cover page for the project

TRANSCRIPT

i

COVER PAGE FOR THE PROJECT

REPORT – 5TH

SEMESTER:

Year: 2016

Semester: 5th

Project title: ENDRON: a case study of Enron’s collapse through the lens of organisational culture

Project supervisor: Jacob Dahl Rendtorff

Group no.: V16-BUSINESS-03A

Total number of characters: 161,431

Group members (full name and student ID No.):

Dominika Hajkova: 55453 Irtaza Zafar: 55011

ii

ENDRON:

A case-study of Enron’s collapse through

the lens of organisational culture

iii

Table of Contents

1. Introduction ....................................................................................................................... 5

1.1 Reading guide ............................................................................................................................ 5

1.2 Project motivation ...................................................................................................................... 6

1.3 Literature review ........................................................................................................................ 7

1.4 Problem area .............................................................................................................................. 9

1.5 Research Question.................................................................................................................... 11

1.6 Sub-questions ........................................................................................................................... 11

1.7 Contextualisation ..................................................................................................................... 12

2. Methodology ..................................................................................................................... 14

2.1 Data collection and research strategy....................................................................................... 14

2.2 Theory and research ................................................................................................................. 14

2.3 Epistemology ........................................................................................................................... 15

2.3.1 Positivism, realism and interpretivism ........................................................................................... 15

2.4 Hermeneutics ........................................................................................................................... 17

2.5 Ontology................................................................................................................................... 18

2.5.1 Objectivism and subjectivism ......................................................................................................... 18

2.6 Case study ................................................................................................................................ 19

2.7 Delimitations of research ......................................................................................................... 21

3. Theoretical framework ................................................................................................... 22

3.1 Levels of Cultural Analysis...................................................................................................... 22

3.2 Primary Embedding Mechanisms ............................................................................................ 24

3.3 The Competing Values Framework ......................................................................................... 25

3.4 Stakeholder theory ................................................................................................................... 27

3.5 Utilitarianism and Egoism ....................................................................................................... 30

3.6 Sub-conclusion ......................................................................................................................... 34

4. Analytical Framework .................................................................................................... 35

4.1 Role of the leadership in shaping Enron’s culture ................................................................... 35

4.1.1 Enron Oil Scandal and response of the leadership ......................................................................... 35

4.1.2 Towards a change in culture ........................................................................................................... 37

iv

4.1.3 The new culture .............................................................................................................................. 40

4.1.4 Enron’s culture and the Competing Values Framework ................................................................ 42

4.1.5 Sub-conclusion ............................................................................................................................... 43

4.2 Stakeholders and the impact of Enron’s culture ...................................................................... 44

4.2.1 Stakeholder salience theory ............................................................................................................ 44

4.2.1 Enron’s culture and the salience model .......................................................................................... 44

4.2.2 Whistle blowers and Enron’s culture.............................................................................................. 46

4.2.3 The board of directors..................................................................................................................... 47

4.3 Unethical actions promoted by the culture .............................................................................. 50

4.3.1 The California Crisis ...................................................................................................................... 50

4.3.2 Enron’s role in the California crisis ................................................................................................ 51

4.3.3 The use of Special Purpose Entities ............................................................................................... 54

4.3.4 The consequences of Special Purpose Entities ............................................................................... 56

4.3.5 Sub-conclusion ............................................................................................................................... 58

5. Discussion ......................................................................................................................... 59

6. Conclusion ........................................................................................................................ 62

7. Bibliography ..................................................................................................................... 64

5

1. Introduction

1.1 Reading guide

The following summary intends to provide an overview of the structure of this paper, in order to

make it easier for the reader to navigate throughout. Altogether, this paper consists of six main

chapter, and each chapter will be briefly described.

Firstly, the paper initiates with the motivation behind our chosen topic by explicating the

preliminary thoughts and interests which led to the focus of this research. This is followed by the

literature review which aims to explain the fundamentals of the topic, organisational culture. This

leads to the problem area, which describes the problem to be investigated in this paper.

Subsequently, the research question and sub-questions are presented.

Secondly, the methodology chapter aims to present the reader with the methods applied in this

paper. This includes the research strategy, epistemology and ontology, and interpretative method, as

well as the limitations this paper has encountered. In the subsequent chapter, theoretical framework,

the five theories which have been incorporated are introduced and their relevance is explained. The

chapter aims to provide a theoretical framework through which to conduct the analysis.

Thirdly, the analytical framework of this paper constitutes of three sub-questions and is, therefore,

divided into three chapters. By applying the theories, the three sub-questions are analysed with the

purpose of answering the research question. Thereafter, the arguments put forth in the analysis are

summarised in the discussion chapter. Lastly, the research question is attempted to be answered in

the concluding chapter, in which the arguments presented throughout the paper are also summed up.

6

1.2 Project motivation

The chosen topic of this paper is based on an interest in the subject of business studies. The research

area of this paper is inspired by the overall topic of corporate bankruptcies, and has emerged from

cases which have occurred in the last two decades, such as the Lehman Brothers, WorldCom and

Enron. What all these cases have in common is their use, or rather misuse, of certain accounting

principles and methods; unethical and illegal activities, which ultimately led to committing fraud.

However, what brought us to question is the factor(s) leading to such behaviour.

It seemed significant to explore how values and beliefs are formed in an organisation, which result

in disastrous consequences. This brought us to the topic of organisational culture. After further

research on the topic, we came to the assumption that the culture of an organisation has a

considerable impact on its operations and performance, and that the leadership plays an important

role in shaping the culture. It seems that culture and leadership are intertwined. Furthermore, there

appears to be a connection between culture and the collapse of an organisation. Accordingly, we

developed a hypothesis that the downfall of an organisation can be explained, to a very large extent,

by analysing its culture, which is ultimately shaped by the values and beliefs of the leadership. In

this regard, and to test the hypothesis, we have opted for Enron as a case study.

7

1.3 Literature review

In order to support our hypothesis, this section intends to review the literature on the topic of

organisational culture. Additionally, reviewing the literature will also explain what organisational

culture is, and its importance in an organisation.

The word “culture” originates from social anthropology. It represents the qualities of any particular

group which are passed on to the next generation (Hasnan et. al. 2015: 367). Culture indicates the

values shared by the members of a group which persist even when the existing members leave and

new members join the group (Hasnan et. al. 2015). According to O'Donnell and Boyle (2008),

“...the concept of culture is the climate and practices that organisations develop around their

handling of people, or to the promoted values and statement of beliefs of an organisation.”.

Organisational culture is the behaviour of humans within an organisation and the meaning which

the members associate to those behaviours (Hasnan et. al. 2015). Culture provides an organisation

with a sense of identity and determines, based on various beliefs and values, the manner in which

““things are done...”” (O'Donnell and Boyle 2008).

According to Schein (2004: 1), organisational culture is created, embedded, evolved, and ultimately

manipulated, and provides stability, structure, and meaning to an organisation. Schein (2004: 8)

argues that “culture is to a group what personality or character is to an individual.”. Schein (2004)

also notes that the leadership of an organisation has a huge impact on the formation and

development of its culture; thus, they are two sides of the same coin. By imposing their own values

and assumptions on a group, which ultimately turn out to be successful, the leadership creates a

culture which defines for the next generation the kinds of leadership that are acceptable; thus, the

culture defines leadership (Schein 2004). The leadership is also responsible of bringing a change in

the culture once the organisation faces adaptive difficulties. Thus, Schein (2004: 11) articulates that

“the only things of real importance that leaders do is to create and manage culture; that the unique

talent of leaders is their ability to understand and work with culture; and that it is an ultimate act of

leadership to destroy culture when it is viewed as dysfunctional.”. However, Kotter (2008) argues

that culture can be very difficult to change because the members, of a group or organisation, are

often oblivious to the values which form the core foundations of their culture.

