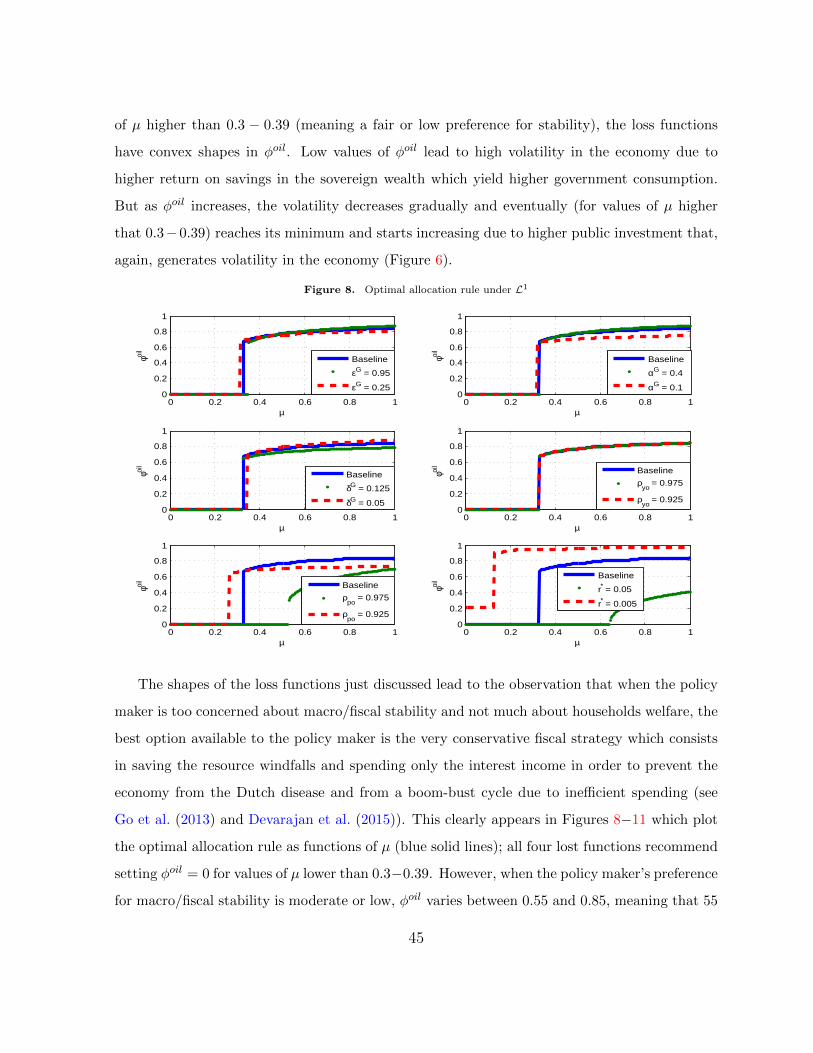

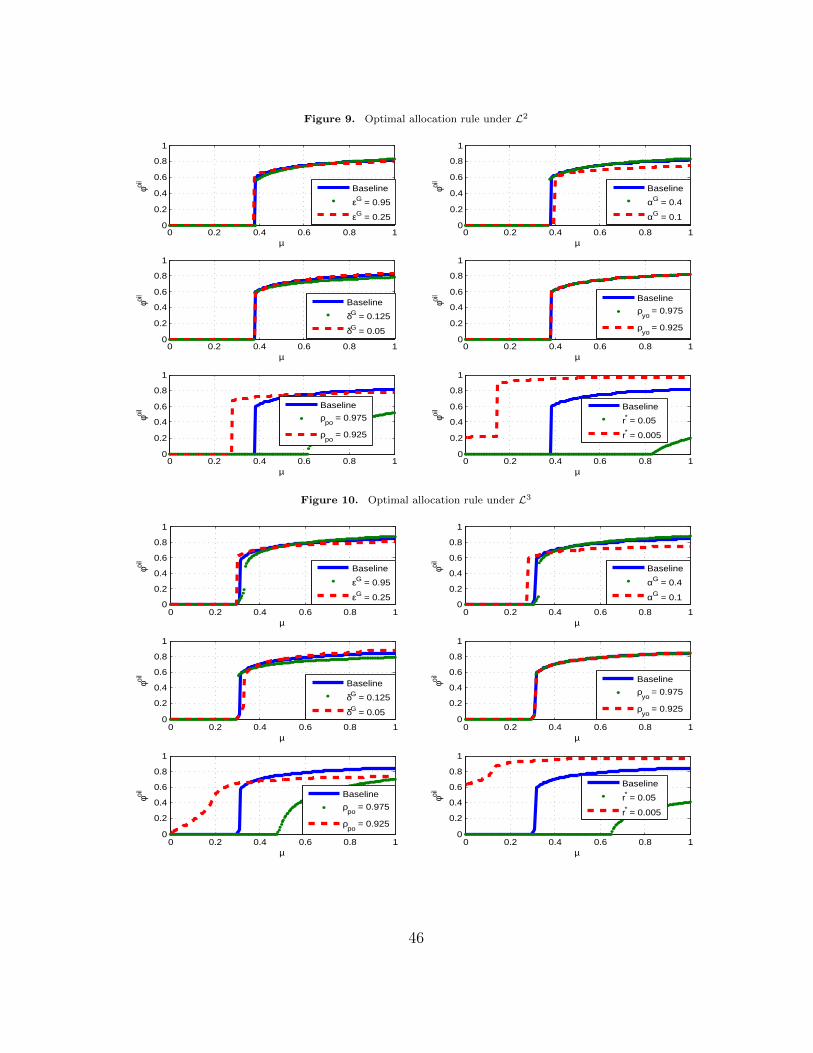

optimal allocation of natural resource surpluses in a...

TRANSCRIPT

Policy Research Working Paper 7910

Optimal Allocation of Natural Resource Surpluses in a Dynamic Macroeconomic Framework

A DSGE Analysis with Evidence from Uganda

Albert ZeufackAlexandre Kopoin

Jean-Pascal NganouFulbert Tchana Tchana

Laurent Kemoe

Africa RegionOffice of the Chief Economist &Macroeconomics and Fiscal Management Global Practice GroupDecember 2016

WPS7910P

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

edP

ublic

Dis

clos

ure

Aut

horiz

ed

Produced by the Research Support Team

Abstract

The Policy Research Working Paper Series disseminates the findings of work in progress to encourage the exchange of ideas about development issues. An objective of the series is to get the findings out quickly, even if the presentations are less than fully polished. The papers carry the names of the authors and should be cited accordingly. The findings, interpretations, and conclusions expressed in this paper are entirely those of the authors. They do not necessarily represent the views of the International Bank for Reconstruction and Development/World Bank and its affiliated organizations, or those of the Executive Directors of the World Bank or the governments they represent.

Policy Research Working Paper 7910

This paper is a product of the the Office of the Chief Economist, Africa Region and the Macroeconomics and Fiscal Management Global Practice Group. It is part of a larger effort by the World Bank to provide open access to its research and make a contribution to development policy discussions around the world. Policy Research Working Papers are also posted on the Web at http://econ.worldbank.org. The authors may be contacted at [email protected], [email protected], [email protected], [email protected], and [email protected]

In low-income, capital-scarce economies that face financial and fiscal constraints, managing revenues from newly found natural resources can be a daunting challenge. The policy debate is how to scale up public investment to meet huge needs in infrastructure without generating a higher public deficit, and avoid the Dutch disease. This paper uses an open economy dynamic stochastic general equilibrium model that is compatible with low-income economies and calibrated on Ugandan’s data to tackle this problem. The paper explores macroeconomic dynamics under three stylized fiscal policy approaches for managing resource windfalls: investing all in public capital, saving all in a sovereign wealth fund, and

a sustainable-investing approach that proposes a constant share of resource revenues to finance public investment and the rest to be saved. The analysis finds that a gradual scaling-up of public investment yields the best outcome, as it minimizes macroeconomic volatility. The analysis then investigates the optimal oil share to use for public invest-ment; the criterion minimizes a loss function that accounts for households’ welfare and macroeconomic stability in an environment featuring oil price volatility. The findings show that, depending on the policy maker’s preference for sta-bility, 55 to 85 percent of oil windfalls should be invested.

Optimal Allocation of Natural Resource Surpluses in

a Dynamic Macroeconomic Framework:

A DSGE Analysis with Evidence from Uganda

Albert Zeufack∗ Alexandre Kopoin† Jean-Pascal Nganou‡

Fulbert Tchana Tchana§ Laurent Kemoe¶

December 8, 2016

JEL Classification: E22, F43, O41, Q32Keywords: Fiscal policy; public investment; resource-rich developing countries; macroeconomicvolatility; optimal resource allocation.

∗Chief Economist, Africa Region, The World Bank, email: [email protected].†Economics Department, OECD and Laval University, email: [email protected].‡Senior Country Economist, The World Bank, email: [email protected].§Senior Economist, The World Bank, email: [email protected].¶Department of Economics and CIREQ, University of Montreal, email: [email protected].

We are grateful to Kevin Moran, Jean-Pierre Pare, Gilles Belanger, Fall Falilou, Juste Some, seminar participants at CSAE Conference 2015: Economic Development in Africa and anonymous referees for helpful comments.

1 Introduction

In low-income, capital-scarce economies that face financial and fiscal constraints, managing rev-

enues from newly found natural resources such as oil can be a daunting challenge. The policy

debate is how to scale up public investment to meet huge needs in public infrastructure with-

out generating a higher public sector deficit, and avoid the Dutch disease, all in an uncertain

world characterized by high occurrence of shocks and price volatility. This less documented

cutting-edge issue− viewed as the optimal scaling-up of public investment in an uncertain pro-

duction environment− remains one of the key elements to accelerate structural transformation

and achieve developmental goals while maintaining the country’s macroeconomic stability and

global competitiveness.

There is a huge literature that looks into the impact of oil windfalls on macroeconomic ag-

gregates and conventional wisdom suggests that natural resource revenues should be either saved

externally in a sovereign wealth fund (SWF) or invested in productive public infrastructures.

However, the first option has a weak ability to avoid poor living conditions and limits sustain-

able investment, in particular in a credit-constrained environment. The second approach which

was promoted to significantly reduce the public infrastructure gap in resource-rich low-income

countries has also become obsolete due to lack of sustainable public policies. (Davis et al. (2001),

Barnett and Ossowski (2003), Berms and Irineu (2011)). Then, the policy trade-offs emanating

from saving fiscal revenue from oil resources to smooth consumption versus spending it upfront

to boost growth is considered as one of the most frequently-cited challenges to resource-rich

low-income countries.

Given this unsolved natural resources management issue, one of the major tasks faced by

economic policymakers is how to reduce the effects of volatile resource prices on the domestic

economy. For instance, if all of the windfall gains are passed through into the economy, this will

generally result in a high inflation and an overvalued real exchange rate. In addition, exports

of other products are unable to gain a foothold in the economy, leaving the economy vulner-

able when the resource wealth runs out and causing a Dutch disease. Thus, addressing these

challenges requires state-of-art macroeconomic models and refined strategies for strengthening

institutional capacities for more effective governance, especially in the area of strategic planning,

2

budgeting and public finance management.

This paper contributes to the ongoing debate by developing an open-economy dynamic

stochastic general equilibrium model with a natural resource sector to study macroeconomic

impacts and fiscal policy responses to natural resource inflows. In low-income countries, given

tremendous infrastructure needs in public infrastructures and international borrowing con-

straints, resource revenues are valuable to finance public investment and can also serve as a

collateral for accessing international financial markets, making it possible to build up a sovereign

capital. In this spirit, the investing-saving pattern becomes not obvious and requires an assess-

ment of several scenarios based on the country’s specific macroeconomic strengths and weak-

nesses. The focus of the analysis is to explore macroeconomic dynamics under three stylized

fiscal policy approaches for managing a resource windfall: (i) investing all in public capital (the

All-Investing Approach); (ii) saving all in a sovereign wealth fund (the All-Saving Approach);

and (iii) using a constant share of the oil revenues to finance public investment and saving the

remaining share in a sovereign wealth fund (the Sustainable-Investing Approach). The paper

also contributes to this literature by providing the optimal share of oil revenue to use in the the

Sustainable-Investing Approach.

In the state-of-the-art macroeconomic modelling and fiscal policy assessments, this paper

contributes to two strands of literature. First, we provide a contribution to the literature

that looks the pattern of natural resources and macroeconomic stability in a developing country.

Sachs and Warner (1999) is considered as a reference paper in this strand of literature by showing

that investing resource windfalls does not necessarily promote sustained economic growth in

developing countries. Second, our paper complements the existing literature that analyzes the

optimal fiscal policy rule in managing of natural resources income by analyzing three innovative

fiscal policy approaches. The model includes key features of a small open economy model with

optimizing agents and nominal rigidities and several important features that are common in New

Keynesian models and developing countries, including Dutch disease, investment inefficiencies

and weak tax systems. In addition, we propose and test diverse approaches to analyze fiscal

policy responses in low-income countries.

However, recent theoretical and empirical studies have looked at the impact of natural re-

3

source revenues on fiscal responses and among others, Devarajan et al. (2015) sheds light on this

issue by simulating the impact of resources windfalls on long-term economic growth and welfare

under resource price uncertainty. Agenor (2014) provides a characterization of the optimal fiscal

response in the presence of oil price shocks using a small open low-income country DSGE model.

While these papers focus on oil price shocks, we analyze the optimal fiscal response from a dif-

ferent perspective by focusing on oil production shocks only, because our paper’s objective is to

provide policy advice to countries that, like Uganda, have not yet started producing. Tilak et al.

(2015) uses the IMF DSGE model to assess some fiscal policy options: i) Household transfers, ii)

Front-load public investment and iii) Gradual public investment. Their fiscal policies are similar

to Berg et al. (2013) as well as Giovanni et al. (2014); but slightly different from ours, because

we do not consider the front-loading option.

Although we focus our impulse response analysis on oil production shocks as we aim to assess

how a sudden increase in public revenues due to oil production affects macroeconomic dynamics,

in our investigations regarding the optimal share of oil windfalls to use for public investment,

we reckon that most of the volatility in oil revenue for a new oil producer comes from oil price

volatility instead of production volatility. For this reason, in these investigations, we use oil

price volatilities as the main source of uncertainty.

We calibrate this model to reproduce key features of the Uganda economy, a Sub-Saharan

Africa low-income country that recently discovered significant oil resources, with an estimated

2.5 billion barrels of reserves. This is a significant development milestone, as it represents

great opportunities for the financing of Uganda’s National Development Plan. According to

the World Bank’s economic projections, oil revenues in Uganda are expected to be relatively

important at an estimate around of 3 percent of the national Gross Domestic Product (GDP)

over the next five years. These estimates, associated with large movements in commodity prices

in the world natural resources market over the past decade, have sparked renewed interest in a

better understanding of the impact of this natural windfall on the Ugandan economy.

