corporate presentation tsx: bne november 2019 · bonterra will generate significant discretionary...

TRANSCRIPT

1

November 2019TSX: BNECORPORATE PRESENTATION

2

Forward Looking InformationCertain statements contained in this Presentation include statements which contain words such as “anticipate”, “could”, “should”, “expect”, “seek”, “may”,“intend”, “likely”, “will”, “believe” and similar expressions, statements relating to matters that are not historical facts, and such statements of our beliefs,intentions and expectations about development, results and events which will or may occur in the future, constitute “forward-looking information” within themeaning of applicable Canadian securities legislation and are based on certain assumptions and analysis made by us derived from our experience andperceptions. Forward-looking information in this Presentation includes, but is not limited to: expected cash provided by continuing operations; future capitalexpenditures, including the amount and nature thereof; oil and natural gas prices and demand; expansion and other development trends of the oil and gasindustry; business strategy and outlook; expansion and growth of our combined business and operations; and maintenance of existing supplier and partnerrelationships; supply channels; accounting policies; credit risks; and other such matters. Forward-looking information in this Presentation also includes, but is notlimited to, the timing and amount of future dividend payments by Bonterra.

All such forward-looking information is based on certain assumptions and analyses made by us in light of our experience and perception of historical trends,current conditions and expected future developments, as well as other factors we believe are appropriate in the circumstances. The risks, uncertainties, andassumptions are difficult to predict and may affect operations, and may include, without limitation: foreign exchange fluctuations; equipment and labourshortages and inflationary costs; general economic conditions; industry conditions; changes in applicable environmental, taxation and other laws and regulationsas well as how such laws and regulations are interpreted and enforced; the ability of oil and natural gas companies to raise capital; the effect of weatherconditions on operations and facilities; the existence of operating risks; volatility of oil and natural gas prices; oil and gas product supply and demand; risksinherent in the ability to generate sufficient cash flow from operations to meet current and future obligations; increased competition; stock market volatility;opportunities available to or pursued by us; and other factors, many of which are beyond our control. The foregoing factors are not exhaustive.

Actual results, performance or achievements could differ materially from those expressed in, or implied by, this forward-looking information and, accordingly, noassurance can be given that any of the events anticipated by the forward-looking information will transpire or occur, or if any of them do so, what benefits will bederived there from. Except as required by law, Bonterra disclaims any intention or obligation to update or revise any forward-looking information, whether as aresult of new information, future events or otherwise.

The term barrels of oil equivalent (BOE) may be misleading, particularly if used in isolation. A BOE conversion ratio of six thousand cubic feet per barrel(6mcf/bbl) of natural gas to barrels of oil equivalence is based on an energy equivalency conversion method primarily applicable at the burner tip and does notrepresent a value equivalency at the wellhead. All BOE conversions in the report are derived from converting gas to oil in the ratio mix of six thousand cubic feetof gas to one barrel of oil.

The forward-looking information contained herein is expressly qualified by this cautionary statement.

3

Forward Looking Information

DRILLING LOCATIONS:

This presentation discloses drilling locations in three categories: (i) proved locations; (ii) probable locations; and (iii) unbooked locations. Proved locations andprobable locations, which are sometimes collectively referred to as “booked locations”, are derived from the Company’s most recent independent reserves evaluationas prepared by Sproule as of December 31, 2018 and account for drilling locations that have associated proved or probable reserves, as applicable.

Unbooked locations are internal estimates based on the Company’s prospective acreage and an assumption as to the number of wells that can be drilled per sectionbased on industry practice and internal review. Unbooked locations do not have attributed reserves or resources. Of the 700+ Net drilling locations identified herein,294 are net proved locations, 4 are net probable locations and 400+ are net unbooked locations. Unbooked locations have specifically been identified by managementas an estimation of our multi-year drilling activities based on evaluation of applicable geologic, seismic, and engineering, production and reserves data on prospectiveacreage and geologic formations. There is no certainty that we will drill all unbooked drilling locations and if drilled there is no certainty that such locations will resultin additional oil and gas reserves, resources or production. The locations that Bonterra drills will ultimately depend upon the availability of capital, regulatoryapprovals, seasonal restrictions, oil and natural gas prices, costs, actual drilling results and other factors. While certain of the unbooked drilling locations have beenderisked by drilling existing wells in relative close proximity to such unbooked drilling locations, the majority of other unbooked drilling locations are farther away fromexisting wells where management has less information about the characteristics of the reservoir and therefore there is more uncertainty whether wells will be drilledin such locations and if drilled there is more uncertainty that such wells will result in additional oil and gas reserves, resources or production.

