstick to measure how well a credit policy and

guidelines, operating procedures, central bank’s directives and credit practices are

being followed. The independent internal audit should seek at a minimum whether the

credit amount is within the banker’s approval authority, whether the security is valid

and sufficient, whether the documentation is complete and accurate, whether review

has done on a timely basis, whether credits are being graded on a timely basis,

whether the credit administration is in overall compliance with the credit operation,

and so forth.

4.13 Credit Monitoring, Review and Early Alert Process

Credit monitoring helps to ensure that the bank’s funds are being used to make

profitable credits with a minimum risk exposure. It includes periodic reviews, ratings

and audits to provide an early indication of the financial health of a borrower. The

frequencies of the review of the CRG of the client shall be regulated by the risk

exposure at the inception of credit and subsequent updated grading. Lower grading

requires more frequency of review. Annual review is to be done in case of superior,

good and acceptable risk grading, half yearly review is to be done in case of

marginal/watch list risk grading and quarterly review is to be done in case of special

mention, sub-standard, doubtful and bad & loss grading.

4.14 Credit Recovery

It is suggested that every bank should have a separate Recovery Unit for conducting

effective and efficient credit recovery functions. This unit will take specific action

Journal of Islamic Economics, Banking and Finance, Vol. 7, No. 3, Jul– Sep 2011 50

plan/ recovery strategy for the accounts with sustained deterioration based on the

recommendations of CRM, pursue all sorts of options to maximize recovery, ensure

adequate and timely credit loss provisioning and regular review of sub-standard and

worse accounts.

4.15 Non-performing Assets (NPA) Management

The Recovery Unit is also responsible for managing NPA of a bank. For this all

NPAs should be assigned to an Account Manager within the Recovery Unit, who will

coordinate and administer the action plan/recovery of account. There should be a

Classified Credit Review Form to know the status of the action plan/recovery plan,

adequacy of provisions etc. on regular basis.

4.16 MIS on Risk Exposure

To maintain the MIS reports of credit risk grading, banks may develop some forms

for the purpose of reporting various risk grading say superior, good, acceptable,

marginal/watch list, special mention, sub-standard, doubtful and bad/loss. Bank-wise

consolidated report, branch and risk grade wise report and grade wise borrower list

may be developed.

4.17 Separate Guidelines for Assessing Risk Exposure of Small Enterprise and

Consumer Financing

Like other credit facilities, the Small Enterprise and Consumer Financing facilities

must be a subject to the bank’s risk management process. Small enterprise means an

entity, ideally not a public limited company, does not employ more than 60 persons

(if it is manufacturing concern) and 20 persons (if it is trading concern) and 30

persons (if it is service concern) and also a service concern with total assets at cost

excluding land and building from Tk. 50,000 to Tk. 30 lac and a trading concern with

total assets at cost excluding land and building from Tk. 50,000 to Tk. 50 lac and a

manufacturing concern with total assets at cost excluding land and building from Tk.

50,000 to Tk. 1 crore (Bangladesh Bank, 2004). At the time of granting facility under

various modes of small enterprise and consumer financing banks shall follow the

prudential guidelines issued by the central bank.

4.18 Application of Financial Spread Sheet

For the purpose of reporting the financial strengths and weakness of the clients in a

precise but comprehensive manner it is advised to use the financial spread sheet

(FSS) in credit decision making under Credit Risk Management practices. The newly

adopted financial spread sheet facilitates trend analysis with the help of common-size

financial statements covering audited as well as company prepared balance sheets and

income statements, financial ratio analysis and cash flow analysis. The cash flow

statement has been adopted in such a way that anyone can easily identify the

Credit Risk Management Practices in Banks: An Appreciation 51

‘Earnings before Interest, Taxes, Depreciation and Amortization (EBITDA)’ cash

flow which is very much essential to know to determine the Debt Service Coverage

(DSC) of a borrower. However, cash flow before and after capital expenditure, total

change in working capital during the year and its impact on cash flow, financing need

or surplus and financing support from the outsides of the business can also be found

from this Cash Flow Statement. FSS contains thirty financial ratios with a view to

assessing the growth of key financial indicators, profitability, debt service coverage,

activity, liquidity and leverage position of the business of a borrower.

