(convenience translation of a report and ... - bossa.com.tr · (convenience translation of a report...

TRANSCRIPT

(Convenience translation of a report and financial statements originally issued in Turkish)

Bossa Ticaret ve Sanayi İşletmeleri T.A.Ş.

Consolidated financial statements for the period between January 1 – December 31, 2016 together with independent auditors’ report

(Convenience translation of a report and financial statements originally issued in Turkish (See additional paragraph below for convenience translation and Note 2)) Table of contents Page

Independent auditors’ report on the consolidated financial statements 1 - 2

Consolidated statement of financial position 3 - 4

Consolidated statement of profit and loss and comprehensive income 5

Consolidated statement of changes in equity 6 - 7

Consolidated statement of cash flows 8

Consolidated disclosures related to financial statements 9 - 61

(Convenience translation into English of independent auditors’ report originally issued in Turkish) INDEPENDENT AUDITOR’S REPORT To the Board of Directors of Bossa Ticaret ve Sanayi İşletmeleri T.A.Ş. We have audited the accompanying balance sheet of Bossa Ticaret ve Sanayi İşletmeleri T.A.Ş. (the Company) and its subsidiary (all together referred to as “the Group”) as at December 31, 2016 and the related statement of profit or loss and other comprehensive income, statement of changes in equity and statement of cash flows for the year then ended and a summary of significant accounting policies and explanatory notes. Management's responsibility for the financial statements Company’s management is responsible for the preparation and fair presentation of financial statements in accordance with the Turkish Accounting Standards and for such internal controls as management determines is necessary to enable the preparation and fair presentation of financial statements that are free from material misstatement, whether due to error and/or fraud. Independent auditors’ responsibility Our responsibility is to express an opinion on these financial statements based on our audit. Our audit was conducted in accordance with standards on auditing issued by the Capital Markets Board of Turkey and standards on auditing issued by POA. Those standards require that ethical requirements are complied with and that the independent audit is planned and performed to obtain reasonable assurance whether the financial statements are free from material misstatement. Independent audit involves performing independent audit procedures to obtain independent audit evidence about the amounts and disclosures in the financial statements. The independent audit procedures selected depend on our professional judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to error and/or fraud. In making those risk assessments, the Company’s internal control system is taken into consideration. Our purpose, however, is not to express an opinion on the effectiveness of internal control system, but to design independent audit procedures that are appropriate for the circumstances in order to identify the relation between the financial statements prepared by the Company and its internal control system. Our independent audit includes also evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the Company’s management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained during our independent audit is sufficient and appropriate to provide a basis for our audit opinion. Opinion In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the financial position of Bossa Ticaret ve Sanayi İşletmeleri T.A.Ş. and its subsidiary as at December 31, 2016 and their financial performance and cash flows for the year then ended in accordance with the Turkish Accounting Standards.

(2)

Emphasis of matters a) We draw attention to the Company’s explanations in footnote 29 related to management’s

plans, estimates and assumptions intended to offset non trade receivables as of December 31, 2016 the Company has a non-trade receivables amounting to TL 245.307.848 from its 93,75% shareholder Akkardan Sanayi ve Ticaret A.Ş. whose operations were discontinued. Our opinion is not qualified in respect of this matter.

b) We draw attention to the Company’s explanations in footnote 18 related to evaluation of its

receivables amounting to TL 122.914.099 from Akkardan Sanayi ve Ticaret A.Ş, shareholder of the Company whose operations were discontinued, in scope of Article 74

of the Law numbered

6552 in order to benefit from given rights in 2014 and obtained the right to derecognize this amount by paying the related taxes; nevertheless, since performed transaction is related to the parent company, the Company management plans to carry the related amount of TL 122.914.099 separately in “Other funds” created under the equity account as of December 31, 2014 and to offset this amount through the other capital market instruments including the dividend payments to be made to the parent company in the future, share sales and merger transactions. Our opinion is not qualified in respect of this matter.

