copyright © 2006 global insight, inc. outlook and risks for the u.s. and global economies nariman...

TRANSCRIPT

Copyright © 2006 Global Insight, Inc.

Outlook and Risks for

The U.S. and Global Economies

Nariman Behravesh

Chief Economist

Canadian Teleconference

March 14, 2006

Copyright © 2006 Global Insight, Inc. 2 03/2006

Outline of the Presentation

Storm CloudsHigh Oil PricesHousing BubblesGrowth and Policy ImbalancesSavings “Glut”/ Investment “Dearth”

Global OutlookRelatively Clear Sailing for Another Year or Two,

Despite Serious Structural Problems

What Would It Take to Trigger a Recession?

Copyright © 2006 Global Insight, Inc.

Storm Clouds

Copyright © 2006 Global Insight, Inc. 4 03/2006

Why Oil Prices Will Stay High in the Near-Term ...But Are Not A Problem

Oil Prices Will Stay High in the Near-Term Because of Robust energy demand growth Relatively modest investment in exploration and drilling High vulnerability to (and fears of) supply disruptions No shortage of potential risks (rebel activity in Nigeria, sabotage in Iraq, nuclear

standoff with Iran) So, the risks are overwhelmingly on the upside for oil prices

Why Near-Record High Energy Prices Are Not a Problem—Yet High prices are demand driven, and growth momentum is strong Petro dollars quickly recycled through investments and financial flows Zero inflationary pressures thanks to increased global competition Prudent monetary policies induce stable inflation expectations Higher energy efficiency in most industrial economies Energy subsidies in emerging markets cushions higher costs Inflation-adjusted prices are still below their early 1980s peaks

Copyright © 2006 Global Insight, Inc. 5 03/2006

(U.S. dollar per barrel, WTI)

Oil Prices Have Tripled Since 2002…

15

30

45

60

75

2002 2003 2004 2005 2006 2007

Oil Prices

Copyright © 2006 Global Insight, Inc. 6 03/2006

In the Longer Term, the Risks for Oil Prices Are Mostly on the Downside

The longer oil prices stay high, the greater the likelihood of a crash

Oil is behaving like any other commodity

In the long run, current constraints on oil markets will not be binding (e.g. OPEC’s cartel power) — technology always comes to the rescue

Supply and demand responses to high prices are always large (in time)

Technology will reduce the dependence on oil and make alternate fuels more viable

New technologies will also likely “solve” China’s and India’s expected surge in energy demand

Copyright © 2006 Global Insight, Inc. 7 03/2006

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005

0

10

20

30

40

50

60

70

Nonferrous Metals (Left scale) Crude Oil (Right scale)

(1994-95=1.0)

With OPEC Surplus Gone, Oil Is Now Just Another Cyclical Commodity

(WTI, $/barrel)

Copyright © 2006 Global Insight, Inc. 8 03/2006

How Big of a Threat Is Housing?

Since 1997, house prices have risen 170% in Spain, 160% in the U.K., 120% in Australia, 80% in the U.S., and 50% in Canada

While there is no national U.S. bubble, a few regional markets (the Boston to Washington corridor, Florida, and California) have valuations that are much higher than market fundamentals

The global rise in home prices has been driven by the fall in long-term interest rates

If national house prices fall by 10%, real GDP growth could be cut by 1% to 2%

While such a scenario may not happen at the national level, it could easily happen in regional housing markets

Copyright © 2006 Global Insight, Inc. 9 03/2006

Global Imbalances

Growth and Policy ImbalancesOutput gaps—divergent trends across the world Policies—U.S. too loose, Eurozone and Japan too tight Near-term growth—domestic-led in the U.S., export-led in the

rest of the worldLonger-term growth—lopsided, only 1.5% to 2% in Europe and

Japan

“Glut” of Savings or “Dearth” of Investment?The savings glut—a major factor behind falling global long-term

bond yields over the past 15 years Too little investment relative to saving in emerging marketsToo little saving relative to investment in the U.S.While this “imbalance” is unlikely to persist in the long term, it will

probably go on for some time, because it is mutually beneficial

Copyright © 2006 Global Insight, Inc.