5. Basel Principles and Credit Risk Management

The Basel Committee provides some guidelines in order to encourage the banking

sector globally to promote sound practices for managing credit risk. The sound

practices set out under the Basel guidelines specially address the following areas:

(a) establishing an appropriate credit risk environment;

(b) operating under a sound credit granting process;

(c) maintaining an appropriate credit administration, measurement and

monitoring process; and

(d) ensuring adequate controls over credit risk. Although specific credit risk

management practices may differ among banks depending upon the nature

and complexity of their credit activities, a comprehensive credit risk

management program will address these four areas. These practices should

also be applied in conjunction with sound practices related to the assessment

of asset quality, the adequacy of provisions and reserves, and the disclosure

of credit risk.

Each bank should develop a credit risk strategy or plan that establishes the objectives

guiding the bank’s credit-granting activities and adopt the necessary policies and

procedures for conducting such activities. The credit risk strategy, as well as

significant credit risk policies, should be approved and periodically reviewed by the

board of directors. The board needs to recognize that the strategy and policies must

cover the many activities of the bank in which there is a significant credit risk

exposure. The credit risk strategy should include a statement of the bank’s

willingness to grant credit based on type (for example, commercial, consumer, real

estate), economic sector, geographical location, currency, and maturity and

anticipated profitability. This would include the identification of target markets and

the overall characteristics that the bank would want to achieve in its credit portfolio

(including levels of diversification and concentration tolerances). A bank’s board of

directors should approve the bank’s strategy for selecting risks and maximizing

profits. The board should periodically review the financial results of the bank and,

Journal of Islamic Economics, Banking and Finance, Vol. 7, No. 3, Jul– Sep 2011 52

based on these results, determine if changes need to be made to the strategy. The

credit risk strategy should be effectively communicated throughout the organization.

All relevant personnel should clearly understand the bank’s approach to granting

credit and should be held accountable for complying with established policies and

procedures. Credit policies establish the framework for credit and guide the credit-

granting activities of a bank. Credit policies should address such topics as target

markets, portfolio mix, pricing, the structure of limits, approval authorities, etc. The

policies should be designed and implemented within the context of internal and

external factors such as the bank’s market position, business area, staff capabilities

and technology. Policies and procedures that are properly developed and

implemented capable the banks to: (i) maintain sound credit-granting standards; (ii)

monitor and control credit risk; (iii) properly evaluate new business opportunities;

and (iv) identify and administer problem credit.

Establishing sound, well-defined credit-granting criteria is essential to approving

credit in a safe and sound manner. The criteria should set out who is eligible for credit

and for how much, what types of credit are available, and under what terms and

conditions the credit should be granted. Banks must receive sufficient information to

enable a comprehensive assessment of the true risk profile of the borrower or counter

party. According to the Basel guidelines, at a minimum the following factors to be

considered and documented in approving credits:

� the purpose of the credit and source of repayment;

� the integrity and reputation of the client/borrower or counter party;

� the current risk profile (including the nature and aggregate amount of risks)

of the borrower or counter party and its sensitivity;

� The borrower’s repayment history and current capacity to repay, based on

historical financial trends and cash flow projections;

� A forward-looking analysis of the capacity to repay based on various

scenarios;

� The legal capacity of the borrower or counter party to assume the liability;

� The borrower’s business expertise and the status of the borrower’s economic

sector and its position within that sector;

� The proposed terms and conditions of the credit, including covenants

designed to limit changes in the future risk profile of the borrower; and

� Where applicable, the adequacy and enforceability of collateral or guarantees,

etc.

Credit Risk Management Practices in Banks: An Appreciation 53

Once the credit-granting criterion has been established, it is essential for the bank to

ensure that the information it receives is sufficient to make proper credit-granting

decisions. This information will also serve as the basis for rating the credit under the

bank’s internal rating system.

Banks should have in place a system for ongoing administration of their various

credit risk bearing portfolios. Credit administration is a critical element in

maintaining the safety and soundness of a bank. Once a credit is granted, it is the

responsibility of the business function, often in conjunction with a credit

administration team, to ensure that the credit is properly maintained. This includes (i)

keeping the credit file up to date; (ii) obtaining current financial information; and (iii)

sending out renewal notices and preparing various documents such as credit

agreements, etc. Given the wide range of responsibilities of the credit administration

function, its organizational structure varies with the size and sophistication of the

bank. In developing credit administration area, bank should ensure:

� The efficiency and effectiveness of credit administration operations,

including monitoring, documentation, contractual requirements, legal

covenants, collateral, etc.;

� The accuracy and timeliness of information provided to management

information system;

� The adequacy of controls overall ‘back office’ procedures; and

� Compliance with prescribed management policies and procedures as well as

applicable laws and regulations.