Our results show that a better fiscal management is to save the resource income in a sovereign

wealth fund for future generation when public capital is almost unproductive. We also find that

the gradual scaling-up of public investment (The Sustainable-Investing Approach) yields the

4

best outcomes as it minimizes macroeconomic volatility. For example, the real exchange rate

appreciation is 30 percent lower than in the all-investing approach, which might be viewed as an

attractive fiscal policy to accelerate economic development in public capital-scarce economies.

The trade balance improves substantially and impulse response functions suggest that output,

non-tradable and tradable goods production, employment and wages rebound faster. We then

investigate the optimal oil share to use for public investment; our optimization criterion is based

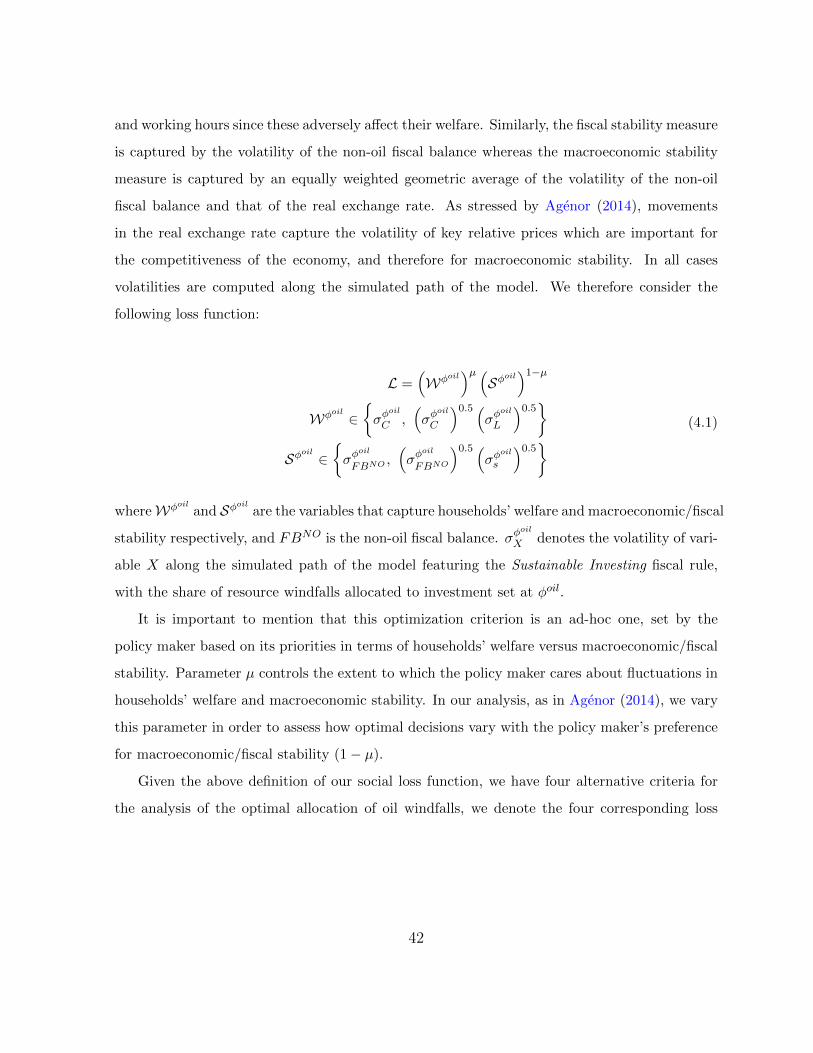

on a loss function that accounts for households’ welfare and macroeconomic/fiscal stability in an

environment featuring oil price volatility. Households’ welfare is captured by the volatilities of

consumption and employment along the simulated path of the model; the fiscal stability measure

is captured by the volatility of the non-oil fiscal balance whereas the macroeconomic stability

measure is captured by an equally weighted average of the volatility of the non-oil fiscal balance

and that of the real exchange rate. We find that depending on the degree of the policy maker’s

preference for stability, 55 to 85 percent of oil windfalls should be used for public investment,

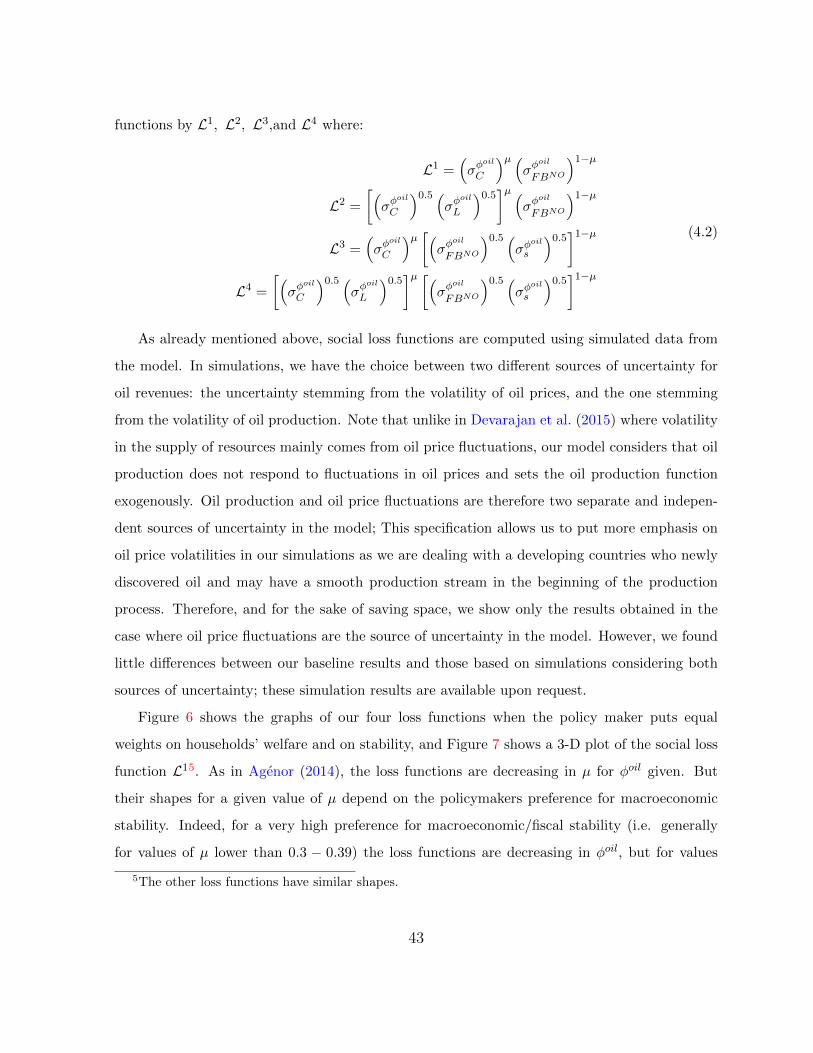

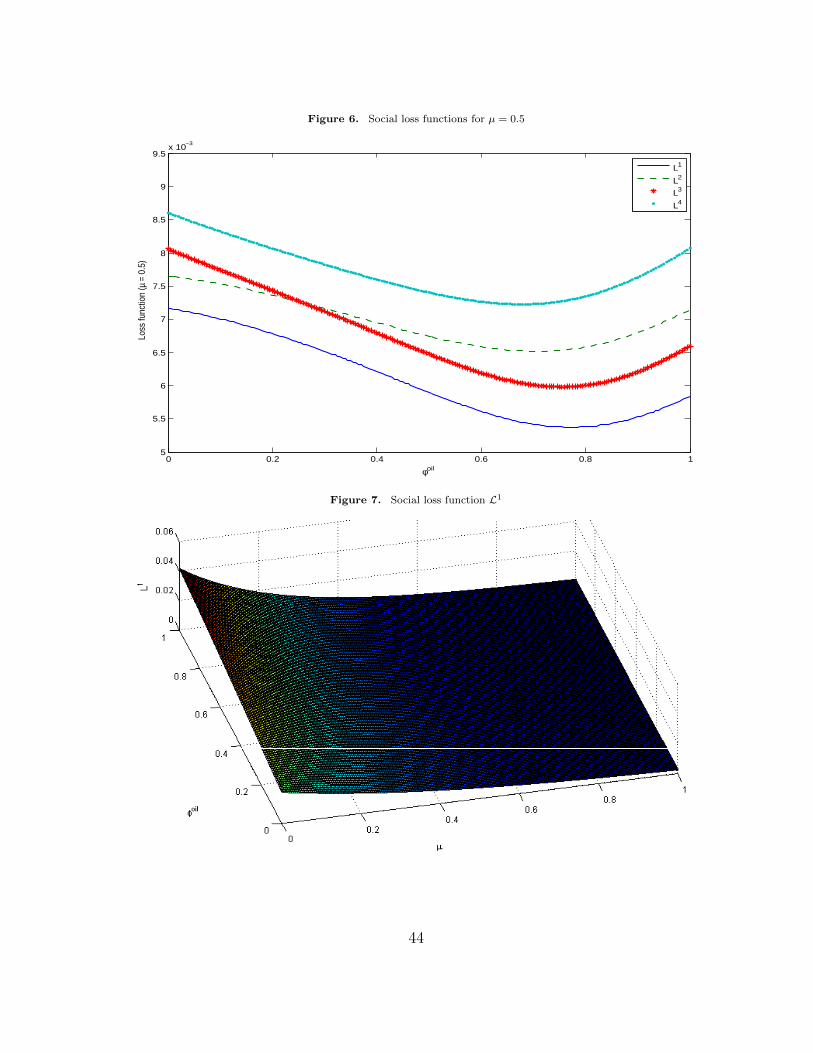

suggesting that 15 to 45 percent of the resource income should be saved in a sovereign wealth

fund. Our optimal share to invest domestically mainly depends on the persistence of oil shocks

and on the interest rate paid on savings. In comparison with the recent literature, the optimal

share to invest is slightly higher than the values estimated in Agenor (2014), which ranges

from 30 percent to 60 percent. Our figures are higher because we abstract from oil production

volatility in our simulations as we are dealing with a country that newly discovered oil; this

reduces the economic volatility and therefore the need for savings in a sovereign wealth fund.

Overall, the key recommendation of this paper is that unlike the all-investing approach which

seems to exacerbate Dutch disease effects, the sustainable approach appears to dominate in

terms of wealth and resources stability with the optimal oil share to be saved in a sovereign fund

varying with the persistence of oil shocks.

The rest of the paper is organized as follows. Section 2 describes the model, whereas section

3 presents a parametrization to mimic the key features of a small open economy such as Uganda.

Section 4 presents our main findings and Section 5 offers a conclusion.

5

2 Model setup

The framework is a small open New Keynesian model adapted from Obstfeld and Rogoff (2000)

and Christiano et al. (2005), in which we include three production sectors: non-traded goods,

traded goods, and a natural resource. The model includes the standard friction of investment

adjustment costs, which is standard in DSGE literature. We also include the friction a la Calvo

in the prices and wages setting as in Christiano et al. (2005) and Kopoin et al. (2013). The

model is calibrated from the Uganda data and includes various exogenous shocks as well as

various fiscal policy regimes.

2.1 Households

The economy is composed of a continuum of infinitely-lived households of mass 1. Households

obtain utility from consumption ct, which is produced by domestic firms, and receive disutility

from labor supply lt. Accordingly, the preferences of the representative household are given by

the following lifetime utility function, which is separable with respect to consumption and hours

worked.

E0

∞∑t=0

βt (log (ct − γct−1) + ψ log (1− lt)) (2.1)

where β denotes the household’s discount factor and ψ is the inverse of Frisch elasticity of labor

supply, whereas γ ∈ (0, 1) is the parameter that controls the extent of habit. Finally, E0 denotes

the conditional expectation operator evaluated at time 0.

Households are assumed to be able to borrow or lend freely in national financial markets

by buying or issuing risk-free bonds denominated in units of consumptions goods, and those

in the non-tradable goods sector set nominal wage using Calvo’s partial indexation mechanism.

Finally, the representative household maximizes the aforementioned utility function subject to

budget constraint in units of domestic composite consumption:

(1 + τ ct )ct + iNt + iTt + bt =Rt−1bt−1

πt+ (1− τ lt )wtlt + ΩN

t + ΩTt

+ rNt kNt−1 + rTt k

Tt−1 + zt,

(2.2)

6

where τ ct and τ lt denote the tax rates on consumption and income from labor supply. Total

private investment − defined as the sum of private investment in the tradable sector and that

in non-tradable sector − is given by: it = iTt + iNt . bt is the domestic government debt paying

a gross nominal rate of Rt = (1 + rbt ), πt is the domestic inflation and wt is the real wage index

expressed in units of consumptions goods. zt denotes total government transfers to households,

whereas ΩNt and ΩT

t are profits from the non-traded and traded goods sectors. rNt kNt−1 + rTt k

Tt−1

is capital income. Throughout the analysis, we assume that households do not have access to

foreign loans.1 This assumption is consistent with the fact that in a typical low-income country,

households are generally hand-to-mouth households. So, they do not have access to assets and

capital markets and consume all their disposable income from labor supply (see Jihad et al.

(2012) and Cherif and Fuad (2012)). However, domestic bonds play an important role in our

setup, allowing households to smooth idiosyncratic shocks. Since these bonds are in zero net

supply, households are subject to the following no-Ponzi game constraint:

limt→∞

Et[bt+j ]

Rjt+j≤ 0. (2.3)

Finally, the consumption basket is a composite of traded goods and non-traded goods, aggregated

using a constant-elasticity-of-substitution (CES) technology.

ct =

(φ

1χ(cNt)χ−1

χ + (1− φ)1χ(cTt)χ−1

χ

) χχ−1

, (2.4)

with χ and φ denoting the intratemporal elasticity of substitution and the degree of home con-

sumption bias. Thus, if φ > 1/2, the representative household has a home bias in consumption.

In this framework, we assume that the composite consumption is the numeraire of the economy

and the law of one price holds for traded goods. Accordingly, the real exchange rate st is also

the relative price of traded goods to composite consumption. As consequence, the price of one

1Most of low-income countries are not able to borrow on international financial markets. This situationhas been worsened by the last financial crisis, which led to credit-rating agencies to downgrade most low-income countries’ obligation bonds.

7

unit of composite consumption is:

1 = φ(pNt)1−χ

+ (1− φ) (st)1−χ . (2.5)

In equation [2.5], pNt denotes the relative price of non-traded goods to composite consumption.