The shape which a culture may take depends to some extent on the organisations’ objectives. What

is important to achieve varies from organisation to organisation. Different companies value

different objectives, such as making money, technological advancements or the well-being of their

8

members (Hasnan et. al. 2015: 367). Regardless of their differences in goals, focus, and

terminology, one thing which all organisations have in common is that they have a culture, and

some have a “stronger” culture than others (Hasnan et. al. 2015: 367). Culture can, substantially,

impact individual members and their performance in an organisation, especially when an

organisation has a competitive environment. This impact, Hasnan et. al. argue (2015), may be

greater than factors such as strategy, organisational structure, management systems etc., which are

frequently discussed in the organisational and business literature. Culture can be measured in terms

of its strengths and weaknesses; and efficiency and inefficiency. Dellaportas et. al. (2007) note, that

a strong and efficient culture influences members’ behaviour in order to become compatible with

the organisations’ values and fulfilment of its goals and strategies. Such a culture is more likely to

effectively achieve goals and strategies, whereas an inefficient and weak culture is less likely in

achieving such efficiency. An inefficient and weak culture can lead to “...jeopardising the survival

of the organisation.” (Dellaportas et. al. 2007).

According to Hasnan et. al. (2015), as well as Schein (2004), the culture of an organisation is

increasingly important and the employees are inspired by the top leadership. This is due to the fact

that the character of the leadership is ultimately reflected in the character of the entire organisation

(Hasnan et. al. 2015). Thus, if the leadership is known for its integrity, it will reflect in the

organisation. On the contrary, if the leadership is more keen to generate short-term profits, by all

means, the members of the organisation will also follow that objective (Hasnan et. al. 2005). Hence,

Dellaportas et. al. (2007) argue that exploiting organisational culture can have destructive effects on

the organisation as a whole, such as unethical and illegal behaviour and fraud.

Based on the reviewed literature, it can be argued that the culture and leadership of an organisation

are certainly interconnected. It is the leadership which shapes and maintains the culture; hence, it is

also their responsibility to ensure that the culture of the organisation is not one which promotes

unethical behaviour, illegal activities and fraud. The literature on Enron (Cohan 2002; Cornford

2006; Cruver 2003; Dembinski et. al. 2006; Gibney 2005; Moncarz et. al. 2006; Murthy and Gore

2011; Thomas 2002) indicates that the leadership formed a certain culture in which ethics was

disregarded, and it was ultimately the culture which led to Enron’s collapse.

9

1.4 Problem area

Enron as a case of organisational culture paints a holistic picture of the importance of organisational

culture and how its misuse can lead to terrible consequences. Having been selected for six

following years as the “America’s most innovative company” (Fortune.com 2001), the post-scandal

Enron fell into a rapid bankruptcy, that came to be known as one of the largest corporate

bankruptcy in the history of the United States (Dobson 2006). As the investigations on Enron’s

financial conditions proceeded, it was demonstrated that Enron was systematically cheating their

financial reports and accounting in order to meet their planned revenues and increase their stock

prices (Cornford 2006). Corporate bankruptcy, however, is not what sets Enron apart from other

cases; Enron’s total assets were valued at $61 billion (Haberly 2002: 4), whereas the largest

bankruptcy, the Lehman Brothers Holdings in 2008, peaked at around $639 billion USD in total

assets (Adu-Gyamfri 2016: 133). What sets Enron apart from other corporate bankruptcies of this

extent is its particular organisational culture, which is described as being arrogant, extremely

decentralised and risk-taking, while still being very innovative and progressive (Gore and Murthy

2011).

Enron had a difficult start after it was formed in 1985 as a “bricks-and-mortar energy business”

(Partnoy 2006: 64). However, due to the deregulation of energy markets, which came into effect in

1980s in the US, Enron shifted their specialisation to become an energy supplier and, more

importantly, started trading natural gas as a commodity on their platform called the Gas Bank,

which proved to be very successful (Cornford 2006). In the years following 1991, Enron shifted

their business plan, as the market trends were changing, with the idea that innovation will help

increase their stock price. Therefore, when the Internet started gaining more importance during the

Internet boom in the late 1990’s, Enron decided to create an online trading platform, called Enron

Online (Partnoy 2006). Moreover, Enron still invested in several countries around the world, where

it was primarily building and operating energy sites (Cornford 2006).

The stock market was on a rise during the 2000’s and everyone, including the working-class, started

investing into various stocks, as they kept growing and increasing in price, and no one expected

them to fail. Enron’s stock price was on a steady rise in the 1990’s; however, the most interesting

increase happened in the last six years before their bankruptcy (Blommestein 2006). The dot-com

bubble, or the Internet bubble, crashed soon after NASDAQ index hit their famous 5000 in the early

2000’s. Even though the dot-com bubble uncovered mainly overpriced technological stocks, it

10

showed the possibility of overvaluation and general lower interest in investing, which moved Enron

one step closer to their bankruptcy (ibid).

Prior to their bankruptcy, from 1996 to 2001, Enron was not only consecutively selected the most

innovative company by Fortune500 but, together with its board members, was considered as the

hero of Wall Street and a shining example of a perfect American corporation (Dobson 2006). Enron

was flourishing, everyone wanted to work for it, not just because of its good salaries, promised

retirement funds and other rewards, but also because of its competitive organisational culture which

appealed to a lot of people (ibid).

Enron’s organisational culture, mainly described as a sick culture, extremely risk-taking,

competitive, and inconsiderate, also helped form a certain attitude, convincing its members that

Enron was capable of anything. In this culture, the code of ethics was merely a facade and profit

became the only benchmark (Gore and Murthy 2011).

Enron’s employees were one of the best from the country, especially after Enron established one of

the toughest employee-ranking system in the country, known as the Performance Review

Committee (PRC). As a consequence of the PRC, Enron fired some 15% of its workers annually,

with the worst performance rating (ibid). This made Enron’s organisational structure and culture

very unusual, and interesting, as according to Schein (2004) and other researchers, organisational

culture is one of the most influential factor in an organisation. Another striking aspect of Enron’s

culture was its ethical considerations towards their stakeholders. The fact that Enron’s shareholders

lost close to $11 billion due to its bankruptcy, without being aware that Enron was internally

collapsing, is neither ethical nor legal (Benston 2003).

As such it becomes relevant to examine the organisational culture of Enron in relation to their

apparent strong growth and increasing power over the years, before their corporate fraud became

public knowledge. The literature on organisational culture indicates that perhaps Enron’s culture is

to blame, to a large extent, for their bankruptcy as it led to taking specific actions, ethical or

unethical, and therefore it becomes relevant to examine the reasons behind these actions. However,

as the culture is formed and changed by the leadership of an organisation, it becomes significant to

examine the Enron’s leadership and their impact on the culture. Moreover, the project will examine

different stakeholders, their importance for the management in relation to the organisational culture,

and the impact the culture had on them.

11

To verify or denounce the hypothesis: “the collapse of Enron was caused by its culture as it,

among other things, promoted unethical and illegal actions”, the paper attempts to answer the

following research question, assisted by three sub-questions.

1.5 Research Question

With a focus on the role of its leadership, how can Enron’s organisational culture explain its

collapse?

1.6 Sub-questions

1. What role did Enron’s leadership play in shaping its organisational culture and how can it be

characterised?

