council budget c s r

TRANSCRIPT

CITY COUNCIL OF SALT LAKE CITY451 SOUTH STATE STREET, ROOM 304P.O. BOX 145476, SALT LAKE CITY, UTAH 84114-5476

COUNCIL.SLCGOV.COM TEL 801-535-7600 FAX 801-535-7651

COUNCIL BUDGET STAFF REPORT

CITY COUNCIL of SALT LAKE CITYwww.slccouncil.com/city-budget

TO: City Council Members

FROM: Allison Rowland

DATE: May 28, 2021

RE: FY2021 BUDGET – GOLF ENTERPRISE FUND

MAYOR’S RECOMMENDED BUDGET PAGES: - Key Changes, B-32 to B-33- Department Overview, E-71 to E-75 - Staffing, F-32

ISSUE AT-A-GLANCEThe Golf Enterprise fund collects the revenue generated and pays most of its expenses associated with the activities of SLC Golf, a division of the Public Services Department. SLC Golf operates six golf courses, providing greens maintenance; golf clinics, camps, lessons, and events; and management of retail pro shops, cafés, and cart rentals. The recommended budget for the Golf Fund would remain flat for Fiscal Year 2021 (FY21), at $8,484,897, which is $23,433 (0.3%) more than in FY20. In recent years, the Golf Fund has relied increasingly on subsidies from the general fund to remain financially solvent. The FY21 Mayor’s Recommended Budget (MRB) would raise the total subsidy to the Golf Fund to $1,467,167, from $1,368,958 in FY20, $ (see summary chart below). The Finance Department has made a number of accounting changes this year to improve transparency in the way that subsidies and other supports for the Golf Fund recorded.

The Administration recommends that the FY21 Golf Fund budget essentially continue on the same path as in the FY20 budget. This would include:

1. Reimbursement of fees paid by the Golf Fund to Information Management Services (IMS) for technology services.

2. Reimbursement of other Administrative Fees paid by the Golf Fund to the general fund.

3. Transfer of funds from the general fund to the Golf Fund to support the payments of Golf’s debt service for irrigation improvements (ESCO). The plan is for the general fund to essentially refinance the ESCO debt through a sales tax bond at lower interest rates. The ownership of the debt will remain with the Golf Fund. Note: The Golf ESCO is a binding contract that has not generated

Item Schedule:Briefing: May 28, 2021Budget Hearings: May 21, June 4Potential Action: June 11 (TBD)

Page | 2

the anticipated savings which, as originally conceived, would have covered debt service. (See section C under Key Budget Issues & Policy Questions.)

4. Providing the second of a planned two-year general fund transfer of $500,000 to the Golf Fund. This subsidy is designed to provide time for new Golf Division leadership to implement its plans for improvement.

5. Implementation of “strategic price increases” to increase FY21 revenues.

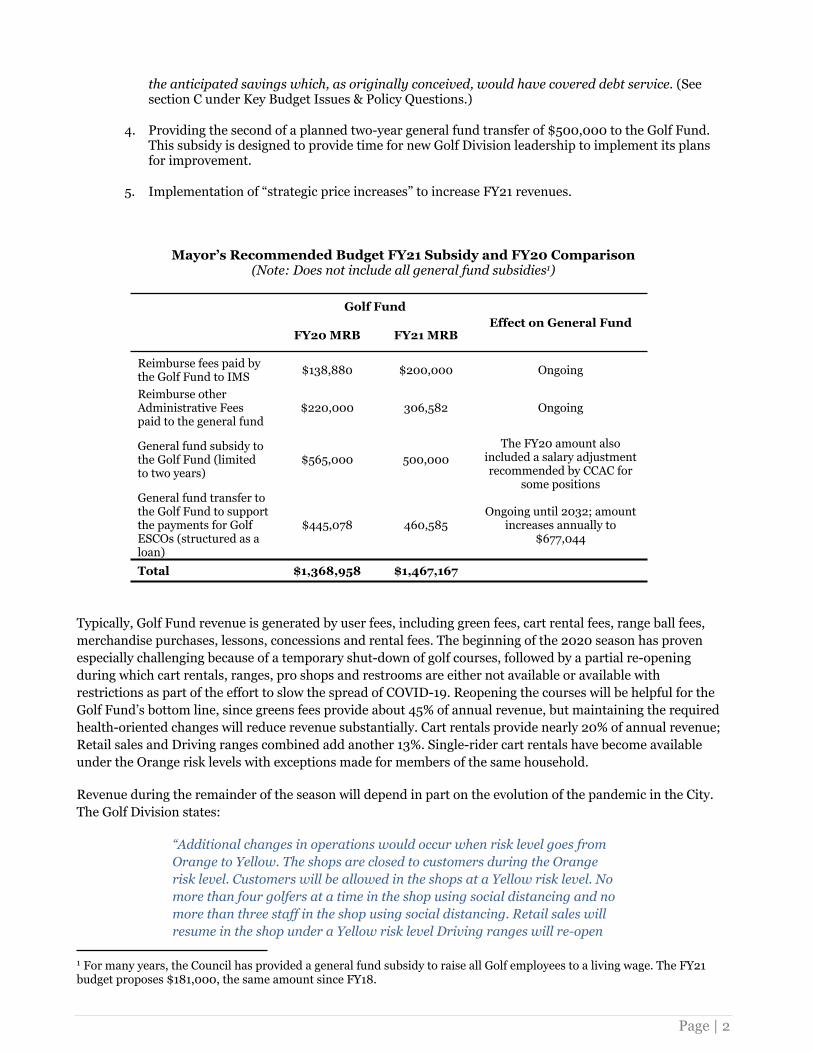

Mayor’s Recommended Budget FY21 Subsidy and FY20 Comparison(Note: Does not include all general fund subsidies1)

Golf Fund

FY20 MRB FY21 MRBEffect on General Fund

Reimburse fees paid by the Golf Fund to IMS $138,880 $200,000 Ongoing

Reimburse other Administrative Fees paid to the general fund

$220,000 306,582 Ongoing

General fund subsidy to the Golf Fund (limited to two years)

