cover april-13 - db.com...account surpluses during 2013 and 2014. these twin surpluses will...

TRANSCRIPT

Financial Services Research A

pril 2013 47

Middle EastMiddle East

Backed by healthy public fi nances and a strong fl ow of petrodollars, several GCC governments are reinforcing their ex-penditure on infrastructure projects and reinvigorating efforts to develop their fi nancial sectors. The seeds of this expan-sion were already germinating during the 2003-8 period. However, GCC markets reacted adversely to the global banking crisis, prompting a sharp drop in GCC stock market indices and a sudden fall in real es-tate prices. Government-owned investment company Dubai World took a severe hit from this slide in asset prices, for example, prompting Abu Dhabi to extend US$10bn assistance in December 2009 to ensure that property development arm Nakheel could meet outstanding debt repayments. Though international and domestic inves-tors have remained cautious in re-exposing themselves to GCC real assets, some have now identifi ed selective opportunities to re-enter the market at attractive levels of pricing.

No doubt, the limited range of listed stock on Middle Eastern equity markets and the limited depth of liquidity continue to present a barrier for some potential buyers. The GCC equity markets currently offer approximately 630 listed stocks in total, of which just over 200 are listed on the Kuwait Stock Exchange and 150 on the Saudi Stock Exchange. However, interna-tional investors are monitoring the growth of GCC capital markets closely, along with the progress of steps in Saudi Arabia to open up the local market further to foreign investors and to allow international compa-nies to list on Tadawul.

A difficult crisis It has been something of a rollercoaster

ride for the GCC region over the past 7-8 years. The oil price boom of 2003-8 fuelled powerful economic expansion and allowed a number of GCC countries to sustain large fi scal and current account surpluses. In several instances, however, this also contributed to overheating and to economic imbalances that became dif-fi cult to manage with onset of the global credit crisis from 2008: external and fi scal surpluses contracted sharply; real estate and equity markets experienced sharp declines; and GCC corporates and fi nancial sector companies found it harder to access external funding on favourable terms.

Indeed, according to Markaz Research and IMF data, real estate prices declined by 60 per cent in Kuwait, 50 per cent in the UAE and 40 per cent in Qatar from their high point in 2008 through to the start of 2010. As a result, construction projects were put on hold or cancelled – Markaz Research estimates that approximately 19 per cent

of the 3000 construction projects active at the start of 2009 were terminated or delayed.

More generally, GCC corporates experi-enced sharp declines in profi tability. Net profi ts of 409 locally listed companies in the GCC slumped by 30 per cent in 2008 and by 48 per cent year on year in Q2 2009, before showing some improvement during Q3 2009. These concerns also fed through into the GCC fi nancial sector. Bank credit to private sector fi rms expanded rapidly during 2003-8, particularly to sup-port construction projects and real-estate lending. Markaz Research estimates that real average credit growth was close to 23 per cent per annum through this period for

In the past, many international investors have tended to view the MENA region as a single asset

class, with the credit quality of the sovereign being a primary determinant of where they will invest.

This is now changing, with foreign investors taking detailed interest in the credit rating of corporate

issuers, along with a company’s recent financial performance, corporate structure and managerial

strategy.

48

Fi

nanc

ial S

ervi

ces

Rese

arch

Apr

il 2

013

Middle EastMiddle East

the GCC region, with expansion particu-larly marked in the UAE and Qatar. With the onset of the credit crisis, a number of GCC banks fell into diffi culties, including the International Banking Corporation and Awal Bank, both Bahrain-based Saudi-owned banks that were placed into administration by the Bahrain authorities in mid-2009. Several investment companies also took a hit. In January 2009, Kuwait-based Global Investment House fell into default on a major chunk of its debt, prior to reaching an agreement with creditors later in the year to restructure its US$1.7bn debt commitments over a three-year term. In May 2009, the Investment Dar, another Kuwait-based investment house, defaulted on a US$100 million sukuk issue, prior to agreeing a plan in June 2011 to restructure US$5bn of its debt.

Recovering healthDuring the past 18-24 months the outlook for the GCC region has taken a signifi cant turn for the better, however. Mike Cowley, Head of Direct Securities Services (DSS) MENA at Deutsche Bank, notes that GCC markets experienced sizeable investment outfl ows in the aftermath of the global fi nancial crisis. Stock market indices have performed strongly in several Gulf markets since the end of 2011 and this has fuelled greater optimism on the part of regional and international investors. The Dubai Financial Market General Index (DFMGI), for example, climbed 20 per cent during 2012 and is up a further 16 per cent during 2013ytd. The Abu Dhabi All Securi-

ties Index (ADI) rose 10 per cent during 2012 and has climbed a further 13 per cent during 2013ytd. With this improved investment outlook, the outfl ow of foreign institutional investment witnessed during the credit crisis has now reversed, with FIIs again increasing their allocations to GCC equity and fi xed income securities. For local retail investors, many of whom retained their holdings of GCC securities throughout the crisis, rising market valuations are now beginning to translate into positive returns on their investments.