2. With a focus on the stakeholders, what impact did Enron’s culture have?

3. How did this culture promote unethical actions and what consequences did they have?

12

1.7 Contextualisation

Enron was founded in 1985 by Kenneth Lay with the purpose of producing and supplying natural

gas. It was founded as a result of a merger between InterNorth Inc. and the Houston Gas Company

(Gore and Murthy 2011: 8). The foundation of Enron was that of an ordinary natural gas firm,

relying on traditional methods of drilling, which made it unappealing to the stock market (Gore and

Murthy 2011: 8). In pursuance of survival and becoming more attractive, Kenneth Lay developed a

new business strategy with the help of an external consulting firm, Mckinsey and Company. In

1990, Jeffrey Skilling, a young consultant with a background in asset and liability management and

banking, was hired by Kenneth Lay in order to implement the new strategy (Thomas 2002: 42).

Skilling premeditated an innovative solution to increase Enron’s profits which was to create a

“bank” through which it would buy and sell gas. Skilling’s solution appealed to Kenneth Lay who

created a new division within Enron, run by Skilling, named Enron Finance Corporation. Within a

short period of time, the new division subjugated the natural gas market and as a result generated

immense profits (Thomas 2002). Due to the immense success of Enron Finance Corporation,

Jeffrey Skilling was appointed President and Chief Operating Officer of the entire Enron

corporation (US District Court 2004: 3).

Subsequently, establishing a compact base in natural gas led Enron to expand its business by

becoming a financial trader and market maker in broadband fibre optic cable capacity, water, paper

and pulp, steel, coal and electric power (Moncarz et. al. 2006: 19). These trading activities made

Enron very innovative and the results were positive as Enron became the seventh largest

corporation in the US (Moncarz et. al. 2006: 19).

What started out as an energy-producing company now became an energy trading company. The

transformed image of Enron as a trading corporation led Jeffrey Skilling to amend the

organisational culture of Enron (Thomas 2002: 42). According to an official document of US

District Court of Texas Houston Division:

“SKILLING closely supervised on a day-to-day basis the activities of each of Enron’s business units

and the heads of those business units, as well as the activities of the senior Enron managers who

conducted the company’s financial and accounting activities.”

(US District Court 2004: 3)

The organisational culture of the company endured some dramatic changes. According to Skilling,

“Our culture is a tough culture. It is a very aggressive, very urgent organisation.” (Gore and Murthy

13

2011: 19). Skilling started hiring top traders from MBA schools throughout the country and

competed with respected investment banks for talented recruits. The employees faced exhausting

work hours; however, this came with its advantages. Skilling indulged in various services and

rewarded the members with merit-based bonuses with no limits, allowing them to “… “eat what

they killed”” (Thomas 2002: 42).

Additionally, Skilling established one of the toughest employee-ranking system in the

country, known as the Performance Review Committee (PRC), which was based on four core

values of Enron – respect, integrity, communication and excellence (known as RICE) (Thomas

2002: 42). The employees were rated on a scale from 1-5, with 5 being the worst performance. The

higher the PRC score, the closer the employee got to being fired, whereas a lower score was

favoured by Skilling. Despite the measure of the PRC score being based the above-mentioned

values, employees were only really measured on the profits they were able to produce for the

company. The introduction of the PRC led Enron to replace the lowest 15% of its employees

(Thomas 2002: 42). Furthermore, as a result of the PRC, there was aggressive competition and

paranoia and secrecy became order of business for the majority of the employees (Thomas 2002:

42). Moreover, employees were reluctant in expressing their opinions or question potential illegal

practices as it could lead to severe consequences from the leadership (Gore and Murthy 2011: 21).

Skilling transformed Enron’s organisational culture into one that was arrogant, extremely

decentralised and created an attitude that Enron was capable of anything.

14

2. Methodology

The purpose of this chapter is to explain the methodological approaches incorporated in this paper.

The chapter initiates by explaining the method used to collect and analyse data. It then describes the

different epistemological and ontological assumptions and identifies the assumptions applied in this

paper. It also discusses the use of hermeneutics and case study, both approaches which are applied

in this paper.

2.1 Data collection and research strategy

Data collection is a key aspect of any research paper and can be collected through two different

research strategies; intensive and extensive. These research strategies are related with the terms

qualitative and quantitative research, where intensive research can be described as qualitative and

extensive research can be described as quantitative (Bahari 2010: 18). There are some key

differences in qualitative and quantitative research such as: research questions, methods of data

collection, limitations of the research and how the objects are defined (Bahari 2010: 19). According

to Bryman (2004: 266), qualitative research has an emphasis on words whereas quantitative

research emphasises quantification in the collection and analysis of data. In contrast to quantitative

research, where the researcher makes knowledge claims based on post-positivist claims, qualitative

researchers use constructivist perspectives in order to develop knowledge (Bahari 2010: 18).

Furthermore, different strategies are applied in qualitative and quantitative research. A qualitative

research design involves strategies such as phenomenologies, ethnographies, grounded theory

studies or case studies. On the contrary, a quantitative research design uses predetermined

instruments in data collection in order to produce statistical data, experiments and surveys (Bahari

2010: 18-19).

This paper can be described as qualitative in nature. The paper does not use quantitative research

strategies, such as experiments, but uses a qualitative strategy; a case study.

Qualitative and quantitative research differs in other aspects as well than just data collection.

Bryman (2004: 19) distinguishes qualitative and quantitative research through three main aspects;

the connection between theory and research, epistemology and ontology.

2.2 Theory and research

There are two primary approaches through which theory and research can be connected; deductive

and inductive. A deductive approach is applied in a quantitative research whereas an inductive

15

approach is applied in a qualitative research approach (Bahari 2010: 19-20). Bryman (2004: 8)

defines a deductive approach as “…an approach to the relationship between theory and research in

which the latter is conducted with reference to hypotheses and ideas inferred from the former.”

According to this definition, the research initiates with the theory which becomes a framework for

the entire study (Bahari 2010: 21). On the contrary, an inductive approach initiates with collecting

data to explore a problem which in turn leads to the development of a theory (Saunders et. al. 2012:

145). When applying an inductive approach, the researcher collects data in order to develop themes

which are, in turn, developed into broad patterns, theories, or generalisations (Bahari 2010: 19-20).

This paper applies the collected data through an inductive approach. It initiates with collecting data

on organisational culture which is developed into themes and are in turn developed into broad

patterns, theories and generalisations. Subsequently, data is collected on the case of Enron to

analyse the developed broad patterns, theories and generalisations.

2.3 Epistemology

There are a variety of epistemological assumptions. According to Saunders et. al. (2012: 132)

epistemology is a theory of knowledge, and is concerned with what creates acceptable knowledge in

a field of study. Epistemological assumptions can be considered to be associated with the nature of

knowledge and the methods by which that knowledge can be attained. Epistemology can also be

considered a question of what is or should be viewed as acceptable knowledge in a field of study

(Bahari 2010: 22). There are three main epistemological assumptions; positivism, realism and

interpretivism.

2.3.1 Positivism, realism and interpretivism

Positivism assumes that there are social facts with an objective reality apart from an individuals’

beliefs (Bahari 2010:22). The philosophy of positivism reflects the philosophical posture of the

natural science in the sense that data is collected about an observable reality to search for

regularities and causal relationships in the data to create law-like generalisations (Saunders et. al.

2012:134). Positivists argue that the social world exists externally and research should be

undertaken, as much as possible, in a value-free way, i.e. the researcher must be independent and

the research conducted with objective methods (Bahari 2010: 23). The research methodologies of

positivism are similar to those of natural science, such as, use of statistics, surveys and

questionnaires (Bahari 2010: 23).