$565,000 500,000The FY20 amount also

included a salary adjustment recommended by CCAC for

some positionsGeneral fund transfer to the Golf Fund to support the payments for Golf ESCOs (structured as a loan)

$445,078 460,585Ongoing until 2032; amount

increases annually to $677,044

Total $1,368,958 $1,467,167

Typically, Golf Fund revenue is generated by user fees, including green fees, cart rental fees, range ball fees, merchandise purchases, lessons, concessions and rental fees. The beginning of the 2020 season has proven especially challenging because of a temporary shut-down of golf courses, followed by a partial re-opening during which cart rentals, ranges, pro shops and restrooms are either not available or available with restrictions as part of the effort to slow the spread of COVID-19. Reopening the courses will be helpful for the Golf Fund’s bottom line, since greens fees provide about 45% of annual revenue, but maintaining the required health-oriented changes will reduce revenue substantially. Cart rentals provide nearly 20% of annual revenue; Retail sales and Driving ranges combined add another 13%. Single-rider cart rentals have become available under the Orange risk levels with exceptions made for members of the same household.

Revenue during the remainder of the season will depend in part on the evolution of the pandemic in the City. The Golf Division states:

“Additional changes in operations would occur when risk level goes from Orange to Yellow. The shops are closed to customers during the Orange risk level. Customers will be allowed in the shops at a Yellow risk level. No more than four golfers at a time in the shop using social distancing and no more than three staff in the shop using social distancing. Retail sales will resume in the shop under a Yellow risk level Driving ranges will re-open

1 For many years, the Council has provided a general fund subsidy to raise all Golf employees to a living wage. The FY21 budget proposes $181,000, the same amount since FY18.

Page | 3

with a Yellow risk level utilizing spacing on the range tee and sanitizing procedures on range balls, buckets and tokens.”

KEY BUDGET ISSUES & POLICY QUESTIONS

A. Golf Fund Revenue Trends. Golf revenue appears to have improved slightly in recent years, since reaching a recent low in FY17. The recommended FY21 figures are not included here because they were projected before the extent of disruption caused by the pandemic was known; it would still be very difficult to estimate the combined effects of health concerns, increased leisure time for some residents, as well as economic distress for many.

FY15 FY16 FY17 FY18 FY19 FY20 Adopted$-

$500,000

$1,000,000

$1,500,000

$2,000,000

$2,500,000

$3,000,000

$3,500,000

$4,000,000

$4,500,000

Green FeesGolf Cart RentalDriving Range FeesRetail Merchandise SalesCIP Fee on rounds, passes

Golf Revenue Sources and Trends

B. Net Revenue. The slight increases in earned revenue in recent years are significant to the extent they indicate the potential of the Golf Fund to improve its financial position. However, the Golf Fund has continued to experience difficulties in covering operating expenses at the City’s six golf courses. For FY21 the problem may be exacerbated by the fact that revenues are likely to be lower than estimated before the pandemic, while expenses are mostly fixed in the short run. Personnel costs are typically around 48% of the total, including part-time, seasonal workers. Water and upkeep costs are also difficult to reduce while preserving the City asset and maintaining playability.

C. Golf Debt. The Golf fund will reimburse the Debt Service Fund for the portion of the debt corresponding to Golf assets. This will not eliminate the debt for Golf.

1. The Golf ESCO was issued specifically to cover secondary water systems at Rose Park and Glendale, and an improved irrigation system at Bonneville.

2. Regardless of how the debt is refinanced, the assets purchased through debt belong to the Golf Fund. By State law, that proportion of the debt must remain in the Golf Fund.

3. As in FY20, the ESCO debt remains in the Golf Fund. That year, the General fund gave or “supported” the Golf Fund so it could pay its debt, but that does not change the ownership of the debt. Golf, as an enterprise fund, must reflect all debt associated with its assets.

Page | 4

4. The refinance of ESCO debt resulted in $34,601 savings, which would be allocated to the Golf Fund based on its proportionate share of the original debt.

The Council may wish to ask the Administration to provide a plan for how and when the Golf Fund will repay the general fund.

D. Fund Balance. The MRB indicates a $554,459 increase in Golf’s fund balance (page B-12). This recommendation was prepared prior to the pandemic, and the status of this plan is not clear.

The Council may wish to request additional information from the Administration on the advantages and disadvantages of increasing the Golf Fund’s fund balance through a general fund subsidy, particularly in this time of economic uncertainty.

E. FY20 Legislative Intent. In an FY20 Legislative Intent, the Council asked the Administration to examine the open space zone ordinance to remove barriers to providing flexible food and beverage options at golf courses. To the extent that barriers exist in State law the Council requested an analysis of those, and that changing them be identified as a future legislative priority. The response from the Division was the following:

“Golf Food and Beverage Options. Golf recently completed an RFP process to secure a concessionaire for the café operations at Bonneville, Forest Dale, Glendale, Nibley Park, and Rose Park locations and are in the final contract negotiations with the selected vendor with anticipated operations beginning by the end of March. We are coordinating with the selected vendor to establish expanded operational hours at select locations to provide year-round breakfast and lunch options to the general public. We will continue to work with the selected vendor to explore improvements to the existing facilities that will make them more appealing and conducive to the new offerings. The selected vendor has indicated a willingness to invest their capital in necessary facility improvements up to a maximum of $15,000 per location. We recommend that the City provide a matching investment in helping to fund these needed improvements so that they become a draw for the public, not just golfers.”

The Council may wish to ask for additional information on the original request of this Legislative Intent, as well as an update on the status of the concessionaire.

F. Other Capital Improvement Projects. The latest list of Golf capital improvement projects dates from January 2015, and included up to $19.5 million in needed but deferred projects.

The Council may wish to ask the Administration for an updated deferred capital projects list that reflects the recommendations of the 2017 Golf Fund consultant.

The Council may wish to ask about the long-term plans for Golf capital improvements.

