creative accounting lesson 10. reference chapter : chapter 20 financial accounting & reporting...

TRANSCRIPT

Creative Accounting

LESSON 10

Reference Chapter :

Chapter 20

Financial Accounting & Reporting

Barry Elliott & Jamie Elliott

In general :

Creative accounting refers to ways used by entities to ‘change’ or ‘window dress’ figures to achieve their desired result. The desired result may be to achieve a profit or loss position, as desired by management.

There are ways to ‘window dress’ the Financial Statements. ‘Window dressing’ inventory or other current assets remain a common way.

Objectives

After finishing this chapter, you should be able to:• define inventory in accordance with IAS 2;• explain why valuation has been controversial;• describe acceptable valuation methods;• describe procedure for ascertaining cost;• calculate inventory value;• explain how inventory could be used for creative

accounting;• explain IAS 41 provisions relating to agricultural

activity;• calculate biological value.

Inventory defined

IAS 2 Inventories defines inventories as assets• held for sale in the ordinary course of business;

• in the process of production for such sale;

• in the form of materials or supplies to be consumed in the production process or in the rendering of services.

Inventory defined (Continued)

The valuation of inventory involves• the establishment of physical existence and

ownership;

• the determination of unit costs;

• the calculation of provisions to reduce cost to net realisable value, if necessary.