16

Realism is another philosophical stance which is similar to positivism as both take a scientific

approach in order to develop knowledge. There are two forms of realism; direct and critical realism

(Saunders et. al. 2012: 136). According to direct realism, what one sees is what one get. This means

what we experience through our senses depicts the world accurately. On the contrary, critical

realism argues that one does not see things directly, rather what one sees are sensations or images of

the real world (Saunders et. al. 2012: 136).

According to Saunders et. al. (2012: 136), direct and critical realism are important in

relation to the pursuit of business and management research. Direct realism would argue that the

world is relatively unchanging and operates, in the business context, at only one level (the

individual, the group or the organisation). In contrast to direct realism, critical realism argues the

importance of multilevel study (at the level of the individual, the group and the organisation), which

is relevant in terms of business (Saunders et. al. 2012: 136-37). The multilevel study is capable of

changing the researchers’ understanding of that which is being studied. On this basis, Saunders et.

al. (2012: 137) argue that critical realism’s position, that the social world is in a constant state of

change, is much more in line with business and management research. Nevertheless, Saunders et. al.

(2012: 137) note that the social world of business and management is too complex to be theorised

by definite laws and law-like generalisations, as the natural sciences.

Unlike positivism and realism, interpretivism promotes the necessity for the researcher to

understand differences between humans in our role as social actors (Saunders et. al. 2012: 137).

Bryman (2008) notes that interpretivism allows the researcher to perceive social actions through a

subjective meaning. Interpretivists consider facts and values to be similar and the researchers’

values and perspective influence the results and conclusions (Bahari 2010: 22). Interpretivist

researchers are considered “feeling” researchers due to their role as “social actors”, where they

could interpret their social roles in line with the meaning given to these roles and interpret the social

roles of others in accordance with their own set of meanings (Bahari 2010: 22).

Interpretivism is related to the intellectual tradition of phenomenology. Phenomenology

refers to the question of how humans make sense of the world around them (Saunders et. al. 2012:

137). According to Bahari (2010: 22), “the concept of phenomenology concerns on how researchers

view social phenomena as socially constructed, and is mainly related with creating meanings and

obtaining insights into those phenomena.” Interpretivist philosophy argues that adopting an

empathetic stance as a researcher is crucial. This is because the researcher must enter the social

17

world of the research topic and try to understand their world from their perspective (Saunders et. al.

2012: 137).

As business and management research is a set of circumstances and individuals, an

interpretivist approach is highly suitable, predominantly in business topics such as organisational

behaviour, marketing and human resource management (Saunders et. al. 2012: 137).

Consequently, the epistemology of this paper is interpretivism. This is due to a number of factors.

Firstly, the paper is based on a qualitative approach and excludes surveys, questionnaires and

interviews. Secondly, the research topic of this paper, being organisational culture, can to a very

large extent be characterised within the epistemology of interpretivism. An organisational culture is

comprised of and affected by the social actors involved in the culture. Lastly, it can be argued that

applying positivism or realism to this research topic is not preferable due to their association with

the philosophical stance of the natural sciences.

2.4 Hermeneutics

Since the epistemology of this paper is interpretivism, it becomes relevant to use the hermeneutic

approach, which is defined as ““the science of interpretation”” (Cole et. al. 2011: 145). The use of

hermeneutics approach is acknowledged as a research methodology by marketing academics and is

used for qualitative studies (Wright and Losekoot 2012: 419-420). Hermeneutics has its origins in

the interpretation of ancient texts, particularly Biblical texts (Noorderhaven 2000: 8), in order to

understand them (Cole et. al. 2011: 145). However, the scope of hermeneutics has extended to

include all human behaviour/action and its consequences (Cole et. al. 2011: 145). The

understanding of these consequences arises from interpretation which is instilled with the

experience of the interpreter as they commemorate the past through the information available to

them (Cole et. al. 2011: 145). The hermeneutics approach attempts to relate text to context and

seeks to answer what happened rather than why it happened (Wright and Losekoot 2012: 420).

However, answering what happened is limited to the bounded rationality of the interpreter, their

ability to understand the experiences of the ones being observed, and their inability of not letting

own prejudices and experiences result in a subconscious bias when interpreting (Wright and

Losekoot 2012: 420).

Hermeneutics approach is relevant to apply in this project because the majority of data collected

on the chosen case-study is qualitative and historical, in that the event occurred almost two decades

ago. When analysing, we will ultimately understand the data as we interpret it. Therefore, we will

18

understand as to what happened with Enron’s culture from within the organisation. This

interpretation of the data, together with the analysis, will enable us to draw final conclusions.

2.5 Ontology

Where epistemology is concerned with what constitutes acceptable knowledge, ontology is

concerned with the nature of reality and raises questions of the assumptions the researcher has about

how the world operates (Saunders et. al. 2012: 130). According to Bryman (2004: 16), ontology is a

theory of the nature of social entities. In other words, ontology is about the nature of the world;

what entities it consists of and how they correlate to each other (Bahari 2010: 23). When conducting

a qualitative research, the researchers are aware and accept the notion of numerous realities rather

than a single reality. There are two main ontological assumptions: objectivism and subjectivism.

2.5.1 Objectivism and subjectivism

Objectivism assumes that social entities exist external to and independent of social actors (Saunders

et. al. 2012: 131). Some researchers emphasise that the goal of social science is to determine

probable reality as objectively as possible, and, thus, promote the notion that social science research

may adopt natural sciences methods, especially the use of statistics and numbers to measure the

relationship between categories (Bahari 2010: 25). Subsequently, it can be said that research based

on a quantitative strategy may use objectivism as the ontology.

The other ontological assumption is subjectivism. Subjectivism emphasises the notion that social

phenomena are created from the perceptions and subsequent actions of the social actors involved; a

continual process which is in a constant state of improving and revising (Saunders et. al. 2012:

132). Objectivism is often associated with constructionism – a view that reality is socially

constructed by the actors involved.

Organisational culture can be viewed through the ontological assumptions of subjectivism and

objectivism. Objectivists would argue that the culture of an organisation is given or something it

“has” (Saunders et. al. 2012: 132). On the contrary, subjectivists would argue that an organisations’

culture is what the organisation “is” due to the process of continuing social enactment. Some

organisational theories, such as management theory, consider organisational culture as objective; a

variable which can be manipulated to fit with the manager’s desires. Subjectivists would argue

otherwise, as they view culture which is created and recreated through social interaction between

the actors and the impact of physical elements to which individuals ascribe certain meanings, myths

and rituals (Saunders et. al. 2012: 132). Therefore, according to subjectivism, it is important to

19

understand these ascribed meanings in order to understand the culture of an organisation. Saunders

et. al. (2012: 132) argue that it is possible to incorporate both ontological assumptions in order to

understand the culture of an organisation.

The ontology of this paper can therefore be described as both objective and subjective, seeing that

the culture of Enron was something it “had” as well as something which was created as desired by

the leadership.