Banks must have in place a system for monitoring the condition of individual credit.

An effective credit monitoring system will include measures to: (i) ensure that the

bank understands the current financial condition of the borrower or counter party; (ii)

ensure that all credits are in compliance with existing covenants; (iii) follow the

approved credit lines; (iv) ensure that projected cash flows on major credits meet debt

servicing requirements; (v) ensure that, where applicable, collateral provides adequate

coverage relative to the obligator’s current condition; and (vi) identify and classify

potential problem credit on a timely basis. An important tool in monitoring the quality

of individual credits, as well as the total portfolio, is the use of an internal risk rating

system. A well-structured internal risk rating system is a good means of

differentiating the degree of credit risk in the different credit exposure of a bank and

facilitates early identification of problem credit. This will also allow more accurate

determination of the overall characteristics of the credit portfolio, concentrations,

problem credits, and the adequacy of credit loss provisions.

Journal of Islamic Economics, Banking and Finance, Vol. 7, No. 3, Jul– Sep 2011 54

Banks must ensure that the credit-granting function is being properly managed and

that credit exposures are within levels consistent with prudential standards and

internal limits. The establishment and enforcement of internal controls, operating

limits and other practices will help ensure that credit risk exposures do not exceed

levels acceptable to the individual bank. Limit systems should ensure that granting of

credit exceeding certain predetermined levels receive prompt management attention.

An appropriate limit system would enable management to control credit risk

exposures, initiate discussion about opportunities and risks, and monitor actual risk

taking against predetermined credit risk tolerances. Internal audits of the credit risk

process should be conducted on a periodic basis to determine that credit activities are

in compliance with the bank’s credit policies and procedures.

6. Stress Testing – A Sophisticated Approach for Managing Risks in

Banks & FIs

Bangladesh Bank introduced a Guideline on Stress Testing through Department of

Offsite Supervision Circular No.01 dated 21 April, 2010 with effect from June, 2010.

In this guideline it is noted that the recent financial turmoil in the US financial system

has augmented the importance of establishing more developed risks management

regime in the financial industry. The financial institutions around the world are

increasingly employing stress testing to determine the impact on the financial

institutions under set of exceptional but plausible assumptions through a series of

tests. IMF and Basel Committee on Banking Supervision have suggested for

conducting stress testing on the financial sector. Bangladesh bank has already

designed the ‘stress testing’ framework for the banks and financial institutions to

proactively manage risks in line with the international best practices. Initially, stress

testing begins with the simple sensitivity analysis and scenario analysis considering

only credit risk and market risk. Eventually it is to be developed as a more

comprehensive approach. As a starting point the stress testing is limited to simple

sensitivity analysis approach with covering five different risk factors viz. non-

performing loans (investment), forced sale value of collateral, interest rate risk,

exchange rate risk and equity price risk Moreover, the liquidity position of the

institutions is to be stressed separately. As per desire of the central bank, all the banks

and financial institutions operating in Bangladesh are to carry out ‘stress testing’ on

quarterly basis i.e. on March 31, June 30, September 30 and December 31. The

reporting format of ‘stress testing’ has been designed in line with the Basel II

framework. At institutional level, stress testing techniques provide a way to quantify

the reactions of changes in a number of risk factors on the assets and liabilities

portfolio of the institution. Effective stress testing requires:

Credit Risk Management Practices in Banks: An Appreciation 55

• Defining the coverage and identifying the data required

• Identifying, analyzing and proper recording of the assumptions used for stress

testing

• Well organized management information system

• Setting up some specific trigger points to meet the benchmark/standards set

by central bank

• Calibrating the scenarios or shocks applied to the data and interpreting the

results, etc.

• Ensuring a mechanism for an ongoing review of the results of stress testing

7. Risk Management Practices in Islamic Banks in Bangladesh

Islamic banks are entities that perform financial intermediation according to the

rulings of Islamic Shari’ah. The unique nature of products differentiates Islamic

banks from conventional banks in many aspects. Exclusion of interest, prohibition of

making money from money, implementation of profit and loss sharing system and

prohibition against excessive uncertainty are main sources of differences associated

with Islamic banks. The types and extend of risks of Islamic banks also differ in great

extend (Hasan and Dicle, 2005).Today nearly four hundred (400) banks and financial

institutions are providing their banking services under Islamic Shari’ah rulings in

about one hundred thirty (130) countries of Asia, Africa, Europe, America, Australia,

Argentina, Germany, Denmark, Luxembourg, Switzerland and United Kingdom. The

banking system of Pakistan and Iran is Islamised and that of Sudan has been totally

remodeled on the basis of Islamic Shari’ah. There has been a rapid growth of Islamic

banking industry and the estimated growth rate not less than 15 per cent annually.

