copyright © 2007 by the mcgraw-hill companies, inc. all rights reserved. reporting and interpreting...

TRANSCRIPT

Copyright © 2007 by The McGraw-Hill Companies, Inc. All rights reserved.

Reporting and Interpreting

Bonds

Chapter 10

10-2

Understanding the Business

The mixture of debt and equity used to finance a company’s operations is called the capital

structure:

Debt - funds from creditors

Equity - funds from owners

10-3

Significant debt needs of a company are often filled

by issuing bonds.

Significant debt needs of a company are often filled

by issuing bonds.

Understanding the Business:Capital Structure - Bonds

Bonds Cash

10-4

Understanding the Business

As liquidity increases . . .

. . . cost of borrowing decreases.

Bonds can be Bonds can be traded on traded on

established established exchanges that exchanges that provide liquidity provide liquidity to bondholders.to bondholders.

Bonds can be Bonds can be traded on traded on

established established exchanges that exchanges that provide liquidity provide liquidity to bondholders.to bondholders.

10-5

Characteristics of Bonds Payable

Advantages of bonds: Stockholders maintain control

because bonds are debt, not equity.

Interest expense is tax deductible.

The impact on earnings is positive because money can often be borrowed at a low interest rate and invested at a higher interest rate.

Advantages of bonds: Stockholders maintain control

because bonds are debt, not equity.

Interest expense is tax deductible.

The impact on earnings is positive because money can often be borrowed at a low interest rate and invested at a higher interest rate.

10-6

Characteristics of Bonds Payable

Disadvantages of bonds: Risk of bankruptcy exists

because the interest and debt must be paid back as scheduled or creditors will force legal action.

Negative impact on cash flows exists because interest and principal must be repaid in the future.

Disadvantages of bonds: Risk of bankruptcy exists

because the interest and debt must be paid back as scheduled or creditors will force legal action.

Negative impact on cash flows exists because interest and principal must be repaid in the future.

10-7

Characteristics of Bonds Payable

$ Bond Issue Price $

Bond Certificate

At Bond Issuance Date

Bonds payable are long-term debt for the issuing company.

Company Issuing Bonds

Company Issuing Bonds

Investor Buying Bonds

Investor Buying Bonds

10-8

Characteristics of Bonds Payable

PeriodicInterest Payments$ $

Principal Payment at End of

Bond Term$ $

Company Issuing Bonds

Company Issuing Bonds

Investor Buying Bonds

Investor Buying Bonds

10-9

1. Face Value (Maturity or Par Value, Principal)2. Maturity Date3. Stated Interest Rate 4. Interest Payment Dates5. Bond Date

Characteristics of Bonds Payable

Other Factors:6. Market Interest Rate7. Issue Date

BOND PAYABLE

Face Value $1,000 Interest 10%

6/30 & 12/31

Maturity Date 1/1/16Bond Date 1/1/06

10-10

Bond Classifications

Debenture bondsDebenture bonds Not secured with the pledge of a specific asset.

Callable bondsCallable bonds May be retired and repaid (called) at any time at

the option of the issuer.

Convertible bondsConvertible bonds May be exchanged for other securities of the

issuer (usually shares of common stock) at the option of the bondholder.

Debenture bondsDebenture bonds Not secured with the pledge of a specific asset.

Callable bondsCallable bonds May be retired and repaid (called) at any time at

the option of the issuer.

Convertible bondsConvertible bonds May be exchanged for other securities of the

issuer (usually shares of common stock) at the option of the bondholder.

An indenture is a bond contract that specifies the legal provisions of a

bond issue.

10-11

Characteristics of Bonds Payable

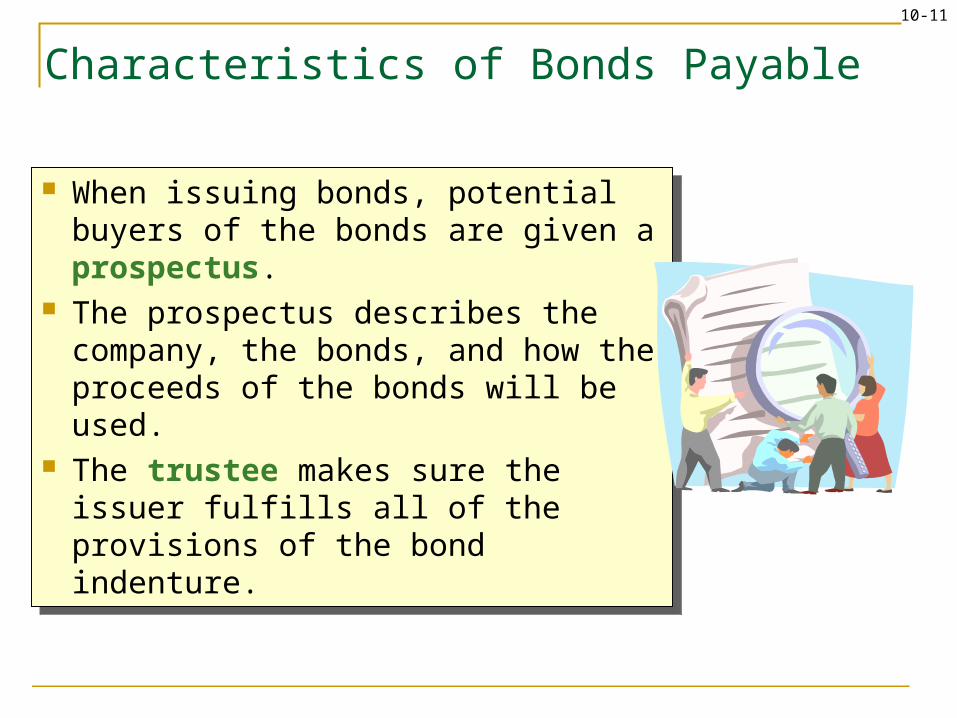

When issuing bonds, potential buyers of the bonds are given a prospectus.