G. Nibley “Golf Entertainment Facility” RFI. In February 2019, the previous Administration published a Request for Information (RFI) on February 11, 2019 designed to improve services at Nibley Golf Course. It was described as an opportunity to develop “a neighborhood scale Golf Entertainment Facility” that would improve the course and public access at Nibley Park. Lease and other revenues were to be used to

Page | 5

support improvements to clubhouse facilities and golf course conditions at other Salt Lake City public golf course locations. (A more complete description can be found in Attachment C1.) When it closed on April 10, 2019, no responses had been submitted. In response to a request, the Golf Division’s listed the following as their understanding of the reasons for this result:

It is not known for certain as to why no one responded but based upon conversations with others who have approached the City in an effort to form a “PPP” we have heard a few things which may include the lack of response.

Our experience with private entities wanting access to our public land often results in a considerable ask from us for capital investments. In the RFP we were placing that burden on the bidder.

We find in our conversations with folks wanting to form a “Partnership” that they are largely interested in maintaining full control of the property and we would simply receive a check if there were profits or for an agreed to lease rate. We are anxious about entering into an agreement where we “turn over the keys” or privatize the public spaces.

We have discussed limited exposure to other efforts within the valley. But, I understand that with one project there was a barrier to completing the agreement due to LEED development requirements and the expense that placed upon the developer.

We continue to meet with parties who may be interested in making investments in the public spaces and are always willing to listen to their sales pitch.

Given the lack of responses to the RFP, the Council may wish to ask the Administration how they will use this experience to inform future RFPs for Nibley and other courses, including the “Rose Park Golf Course and Jordan Par 3 Park Area Improvement Concept,” discussed in the next section.

H. Rose Park Golf Course and Jordan Par 3 Park Area Improvement Concept. In response to a request for updates on the Rose Park Golf Course and Jordan Par 3 Park Area Improvement Concept begun under the previous Administration, the Golf Division responded the following:

“We continue to work with Public lands who has contracted with a consulting team to develop construction documents for the proposed trail network for the Rose Park and Jordan par 3 areas. Public lands anticipates completing 100% design documents by June 2020 and construction to start in the fall of 2020. The final plans include a looped trail system through the Jordan River Par 3 Disc Golf Course and a connection through the Rose Park Golf Course between the Jordan River Parkway Trail and Rosewood Park. The original proposal included additional trail through the Rose Park Golf Course, but this will be postponed at this time due to complications with alignments through and around the Public Utilities influent sewer tunnel project that is planned through portions of the Rose Park Golf Course. We continue to have discussions with potential partners to gauge interest but have been delayed by COVID-19 and an uncertainty around available investment resources.”

Additional details on the concepts of a new community center administered by the Youth and Family Division, and a “golf development center” on the back nine at Rose Park are presented in Attachment C1.

Page | 6

The Council may wish to request a detailed update on the Administration’s plans for this project. Based on previous discussions, topics could include some or all of the following questions:

o How these public lands improvements at the Jordan River Par 3 property will contribute to the City’s portfolio of parks and open spaces

o How funding might be acquired for a new community center on the propertyo How maintenance for these enhanced amenities may be funded. o How a “golf development center” at Rose Park Golf Course would fit with the role Nibley

Golf Course currently plays as a development center, and whether or how both can complement each other.

o How the approaches mentioned above will result in revenues at Nibley and Rose Park increasing sufficiently to cover expenses.

o How programming for the community center and the golf development center would be funded.

I. Wingpointe Golf Course. The previous Administration worked with a private group that was exploring partnerships to reopen Wingpointe. Would the Council like to request an update on this project from the Administration?

J. Golf CIP. The Golf CIP fund was established as the repository for a Council-mandated surcharge of $1 per round for the purpose of catching up on deferred maintenance and critical capital projects at all City courses. At the time it was established the Council’s intent was that these funds not be used to cover operational deficits. However, in years with an operations deficit, the Golf CIP fund has been used to “balance” short-term loans from the general fund so that operations can continue, from an accounting perspective.

The Council may wish to ask the Administration if the two-year plan includes a plan to get back to ideal spending levels for needed capital projects.

Meanwhile, given Golf’s aging infrastructure, in recent years urgent preventative maintenance or emergencies have arisen at courses. In response to a Council staff question during the FY20 budget discussions about the plans to address these, the Administration stated, “At this time we are primarily focused on emergency and high priority repairs as we are not in a place where we can begin to strategically invest in a formal capital facilities plan. Ideally we would like to mirror the strategies Facilities is looking to employ through the Capital Facilities Plan. The club houses and other structures are included in the Capital Facilities Plan.”

K. Council Policy Principles. A number of Golf Fund policy issues come up with regularity over the years. The Council adopted Guiding Policy Principles for Changes to the Golf Enterprise Fund (Attachment C2) in 2015. The Council may wish to discuss whether it would be helpful to review and update these to determine relevance to the FY21 budget and current policy goals of the Council.

1. The Council also may wish to discuss their adopted Guiding Policy Principles for Changes to the Golf Enterprise Fund in light of the FY21 MRB, reaffirming or reconsidering these with reference to the current situation. The City has a longstanding general policy of not subsidizing enterprise funds with general tax dollars, and the Council’s Policy Principles discourage general fund subsidies to the Golf Fund specifically, although in recent years there have been limited exceptions made to this rule. As part of these guiding policy statements, the Council also agreed that City-owned open space should be protected.

Page | 7

2.The traditional rationale for charging recreation fees for some amenities is related to the need for “exclusive” use of recreation facilities, like baseball diamonds and soccer fields during league play, or park pavilions for parties. Golf has been considered more similar to these exclusive uses than to “non-exclusive” uses like walking on a trail or playing catch on a grassy area, but there may be reasons to re-examine this view.

ADDITIONAL & BACKGROUND INFORMATION

A. Golf Advisory Board. The terms of all current board members have expired. Names were submitted to the previous Administration but no additional appointments have been recommended. City policy allows appointees to continue serving until a new appointment is made.