4

Current Corporate Snapshot

(1)Based on Share Price of $3.50

Financial TSX: BNE

Common Shares Outstanding 33.3 million

Insider Ownership 25%

Current Monthly Dividend $0.01 per share

Current Annualized Yield (1) 3.4%

Tax Pools at Q3 2019 $359 million

Tax Horizon ~2020

Q3 2019 Exit Net Debt ~$308 million

Bank Line $325 million ($283 million drawn at Q3 2019 exit)

Operational

Average Production (Q3 2019) 12,136 boepd

2019 Production Guidance ~12,400 boepd

Oil and Liquids Weighting 69% (62% oil & 7% liquids)

Natural Gas Weighting 31%

Average Corporate Production Decline Rate ~20%

Reserve Life Index (PDP) 8 years

Reserve Life Index (1P) 17 years

Reserve Life Index (2P) 21 years

4

5

Consistent Strategy

DIVIDENDPlus

GROWTH

DEBT REPAYMENT

FREE CASH FLOW GENERATION

A proven track record built on generating long-term, sustainable value through a combination of growth plus

returning capital to shareholders via dividends

Excess free cash flow will be directed to reduce overall debt, and then assess increases to the

dividend or capital budget

Low corporate decline rate ensures minimal capital required to sustain

production, which supports maximizing free cash flow

Bonterra’s focus will remain on generating strong, sustainable free cash flow which can be used

to reduce debt, and as leverage is reduced look to increase the dividend

6

Bonterra: Focused on Fundamentals

Disciplined Oil Exposure

Low CostOperations

VALUE CREATION

Focus onBalance Sheet

Concentrated Asset Base

Significant Low Risk Drilling Inventory:

Established and Controlled Infrastructure:

~20% Corporate Decline

Free Cash Flow Generation

Bonterra’s proven track record has been built on a model of generating long-term, sustainable

value through a combination of returning capital to shareholders via dividends and modest growth

Light oil focused with Pembina & Willesden Green Areas representing ~97% of production

700+ net locations identified and 298 net locations booked (43%)(1)

Minimal facility capital required to scale up production; 92% of production is operated

Strategy underway to reduce debt to funds flow ratio through capital allocation,

dividend adjustment, cost control

leads to low maintenance

capex

(1)Please see disclaimers for drilling locations in forward looking statements.

7

Returning Capital to Shareholders

• Bonterra remains a yield company focused on per share value creationachieved by paying dividends and growing production, reserves and cash flow per share

• Financial flexibility allows Bonterrato adjust the dividend in responseto broader commodity pricefluctuations

• Focus on generating free cash flowthat can be allocated to debt repayment, growth capital orpotentially adjusting the dividend upward

• Relative to pure growth-oriented companies, Bonterra shareholders realize a return via monthly dividends, coupled with opportunities for corporate growth that can lead to multiple expansion

Yield + sustainability strategy affords flexibility to adapt to commodity price environment

while continuing to return capital to shareholders

$0

$20

$40

$60

$80

$100

$120

$140

$160

$-

$0.10

$0.20

$0.30

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

Jan

-08

Jan

-09

Jan

-10

Jan

-11

Jan

-12

Jan

-13

Jan

-14

Jan

-15

Jan

-16

Jan

-17

Jan

-18

Jan

-19

Dividend EDM Light Share Price

Edm

onto

n L

ight

($/b

bl) &

BN

E S

hare

Price ($

/share

)

Div

iden

d (

$/m

on

th)

8

Long-Term Development Opportunities

West Pembina

Willesden Green

Keystone

Rose Creek

Carnwood

BlueRapids

Cynthia

Concentrated assets in the Pembina & Willesden Green area support efficient operations and offer

exposure to significant upside through a large inventory of low-risk, highly economic undrilled locations

Pembina & Willesden Green Lands by the Numbers

473 grossSections of land (312 net) 92%

Operated Production

101.2 MBOEP+P Reserves

21 yearsReserve Life Index (P+P)

700+ netInternally identified multi-zone locations

298 netBooked locations

Ferrier

9

Pembina Cardium Overview

Original Oil in Place per Section Recovery Factor

5,000 to 10,000 Mbbl

10,000 to 20,000 Mbbl

20,000 to 25,000 Mbbl

0 to 5,000 Mbbl

25,000+ Mbbl

5%

10%

15%

0%

20%

25%

• Pembina is the largest conventional oilfield in Canada with large oil-in-place and low recovery to date, offering long-term stable production, high-quality oil and attractive netbacks

• Majority of Bonterra land covers areas with significant remaining original-oil-in-place

• Opportunity to increase recovery factors can contribute to sizable increases in reserves and production

10

Pembina Cardium Geology

Conglomerate

Sandstone

Sandstone

Bioturbated

Mudstone

Shale

Shale

• Interbedded sandstone and shale with local conglomerate and prevalent underlying low permeability bioturbated mudstone