Report on Independent Auditor’s Responsibilities Arising from Other Regulatory Requirements 1) In accordance with subparagraph 4 of Article 398 of the Turkish Commercial Code (“TCC”)

6102, the Independent Auditor’s Report on the Early Identification of Risk System and Committee was submitted to the Board of Directors of the Company on February 17, 2017.

2) In accordance with Article 402 TCC, no significant matter has come to our attention that leads

us to believe that the Company’s bookkeeping activities for the period January 1 - December 31, 2016 is not in compliance with the code and provisions of the Company’s articles of association in relation to financial reporting.

3) In accordance with Article 402 of the TCC, the Board of Directors has provided us with the

required explanations and documents. Additional paragraph for convenience translation into English of financial statements originally issued in Turkish As at December 31, 2016, the accounting principles described in Note 2 (defined as Turkish Accounting Standards/Turkish Financial Reporting Standards) to the accompanying financial statements differ from International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board with respect to the application of inflation accounting, certain reclassifications and also for certain disclosures requirements of the POA. Accordingly, the accompanying financial statements are not intended to present the financial position and results of the operations in accordance with IFRS. Güney Bağımsız Denetim ve Serbest Muhasebeci Mali Müşavirlik Anonim Şirketi A member firm of Ernst&Young Global Limited Necati Tolga Kırelli, SMMM Partner 17 February 2017 Istanbul, Turkey

(Convenience translation of financial statements originally issued in Turkish (See Note 2)) Bossa Ticaret ve Sanayi İşletmeleri T.A.Ş. Consolidated statement of financial position as of December 31, 2016 (Amounts expressed in Turkish Lira (“TL”) unless otherwise stated)

The accompanying policies and explanatory notes form an integral part of these consolidated financial statements.

(3)

Current period Prior period

(Audited) (Audited)