2.6 Case study

Case study is one of the research methods which is primarily used when conducting a qualitative

research. It can be considered a practical demonstration of theory; an approach of practical studies

of particular cases which makes knowledge more accurate (Rendtorff 2015: 37). A quantitative

research, on the contrary, lacks in providing complete and in-depth explanations of the social and

behavioural problems, emphasising the use of a case study as even more useful. The use of a case

study enables the researcher to transcend quantitative results and explain social actions through the

perspective of actors involved (Zainal 2007: 1). Case studies provide a holistic and in-depth

investigation of a specific topic (Zainal 2007: 1). Not only do case studies make theory useful and

meaningful but also provide the capability of operating in real life (Rendtorff 2015: 40). In business

terms, case studies contribute to an understanding of organisations as practical fields of actions that

reflect and exemplify theoretical problems (Rendtorff 2015: 41). Rendtorff (2015: 41) notes that

“...case analysis is concerned with the practical aspects of management, leadership, administration,

and ethics in organisations and business firms.”. Case analysis is hermeneutic - an approach applied

in this paper - as it contemplates meaning and action in practice (Rendtorff 2015). Case study and

hermeneutics are interconnected in the sense that a case study is concerned with dialogue,

understanding and communication (Rendtorff 2015: 42). In hermeneutics approach, text is

considered a model for action and to obtain an understanding of the structures of action, one

analyses the action as a text (Rendtorff 2015: 42). In this sense, a case study of an organisation can

be regarded as a text, which is written into a case, whereafter it is analysed, as a text, in order for

the interpreter to obtain a better understanding of alternative actions (Rendtorff 2015). According to

Max Weber (Rendtorff 2015: 45), the fundamental hermeneutics of a case study can be considered

the interpretative and understanding sociology, “...where social science first of all is about

understanding social phenomena and afterward about causal explanation from general laws because

20

social science is about understanding the structures of meaning of social phenomena as they

manifest themselves in the human social world.” (Rendtorff 2015: 45).

The scientific validity of case studies as hermeneutic has received a great deal of criticism. For

example, case studies are considered too abstract and unable to provide direct knowledge of reality

(Rendtorff 2015: 45). Additionally, case studies have been criticised as distant from the concept of

generality and universality of experimental natural sciences, i.e. case studies are not suitable for

making generalisation. Case studies are also considered as unscientific due to a lack of prospects of

truth and objective validity (Rendtorff 2015: 45).

Despite its criticism, Rendtorff (2015: 46) notes that a case study can very well be used to give

ideal-typical-knowledge as it describes the core structure of meaning which represents an

organisational phenomenon. Case studies can provide us with knowledge which has a high level of

universal affirmation, and divulge important facets of human life in organisations (Rendtorff 2015:

46). The structure of meaning that is disclosed through a case study demonstrates a horizon of

meaning and “the researcher can be said to enter into the horizon of meaning of the case and

thereby contribute to the description of the phenomenon that shows itself in the case…” (Rendtorff

2015: 47). Thus, according to Rendtorff (2015: 47), a hermeneutic approach case study is concerned

with the exploration of ideal-typical structures in the case which contributes to the profound

understanding of the structures and principles which form human social life in business

organisations.

Case studies can be used for various topics in a business context, such as ethics (Rendtorff 2015:

49). In doing so, the concepts of power and domination can be examined as well as other

management theories, for example knowledge management, project management or theories of

organisational culture (Rendtorff 2015: 49). Other issues which a case study, concerned with ethics,

can include are: the arrogance of businesses in relation to the environment, the importance of a code

of conduct, profit maximisation as a dictum for economic action, responsibility to shareholders

and/or employees, accounting ethics, and personal integrity versus organisational culture (Rendtorff

2015: 51-52).

This paper uses a single-case design as it analyses the culture of a single organisation, Enron. It is

primarily due to a time-constraint that this paper only makes use of a single-case. The use of a case

study in this paper can be considered a case-study in ethics, as it analyses the organisational culture

21

of Enron, which is believed to have led to the collapse of Enron because the culture promoted

unethical and illegal actions.

2.7 Delimitations of research

It is important to acknowledge the limitations of this paper. Firstly, this paper is solely based on a

qualitative research, in which most of the data collected is secondary and is applied through an

inductive approach. Some limitations of secondary data include: (i) the secondary data is most

likely collected for a purpose other than our research problem (thus aggregated in some way), (ii)

the data represents the interpretation of the producer, rather than an objective view, and (iii) the way

the data is presented in a document depends on the purpose of the document, thus it may not be

entirely relevant for other researches (Saunders et. al. 2012: 320). The paper could have made use

of conducting interviews with former Enron employees; however, it can be argued that this rather

exceeded our scope, both in terms of economic resources and due to time-constraint. Nevertheless,

for future research, a quantitative research may be conducted which collects first-hand data, i.e.

surveys, questionnaires, statistics etc., and applies it through a deductive approach. Alternatively, a

future research on this topic may also use abduction as a research approach, which is essentially a

combination of deduction and induction (Saunders et. al. 2012: 147). According to Saunders et. al.

(2012: 147), abduction initiates with the observation of a “surprising fact” and then works out a

conceivable theory of how this could have occurred.

Another limitation can be identified as the interpretative method used in this paper, a case study.

This is not a limitation in itself but rather, it is important to note that the validity of the research

could have been increased by using multiple case studies or by applying a triangulation of methods,

i.e. incorporating other methods.

22

3. Theoretical framework

The previous chapter identified the methods which are used to gather and apply data. The purpose

of this chapter is to discuss the theories which are applied to answer the research question.

3.1 Levels of Cultural Analysis

Culture is constantly present in our surroundings. It is endorsed and created by our interactions with

others and shaped by leadership behaviour, and a set of structures, routines, rules and norms that

guide and compel behaviour (Schein 2004: 1). Culture can be viewed as a concept which is present

within individuals but as we join other people, in an organisation or otherwise, new cultures are

created; thus, even on the individual level, culture is in a constant state of evolvement (Schein 2004:

8). On the organisational level, it is evident how culture is created, rooted, evolved and deployed

while constraining, stabilising and providing structure and meaning to the organisation’s members.

According to Schein (2004: 1), the creation and management of culture is at the heart of the

leadership and that culture and leadership are in fact interrelated. The leadership creates and

manages culture and can understand and work with the culture; however, once it becomes

dysfunctional, it is the leaderships’ responsibility to terminate the culture (Schein 2004: 1).

Culture provides a sense of group identity and structural stability. Once this is achieved, the

culture acts as a stabilising strength which members will be reluctant in giving up. Therefore,

culture is hard to change as it provides stability and identity (Schein 2004: 14). Culture is deeply

embedded, hence less visible, and covers all aspects of how an organisation handles its main tasks

and its internal actions (Schein 2004: 14). Culture is therefore defined as:

“a pattern of shared basic assumptions that was learned by a group as it solved its problems of

external adaptation and internal integration, that has worked well enough to be considered valid

and, therefore, to be taught to new members as the correct way to perceive, think, and feel in

relation to those problems.” (Schein 2004: 17).

In order to comprehend culture, it can be analysed on three levels; artefacts, espoused beliefs and

values and basic underlying assumptions.

Artefacts can be described as the surface of a culture. They include the observable products

of the organisation, such as the physical environment: language, technology and products, artistic

creations, style (as in clothing, conducts of address, emotional displays, and myths and stories told

about the organisation), its published lists of values, and its rituals and ceremonies (Schein 2004:

23

25-26). Artefacts are easy to observe but very difficult to interpret. The interpretation of artefacts

can differ due to the observer’s own reactions and feelings; thus, culture cannot solely be analysed

based on artefacts. Therefore, to understand the meaning of the artefacts, it is important to analyse

the second level of culture, espoused beliefs and values.

According to Schein (2004: 28), when an organisation is established or an already

established one has to deal with a task or problem, the solution or action proposed to counter the

problem essentially reflects someone’s own assumptions as to what is the most appropriate solution

and whether it will work. If the solution turns out to be effective in dealing with the problem, the

individual who proposed the solution will ultimately be identified as the founder or leader of the

organisation (Schein 2004: 28). However, until then there is not a shared basis for determining

whether what the leader proposed as a solution will have a positive outcome (Schein 2004: 28).