The prospectus describes the company, the bonds, and how the proceeds of the bonds will be used.

The trustee makes sure the issuer fulfills all of the provisions of the bond indenture.

When issuing bonds, potential buyers of the bonds are given a prospectus.

The prospectus describes the company, the bonds, and how the proceeds of the bonds will be used.

The trustee makes sure the issuer fulfills all of the provisions of the bond indenture.

10-12

Reporting Bond Transactions

When a company issues bonds, it specifies two When a company issues bonds, it specifies two cash flows related to the transaction: cash flows related to the transaction:

PrincipalPrincipalInterestInterest

When a company issues bonds, it specifies two When a company issues bonds, it specifies two cash flows related to the transaction: cash flows related to the transaction:

PrincipalPrincipalInterestInterest

Assume Dino Oil issues $100,000 in bonds at par on January Assume Dino Oil issues $100,000 in bonds at par on January 1, 2006. The bonds pay 8% interest annually on December 31. 1, 2006. The bonds pay 8% interest annually on December 31.

What journal entry should be made on January 1, 2006?What journal entry should be made on January 1, 2006?

10-13

Reporting Bond Transactions

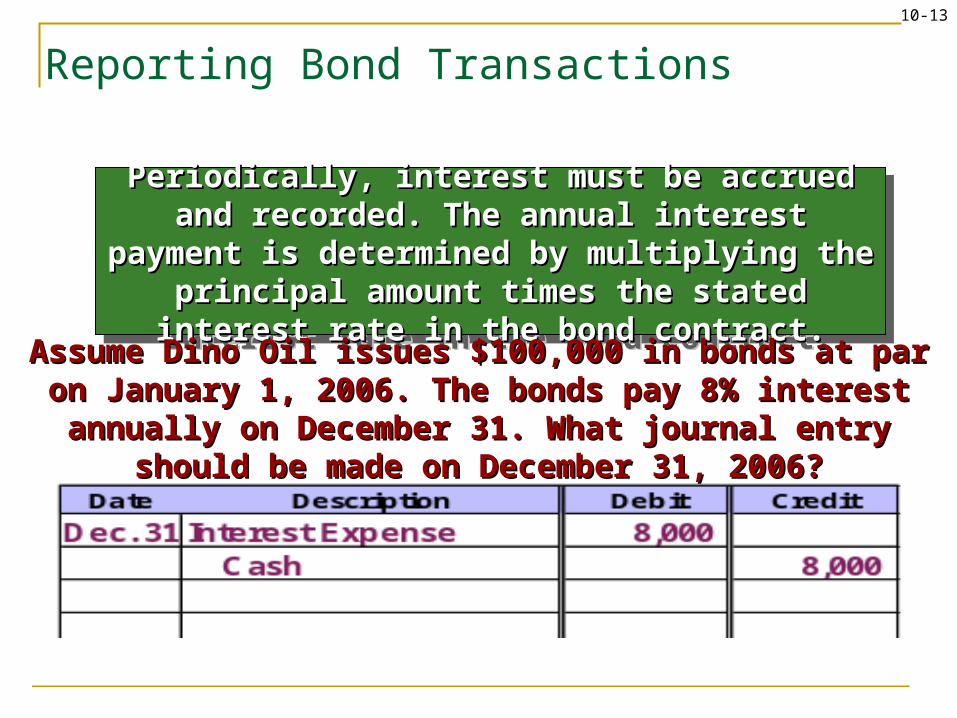

Periodically, interest must be accrued and Periodically, interest must be accrued and recorded. The annual interest payment is recorded. The annual interest payment is

determined by multiplying the principal amount determined by multiplying the principal amount times the stated interest rate in the bond contract.times the stated interest rate in the bond contract.

Periodically, interest must be accrued and Periodically, interest must be accrued and recorded. The annual interest payment is recorded. The annual interest payment is

determined by multiplying the principal amount determined by multiplying the principal amount times the stated interest rate in the bond contract.times the stated interest rate in the bond contract.

Assume Dino Oil issues $100,000 in bonds at par on January Assume Dino Oil issues $100,000 in bonds at par on January 1, 2006. The bonds pay 8% interest annually on December 31. 1, 2006. The bonds pay 8% interest annually on December 31.

What journal entry should be made on December 31, 2006?What journal entry should be made on December 31, 2006?