Recall that, non-traded and traded consumption are a composite goods.

cNt =

(∫ 1

0cNt (i)

1− 1χdi

) χχ−1

, and cTt =

(∫ 1

0cTt (i)

1− 1χdi

) χχ−1

. (2.6)

Finally, households supply differentiated labor lt to both traded and non-traded sectors (lNt and

lTt ), and we assume that there is imperfect labor mobility captured by the following constant

elasticity of substitution (CES) function for total labor

lt =

(ω− 1ξ(lNt) 1+ξ

ξ + (1− ω)− 1ξ(lTt) 1+ξ

ξ

) ξ1+ξ

, (2.7)

where ω is the steady-state share of labor supply in the non-traded goods sector, which also

governs labor sectoral mobility in the economy. In equation [2.7], ξ (ξ > 0) is the elasticity of

substitution between the two types of labor. Then, the aggregate real wage index corresponds

to

wt =(ω(wNt)1+ξ

+ (1− ω)(wTt)1+ξ

) 11+ξ

, (2.8)

where wNt and wTt are the real wage rate in the non-traded and traded goods sector, respectively.

Efficient allocation: Given the preferences and the budget constraint, the household’s

optimization problem consists of choosing ct, iNt , iTt , kNt , kTt , and bt for all t ∈ [0,∞) to maximize

lifetime utility function, Ut(·). Finally, given [2.1] and [2.2], households

ψ

1− lt− λt(1− τ l)wt = 0, (2.9)

− λt + βEt

(λt+1

Rt+1

πt+1

)= 0, (2.10)

8

1+ϕN

(kNtkNt−1

− 1

)= βEt

λt+1

λt

1− δN + rNt + ϕN

(kNt+1

kNt− 1

)kNt+1

kNt+ϕN

2

(kNt+1

kNt− 1

)2 ,

(2.11)

1 + ϕT

(kTtkTt−1

− 1

)= βEt

λt+1

λt

1− δT + rTt + ϕT

(kTt+1

kTt− 1

)kTt+1

kTt+ϕT

2

(kTt+1

kTt− 1

)2 .

(2.12)

2.2 Firms

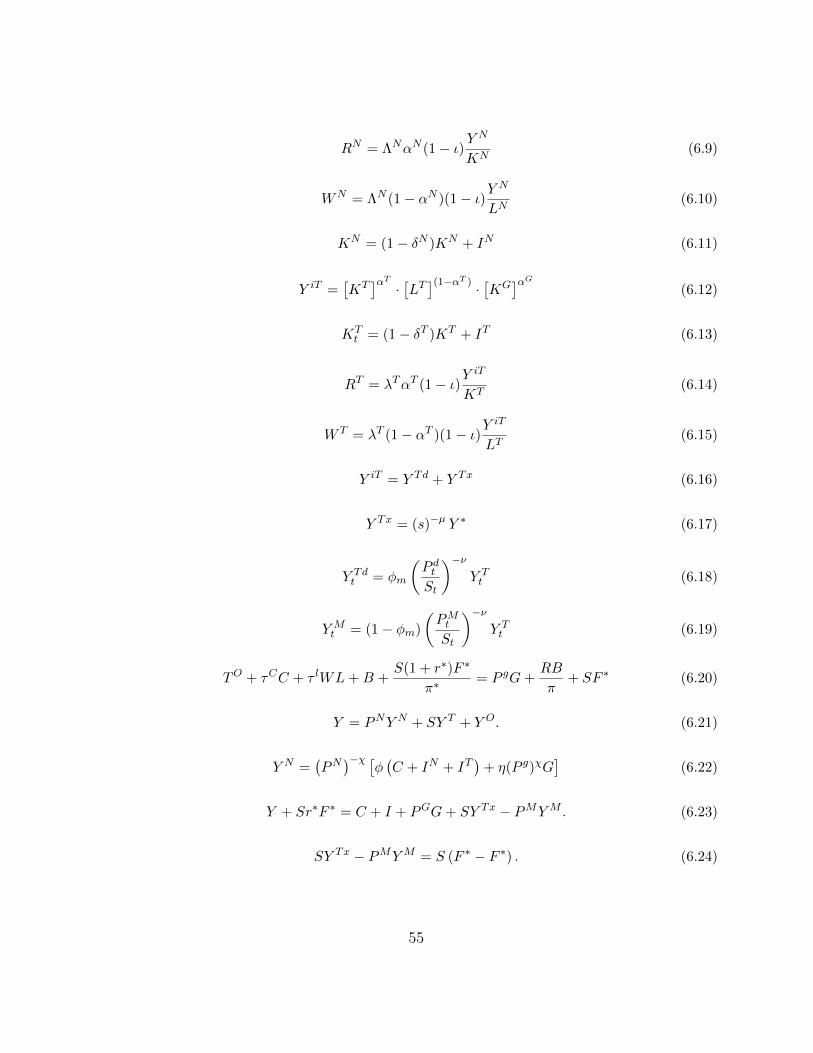

Non-traded good firms are assumed to be monopolistically competitive, while traded good sector

firms are perfectly competitive. In each sector, firms produce goods using labor lt, private

capital (kNt or kTt ) and public capital kGt . In contrast to the natural resource sector, production

and oil prices are assumed to follow exogenous deterministic processes. These assumptions are

consistent and match clearly low-income and small-open economy frameworks since Uganda’s

oil production, as estimated, is relatively small in comparison to world’s oil supply.2 In the

following subsections, we describe the production chain in the tradable and non-tradable goods

sectors.

2.2.1 Non-traded Good Sector

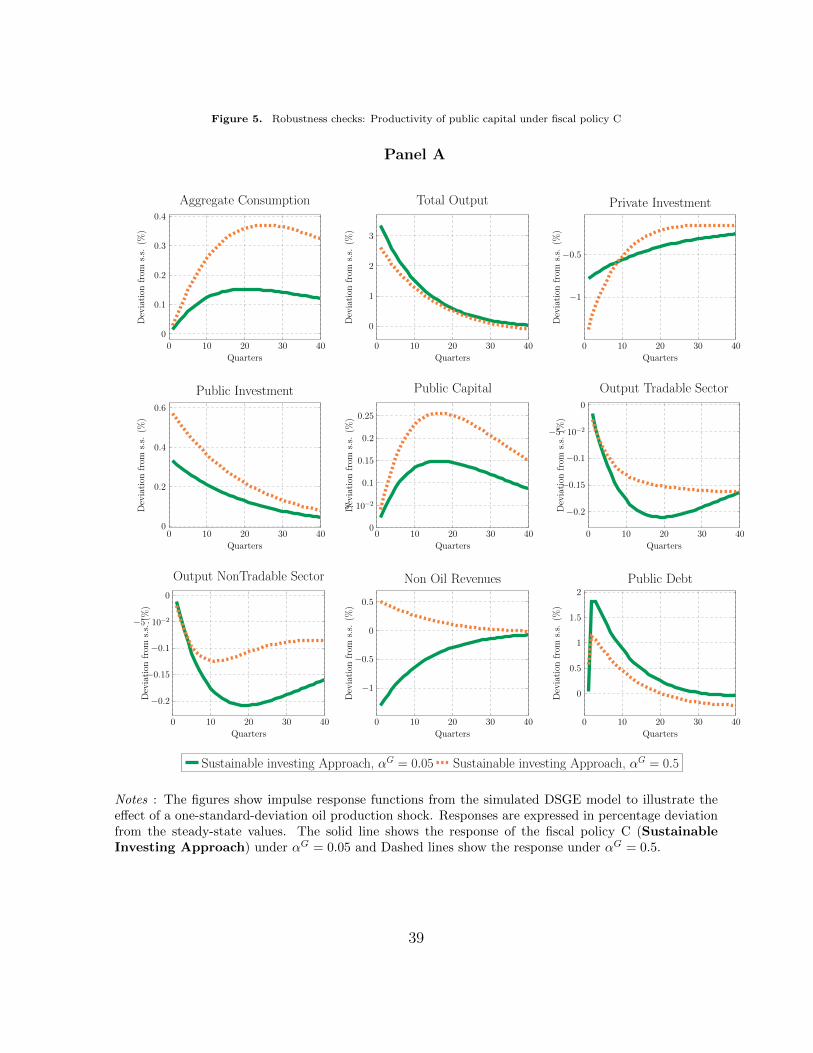

The monopolistic producer i ∈ (0, 1) uses the following technology

yNt = aNt(kNt)αN · (lNt )(1−αN ) ·

(kGt)αG

(2.13)

where aNt is the sectoral total factor productivity (TFP), and kGt−1 is the public capital stock

with an output elasticity of αG. This production technology is well received and documented

in neoclassical literature, featuring public capital as a key input. Following this literature,

Baxter and King (1993) and Kamps (2004) have considered a constant returns to scale function

associated with private inputs (private capital and labor) and an increasing returns to scale

technology, when considering all input factors including public capital. Relative to another

2These assumptions and their quantitative implications are well documented in Ambler et al. (2004),Cherif and Fuad (2012) and Jihad et al. (2012).

9

common specification with constant return to scale to all production factors, this specification

has the advantage that αT and αN can be calibrated to match income shares of labor and private

capital of an economy. Finally, this specification has the advantage to facilitate the steady-state

computation. Private capital evolves by the law of motion

kNt+1 = (1− δN )kNt +

1− ϕN

2

(kNt+1

kNt− 1

)2 iNt︸ ︷︷ ︸

Θ(kNt )

(2.14)

where, Θ(kNt ), is the investment adjustment cost function, satisfying: Θ(1) = Θ′(1) and Θ′′ > 0.3

As in Obstfeld and Rogoff (2000), the monopolistic producer i faces a demand function for the

variety i

yNt (i) =

[pNt (i)

pNt

]yNt , (2.15)

where yNt is the aggregate non-traded demand. A representative non-traded good firm chooses

its price (pNt (i)), labor demand (lNt (i)), and capital stock (kNt+1(i)) to maximize its net present-

value profits, weighted by the household’s marginal utility of consumption (λt).

Et

∞∑t=0

βtλt[(1− ι)pNt (i)yNt (i)− wNt lNt −Adjt(i)− rNt kNt (i) + ιpNt y

Nt

](2.16)

subject to the production function defined in equation [2.13] and the demand function in equation

[2.15]. ι captures distortions in developing countries that discourage firms from investing and

hiring further. ι may be viewed as a distorting tax on firms, but revenue collected remains in

the private sector and is distributed to households and profits. Additionally, this tax helps to

match the relatively low investment to GDP ratios observed in developing countries. However,

this implicit tax is rebated back to the firms as lump-sum transfers.

Denoting by λNt , the Lagrange multiplier associated with the optimization program, which

also may be interpreted as the real marginal cost of producing one unit of output yNt , then the

3Under this specification, the steady-state level of capital stock is not affected by the presence ofadjustment costs.

10

first order conditions of a costs minimizing problem are given by

rNt = λNt αN (1− ι)y

Nt

kNt,

wNt = λNt (1− αN )(1− ι)yNt

lNt,

(2.17)

Price setting: Price rigidity is introduced following a strategy a la Calvo. To this end, we

assume that in each period, a fraction φp of firms cannot change their prices. When allowed to

do so, firm in the non-tradable goods sector chooses the price of its output, pNt (j), in order to

maximize its discounted real profits. All other firms can only index their prices to past inflation

of the composite good price. Indexation is controlled by χp ∈ (0, 1) (χp = 0 refers to a no

indexation case while χp = 1 is a perfect indexation). Intermediate good producer j chooses

the optimal price pNt (j) at the time t. Then, after h periods with no reoptimizing, firm’s price

would evolve over time according to the following recursive equation

pNt+h(j) = (πt+1)χp × (πt+2)χp × · · · × (πt+h−1)χp × pNt (j) =

h−1∏i=1

(πt+i)χppNt (j), (2.18)

where πt+h = pt+h/pt+h−1. The problem of firm j is then:

maxpNt (j)

Et

∞∑i=0

(βφp)lλNt+h

(h−1∏i=1

(πt+i)χp p

Nt (j)

pNt+h−mct+h

)yNt+h(j)

s.c. yNt+h(j) =

(h−1∏i=1

(πt+i)χp p

Nt (j)

pNt+h

)−ξpyNt+h,

(2.19)

where λNt+h is the marginal utility of wealth for a firm j after t + h periods. Assuming that all

firms of type j adopt a same strategy, then the first order condition related to the optimal price

of a domestic intermediate good j is

pNt =ξp

ξp − 1

Et

∞∑i=0

(βφp)hλNt+h

(h−1∏i=1

(πt+i)χp

πt+i+1

)−ξptyNt+h(j)

Et

∞∑i=0

(βφp)lλNt+h

(h−1∏i=1

(πt+i)χp

πt+i+1

)1−ξh,t

yNt+h(j)

, (2.20)

11

In the case of a full indexation (χp = 1), equation [2.20] may be rewritten to derive the New

Keynesian Phillips curve given by: (pNt )1−ξp = φp(pNt−1)1−ξp + (1− φp)(pNt )1−ξp .

Wage setting: Recall that households supply differentiated labor inputs used by interme-

diate good producers and set their nominal wage using Calvo’s partial indexation. We assume

that the aggregate labor is supplied by a representative competitive firm that hires labor sup-

plied by households individually. The differentiated labor inputs supplier aggregates labor using

a constant elasticity of substitution function given by lNt =(∫ 1

0 lNt (i)

ξw−1ξw di

) ξwξw−1

, where ξw

(ξw ∈ (0,∞)) is the elasticity of substitution among different types of labor. The differentiated

labor inputs supplier maximizes profits subject to the production function given all differenti-

ated labor wages, wNt (i), and the aggregate wage, wNt . The first order conditions are such that

lNt (i) =(wNt (i)

wNt

)−ξwlNt and wNt =

(∫ 10 w

Nt (i)1−ξwdi

) 11−ξw . Following Calvo (1983), we include

nominal rigidities on households’ wage setting. Thus, in each period, a fraction 1 − φw can

change their wages, i.e., households only reset optimally the wage contract in states of nature

with a constant probability 1−φw. All others are not able to lay out the optimal wage contract.

In that case, they can only partially index their wages to the past inflation of the composite

domestic goods. The level of indexation is captured by χw ∈ (0, 1). This nominal rigidity implies

that if the household cannot change its wage for h periods, then, its normalized wage is given

byh∏i=1

πχwt+s−1

πt+i

wNt (i)

pt.

Recall that, under the labor supply constraint ( lNt+h(i) =

(∏hi=1

πχwt+h−1

πt+h

wNt (i)

wNt+h

)−ξwlNt+h), the

efficient wage can be written as a geometric average of past real wage and the new optimal wage

in the case of full indexation π1−ξwt

(wNt)1−ξw = φw

(wNt−1

)1−ξw π1−ξwt−1 +(1−φw)π1−ξw

t

(wNt)1−ξw .