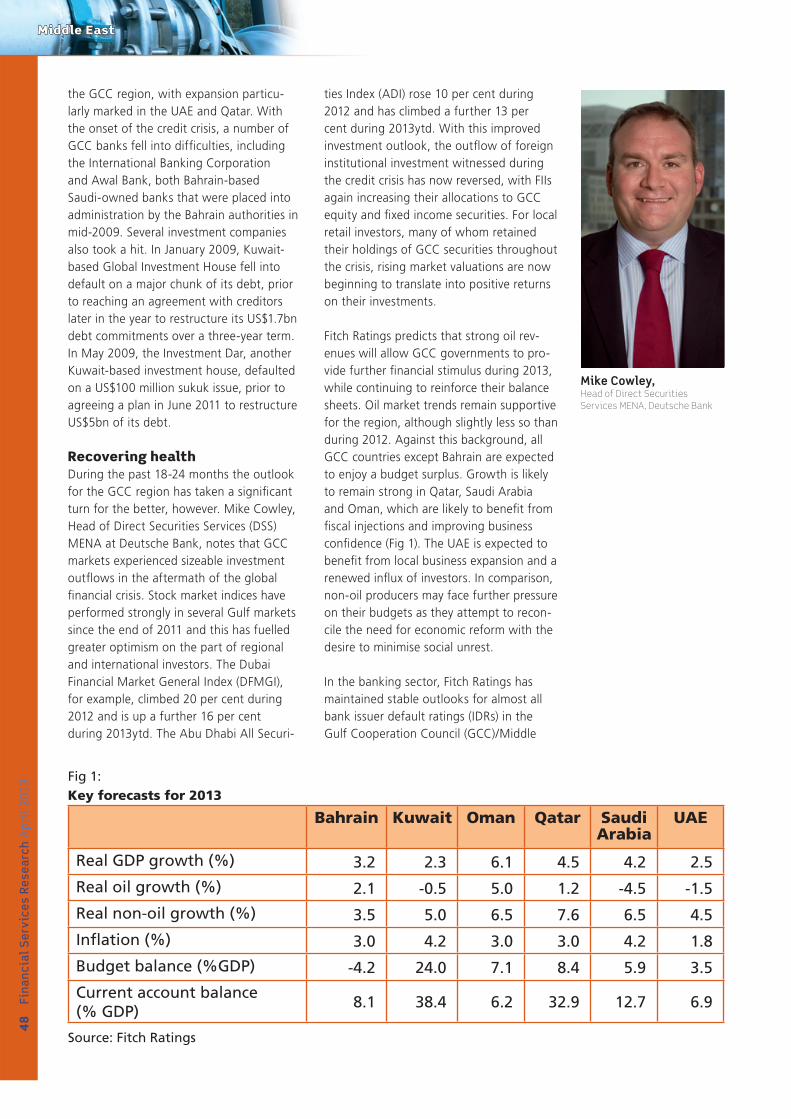

Fitch Ratings predicts that strong oil rev-enues will allow GCC governments to pro-vide further fi nancial stimulus during 2013, while continuing to reinforce their balance sheets. Oil market trends remain supportive for the region, although slightly less so than during 2012. Against this background, all GCC countries except Bahrain are expected to enjoy a budget surplus. Growth is likely to remain strong in Qatar, Saudi Arabia and Oman, which are likely to benefi t from fi scal injections and improving business confi dence (Fig 1). The UAE is expected to benefi t from local business expansion and a renewed infl ux of investors. In comparison, non-oil producers may face further pressure on their budgets as they attempt to recon-cile the need for economic reform with the desire to minimise social unrest.

In the banking sector, Fitch Ratings has maintained stable outlooks for almost all bank issuer default ratings (IDRs) in the Gulf Cooperation Council (GCC)/Middle

Fig 1: Key forecasts for 2013

Bahrain Kuwait Oman Qatar Saudi Arabia

UAE

Real GDP growth (%) 3.2 2.3 6.1 4.5 4.2 2.5

Real oil growth (%) 2.1 -0.5 5.0 1.2 -4.5 -1.5

Real non-oil growth (%) 3.5 5.0 6.5 7.6 6.5 4.5

Infl ation (%) 3.0 4.2 3.0 3.0 4.2 1.8

Budget balance (%GDP) -4.2 24.0 7.1 8.4 5.9 3.5

Current account balance (% GDP)

8.1 38.4 6.2 32.9 12.7 6.9

Source: Fitch Ratings

Mike Cowley, Head of Direct Securities Services MENA, Deutsche Bank

Financial Services Research A

pril 2013 4

9Middle EastMiddle East

East region. This refl ects the strong track record of GCC governments in supporting the banking sector, when it has been necessary, and the strong fi nancial position of most of these countries, underpinned by healthy government revenues from oil and gas sales, low levels of debt, and substan-tial accumulation of assets in sovereign wealth funds.

Monica Malik, Chief Economist at EFG-Hermes, predicts that real weighted GDP growth for the GCC region is likely to weaken from 5.5 per cent in 2012 to 4.1 per cent in 2013, refl ecting a slightly weaker outlook for hydrocarbon revenues. Several GCC countries recorded strong oil sales during 2012 as they ramped up production to fi ll the gap in Iranian output, which declined to its lowest levels for more than two decades in the face of US and European sanctions.