10-14

Reporting Bond Transactions

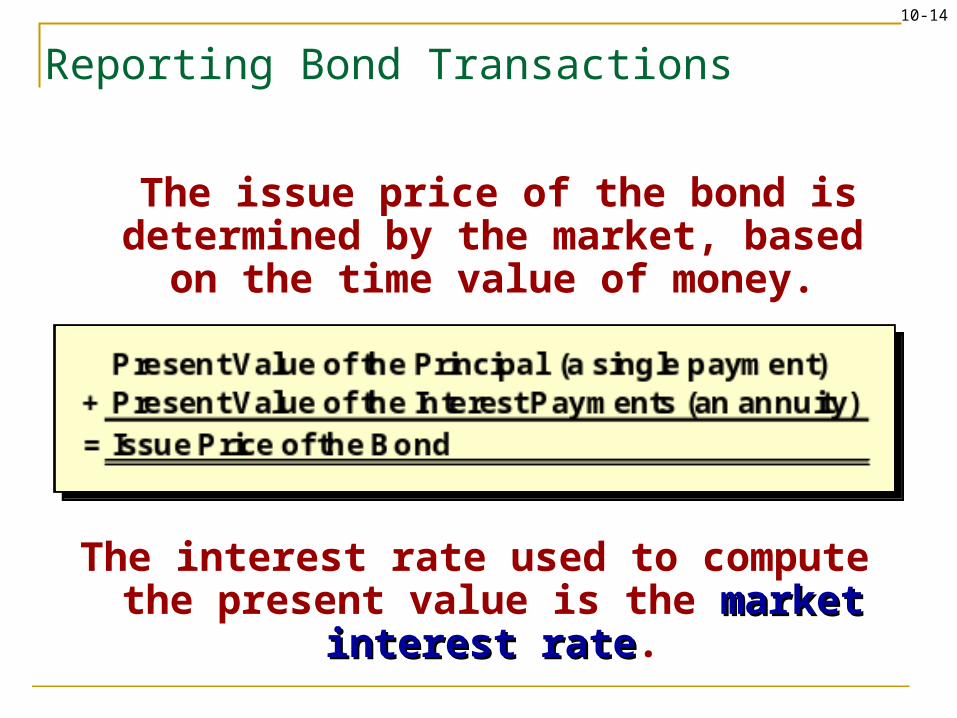

The issue price of the bond is determined by the market, based on the time value of

money.

The interest rate used to compute the present value is the market interest ratemarket interest rate.

10-15

Reporting Bond Transactions

=

<

>

=

<

>

10-16

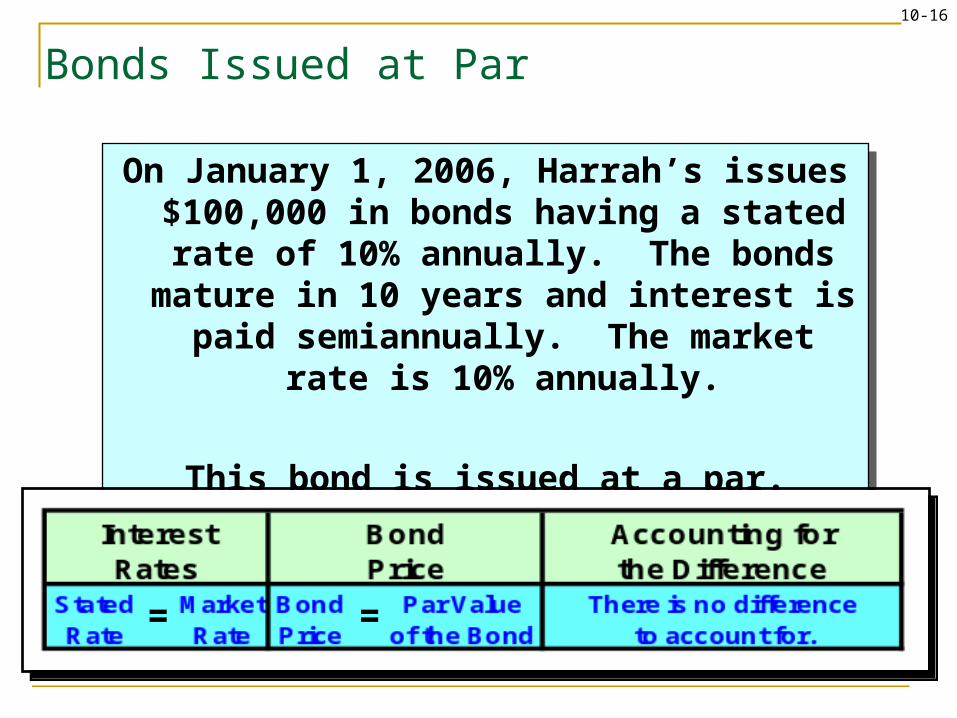

Bonds Issued at Par

On January 1, 2006, Harrah’s issues $100,000 in bonds having a stated rate of

10% annually. The bonds mature in 10 years and interest is paid semiannually.

The market rate is 10% annually.

This bond is issued at a par.

On January 1, 2006, Harrah’s issues $100,000 in bonds having a stated rate of

10% annually. The bonds mature in 10 years and interest is paid semiannually.

The market rate is 10% annually.

This bond is issued at a par.