The history of Islamic banking began from the early days of Islam. The establishment

of Mit Ghamr Local Savings Bank (Islamic Shari’ah based bank) in the Nile Delta of

Egypt is considered one of the important events in the history of Islamic banking. In

1963/1964, the first financial year after commencement of banking business a total of

17,560 depositors put their many as deposit in this bank. Mit Ghamr is considered as

the milestone of modern Islamic banking system. The achievements made by the Mit

Ghamr Bank in Egypt and subsequently the establishment of the Islamic

Development Bank (IDB) in 1975, the International Association of Islamic Banks

(IAIB) in 1977 motivated the Scholars and Jurists throughout the Muslim world to

take steps for establishing Islamic banks in their own countries with the support of

regulatory authorities and Governments. The Association provides technical

assistance and expertise to Islamic communities wishing to establish Islamic banks

Journal of Islamic Economics, Banking and Finance, Vol. 7, No. 3, Jul– Sep 2011 56

and assist in the development of such banks both at national and international levels.

Islamic Banking is a form of banking where banking operations are conducted in

consonance with the Islamic principles. The philosophies and objectives of Islamic

banking are not similar to the conventional banking rather these are in line with the

principles highlighted in the Holy Qur’an and Hadith/Sunnah. In view with the

Islamic principles particularly prohibition of interest, establishing honesty, justice and

equity in socio-economic arena it may be considered as a system of financial

intermediaries (FIs) that avoids receipt and payment of interest (riba) in its operations

and conducts its operations in a way that it helps achieving the objectives of an

Islamic economy. The General Secretariat of the OIC defined the Islamic bank as ‘a

financial institution whose statutes, rules and procedures expressly state its

commitment to the principles of Islamic Shari’ah and to the banning of the receipt

and payment of interest on any of its operation.’ The Islamic banking system in

Bangladesh started with the establishment of first private sector commercial bank

Islami Bank Bangladesh Limited (IBBL) in 1983. At present seven (7) full-fledged

Islamic banks and eleven (11) conventional banks with their twenty-four (24) Islamic

banking branches are providing Islamic banking services. Internationally reputed

banks like the Hong Kong and Shanghai Banking Corporation (HSBC) Ltd., Citi

Bank N.A., Standard Chartered Bank and Commercial Bank of Ceylon introduced

Islamic products. The state owned commercial banks (former NCBs) have opened

their Islamic banking wings to provide Shari’ah compliant services. A state owned

bond called Bangladesh Government Islamic Investment Bond (BGIIB) has been

issued by the central bank. The five Islamic insurance companies operating under the

private sector in this country as Islamic financial institutions these are Islamic

Insurance Bangladesh Limited, Islamic Commercial Insurance Limited, Takaful

Insurance Company Limited, Far East Islamic Life Insurance Limited and Padma

Islamic Life Insurance Company Limited. In Bangladesh, the share of deposit

mobilization and investments of Islamic banking in total banking industry are 16 per

cent and 20 per cent respectively. Recently a study was done by Ahmed (2010) to

identify the potential for Islamic finance and to examine its impact. This study shows

the trends of savings and investment of some selected Islamic and conventional banks

which are established in contemporary period in Bangladesh. According to the

findings of the study, during 2004 to 2008 the total savings of Islamic banks is higher

than those of the conventional banks (Table 1). Over the years the savings

mobilization gaps widened in favor of the Islamic banks. The differential amounts of

savings mobilization between Islamic and conventional banks are BDT 45,036

million, BDT 49,897 million, BDT 56,821 million, BDT 89,109 million and BDT

113,180 million during the period under study.