B. Season Passes. In response to a question, the Golf Division stated:“In a recent analysis of our annual pass programs, we found certain aspects of the Corporate VIP pass program were being utilized in ways not consistent with the intended purpose of the program and it was deemed necessary to suspend the program while a replacement product was developed. Additionally, two season pass programs (2-course passes) were cancelled due to market pricing inconsistencies and low revenue per round returns. The advantages to the Game Pack product is that they are like digital punch cards that are transferrable and holders can designate other users (family members, friends, work associates) to be able to redeem without payment due at course. Game Packs are single course use and are therefore priced lower than traditional passes and provide a more cost effective entry into this discount program. The disadvantage of the program is that they are limited to a single course and the overall per use discount is lower than a traditional pass. We still have retained our two most popular pass programs as an alternative. Both passes represent excellent value and are priced below competing pass programs. We are close to being able to offer the new programs online with payment options, which will be a major plus with customers.”

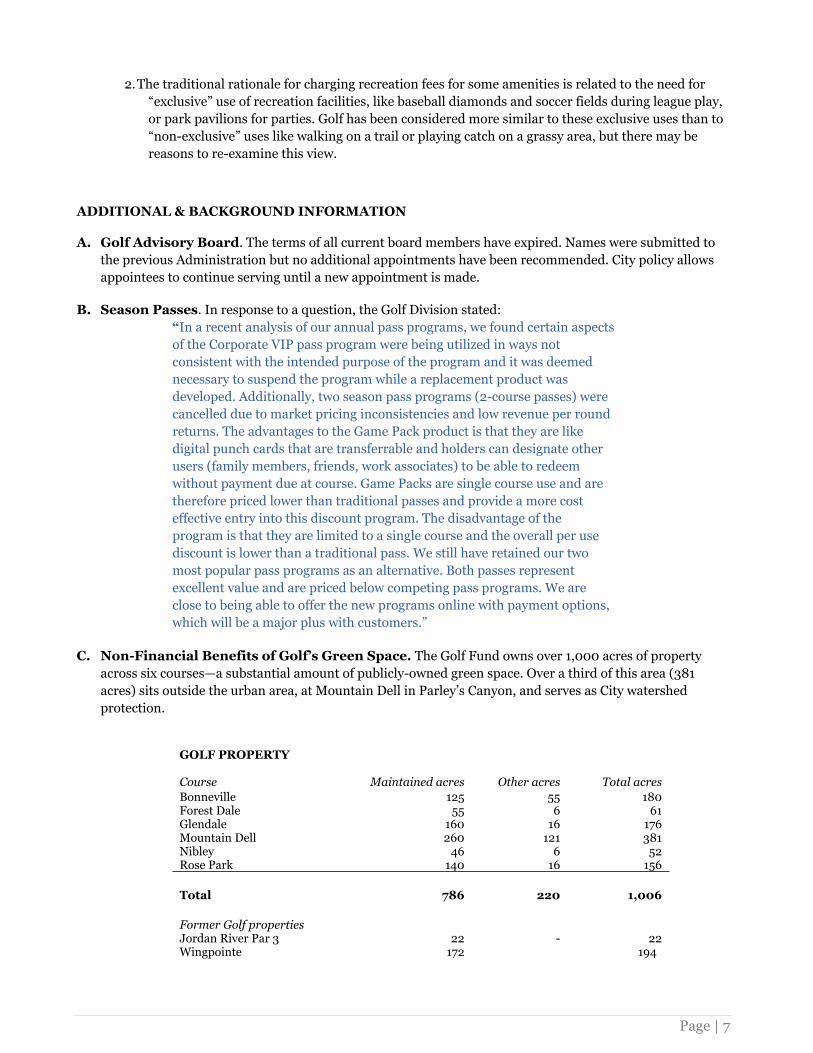

C. Non-Financial Benefits of Golf’s Green Space. The Golf Fund owns over 1,000 acres of property across six courses—a substantial amount of publicly-owned green space. Over a third of this area (381 acres) sits outside the urban area, at Mountain Dell in Parley’s Canyon, and serves as City watershed protection.

GOLF PROPERTY

Course Maintained acres Other acres Total acres Bonneville 125 55 180 Forest Dale 55 6 61 Glendale 160 16 176 Mountain Dell 260 121 381 Nibley 46 6 52 Rose Park 140 16 156

Total 786 220 1,006

Former Golf propertiesJordan River Par 3 22 - 22 Wingpointe 172 194

Page | 8

The Administration has indicated that there are Citywide benefits to maintaining golf courses as partially-funded green open space, though they acknowledge that the non-golf benefits are experienced by most taxpayers in a passive manner. In response to a question, the Division noted:

“Much of the non-golf use is passive in nature, and the access and preservation of the open public spaces provide many opportunities and benefits to the public such as:

Trees and Open Space. Contributes benefits to air quality, urban heat islands, urban wildlife interfaces and

Other activities include winter time access, walking, snowshoe, dogs, and trails.

Public access to clubhouse and cafe’s Public meeting space at Forest Dale Jordan River Trail Glendale and Rose Park Disc Golf and Footgolf at Rose Park”

D. Comparative Research in 2019. The Finance Department conducted a review of many municipally-owned golf course systems around the country, as well as a more in-depth review of the accounting laws governing enterprise funds in the State of Utah.

Key takeaways from the Administration following their review:

Cities of Salt Lake City’s population size do not typically have such extensive public golf systems. Most of the comparisons are with larger cities in the West.

No other system studied charges administrative fees—although the same municipalities do charge fees to other enterprise funds.

All but one municipal system operated with a structural and persistent deficit. All those deficits were supplemented with ongoing support of the municipal general fund.

The State of Utah has legal and accounting barriers that the Finance Department has interpreted to prohibit simply “absorbing” the Golf Fund into the City general fund. They appear to mean that SLC Golf must remain a separate enterprise fund. To confirm this interpretation, the Attorney’s Office has been asked to provide an opinion on the matter.

Similarly, there are legal and accounting barriers to the general fund “assuming” the Golf Fund’s ESCO (existing secondary water-system debt). However, the general fund is permitted to provide funds to the Golf Fund to pay these debts.

The Administration does not indicate any interest in selling or developing Golf property for a different use.

