counseling and advisory services for improving the capacity and the capability of smes presented by...

TRANSCRIPT

Counseling and advisory Counseling and advisory services for improving services for improving the capacity and the the capacity and the capability of SMEscapability of SMEs

Presented by Naoyuki Yoshino Professor, Keio University, Japan, July 25, 2011 Video Presentation from Japan [email protected] 1

1

Outline of Presentation

1, SME dominates Asian Economy2, SMEs are difficult to borrow money from Banks3, Heavy reliance on Micro-credit4, Book Keeping Data collection5, Financial Education6, Interest rate, Amount of sales

2

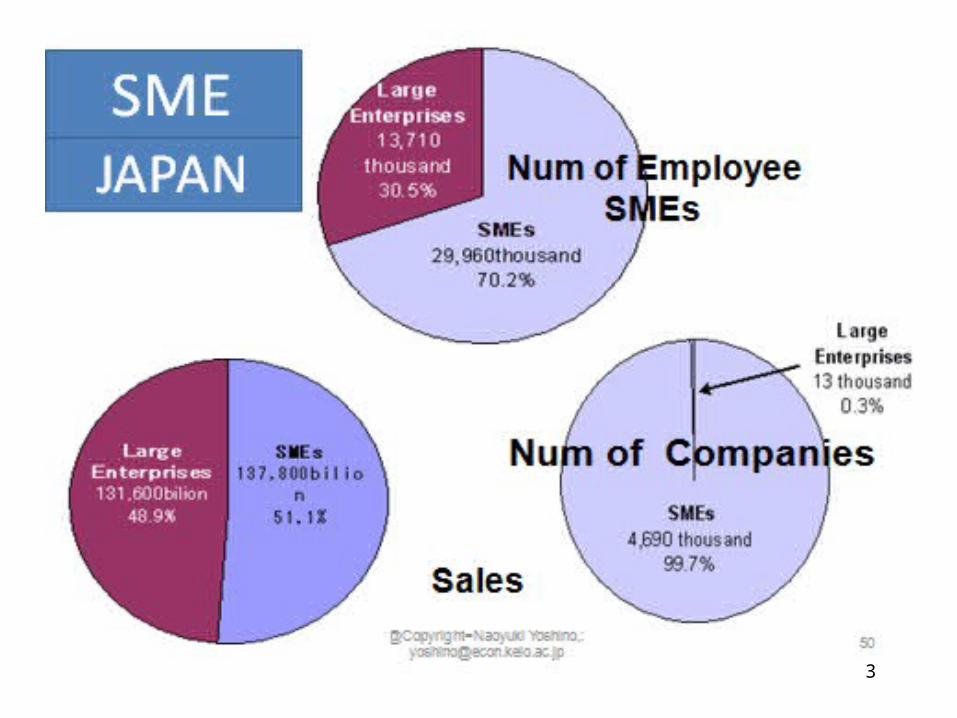

3

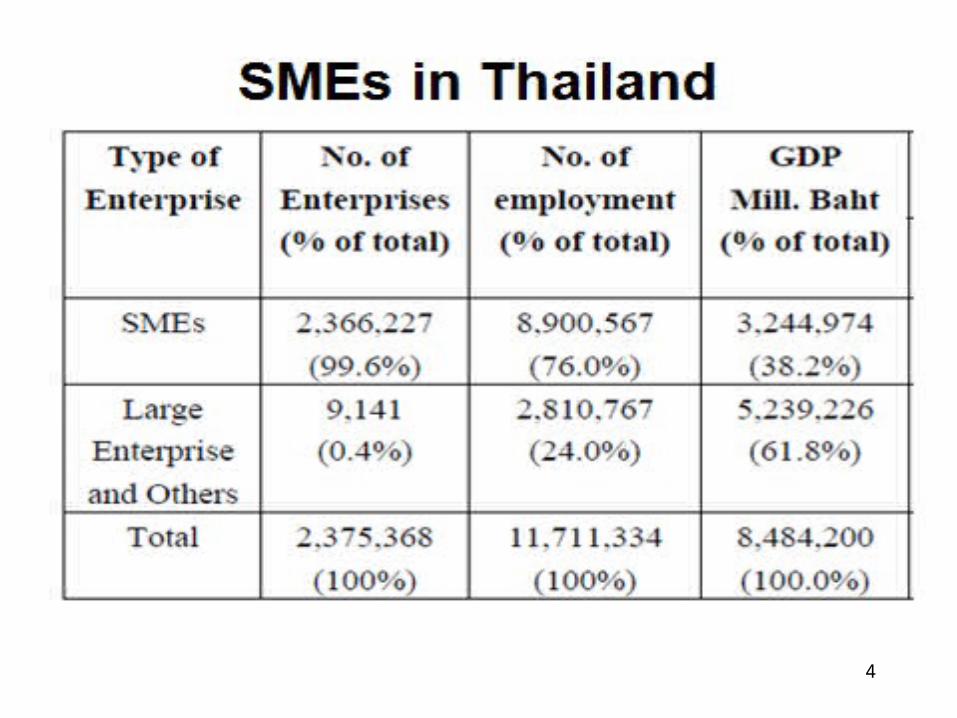

4

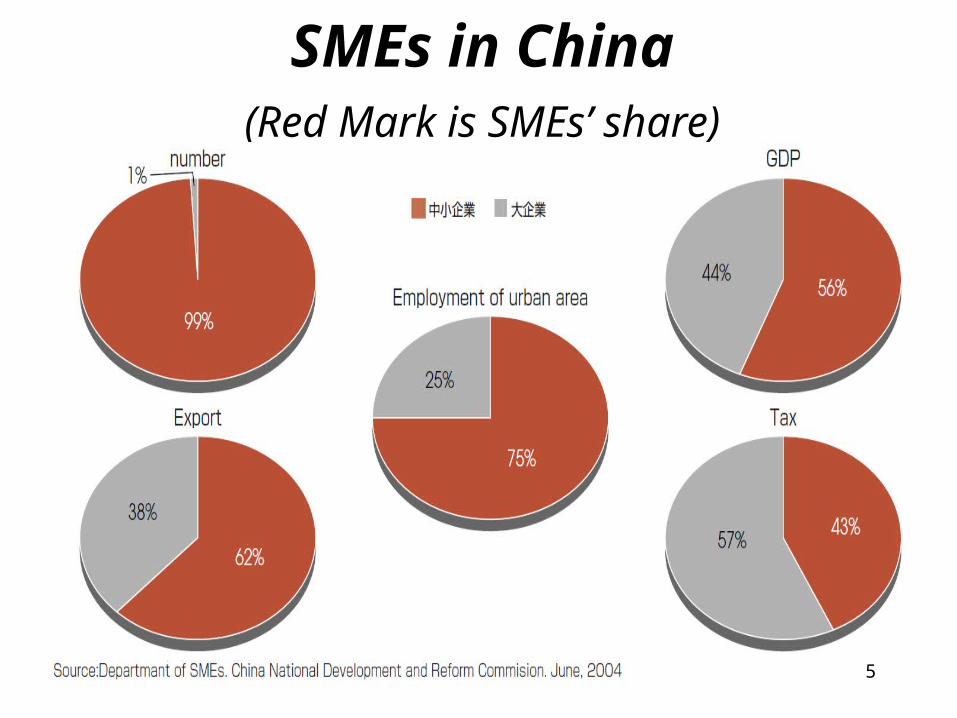

SMEs in China (Red Mark is SMEs’ share)