Credit Risk Management Practices in Banks: An Appreciation 57

Table 1: Savings Mobilization by Islamic and Conventional Banks

Amount in Million BDT

Savings of Islamic Banks

(A)

Savings of Conventional

Banks (B) Year

IBBL SIBL ARAFAH

Total

(A) NBL IFIC CBL

Total

(B)

Difference

(A-B)

2004 87721 19704 10108 117533 29486 20774 22237 72497 45036

2005 107788 16863 11644 136295 33335 22505 30558 86398 49897

2006 132419 16171 16775 165365 40351 28621 39572 108544 56821

2007 166325 18176 23009 207510 47961 29900 40540 118401 89109

2008 200343 22688 31470 254501 60195 36092 45034 141321 113180

Source: Ahmed (2010).

Note: IBBL = Islami Bank Bangladesh Ltd., SIBL=Social Islami Bank Ltd., ARAFAH= Al-

Arafah Islami Bank Ltd., NBL= National Bank Ltd., IFIC= International Finance Investment

and Commerce Bank Ltd. and CBL=The City Bank Ltd.

The study also shows the investment trends of Islamic and conventional banks to

justify the potential of Islamic finance. Table 2 shows the year-wise amount of

investment of Islamic and conventional banks under study.

Table 1: Investment of Islamic and Conventional Banks

Amount in Million BDT

Investment of Islamic

Banks (A)

Investment of

Conventional Banks (B) Year

IBBL SIBL Arafah

Total

(A) NBL IFIC CBL

Total

(B)

Difference

(A-B)

2004 76826 12887 8150 97863 22972 21281 17028 61281 36582

2005 93644 15097 11474 120215 27020 21695 23326 72041 48174

2006 1113575 15313 17423 146311 32709 25490 30789 88988 57323

2007 144921 15869 19214 180004 36476 28361 26788 91625 88379

2008 191230 18725 29723 239678 49665 33018 34421 117104 122574

Source: Ibid.

It is observed that like savings mobilization gaps, the gaps of investment making also

widened in favor of Islamic banks. Though the market penetration of Islamic banks in

Bangladesh is significant but still now there no separate risk management guidelines

for Islamic banks. Both the conventional and Islamic banks are following the same

guidelines which have been advised by the central bank for managing their risks in

operations. The central bank through a circular dated November 09, 2009 introduced

a ‘Guidelines for Islamic Banking’ with a view to bringing greater transparency and

accountability in Islamic banking. The Guideline covers the main areas of Islamic

banking – liquidity, maintenance of books of accounts, preparation of financial

statements and related issues. It is a supplementary to the existing banking laws.

Journal of Islamic Economics, Banking and Finance, Vol. 7, No. 3, Jul– Sep 2011 58

Islamic banking, also known as participatory banking, refers to a system of banking

or banking activity that is consistent with the principles of Islamic Shari’ah and its

practical application through the development of Islamic economics. In order to fully

comply with the Islamic Shari’ah rules in banking transaction all the banks have their

own Shari’ah Council. Besides Bangladesh Bank has formed a Central Shari’ah

Council and related issues. In addition, they are also advised to follow the accounting

and auditing standards prescribed by the Accounting and Auditing Organization for

Islamic Financial Institutions (AAOIFI). There are seventy (70) standards on

accounting, auditing and governance along with the code of ethics and Shari’ah

Standards of AAOIFI. The Islamic banks have a number of objectives to perform

their activities say, abolition of interest (riba) in banking operations, allowing

Shari’ah permissible products/sectors for financing, risk sharing and participatory

banking, working as catalyst of development, upholding Islamic ethical standards etc.

7.1 Guiding Principles of Islamic Financial Services Board (IFSB) for Managing

Risks

Islamic banking sector continues to grow globally at a rapid pace. The Islamic

Financial Services Board IFSB) is even more optimistic in its outlook for the growth

of the global Islamic banking industry. It forecasts that total asset value of Islamic

banking industry will expand to US Dollar 2.8 trillion in 2015 compared to US Dollar

1.4 trillion in 2010. The IFSB has developed guiding principles for Islamic banking

industry. The issuance of the Guiding Principles of risk management by the Islamic

Financial Services Board (IFSB) is a giant step for the Institutions offering Islamic

Financial Services (IIFS). The IIFSs include the commercial banks, investment banks,

finance houses and other fund mobilizing institutions that offer services in accordance

with Islamic Shari’ah rules and principles. The Guiding Principles of IFSB provides a

set of guidelines of best practice for establishing and implementing effective risk

management in IIFS. The main features of the Guiding Principles are:

• It has been endorsed by the Shari’ah Advisory Committee, Islamic

Development Bank (IDB) and co-opted Shari’ah scholars representing central

banks and monetary agencies which are members of the IFSB.

