counterparty credit risk in financial institutions · counterparty credit risk in financial...

TRANSCRIPT

Counterparty Credit Risk in Financial Institutions

Ivan Sergienko Director, Counterparty Credit Risk Measurement

University of Waterloo, 4 February 2014

2 GLOBAL RISK MANAGEMENT

My previous research

About Scotiabank

Review of a simple transaction: Market Risk vs Counterparty Credit Risk

Counterparty Risk Measures: PFE, Expected Exposure, CVA, Capital

Mitigation of counterparty credit risk: Netting, Collateral

CCR System at Scotiabank

Outline

3 GLOBAL RISK MANAGEMENT

Past Research

Memorial University of Newfoundland 2002-2004

Oak Ridge National Laboratory, 2004-2007

Non-centrosymmetric superconductors

Magnetoelectric materials

4 GLOBAL RISK MANAGEMENT

From Science/Math/Eng to Finance

Options:

• Quant Finance Programs:

o Prepare you for day 1 and beyond. o Don’t do if you have a PhD.

• CFA®: o Targeted for stock analysts, investment bankers. o Broad business knowledge/accounting.

• FRM®: o Focus on statistics, derivatives. o Very quantitative.

• MBA: o Broad business knowledge/strategy. o Need good school ($$$$).

Programming a must!

5 GLOBAL RISK MANAGEMENT

About Scotiabank

1832 – Founded in Halifax with a capital of £100,000

1889 – Branch in Jamaica

1897 – Branch in Toronto

6 GLOBAL RISK MANAGEMENT

Scotiabank Business Lines

18%

22% 34%

26%

Net Income

Global Wealth &Insurance

Global Banking &Markets

Canadian Banking

International Banking

7 GLOBAL RISK MANAGEMENT

Market Risk

Client (NG producer)

$ x

8 GLOBAL RISK MANAGEMENT

Market Risk

Client (NG producer)

$ x

Bank

$ x

$ 4.00

9 GLOBAL RISK MANAGEMENT

Market Risk

Client (NG producer)

$ x

Bank

$ x

$ 4.00

Market

$ x

$ 4.10

Client: x + (4.00 – x) = 4.00 Bank: (x – 4.00) + (4.10 – x) = 0.10 Market: x – 4.10 - Market Risk Taker