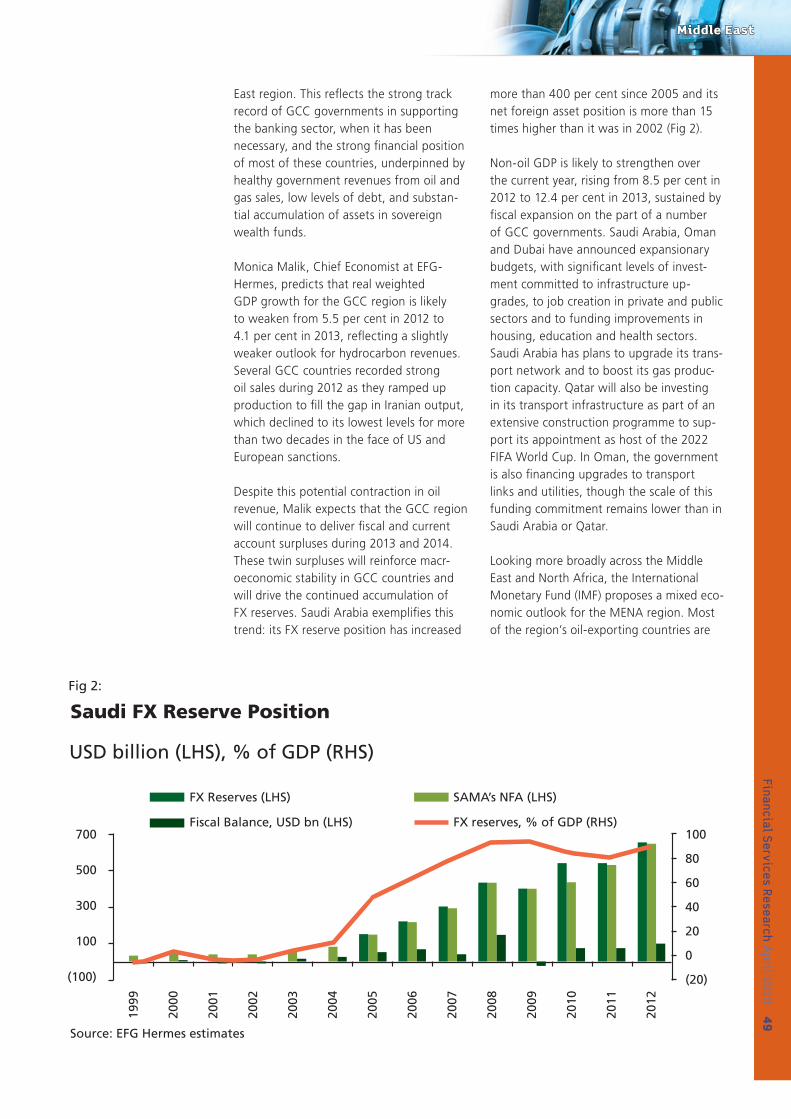

Despite this potential contraction in oil revenue, Malik expects that the GCC region will continue to deliver fi scal and current account surpluses during 2013 and 2014.These twin surpluses will reinforce macr-oeconomic stability in GCC countries and will drive the continued accumulation of FX reserves. Saudi Arabia exemplifi es this trend: its FX reserve position has increased

more than 400 per cent since 2005 and its net foreign asset position is more than 15 times higher than it was in 2002 (Fig 2).

Non-oil GDP is likely to strengthen over the current year, rising from 8.5 per cent in 2012 to 12.4 per cent in 2013, sustained by fi scal expansion on the part of a number of GCC governments. Saudi Arabia, Oman and Dubai have announced expansionary budgets, with signifi cant levels of invest-ment committed to infrastructure up-grades, to job creation in private and public sectors and to funding improvements in housing, education and health sectors. Saudi Arabia has plans to upgrade its trans-port network and to boost its gas produc-tion capacity. Qatar will also be investing in its transport infrastructure as part of an extensive construction programme to sup-port its appointment as host of the 2022 FIFA World Cup. In Oman, the government is also fi nancing upgrades to transport links and utilities, though the scale of this funding commitment remains lower than in Saudi Arabia or Qatar.

Looking more broadly across the Middle East and North Africa, the International Monetary Fund (IMF) proposes a mixed eco-nomic outlook for the MENA region. Most of the region’s oil-exporting countries are

Fig 2:

Saudi FX Reserve Position

USD billion (LHS), % of GDP (RHS)

FX Reserves (LHS) SAMA’s NFA (LHS)

Fiscal Balance, USD bn (LHS)

Source: EFG Hermes estimates

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

700

500

300

100

(100)

100

80

60

40

20

0

(20)

FX reserves, % of GDP (RHS)

50

Fi

nanc

ial S

ervi

ces

Rese

arch

Apr

il 2

013

Middle EastMiddle East

growing at healthy rates, while the oil im-porters face subdued economic prospects. As a result of higher oil prices and produc-tion, the region’s oil-exporting countries – Algeria, Bahrain, Iran, Iraq, Kuwait, Libya, Oman, Qatar, Saudi Arabia, the United Arab Emirates, and Yemen – grew at 6.6 per cent during 2012 but are expected to experience weaker growth during 2013.

However, faced with a diffi cult external en-vironment, the region’s oil importers – in-cluding, Egypt, Jordan, Lebanon, Morocco, Sudan, and Tunisia – recorded growth of close to 2 per cent in 2012. In the Arab countries in transition, continued political disruption is also acting as a brake on eco-nomic growth. Masood Ahmed, Director of the IMF’s Middle East and Central Asia Department, comments: “The biggest challenge facing governments in the Arab

countries in transition is how to manage the rising expectations of populations that are becoming increasingly impatient to see a transition dividend at a time when there are threats to near-term macroeconomic stability and the margin for policy ma-noeuvre is limited.”

In the GCC countries, the IMF indicates that expansionary fi scal policies and accom-modative monetary conditions contribute to a robust growth outlook through the near term, although growth is likely to slow from 7.5 per cent in 2011 to 3.7 per cent in 2013 as oil production hits a plateau. The IMF estimates that with oil prices remaining above US$100 per barrel through 2013, the combined current account surplus of the oil exporter countries is likely to remain close to its historic high of about $400 billion in 2012 (see Fig 3). Although many of the

Fig 3:

Faring well

Combined current account surplus of oil exporters in the MENA region is anticipated to remain near its historic highs.