2.2.2 Traded Good Sector (Exportable Goods)

I Intermediate tradable good production:

The intermediate traded good sector is perfectly competitive and goods are produced using

12

a similar technology to that in the non-traded good sector.

yiTt = aTt(kTt)αT · (lTt )(1−αT ) ·

(kGt)αG

(2.21)

The total factor productivity (TFP) in the tradable good sector, aTt , is subject to learning-by-

doing externalities, depending on the last period traded output: lnaTt = ρzT lnaTt−1 + d ln yTt−1.

Private capital in the traded good sector also evolves by the law of motion

kTt+1 = (1− δT )kTt +

1− ϕT

2

(kTt+1

kTt− 1

)2 iTt︸ ︷︷ ︸

Θ(kTt )

. (2.22)

Each firm maximizes its weighted present-value profits,

Et

∞∑t=0

βtλTt[(1− ι)styTt (i)− wTt lTt −AdjTt (i)− rTt kTt (i) + ιsty

Tt

](2.23)

Let λTt be the Lagrange multiplier associated with the production function constraint in the

tradable goods sector, which may be interpreted as the real marginal cost of producing one unit

of output yTt . The first order conditions of a minimizing problem are given by

rTt = λTt αT (1− ι)y

iTt

kTt,

wTt = λTt (1− αT )(1− ι)yiTt

lTt,

(2.24)

A part of the intermediate traded good production in the traded goods sector, yTdt , is used for

the domestic market and the remaining part, yTx, is exported in fully competitive market. So

that,

yiTt = yTdt + yTxt . (2.25)

The foreign demand for locally produced goods is as follows:

yTxt =

(pxtp∗t

)−µy∗t , (2.26)

13

where (µ − 1)/µ captures the elasticity of substitution between the exported goods and

foreign-produced goods in the consumption basket of foreign consumers, and y∗t and p∗t are,

respectively, foreign output and the price index. Both variables are exogenously given.

I Final tradable good production:

There is a continuum of intermediate-good-importing firms in a monopolistic competition

market for, which are imperfect substitutes for each other in the production of the composite

imported good, yMt , produced by a representative competitive firm. We also assume Calvo-

type staggered price setting in the imported goods sector to capture the empirical evidence on

incomplete exchange rate pass-through into import prices. The final traded good is produced

by a competitive firm that uses domestically consumed traded goods, yTdt , and imports goods,

yMt following a CES technology

yTt =

(φ

1νm

(yTdt

) ν−1ν

+ (1− φm)1ν(yMt) ν−1

ν

) νν−1

, (2.27)

where φm is the share of domestically consumed traded goods in the final traded goods basket at

the steady state, and ν (ν > 0) is the elasticity of substitution between domestic and imported

goods. The first-order conditions lead to

yTdt = φm

(pdtst

)−νyTt , (2.28)

yMt = (1− φm)

(pMtst

)−νyTt . (2.29)

The final traded good price, pT , which corresponds to the numeraire of our economy is given

by

1 =

[φm

(pdt

)1−ν+ (1− φm)

(pMt)1−ν] 1

1−ν. (2.30)

2.2.3 Natural Resource Sector

Output in the natural resource sector is assumed to follow an exogenous process. This assump-

tion is consistent with the empirical observations since most natural resource production is in

14

reality capital intensive and does not depend on country’s endogenous factors. In addition, most

of resource investments in low-income countries is financed by foreign direct investment (FDI)

that controls the level of oil exploitation. The production function is

ln

(yOtyO

)= ρyo ln

(yOt−1

yO

)+ εyot , (2.31)

where the exogenous process returns to the steady-state level yO with the autoregressive param-

eter ρyo. The resource production shock is assumed to be εyot ∼ i.i.d. and follows a standard

normal distribution with a standard deviation of σyo (εyot ∼ N(0, σ2yo)).

The country’s resource output is assumed relatively small in the world market. Consequently,

Uganda’s resource production is assumed to not be able to affect the international commodity

price pO∗

t . As a result, the international commodity price pO∗

t (relative to the foreign goods)

evolves according to an exogenous process defined by

ln

(pO

∗t

pO∗

)= ρpo ln

(pO

∗t−1

pO∗

)+ εpot , (2.32)

where the international commodity price shock εyot ∼ N(0, σ2yo), and is an i.i.d. process. The

resource GDP from the natural resource sector in units of domestic composite consumption is:

Y Ot = stp

O∗t yOt . (2.33)

As in many resource-rich economies, resource production in Uganda is subject to a royalty at a

rate of τ ot . Thus, the resource revenue collected from the natural resource sector is

TOt = st

(τ ot p

O∗t yOt

)= stT

O∗t . (2.34)

where TO∗t is the resource revenue collected from the natural resource sector expressed in foreign

goods.

15

2.3 Public Sector

The model allows for flexible public policy specifications, and we assume that the public sector

consists of a government and a central bank. In each period, government receives taxes and

contracts domestic debt bt. Total expenditures include government consumption (gCt ), public

investment (gIt ) and debt services. If capital letters denote the aggregate level of a variable, then

government budget constraint may be written as

TOt + τCt Ct + τ ltWtLt +Bt +st(1 + r∗)

π∗tF ∗t−1 = pgtGt +

Rt−1Bt−1

πt+ stF

∗t , (2.35)

where F ∗t is the asset value of resource fund, which generates a constant interest rate r∗. In

[2.36], Gt is government purchases with a relative price to composite consumption goods of pgt .

The model allows external assets accumulation, while we abstracts from external commercial

borrowing. Despite taxing revenues from the non-tradable and tradable goods sectors (ιpNt YNt

and ιstYTt ), the government is unable to use this as an additional source of fiscal revenue.

Consequently, this tax does not appear as revenue in the government’s budget constraint (2.36).

By assuming that they are rebated to the firms, the model captures the inefficiencies of revenue

mobilization in Uganda. Including this feature, our specification makes explicit the challenges

that fiscal authorities in developing economies face regarding tax revenue mobilization. However,

the government collects taxes on revenues from the natural resource sector and they account as

a financing source for public infrastructures.

We define the non-oil fiscal balance that will be used for the fiscal stability measure in the

investigations about the optimal share of oil revenue to be used for public investment as follows:

FBNOt = τCt Ct + τ ltWtLt +Bt − pgtGt −

Rt−1Bt−1

πt. (2.36)

Finally, government purchases consist of expenditures on government consumption GCt and

public investment GI . As in the private consumption, we assume that government purchases

are a CES function of traded and non-traded goods.

Gt =

[η

1χ(GNt)χ−1

χ + (1− η)1χ(GTt)χ−1

χ

] χχ−1

, (2.37)

16

where η is the degree of home bias in government purchases. The relative price of government

consumption to private consumption is

pgt =[η(pNt)1−χ

+ (1− η) (st)1−χ] 1

1−χ. (2.38)

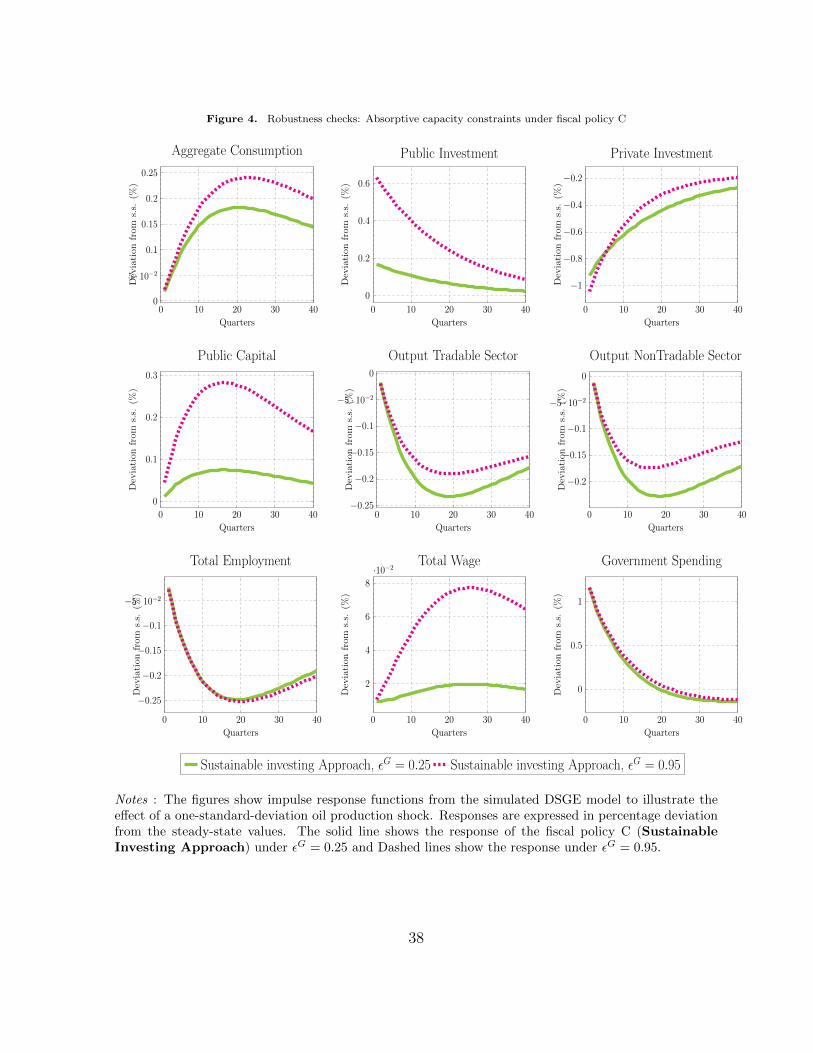

2.3.1 Absorptive Capacity Constraints and Inefficiency of Public Investment

In our framework, we introduce the concept of inefficiency of public investment to capture the

stylized fact of effective public investment in low-income countries by allowing the model to take

into account potential investment inefficiencies and absorptive capacity constraints. As a result,

public investment generates capital accumulation following this law of motion

kGt+1 = (1− δG)kGt + εGGIt , (2.39)

where 0 < (1 − εG) ≤ 1 governs the inefficiency of public investment and δG is the constant

depreciation rate of public capital.

2.3.2 Fiscal Policy

In this framework, we introduce three approaches to analyze fiscal policy in Uganda, which are

different from the use of the fund from the natural resource sector. This involves three regimes of

management of the fiscal policy: the all-investing, the all-saving and the sustainable approaches.

I Policy A: The All-Investing Approach.

Under this approach, the resource fund stays at its initial level, and all additional revenues from

the natural resources sector as well as wage and consumption taxes, and revenues from bonds

issuance are invested in public infrastructures and government consumption. Thus, F ∗t = F ∗,

∀t, while public investment evolves as follows:

GIt = GI +

[TOtpgt− TO

pg

], (2.40)

Gt = GCt +GIt , and (2.41)

17

F ∗t = F ∗, ∀t ∈ [0,∞), (2.42)

where GI , TO and pg are, respectively, the steady state values of GIt , TOt and pgt .

I Policy B: The Saving in a Sovereign Wealth Fund.

Under this fiscal policy, all the resource revenues are saved externally in a sovereign wealth fund

for the future generation. Thus, the resource fund evolves as follows:

F ∗t = F ∗t−1 +

[TOtst− TO

s

](2.43)

Gt = GCt +GIt , and (2.44)

GIt = GI , (2.45)

where s is the steady state values of the real exchange rate.

I Policy C: The Sustainable Investing Approach.

This approach, which may be viewed as a combination of the first two fiscal policies, allows

a constant share of the resource revenues to finance public investment and the remaining part

is saved in a sovereign wealth fund. Under this fiscal policy, the country’s foreign wealth and

public investment are defined as follows:

GIt = GI + φoil[TOtpgt− TO

pg

], (2.46)

Gt = GCt +GIt , and (2.47)

F ∗t = F ∗t−1 + (1− φoil)[TOtst− TO

s

], (2.48)

where φoil is a fiscal policy parameter that satisfies 0 ≤ φoil ≤ 1. At this point, it’s worth

mentioning that the Sustainable Investing Approach and the all-investing approach produce the

same fiscal responses under φoil = 1, and the all-saving approach is obtained by setting φoil = 0.

18

2.3.3 Central Bank

Monetary policy is conducted by the central bank, which manages the short-term nominal

interest rate Rt = (1 + rbt ), in response to fluctuations in domestic output gap and in consumer

price inflation gap using a Taylor-type rule. This managing rule allows the central bank to

smooth nominal interest rates through open market operations.4

log(Rt/R

)= λr log

(Rt−1/R

)+ (1− λr)

(λπlog (πt/π) + λy log

(Yt/Y

))+ ϕt, (2.49)

where Yt denotes the country’s growth domestic product (GDP) and ϕt are i.i.d. normal inno-

vations with a standard deviation of σr.

2.4 Rest of the World

Following the 2014 World Economic Outlook (WEO) released by the IMF, Uganda is considered

as a small open economy. Consequently, a plausible assumption is to assume that domestic

developments do not affect the rest of the world economy. However, the foreign economy’s

dynamics (oil prices) have an impact on the domestic economy. For simplicity, we assume that

the foreign interest rate, foreign output and the world inflation rate are exogenous and follow

AR(1) processes.

2.5 Market Clearing and Competitive Equilibrium

In a competitive equilibrium, the markets for goods, labor and capital all clear. The goods

markets clears when the demand from the agents can be meet by the production of the final

good. To do this, we define real aggregate GDP as the sum of value added in the three sectors,

measured by their steady state prices.

Yt = pNt YNt + stY

T + Y Ot . (2.50)

4The use of the previous period interest rate allows us to match the smooth profile of the observedinterest rate in the data.

19

Then, the general equilibrium in the goods markets involves:

(Ct + It + pGt Gt) + (pxt YTxt − pMt YM

t ) + st(F ∗t − F ∗t−1

)= Yt + str

∗F ∗t−1, (2.51)

where It = INt + ITt is the private investment, and Ct = CNt + CTt is the total consumption.

Recall that government purchases consist of expenditures on government consumption GCt and

public investment GI , therefore Gt = GCt + GIt . Let denote by CAt the current account, then

the balance of payment condition is given by

CAt = pxt YTxt − pMt YM

t + st[(F ∗t − F ∗t−1

)]. (2.52)

Then, labor market clearing requires demand for labor by firms in both sectors to equal the

sector specific supply of labor. This implies that:

Wt ≡∫ 1

0wt(i)di =

∫ 1

0(wNt (i) + wTt (i))di = WN

t +W Tt (2.53)

and

Lt ≡∫ 1

0lt(i)di =

∫ 1

0(lNt (i) + lTt (i))di = LNt + LTt = Ldt , (2.54)

where Ldt denotes total demand for labor by firms in both sectors.