5

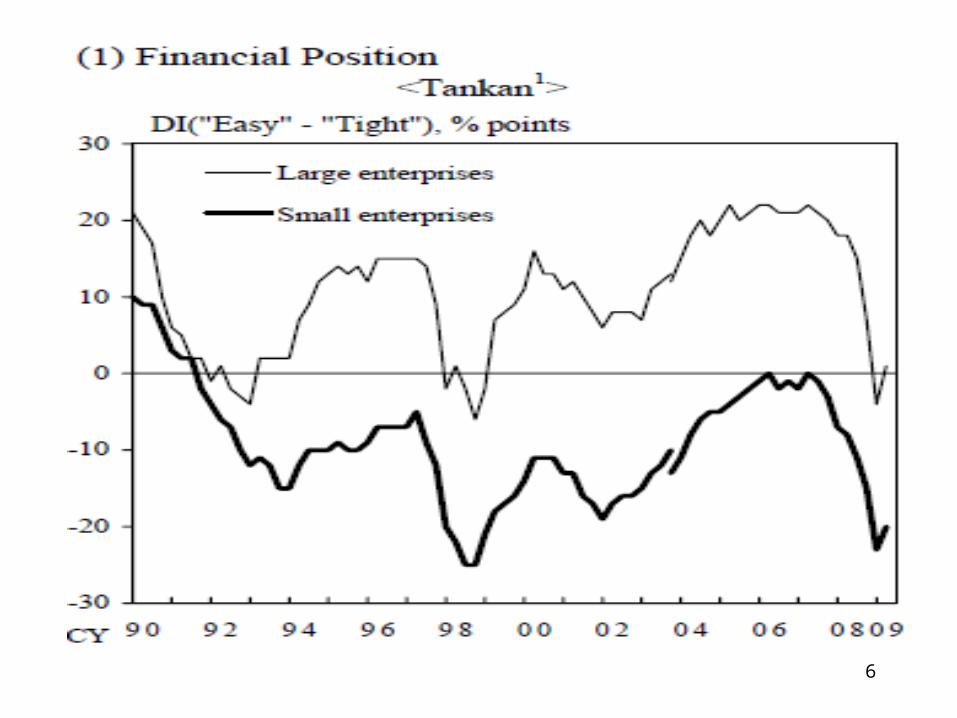

6

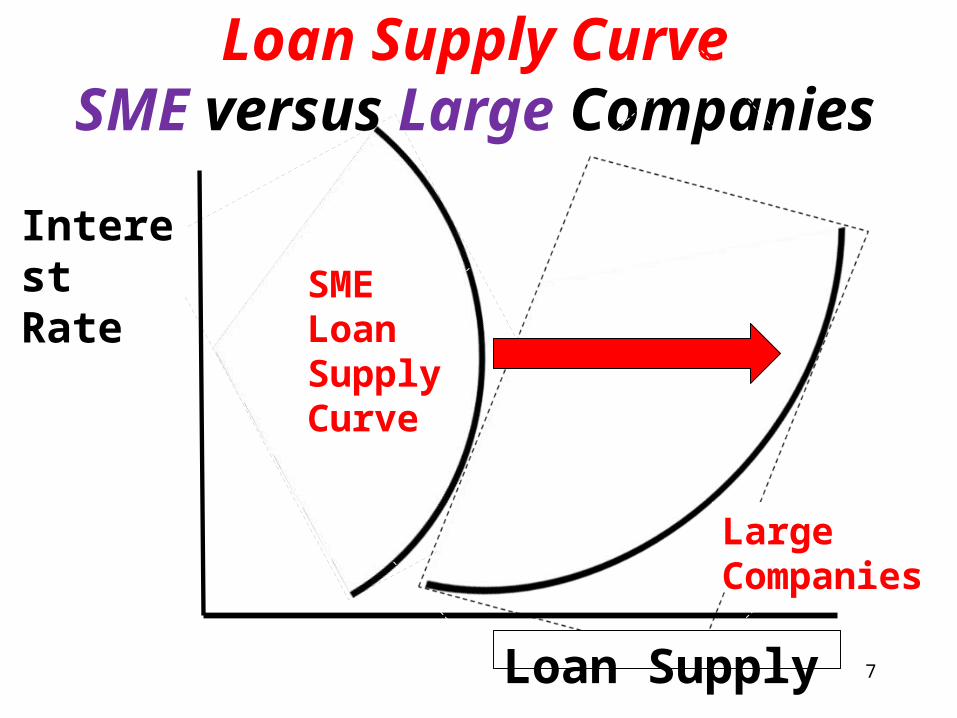

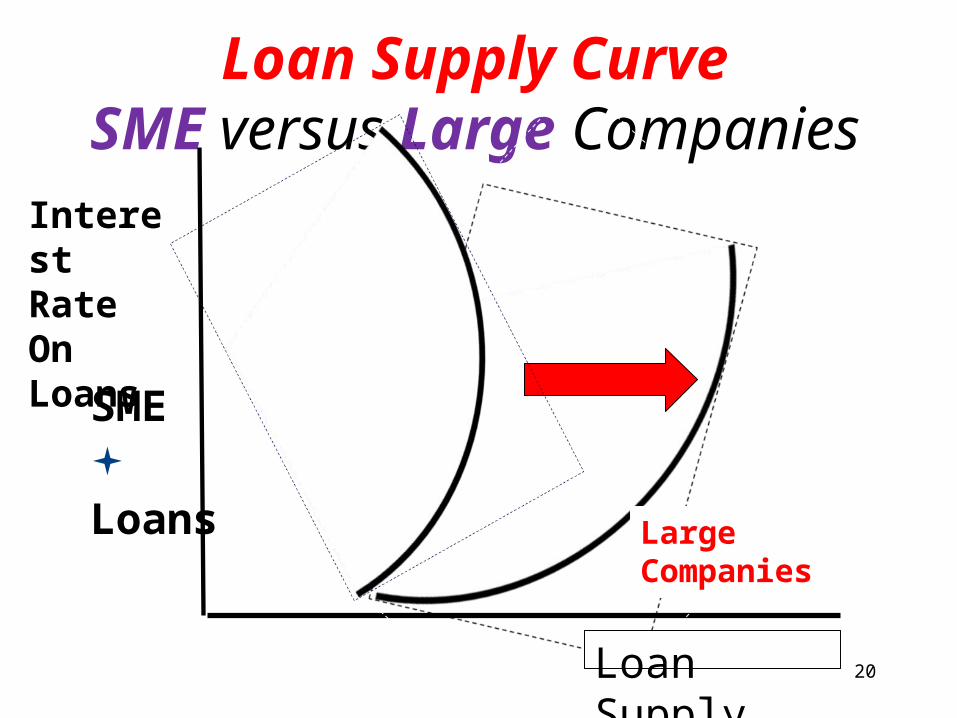

Loan Supply CurveSME versus Large

Companies

7

SME Loan Supply Curve

LargeCompanies

Interest Rate

Loan Supply

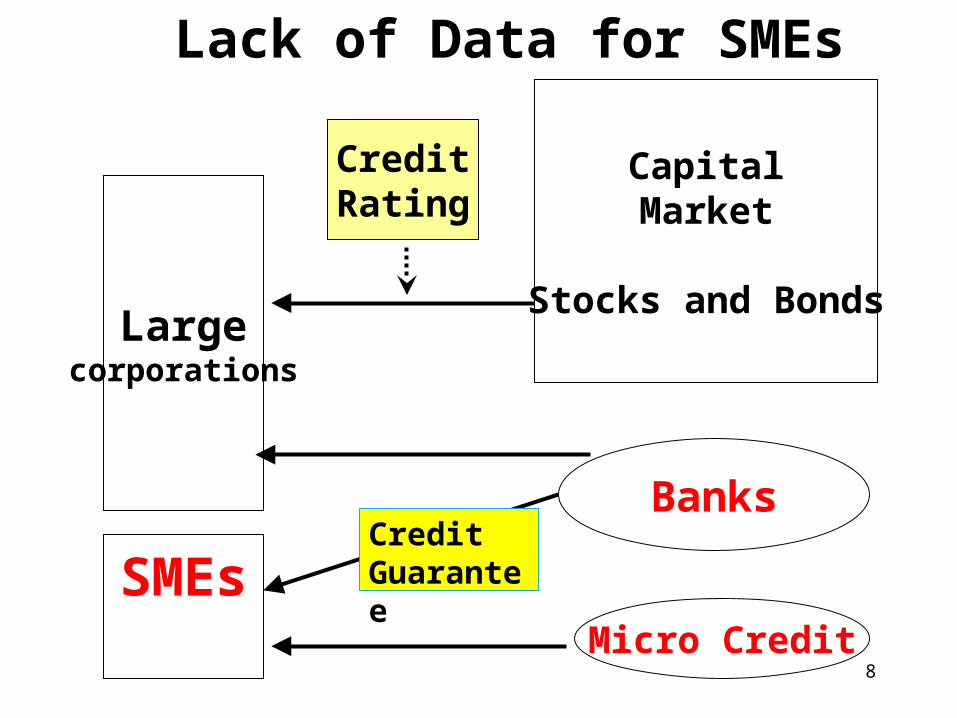

Lack of Data for SMEs

Largecorporations

SMEs

Banks

Micro Credit

CapitalMarket

Stocks and Bonds

CreditRating