Saudi Arabia Non-Gulf Cooperation Council

Rest of Gulf Cooperation Council

Source: IMF, Middle East and Central Asia Regional Economic Outlook.

180

160

140

120

100

80

60

40

20

0

Cu

rren

t ac

cou

nt

bal

ance

s, U

S$b

n

2007 2008 2009 2010 2011 2012 2013

52

Fi

nanc

ial S

ervi

ces

Rese

arch

Apr

il 2

013

Middle EastMiddle East

oil exporters have accumulated reserves to withstand short-run oil price volatility, the IMF notes that a sustained drop in oil prices resulting from a further slowdown in global economic activity is a risk that cannot be overlooked. For example, a 10 per cent drop in oil prices will reduce the combined current account surplus of these oil ex-porting countries by approximately US$150 billion. “Looking ahead, the main issue facing Middle East oil exporters is how to take advantage of their current positive po-sition to strengthen their resilience against oil price declines and diversify their econo-mies to boost private-sector job creation,” comments Masood Ahmed. “Fiscal policy could gradually shift to bolstering national savings, and countries could ease the pace of government spending, especially on expenditures that are hard to reverse, like public-sector hiring.”

International investors are monitoring Riy-adh’s reform agenda closely to determine when Saudi Arabia will open its equity market to direct foreign investment. “That is one of the major questions confronting foreign investors in the MENA region,” says Deutsche Bank’s Mike Cowley. “In August 2008, the market authorities extended ac-cess for GCC investors to the Saudi equities market; and the Capital Market Authority (CMA) swap product was rolled out the following year, enabling international investors to build exposure to Saudi-listed equities without formally being permitted to take direct ownership of the underlying instrument. Many observers expected foreign institutional investors to be granted authority to invest directly in Saudi equities during 2012, but so far this has not been forthcoming.”

Saudi Arabia offers by far the largest equities market in the region, with market capitalisation of more than US$380 bil-lion (representing approximately 60 per cent of the aggregate MENA market by market capitalisation, trading more than US$1 billion per day) and is thus central to the ambitions of many international and regional investors in the MENA region. “At Deutsche Bank, we continue to strengthen our product in the Saudi market in order to support growing trading activity from

domestic and regional investors – and to facilitate market access for foreign investors when necessary regulatory changes make this possible,” notes Cowley.

Indeed, Saudi Arabia remains a regional powerhouse in the MENA area, driven by its considerable oil reserves. In March 2013, Fitch Ratings affi rmed Saudi Arabia’s Long-Term foreign and local currency Issuer Default Ratings (IDRs) at ‘AA-’ and revised its outlook from Stable to Positive. Paul Gamble, Director of the Africa and Middle East team in Fitch’s Sovereign Ratings Group and primary analyst for this ratings review, confi rms that the Saudi govern-ment’s balance sheet remains very strong. High oil revenues have enabled the Saudi government to build fi scal and external buffers to levels matched by few Fitch-rated sovereigns, while at the same time the government has been able to sustain high levels of capital expenditure. With 2013 GDP growth forecast at 12.7 per cent, Fitch predicts that Saudi Arabia will deliver its tenth double digit current account sur-plus since 2003.

No doubt, the economy remains heavily dependent on oil production and related activities; oil still accounts for 90 per cent of government revenues and 80 per cent of current account receipts. While this does create some vulnerability to sharp fl uctuations in oil prices, Saudi Arabia’s sizeable buffers afford it considerable protection and Fitch believes it would take an extended period of lower oil prices to undermine its public and external fi nan-cial positions. Real non-oil private sector growth has remained strong, at 7.5 per cent in 2012, indicating some progress in encouraging economic diversifi cation. At an annual average of over 6 per cent, real non-oil growth is expected to exceed growth in the oil sector for 2013 and 2014.

Equities market recoveryAgainst this economic background, Robert Tabet, Regional Head South Asia, Middle East and Africa, at Clearstream, identifi es signs that the GCC region is coming back, with the UAE, Qatar and Saudi Arabia becoming increasingly attractive to inves-tors. “Stock market valuations have pushed

Financial Services Research A

pril 2013 5

3Middle EastMiddle East

upwards during 2012 and early 2013 and money is starting to fl ow back into GCC-listed equities,” he says. “UAE equity markets are up approximately 20 per cent for the year. Bahrain is up 12 per cent ytd, Jordan is up four per cent.”

In line with this growing optimism, there has been a revival in the pipeline of securi-ties issuance, with a number of sizeable GCC companies coming to the market in

recent weeks. In the past, many interna-tional investors have tended to view the MENA region as a single asset class, with the credit quality of the sovereign being a primary determinant of where they will invest. This is now changing, with foreign investors taking detailed interest in the credit rating of corporate issuers, along with a company’s recent fi nancial perform-ance, corporate structure and managerial strategy.

Clearstream has been active in the Middle East for almost 18 years, having opened its offi ce in Dubai to support GCC business in 1995. “Our commitment to the region has re-mained undiminished since this time, despite the challenges presented by the global economic downturn from 2008 and political and social instabilities in some MENA countries over the past 24-36 months,” says Tabet. “During those tough times, the head of the Dubai offi ce Nazely Mardirossian and her colleagues kept in daily contact with the customers in the troubled countries to help them run their business as close to nor-mality as possible and were on the fi rst fl ights to go back to visit them after things settled down. “

The uncertainties triggered by the Arab Spring have prompted some investors to limit their exposure to the region and some issuers to postpone capital raising activities until they have greater certainty re-garding the financial outlook for the Middle East. However, Clearstream has noted growing number of is-suers coming to market since the start of 2013. Moreover, with several GCC equities market indices up significantly since the start of the

year, rising numbers of investors are taking a view that it is an ap-propriate time to be building their exposure to GCC-listed equities.