• It has been designed to complement the current risk management principles

issued by the BCSB and other international standard setting bodies.

• It sets out fifteen principles of risk management that have practical effect to

managing risks. The IFSB will oversee these matters.

• It retains the existing applicable Shari’ah-compliant international principles.

Credit Risk Management Practices in Banks: An Appreciation 59

• It outlines a set of principles applicable to managing major six risk areas like

credit risk, equity investment risk, market risk, liquidity risk, rate of return

risk and operational risk.

7.2 Compliance of Basel II Accord with the Islamic Banks

Hassan and Dicle (2005) have noted in a recent article that the Accounting and

Auditing Organization for Islamic Financial Institutions (AAOIFI, 1999) suggests a

formula for the capital adequacy ratio: CAR = OC / (WOC+L+WPLS * 50%). Where,

CAR is the capital adequacy ratio, WOE+L is the average risk weight of assets financed

with the Islamic bank’s own capital and liabilities other than investment accounts,

WPLS is the average risk weight of investment accounts. AAOIFI requires the CAR to

be equal to 8 percent.

In Bangladesh, Basel-I accord was started in 1996. Initially in accordance with Basel-

I the Capital Adequacy Ratio (CAR) was 8% on Risk Weighted Assets which was

increased to 9% on 30.06.2003 and 10% on 31.12.2007. The revised accord i.e.

Basel-II was introduced in Bangladesh through a BRPD circular No.9 dated

31.12.2008. For implementing the revised accord experimentally, the parallel run of

Basel-II was started from 01 January, 2009 for 1 year and full operation was started

from 01 January, 2010. All the banks are advised to meet the regulatory capital BDT

400 crore or 9% of risk weighted assets whichever higher by August, 2011. It is noted

that most of the Islamic banks have fulfilled the revised capital requirements. The

Basel Committee on Banking Supervision suggests considering the credit risk,

operational risk and market risk determining the risk weighted assets through using

various approaches say standardized approach, internal rating based approach, basic

indicator approach, advanced measurement approach, internal model approach etc.

Note that Bangladesh Bank has advised all the scheduled banks (both conventional

and Islamic banks) to follow standardized approach, basic indicator approach and the

standardized approach to measure credit risk, operational risk and market risk

respectively.

8. Concluding Remarks

In every economy bankers are regarded as a creator of socio-economic development

as they collect funds from the surplus units of the society and to channelise the same

to the deficit units (user groups) of the society with the objectives to deploy the funds

in economic activities for enhancing industrial growth and employment. But to earn

positive return or profit from the credit activities is also the prime consideration for

their survival. Since banking business is a mechanism of channeling depositors’ funds

as advance from one unit to another unit of a society and the derivative products of

this mechanism are to earn profit, generate employment etc. that’s why bankers are to

Journal of Islamic Economics, Banking and Finance, Vol. 7, No. 3, Jul– Sep 2011 60

take a lot of precautions before disbursing the depositors’ money as credit. Banks deal

with the depositors’ money and the banking philosophy is primarily based on ‘trust’

and any inconsistency in the case of disbursing credit may breach the trust and

confidence of the depositors and which may ultimately create the financial distress in

the economy. Thus, an efficient banker should always think about the probability of

non-repayment of credit (credit risk) before disbursing it to the borrowers. In this

context, the use of sophisticated risk grading techniques shows paramount importance

for measuring the financial risk, business or industry risk, management risk, security

risk and relationship risk of the borrowers so as to minimize the risk exposure of

credit which may come from default. The banks in Bangladesh should follow the

techniques for measuring risk by customizing these according to our socio-economic

circumstances and organizational set up. Each bank may establish data bank for its

own consumption at the time of taking credit decision under the sophisticated credit

screening techniques. Besides the data bank, well accepted norms and industry

average may be developed based on the clients’ information in sector-wise funding

for better practicing financial analysis. Uniform practices for preparing projected

financial statements may be established in the banks for the clients who will seek

facilities from the banks. Most of the banking problems have been either explicitly or

indirectly caused by weakness in credit risk management. Several credit losses in the

banking system usually reflect simultaneous problem in several areas such as

concentration, credit processing, failure of due diligence and inadequate monitoring.