Credit Guarantee

8

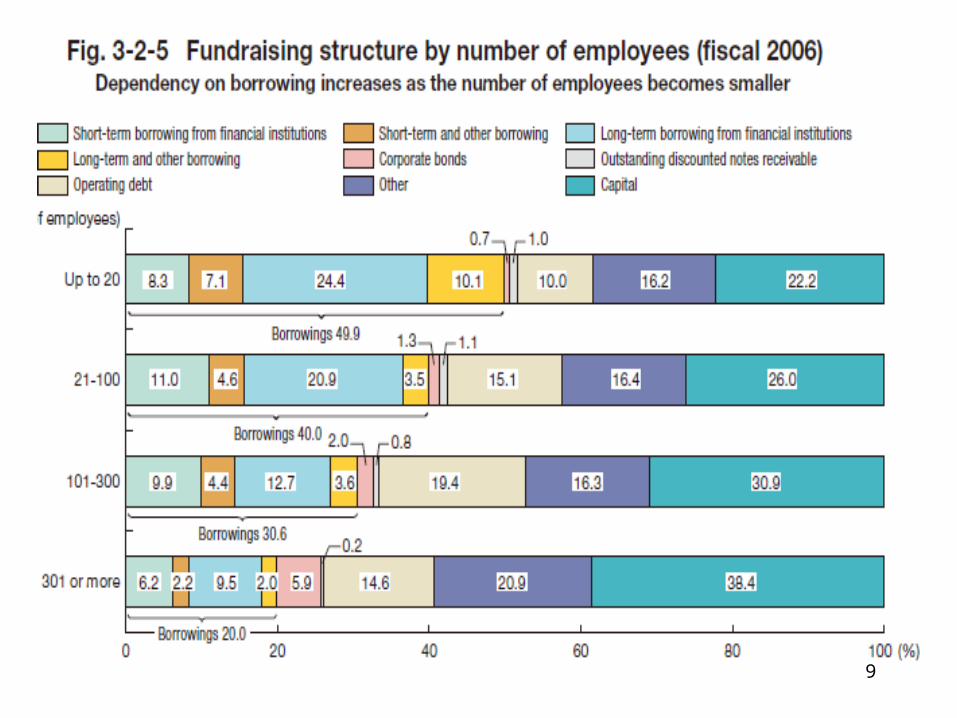

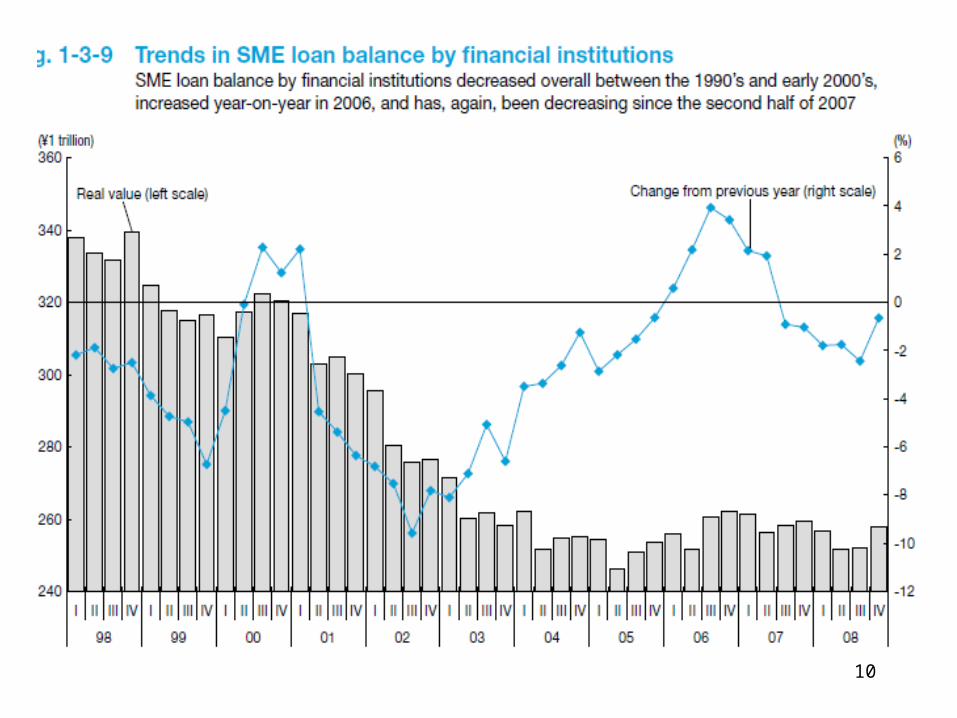

9

10

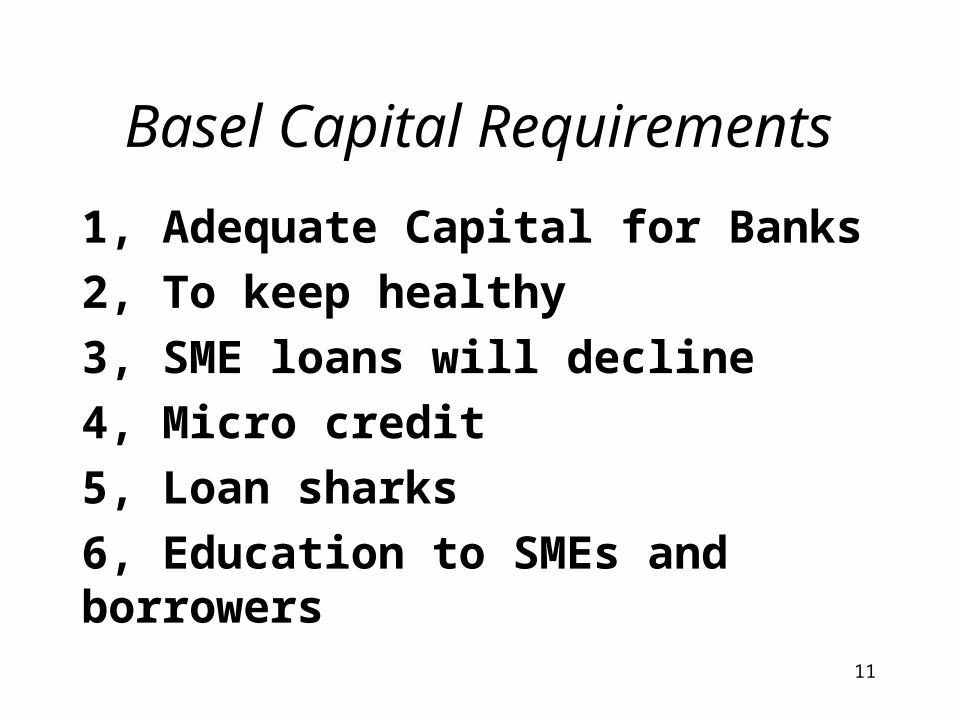

Basel Capital Requirements

1, Adequate Capital for Banks2, To keep healthy3, SME loans will decline4, Micro credit 5, Loan sharks6, Education to SMEs and borrowers

11

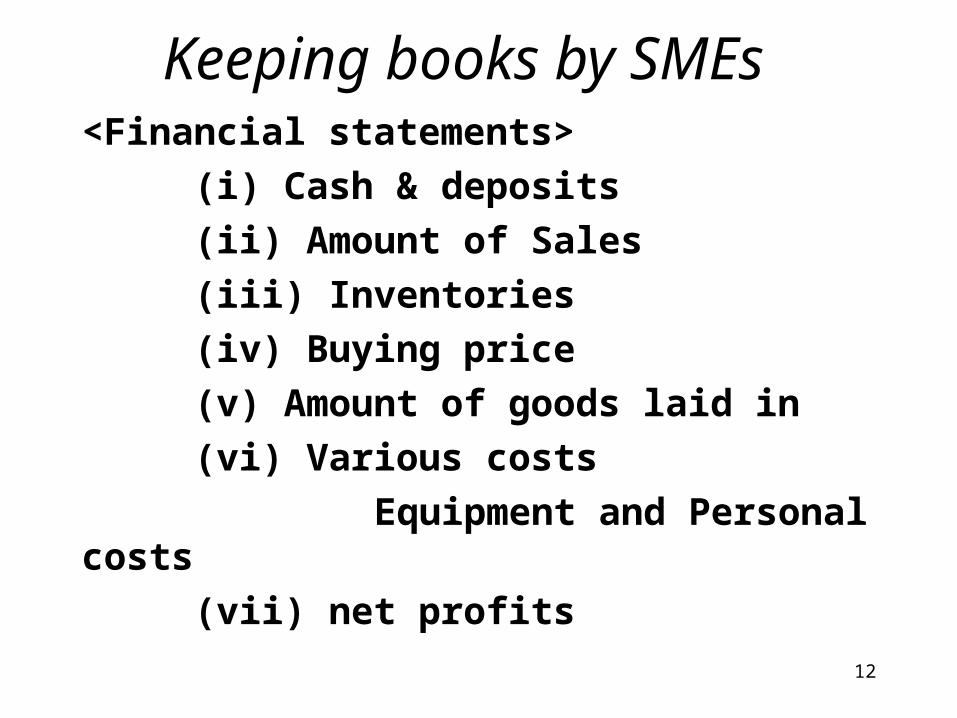