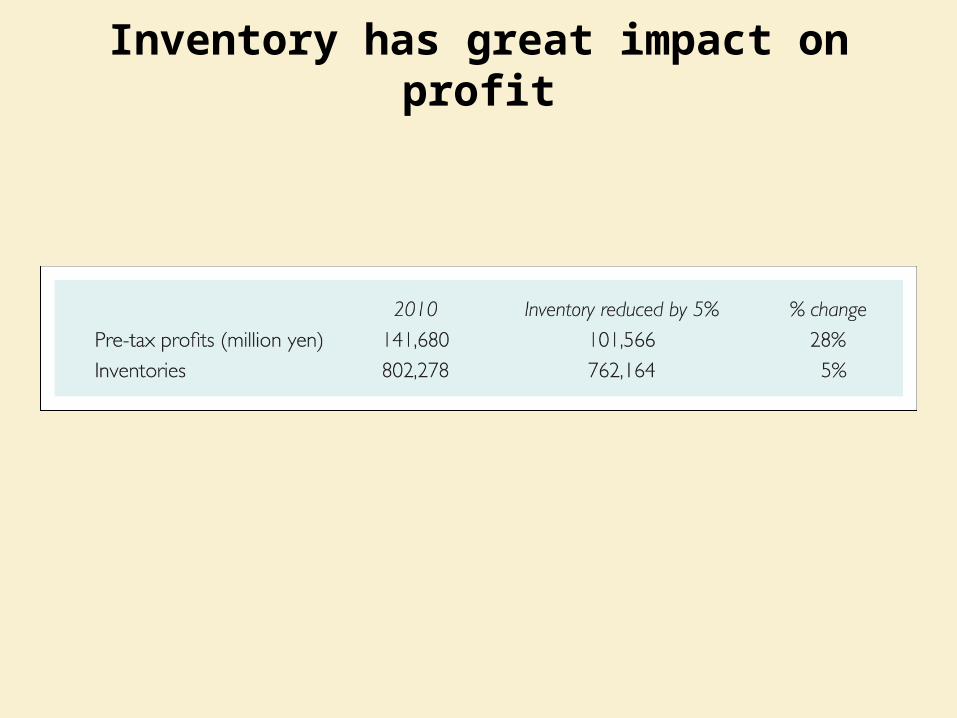

Inventory has great impact on profit

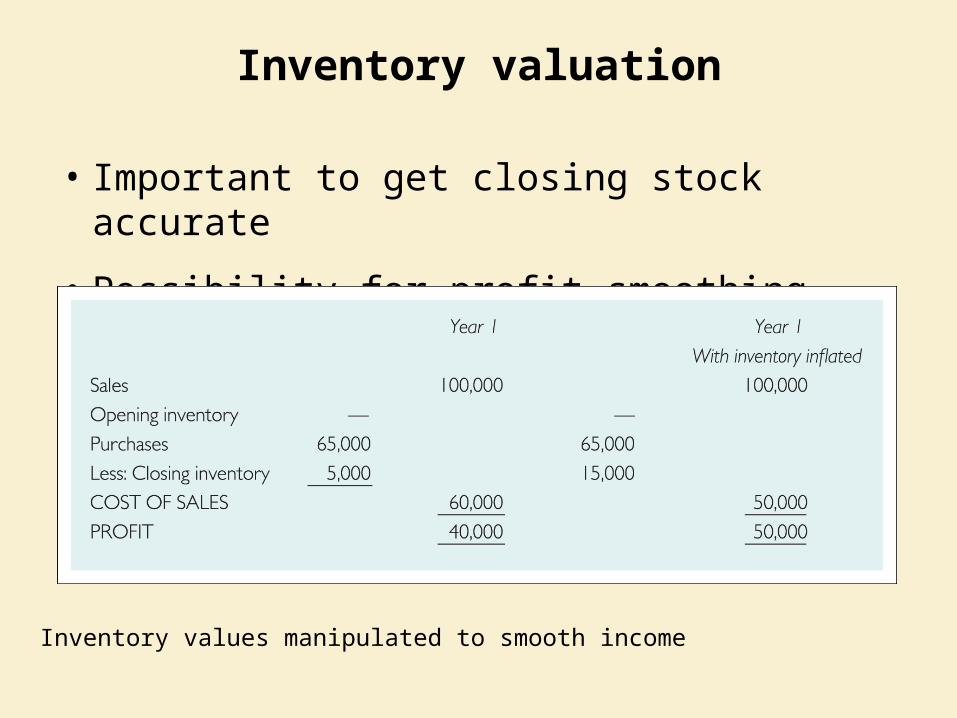

Inventory values manipulated to smooth income

Inventory valuation

• Important to get closing stock accurate

• Possibility for profit smoothing.

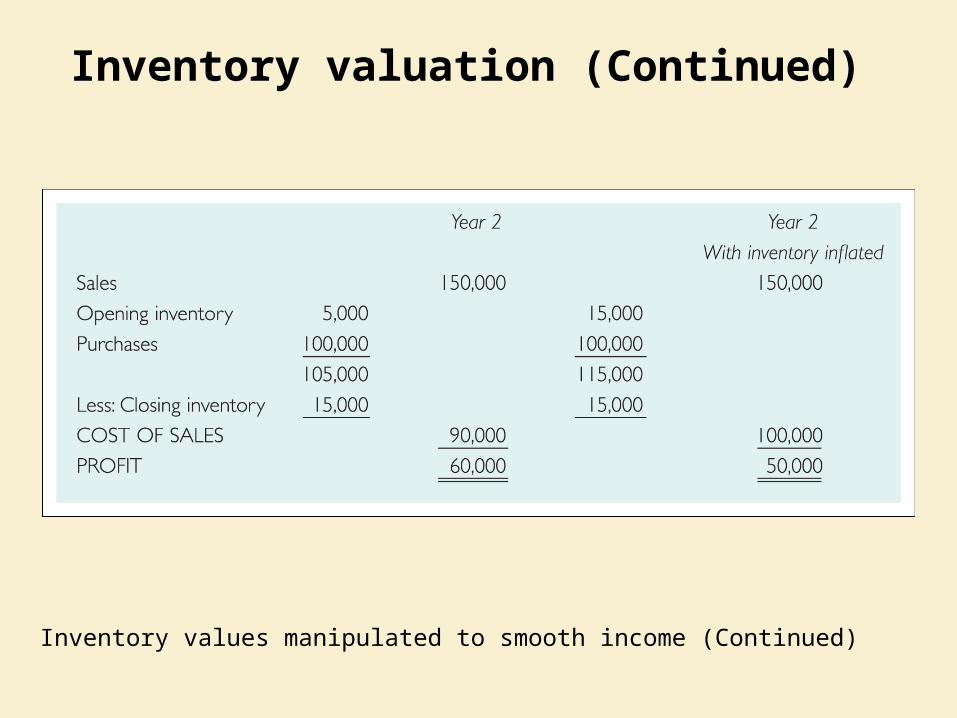

Inventory valuation (Continued)

Inventory values manipulated to smooth income (Continued)