= =

10-17

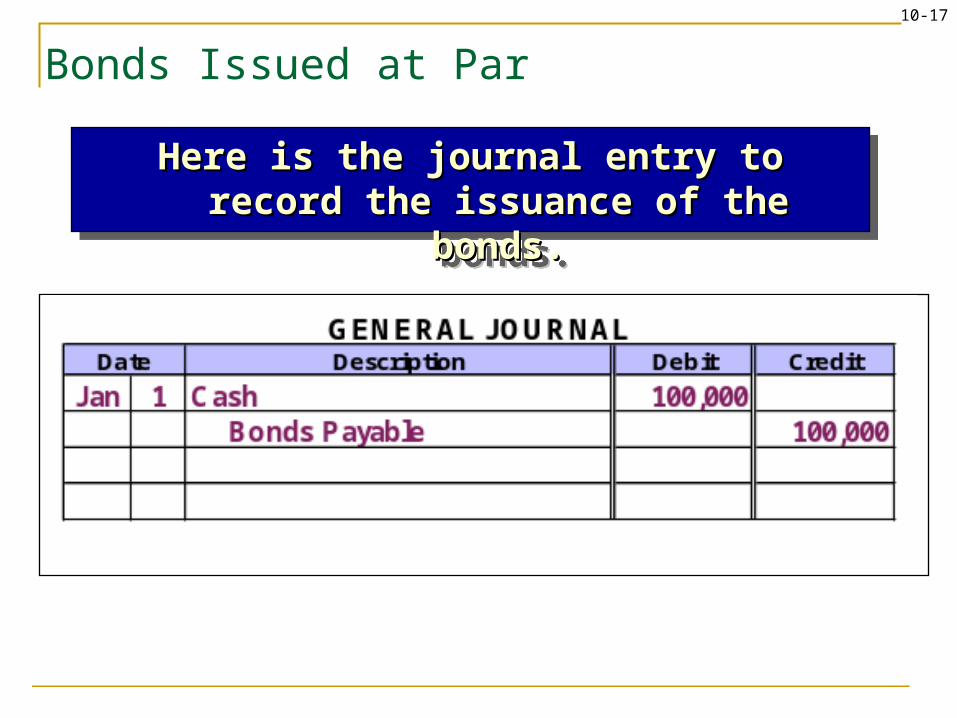

Bonds Issued at Par

Here is the journal entry to record the Here is the journal entry to record the issuance of the bonds.issuance of the bonds.

Here is the journal entry to record the Here is the journal entry to record the issuance of the bonds.issuance of the bonds.

10-18

Bonds Issued at Par

Here is the entry made every six months to Here is the entry made every six months to record the interest payment.record the interest payment.

Here is the entry made every six months to Here is the entry made every six months to record the interest payment.record the interest payment.

10-19

Bonds Issued at Par

Here is the entry to record the maturity of Here is the entry to record the maturity of the bonds.the bonds.

Here is the entry to record the maturity of Here is the entry to record the maturity of the bonds.the bonds.

10-20

Bonds Issued at Discount

On January 1, 2006, Harrah’s issues $100,000 in bonds having a stated rate of

10% annually. The bonds mature in 10 years (Dec. 31, 2015) and interest is paid

semiannually. The market rate is 12% annually.

This bond is issued at a discount.

On January 1, 2006, Harrah’s issues $100,000 in bonds having a stated rate of

10% annually. The bonds mature in 10 years (Dec. 31, 2015) and interest is paid

semiannually. The market rate is 12% annually.

This bond is issued at a discount.

< <

10-21

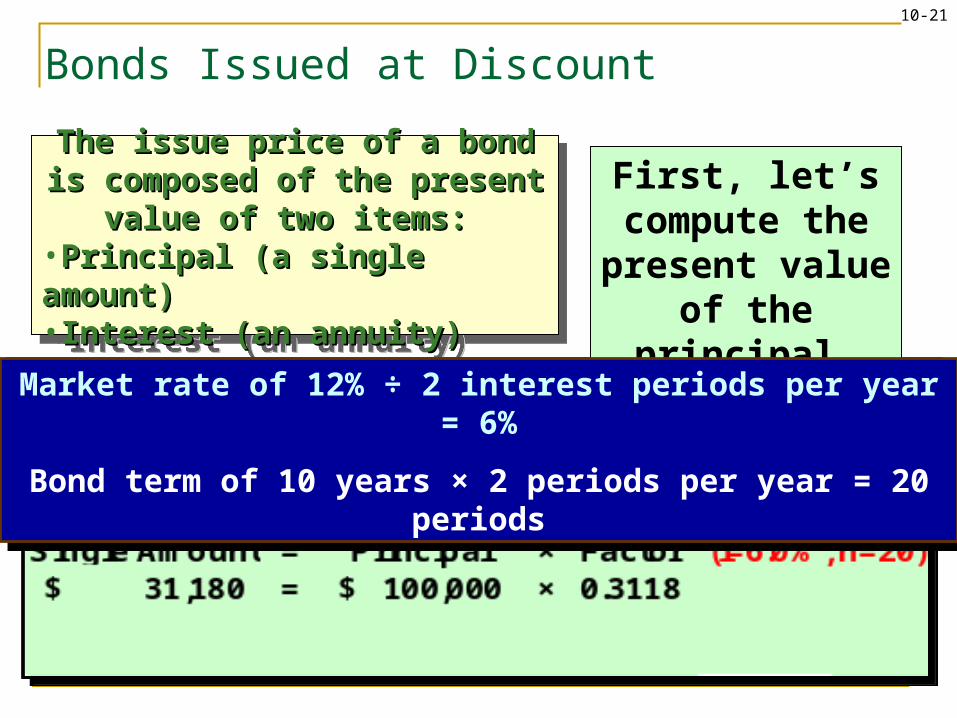

Bonds Issued at Discount

Use the present value of a single amount table to find the appropriate factor.