Keeping books by SMEs<Financial statements> (i) Cash & deposits (ii) Amount of Sales (iii) Inventories (iv) Buying price (v) Amount of goods laid in (vi) Various costs Equipment and Personal costs (vii) net profits

12

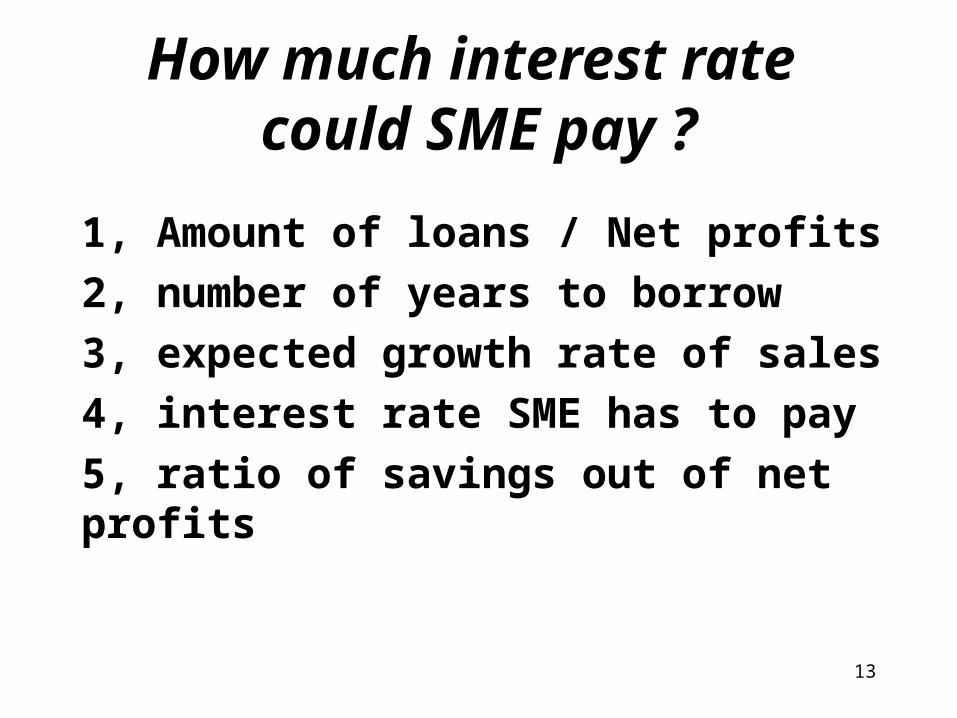

How much interest rate

could SME pay ?1, Amount of loans / Net profits2, number of years to borrow3, expected growth rate of sales4, interest rate SME has to pay5, ratio of savings out of net profits