• Depths range from 1,200 m TVD in NE Pembina to 2,000m TVD in SW Pembina

11

2019 Production Forecast – Q3 Update

~21% Corporate Decline Rate

Low decline rate means less capital is required to maintain production, contributing to free

cash flow growth over time

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

Jan-18 Apr-18 Jul-18 Oct-18 Jan-19 Apr-19 Jul-19 Oct-19 Jan-20

BO

E/d

Vertical Wells Horizontal Wells 2019 Capital Program

12

2019 Q3 Update

(1) Realized Oil Price calculated as follows: (WTI Oil Price – Differential) x FX rate – (Quality Adjustment) (2) Assumptions: Edmonton light differential: U$6.00; FX: 0.76 CAD/US; Quality adjustment C$3.25/bbl; BNE Realized Gas $2.00/mcf; BNE Realized Liquids: 40% of

realized oil(3) CAPEX decrease of MM$C 3 versus Q2 update results from delaying completions on 3 Net wells until January 2020

Bonterra will generate significant discretionary cash under the varying price forecasts and

exhibits great torque to improving commodity prices

Assumptions:

2019 WELLS DRILLED 30 Gross (23.7 Net) 2019 FORECASTED ANNUAL PRODUCTION 12,400 boe/d

OIL PRICE (WTI) USD/bbl $50.27 $54.07 $57.87 $61.67 $65.47

REALIZED OIL PRICE(1) CAD/bbl $55.00 $60.00 $65.00 $70.00 $75.00

FUNDS FLOW (2) MM$C 78 88 99 105 120

CAPEX MM$C 56 56 56 56 56

CASH FLOW MM$C 21 32 43 49 64

DIVIDEND MM$C 4 4 4 4 4

DISCRETIONARY CASH MM$C 17 28 39 45 60

YE2019 DEBT ESTIMATE MM$C 312 301 290 284 269

DEBT/FUNDS FLOW MM$C 4.01x 3.40x 2.92x 2.69x 2.25x

13

Average BNE Cardium Full Cycle Economics

WTI $USD/bbl $ 50.12 $ 53.85 $ 57.59 $ 61.32 $ 65.05

BNE Realized Price (1,2) $CAD/bbl $ 55.00 $ 60.00 $ 65.00 $ 70.00 $ 75.00 Full Cycle Capital (3) M$C $ 2,155 $ 2,265 $ 2,265 $ 2,265 $ 2,265

BT Payout Years 2.2 2.0 1.6 1.4 1.2 Rate of Return % 37% 42% 53% 66% 81% BT NPV10 M$C $ 939 $ 1,140 $ 1,432 $ 1,706 $ 1,971Capital Efficiency S/boepd $19,250 $20,210 $20,210 $20,210 $20,210 Recycle Ratio 1.9 2.0 2.2 2.4 2.4

(1) Realized Oil Price calculated as follows: (WTI Oil Price – Differential) x FX rate – (Quality Adjustment) (2) Assumptions: Edmonton light differential: U$6.62; FX: 0.747 CAD/US; Quality adjustment C$3.25/bbl; BNE Realized Gas $1.88/mcf; BNE Realized Liquids: 50% of realized oil(3) Drill, Complete, Equip, Tie-In, Facilities

0

50

100

150

200

250

300

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24

BO

E/D

Month

BNE Type Curve: Full Cycle Price and Capital Sensitivities

Reserves per well (MBOE) 165

IP (12 months) (boe/d) 112

Cardium wells are repeatable, predictable and generate strong returns even in a weak

commodity price environment

14

2015 2016 2017 2018

12,656 12,650

$20

$30

$40

$50

$60

$70

$80

$90

Cap

ital

Exp

end

itu

res

($m

m)

Capital Expenditures ($mm)

Annual Production

Annual Production (BOE per day)

Successfully maintaining production levels through a challenging commodity price environment

12,82713,206

OIL & NGL GAS

Consistent and conservative production management delivers predictable returns across