Use the present value of a single amount table to find the appropriate factor.

The issue price of a bond is The issue price of a bond is composed of the present value composed of the present value

of two items: of two items: •Principal (a single amount)Principal (a single amount)•Interest (an annuity)Interest (an annuity)

The issue price of a bond is The issue price of a bond is composed of the present value composed of the present value

of two items: of two items: •Principal (a single amount)Principal (a single amount)•Interest (an annuity)Interest (an annuity)

First, let’s compute the

present value of the principal.

Market rate of 12% ÷ 2 interest periods per year = 6%

Bond term of 10 years × 2 periods per year = 20 periods

Market rate of 12% ÷ 2 interest periods per year = 6%

Bond term of 10 years × 2 periods per year = 20 periods

10-22

Use the present value of an annuity table to find the appropriate factor.

Use the present value of an annuity table to find the appropriate factor.

Bonds Issued at Discount

The issue price of a bond is The issue price of a bond is composed of the present value composed of the present value

of two items: of two items: •Principal (a single amount)Principal (a single amount)•Interest (an annuity)Interest (an annuity)

The issue price of a bond is The issue price of a bond is composed of the present value composed of the present value

of two items: of two items: •Principal (a single amount)Principal (a single amount)•Interest (an annuity)Interest (an annuity)

Now, let’s compute the

present value of the interest.

Market rate of 12% ÷ 2 interest periods per year = 6%

Bond term of 10 years × 2 periods per year = 20 periods

Market rate of 12% ÷ 2 interest periods per year = 6%

Bond term of 10 years × 2 periods per year = 20 periods

10-23

Bonds Issued at Discount

31,180$ Present Value of the Principal

+ 57,350 Present Value of the Interest

= 88,530$ Present Value of the Bonds

31,180$ Present Value of the Principal

+ 57,350 Present Value of the Interest

= 88,530$ Present Value of the Bonds

The issue price of a bond is The issue price of a bond is composed of the present value composed of the present value

of two items: of two items: •Principal (a single amount)Principal (a single amount)•Interest (an annuity)Interest (an annuity)

The issue price of a bond is The issue price of a bond is composed of the present value composed of the present value

of two items: of two items: •Principal (a single amount)Principal (a single amount)•Interest (an annuity)Interest (an annuity)

Finally, we can determine the issue price of

the bond.

The $88,530 is less than the face amount of $100,000, so the bonds are issued at a discount of

$11,470.

The $88,530 is less than the face amount of $100,000, so the bonds are issued at a discount of

$11,470.

10-24

Bonds Issued at Discount

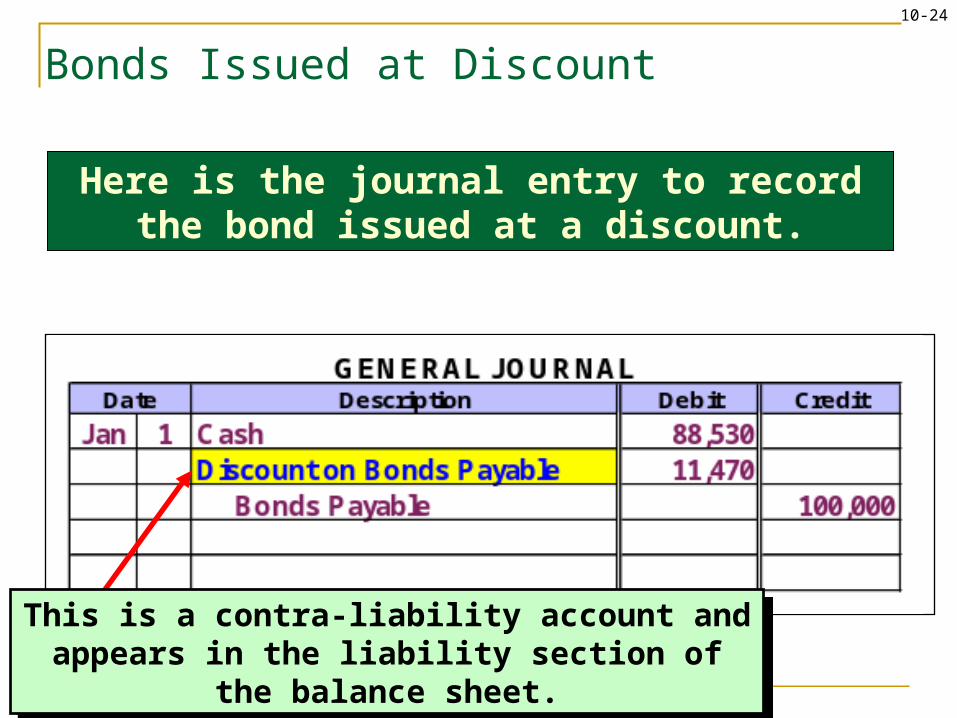

This is a contra-liability account and appears in the liability section of the balance sheet.

This is a contra-liability account and appears in the liability section of the balance sheet.

Here is the journal entry to record the bond issued at a discount.