There is much talk about Saudi Arabia liberalising its equities mar-kets to foreign direct investment. Throughout 2012, the international investor community kept a close eye on the Saudi market in the expecta-tion that it would ease ownership restrictions on foreign investors. “However, we are still waiting for clarifi cation regarding how far these reforms will go and when they will be implemented,” says Tabet. “In this context, we maintain a close dialogue with regional and interna-tional customers regarding how best we can support their investment objectives or their capital raising ac-tivities in this part of the world – and we monitor closely any changes to regulation, infrastructure or market outlook that may infl uence how they approach these activities.”

Importantly, Clearstream’s ambitions extend beyond the Middle East and North Africa to embrace opportuni-ties that markets in sub-Saharan Africa may extend to international and domestic investors. For some

emerging and frontier market investors, selected African markets are becoming increasingly attrac-tive as a source of potential invest-ment return. The World Bank and International Finance Corporation (IFC) are promoting measures to de-velop capital markets and corporate governance frameworks in a range of SSA states, ensuring that fi nancial infrastructure meets the standards expected by global investors and offering local issuers secure and ef-fi cient channels through which they can raise funds through securities issuance in domestic currencies.

“To support our ambitions in SSA, we have appointed Standard Chartered as sub-custodian in the South African market and our net-work management team is evaluating the pace at which we should extend our market coverage across other SSA states” adds Tabet. “Given that investment fl ows into some SSA mar-kets are building from low levels, the challenge for Clearstream is to gauge the pace at which regional and cross-border investors will increase their allocations to these markets and to extend our market coverage to sup-port this activity in a cost-effi cient manner.”

Middle East and beyondClearstream’s ambitions extend beyond the Middle East and North Africa to embrace opportunities that markets in sub-Saharan Africa may extend to international and domestic investors. Robert Tabet, Regional Head South Asia, Middle East and Africa Clearstream, tells FSR readers about plans for developing its service coverage

56

Fi

nanc

ial S

ervi

ces

Rese

arch

Apr

il 2

013

Middle EastMiddle East

as the government takes steps to form a global hub for Shariah-compliant fi nance. Markaz Research indicates that sukuk sales from the emirate have jumped 46 per cent to US$1.75 billion ytd, the most since the same period seven years ago. Dubai-based issuers tripled Islamic bond sales during 2012 to US$4.6 billion as the city’s bor-rowing costs dropped twice as much as the global average for Shariah-compliant notes. As activity continues to grow, issuers will be watching with interest to see whether Dubai can promote itself as a centre that can compete effectively with Malaysia, an established global hub for the issuance of Shariah-compliant products that currently accounts for more than 60 per cent of sukuk issued globally.

To support this momentum, NASDAQ Dubai aims to be the exchange of choice for re-gional and international issuers of Shariah-compliant securities. “NASDAQ Dubai is already playing a key role in Dubai’s intention to become the global capital of the Islamic economy by providing a venue for sukuk listings that benefi ts from an ef-fi cient and straightforward listing process,” says a NASDAQ Dubai spokesperson. “We intend to develop our Islamic sector further through new services for issuers and by attracting more Shariah-compliant listings across different asset classes.”

In the past, sukuk represented an asset class that was not well understood by inter-national investors, observes Clearstream’s Robert Tabet. Gradually this is changing, with some global investment banks taking steps to educate investors about the structure and appeal of Shariah-compliant investment products. A number of pension funds, insurance companies and mutual funds in the Middle East are now interested to increase their allocations to Shariah-compliant products.

Clearstream reports that since the start of the year the pipeline of sukuk issuance has been gathering momentum on a week-by-week basis. A wide body of issuers have re-turned to the market, including sovereigns and semi government owned institutions. In Egypt, the government is currently de-bating the introduction of a new law that

will offer potential for Egyptian companies to raise fi nance through international issu-ance of sukuk.

In July 2012, Qatar sold the largest USD-denominated Islamic bond ever issued, its fi rst issue of Shariah-compliant debt for nine years. This sovereign issue was structured through fi ve-year and ten-year tranches, each US$2 billion in size, reportedly at-tracting an order book of over US$24 billion. The Qatar Central Bank has given indica-tion of plans during 2013 to sell QAR3bn (US$0.8bn) of 3yr and 5yr bonds and QAR1bn of Shariah-compliant notes as part of its plans to build a yield curve to guide future domestic currency debt issuance.

Alongside this, there have been promi-nent sukuk issues from corporate issuers, including Emirates Airline (a US$1 billion sukuk issued in March 2013), the Abu Dhabi Islamic Bank and the Emirates NBD.

Reclassification to MSCI Emerging MarketsSeveral GCC countries have been pushing hard to be reclassifi ed by MSCI from a Frontier Market into the MSCI Emerging Markets Index. However, MSCI has so far resisted calls to promote GCC states to the EM category. MSCI indicates that the MSCI Qatar Index and MSCI UAE Index will remain in Frontier Markets and will be under review for potential reclassifi cation to Emerging Markets as part of the 2013 Annual Market Classifi cation Review.