Given the proposed elimination of Administrative Fees currently paid to the general fund by other Enterprise funds (such as the Airport), the Council may wish to request the Administration’s key public policy findings that support the notion of not charging Administrative fees and supporting the debt of an enterprise fund. There is close scrutiny on the topic of Administrative fees, which is the allocation of expenses to departments and entities. To preserve the integrity of the City’s cost allocation system, the Council may wish to ask the Administration to provide a more formal assessment of the public benefit and reasoning for this change to be included in the public record.

Page | 9

E. Tree Nursery on Golf Property. The Division reports that it is working with the Golf Division on an initiative to create a tree nursery with a gravel bed on a small (50’x50’) space of unused golf course property. The tree nursery is not anticipated to save City funding but rather, would be an opportunity to evaluate and learn more about tree growth and tree adaptability in the Utah environment. The Division states:

“A nursery at every golf course would not be efficient, as many trees can be nurtured into larger trees in a small space. Urban Forestry does not foresee any significant financial aspect to keeping trees on golf course property. The trees and nursery supplies can be paid out of the UF Division reforestation budget and water use would be minimal. Due to the small space requirements of a gravel bed nursery, it is possible to use park space or other City property locations to grow trees. An appropriate site needs to be relatively secure and have water available. Preferably, UF would start a program like this with a small-scale tree growing program and evaluate the feasibility over the course of a few years.”

F. Parks and Golf Expenses Comparison. In 2017, at the request of the Council, the Public Services Division provided a comparison of annual maintenance and operations costs-per-acre for Liberty Park ($10,682 per acre) versus the average for golf courses ($7,288 per acre). These were offered as only rough figures, since at that time data collection was not as systematic. There were also a number of important limitations to the data, including that Liberty Park has especially high costs because of special features and events, as well as year-around use. In addition, most golf courses were not on secondary water at the time, though Liberty Park was already. The Department offered to provide more detailed figures for comparison once the Accela program was operable. An update to this comparison would be useful, specifically, for parks of different classes (regional, community, neighborhood) and each of the golf courses. Data on average daily users would also be of interest, since most parks are used much more intensively than golf courses.

The Public Services Department provided the following update for FY21:

“This is a question that Public Lands has been working to answer for Liberty and every park in our system for several years now. What does it cost to maintain each park, trail mile, median and natural space in our system? The good news is that Public Services now has a software system, Cartegraph, that appears to have the functionality needed to accomplish answering this question. Parks staff began use of this new system in December of 2019, tracking labor hours at each site (Parks staff may work at multiple sites in a day). The next step will be to include materials costs. This appears to be a feature that will be added soon. Once fully implemented, a year of data input will be needed to calculate an average cost by park per acre.

Data on average daily users is a project that IMS is helping Public Lands to achieve. Together we are looking to pilot two smart park benches in our parks that will provide park users wi-fi access, device charging, and average daily use by tracking the number of IP addresses that pass by the bench within a specified radius. This device will provide user counts only and no other information about who has visited the park.”

G. General Background. As an enterprise fund, the Golf Fund is charged with managing and maintaining the courses within the revenues that it can generate through its operations. The Council has been concerned about the financial sustainability of the Golf Fund since at least 2007. As early as 2004, deficits began to appear in the Golf Fund, though these problems typically were described as temporary anomalies,

Page | 10

rather than longer-term structural issues, and were covered with the Golf Fund’s then-substantial fund balance, that was built up in the late 90s and early 2000s when Golf was significantly more profitable.

In 2014, after then-Mayor Ralph Becker indicated that he would close courses, the Council adopted a series of policy statements to define their shared view of how the system should serve golfers, as well as the limits of what could be done to change the system (Attachment C2). Later that year, the Council embarked on a process of information gathering and pursued an extensive process to gather ideas from the public. The Council also hired a municipal finance consultant to identify options that could help the Golf Fund maintain financial solvency over the long term. In late 2014 and early 2015, a Council-appointed citizen task force reviewed all the information assembled, including the consultant’s report and all of the public’s ideas for Council consideration, and provided their recommendations to the Council. The process culminated in the Council’s own recommendations to the Administration in February, 2015 (Attachment C3).

Then-Mayor Biskupski’s Administration was optimistic about potential for Golf’s turnaround, and appeared to prefer a more incremental approach to change. The guiding policy ultimately articulated was that City golf courses should be subsidized because they are “public open spaces” that nearly pay for themselves—unlike traditional parks, which do not raise significant revenue. Another initiative was to plan for more trail uses at Jordan Par 3 and around Rosepark, which would require substantial capital investment, some of which was begun during her term (see Attachment C1). As noted above, an RFI was published for a “TopGolf”-like experience at Nibley (2019), but did not attract any proposals.

ATTACHMENTS

Attachment C1. Biskupski Administration Summaries of Nibley and Rose Park RFP Plans

Attachment C2. 2014 Guiding Policy Principles for Changes to the Golf Enterprise Fund

Attachment C3. 2015 Council Recommendations to the Administration Options to Address Long-Term Golf Fund Issues

Attachment C4. Rounds by Course, 2001 to 2019

Page | 11

Attachment C1. Administration Summaries of Nibley RFP and Rose Park/Jordan River Par 3 Plans, May 16, 2019