10 GLOBAL RISK MANAGEMENT

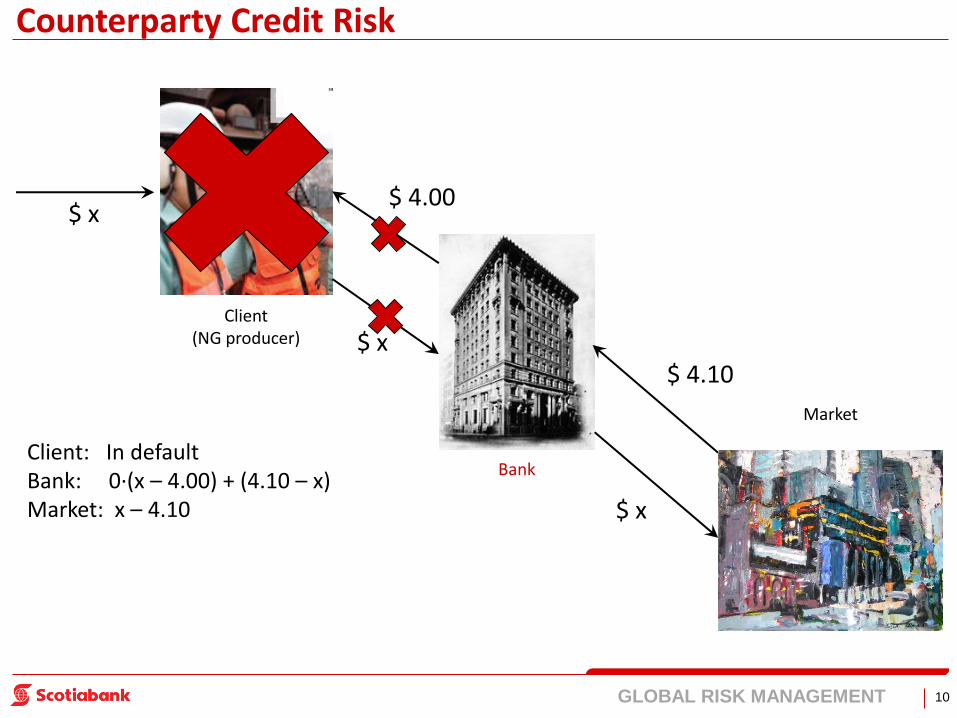

Counterparty Credit Risk

Client (NG producer)

Bank

Market

$ x

$ x

$ 4.00

$ x

$ 4.10

Client: In default Bank: 0∙(x – 4.00) + (4.10 – x) Market: x – 4.10

11 GLOBAL RISK MANAGEMENT

Counterparty Credit Risk

Bank

Market

$ x

$ 4.10

Assume: x = 5.00 Bank: 0∙1.00 + (- 0.90) = - 0.90 Market: 0.90

Assume: x = 3.50 Bank: 0∙(-0.50) + (0.60) = 0.60 Market: - 0.60

12 GLOBAL RISK MANAGEMENT

Counterparty Credit Risk Concepts

-3 -2 -1 0 1 2 3 4 5

-10

-5

0

5

10

15

Millio

ns

possible future

paths PFE

profile

expected

exposure profile

expected MTM

profile

history of

MTM

PFE

0.00

0.02

0.04

0.06

0.08

0.10

0.12

0.14

-10 -5 0 5 10 15

MTM

Exposure

90% Tail

E[MTM] EE

PFE

t = 3 y

13 GLOBAL RISK MANAGEMENT

Counterparty Credit Risk Concepts

-3 -2 -1 0 1 2 3 4 5

-10

-5

0

5

10

15

Millio

ns

possible future

paths PFE

profile

expected

exposure profile

expected MTM

profile

history of

MTM

PFE

E[MTM] – Rarely interesting

EE – used in:

o CVA – cost of risk (PD adjusted)

o Capital requirements

o DVA, FVA, etc.

PFE – used for limit monitoring

14 GLOBAL RISK MANAGEMENT

Counterparty Credit Risk Concepts

-3 -2 -1 0 1 2 3 4 5

-10

-5

0

5

10

15

Millio

ns

possible future

paths PFE

profile

expected

exposure profile

expected MTM

profile

history of

MTM

PFE

E[MTM] – Rarely interesting

EE – used in:

o CVA – cost of risk (PD adjusted)

o Capital requirements

o DVA, FVA, etc.

PFE – used for limit monitoring

0

100

200

300

400

500

600

700

PFE profile

Limit

15 GLOBAL RISK MANAGEMENT

Counterparty Credit Risk Concepts - Netting

If you owe me $100, and I owe you $60, don’t you just owe me $40?

Not always!

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

4/2/2013 4/2/2014 4/2/2015 4/2/2016 4/2/2017

PFE (Non-netted)

PFE (Netted)

Trade 1: CAD$100M, 5 year Single Currency Swap (CAD) Trade 2: USD$100M, 1 year FEC (CAD/USD)

16 GLOBAL RISK MANAGEMENT

Counterparty Credit Risk Concepts - Collateral

Profile decreases dramatically with a margin agreement. Model assumes collateral at any point in time equals the MTM some time previously.