Global Outlook: Relatively Clear Sailing for Another

Year or Two, Despite Serious Structural Problems

Copyright © 2006 Global Insight, Inc. 11 03/2006

(Real GDP, percent change)

Growth in the World Economy

0

1

2

3

4

5

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

Copyright © 2006 Global Insight, Inc. 12 03/2006

Growth Remains Very Uneven Across the World

(Real GDP, percent change)

0.0

1.5

3.0

4.5

6.0

7.5

NAFTA OtherAmericas

WesternEurope

EmergingEurope

Japan OtherAsia

MiddleEast

Africa

2004 2005 2006 2007

Copyright © 2006 Global Insight, Inc. 13 03/2006

World Growth Contributions 2000–2005

(Percent)

Asia-Pacific 34

China 14

India 5

Japan 5

United States 30

Western Europe 16

Copyright © 2006 Global Insight, Inc. 14 03/2006

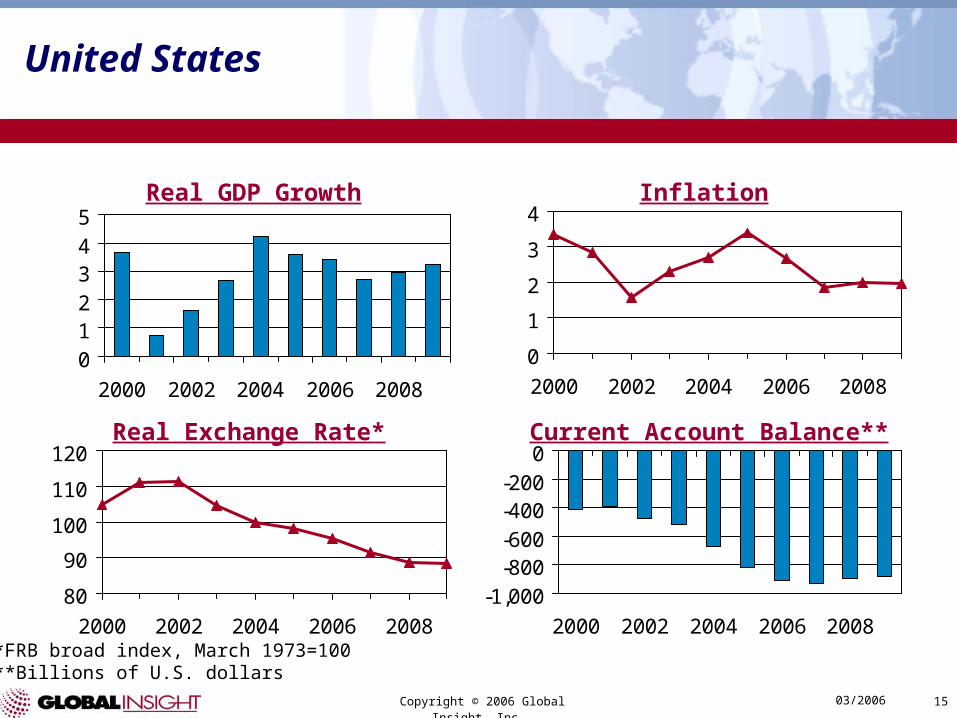

United States

A Strong Dynamic Locomotive, or… The resilience of the U.S. economy in the face of repeated shocks

has been remarkable Above average productivity growth Strong growth in exports and capital spending will offset weaker

consumer and government spending The U.S. budget deficit is a manageable problem Global savings flows into the U.S. are financing global

growth, and not American profligacy

… An Accident Waiting to Happen? The U.S. is vulnerable to higher inflation and higher interest rates Not enough of the global savings that flows into the U.S. has gone into

productive investments The U.S. is becoming increasingly vulnerable to shifts in portfolio

re-allocations

Bottom Line While the ever-growing U.S. imbalances are not sustainable in the medium

to long term, a painful unwinding is far from inevitable, given the American economy’s strong growth potential and resilience