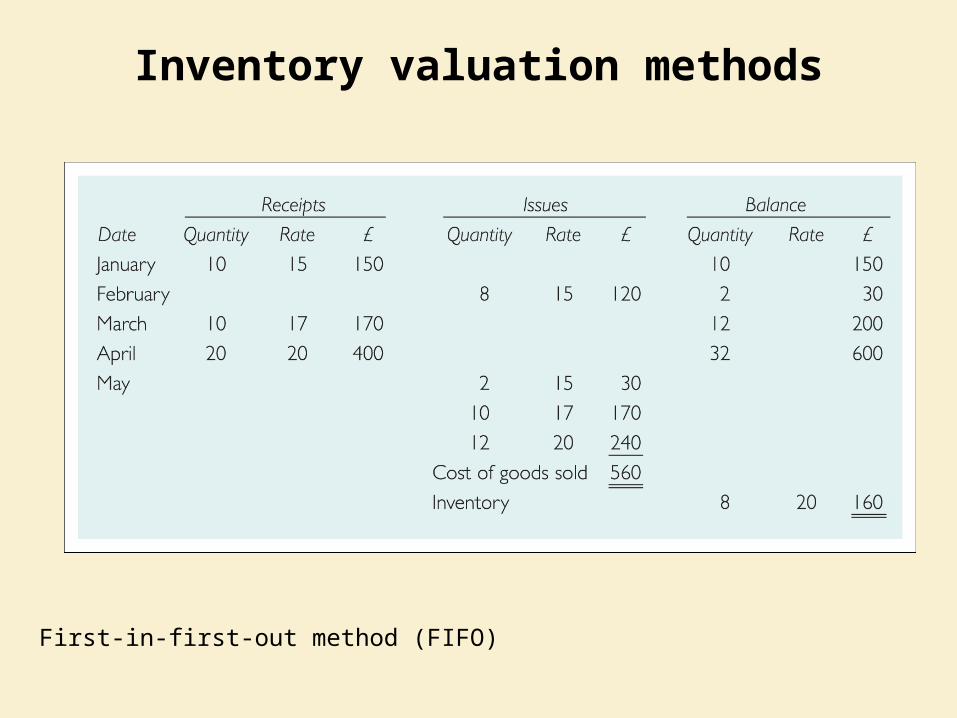

Inventory valuation methods

First-in-first-out method (FIFO)

Inventory valuation methods (Continued)

Average cost method (AVCO)

Methods rejected by IAS 2

LIFO and (by implication) replacement cost are rejected by IAS 2.

Last-in-first-out (LIFO)

• The cost of the inventory most recently received is charged out first at the most recent ‘cost’, that is the inventory value is based upon an ‘old cost’, which may bear little relationship to the current ‘cost’.