13

14

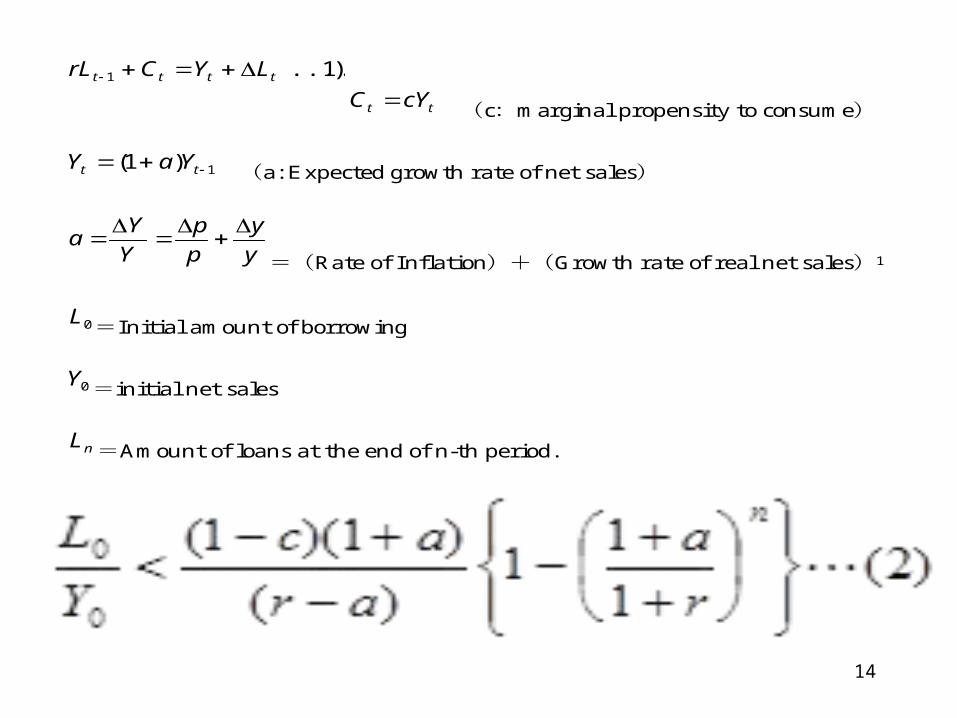

)1....( 1 tttt LYCrL

tt cYC (c:marginal propensity to consume)

1)1( tt YaY (a: Expected growth rate of net sales)

y

y

p

p

Y

Ya

=(Rate of Inflation)+(Growth rate of real net sales)1

0L =Initial amount of borrowing

0Y =initial net sales

nL =Amount of loans at the end of n-th period.

1 Y=py(p;価格、y;実質所得)と表すことができるため。

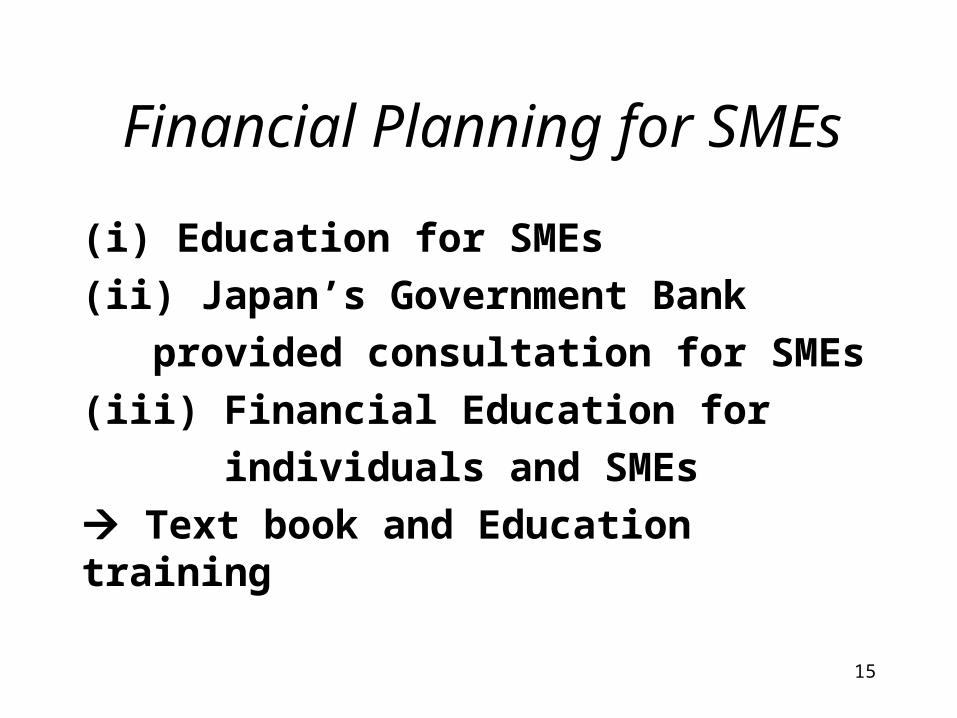

Financial Planning for SMEs

(i) Education for SMEs(ii) Japan’s Government Bank provided consultation for SMEs(iii) Financial Education for individuals and SMEs Text book and Education training

15

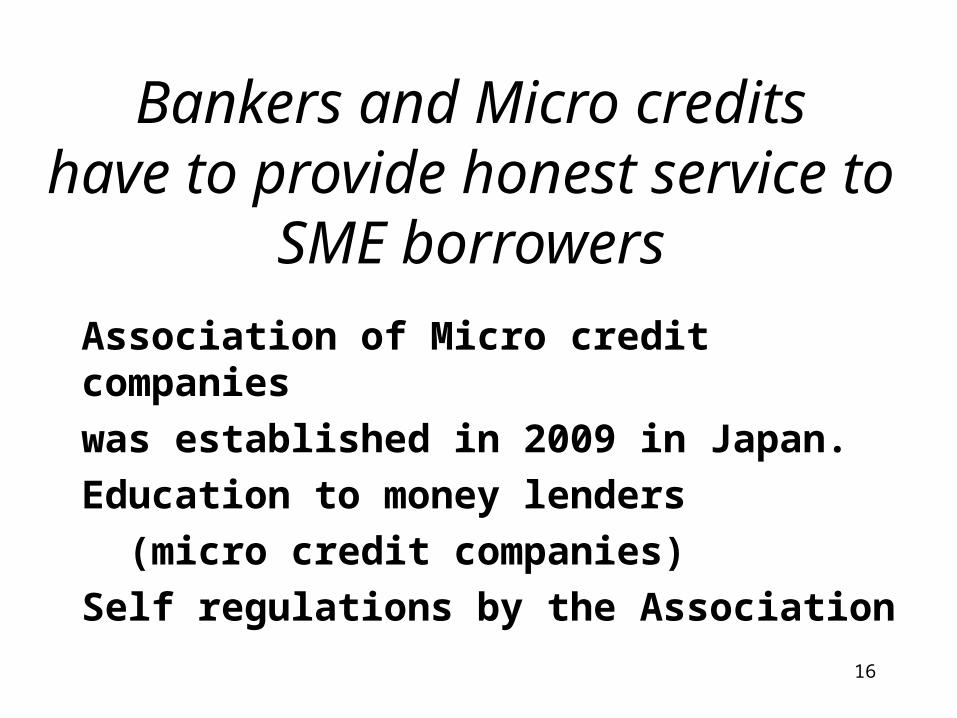

Bankers and Micro creditshave to provide honest

service to SME borrowers

Association of Micro credit companieswas established in 2009 in Japan.Education to money lenders (micro credit companies)Self regulations by the Association