Copyright © 2006 Global Insight, Inc. 15 03/2006

-1,000-800-600-400-200

0

2000 2002 2004 2006 2008

United States

80

90

100

110

120

2000 2002 2004 2006 2008

0

1

2

3

4

2000 2002 2004 2006 2008012345

2000 2002 2004 2006 2008

Real GDP Growth Inflation

Real Exchange Rate* Current Account Balance**

*FRB broad index, March 1973=100**Billions of U.S. dollars

Copyright © 2006 Global Insight, Inc. 16 03/2006

0

1

2

3

4

5

6

7

1999 2000 2001 2002 2003 2004 2005 2006 2007

Federal Funds 2-Year Treasury Yield 10-Year Treasury Yield

(Percent)

The Fed Has More Work to Do

Copyright © 2006 Global Insight, Inc. 17 03/2006

0 30 60 90 120 150

Italy

France

Germany

United States

Canada

United Kingdom

Japan

1991 2003

Is the U.S. Household Sector Profligate?(Household Debt as a Share of Disposable Income)

(Percent of disposable income)

Source: OECD

Copyright © 2006 Global Insight, Inc. 18 03/2006

Low Saving Rates — Not Just in the U.S.

-10

-5

0

5

10

15

1987 1989 1991 1993 1995 1997 1999 2001 2003

Australia New Zealand Canada United States

(Percent)

Copyright © 2006 Global Insight, Inc. 19 03/2006

A Low U.S. Saving Rate Limits the Recovery in Household Net Worth

-2

0

2

4

6

8

10

12

1980 1984 1988 1992 1996 2000 2004 2008

3.6

4.0

4.4

4.8

5.2

5.6

6.0

6.4

Saving Rate Household Net Worth/Disposable Income

(Percent of disposable income) (Ratio to disposable income)

Copyright © 2006 Global Insight, Inc. 20 03/2006

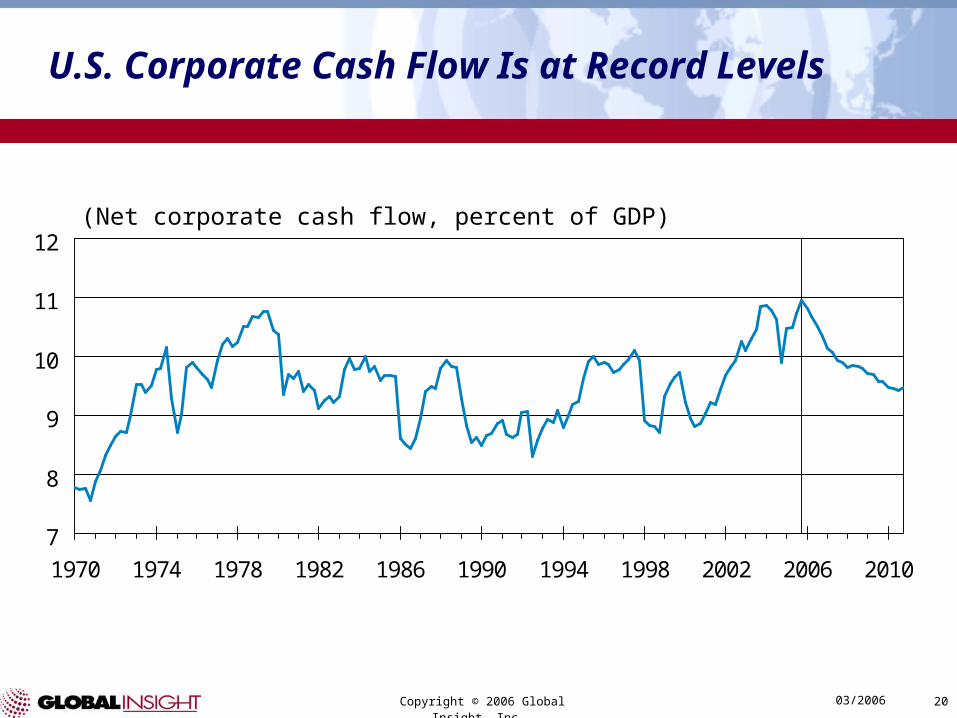

U.S. Corporate Cash Flow Is at Record Levels

(Net corporate cash flow, percent of GDP)