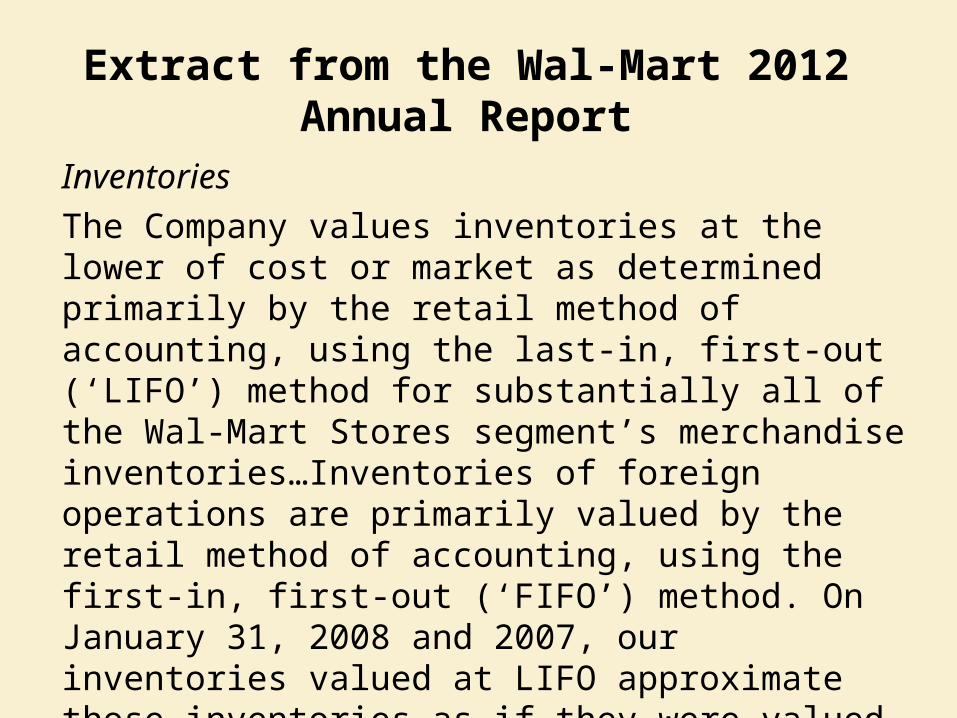

Extract from the Wal-Mart 2012 Annual Report

Inventories

The Company values inventories at the lower of cost or market as determined primarily by the retail method of accounting, using the last-in, first-out (‘LIFO’) method for substantially all of the Wal-Mart Stores segment’s merchandise inventories…Inventories of foreign operations are primarily valued by the retail method of accounting, using the first-in, first-out (‘FIFO’) method. On January 31, 2008 and 2007, our inventories valued at LIFO approximate those inventories as if they were valued at FIFO.

Last-in-first-out

Procedure to ascertain cost

• Direct material• Direct labour• Appropriate overhead

Five types of overhead

1.Direct–Subcontract, royalties

–Non-routine subcontract might be expensed.

2.Indirect –Factory rent, rates

–Power

–Depreciation of plant and machinery

–Warehouse cost of finished goods.

Five types of overhead (Continued)

3.Administration – Office costs easily identifiable to production– Apportion wages department on head count– Production-specific admin – canteen.

4.Selling and distribution – Advertising, delivery, sales salaries – Not normally included in inventory valuation – Sale or return basis incurs delivery costs– Included in inventory valuation.

5.Finance– Cost of borrowing, fees for letters of credit– May be a case for including in inventory.

How much of total overhead to include

• Important to use normal activity basis.

Numerical example – normal activity

How much of total overhead to include (Continued)

Numerical example – normal activity (Continued)

Net realisable value (NRV)

• Prudence requires lower of cost and NRV– Permanent fall in market price

– Excessively priced stock

– High stock levels and liquidity problems

– Deteriorating

– Obsolescence

– Marketing strategy to penetrate a market.

Net realisable value (NRV) (Continued)

• Numerical example

Inventory control

• Problem when inventory is taken at different date to year-end

Adjusted inventory figure

Creative accounting

• Year-end manipulation– Ineffective cut-off procedures

– Suppression of invoices

– Window dressing

– Subjective use of NRV rule

– Load overheads onto inventory in low profit periods

– Optimistic view of obsolescence

– Inaccuracies in the physical inventory count.

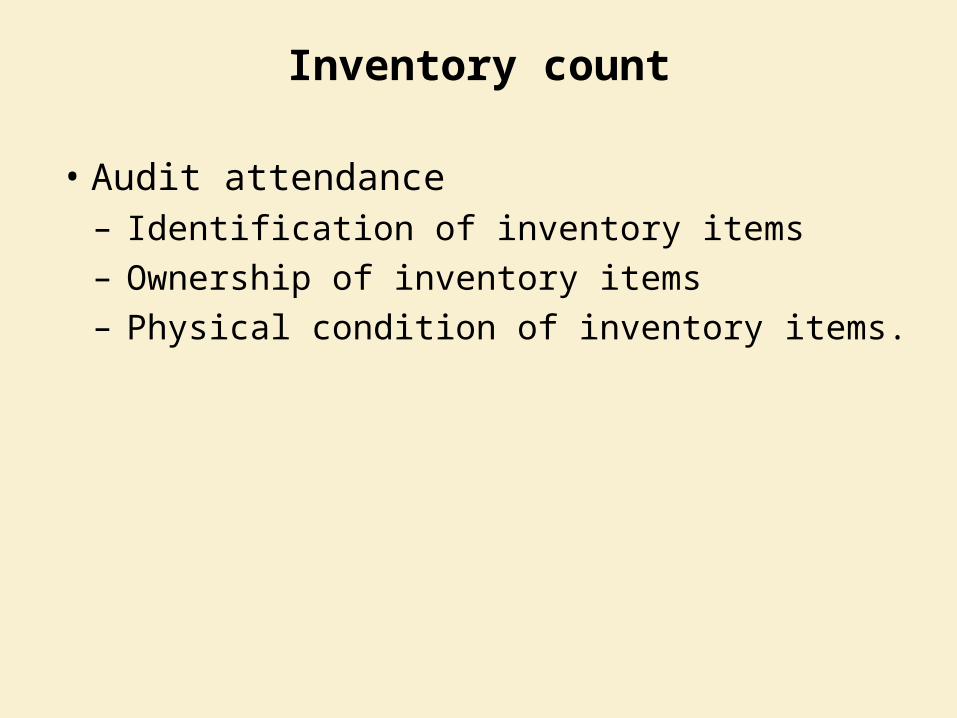

Inventory count

• Audit attendance– Identification of inventory items

– Ownership of inventory items

– Physical condition of inventory items.