Notes 31 December 2016 31 December 2015

ASSETS

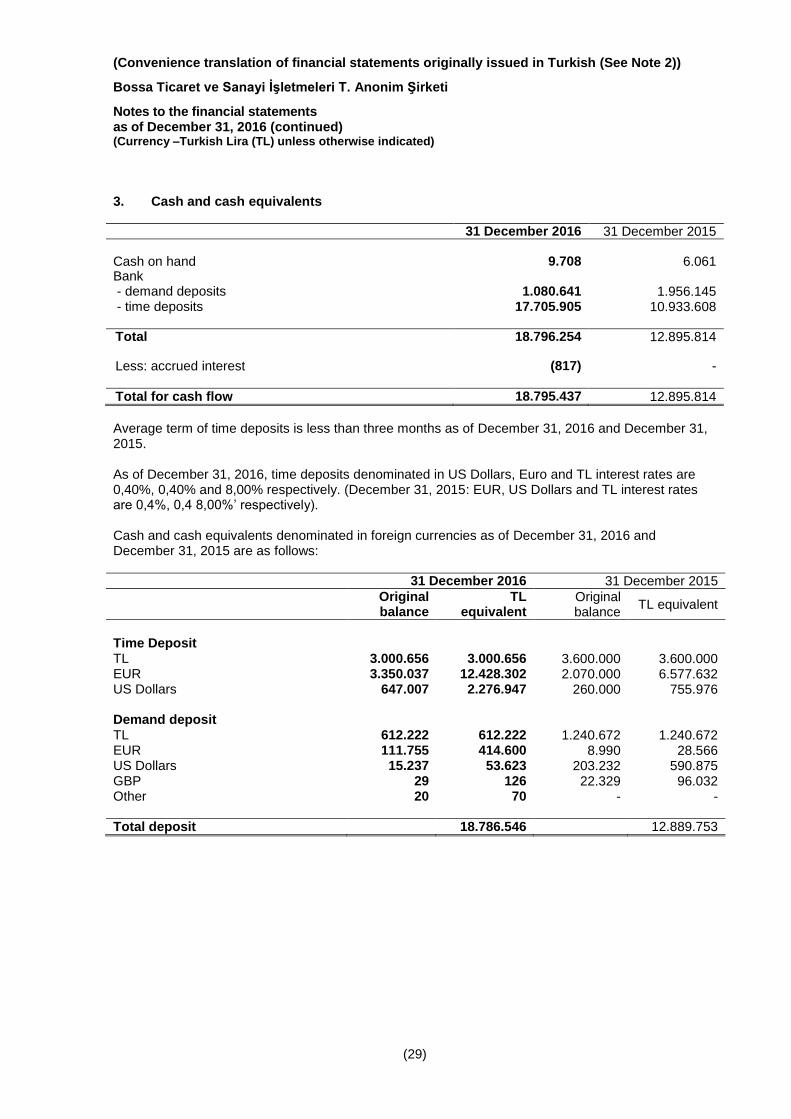

Current assets Cash and cash equivalents 3 18.796.254 12.895.814

Trade receivables

73.270.067 94.873.516 - Trade receivables, third parties 5 73.270.067 94.873.516 Other receivables

3.232.620 5.964.928

- Other receivables, third parties 6 2.792.620 5.964.928 - Other receivables, related party 29 440.000 -

Inventories 9 66.792.839 72.886.625 Prepaid expenses 7 1.743.469 - - Other receivables, third parties 1.743.469 -

Assets related to current period tax 25 2.070.425 - Other current assets 8 1.449.186 1.942.902 - Other receivables, third parties 1.449.186 1.942.902

SUBTOTAL 167.354.860 188.563.785

Asset held for sale 10 37.866.603 51.994.240

TOTAL CURRENT ASSETS

205.221.463 240.558.025

Non-current assets

Other receivables

245.307.848 228.177.995 - Other receivables, related parties 29 245.307.848 228.177.995

Investment Properties

87.228.000 - Tangible assets 11 168.123.794 210.529.372 Intangible assets 12 11.498.630 7.106.450

Prepaid Expenses 7 1.552.026 - - Prepaid expenses, third parties

1.552.026 -

TOTAL NON-CURRENT ASSETS

513.710.298 445.813.817

TOTAL ASSETS 718.931.761 686.371.842

(Convenience translation of financial statements originally issued in Turkish (See Note 2)) Bossa Ticaret ve Sanayi İşletmeleri T.A.Ş. Consolidated statement of financial position As of December 31, 2016 (Amounts expressed in Turkish Lira (“TL”) unless otherwise stated)

The accompanying policies and explanatory notes form an integral part of these consolidated financial statements.

(4)

Current period Prior period

(Audited) (Audited)

Notes 31 December 2016 31 December 2015

LIABILITIES

Short term liabilities:

Short term liabilities 130.266.284 86.952.822 Short term liabilities, third parties 130.266.284 86.952.822

- Bank loans 4 86.454.204 63.952.431 - Financial liabilities (leasing) 4 2.432.285 1.381.144 - Bonds issued 4 41.379.795 21.619.247 Trade payables

104.396.257 85.700.402

- Trade payables, third parties 5 104.396.257 85.700.402 Employee benefit obligations 14 7.083.214 6.221.829 Other payables

21.130 29.533

- Other payables, third parties 6 21.130 29.533 Deferred income 15 1.384.438 2.161.149 - Deferred income, third parties 15 1.384.438 2.161.149 Government incentives and grants 15 269.760 323.320 Provision for taxation on income 26 - 3.356.205 Short-term provisions 16,17 4.215.127 2.563.314 - Other short-term provisions 17 3.259.044 1.404.148

- Provisions for employee benefits 16 956.083 1.159.166 Other current liabilities 8 4.547.138 4.451.641

- Other current liabilities, third party 4.547.138 4.451.641

TOTAL CURRENT LIABILITIES

252.183.348 191.760.215

Non-current liabilities: Non- current liabilities 139.256.221 159.832.568

Long term liabilities, third parties 139.256.221 159.832.568 - Bank loans 4 136.454.946 136.407.550 - Financial liabilities (leasing) 4 2.801.275 3.252.612 - Bonds issued 4 - 20.172.406 Government incentives and grants 15 209.162 478.921 Long term provisions