Once the members of the organisation have a shared perception, the value of the leaders’ solution

becomes a shared value or belief and eventually a shared assumption. These shared values or beliefs

are further confirmed by the shared social experience of the organisations members, which Schein

(2004: 29) defines as social validation. Social validation also applies to broader values, which are

not demonstrable, such as aesthetics and ethics (Schein 2004: 29). As the values and beliefs

continue to work, in terms of dealing with ambiguity of the organisations functioning, they are

ultimately transformed into non-discussable assumptions reinforced by expressed sets of norms and

beliefs which are embodied in an ideology or organisational philosophy (Schein 2004: 29).

However, espoused values and beliefs often lack in explaining large fragments of behaviour.

Therefore, to fully understand the culture of an organisation, it is important to analyse the third and

final level of culture, basic underlying assumptions.

Basic underlying assumptions can be defined as values and beliefs which are taken for

granted to such an extent that there is no room for variation (Schein 2004: 31). This is a

consequence of the success of the values and beliefs, and members of the organisation will find any

other solution to be implausible. Basic assumptions are often non-confrontable and non-negotiable;

hence, they are very difficult to change (Schein 2004: 31). This is due to the fact that changing

basic assumptions disrupts the cognitive and personal environment, resulting in anxiety. Hence,

rather than enduring anxiety, the members consider their environment as congruent, based on their

assumptions, even to the extent of altering and denying their environment (Schein 2004: 31-32).

This psychological process demonstrates the power culture has. Culture as basic underlying

assumptions guide what to focus on, the purpose of things, how to emotionally respond, and which

24

actions to take in different situations (Schein 2004: 32). Culture can be thought of as a defence

mechanisms which allows the organisation to operate; hence, the core of a culture can be found in

the pattern of basic underlying assumption (Schein 2004: 36).

3.2 Primary Embedding Mechanisms

According to Schein (2004: 246), there are five primary embedding mechanisms, which the

leadership can use to communicate to their employees, as to how to perceive, think, feel and

behave. These mechanisms create the “climate” of an organisation.

Firstly, what leaders pay attention to, measure, and control on a regular basis is one of the most

influential mechanisms the leadership can use to communicate what they are fond of and what they

believe in. This includes what they comment on and notice to what they reward, and can be

considered as a formal control mechanism and measurement (Schein 2004: 246-247). Essentially,

this mechanism communicates to the employees the leadership’s priorities, aims and expectations.

Secondly, leader reactions to critical incidents and organisational crises is another

mechanism. The way the leadership handles incidents and crises creates new values and norms,

revealing significant basic underlying assumptions, which are then adopted by the members of the

organisation, as mentioned earlier. According to Schein (2004: 256), the reaction to a crisis is an

optimal chance for the leader to communicate their own assumptions about human nature and

relationships.

Deliberate role modelling, teaching, and coaching is the third mechanism available to the

leaders to communicate assumptions and behaviours to members, particularly the newly hired.

Schein (2004: 248), argues that informal messages by leaders are more significant in

communicating than messages delivered on stage or by videos.

The fourth mechanism which is important in communicating beliefs and values of the

leadership is how leaders allocate rewards and status. It is the actual nature of the behaviour

punished or rewarded and the reward itself that is essential for communicating (Schein 2004: 259).

Leaders can achieve the desired behaviour and ensure that members will learn the core values and

assumption by consistently rewarding the members who meet the expectations.

The final mechanism to communicate is how leaders recruit, select, promote, and

excommunicate. This is one of the most powerful mechanisms by which leaderships’ assumptions

25

and values embed and preserve; hence, embedding and preserving the culture of the organisation

(Schein 2004: 261).

3.3 The Competing Values Framework

There are various types of cultures which an organisation can be characterised as. The specific type

of culture varies from organisation to organisation. Thus, this section presents the four major types

of cultures which are based on the Competing Values Framework (CVF), developed by Quinn and

Rohrbaugh (1983). The four types of culture are hierarchy culture, market culture, clan culture, and

adhocracy culture.

The hierarchy culture has its roots in the works of Max Weber about government

organisations in Europe in the early 1900s (Cameron and Quinn 2006: 37). Hierarchy culture is

based on the key characteristics of bureaucracy: rules, specialisation, meritocracy, hierarchy,

separate ownership, impersonality, and accountability (Cameron and Quinn 2006: 37). Thus,

hierarchy culture can be described as a formalised and structured culture where procedures direct

members to what to do; hence, formal rules and guidelines are fundamental. In this culture, good

leaders are effective coordinators and organisers. Also, efficiency, productivity, predictability, and

stability are vital for such a culture (Cameron and Quinn 2006: 38). Examples of a hierarchy culture

include government agencies, restaurants, and large organisations (such as automobile corporations)

(Cameron and Quinn 2006: 38). In order to get rewarded, or promoted, in such a culture, members

have to demonstrate the ability of following rules and procedures of the organisation.

Market culture is another form of culture which many organisations have opted. This culture

relies on different assumptions compared to the hierarchy culture. The most fundamental activity in

such a culture is transaction costs. The concept of a market culture does not refer to the marketing

function but to a form of organisation which operates as a market itself (Cameron and Quinn 2006:

39). The focus is on the external environment, which impacts the organisation rather than internal

activities, and on transactions with external actors such as customers, suppliers, and contractors

with the purpose of creating competitive advantage (Cameron and Quinn 2006: 39). Therefore, the

key aims of market culture can be described as profitability, bottom-line results, strong point in

market positions, and secure client bases. The values and beliefs, imposed by the leadership of the

organisation, can thus be characterised as competitiveness and productivity attained through a

prominence on external standing and control (Cameron and Quinn 2006: 39). Due to this, the

26

leadership tends to be result-oriented, adopts an aggressive strategy with tough procedures and an

emphasis on winning (Cameron and Quinn 2006: 40).

The third type of culture is clan culture. It refers to a family-type organisation due to

common goals and values, unity, participativeness, and uniqueness (Cameron and Quinn 2006: 41).

Unlike a hierarchical and market culture, clan culture is driven by teamwork, member participation

programs, and corporate assurance to members who are rewarded/promoted based on team rather

than individual achievements. In this culture, “…the environment can be best managed through

teamwork and employee development, customers are best thought of as partners, the organization is

in the business of developing a humane work environment, and the major task of management is to

empower employees and facilitate their participation, commitment, and loyalty.” (Cameron and

Quinn 2006: 41). An organisation with a clan culture is a friendly workplace with high level of

commitment, where the leadership is more of a mentor, and the organisation is generally glued

together by loyalty and tradition (Cameron and Quinn 2006: 42-43).

With a shift from industrial to material age came a new culture, known as adhocracy

culture. This type of culture puts emphasis on innovation and pioneering, and developing new

services and products due to a continuous change in the market (Cameron and Quinn 2006: 43).

Essentially, an adhocracy culture is a temporary culture in that it is quick in reconfiguring itself

when there is a change in circumstances. Therefore, this culture values adaptability, creativity, and

flexibility. Adhocracy organisations are challenged in the sense that they must produce new and

innovative products to suit the needs of the market. Power in such an organisation flows from team

to team or individual to individual, unlike market and hierarchies where power is centralised

(Cameron and Quinn 2006: 44). Such organisational culture also puts emphasis on risk-taking and

an individual's’ ability to develop a new and innovative product/service. Adhocracy culture can

exist as a sub-culture in large organisations where there is a different dominant culture type

(Cameron and Quinn 2006: 44). Subsequently, an adhocracy culture can be described as

entrepreneurial, energetic, and creative in which members are encouraged to take risks. Leadership

in such a culture tends to be visionary, innovative, and risk-oriented and emphasises rapid long-

term growth in which success is defined as producing exceptional services/products (Cameron and

Quinn 2006: 45-46).