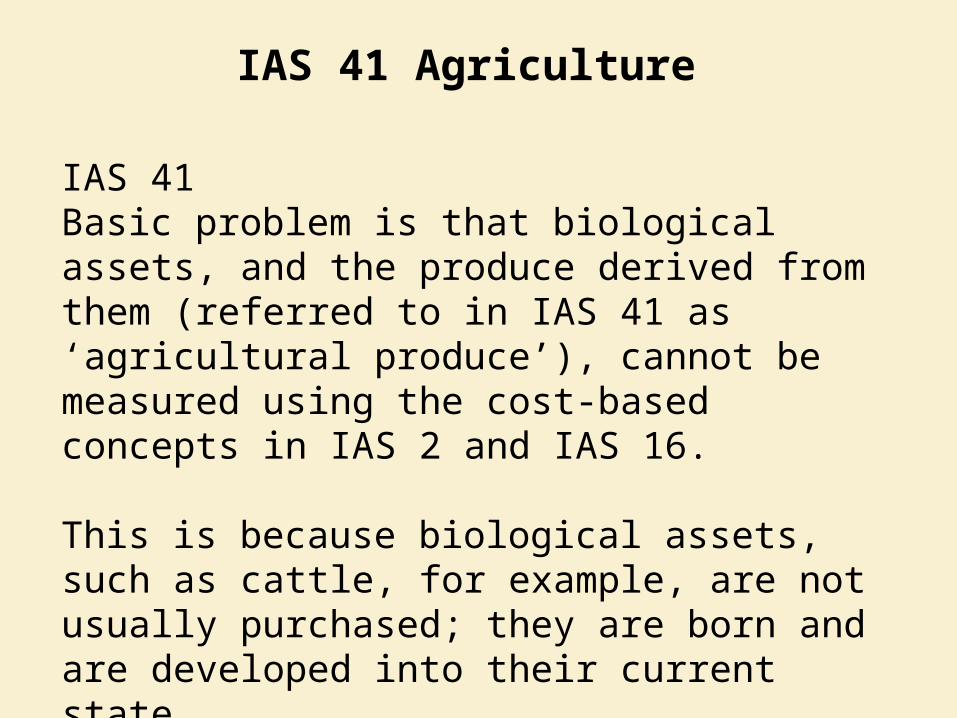

IAS 41Basic problem is that biological assets, and the produce derived from them (referred to in IAS 41 as ‘agricultural produce’), cannot be measured using the cost-based concepts in IAS 2 and IAS 16.

This is because biological assets, such as cattle, for example, are not usually purchased; they are born and are developed into their current state.