7

8

9

10

11

12

1970 1974 1978 1982 1986 1990 1994 1998 2002 2006 2010

Copyright © 2006 Global Insight, Inc. 21 03/2006

-600

-450

-300

-150

0

150

300

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010 2013

-6.0

-4.5

-3.0

-1.5

0.0

1.5

3.0

Unified Budget Deficit Deficit as % of GDP

The Federal Budget Deficit

(Billions of dollars, fiscal years) (Percent of GDP)

Copyright © 2006 Global Insight, Inc. 22 03/2006

0 30 60 90 120 150 180

United Kingdom

United States

Canada

Eurozone

Japan

1991 2004

Is the U.S. Public Sector Profligate?

Source: OECD

(Public debt as a share of GDP)

Copyright © 2006 Global Insight, Inc. 23 03/2006

The “Twin Deficits”

-7.5

-6.0

-4.5

-3.0

-1.5

0.0

1.5

3.0

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

U.S. Federal Deficit to GDP Current Account Deficit as % of GDP

Copyright © 2006 Global Insight, Inc. 24 03/2006

Europe

A Source of Stability, or… Not one Europe, but many Europe is a savings surplus region, which should help it in a crisis (e.g.

an oil shock) Inflationary pressures may be more muted than in the U.S. European companies have done better than European economies

…Dangerous Stagnation? Macro policies are (still) too restrictive Recent political turmoil has more to do with weak growth

than fears of globalization and enlargement Declining productivity growth and growing output gaps

are serious political and economic threats Rising youth unemployment and low labor force participation will

increase political tensions and worsen the pensions burden Budget challenges are more daunting than the U.S. given

lower trend growth, more rapidly aging populations, and higher tax rates

Bottom Line While the doom and gloom about Europe has undoubtedly been

overdone, it faces much bigger challenges than the U.S.

Copyright © 2006 Global Insight, Inc. 25 03/2006

-60-30

0306090

2000 2002 2004 2006 2008

Eurozone

0.5

0.7

0.9

1.1

1.3

2000 2002 2004 2006 2008

1.5

1.8

2.1

2.4

2.7

2000 2002 2004 2006 20080

1

2

3

4

2000 2002 2004 2006 2008

Real GDP Growth Inflation

Exchange Rate per US$* Current Account Balance**

*Year-end**Billions of U.S. dollars

Copyright © 2006 Global Insight, Inc. 26 03/2006

Japan

Is it Different This Time, or… Japan has come a long way in cleaning up its banking system and

restructuring its corporate balance sheets Macro policies have been better than in Europe (at least recently) Proximity to China has helped Domestic demand is growing—albeit slowly Top-100 firms continue to do well

…Is This Just Another False Dawn? Highest debt levels (public and private) among the industrialized

economies One of the most rapidly aging populations—in 2005 population

actually decreased Saving and investment ratios have been falling Deflation has not yet been eliminated

Bottom Line While Japan will probably not suffer another relapse soon, and short-

term prospects are better than in Europe, long-term prospects are problematic

Copyright © 2006 Global Insight, Inc. 27 03/2006

Japan

050

100150200250

2000 2002 2004 2006 2008

75

90

105

120

135

2000 2002 2004 2006 2008

-2-10123

2000 2002 2004 2006 20080.00.51.01.52.02.53.0

2000 2002 2004 2006 2008

Real GDP Growth Inflation

Exchange Rate per US$* Current Account Balance**

*Year-end**Billions of U.S. dollars

Copyright © 2006 Global Insight, Inc. 28 03/2006

Asia

Independent Engine of Growth, or… Domestic demand in much of Asia has contributed to growth

(investment-driven in China, consumption driven in South Korea) Monetary and fiscal policies have been largely supportive of growth Inflation remains low (except in India) High oil prices have done limited damage in a few economies

(e.g. South Korea and Taiwan)

…Still Too Dependent on the U.S.? Either directly or indirectly (through China), exports still play a big role

in growth Rates of investment are too low (except for China) for economies that

are growing rapidly By preventing their exchange rates from appreciating, the Asian

economies have become part of the “global imbalance problem”