Nibley Park Golf Course RFP with Background Discussion It was determined as a part of the 2019 budget process and following the review of the 2017 RFI’s relating to golf management that we would prepare an RFP for enhanced services at Nibley Park Golf Course. This RFP has been prepared and was published on February 11, 2019 with a response period of eight weeks. The development of the RFP needed to be sensitive to a couple core issues. First, the new development needs to be sensitive to the 1921 donation agreement and done in a way that public access is guaranteed, and that golf remains the core focus of the space. The Second core issue is that the development needs to be done in a way that impacts on the community are community. Additionally, the driving range portion of Nibley Park is in South Salt Lake City and as such a boundary adjustment with south Salt Lake City will be required. Currently the South Salt Lake City boundary maps do not show this are to be a part of South Salt Lake City, but the Salt Lake City boundary maps do show the area as outside of Salt Lake City. Objective: Develop a neighborhood scale “Golf Entertainment Facility” located at the Nibley Park Golf Course. It is a requirement that the existing public golf course remain operational and that the new facility will complement and support the public course. The facility must be publicly available and promote recreation and pleasure in connection with Golf. The new facility needs to be designed with the neighborhood location in mind. This means location, lighting and noise must be designed in a way that it mitigates glare and sound beyond the property boundaries. The facility needs to be architecturally complementary to the neighborhood environment, additional parking and accessory structures should be screened or designed in a way that changes maximize the open green space feel of the course. Nibley Park Golf has operated with an operational deficit for years and has leveraged revenues from other courses to maintain its operations. This leveraging of the Golf Enterprise Fund has resulted in a lack of reinvestment in course facilities at “profitable” locations. It is the intention that this development will improve the course and public access at Nibley Park, and lease/additional revenues may be used to support the Golf Enterprise Fund finance improvements to clubhouse facilities and golf course conditions at other Salt Lake City public golf course locations. It is a core intention of this project to help stabilize the Golf Enterprise Fund and set a course for longer term financial stability. Council Principles/ Legislative Intents: Here is a list of a few of the “Council Principles” which are relevant to this project. These may be leveraged as a part of the RFP Selection/development of the decision criteria. ○ Make decisions based on the best interest of Salt Lake City residents.○ The Golf Fund should be self-sustaining and without general fund subsidy.○ Commercial development on open space should be avoided wherever possible.○ Any re-purposing of golf courses should add value for the neighborhood and its residents, and benefit residents through high quality amenities.○ Neighborhood quality of life is enhanced by adjacent open space, regardless of use, and therefore should be protected.○ All solutions for the Golf Fund’s financial issues will be evaluated on a 10-year basis.○ Golf Task Force Presentation http://www.slccouncil.com/wp-content/uploads/2015/01/GolfTaskForce_Presentation.pdfOutcome:

Page | 12

The RFP closed on April 10, 2019, there were no responses submitted. We will take some time to reflect on this and try and determine a best next step. In preparation for this a petition for a boundary adjustment was initiated and the Planning Division has contacted South Salt Lake to begin the conversations relating adjusting the City boundaries.

Rose Park Golf Course and Jordan Par 3 Park Area Improvement Concept

Salt Lake City Golf has been looking at how we can improve access to the public open space while maintaining a high-quality golf experience. Rose Park Golf Course is an 18-hole course consisting of the original course on the west side along Redwood Road, a newer nine-hole course to the east of the river, and a large open space to the south of the club house which has been used as a driving range and a pitch and putt area but is largely unprogrammed open space. Rose Park has struggled financially, this struggle has impacted the Golf Funds ability to make investments in other courses. Golf rounds at Rose Park for 18 holes averages about the same for rounds played at Forest Dale Golf Course, which has nine holes. This average coupled with the public access via the Jordan River Trail, the new multipurpose trail and future management/programming development of the Jordan River Par 3 Property makes the Rose Park Golf Course ripe for discussion about how we might re-imagine this area in a way that broadens public access, maintains a high quality golf experience and incorporates financial strategies that support a long term vision for the public space. Jordan River Par 3 Property:In November 2014 the Jordan River Par 3 golf course was transitioned from a traditional golf course managed by Salt Lake City Golf Division to a disc golf course managed by Salt Lake City Public Lands. At this time the City entered into an agreement with The Tunnel Runners Association to continue operation of a public disc golf course on the property. The agreement between SLC and the Tunnel Runners Association is renewed on an annual basis.In 2016 SLC Public Lands contracted with BioWest Incorporated to begin work on a management and use plan for the Jordan River Par 3 property. The priorities for this project included; providing safe pedestrian access through proper trail design and layout; making the project area readily accessible via trail networks that include wayfinding and signage; identifying natural systems strategies for planning, design, and long term management; developing management strategies for mixed recreational uses (e.g., golfers and trail users) throughout the project area; identifying potential partnerships that have a role in programming and stewardship; and identifying ways to foster appropriate use and stewardship of the site.During the initial phase of this project, it was determined that SLC Public Lands would request funding for design and construction of a public use trail through both the Jordan River Par 3 property and the adjacent Rose Park Golf Course. In 2018, funding for the trail system was secured through the City’s CIP fund and SLC is now working with BioWest Incorporated to include the necessary construction documents for the trail as part of the Jordan River Par 3 project. The final design for the trail system will include landscaping and management strategies to improve the recreational experience and ensure safety for all trail users. Complete design of the trail system and landscaping improvements is estimated to be complete in the Summer/Fall of 2019 with anticipated construction occurring in Spring of 2020.Two new possibilities for the space are the development of a community center supporting learning, family support and recreation opportunities and a golf development center, these are just ideas for discussion.

Community Center; Salt Lake City through Youth and Family Division provides a broad range of programs and services to the community. Our current locations are Central City Rec. Center, Fairmont Park, Liberty Park, Ottinger Hall, and across the Sorenson Campus. Due to space limitations the only program currently provided by Youth and Family serving residents in Rose Park, Poplar Grove and Fairpark neighborhoods is a small teen program at the Northwest Recreation Center. Five elementary and one middle school serve the Northwest Quadrant of the City. All six schools are title one schools with over 85% of their students qualifying for free lunch. The schools are minority majority and many of the students come from families where English is a second language. Salt Lake City has a rich history of supporting, youth, families, and allied community

Page | 13

partners and organizations. Salt Lake City Corporation has successfully established programs and services in all quadrants of the City with the notable exception of the Northwest Quadrant.

Golf Development Area; We are hearing throughout the Golf community about the need for a golf development space that will encourage the growth of the game of golf through improved player development. This is a space that includes driving ranges, pitch and putt spaces, practice holes and spaces for swing improvement and analysis. We are looking at converting the “back nine” or holes east of the Jordan River to a Golf Development area. An additional contributing factor to this change relates to the development of the multi-use trail. Routing a trail through a golf course has some safety challenges and it was determined that there is no safe route through the “front nine”, as such, we are looking at the potential to design the golf development area to include the multi-use trail. This redesign opportunity is essential to the development of the new trail. To bring this all together we need to have more conversations with the community, outline options for development funding, and management and operations. The following graphic illustrates this concept. Compared to the Nibley RFP this project needs to be built off of a more traditional public private partnership v a transition to a privately managed operation on public property, like we tried with Nibley Park Golf Course.