The Levels of Cultural Analysis model, the Primary Embedding Mechanisms, and the Competing

Values Framework will be applied to answer the first sub-question. The levels of cultural analysis

27

and the primary embedding mechanisms used by the leadership will assist in analysing the role

Enron’s leadership played in shaping its culture. The competing values framework will be applied

to determine which of the four types of cultures can Enron be best characterised as.

3.4 Stakeholder theory

In order to gain a better understanding of the people and entities which Enron was dependent on, in

order to exist, and also the ones dependent on Enron’s existence, we will examine the stakeholder

theory. A stakeholder is anybody that has something to do with a certain company; it can be the

employees, customers, suppliers but also the government, trade unions, or others. Stakeholder

theory was first described by R. Edward Freeman in 1984, where the main reason for theorising

stakeholders was to address “principle of who and what really counts” (Freeman via Mitchell et. al.

1997). Freeman was the first to argue that people such as employees, customers and suppliers are

very important to the company and their needs should be addressed first. This was quite a radical

turn from the traditional view, where shareholders and the owners were the only groups of interest,

as they were the ones actually investing money in the company. Freeman, however, argues that

employees and other stakeholders also invest in the company by working for them, and expecting to

be paid at the end of the month. If stakeholders are not paid, they can refuse to work and strike, in

which case the company cannot continue to operate. On the other hand, stakeholders can also be

dependent on the company, in the sense that customers might be dependent on the product that a

certain company produces (Mitchell et. al. 1997).

There have been some developments in the stakeholder theory since it initiated. One development is

by Mitchell et. al. (1997) who further extended the main theory by Freeman. This is called the

stakeholder salience model. They added one main element in their analysis, which is the

categorisation of the different stakeholders into “(1) the stakeholder's power to influence the firm,

(2) the legitimacy of the stakeholder's relationship with the firm, and (3) the urgency of the

stakeholder's claim on the firm.” (Mitchell et. al. 1997: 854).

Power can be defined as "a relationship among social actors in which one social actor, A, can get

another social actor, B, to do something that B would not otherwise have done" (Mitchell et. al.

1997: 865). As defined by Mitchell et. al. (1997), there are different means that make one powerful;

coercive power works through violence and other physical force, utilitarian power works through

financial incentive and other material resources and normative power which works through

symbolic resources, for instance prestige. (Mitchell et. al. 1997: 865). One significant point, when

28

defining different types of stakeholders, is to remember that one can lose the attribute of power, as

well as gain power (ibid).

Legitimacy refers to “socially accepted and expected structures or behaviours” (Mitchell et. al.

1997: 866). Some researchers argue that legitimacy is closely tied to power, as “In the long run,

those who do not use power in a manner which society considers responsible will tend to lose it"

(Davis 1973: 31 via Mitchell et. al. 1997: 866). This means that power and legitimacy are

interrelated, whether a stakeholder already possesses the attribute of power or legitimacy, they

should aim for the other attribute, otherwise they may lose it. On the other hand, Weber (1947) (via

Mitchell et. al. 1997: 866) argues that the combination of legitimacy and power might create a

stronger attribute, called authority; however, that does not mean that one cannot be only legitimate

or only powerful (ibid).

Urgency, as described by Mitchell et. al. (1997: 867) is “when a relationship or claim is of a time-

sensitive nature and secondly, when that relationship or claim is important or critical to the

stakeholder”. Therefore, urgency is a very important attribute in the stakeholder salience theory, as

when a stakeholder is concerned about potential threat to the company, the management needs to be

able to understand the urgency of the issue (ibid).

The point of categorising stakeholders according to their attributes is to be able to recognise their

importance in order to use them to their full potential. Mitchell et. al. (1997) argue that this allows a

company to achieve better results during their normal state, but also, once a company is in crises,

the management can firstly decide to focus on the important stakeholders in order to stabilise the

company (Mitchell et. al. 1997). However, this categorisation was not enough because, as Mitchell

et. al. (1997) argue, managers and other stakeholder theorists were still limiting their search while

categorising the stakeholders; hence, another categorisation is made. Here, stakeholders are divided

according to how many attributes they hold, into following categories; Latent stakeholders: who

only have one of the attributes; power, legitimacy or urgency, Expectant stakeholders: who have

two attributes, and definitive stakeholders: who have all three attributes. There is also a group for

the stakeholders who do not have any of these attributes; they are considered non-stakeholders or

potential stakeholders (ibid). Here, the salience can be measured: latent stakeholders have low

salience with minimal power, and definitive stakeholders have high level of salience. Definitive

stakeholders are the most important stakeholders for a company, and therefore should be taken

seriously and have the highest priority (Mitchell et. al. 1997: 872-874).

29

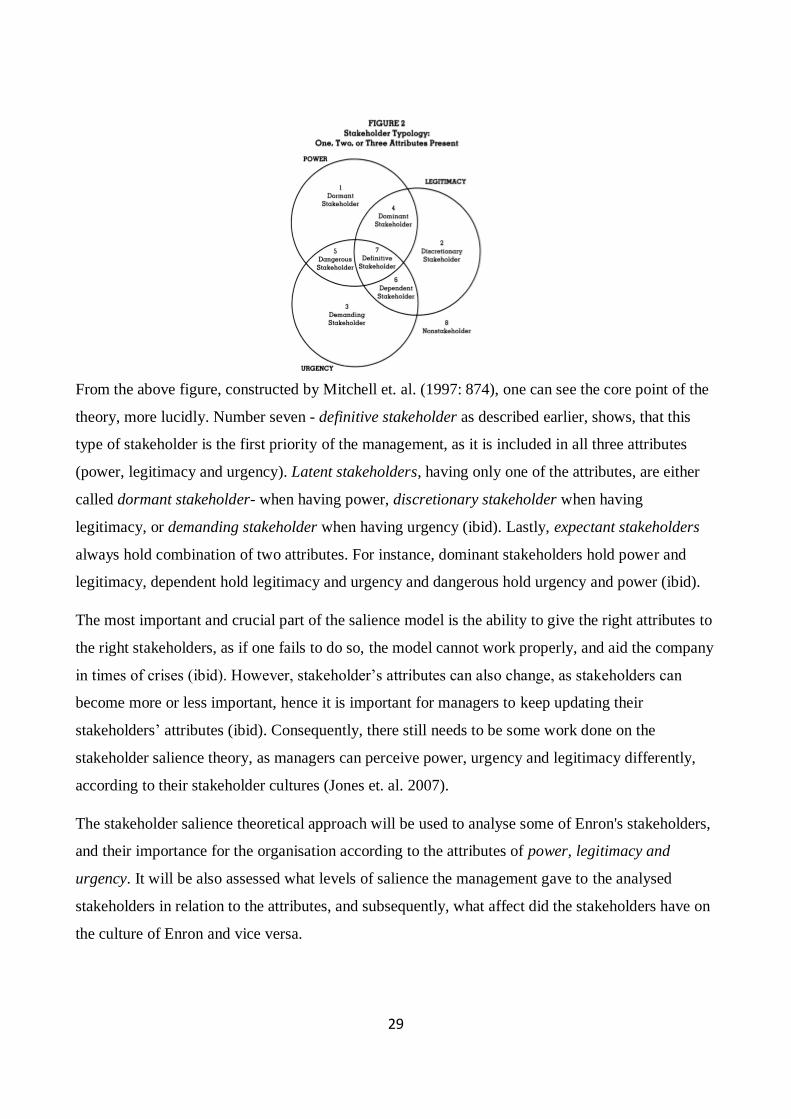

From the above figure, constructed by Mitchell et. al. (1997: 874), one can see the core point of the

theory, more lucidly. Number seven - definitive stakeholder as described earlier, shows, that this

type of stakeholder is the first priority of the management, as it is included in all three attributes

(power, legitimacy and urgency). Latent stakeholders, having only one of the attributes, are either

called dormant stakeholder- when having power, discretionary stakeholder when having

legitimacy, or demanding stakeholder when having urgency (ibid). Lastly, expectant stakeholders

always hold combination of two attributes. For instance, dominant stakeholders hold power and

legitimacy, dependent hold legitimacy and urgency and dangerous hold urgency and power (ibid).