Bottom Line Asian Economies will continue to be the star performers of the world

economy, but will have to wean themselves off their “addiction” to U.S. consumer spending

Copyright © 2006 Global Insight, Inc. 29 03/2006

Real GDP Growth in Asian Economies

0

2

4

6

8

10

12

China South Korea India Taiwan Hong Kong

2004 2005 2006 2007

(Percent change)

Copyright © 2006 Global Insight, Inc. 30 03/2006

0

2

4

6

8

10

Australia Indonesia Singapore Malaysia Philippines

2004 2005 2006 2007

(Percent change)

Real GDP Growth in Asian Economies

Copyright © 2006 Global Insight, Inc.

What Would it Taketo

Trigger a Recession?

Copyright © 2006 Global Insight, Inc. 32 03/2006

No Recession in the Next Couple of Years, Without the Convergence of Two or More Big Shocks

The resilience of the U.S. and world economies allowed them to withstand a number of sizeable shocks in 2005One of the worst tsunamis on recordOne of the worst hurricanes on recordRecord-high oil prices

What would it take to trigger a recession?Oil prices over $100A wage price spiralA 300 basis point rise in long-term interest ratesA 10% drop in house prices

Fortunately, the risk of a recession in the next two years is less than 20%

Copyright © 2006 Global Insight, Inc. 33 03/2006

Recession Scenario — Oil Prices

25

50

75

100

125

2005 2006 2007 2008 2009 2010 2011 2012

World Recession Scenario Baseline

(U.S. dollar per barrel)

Copyright © 2006 Global Insight, Inc. 34 03/2006

Recession Scenario — House Prices

2006 2007–25

Great Britain -5.00 -10.00

Spain -5.00 -10.00

Australia -5.00 -10.00

France -5.00 -10.00

Italy -5.00 -10.00

United States -5.00 -10.00

Canada -5.00 -10.00

(Percent deviation)

Copyright © 2006 Global Insight, Inc. 35 03/2006

Recession Scenario — Real GDP Growth

0.00.51.01.52.02.5

2006 2008 2010 2012

1

2

3

4

5

2006 2008 2010 20121

2

3

4

5

2006 2008 2010 2012

(Percent change)World

4.5

6.0

7.5

9.0

10.5

2005 2007 2009 2011

United States

Japan China

World Recession Scenario BaselineSource: Global Insight Global Scenario Model

Copyright © 2006 Global Insight, Inc. 36 03/2006

Recession Scenario — Real GDP Growth

0.51.01.52.02.53.0

2006 2008 2010 2012

0.5

1.0

1.5

2.0

2.5

2006 2008 2010 20120

1

2

3

4

2006 2008 2010 2012

(Percent change)United Kingdom

-1

0

1

2

3

2006 2008 2010 2012

Germany

France Italy

Source: Global Insight Global Scenario ModelWorld Recession Scenario Baseline

Copyright © 2006 Global Insight, Inc. 37 03/2006

Conclusions

Higher oil prices are not a serious threat—yet Some housing bubbles are deflating—recessions will probably not follow The short- and long-term growth imbalances are a major source of

concern The savings “glut” is less of a threat than the “dearth” of investment The U.S. and China will remain the primary engines of growth for the next

year or two No recession likely in 2006, or even 2007 What could trigger a recession? A combination of:

Much higher energy prices — but not alone Rising inflation expectations Sharply higher interest rates Big drops in house prices Timing: No earlier than 2007 Probability: No more than 20%

Copyright © 2006 Global Insight, Inc.