Page

| 14

Improvement Concept Rose Park Golf Course and Jordan Par3 Park Area Salt Lake City Public Services Department. Golf Division

0 New Golf Amenity 0 Rose Park Trail

0 Existing Golf -Course Land - Jordan River Trail

0 Land Transfer to Parks

- Land Use sF ..:;;$' I - TBD

~ a::: 0 z

I IC::: 0 z 0 0 0

I

h: 0 z 0 0 0

Page | 15

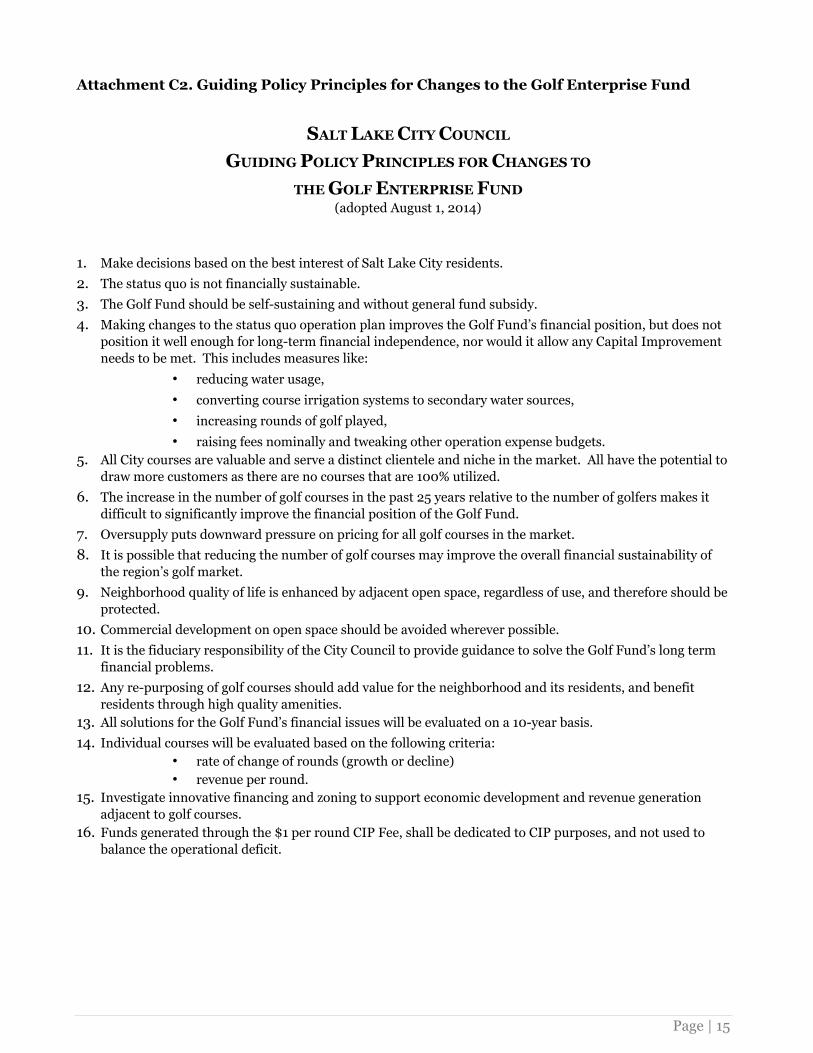

Attachment C2. Guiding Policy Principles for Changes to the Golf Enterprise Fund

SALT LAKE CITY COUNCIL GUIDING POLICY PRINCIPLES FOR CHANGES TO

THE GOLF ENTERPRISE FUND (adopted August 1, 2014)

1. Make decisions based on the best interest of Salt Lake City residents. 2. The status quo is not financially sustainable. 3. The Golf Fund should be self-sustaining and without general fund subsidy. 4. Making changes to the status quo operation plan improves the Golf Fund’s financial position, but does not

position it well enough for long-term financial independence, nor would it allow any Capital Improvement needs to be met. This includes measures like:

• reducing water usage,

• converting course irrigation systems to secondary water sources,

• increasing rounds of golf played,

• raising fees nominally and tweaking other operation expense budgets. 5. All City courses are valuable and serve a distinct clientele and niche in the market. All have the potential to

draw more customers as there are no courses that are 100% utilized. 6. The increase in the number of golf courses in the past 25 years relative to the number of golfers makes it

difficult to significantly improve the financial position of the Golf Fund. 7. Oversupply puts downward pressure on pricing for all golf courses in the market. 8. It is possible that reducing the number of golf courses may improve the overall financial sustainability of

the region’s golf market. 9. Neighborhood quality of life is enhanced by adjacent open space, regardless of use, and therefore should be

protected. 10. Commercial development on open space should be avoided wherever possible. 11. It is the fiduciary responsibility of the City Council to provide guidance to solve the Golf Fund’s long term

financial problems. 12. Any re-purposing of golf courses should add value for the neighborhood and its residents, and benefit

residents through high quality amenities. 13. All solutions for the Golf Fund’s financial issues will be evaluated on a 10-year basis. 14. Individual courses will be evaluated based on the following criteria:

• rate of change of rounds (growth or decline) • revenue per round.

15. Investigate innovative financing and zoning to support economic development and revenue generation adjacent to golf courses.

16. Funds generated through the $1 per round CIP Fee, shall be dedicated to CIP purposes, and not used to balance the operational deficit.