changing commodity prices and preserves long-term shareholder value

15

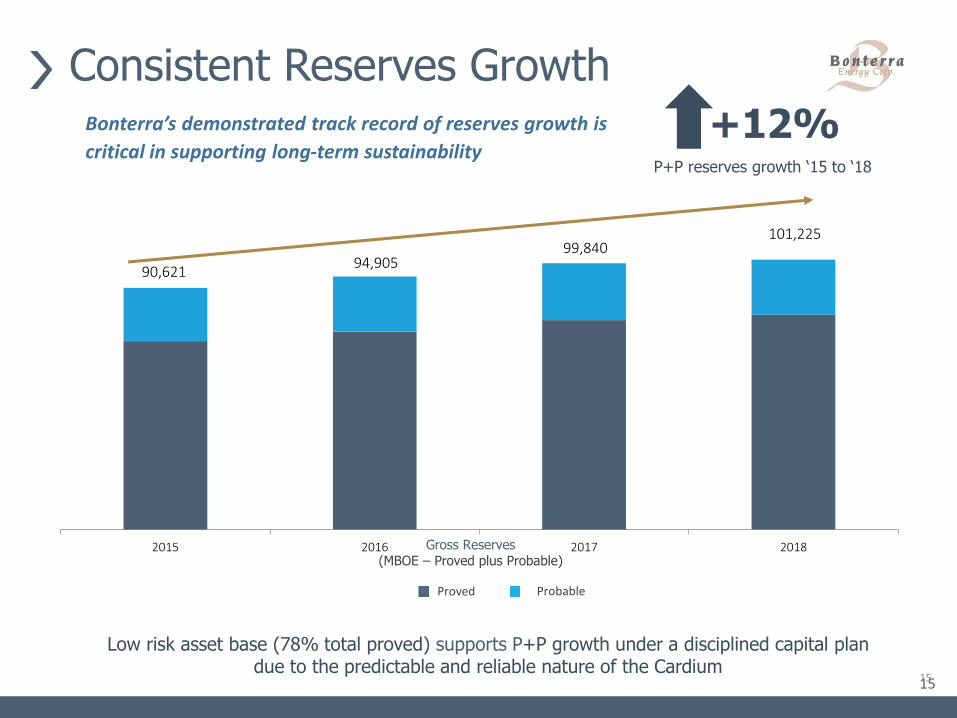

Consistent Reserves Growth

Low risk asset base (78% total proved) supports P+P growth under a disciplined capital plan due to the predictable and reliable nature of the Cardium

15

Gross Reserves(MBOE – Proved plus Probable)

+12%P+P reserves growth ‘15 to ‘18

Proved Probable

90,62194,905

99,840101,225

2015 2016 2017 2018

Bonterra’s demonstrated track record of reserves growth is

critical in supporting long-term sustainability

16

Building per Share Value

Production per Share(BOE per share)

Reserves per Share(BOE per share) (P+P)

Continuous value creation on a per share basis from 2015 to 2018

4%Production per share Reserves per share

9%

2.7

8

2.8

5

3.0

0

3.0

4

2015 2016 2017 2018

0.1

39

0.1

40

0.1

41

0.1

45

0.100

0.105

0.110

0.115

0.120

0.125

0.130

0.135

0.140

0.145

0.150

2015 2016 2017 2018

17

Investment Summary: Why Bonterra?Oil weighted producer offering yield and exposure to oil price upside through operational

excellence and conservative financial management

Insiders own ~25%

Industry low ~20% decline

$1.1B has been returned to shareholders in dividends since 1998

Low-risk asset base with 78% 1P reserves

Experienced & Aligned

Management

Low Corporate

Decline Rate

Yield

Low-Risk Drilling

Inventory

Shareholder Value

Creation

18

Appendix

19

Cash Flow Sensitivities

Sensitivity Analysis(1)

(estimate for 2019) Cash FlowCash Flow

Per Share(2)

Change of Canadian $1.00 per barrel of oil and NGLs $2,843,000 $0.09

Change of Canadian $0.10 per MCF of natural gas $1,007,000 $0.03

Change of Canadian $0.01 / U.S.$ exchange rate $1,507,000 $0.05

Per Annum

(1) This analysis uses current royalty rates, annualized estimated average production of 12,600 BOE per day and no changes in working capital(2) Based on annualized basic weighted average shares outstanding of 33,388,796

20

Corporate Information

DIRECTORSG. F. Fink G. J. DrummondR. M. JarockR. A. TourignyA. M. WalshD. Reuter

Bonterra Energy Corp.

Suite 901, 1015 – 4th St SW

Calgary, AB T2R 1J4

Phone: 403.262.5307

HEAD OFFICE

OFFICERSG. F. Fink

CEO & Chairman of the Board

R. D. ThompsonCFO & Corporate Secretary

A. Neumann Chief Operating Officer

B. A. CurtisSenior VP, Business Development

STOCK EXCHANGE LISTINGTSX: BNE

LEGAL COUNSELBorden Ladner Gervais LLP

BANKSCIBC

National Bank of Canada

The Toronto Dominion Bank

Alberta Treasury Branches

Business Development Bank of Canada

REGISTRAR & TRANSFER AGENTOdyssey Trust Company of Canada

AUDITORSDeloitte LLP

INDEPENDENT RESERVE ENGINEERSproule Associates Limited