Canadian Economic Performanceand Fiscal Policy Issues

Dale Orr

Canadian Macroeconomic Services

Global Insight

Copyright © 2006 Global Insight, Inc. 39 03/2006

Outline

1. Canada’s Economic Performance: How Are We Doing?

2. What Can We Expect In Budget 2006?

3. Conclusions

Copyright © 2006 Global Insight, Inc. 40 03/2006

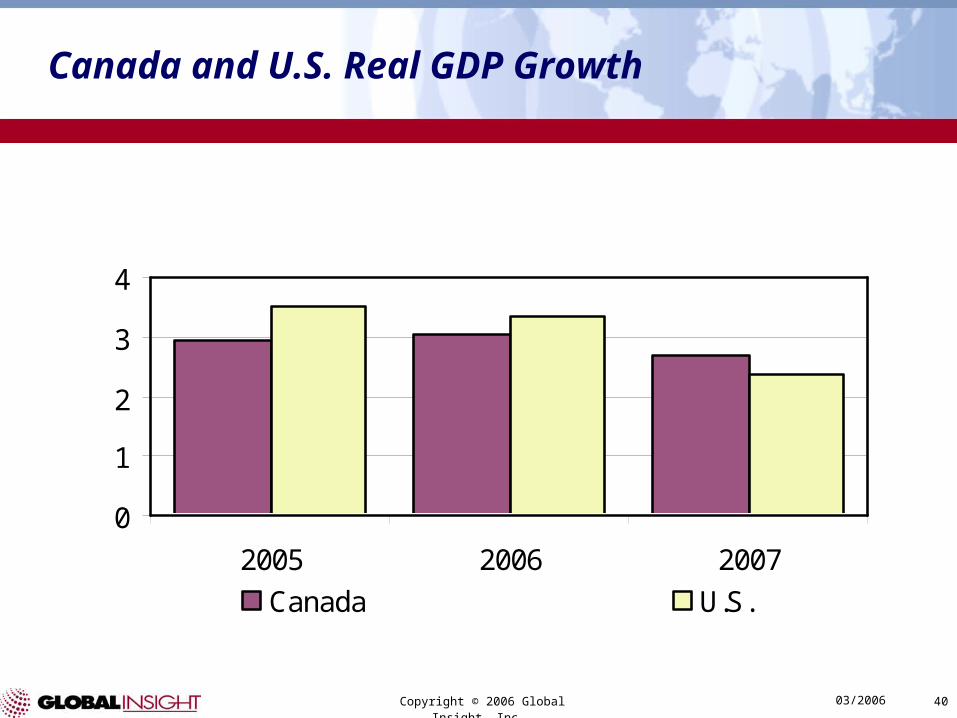

Canada and U.S. Real GDP Growth

0

1

2

3

4

2005 2006 2007

Canada U.S.

Canada Decent, But Falling Short of the U.S.(Percent)

Copyright © 2006 Global Insight, Inc. 41 03/2006

Canada: Unemployment Rate

6.5

7.5

8.5

9.5

10.5

11.5

1993

1995

1997

1999

2001

2003

2005

2007

Unemployment Rate: Falling For A Decade(Percent)

Copyright © 2006 Global Insight, Inc. 42 03/2006

Canada: Inflation

0

1

2

3

05Q

1

05Q

2

05Q

3

05Q

4

06Q

1

06Q

2

06Q

3

06Q

4

07Q

1

07Q

2

07Q

3

07Q

4

Benefitting From The GST Cut This Year(CPI, year-over-year percent change)

Copyright © 2006 Global Insight, Inc. 43 03/2006

Canadian Dollar

6064687276808488

02Q

1

02Q

3

03Q

1

03Q

3

04Q

1

04Q

3

05Q

1

05Q

3

06Q

1

06Q

3

07Q

1

07Q

3

Canadian Dollar Will Level Off Now(U.S. cents)

Copyright © 2006 Global Insight, Inc. 44 03/2006

Nominal GDP

1563

14281496

14491498

1560

1000

1100

1200

1300

1400

1500

1600

2006 2007 2008

Econ. Stat. Nov 05 March 06

The "Tax Base" Up Slightly Since Economic Statement (Billions of Dollars)

Copyright © 2006 Global Insight, Inc. 45 03/2006

Issues in Budget 2006

● Balanced Budget Every Year

● Reduce GST

● Financing GST Reduction by PIT Rollbacks

● Capital Gains

● Child Care

● Spending Plans

Copyright © 2006 Global Insight, Inc. 46 03/2006

The Plan For Program Spending

187.2

172.2 171.6170.7

189.6184.7

160165

170175180185

190195

2006/07 2008/09

1. Econ Stat Nov 05 2. Liberal Election Plan Jan 06

3. Conservative Plan Jan 06

Conservative Program Spending Plan in Perspective(Billions of dollars)