Finally, capital market clearing conditions imply that:

Kt ≡∫ 1

0kt(j)dj =

∫ 1

0(kNt (j) + kTt (i))di = KN

t +KTt , (2.55)

and ∫ 1

0Bt(i)di = 0. (2.56)

2.6 Driving Forces

There are seven sources of uncertainty in our framework: One productivity shock in each of the

two sectors (tradable and non-tradable), an oil price shock that aims to capture the volatility

in the oil price markets, an oil production shock, a foreign demand shock, a foreign price shock

20

captured by foreign inflation and a domestic monetary policy shock. We assume that all shocks

follow autoregressive processes of order one. This assumption gives rise to the following laws of

motion:

ln(aNt ) = ρzN ln(aNt−1) + εNZ,t : Productivity shock in the non-tradable sector

ln(aTt ) = ρzT ln(aTt−1) + εTZ,t : Productivity shock in the tradable sector

ln(ϕt) = ρϕ ln(ϕt−1) + εϕ,t : Monetary policy shock

ln(Y Ot /Y

O)

= ρyo ln(Y Ot−1/Y

O)

+ εyot : Oil production shock

ln(PO

∗t /PO

∗)

= ρpo ln(PO

∗t−1/P

O∗)

+ εpot : Oil price shock

ln(π∗t ) = (1− ρπ∗) ln(π∗) + ρπ∗ ln(π∗t−1) + επ∗t : World price shock

ln(Y ∗t ) = (1− ρY ∗) ln(Y ∗) + ρY ∗ ln(Y ∗t−1) + εY ∗t : Foreign demand shock

(2.57)

2.7 Competitive equilibrium

A competitive equilibrium is defined as a set of sequences of functions for (i) households’ policies

Ct(i), Lt(i), Bt(i) and It(i) that solve the maximization problem of the household; (ii) firms’

policies Kt(j), Ldt (j) and Wt(i) that solves firms maximization problem; (iii) aggregate prices

PNt , P xt , St and P ∗t ; (iv) saving and consumption decision rules for government; and (v) all

markets clear. The equilibrium system of the model consists of the private agents optimal-

ity conditions, the government budget constraint, fiscal policy, market clearing conditions, the

balance of payment condition, and the exogenous processes of the shocks.

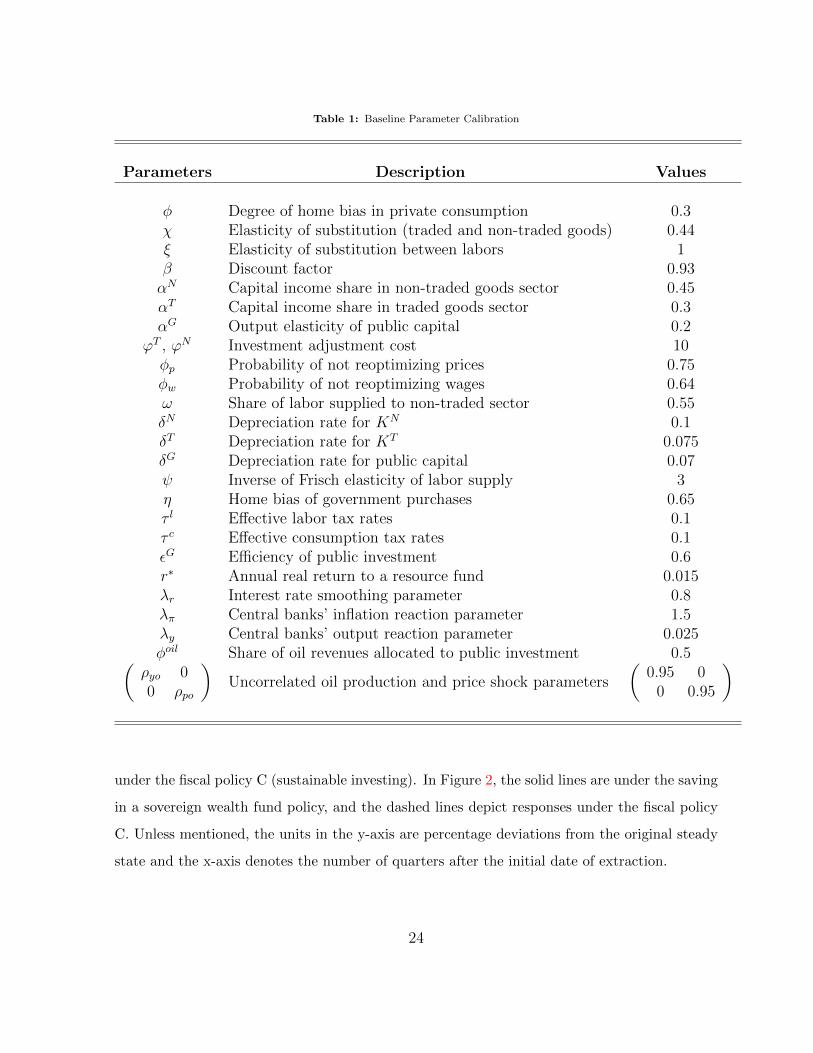

3 Model Calibration

To evaluate the impact of fiscal responses to resource revenue on macroeconomic stability in

Uganda, we set the parameters of our model to reflect most of key features of a small-open

economy with abundant natural resources. The model is at the quarterly frequency, and Tables

1, 2 summarize the baseline calibrations and some steady-state ratios using macroeconomic

fundamentals of the Uganda. These parameters and ratios are consistent to those in line with the

evidence for low-income countries and calibrated in Angenor and Aizenman (1999), Goldberg

21

(2011) and Agenor (2014). Data sources used to match key ratios include the IMF’s World

Economic Outlook (WEO) database, the oil and revenue management policy framework provided

by the Uganda’s Ministry of Finance and various research papers such as Pritchett (2000),

Goldberg (2011), Angenor and Aizenman (1999), Kopoin et al. (2013) and Agenor (2014).

In the representative household’s utility function, the weight on leisure ψ is set to 3, which

leads to the steady-state value of household work effort to be 40 percent of available time. The

household’s discount factor, β, is set 0.93, implying a long-run real interest rate of 9.68 percent

annually. This assumption is fairly reasonable and consistent regarding banks’ interest rates in

most of low-income countries (see African Development Indicators (ADI)). In addition, the share

of capital in the production function for intermediate goods in the non-traded goods sector, αN ,

is set to 0.45, while it is set to 0.3 in the traded goods sector. These values indicate that the

informal (non-tradable goods sector) sector is more intensive in labor than the tradable goods

sector. The depreciation rates of capital are fixed to 0.1 in the informal sector and 0.075 in

the tradable goods sector. All these values are consistent with studies on Sub-Saharan African

countries and reported in Jihad et al. (2012), Cherif and Fuad (2012) and Agenor (2014).

In our paper, we use the empirical evidence based on Mexican data from 1980 to 1994 by

Arestoff and Hurlin (2006) to pin-down the parameter that governs the efficiency of public invest-

ment εG. This paper shows that the coefficient of regressing public capital produced (effective

investment in our model) on investment expenditures falls between 0.4 and 0.65. This range of

investment efficiency is in line with the estimates in Pritchett (2000) for Sub-Saharan African

countries with a linear specification between effective investment and investment expenditures.

Based on these empirical papers and the macroeconomic efforts undertaken by the government

to sustain public investment, we set εG to 0.6.

The nominal price rigidity parameter in the non-traded goods sector, as well as the nominal

wage-setting parameter are set following Calvo’s model of staggered price and wage adjustment.

As in Christiano et al. (2005), the probability of not reoptimizing for price and wage setters in

the domestic country, φp and φw, are fixed to 0.75 and 0.64, respectively. The degree of home

bias in private consumption, φ, and the elasticity of substitution between domestic labor types,

ξ, are set to 0.4 and 1, respectively. These values are estimated in Christiano et al. (2010) for

22

the U.S. economy and are commonly used in the literature of developing countries.

The domestic monetary policy parameters λr, λπ et λy are set to 0.8, 1.5 and 0.1/4, respec-

tively. These values satisfy the Taylor principle and are consistent to those estimated in Agenor

(2014) and Kopoin et al. (2013). The standard deviation of both domestic and foreign mone-

tary policy shocks is fixed to 0.0016, ρmp = ρRf = 0.0016, which ensures that a one-standard

deviation shock moves the interest rate by 0.6 percentage points. This value is consistent to the

empirical estimates reported in Christiano et al. (2005).

The model is solved using a second-order perturbation method around its deterministic

steady state.

4 Findings

The patterns of investment and saving out of income from the oil windfall in managing of the

optimal fiscal policy remain ambiguous for policymakers. In practice, the key issue for the

spending of oil revenue by the government, viewed as a Ramsey problem, is to scale up public

investment to meet huge needs in public infrastructure without generating higher public sector

deficits and a Dutch disease in an uncertain oil production world, characterized by unexpected

shocks and prices volatility. To address this issue with our baseline DSGE model, we simulate

the effects of oil production shocks and interpret it as a boom in the oil sector. Using the

parameters calibrated to reflect the key features of a small open economy such as Uganda, we

focus on the impulse response functions of some key variables. Throughout, we simulate and

compare the impulse responses to a one standard-deviation shock to the oil production.

Figures 1, 2 and 3 show impulse responses by illustrating macroeconomic dynamics under

three stylized fiscal policy approaches for managing a resource windfall: investing in public

capital, saving in a sovereign wealth and sustainable investing in public capital. In Table 1, the

solid lines present the responses under the fiscal policy A (investing in public capital), and the

dashed lines are under the fiscal policy B (saving in a sovereign wealth fund). Solid lines in

Figure 3 remain the responses under the fiscal policy A, while dashed lines present responses

23

Table 1: Baseline Parameter Calibration

Parameters Description Values

φ Degree of home bias in private consumption 0.3χ Elasticity of substitution (traded and non-traded goods) 0.44ξ Elasticity of substitution between labors 1β Discount factor 0.93αN Capital income share in non-traded goods sector 0.45αT Capital income share in traded goods sector 0.3αG Output elasticity of public capital 0.2

ϕT , ϕN Investment adjustment cost 10φp Probability of not reoptimizing prices 0.75φw Probability of not reoptimizing wages 0.64ω Share of labor supplied to non-traded sector 0.55δN Depreciation rate for KN 0.1δT Depreciation rate for KT 0.075δG Depreciation rate for public capital 0.07ψ Inverse of Frisch elasticity of labor supply 3η Home bias of government purchases 0.65τ l Effective labor tax rates 0.1τ c Effective consumption tax rates 0.1εG Efficiency of public investment 0.6r∗ Annual real return to a resource fund 0.015λr Interest rate smoothing parameter 0.8λπ Central banks’ inflation reaction parameter 1.5λy Central banks’ output reaction parameter 0.025φoil Share of oil revenues allocated to public investment 0.5(

ρyo 00 ρpo

)Uncorrelated oil production and price shock parameters

(0.95 0

0 0.95

)

under the fiscal policy C (sustainable investing). In Figure 2, the solid lines are under the saving

in a sovereign wealth fund policy, and the dashed lines depict responses under the fiscal policy

C. Unless mentioned, the units in the y-axis are percentage deviations from the original steady

state and the x-axis denotes the number of quarters after the initial date of extraction.

24

Table 2: Steady-state Values in percentage of total output

Steady-state ratios Description Values

Y O/Y Oil revenues to GDP ratio in steady state 0.072I/Y Total investment to GDP ratio in steady state 0.1468Y T/Y Tradable to GDP ratio in steady state 0.329Y N/Y Tradable to GDP ratio in steady state 0.665LN/L Share of employment in non-tradable sector 0.583LT/L Share of employment in tradable sector 0.417CN/C Non-tradable goods consumption to C 0.316GC/Y Government consumption to GDP ratio in steady state 0.53GI/Y Public investment to GDP ratio in steady state 0.32