10-25

Bonds Issued at DiscountThe discount The discount

will be will be amortizedamortized

over the 10-over the 10-year life of the year life of the

bonds.bonds.Two methods Two methods

of amortization of amortization are commonly are commonly

used:used:

Straight-lineStraight-line

Effective-Effective-interest.interest.

10-26

Reporting Interest Expense: Straight-line Amortization

Identify the amount of the Identify the amount of the bond discount.bond discount.

Divide the bond discount by Divide the bond discount by the number of interest the number of interest periods.periods.

Include the discount Include the discount amortization amount as part amortization amount as part of the periodic interest of the periodic interest expense entry.expense entry.The discount will be reduced The discount will be reduced

to zero by the maturity date.to zero by the maturity date.

Identify the amount of the Identify the amount of the bond discount.bond discount.

Divide the bond discount by Divide the bond discount by the number of interest the number of interest periods.periods.

Include the discount Include the discount amortization amount as part amortization amount as part of the periodic interest of the periodic interest expense entry.expense entry.The discount will be reduced The discount will be reduced

to zero by the maturity date.to zero by the maturity date.

10-27

Reporting Interest Expense: Straight-line Amortization

Harrah’s issued their bonds on Jan. 1, 2006. The Harrah’s issued their bonds on Jan. 1, 2006. The discount was $11,470. The bonds have a 10-year discount was $11,470. The bonds have a 10-year maturity and $5,000 interest is paid semiannually.maturity and $5,000 interest is paid semiannually.

Compute the periodic discount amortization Compute the periodic discount amortization using the straight-line method. using the straight-line method.

Harrah’s issued their bonds on Jan. 1, 2006. The Harrah’s issued their bonds on Jan. 1, 2006. The discount was $11,470. The bonds have a 10-year discount was $11,470. The bonds have a 10-year maturity and $5,000 interest is paid semiannually.maturity and $5,000 interest is paid semiannually.

Compute the periodic discount amortization Compute the periodic discount amortization using the straight-line method. using the straight-line method.

10-28

Reporting Interest Expense: Straight-line Amortization

Here is the journal entry to record the payment Here is the journal entry to record the payment of interest and the discount amortization for of interest and the discount amortization for

the six months ending on June 30, 2006.the six months ending on June 30, 2006.

Here is the journal entry to record the payment Here is the journal entry to record the payment of interest and the discount amortization for of interest and the discount amortization for

the six months ending on June 30, 2006.the six months ending on June 30, 2006.

10-29

Reporting Interest Expense: Straight-line Amortization

As the discount is

amortized, the carrying

amount of the bonds

increases.

10-30

Straight-Line Amortization TableInterest Interest Discount Unamortized Book

Date Payment Expense* Amortization* Discount Value1/1/2006 11,470$ 88,530$

6/30/2006 5,000$ 5,574$ 574$ 10,897 89,104 12/31/2006 5,000 5,574 574 10,323 89,677 6/30/2007 5,000 5,574 574 9,750 90,251

12/31/2007 5,000 5,574 574 9,176 90,824 6/30/2008 5,000 5,574 574 8,603 91,398

12/31/2008 5,000 5,574 574 8,029 91,971

6/30/2015 5,000 5,574 574 574 99,426 12/31/2015 5,000 5,574 574 0 100,000

100,000$ 111,470$ 11,470$ * Rounded.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

10-31

Reporting Interest Expense: Effective-interest Amortization

The effective interest method The effective interest method is the theoretically preferred is the theoretically preferred method.method.

Compute interest expense by Compute interest expense by multiplying the current unpaid multiplying the current unpaid balance times the market rate balance times the market rate of interest.of interest.

The discount amortization is The discount amortization is the difference between the difference between interest expense and the cash interest expense and the cash paid (or accrued) for interest. paid (or accrued) for interest.

The effective interest method The effective interest method is the theoretically preferred is the theoretically preferred method.method.

Compute interest expense by Compute interest expense by multiplying the current unpaid multiplying the current unpaid balance times the market rate balance times the market rate of interest.of interest.

The discount amortization is The discount amortization is the difference between the difference between interest expense and the cash interest expense and the cash paid (or accrued) for interest. paid (or accrued) for interest.

10-32

Reporting Interest Expense: Effective-interest Amortization

Harrah’s issued their bonds on Jan. 1, 2006. The Harrah’s issued their bonds on Jan. 1, 2006. The issue price was $88,530. The bonds have a 10-issue price was $88,530. The bonds have a 10-

year maturity and $5,000 interest is paid year maturity and $5,000 interest is paid semiannually.semiannually.

Compute the periodic discount amortization Compute the periodic discount amortization using the effective interest method. using the effective interest method.

Harrah’s issued their bonds on Jan. 1, 2006. The Harrah’s issued their bonds on Jan. 1, 2006. The issue price was $88,530. The bonds have a 10-issue price was $88,530. The bonds have a 10-

year maturity and $5,000 interest is paid year maturity and $5,000 interest is paid semiannually.semiannually.

Compute the periodic discount amortization Compute the periodic discount amortization using the effective interest method. using the effective interest method.

Unpaid Balance × Effective Interest Rate × n/12

$88,530 × 12% × 1/2 = $5,312

Unpaid Balance × Effective Interest Rate × n/12

$88,530 × 12% × 1/2 = $5,312

10-33

Reporting Interest Expense: Effective-interest Amortization

Here is the journal entry to record the payment Here is the journal entry to record the payment of interest and the discount amortization for of interest and the discount amortization for

the six months ending on June 30, 2006.the six months ending on June 30, 2006.