Copyright © 2006 Global Insight, Inc. 47 03/2006

Forecast Surpluses

1.7

4.7 5.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

2006/07 2007/08 2008/09

Small "Surpluses" Forecast by Conservatives Fiscal Plan(Billions of Dollars)

Copyright © 2006 Global Insight, Inc. 48 03/2006

Challenges Beyond Budget 2006

● Fiscal Imbalance

● BPA to $10,000 by 2009

● GST to 5% Over Five Years

Copyright © 2006 Global Insight, Inc. 49 03/2006

Conclusions

● Canadian Economy: The Canadian Economy is in solid shape relative to historical performance, as well as relative to other developed countries. However, growth in Canada has been a shade weaker than in the U.S. in recent years, and that will continue this year.

● Budget 2006: Budget 2006 in April will provide the promised reduction in the GST and a balanced budget every year. Financing these key objectives will be a political challenge and leave little flexibility to make progress towards other objectives, in spite of a slightly stronger economic outlook.

● Finance Minister Flaherty will have little flexibility over the next few years. There will be limited opportunities for any new tax reduction initiatives.

Copyright © 2006 Global Insight, Inc.

Canada: Prepare for the Long-Term Slowdown

Wojciech Szadurski

Senior Economist

Canadian Macroeconomic Service

March 14, 2006

Copyright © 2006 Global Insight, Inc. 51 03/2006

3% Growth Has Been the Norm

Real GDP growth bounced around 3%:Bank of Canada’s

estimate of potential.

Population growth was around 1%.

Employment grew 1.9% per year—much faster than population.

Labor productivity improved about 1.1% per year.

0

1

2

3

4

5

76-80

81-85

86-90

91-95

96-00

01-05

06-10

Real GDP Population

(Per

cent

cha

nge)

Copyright © 2006 Global Insight, Inc. 52 03/2006

Employment Will Slow More Than Population…

-1

0

1

2

3

4

76-80 86-90 96-00 06-10 16-20 26-30

Population Employment

(Per

cent

cha

nge)

Copyright © 2006 Global Insight, Inc. 53 03/2006

…as the Share of People 65-Plus Years Old in Working-Age Population Increases

As baby boomers retire, the labor force participation rate will decline from 67% currently to about 60%.

A low unemployment rate of old workers will provide a slight offset.

10

15

20

25

30

76-80

81-85

86-90

91-95

96-00

01-05

06-10

11-15

16-20

21-25

26-30

(Per

cent

)

Baby

Boomer

s

Retire

Copyright © 2006 Global Insight, Inc. 54 03/2006

A Slowdown is in Store…

Employment

-1

0

1

2

3

4

5

76-80

81-85

86-90

91-95

96-00

01-05

06-10

11-15

16-20

21-25

26-30

(Per

cent

cha

nge)

Copyright © 2006 Global Insight, Inc. 55 03/2006

…Even With Solid Productivity Growth

Employment Productivity GDP

-1

0

1

2

3

4

5

76-80

81-85

86-90

91-95

96-00

01-05

06-10

11-15

16-20

21-25

26-30

(Per

cent

cha

nge)

Copyright © 2006 Global Insight, Inc. 56 03/2006

Pressing Questions

Can immigration solve the employment problem?

How to boost productivity?

Will the standard of living for Canadians decline?

How does Canada measure up in the world?

What does this all mean for my business?

Copyright © 2006 Global Insight, Inc. 57 03/2006

Can Immigration Solve the Employment Problem?

In order to keep employment growth at 1.2%, the numbers of immigrants admitted to Canada would have to grow from about 225,000 currently to 400K+ in the next decade and 700K in the 2020s.

In such a scenario, the ratio of immigrants to 1,000 Canadians would rise from 7 to 17.

This ratio has fluctuated between 4 and 10 over the past 30 years.

Disappointing economic performance of immigrants since the 1990s favors neither adoption nor achievement of aggressive immigration targets.