IAS 41 Agriculture

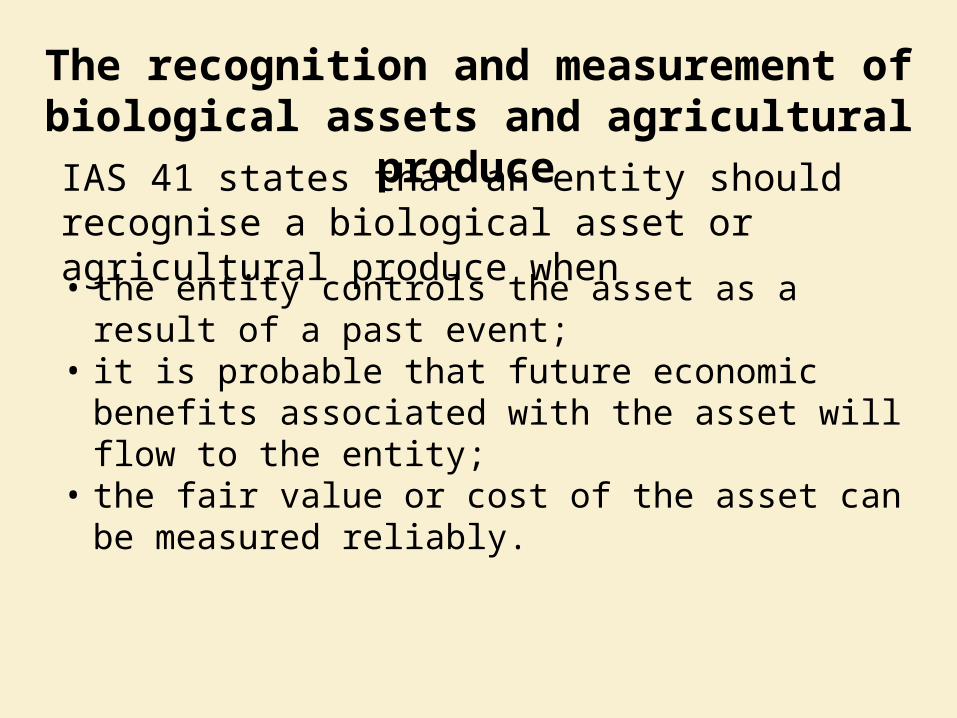

• the entity controls the asset as a result of a past event;

• it is probable that future economic benefits associated with the asset will flow to the entity;

• the fair value or cost of the asset can be measured reliably.

The recognition and measurement of biological assets and agricultural produce

IAS 41 states that an entity should recognise a biological asset or agricultural produce when

An illustrative example

A farmer owned a dairy herd. At the start of the period the herd contained 100 animals that were 2 years old and 50 newly born calves. At the end of the period, a further 30 calves were born. None of the herd died during the period. Relevant fair value details were as follows:

Start of period End of period $ $

Newly born calves 50 55One-year-old animals 60 65Two-year-old animals 70 75Three-year-old animals 75 80

Fair value at end of the year = (100 × $80) + (50 × $65) + (30 × $55) = $12,900

Fair value at start of the year = (100 × $70) + (50 × $50) = $9,500

The change in the fair value of the herd is $3,400, made up as follows:

An illustrative example (Continued)

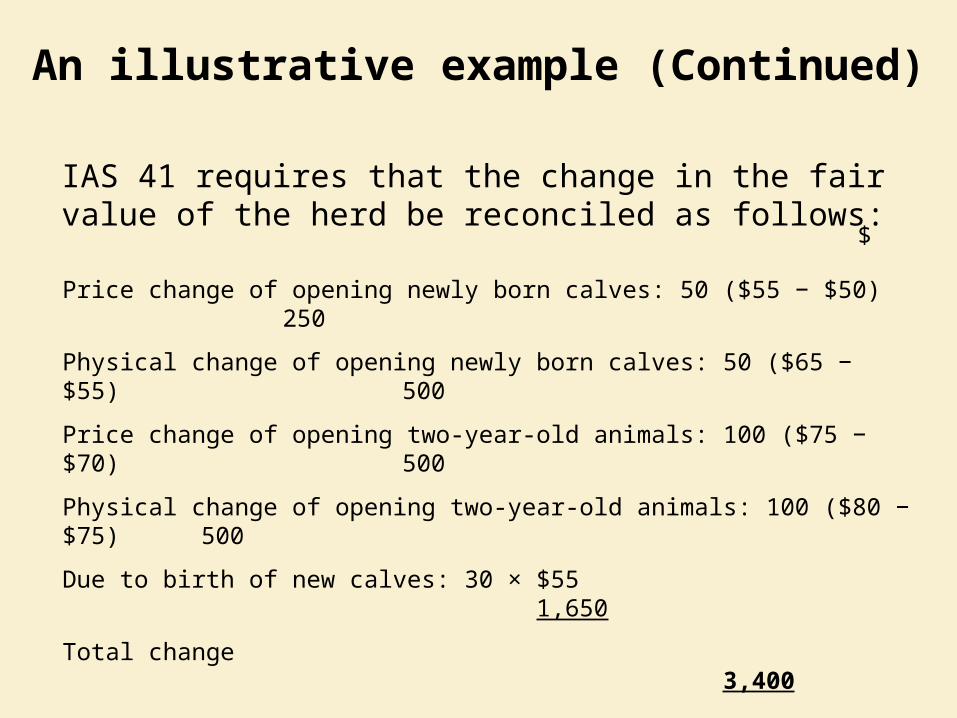

Price change of opening newly born calves: 50 ($55 − $50) 250

Physical change of opening newly born calves: 50 ($65 − $55) 500

Price change of opening two-year-old animals: 100 ($75 − $70) 500

Physical change of opening two-year-old animals: 100 ($80 − $75) 500

Due to birth of new calves: 30 × $55 1,650

Total change 3,400

IAS 41 requires that the change in the fair value of the herd be reconciled as follows:

$

An illustrative example (Continued)

• End of Lesson

• Please complete all theory and practice questions