11.138.546 10.602.701

- Long term provision for employee benefits 16 11.138.546 10.602.701 Deferred tax liabilities 26 14.895.682 15.907.748

Long Term Liabilities 7 2.980.304 - - Long term liabilities, third party 2.980.304 -

TOTAL NON-CURRENT LIABILITIES

168.479.915 186.821.938

Shareholders’ equity Shareholders’ equity

298.268.498 307.789.689 Paid-in share capital 18 108.000.000 108.000.000 Paid-in capital restatement difference 18 149.104.739 149.104.739 Share premium 18 3.435 3.435 Restricted reserves 18 41.022.230 39.316.910 - Legal reserves 31.489.253 29.783.933 - Gain on sale of real estate subsidiary surplus to capital 9.532.977 9.532.977 Other equity shares 18, 29 (122.914.099) (122.914.099) Other comprehensive income/loss not to be reclassified to profit or loss 18 129.599.668 110.113.955 - Revaluation funds 18 146.917.072 120.412.671 - Actuarial gain or loss arising from defined benefit plans 18 (17.317.404) (10.298.716) Retained earnings 18 2.115.102 2.361.676 Net (loss)/profit for the period 18 (8.662.577) 21.803.073

TOTAL EQUITY

298.268.498 307.789.689

TOTAL LIABILITIES AND EQUITY

718.931.761 686.371.842

(Convenience translation of financial statements originally issued in Turkish (See Note 2)) Bossa Ticaret ve Sanayi İşletmeleri T.A.Ş. Consolidated statement of profit and loss and comprehensive income for the year ended December 31, 2016 (Amounts expressed in Turkish Lira (“TL”) unless otherwise stated)

The accompanying policies and explanatory notes form an integral part of these consolidated financial statements.

(5)

Current period Prior period

(Audited) (Audited)

STATEMENT OF PROFIT AND LOSS AND OTHER COMPREHENSIVE INCOME Notes

1 January - 31 December

2016

1 January - 31 December

2015

PROFIT(LOSS)

Revenue 19 361.200.233 374.615.566 Cost of sales (-) 19 (282.410.665) (279.201.141)

GROSS PROFIT

78.789.568 95.414.425

Marketing expenses (-) 20 (33.523.056) (38.659.783) General administrative expenses 20 (28.042.156) (32.021.667) Other operating income 21 58.845.786 67.335.138 Other operating expenses (-) 21 (45.317.979) (44.502.850)

OPERATING PROFIT

30.752.163 47.565.263

Income from investment activities 24 3.916.004 4.437.534 Expense from investment activities (-) 25 (15.426.935) (316.498)

OPERATING PROFIT BEFORE FINANCIAL ACTIVITIES

19.241.232 51.686.299

Financial income 22 21.260.140 26.551.537 Financial expenses (-) 23 (50.208.141) (52.892.586)

PRE-TAX INCOME (LOSS) FROM CONTINUING OPERATIONS

(9.706.769) 25.345.250

Tax expense from continuing operations

1.044.192 (3.542.177) - Current tax expense (-) 26 (1.455.354) (4.301.859) - Deferred tax income/(expense) 26 2.499.546 759.682

İNCOME / (LOSS) FROM CONTINUING OPERATIONS

(8.662.577) 21.803.073

PROFIT / (LOSS) FOR THE PERIOD

(8.662.577) 21.803.073

OTHER COMPREHENSIVE INCOME/LOSS

21.594.586 45.238.035

Not to be reclassified to profit or loss 31.855.426 55.402.546 Actuarial loss arising from employee benefits 16 (8.773.360) (6.619.153) Income tax on comprehensive income or loss not to be reclassified to profit or loss

(1.487.480) (3.545.358)

Deferred tax effect

(1.487.480) (3.545.358)

TOTAL COMPREHENSIVE INCOME

12.932.009 67.041.108

Earnings per share

- Earnings per share from continuing operations 27 (0,0008) 0,0020

(Convenience translation of financial statements originally issued in Turkish (See Note 2)) Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi Consolidated statement of changes in equity for the year ended December 31, 2016 (Currency –Turkish Lira (TL) unless otherwise indicated)

The accompanying policies and explanatory notes form an integral part of these financial statements.