Here is the journal entry to record the payment Here is the journal entry to record the payment of interest and the discount amortization for of interest and the discount amortization for

the six months ending on June 30, 2006.the six months ending on June 30, 2006.

10-34

Reporting Interest Expense: Effective-interest Amortization

As the discount is

amortized, the carrying

amount of the bonds

increases.

10-35

Effective-Interest Amortization TableInterest Interest Discount Unamortized Book

Date Payment Expense* Amortization* Discount* Value1/1/2006 11,470$ 88,530$

6/30/2006 5,000$ 5,312$ 312$ 11,158 88,842 12/31/2006 5,000 5,331 331 10,828 89,172 6/30/2007 5,000 5,350 350 10,477 89,523

12/31/2007 5,000 5,371 371 10,106 89,894 6/30/2008 5,000 5,394 394 9,712 90,288

12/31/2008 5,000 5,417 417 9,295 90,705

6/30/2015 5,000 5,890 890 944 99,056 12/31/2015 5,000 5,943 943 0 100,000

100,000$ 111,470$ 11,470$ * Rounded.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

10-36

Zero Coupon Bonds

Zero coupon bonds do not pay periodic interest.

Because there is no interest annuity . . .

This is called a deep discount deep discount bondbond.

PV of the Principal = Issue Price of the BondsPV of the Principal = Issue Price of the Bonds

10-37

Bonds Issued at Premium

On January 1, 2006, Harrah’s issues $100,000 in bonds having a stated rate of

10% annually. The bonds mature in 10 years (Dec. 31, 2015) and interest is paid

semiannually. The market rate is 8% annually.

This bond is issued at a premium.

On January 1, 2006, Harrah’s issues $100,000 in bonds having a stated rate of

10% annually. The bonds mature in 10 years (Dec. 31, 2015) and interest is paid

semiannually. The market rate is 8% annually.

This bond is issued at a premium.

> >

10-38

Bonds Issued at Premium

Use the present value of a single amount table to find the appropriate factor.

Use the present value of a single amount table to find the appropriate factor.

The issue price of a bond is The issue price of a bond is composed of the present value composed of the present value

of two items: of two items: •Principal (a single amount)Principal (a single amount)•Interest (an annuity)Interest (an annuity)

The issue price of a bond is The issue price of a bond is composed of the present value composed of the present value

of two items: of two items: •Principal (a single amount)Principal (a single amount)•Interest (an annuity)Interest (an annuity)

First, let’s compute the

present value of the principal.

Market rate of 8% ÷ 2 interest periods per year = 4%

Bond term of 10 years × 2 periods per year = 20 periods

Market rate of 8% ÷ 2 interest periods per year = 4%

Bond term of 10 years × 2 periods per year = 20 periods

10-39

Use the present value of an annuity table to find the appropriate factor.

Use the present value of an annuity table to find the appropriate factor.

Bonds Issued at Premium

The issue price of a bond is The issue price of a bond is composed of the present value composed of the present value

of two items: of two items: •Principal (a single amount)Principal (a single amount)•Interest (an annuity)Interest (an annuity)

The issue price of a bond is The issue price of a bond is composed of the present value composed of the present value

of two items: of two items: •Principal (a single amount)Principal (a single amount)•Interest (an annuity)Interest (an annuity)

Now, let’s compute the

present value of the interest.

Market rate of 8% ÷ 2 interest periods per year = 4%

Bond term of 10 years × 2 periods per year = 20 periods

Market rate of 8% ÷ 2 interest periods per year = 4%

Bond term of 10 years × 2 periods per year = 20 periods

10-40

Bonds Issued at Premium

45,640$ Present Value of the Principal

+ 67,952 Present Value of the Interest

= 113,592$ Present Value of the Bonds

45,640$ Present Value of the Principal

+ 67,952 Present Value of the Interest

= 113,592$ Present Value of the Bonds

The issue price of a bond is The issue price of a bond is composed of the present value composed of the present value

of two items: of two items: •Principal (a single amount)Principal (a single amount)•Interest (an annuity)Interest (an annuity)

The issue price of a bond is The issue price of a bond is composed of the present value composed of the present value

of two items: of two items: •Principal (a single amount)Principal (a single amount)•Interest (an annuity)Interest (an annuity)

Finally, we can determine the issue price of

the bond.

The $113,592 is greater than the face amount of $100,000, so the bonds are issued at a premium of

$13,592.

The $113,592 is greater than the face amount of $100,000, so the bonds are issued at a premium of

$13,592.

10-41

Bonds Issued at Premium

This is an adjunct-liability account and appears in the liability section of the balance sheet.

This is an adjunct-liability account and appears in the liability section of the balance sheet.

Here is the journal entry to record the bond issued at a premium.

10-42

Bonds Issued at PremiumThe premium The premium

will be will be amortizedamortized

over the 10-over the 10-year life of the year life of the

bonds.bonds.Let’s look at Let’s look at

the the amortization amortization tables usingtables usingStraight-lineStraight-line

andandEffective-Effective-interest.interest.