First, concentration would include concentration of credits to single borrower or

counterparty, a group of connected counterparties, and sectors or industries. Banking

supervisors should have specific regulations limiting concentrations to one client or

set of related clients, and, in fact, should also expect banks to set much lower

concentrations Banks are to explore techniques to identify concentrations based on

common risk factors. Second, many credit problems reveal basic weaknesses in the

credit granting and monitoring process. A thorough credit assessment (or basic due

diligence) needs for financial information based on sound accounting standards and

timely macroeconomic and flow of funds data. When this information is not available

or reliable, banks may dispense with financial and economic analysis and support

credit decisions with subjective information. The absence of testing and validation of

new techniques of credit decision making is another important problem. Third, many

banks that experienced asset quality problems due to lack of effective credit review

process. The purpose of credit review is to provide appropriate checks and balances to

ensure that credits are made in accordance with bank policy and to provide an

independent judgment of asset quality. Fourth, a common and very important

problem in credit process is lack of monitoring client or collateral value. In absence

of monitoring process the bank will fail to recognize early signs that asset quality will

Credit Risk Management Practices in Banks: An Appreciation 61

deteriorate and will miss the opportunities to work with clients to stem their financial

deterioration and to protect the bank’s position. In some cases, the failure to perform

adequate due diligence and financial analysis and to monitor the client can result in a

breakdown of control to detect credit related fraud. So, an effective credit review

department and independent collateral appraisals are important protective measures.

Fifth, due to lack of sufficient account of business cycle effects in taking credit

decisions, the banks will fail to understand the income prospects and assets value that

may change for changing business cycle. Effective ‘stress testing’ which takes

account of business or product cycle effects is one approach to incorporating into

credit decisions a fuller understanding of a client’s credit risk. Fifth, the lack of

applying risk sensitive pricing methodology in credit decision making. Banks that

lack a sound pricing methodology and the discipline to follow consistently such a

methodology will tend to attract a disproportionate share of under-priced risks. These

banks will be increasingly disadvantaged relative to banks that have superior pricing

skills. Finally, Hassan and Dicle (2005) have noted in their article that the unique

products and procedures of Islamic banks require specialized rating process. Such

process should include specialized models and rating systems designed in accordance

with Islamic banks and associated risks. Basel II proposes internal ratings based

(IRB) approach for banks to differentiate their risk measurement systems

References

Ahmed, Mahmood (2010), ‘The Potential for Islamic Finance,’ A Paper Presented in The

International Seminar on Islamic Finance in India: Products, Institutions & Regulations,

organized by The Islamic Research and Training Institute (IRTI), IDB and The Islamic

University (Al Jamia Al Islamia), Kerala, held in Kerala, India, October 4-6.

Bangladesh Bank (2003), Managing Core Risks in Banking: Credit Risk Management, Dhaka:

Bangladesh Bank, Head Office.

______________ (2005), Credit Risk Grading Manual, Dhaka: Bangladesh Bank, Head

Office.

______________(2004), Prudential Regulations for Small Enterprises Financing, Dhaka:

Bangladesh Bank, Head Office.

______________ (2010), Guidelines on Stress Testing, Dhaka: Bangladesh Bank, Head

Office.

FSRP Bangladesh (1993), Credit Risk Analysis Manual, Dhaka: Bangladesh Bank, Head

Office.

Journal of Islamic Economics, Banking and Finance, Vol. 7, No. 3, Jul– Sep 2011 62

Hassan, M. Kabir and Mehmet F. Dicle (2005), “Basel II and Capital Requirements for

Islamic Banks,” in the Proceedings (Volume 2) of International Conference on Islamic

Economics and Finance, Islamic Economics and Banking in the 21st Century, held in

Jakarta, Indonesia, November 21-24.

Hassan, M. Kabir and Mehmet F. Dicle (2007), “Basel II and Corporate Governance of

Islamic Banks,” in Integrating Islamic Finance into the Mainstream: Regulation,

Standardization and Transparency, edited by Nazim Ali, Islamic Finance Program,

Islamic Legal Studies Program, Harvard Law School.

Rose, Peter S. (1996), “Commercial Bank Management”, 3rd

edition, Boston: Irwin-McGraw-

Hill Publishing.

Saha, Sujit, Md. Saidur Rahman and Mosaddak Ul Alam (2001), ‘Credit Risk Analysis

Practices in Credit Decisions in Banks’, Bank Parikrama, Vol. XXVI, No.2, June, Dhaka:

Bangladesh Institute of Bank Management.