In the case of Qatar, an MSCI spokesperson indicated that the very low foreign owner-ship limits imposed on Qatari companies is the principal impediment remaining to the reclassifi cation of the MSCI Qatar Index to Emerging Markets. “Based on current data, the total free fl oat adjusted market capi-talisation of the MSCI Qatar Index available to foreign investors is US$10 billion. In an extreme scenario, were the Qatari equity market to witness a net foreign capital infl ow of US$10 billion or more, the share of free fl oat available to foreign investors would be reduced to zero. This would make all current index constituents ineligible, leading to the discontinuation of the MSCI Qatar Index.”

Financial Services Research A

pril 2013 5

7Middle EastMiddle East

In addressing this concern, MSCI is en-couraging the Qatari authorities to look at different ways to increase the FOL limits currently applied by Qatari companies – potentially taking into account how other markets within the current MSCI Emerging Markets Index have resolved similar issues in the past. “Countries have increased the share in their equity market accessible to foreign investors using alternative mecha-nisms such as increasing the FOL levels in industries deemed to be of less strategic nature (e.g., India) or introducing specifi c share classes fully open to foreign inves-tors that preserve all economic rights but limit voting rights (e.g., Brazil, Mexico and Thailand),” it notes.

Signifi cantly, MSCI welcomes the intro-duction on 1 May 2012 of a “false trade

mechanism” for the Qatari equity market. This development will potentially remove the need for international institutional in-vestors to maintain segregated trading and custody accounts (a dual account structure, see below), although the effectiveness of this mechanism still needs to be fully evalu-ated by international investors.

An MSCI spokesperson reports that MSCI UAE Index meets all requirements for entry to the EM Index with the excep-tion of specifi c market accessibility issues relating to custody, clearing and settlement. “Based on current information, the Emirati regulator (Emirates Security and Commodi-ties Authority, ESCA), the Dubai Financial Market (DFM) and the Abu Dhabi Securities Exchange (ADX) have taken the decision to delay the implementation of a proper false

Deutsche Bank has been expanding its sub-custody and fund services capa-bility in the MENA region since 2008, supporting this from a Dubai hub. Currently, DSS offers direct custody access in Abu Dhabi, Dubai and Saudi Arabia through branches that it has es-tablished in these locations. In MENA markets where Deutsche Bank does not currently offer direct access, clients are able to access these locations via its Dubai hub. Through this arrange-ment, DSS offers custody coverage for approximately 90 per cent of GCC listed equities by market capitalisation.

“When we launched our DCC of-fering for the MENA region fi ve years ago, the forecast was substantially different in terms of growth projec-tions for the global economy and predicted investment fl ows into the Middle East,” says Cowley. “We have weathered the worst effects of the global credit crisis and we have continued to extend our market presence, adding new clients to our

platform and expanding the range of services offered through our GCC product suite. We continue to invest in our fund services capability, for example, and we have made available an expanding range of services from DCC’s global product offering (in-cluding securities lending services for instance as well as dbIntegrate, our new solution for end-to-end execu-tion, settlement and custody services) in MENA markets.”

With the attention that the global fi nancial crisis has focused on im-proving asset protection and reducing operational costs, Cowley notes that growing numbers of regional investors are recognising the value that a strong regional sub-custodian can bring to their investment activi-ties. DSS has also attracted a stream of new business as established fund managers outsource fund administra-tion and custody functions that they previously conducted in-house and new fund management companies

seek a high quality fund services pro-vider to support their money manage-ment activities.

More broadly, Deutsche Bank con-tinues to work with market authorities and with local market participants to encourage harmonisation of registra-tion procedures, account opening requirements and post-trade market practice across the GCC area. “For example, we have been liaising closely with other custody and clearing providers in order to streamline ac-count opening requirements across the GCC area, ensuring that compa-rable documentation is required by different market authorities across the Gulf region,” says Cowley. “Where inconsistencies persist, we have worked hard to insulate the customer from these differences by ensuring that Deutsche Bank’s systems and processes look the same across the GCC states and the other 33 markets in which we support sub-custody and clearing services globally.”

Supporting GCC from a Dubai HubMike Cowley, Head of Direct Securities Services (DSS) MENA at Deutsche Bank, speaks to FSR about the evolution of the bank’s DSS offering in the Middle East

58

Fi

nanc

ial S

ervi

ces

Rese

arch

Apr

il 2

013

Middle EastMiddle East

trade mechanism.” The implementation of this new mechanism, as well as the formal introduction of a regulation governing secu-rities lending and borrowing arrangements – both steps that international investors have highlighted as a means to eliminating the need for dual account structures – are now expected in 2013.

Commenting on this process, Deutsche Bank’s Mike Cowley indicates that consider-able work has been done to push through reforms that move GCC markets closer to meeting MSCI criteria. However, some outstanding issues remain diffi cult to solve. For example, limits on foreign investor

ownership of shares in Qatar still present an obstacle to accession to the MSCI EM Index. Many Qatar-based companies restrict foreign ownership to 25 per cent of listed shares, although some companies may offer greater access if shareholders agree. Foreign investors are also pressing for tighter controls on transfers from client trading accounts to ensure that securities can only be transferred on instruction from the client. Under current arrangements, use of dual account structures (with segrega-tion of custody and trading accounts) remains common, given unlimited access that brokers may have to client trading ac-counts.

Clearstream’s Robert Tabet notes that a lack of real-time settlement and true DvP in MENA markets continues to present a challenge to international investors. In some markets the cash leg of a securities transaction will settle with a commercial bank outside of the central infrastructure and investors may be required to pre-fund on SD-1 to ensure timely settlement. As noted, foreign investors may also fi nd it necessary to maintain segregated trading

and custody securities accounts in the local market to ensure that securities can only be transferred on direct instruction from the client.