F ∗/GDP Sovereign wealth fund to GDP ratio in steady state 0.08

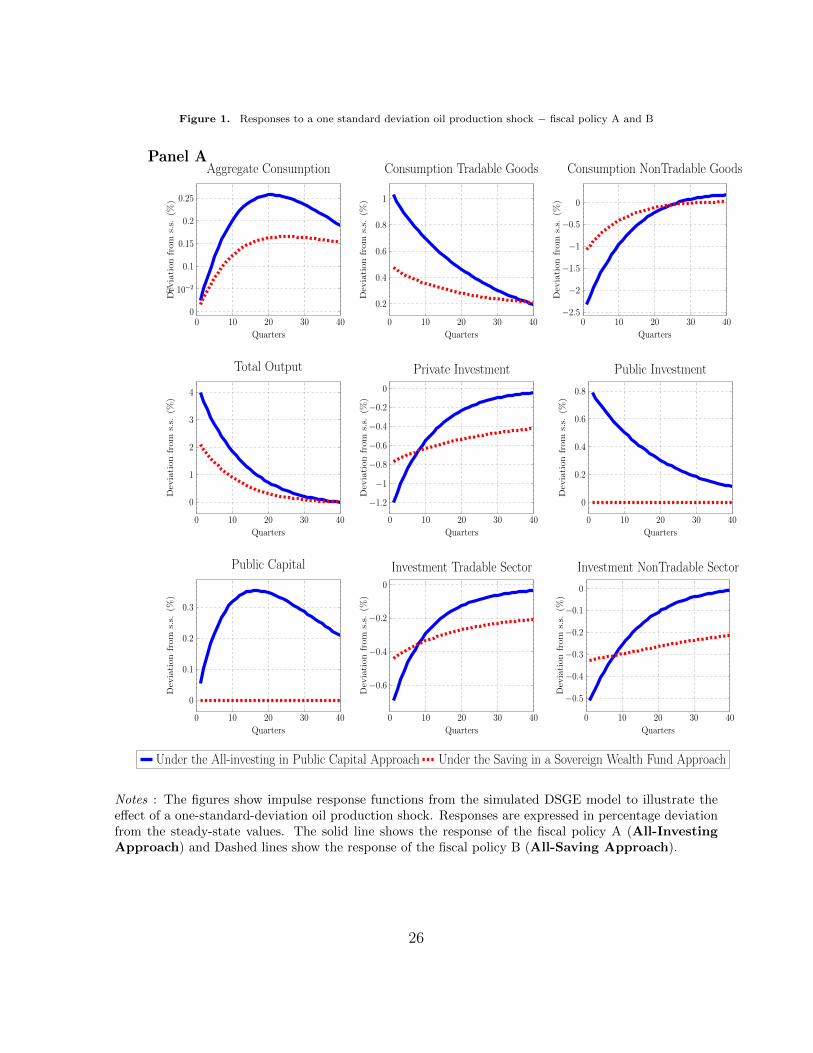

4.1 All-investing and saving in a sovereign wealth fund

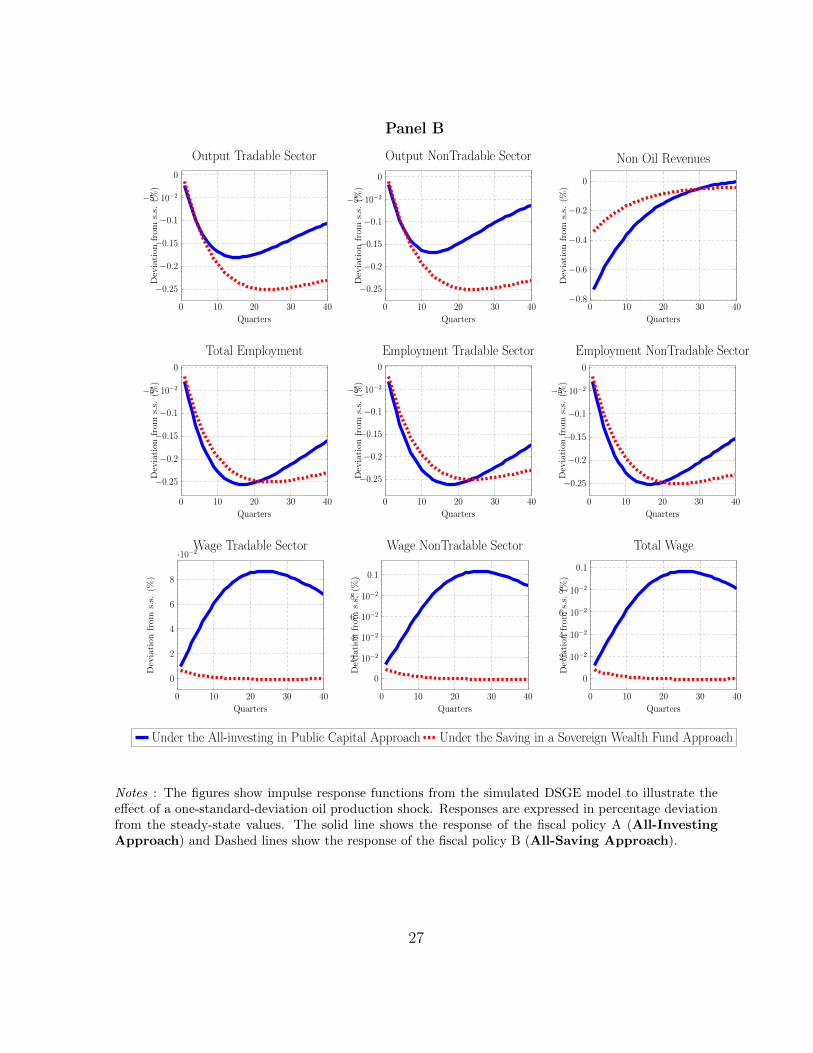

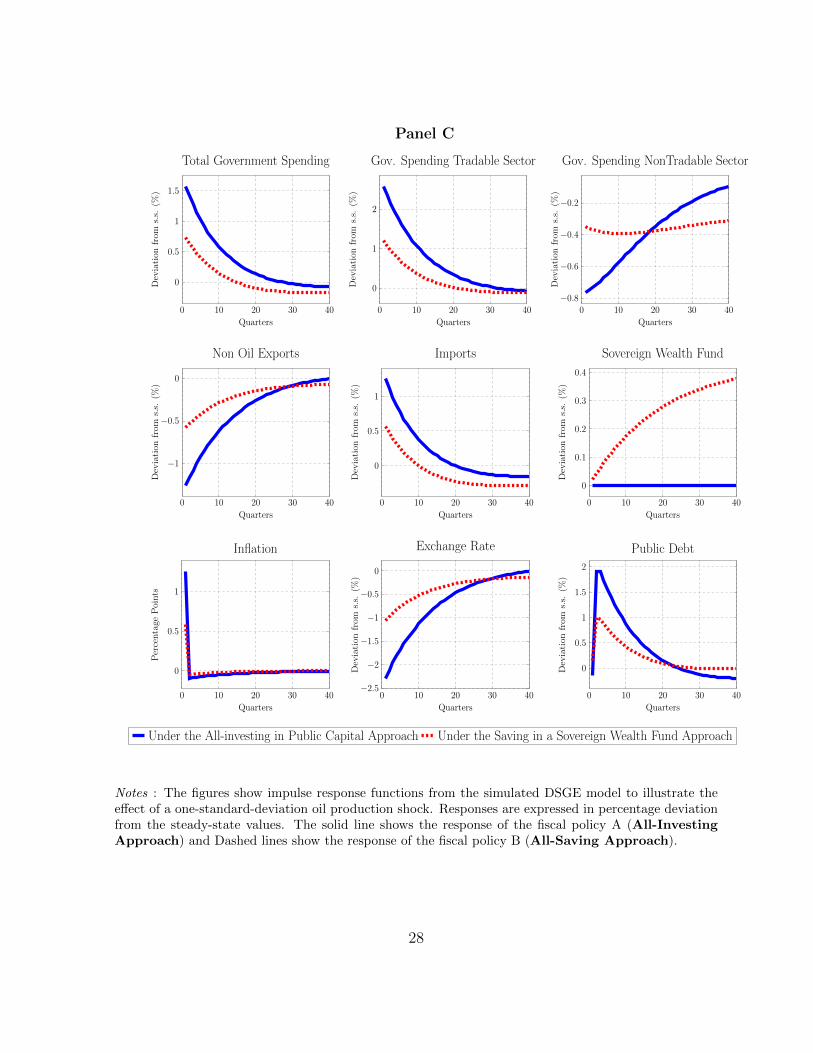

In response to an increase in the oil production, oil output and total output rise gradually,

and this drives up the oil revenue. Under the saving in a sovereign wealth fund policy, foreign

reserves increase permanently, reaching around 10 percent of GDP after 10 years (Figure 1,

panel A and C). As higher output means more income to households, under the all-investing

approach, this exogenous shock leads to an increase in the private consumption to reach about

0.25 percent after 5 years (Figure 1, panel A). On the other hand, since the government budget

constraint includes interest earnings from foreign reserves, private consumption also rises under

the saving in a sovereign wealth fund policy, reaching around 0.17 percent after 6 years. Higher

private consumption, in turn, leads households to reduce labor supply by about 0.25 percent and

lower the marginal product of private investment. Consequently, wages increase sharply in both

the tradable and the non-tradable goods sectors. Lower labor supply and private investment

lead to a decline of non-oil GDP (Figure 1, panel A and B). Public capital also rises sharply by

around 0.35 percent after 3 years and half under the all-investing approach, and remains at the

pre-windfall level under the all-saving approach because none of the resource income is allocated

for public investment (Figure 1, panel B).

25

Figure 1. Responses to a one standard deviation oil production shock − fiscal policy A and B

7 Simulated results

Table 3: Responses to a one standard deviation oil production shock − fiscal policy A and B

Panel A

0 10 20 30 400

5 · 10−2

0.1

0.15

0.2

0.25

Quarters

Dev

iati

on

from

s.s.

(%)

Aggregate Consumption

0 10 20 30 40

0.2

0.4

0.6

0.8

1

Quarters

Dev

iati

on

from

s.s.

(%)

Consumption Tradable Goods

0 10 20 30 40−2.5

−2

−1.5

−1

−0.5

0

Quarters

Dev

iati

on

from

s.s.

(%)

Consumption NonTradable Goods

0 10 20 30 40

0

1

2

3

4

Quarters

Dev

iati

on

from

s.s.

(%)

Total Output

0 10 20 30 40

−1.2

−1

−0.8

−0.6

−0.4

−0.2

0

Quarters

Dev

iati

on

from

s.s.

(%)

Private Investment

0 10 20 30 40

0

0.2

0.4

0.6

0.8

Quarters

Dev

iati

on

from

s.s.

(%)

Public Investment

0 10 20 30 40

0

0.1

0.2

0.3

Quarters

Dev

iati

on

from

s.s.

(%)

Public Capital

0 10 20 30 40

−0.6

−0.4

−0.2

0

Quarters

Dev

iati

on

from

s.s.

(%)

Investment Tradable Sector

0 10 20 30 40

−0.5

−0.4

−0.3

−0.2

−0.1

0

Quarters

Dev

iati

on

from

s.s.

(%)

Investment NonTradable Sector

Under the All-investing in Public Capital Approach Under the Saving in a Sovereign Wealth Fund Approach

Notes : The figures show impulse response functions from the simulated DSGE model toillustrate the effect of a one-standard-deviation oil production shock. Responses are

expressed in percentage deviation from the steady-state values. The solid line shows theresponse of the fiscal policy A (All-Investing Approach) and Dashed lines show the

response of the fiscal policy B (All-Saving Approach).

49

Notes : The figures show impulse response functions from the simulated DSGE model to illustrate theeffect of a one-standard-deviation oil production shock. Responses are expressed in percentage deviationfrom the steady-state values. The solid line shows the response of the fiscal policy A (All-InvestingApproach) and Dashed lines show the response of the fiscal policy B (All-Saving Approach).

26

Panel B

0 10 20 30 40

−0.25

−0.2

−0.15

−0.1

−5 · 10−2

0

Quarters

Dev

iati

on

from

s.s.

(%)

Output Tradable Sector

0 10 20 30 40

−0.25

−0.2

−0.15

−0.1

−5 · 10−2

0

Quarters

Dev

iati

on

from

s.s.

(%)

Output NonTradable Sector

0 10 20 30 40−0.8

−0.6

−0.4

−0.2

0

Quarters

Dev

iati

on

from

s.s.

(%)

Non Oil Revenues

0 10 20 30 40

−0.25

−0.2

−0.15

−0.1

−5 · 10−2

0

Quarters

Dev

iati

on

from

s.s.

(%)

Total Employment

0 10 20 30 40

−0.25

−0.2

−0.15

−0.1

−5 · 10−2

0

Quarters

Dev

iati

on

from

s.s.

(%)

Employment Tradable Sector

0 10 20 30 40

−0.25

−0.2

−0.15

−0.1

−5 · 10−2

0

Quarters

Dev

iati

on

from

s.s.

(%)

Employment NonTradable Sector

0 10 20 30 40

0

2

4

6

8

·10−2

Quarters

Dev

iati

on

from

s.s.

(%)

Wage Tradable Sector

0 10 20 30 40

0

2 · 10−2

4 · 10−2

6 · 10−2

8 · 10−2

0.1

Quarters

Dev

iati

on

from

s.s.

(%)

Wage NonTradable Sector

0 10 20 30 40

0

2 · 10−2

4 · 10−2

6 · 10−2

8 · 10−2

0.1

Quarters

Dev

iati

on

from

s.s.

(%)

Total Wage

Under the All-investing in Public Capital Approach Under the Saving in a Sovereign Wealth Fund Approach

Notes : The figures show impulse response functions from the simulated DSGE model toillustrate the effect of a one-standard-deviation oil production shock. Responses are

expressed in percentage deviation from the steady-state values. The solid line shows theresponse of the fiscal policy A (All-Investing Approach) and Dashed lines show the

response of the fiscal policy B (All-Saving Approach).

50

Notes : The figures show impulse response functions from the simulated DSGE model to illustrate theeffect of a one-standard-deviation oil production shock. Responses are expressed in percentage deviationfrom the steady-state values. The solid line shows the response of the fiscal policy A (All-InvestingApproach) and Dashed lines show the response of the fiscal policy B (All-Saving Approach).

27

Panel C

0 10 20 30 40

0

0.5

1

1.5

Quarters

Dev

iati

on

from

s.s.

(%)

Total Government Spending

0 10 20 30 40

0

1

2

Quarters

Dev

iati

on

from

s.s.

(%)

Gov. Spending Tradable Sector

0 10 20 30 40−0.8

−0.6

−0.4

−0.2

Quarters

Dev

iati

on

from

s.s.

(%)

Gov. Spending NonTradable Sector

0 10 20 30 40

−1

−0.5

0

Quarters

Dev

iati

on

from

s.s.

(%)

Non Oil Exports

0 10 20 30 40

0

0.5

1

Quarters

Dev

iati

on

from

s.s.

(%)

Imports

0 10 20 30 40

0

0.1

0.2

0.3

0.4

Quarters

Dev

iati

on

from

s.s.

(%)

Sovereign Wealth Fund

0 10 20 30 40

0

0.5

1

Quarters

Per

centa

ge

Poin

ts

Inflation

0 10 20 30 40−2.5

−2

−1.5

−1

−0.5

0

Quarters

Dev

iati

on

from

s.s.

(%)

Exchange Rate

0 10 20 30 40

0

0.5

1

1.5

2

Quarters

Dev

iati

on

from

s.s.

(%)

Public Debt

Under the All-investing in Public Capital Approach Under the Saving in a Sovereign Wealth Fund Approach

Notes : The figures show impulse response functions from the simulated DSGE model toillustrate the effect of a one-standard-deviation oil production shock. Responses are

expressed in percentage deviation from the steady-state values. The solid line shows theresponse of the fiscal policy A (All-Investing Approach) and Dashed lines show the

response of the fiscal policy B (All-Saving Approach).

51

Notes : The figures show impulse response functions from the simulated DSGE model to illustrate theeffect of a one-standard-deviation oil production shock. Responses are expressed in percentage deviationfrom the steady-state values. The solid line shows the response of the fiscal policy A (All-InvestingApproach) and Dashed lines show the response of the fiscal policy B (All-Saving Approach).