Page | 16

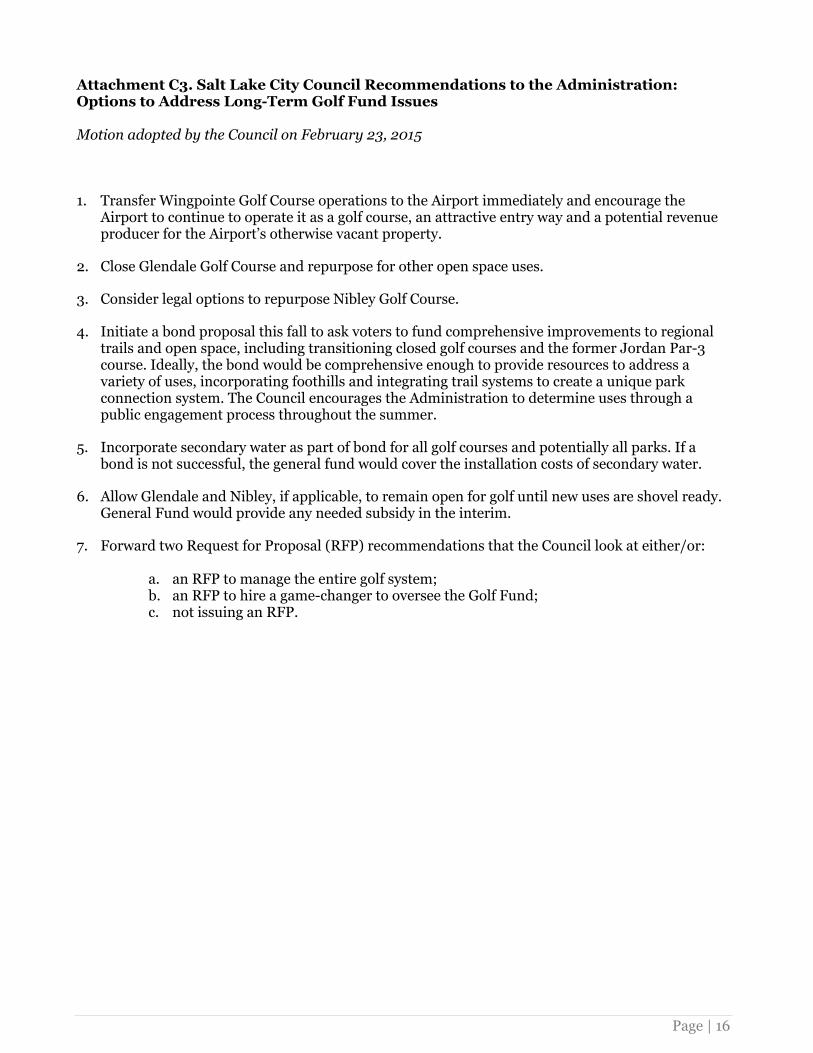

Attachment C3. Salt Lake City Council Recommendations to the Administration: Options to Address Long-Term Golf Fund Issues Motion adopted by the Council on February 23, 2015

1. Transfer Wingpointe Golf Course operations to the Airport immediately and encourage the Airport to continue to operate it as a golf course, an attractive entry way and a potential revenue producer for the Airport’s otherwise vacant property.

2. Close Glendale Golf Course and repurpose for other open space uses.

3. Consider legal options to repurpose Nibley Golf Course.

4. Initiate a bond proposal this fall to ask voters to fund comprehensive improvements to regional trails and open space, including transitioning closed golf courses and the former Jordan Par-3 course. Ideally, the bond would be comprehensive enough to provide resources to address a variety of uses, incorporating foothills and integrating trail systems to create a unique park connection system. The Council encourages the Administration to determine uses through a public engagement process throughout the summer.

5. Incorporate secondary water as part of bond for all golf courses and potentially all parks. If a bond is not successful, the general fund would cover the installation costs of secondary water.

6. Allow Glendale and Nibley, if applicable, to remain open for golf until new uses are shovel ready. General Fund would provide any needed subsidy in the interim.

7. Forward two Request for Proposal (RFP) recommendations that the Council look at either/or:

a. an RFP to manage the entire golf system; b. an RFP to hire a game-changer to oversee the Golf Fund; c. not issuing an RFP.

Salt Lake City Golf Courses

Average Rounds of Golf Played (9 Hole Equivalents)For Fiscal Years 2001 to 2019

Bonneville Forest Dale GlendaleMountain Dell

All Nibley Park Rose Park Annual Total

19-Year Average 75,570 45,293 67,591 100,949 32,554 57,336 379,293 2010-2019 Average 70,403 41,184 67,622 93,791 31,531 52,439 356,970 2015-2019 Average 67,388 40,690 67,026 92,018 30,200 51,047 348,369

0

20000

40000

60000

80000

100000

120000

140000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Attachment C4. Trends in Rounds by Course, 2001 to 2019

Bonneville Forest Dale Glendale Mountain Dell All Nibley Park Rose Park

Salt Lake City Golf Courses

Total Rounds of Golf Played (9 Hole Equivalents)For Fiscal Years 2001 to 2019

Bonneville Forest Dale GlendaleMountain Dell

All Nibley Park Rose Park Annual Total 2001 88,921 54,959 65,905 125,067 36,514 68,328 439,694 2002 88,955 53,306 69,116 119,752 34,760 70,977 436,866 2003 86,939 54,394 74,612 113,236 31,796 73,695 434,672 2004 79,012 48,342 65,613 110,403 30,528 59,615 393,513 2005 76,832 46,887 63,694 93,377 34,400 58,033 373,223 2006 77,331 48,791 63,308 104,874 34,958 58,265 387,527 2007 79,145 49,092 65,547 108,699 33,417 57,722 393,622 2008 77,682 47,183 68,800 103,264 32,955 56,634 386,518 2009 76,982 45,768 71,407 101,445 33,893 61,735 391,230 2010 72,624 41,608 72,376 95,802 32,819 60,991 376,220 2011 70,731 38,970 63,318 93,227 30,023 50,806 347,075 2012 79,847 45,125 72,170 100,803 36,526 54,509 388,980 2013 69,980 41,305 66,418 95,084 32,769 50,998 356,554 2014 73,902 41,382 66,812 92,908 32,177 51,848 359,029 2015 69,356 43,375 68,091 92,542 31,872 53,371 358,607 2016 62,352 40,042 63,621 88,589 30,162 48,595 333,361 2017 66,073 40,652 67,802 91,361 30,637 47,145 343,670 2018 67,750 40,283 68,496 95,675 28,870 54,581 355,655 2019 71,411 39,099 67,118 91,922 29,457 51,543 350,550

19-Year Average 75,570 45,293 67,591 100,949 32,554 57,336 379,293