So too, ISO standard message communica-tion with the local CSDs is still not widely established. The majority of CSDs in the MENA region communicate with market participants using proprietary message formats – although SWIFT has been in dialogue with CSDs and with market par-ticipants to encourage use of ISO 15022 standard messaging to support securities transactions. In the current environment, the local sub-custodian will typically pro-

vide message conversion to ensure that international clients can submit and receive communication using ISO-standard mes-sage formats.

Deutsche Bank’s Mike Cowley indicates that the Emirates Securities and Commodities Authority (ESCA) has taken important steps, working in association with Emirati stock exchanges (ADX, DFM, Nasdaq Dubai) and their post-trade infrastructures to promote steps towards DvP settlement, to estab-lish fails coverage procedures and, more generally, to improve STP rates across the transaction value chain. However, there is still work to be done to establish a model that is acceptable to all participants in the value chain (broker, custodian, CCP, CSD ...), that fulfi lls MSCI criteria and that meets with the operational and risk management standards expected by international inves-tors and their global intermediaries. These stock exchange groups will need, in the near future, to defi ne clearly which model will apply in the local market, thereby providing common ground around which all market intermediaries and their underlying clients must align.

Still there is considerable work to do in establishing DvP settlement mechanisms – though for DFM

or ADX which currently support less than 4000 trades per day and less than US$175 million in daily

traded value, it represents a sizeable commitment for these infrastructure groups to advance

the investment required to establish full DvP settlement supported by ISO 15022 standard SWIFT

reporting.

60

Fi

nanc

ial S

ervi

ces

Rese

arch

Apr

il 2

013

Middle EastMiddle East

Still there is considerable work to do in establishing DvP settlement mechanisms – though for DFM or ADX which currently support less than 4000 trades per day and less than US$175 million in daily traded value, it represents a sizeable commitment for these infrastructure groups to advance the investment required to establish full DvP settlement supported by ISO 15022 standard SWIFT reporting. “As an established provider of domestic custody and clearing services across more than 30 markets globally, we are well positioned to insulate the international client from these ineffi ciencies, interfacing with the CSD via its proprietary format messaging but providing the necessary translation services such that instructions and reporting to the client are communicated via ISO-standard messages,” says Cowley.

Despite these remaining obstacles, Cowley believes we should not undervalue the progress that has been made in a number of GCC markets. Five years ago, for example, DFM, DIFX and ADX still operated as distinct

stock exchange companies in the UAE. Sub-sequently, NASDAQ has acquired DIFX (cre-ating NASDAQ Dubai) and there has been considerable realignment in the post-trade segment, with NASDAQ Dubai outsourcing its key market operations for equities to DFM in July 2010. Nasdaq Dubai and ADX have also worked closely to develop a common clearing, settlement and depository frame-work. Though it is unlikely that we will see a formal merger between these exchange silos any time soon, Cowley believes that gradual harmonisation of market procedures across these respective markets represents an im-portant step forward compared with where we sat fi ve years ago.

Clearstream’s Robert Tabet agrees that commendable advances have been made in a number of GCC markets – but short-comings remain. Informal word around the market is that, although policymakers have signifi cant resources at their disposal to cover the cost of these adaptations, not all are convinced of the merits of reforming market practice in line with global stand-ards as a means to attract capital from a wider body of international investors.

More broadly, international investors remain concerned by the heavy administra-tive demands imposed by registration and account opening procedures, including the high levels of documentation that foreign participants are required to submit to attain necessary approvals required to invest in MENA markets.

Concluding thoughtsLooking ahead, Tabet is cautiously op-timistic about prospects for the region. There are signs that the GCC region is

returning to health, with UAE, Saudi Arabia and Qatar proving increasingly attractive to the investment community. “However, past experience has taught us to be wary of the prospect that these strong money fl ows into risk assets may trigger overheating similar to that witnessed in the GCC, par-ticularly in real estate markets, prior to the 2008 slide,” he says. “With a large fl ow of regional and international investment chasing a relatively limited number of new equity issues, there is a danger that this may lead to a bubble in equity markets and we have already noted a sharp rise in the UAE equity market indices during 2012 and early 2013.”

In the past, sukuk represented an asset class that was not well understood by international investors.

Gradually this is changing, with some global investment banks taking steps to educate investors

about the structure and appeal of Shariah-compliant investment products. A number of pension

funds, insurance companies and mutual funds in the Middle East are now interested to increase their

allocations to Shariah-compliant products.

Financial Services Research A

pril 2013 61

Middle EastMiddle East

In efforts to curb speculation in real estate markets, the UAE central bank issued rules effective from the start of 2013 which restricted mortgages for expatriates to 50 per cent of the value of a fi rst home and 40 per cent for a second home. For UAE citizens, equivalent curbs were imposed of 70 per cent of the value of a fi rst residence and 60 per cent for a second. Subse-quently, however, the central bank gov-ernor has indicated that these restrictions may be eased after protests by mortgage lenders.

But there are preliminary signs that the real-estate sector may be recovering its lustre. In April 2013, Dubai government-owned property developer Nakheel reported a 36 per cent y-o-y rise in fi rst quarter net profi t, driven by delivery of long-delayed units to its customers. This was after Nakheel Chairman Ali Rashid Lootah fi rmly denied rumours the pre-ceding month that the company might face diffi culties in repaying a US$1.1bn Islamic bond and approximately US$2 billion of bank debt due in 2016. Nakheel previously agreed a US$16 billion debt restructuring in 2011 and had reined in a number of high profi le projects since falling victim to the Dubai real estate crash.