-3 -2 -1 0 1 2 3 4 5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Mill

ion

s possible future paths

PFE profile expected exposure profile

expected MTM - Collateral

history of MTM

-3 -2 -1 0 1 2 3 4 5

-10

-5

0

5

10

15

Millio

ns

possible PFE

expected

expected MTM

history of

PFE

17 GLOBAL RISK MANAGEMENT

Counterparty Credit Risk Concepts - Collateral

Trade 1: CAD$100M, 5 year Single Currency Swap (CAD) Trade 2: USD$100M, 1 year FEC (CAD/USD)

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

4/2/2013 4/2/2014 4/2/2015 4/2/2016 4/2/2017

PFE (Non-netted)

PFE (Netted)

PFE (Netted + 0 TH CSA)

18 GLOBAL RISK MANAGEMENT

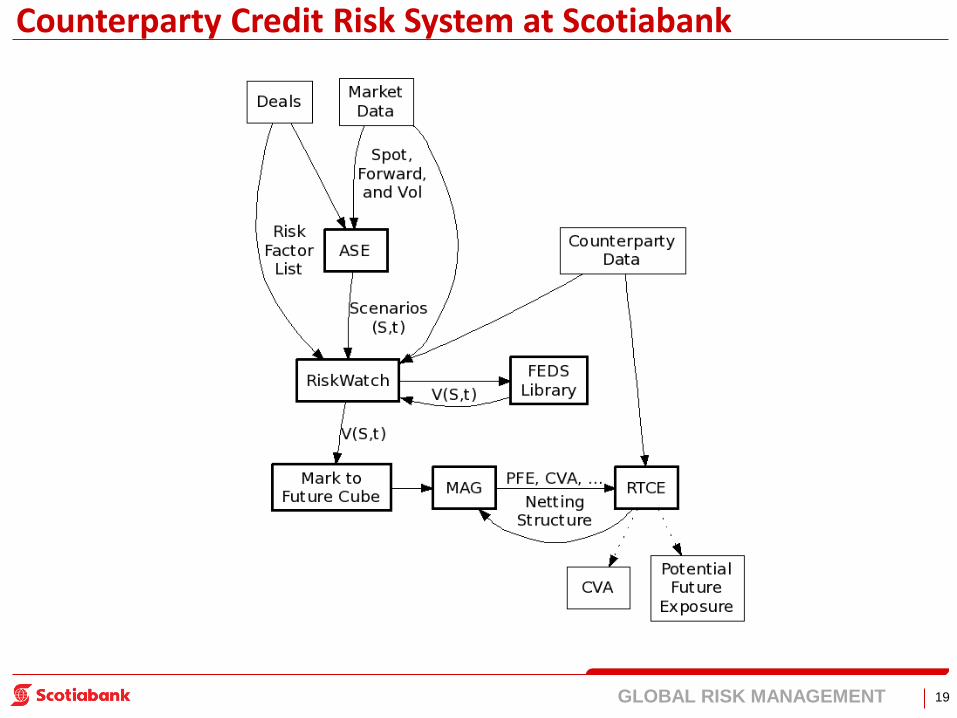

Counterparty Credit Risk System at Scotiabank

In collaboration with IBM Risk Analytics/Algorithmics.

Trading systems

Trades, Market prices

Collateral system

Counterparty operations

Algo

Credit

Collateral data

Risk reports

Netting setup Credit ratings

Trading systems

Trade

Algo

Credit

Incremental Risk Measures

End of day

architecture

Intra-day

architecture

Best Counterparty Risk Initiative

American Financial Technology Awards

2010

19 GLOBAL RISK MANAGEMENT

Counterparty Credit Risk System at Scotiabank

20 GLOBAL RISK MANAGEMENT

Questions?

Thank you for your time.

21 GLOBAL RISK MANAGEMENT

Abstract

Counterparty credit risk (CCR) management of today is a complex process

involving many groups within financial institutions. I will describe Scotiabank’s

award winning CCR initiative . I will review basic CCR concepts and explain

how CCR measures are calculated. I will also talk about my career

experience in science and financial industry.

Bio Ivan Sergienko is Director, Counterparty Credit Risk Management at

Scotiabank. He leads implementation of a comprehensive CCR framework

covering major derivatives types. Before joining Scotiabank in 2007 he held

research positions at Memorial University of Newfoundland and Oak Ridge

National Laboratory. He hold a PhD in Physics and the Chartered Financial

Analyst® designation