16

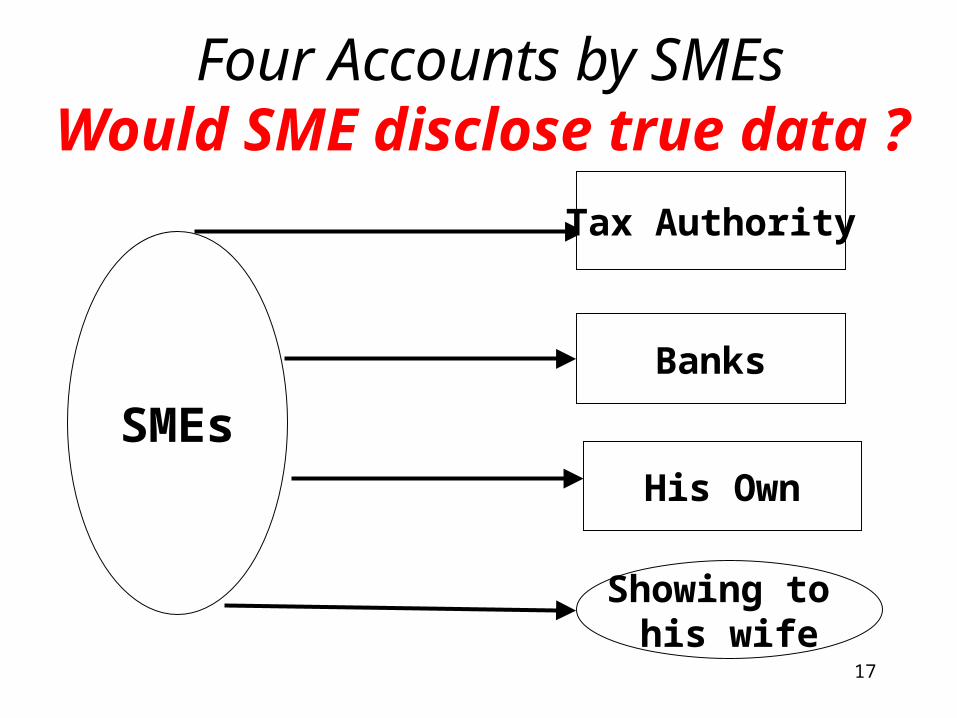

Four Accounts by SMEsWould SME disclose true

data ?

SMEs

Tax Authority

Banks

Showing to his wife

His Own

17

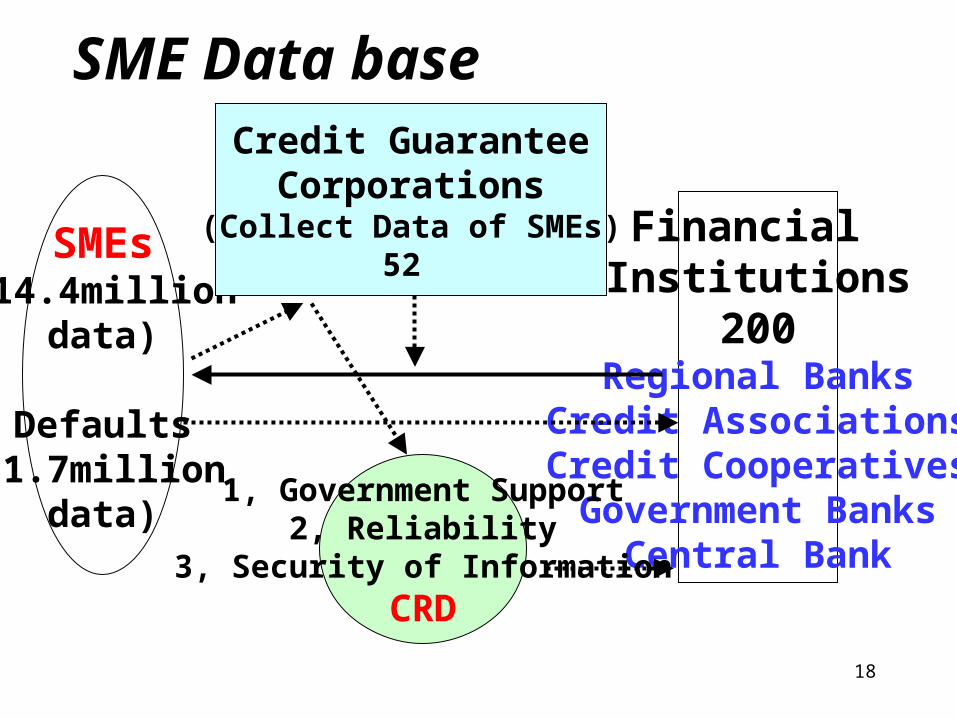

SMEs(14.4million

data)

Defaults(1.7million

data)

Financial Institutions

200Regional Banks

Credit AssociationsCredit CooperativesGovernment Banks

Central Bank

Credit GuaranteeCorporations

(Collect Data of SMEs)52

1, Government Support2, Reliability

3, Security of InformationCRD

SME Data base

18

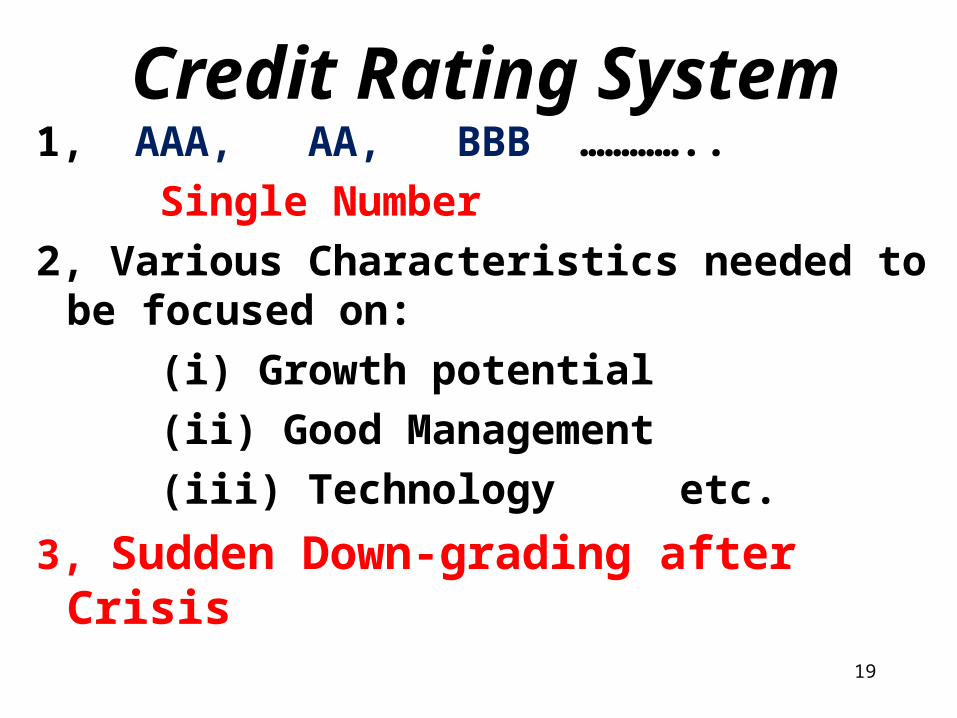

Credit Rating System1, AAA, AA, BBB …………..

Single Number2, Various Characteristics needed to

be focused on: (i) Growth potential (ii) Good Management (iii) Technology etc.