28

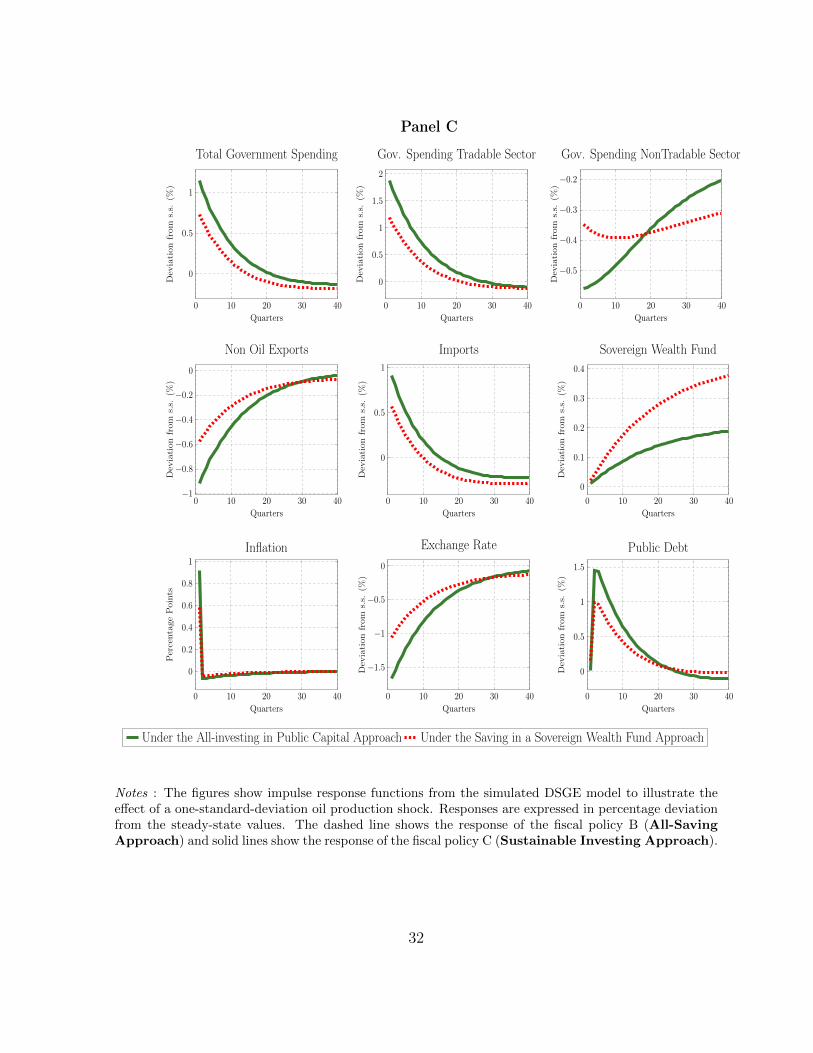

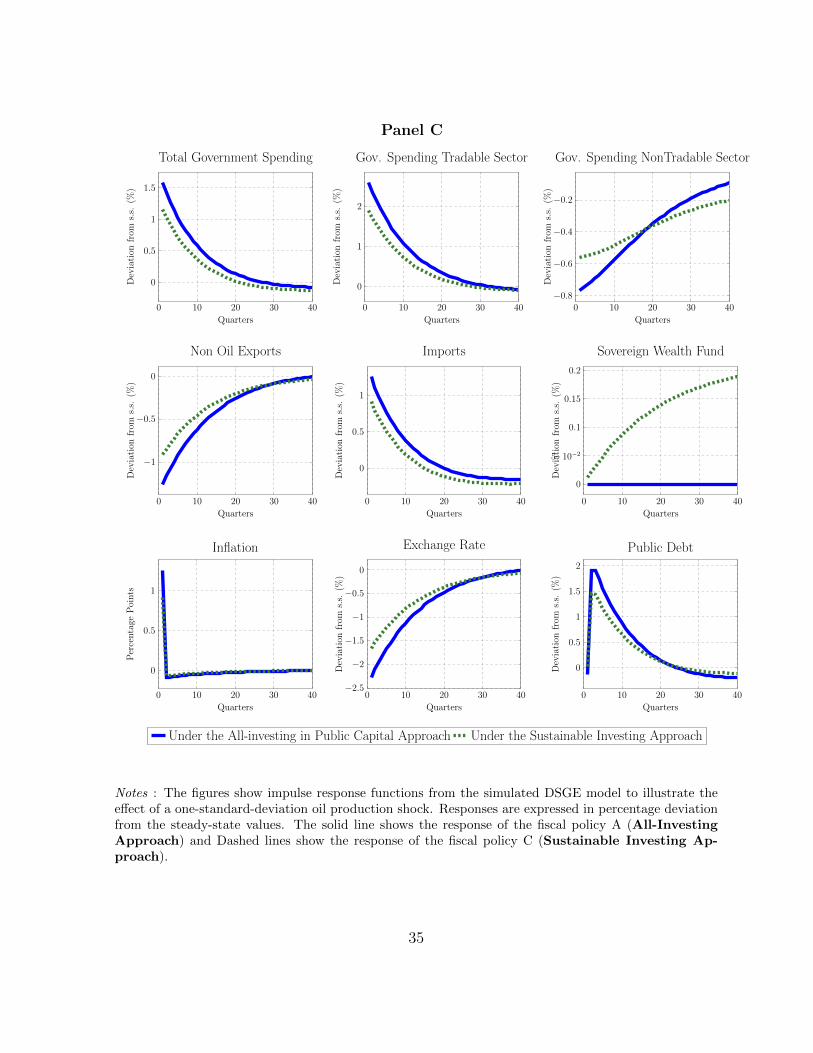

A boom in the oil sector makes the country a net exporter. Then, the wealth and income

accumulated from the resource windfall increase, generating more revenue for government. As

a result, demand in the non-tradable goods sector increases, leading to a substantial rise in

the prices of non-tradable goods. Since Uganda is considered as a small open economy and

a price taker in the international tradable goods market, the real exchange rate, defined as

the relative price of non-tradable to tradable, appreciates consequently. This appreciation,

which is more pronounced under the all-investing approach, reduces the competitiveness of

the country’s exports and domestic imports-competing products. Therefore, imports become

relatively cheaper, leading to a rise in the total imports by about 1.2 percent and a fall of non-

oil exports by around 1.3 percent (Figure 1, panel C). Finally, under the all-saving approach,

the economy experiences smaller movements because resource income is directly saved into

a foreign account. In contrast, under the all-investing approach, the oil production shock is

more persistent and the return to the pre-windfall equilibrium is done more slowly. Comparing

these two stylized fiscal policies, simulations show that the boom in the oil production sector

generates sizeable macroeconomic activity under the all-investing approach. However, the all-

saving approach is much less susceptible to generate Dutch disease effects.

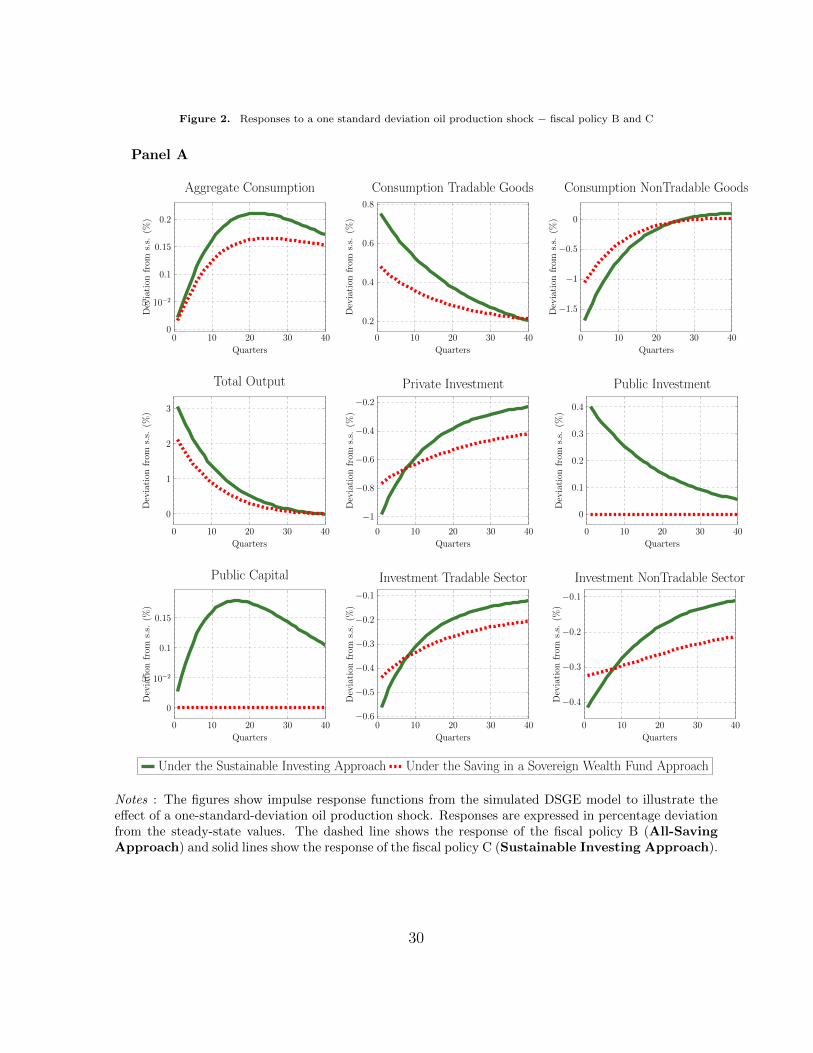

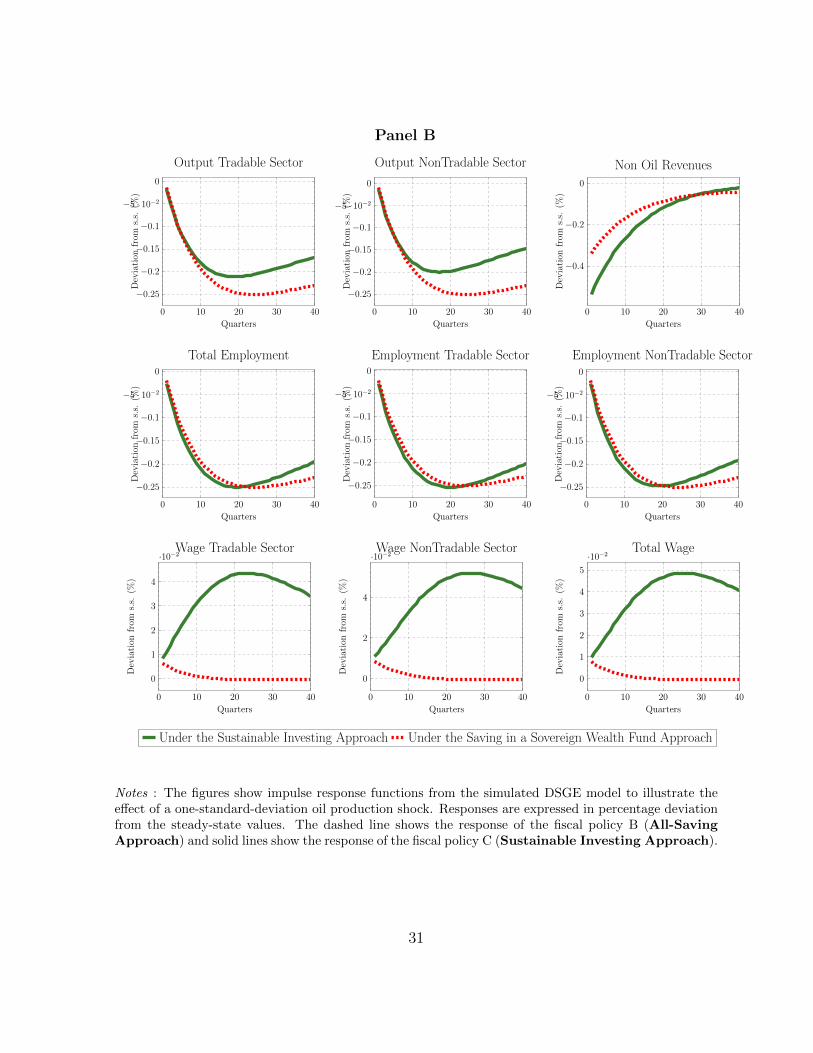

4.2 The sustainable investing approach

In this subsection, we compare the first two fiscal approaches to the sustainable investing ap-

proach. This latter fiscal policy, which may be viewed as a mixed policy, can conciliate public

investment and saving approach by proposing a new investment with external saving approach.

We allow the government to use half of the oil revenue for public investment (φoil = 0.5) and to

save the remaining half; Section 4.4 investigates the optimal value of φoil. As described in 2.48,

this new approach allows policymakers to choose an optimal scaling up magnitude given the size

of the oil production and economic characteristics. Figures 2 and 3 show impulse responses of

the main macroeconomic aggregates in comparison with the first two fiscal policy approaches.

Under the three stylized fiscal policies, simulations show that the boom in the oil sector leads

to deteriorate employment in both the tradable and non-tradable goods sectors. This result,

which might be surprising, is resulting from two macroeconomic effects: substitution and wealth

29

Figure 2. Responses to a one standard deviation oil production shock − fiscal policy B and CTable 4: Responses to a one standard deviation oil production shock − fiscal policy B and C

Panel A

0 10 20 30 400

5 · 10−2

0.1

0.15

0.2

Quarters

Dev

iati

on

from

s.s.

(%)

Aggregate Consumption

0 10 20 30 40

0.2

0.4

0.6

0.8

QuartersD

evia

tion

from

s.s.

(%)

Consumption Tradable Goods

0 10 20 30 40

−1.5

−1

−0.5

0

Quarters

Dev

iati

on

from

s.s.

(%)

Consumption NonTradable Goods

0 10 20 30 40

0

1

2

3

Quarters

Dev

iati

on

from

s.s.

(%)

Total Output

0 10 20 30 40

−1

−0.8

−0.6

−0.4

−0.2

Quarters

Dev

iati

on

from

s.s.

(%)

Private Investment

0 10 20 30 40

0

0.1

0.2

0.3

0.4

Quarters

Dev

iati

on

from

s.s.

(%)

Public Investment

0 10 20 30 40

0

5 · 10−2

0.1

0.15

Quarters

Dev

iati

on

from

s.s.

(%)

Public Capital

0 10 20 30 40−0.6

−0.5

−0.4

−0.3

−0.2

−0.1

Quarters

Dev

iati

on

from

s.s.

(%)

Investment Tradable Sector

0 10 20 30 40

−0.4

−0.3

−0.2

−0.1

Quarters

Dev

iati

on

from

s.s.

(%)

Investment NonTradable Sector

Under the Sustainable Investing Approach Under the Saving in a Sovereign Wealth Fund Approach

Notes : The figures show impulse response functions from the simulated DSGE model toillustrate the effect of a one-standard-deviation oil production shock. Responses are

expressed in percentage deviation from the steady-state values. The dashed line showsthe response of the fiscal policy B (All-Saving Approach) and solid lines show the

response of the fiscal policy C (Sustainable Investing Approach).

52

Notes : The figures show impulse response functions from the simulated DSGE model to illustrate theeffect of a one-standard-deviation oil production shock. Responses are expressed in percentage deviationfrom the steady-state values. The dashed line shows the response of the fiscal policy B (All-SavingApproach) and solid lines show the response of the fiscal policy C (Sustainable Investing Approach).