(6)

Accumulated other comprehensive income and expense that is not subject

to reclassification to income or loss

Gain or loses revaluation and

remeasurement

Accumulated profits

Prior Period

Paid-in share

capital

Paid-in capital

restatement difference

Share premium Revaluation funds

Actuarial gain or loss arising from

defined benefit plans

Restricted reserves

Other equity shares

Retained earnings

Net profit for the period Total equity

Opening balance, 1 January 2015 108.000.000 149.104.739 3.435 72.179.949 (5.003.393) 50.822.788 (122.914.099) 34.325.411 7.041.751 293.560.581

Transfers - - - (2.300.635) - 4.741.200 - 4.601.186 (7.041.751) - Dividend - - - - - (16.247.078) - (36.564.921) - (52.811.999)

Period income (loss) - - - - - - - - 21.803.073 21.803.073 Other comprehensive income (expense) - - - 50.533.357 (5.295.323) - - - - 45.238.034

Total comprehensive income (expense) - - - 50.533.357 (5.295.323) - - - 21.803.073 67.041.107

Closing balance, 31 December 2015 108.000.000 149.104.739 3.435 120.412.671 (10.298.716) 39.316.910 (122.914.099) 2.361.676 21.803.073 307.789.689

Opening balance, 1 January 2016 108.000.000 149.104.739 3.435 120.412.671 (10.298.716) 39.316.910 (122.914.099) 2.361.676 21.803.073 307.789.689

Transfers - - - (2.108.873) - 1.705.320 - 22.206.626 (21.803.073) - Dividend - - - - - - - (22.453.200) - (22.453.200)

Other comprehensive income (expense) - - - 28.613.274 (7.018.688) - - - - 21.594.586 Period income (loss) - - - - - - - - (8.662.577) (8.662.577)

Total comprehensive income (expense) - - - 28.613.274 (7.018.688) - - - (8.662.577) 12.932.009

Closing balance, 31 December 2016 108.000.000 149.104.739 3.435 146.917.072 (17.317.404) 41.022.230 (122.914.099) 2.115.102 (8.662.577) 298.268.498

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Consolidated statements of cash flows for the year ended December 31, 2016 (Currency –Turkish Lira (TL) unless otherwise indicated)

The accompanying policies and explanatory notes form an integral part of these financial statements.

(7)

Current period Prior period

(Audited) (Audited)

Notes

1 January - 1 January -

31 December 2016 31 December 2015

CASH FLOWS FROM OPERATING ACTIVITIES

21.260.002 (53.628.503)

Profit / Loss for the period

(8.662.577) 21.803.073 Profit / Loss from continuing operations

(8.662.577) 21.803.073

Adjustments related to net income/(loss) reconciliation

35.265.513 26.045.644

Depreciation and amortisation 11, 12 19.175.038 21.115.961 Adjustments related to provisions

4.903.622 3.565.846

- Adjustments related to provisions for employee benefits 16 2.940.928 3.081.223 - Adjustments related to provisions for litigation 17 1.962.694 484.623 Adjustments related to impairment

17.080.791 1.071.687 - Adjustments related to impairment on receivables 5 2.953.154 1.071.687 - Adjustments related to impairment on fixed assets held for sale 10 14.127.637 - Adjustments related to interest income and expense (2.233.040) 871.008 - Adjustments related to interest income 22 (18.925.560) (20.758.605) - Adjustments related to interest expense 23 17.316.303 21.856.150 Unearned financial income from forward sales 5 (511.970) (292.831) Deferred financial expense from forward purchases 5 (111.813) 66.294 Adjustments related to gain/losses from disposals of fixed assets