3, Sudden Down-grading after Crisis

19

Loan Supply CurveSME versus Large

Companies

20

LargeCompanies

Interest RateOn Loans

Loan Supply

SME Loans

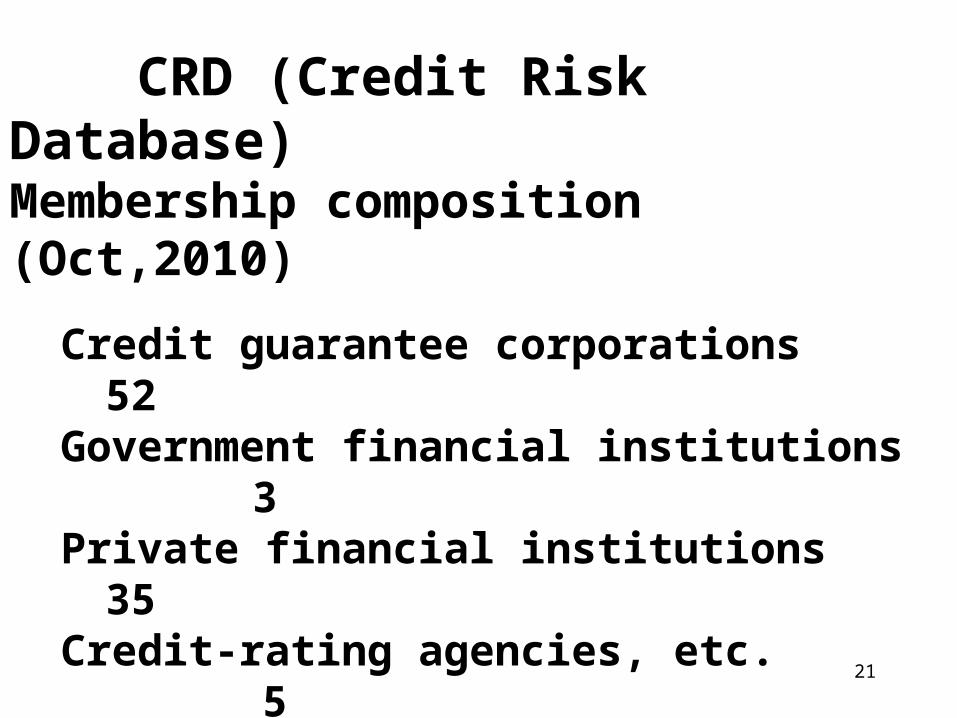

CRD (Credit Risk Database)Membership composition (Oct,2010)

Credit guarantee corporations 52 Government financial institutions 3 Private financial institutions 35 Credit-rating agencies, etc. 5 Small and Medium Enterprises Agency, Bank of Japan, etc. 5 Total 200 Annual fee=4 million (1st Year) 3 million yen (2nd yr)

21

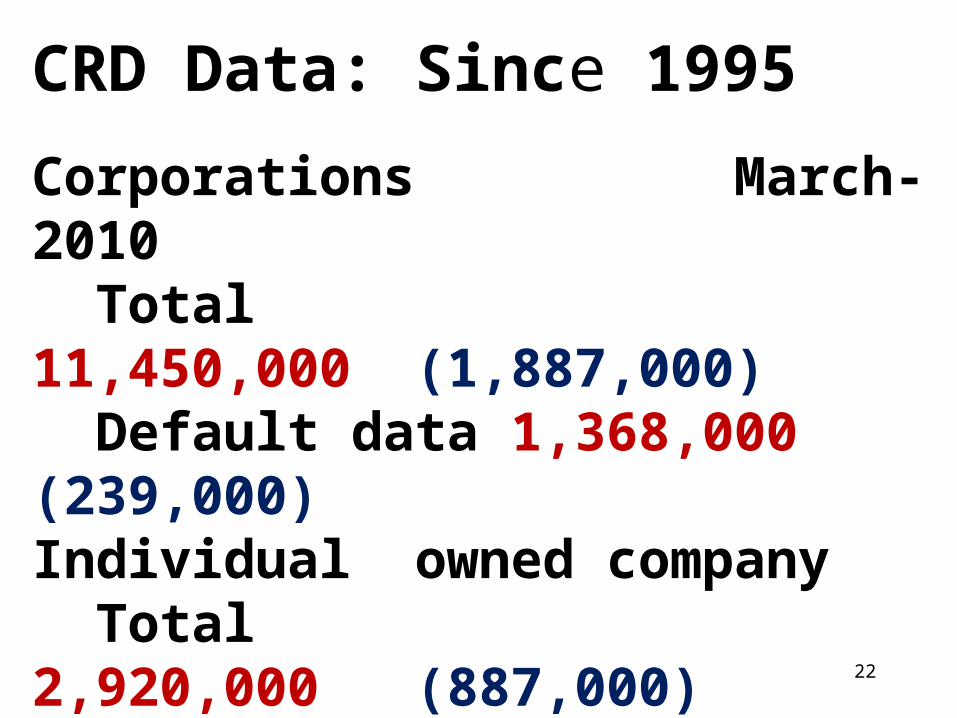

CRD Data: Since 1995

Corporations March-2010 Total 11,450,000 (1,887,000) Default data 1,368,000 (239,000)Individual owned company Total 2,920,000 (887,000) Default data 369,000 (369,000) Number of (Number of Accounts companies)

22

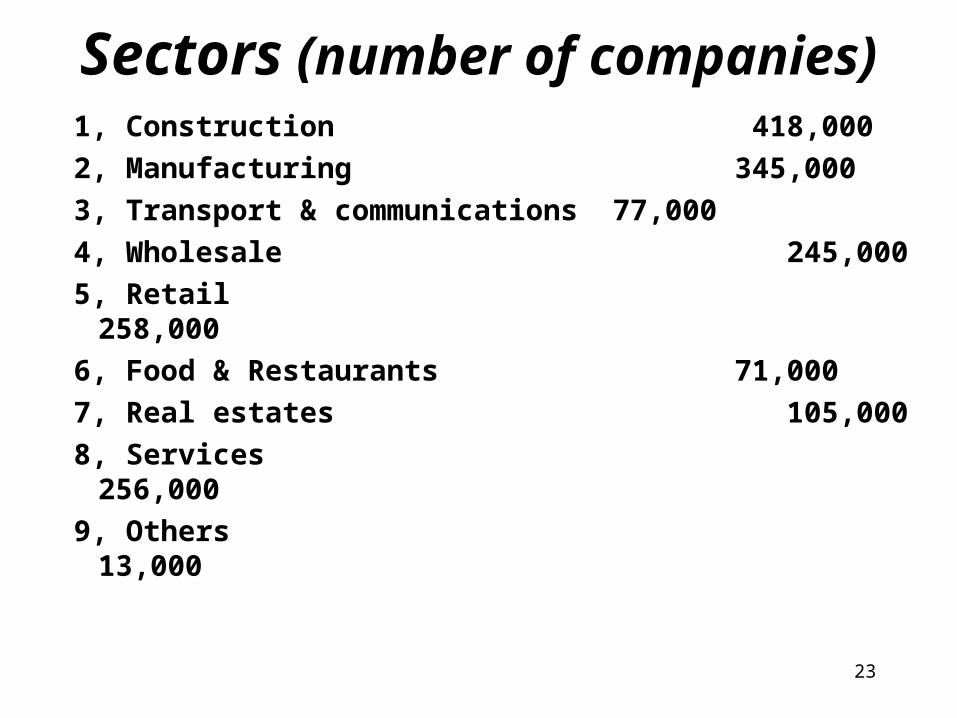

Sectors (number of companies)

1, Construction 418,0002, Manufacturing 345,0003, Transport & communications 77,0004, Wholesale 245,0005, Retail 258,0006, Food & Restaurants 71,0007, Real estates 105,0008, Services 256,0009, Others 13,000