The most important and crucial part of the salience model is the ability to give the right attributes to

the right stakeholders, as if one fails to do so, the model cannot work properly, and aid the company

in times of crises (ibid). However, stakeholder’s attributes can also change, as stakeholders can

become more or less important, hence it is important for managers to keep updating their

stakeholders’ attributes (ibid). Consequently, there still needs to be some work done on the

stakeholder salience theory, as managers can perceive power, urgency and legitimacy differently,

according to their stakeholder cultures (Jones et. al. 2007).

The stakeholder salience theoretical approach will be used to analyse some of Enron's stakeholders,

and their importance for the organisation according to the attributes of power, legitimacy and

urgency. It will be also assessed what levels of salience the management gave to the analysed

stakeholders in relation to the attributes, and subsequently, what affect did the stakeholders have on

the culture of Enron and vice versa.

30

3.5 Utilitarianism and Egoism

Decision-making is a crucial part of everyday life, whether it is in personal lives, economic,

political or business context, in which morality and ethics should be taken into consideration. What

remains disputed is whether it is the decision’s action or consequence that should be morally and

ethically correct. Thus, decision-making can be contrasted between deontological and

consequentialist perspectives (Tanner et. al. 2007: 1). Deontology is concerned with the concept of

duty, deriving from the Greek word deon, as it is morally directed actions or proscriptions such as

the duty to be truthful (Tanner et. al. 2007: 757). A deontological perspective puts emphasis on the

nature of the action more than the actual consequence of it. On the contrary, consequentialism is

more concerned with the consequence of an action rather than the action itself. Thus,

consequentialism draws inferences of the moral and ethical correctness based on the consequences

of an action (Tanner et. al. 2007: 757). Consequentialist ethical theories include utilitarianism and

egoism.

Utilitarianism is a consequentialist theory as it deals with the rightness or wrongness of an action

based on the consequences of the action. The most fundamental idea of utilitarianism is that actions

should result in best consequences. If an action does not bring about the best consequences, the

action is morally wrong (Snoeyenbos and Humber 2002). Thus, along with consequentialism,

utilitarianism also resonates aspects of ethical hedonism which postulates that a good life is a life

spent in the pursuit of pleasure; defined as avoiding pain (Robertson and Walter 2007: 1).

Utilitarianism can be used in various contexts, such as business. It can be used to make rational

decisions, based on the principles of the theory (Nathan 2014). In a business context, the various

stakeholders involved in the organisation can be defined as the ones affected by the actions of the

organisations. Thus, if an action taken by an organisation results in positive consequences for the

stakeholders, it can be said to be morally correct. There are two main utilitarian philosophers,

Jeremy Bentham and John Stuart Mill, who advocated a different variety of utilitarianism,

hedonistic and idealistic. Even though both varieties aim to maximise human well-being, they differ

in their definition of well-being (Brusseau 2011: 113).

Bentham was the advocate of hedonistic utilitarianism and believed that pleasure and

happiness are ultimately identical. According to him, the aim of ethics is to maximise pleasures –

all forms of pleasures – which are felt by individuals (Brusseau 2011: 114). On the contrary, Mill

agreed with Bentham’s view on ethics seeking to maximise pleasure; however, as his views on

utilitarianism were more idealistic, he differentiated between straightforward and intellectual

31

pleasures (Brusseau 2011: 114). Straightforward pleasures, according to Mill, are the physical

feelings which both humans and animals can enjoy. On the other hand, intellectual pleasures are not

simply physical joys but rather the enjoyments of mind, such as learning and learnedness, which

have more real value (Brusseau 2011: 114).

Whereas hedonistic and idealistic are varieties of utilitarianism the two main versions of

utilitarianism are, act utilitarianism and rule utilitarianism.

Act utilitarianism is the most basic form of utilitarianism. According to act utilitarianism,

the right action is the one which produces the greatest amount of well-being and, hence, each action

should aim to maximise well-being (Mulgan 2014: 115). This version of utilitarianism believes that

one should pursue “the greatest good for the greatest number” (Brusseau 2011: 107). To do this, act

utilitarianism suggests that all available action should be considered, their consequences predicted,

and the action with the best consequences should be chosen (Nathan 2014). Because each individual

action produces a differing amount of well-being, act utilitarianism applies the principles of

utilitarianism to individual acts rather than groups of action (Nathan 2014). Since the key goal of

act utilitarianism is to maximise well-being, the action can be generous or miserable, honest or

dishonest, as long as it meets the goal (Brusseau 2011: 107). One quality of act utilitarianism is that

it can be used to deal with moral questions in an objective way. For example, based on act

utilitarianism, if two people are in need of water and there is only enough water for one, the person

with the most desperate need should be given the water. On the contrary, there are some downsides

of act utilitarianism as well. According to Mulgan (2014: 115), act utilitarianism is “self-defeating”

because constantly calculating does not maximise well-being. He argues that if the target if to

maximise well-being, it is sometimes better not to directly aim at that. For example, if one is about

to be hit by a truck, one should not waste time on calculating precise utilitarian calculations

(Mulgan 2014: 116).

On the contrary, unlike act-utilitarianism which evaluates individual actions, rule-

utilitarianism evaluates codes of moral rules. Rule-utilitarianism asserts that if obeying a rule, such

as not to steal, would benefit everyone and maximise well-being, then everyone should obey the

rule (Brusseau 2011: 116). However, rule-utilitarianism do not obey rules, such as not to steal, if it

brings about maximum well-being. Thus, the ideal code is the set of rules in which the

consequences of everyone following them would be greater compared to the consequences of

everyone following any other set of rules (Mulgan 2014: 120). Therefore, the morally right action

32

depends on the action recommended by the ideal code. In a business context, organisations can be

said to have rule-utilitarianism in the sense that there are certain rules which the organisations’

members must follow in order to maximise profits. However, even though rule-utilitarianism is

intuitively very appealing, better can often be done by individuals breaking moral rules than

following them (Mulgan 2014: 116). Rule-utilitarianism has often been criticised, mostly by other

utilitarians, to be useless, indistinguishable or illogical (Mulgan 2014: 120). The most common

criticism of rule-utilitarianism is the very nature of it; rule worship. It has the commitment of

utilitarianism of maximising well-being; however, with rules to do so, even if the action according

to them will not result in the greatest consequences (Mulgan 2014: 120-121). Another great critique

of rule-utilitarianism is its collapse into act-utilitarianism because, essentially, the ideal code of

rule-utilitarianism consists of one single rule of always maximising well-being (Mulgan 2014: 122).