30

Panel B

0 10 20 30 40

−0.25

−0.2

−0.15

−0.1

−5 · 10−2

0

Quarters

Dev

iati

onfr

oms.

s.(%

)

Output Tradable Sector

0 10 20 30 40

−0.25

−0.2

−0.15

−0.1

−5 · 10−2

0

Quarters

Dev

iati

onfr

oms.

s.(%

)

Output NonTradable Sector

0 10 20 30 40

−0.4

−0.2

0

Quarters

Dev

iati

onfr

oms.

s.(%

)

Non Oil Revenues

0 10 20 30 40

−0.25

−0.2

−0.15

−0.1

−5 · 10−2

0

Quarters

Dev

iati

onfr

oms.

s.(%

)

Total Employment

0 10 20 30 40

−0.25

−0.2

−0.15

−0.1

−5 · 10−2

0

Quarters

Dev

iati

onfr

oms.

s.(%

)Employment Tradable Sector

0 10 20 30 40

−0.25

−0.2

−0.15

−0.1

−5 · 10−2

0

Quarters

Dev

iati

onfr

oms.

s.(%

)

Employment NonTradable Sector

0 10 20 30 40

0

1

2

3

4

·10−2

Quarters

Dev

iati

onfr

oms.

s.(%

)

Wage Tradable Sector

0 10 20 30 40

0

2

4

·10−2

Quarters

Dev

iati

onfr

oms.

s.(%

)

Wage NonTradable Sector

0 10 20 30 40

0

1

2

3

4

5

·10−2

Quarters

Dev

iati

onfr

oms.

s.(%

)Total Wage

Under the Sustainable Investing Approach Under the Saving in a Sovereign Wealth Fund Approach

Notes : The figures show impulse response functions from the simulated DSGE model toillustrate the effect of a one-standard-deviation oil production shock. Responses are

expressed in percentage deviation from the steady-state values. The dashed line showsthe response of the fiscal policy B (All-Saving Approach) and solid lines show the

response of the fiscal policy C (Sustainable Investing Approach).

53

Notes : The figures show impulse response functions from the simulated DSGE model to illustrate theeffect of a one-standard-deviation oil production shock. Responses are expressed in percentage deviationfrom the steady-state values. The dashed line shows the response of the fiscal policy B (All-SavingApproach) and solid lines show the response of the fiscal policy C (Sustainable Investing Approach).

31

Panel C

0 10 20 30 40

0

0.5

1

Quarters

Dev

iati

on

from

s.s.

(%)

Total Government Spending

0 10 20 30 40

0

0.5

1

1.5

2

Quarters

Dev

iati

on

from

s.s.

(%)

Gov. Spending Tradable Sector

0 10 20 30 40

−0.5

−0.4

−0.3

−0.2

Quarters

Dev

iati

on

from

s.s.

(%)

Gov. Spending NonTradable Sector

0 10 20 30 40−1

−0.8

−0.6

−0.4

−0.2

0

Quarters

Dev

iati

on

from

s.s.

(%)

Non Oil Exports

0 10 20 30 40

0

0.5

1

Quarters

Dev

iati

on

from

s.s.

(%)

Imports

0 10 20 30 40

0

0.1

0.2

0.3

0.4

Quarters

Dev

iati

on

from

s.s.

(%)

Sovereign Wealth Fund

0 10 20 30 40

0

0.2

0.4

0.6

0.8

1

Quarters

Per

centa

ge

Poin

ts

Inflation

0 10 20 30 40

−1.5

−1

−0.5

0

Quarters

Dev

iati

on

from

s.s.

(%)

Exchange Rate

0 10 20 30 40

0

0.5

1

1.5

Quarters

Dev

iati

on

from

s.s.

(%)

Public Debt

Under the All-investing in Public Capital Approach Under the Saving in a Sovereign Wealth Fund Approach

Notes : The figures show impulse response functions from the simulated DSGE model toillustrate the effect of a one-standard-deviation oil production shock. Responses are

expressed in percentage deviation from the steady-state values. The dashed line showsthe response of the fiscal policy B (All-Saving Approach) and solid lines show the

response of the fiscal policy C (Sustainable Investing Approach).

54

Notes : The figures show impulse response functions from the simulated DSGE model to illustrate theeffect of a one-standard-deviation oil production shock. Responses are expressed in percentage deviationfrom the steady-state values. The dashed line shows the response of the fiscal policy B (All-SavingApproach) and solid lines show the response of the fiscal policy C (Sustainable Investing Approach).

32

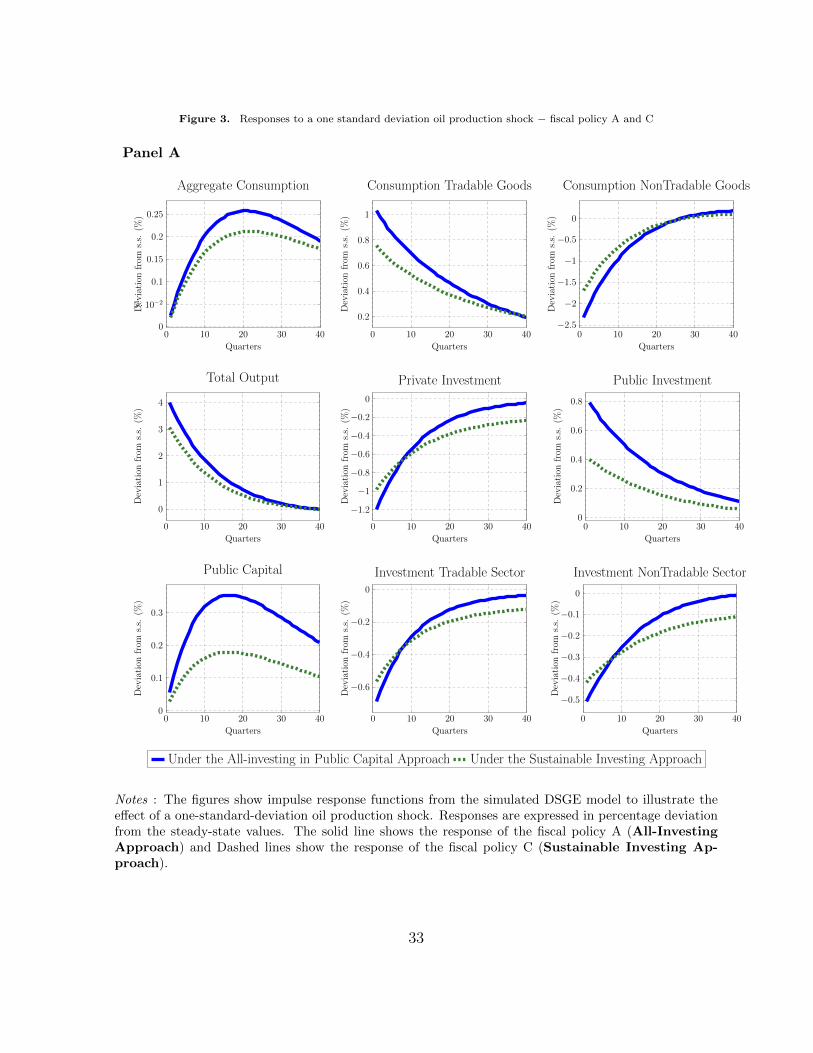

Figure 3. Responses to a one standard deviation oil production shock − fiscal policy A and CTable 5: Responses to a one standard deviation oil production shock − fiscal policy A and C

Panel A

0 10 20 30 400

5 · 10−2

0.1

0.15

0.2

0.25

Quarters

Dev

iati

onfr

oms.

s.(%

)

Aggregate Consumption

0 10 20 30 40

0.2

0.4

0.6

0.8

1

QuartersD

evia

tion

from

s.s.

(%)

Consumption Tradable Goods

0 10 20 30 40−2.5

−2

−1.5

−1

−0.5

0

Quarters

Dev

iati

onfr

oms.

s.(%

)

Consumption NonTradable Goods

0 10 20 30 40

0

1

2

3

4

Quarters

Dev

iati

onfr

oms.

s.(%

)

Total Output

0 10 20 30 40

−1.2

−1

−0.8

−0.6

−0.4

−0.2

0

Quarters

Dev

iati

onfr

oms.

s.(%

)

Private Investment

0 10 20 30 400

0.2

0.4

0.6

0.8

Quarters

Dev

iati

onfr

oms.

s.(%

)

Public Investment

0 10 20 30 400

0.1

0.2

0.3

Quarters

Dev

iati

onfr

oms.

s.(%

)

Public Capital

0 10 20 30 40

−0.6

−0.4

−0.2

0

Quarters

Dev

iati

onfr

oms.

s.(%

)

Investment Tradable Sector

0 10 20 30 40

−0.5

−0.4

−0.3

−0.2

−0.1

0

Quarters

Dev

iati

onfr

oms.

s.(%

)

Investment NonTradable Sector

Under the All-investing in Public Capital Approach Under the Sustainable Investing Approach

Notes : The figures show impulse response functions from the simulated DSGE model toillustrate the effect of a one-standard-deviation oil production shock. Responses are

expressed in percentage deviation from the steady-state values. The solid line shows theresponse of the fiscal policy A (All-Investing Approach) and Dashed lines show the

response of the fiscal policy C (Sustainable Investing Approach).

55

Notes : The figures show impulse response functions from the simulated DSGE model to illustrate theeffect of a one-standard-deviation oil production shock. Responses are expressed in percentage deviationfrom the steady-state values. The solid line shows the response of the fiscal policy A (All-InvestingApproach) and Dashed lines show the response of the fiscal policy C (Sustainable Investing Ap-proach).

33

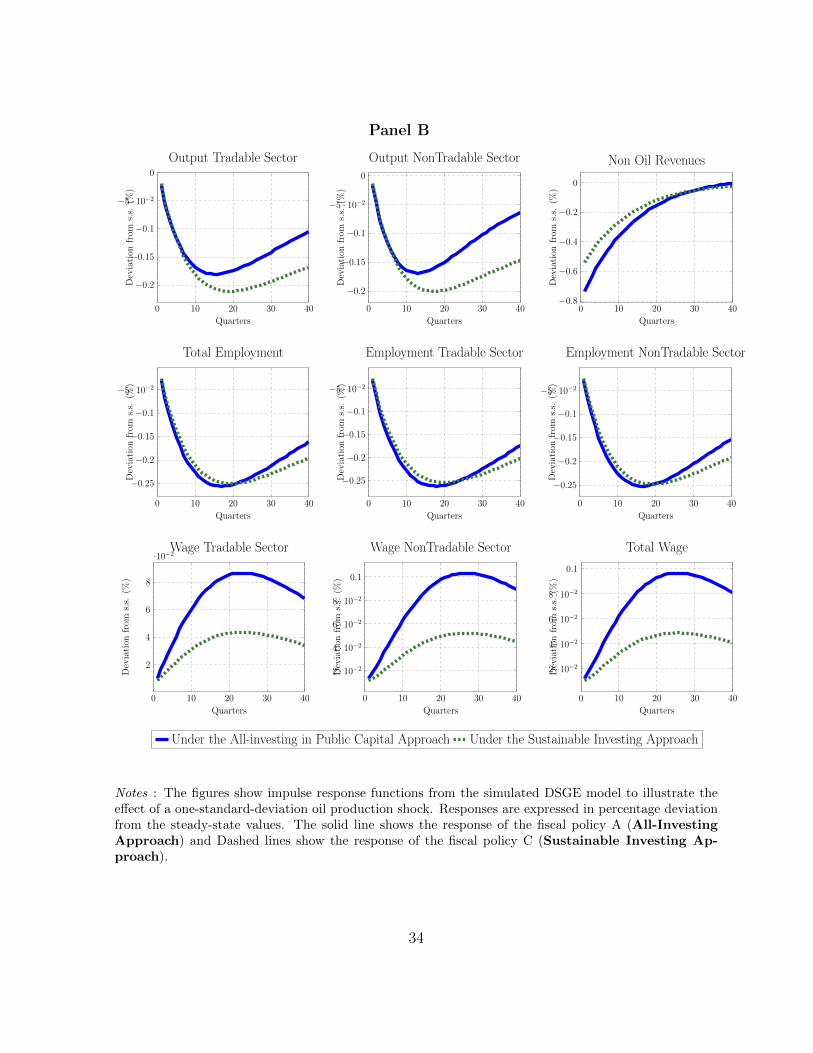

Panel B

0 10 20 30 40

−0.2

−0.15

−0.1

−5 · 10−2

0

Quarters

Dev

iati

on

from

s.s.

(%)

Output Tradable Sector

0 10 20 30 40

−0.2

−0.15

−0.1

−5 · 10−2

0

Quarters

Dev

iati

on

from

s.s.

(%)

Output NonTradable Sector

0 10 20 30 40−0.8

−0.6

−0.4

−0.2

0

Quarters

Dev

iati

on

from

s.s.

(%)

Non Oil Revenues

0 10 20 30 40

−0.25

−0.2

−0.15

−0.1

−5 · 10−2

Quarters

Dev

iati

on

from

s.s.

(%)

Total Employment

0 10 20 30 40

−0.25

−0.2

−0.15

−0.1

−5 · 10−2

Quarters

Dev

iati

on

from

s.s.

(%)

Employment Tradable Sector

0 10 20 30 40

−0.25

−0.2

−0.15

−0.1

−5 · 10−2

Quarters

Dev

iati

on

from

s.s.

(%)

Employment NonTradable Sector

0 10 20 30 40

2

4

6

8

·10−2

Quarters

Dev

iati

on

from

s.s.

(%)

Wage Tradable Sector

0 10 20 30 40

2 · 10−2

4 · 10−2

6 · 10−2

8 · 10−2

0.1

Quarters

Dev

iati

on

from

s.s.

(%)

Wage NonTradable Sector

0 10 20 30 40

2 · 10−2

4 · 10−2

6 · 10−2

8 · 10−2

0.1

Quarters

Dev

iati

on

from

s.s.

(%)

Total Wage

Under the All-investing in Public Capital Approach Under the Sustainable Investing Approach

Notes : The figures show impulse response functions from the simulated DSGE model toillustrate the effect of a one-standard-deviation oil production shock. Responses are

expressed in percentage deviation from the steady-state values. The solid line shows theresponse of the fiscal policy A (All-Investing Approach) and Dashed lines show the

response of the fiscal policy C (Sustainable Investing Approach).

56

Notes : The figures show impulse response functions from the simulated DSGE model to illustrate theeffect of a one-standard-deviation oil production shock. Responses are expressed in percentage deviationfrom the steady-state values. The solid line shows the response of the fiscal policy A (All-InvestingApproach) and Dashed lines show the response of the fiscal policy C (Sustainable Investing Ap-proach).

34

Panel C

0 10 20 30 40

0

0.5

1

1.5

Quarters

Dev

iati

onfr

oms.