Copyright © 2006 Global Insight, Inc. 58 03/2006

The Productivity Challenge

Canada has the potential for robust productivity growth.Productivity growth averaged 2.0% in 1995–99.Labor market shortages will force companies to extract

more output out of the existing workforce.

But there are good reasons not to be overly optimistic.Productivity grew only 0.7% a year in 2001–05.Productivity growth averaged 1% a year over the

past 30 years.Older societies often opt for stability rather than change,

while change is the very essence of productivity growth.

Copyright © 2006 Global Insight, Inc. 59 03/2006

What can government do?

Cut capital taxes.

– Canada has the second highest

marginal effective rate on capital

among 37 major economies.

Improve the quality of university

education, especially at the graduate

level.

– Masters and PhD program

graduates are key drivers of

innovation.

Provide a competitive tax regime to

keep most productive (high-income)

people in Canada.

What can business do? Provide employees with more capital to work with.

–Canada’s service sector badly trails the U.S. in capital intensity per worker.

Put greater emphasis on research, innovation, and technology adoption.

Focus on more value-added production.

What Can Be Done to Boost Productivity Growth?

Although there is no silver bullet, there are a number of options.

Copyright © 2006 Global Insight, Inc. 60 03/2006

Canadians’ Standard of Living Will Increase, But…

Rising productivity growth will ensure steady growth in living standards.

The gap with the United States, however, will rise from 15% currently to over 20%.20

30

40

50

60

76-80

81-85

86-90

91-95

96-00

01-05

06-10

11-15

16-20

21-25

26-30

(Tho

usan

ds o

f 199

7$ p

er c

apita

)

Copyright © 2006 Global Insight, Inc. 61 03/2006

Canada’s Long-Term Growth from Global Perspective

Copyright © 2006 Global Insight, Inc. 62 03/2006

Implications for Business

Overall domestic demand will slow,with important differences among businesses

serving particular age groups, e.g., elderly vs. youth.

Overall foreign demand will outpace domestic demand.The United States will grow faster than Canada, but

most European nations will grow slower.

Domestic labor will become scarce and older.

Copyright © 2006 Global Insight, Inc.

How Can Businesses Adjust?

Copyright © 2006 Global Insight, Inc. 64 03/2006

Framework for Analysis—Domestically-Oriented Business

Degree of Export Orientation

Ab

ilit

y to

Tap

in

to F

ore

ign

In

pu

ts,

Lab

or,

etc

. Companies serving mostly the

domestic market, e.g., in retail, construction,

business services, health-care, and

education

Copyright © 2006 Global Insight, Inc. 65 03/2006

Framework for Analysis—Export-Oriented Business

Degree of Export Orientation

Ab

ilit

y to

Tap

in

to F

ore

ign

In

pu

ts,

Lab

or,

etc

.

Companies that can plug into global supply networks; e.g., many manufacturers

Companies that have to undertake most of their production in Canada, e.g., agriculture, forestry and logging, and mining

Copyright © 2006 Global Insight, Inc. 66 03/2006

How Could Businesses Respond?

Degree of Export Orientation

Ab

ilit

y to

Tap

in

to F

ore

ign

In

pu

ts,

Lab

or,

etc

.

● Incorporate more imported inputs in production

● Offshore less value-added processes

● Increase capital intensity per worker

● Increase capital intensity per worker

● Increase reliance on foreign workers

● Scale down operations alongside slower growth

● Adjust to serve fastest growing population segments such as the elderly or children of visible minorities

● Outsource labor-intensive work offshore, e.g., Bangalore

● Explore export opportunities

Copyright © 2006 Global Insight, Inc. 67 03/2006

In Summary

As baby boomers retire over the next decade or so, Canada’s economic growth will decline.Governments could ease, but not prevent, the

slowdown in GDP and employment.

Fortunately, global demand will continue to grow at a solid pace and Canadians’ standard of living will increase.

Unfortunately, businesses will have to adjust to the increased scarcity of labor and the Canada-U.S. standard-of-living gap will widen.

Slow-growing Europe could offer valuable lessons and case studies for Canadian governments and companies.

Copyright © 2006 Global Insight, Inc. 68 03/2006

Dale Orr

Wojciech Szadurski

Nariman [email protected]

Thank you