Signifi cantly, it appears that UAE has ben-efi ted from a redirection of capital fl ows as investors have become uneasy about committing funds to MENA countries in political transition. Markaz Research indi-cates that the UAE attracted approximately US$8.2 billion of direct foreign investment during 2012 as signifi cant amounts of capital fl ed Egypt, Tunisia, Syria, Yemen and some other Arab countries disrupted by political and economic instabilities. A sizeable share of this capital has been redi-rected towards the UAE as a potential safe haven while instabilities persist in parts of the Arab world.

Deutsche Bank’s Mike Cowley notes that, with the attention that the global fi nan-cial crisis has accorded to improving asset protection and reducing operational costs, growing numbers of regional investors are recognising the value that a strong regional sub-custodian can bring to their investment

activities. The larger GCC-based sovereign wealth funds and other major asset owners typically have a global custodian in place to support their asset allocations across mul-tiple markets and asset classes. However, mid-sized institutional investors, family offi ce and corporate customers are also reviewing the structures they have in place to support their investment strategies and, increasingly, they are consolidating through a investor services specialist that can offer high standards of asset protection and a strong product suite across a broad range of MENA markets..

Signifi cantly, the Emirates Securities and Commodities Authority (ESCA) has issued a new Regulation on Investment Funds which became effective on 27 August 2012, designed to provide a comprehen-sive framework for the supervision of fund management activities. Among other developments, these require asset man-agement houses to appoint a third-party fund administrator and fund depositary to support their money management ac-tivities. “As a result, DSS has attracted a steady fl ow of new business as established fund managers outsource fund adminis-tration and custody functions that they previously conducted in-house and new fund management companies seek a high quality fund services provider to support their money management activities,” says Cowley.

Clearstream currently supports more than 120,000 investment funds across all fund classes from 33 jurisdictions on its Vestima order routing platform. To date, how-ever, it has seen only limited uptake from asset management companies registered in GCC markets – though Robert Tabet notes that there is potential for growth in the future. “We have had interest from a Saudi Arabia-based fund manager that wishes to create Luxembourg-domiciled UCITS and to support distribution of these funds on Vestima,” he comments. “This may set an example for other Saudi-based fund companies that wish to extend their distribution reach in Europe and globally via Luxembourg- or Dublin-domiciled UCITS, though this is at a preliminary stage currently.”

62

Fi

nanc

ial S

ervi

ces

Rese

arch

Apr

il 2

013

Middle EastMiddle East

So too, Tabet anticipates that the Saudi authorities will gradually liberalise access for foreign investors to the Saudi market. At present we see interest from foreign in-vestors in building exposure to Saudi-listed equities through P-note structures which are linked to an underlying Saudi-listed stock. Given the size of the market and (by GCC standards) the depth of liquidity, international investors remain excited about the potential to invest directly into Saudi-listed securities and investment funds.

Following its acquisition by Dubai Financial Markets (DFM) which was confi rmed in December 2009, Nasdaq Dubai has pro-gressively been outsourcing its trading, clearing, settlement and custody functions for equities to DFM. “This outsourcing

brought DFM’s investor base of more than 500,000 investors (mainly retail) into one liquidity pool with NASDAQ Dubai’s inves-tors (mainly institutional),” notes a Nasdaq Dubai spokesperson. “This step has made it easier for DFM retail investors to trade on NASDAQ Dubai, since they can now use the same DFM Investor Number that they already used for DFM.”

Additionally, Dubai SME and NASDAQ Dubai have signed an agreement to guide SMEs towards suitable fi nancing options, including conducting an IPO. NASDAQ Dubai indicates that preparations for an SME market is underway and NASDAQ Dubai has set up an advisory group of banks, lawyers and other advisers (in-cluding Dubai SME) to advise on the shape of this initiative. “This will include creating an environment where external advice for SMEs, to enable them to IPO, is priced attractively,” notes the NASDAQ

Dubai spokesperson. “We want to ensure that our market’s rules are geared to the specifi c needs of SMEs, such as the level of sponsorship required.”

In concluding, M.R. Raghu and his team at Markaz Research highlight a need for prompt review of GCC bankruptcy laws in order to create a more effective legal framework for business development. “The absence of effective laws governing liquidation and insolvency represent a serious gap in the regulatory framework of regional markets,” they note. “There is a stigma associated with bankruptcy in the GCC, which makes fi ling for bankruptcy protection almost unheard of in the region. This is both due to the cultural stigma at-tached in addition to the inadequacy of re-

gional bankruptcy laws where they exist.” (see further in Markaz Research, Dealing with Bankruptcy in the GCC, a missing block in the reform agenda, Jan 2013) With the increase in cases of repayment defaults by many companies in 2009-10, it became evident to creditors and investors that the bankruptcy laws in GCC were not suf-fi cient to handle the crisis. “Owing to the inadequacy of bankruptcy laws, most GCC companies that faced debt issues opted to deal with creditors directly, and more often than not, reached agreements and received extensions on loan facilities all by them-selves,” they add. “A closer look reveals that the bankruptcy laws in GCC are pri-marily liquidation laws and are insuffi cient to help an ailing company to restructure its debt so that it can continue in business.” In trying to learn lessons from the crisis, many governments in the GCC are considering the need for a review of legislation to ad-dress these concerns.

The absence of effective laws governing liquidation and insolvency represent a serious gap in the

regulatory framework of regional markets. There is a stigma associated with bankruptcy in the GCC,

which makes filing for bankruptcy protection almost unheard of in the region.