10-43

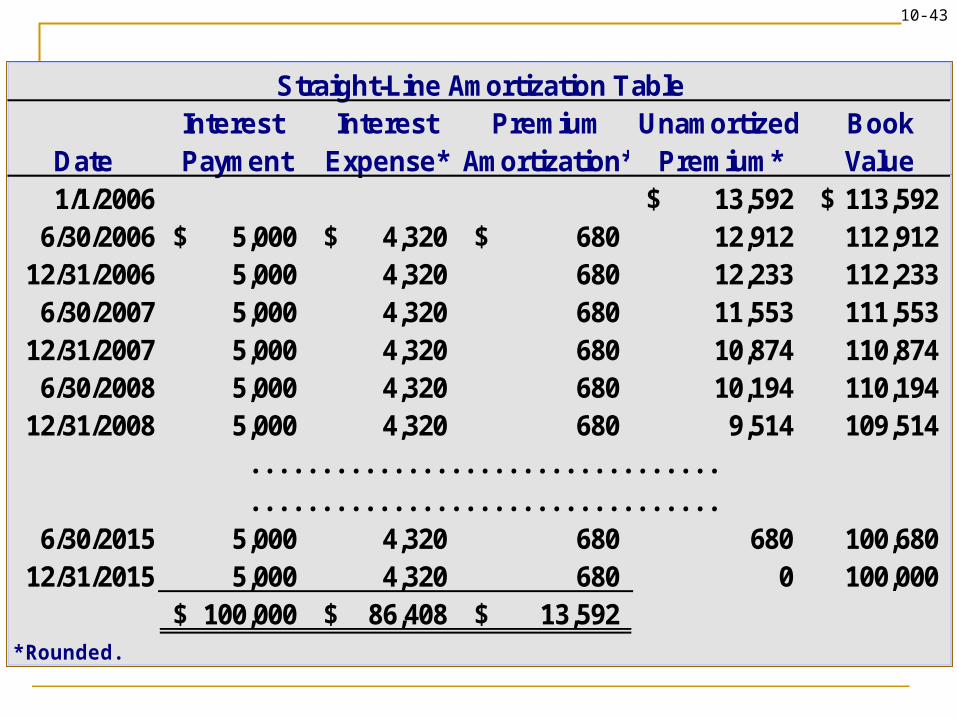

Straight-Line Amortization TableInterest Interest Premium Unamortized Book

Date Payment Expense* Amortization* Premium* Value1/1/2006 13,592$ 113,592$

6/30/2006 5,000$ 4,320$ 680$ 12,912 112,912 12/31/2006 5,000 4,320 680 12,233 112,233 6/30/2007 5,000 4,320 680 11,553 111,553

12/31/2007 5,000 4,320 680 10,874 110,874 6/30/2008 5,000 4,320 680 10,194 110,194

12/31/2008 5,000 4,320 680 9,514 109,514

6/30/2015 5,000 4,320 680 680 100,680 12/31/2015 5,000 4,320 680 0 100,000

100,000$ 86,408$ 13,592$ * Rounded.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

10-44

Reporting Interest Expense: Straight-line Amortization

Here is the journal entry to record the payment Here is the journal entry to record the payment of interest and the premium amortization for of interest and the premium amortization for

the six months ending on June 30, 2006.the six months ending on June 30, 2006.

Here is the journal entry to record the payment Here is the journal entry to record the payment of interest and the premium amortization for of interest and the premium amortization for

the six months ending on June 30, 2006.the six months ending on June 30, 2006.

10-45

Effective-Interest Amortization TableInterest Interest Premium Unamortized Book

Date Payment Expense* Amortization* Premium* Value1/1/2006 13,592$ 113,592$

6/30/2006 5,000$ 4,544$ 456$ 13,136 113,136 12/31/2006 5,000 4,525 475 12,661 112,661 6/30/2007 5,000 4,506 494 12,168 112,168

12/31/2007 5,000 4,487 513 11,654 111,654 6/30/2008 5,000 4,466 534 11,120 111,120

12/31/2008 5,000 4,445 555 10,565 110,565

6/30/2015 5,000 4,076 924 965 100,965 12/31/2015 5,000 4,039 965 0 100,000

100,000$ 86,408$ 13,592$ * Rounded.

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

*

10-46

Reporting Interest Expense: Effective-interest Amortization

Here is the journal entry to record the payment Here is the journal entry to record the payment of interest and the premium amortization for of interest and the premium amortization for

the six months ending on June 30, 2006.the six months ending on June 30, 2006.

Here is the journal entry to record the payment Here is the journal entry to record the payment of interest and the premium amortization for of interest and the premium amortization for

the six months ending on June 30, 2006.the six months ending on June 30, 2006.

10-47

Early Retirement of Debt

Occasionally, the issuing Occasionally, the issuing company will call (repay company will call (repay early) some or all of its early) some or all of its bonds.bonds.

Gains/losses are Gains/losses are calculated by comparing calculated by comparing the bond call amount the bond call amount with the book value of the with the book value of the bond.bond.

Occasionally, the issuing Occasionally, the issuing company will call (repay company will call (repay early) some or all of its early) some or all of its bonds.bonds.

Gains/losses are Gains/losses are calculated by comparing calculated by comparing the bond call amount the bond call amount with the book value of the with the book value of the bond.bond.

Book Value > Retirement Price = GainBook Value < Retirement Price = Loss