23

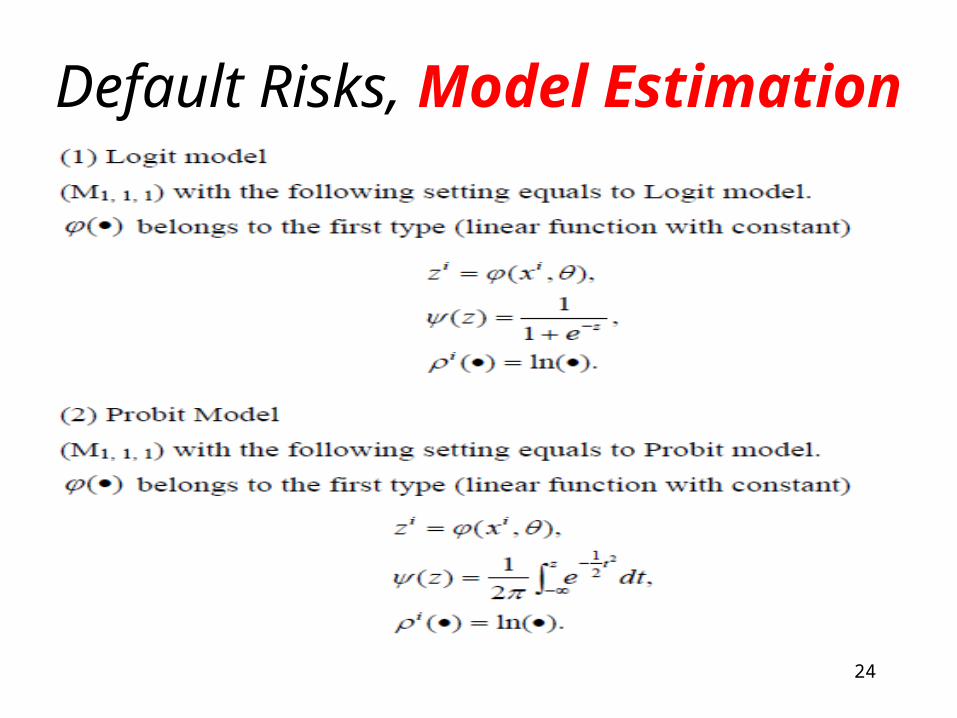

Default Risks, Model Estimation

24

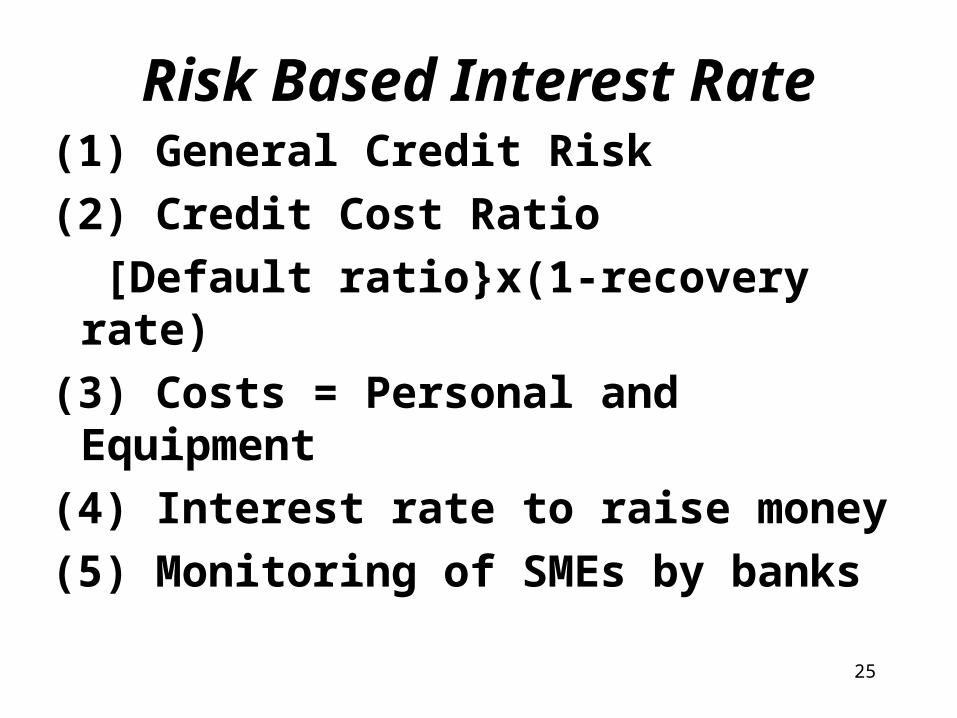

Risk Based Interest Rate

(1) General Credit Risk(2) Credit Cost Ratio [Default ratio}x(1-recovery rate)

(3) Costs = Personal and Equipment

(4) Interest rate to raise money(5) Monitoring of SMEs by banks 25

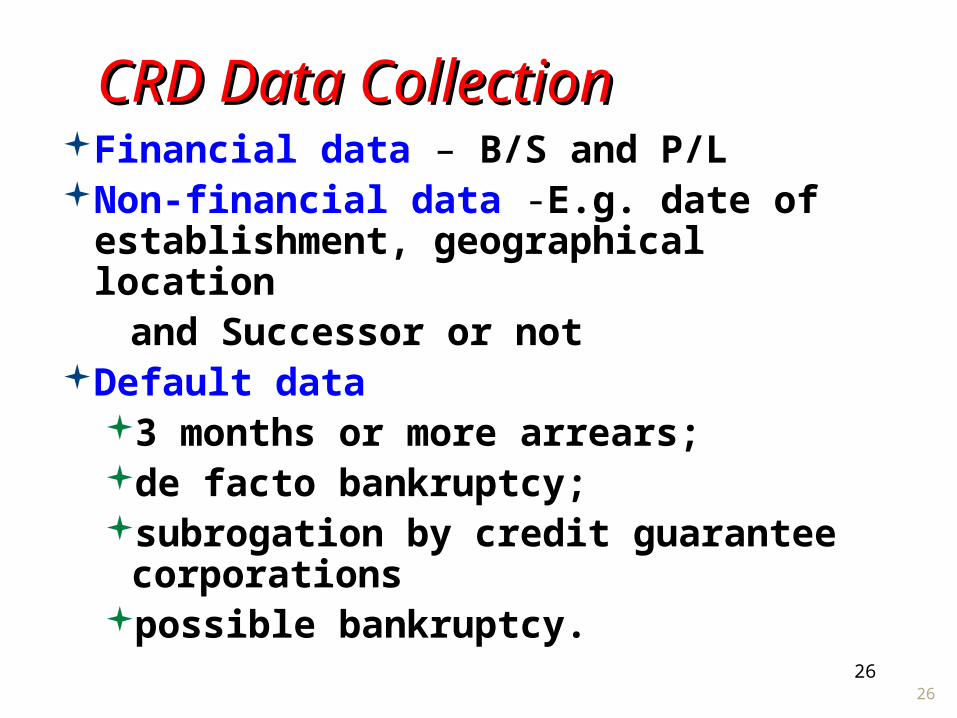

26

CRD Data CollectionCRD Data CollectionFinancial data – B/S and P/LNon-financial data -E.g. date of

establishment, geographical location

and Successor or notDefault data

3 months or more arrears; de facto bankruptcy; subrogation by credit guarantee

corporationspossible bankruptcy.

26

ReferencesYoshino, Suzuki, Maehara and Abe

(2009) Development of Corporate Credit Information Database and Credit Guarantee System,

ASEAN Secretariat, Feb. 2009.Yoshino, N.(2010),OECD, Southeast Asian

Economic Outlook, Fall 2010, Chapter 6Yoshino, N., OECD-ADB, THE GLOBAL

IMBALANCE AND THE DEVELOPMENT OF CAPITAL FLOWS AMONG ASIAN COUNTRIES

March 17, 2011, OECD

27

28

Asia’s Characteristics1, Large Share o f SMEs

(Small and Medium Enterprises)

2, Bank Dominated Market3, Long term commitment4, Large Share of Micro Credit5, High Savings Rate

29