(2.616.706) (4.121.036)

Adjustments related to gain/losses from disposals of tangible fixed assets 24, 25 (2.616.706) (4.121.036) Adjustments related to tax income and expenses 26 (1.044.192) 3.542.177

Changes in working capital 10.240.973 (92.293.771)

Adjustments related to Increase/decrease in trade receivables

17.557.872 (10.079.643) - Increase/decrease in trade receivables from related parties

17.557.872 (10.079.643) Adjustments related to increase/decrease in other receivables related to operations

(35.446.711) (93.925.432)

- Increase/decrease in trade receivables from related parties

(38.619.019) (141.711.832) - Increase/decrease in trade receivables from other parties

3.172.308 47.786.400 Adjustments related to other increase/decrease in inventories 9 6.093.786 16.187.308 Increase/decrease in prepaid expenses

(3.295.495) 1.569.996

Adjustments related to Increase/decrease in trade payables

18.807.668 (12.355.846) - Increase/decrease in trade payables from other parties

18.807.668 (12.355.846) Increase/decrease in deferred income

(776.711) 2.161.149

Adjustments related to other increase/decrease in working capital

7.300.564 4.148.697 - Increase/decrease in other assets related to operations

493.717 (405.907) - Increase/decrease in other liabilities related to operations

6.806.847 4.554.604

Cash flows from operating activities 36.843.909 (44.445.054)

Taxes paid 26 (6.881.984) (1.944.353) Employment termination benefits paid 16 (10.198.518) (8.285.994) Other cash inflows / outflows 5 1.496.595 1.046.898

CASH FLOWS FROM INVESTING ACTIVITIES (34.240.828) 3.589.748

Cash inflows due to sales of tangible and intangible fixed assets

6.045.178 5.361.730 - Cash inflows due to sale of tangible fixed assets 11 6.045.178 5.361.730 Cash outflows due to purchase of tangible and intangible fixed assets

(39.962.687) (1.810.445) - Cash outflows due to purchase of tangible and intangible fixed assets 11, 12 (39.962.687) (1.810.445) Government grants and incentives 15 (323.319) 38.463

CASH FLOWS FROM FINANCIAL ACTIVITIES 18.880.449 48.295.813

Cash outflows due to loan repayments

(93.832.856) (226.898.340) Cash inflows due to borrowing

116.382.025 302.281.452

Cash inflows due to other financial liabilities

599.804 (344.780) Cash outflows arising from the repayment of bonds

(24.472.930) (45.842.557)

Cash inflows from bond issuance

20.000.000 23.500.000 Dividend payment 18 (1.404.034) (3.302.417) Interest received 22 18.600.333 20.815.060 Interest paid 23 (16.991.893) (21.912.605)

BEFORE THE EFFECT OF CHANGE IN FOREIGN EXCHANGE RATES NET INCREASE/DECREASE ON CASH AND CASH EQUIVALENTS 5.899.623 (1.742.942)

The effect of change in foreign exchange rates on cash and cash equivalents

- -

NET INCREASE/DECREASE IN CASH AND CASH EQUIVALENTS 5.899.623 (1.742.942)

CASH AND CASH EQUIVALENTS AT THE BEGINNING OF THE PERIOD 3 12.895.814 14.638.756

CASH AND CASH EQUIVALENTS AT THE END OF THE PERIOD 3 18.795.437 12.895.814

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (Currency –Turkish Lira (TL) unless otherwise indicated)

(8)

1. Organisation and nature of operations Bossa Ticaret ve Sanayi İşletmeleri T.A.Ş. (“Bossa” or the “Company”) was established in 1951. The main operations of the Company is manufacturing, marketing and selling textile products. Bossa Ticaret ve Sanayi İşletmeleri T.A.Ş and its subsidiary (all together “Group”) consist of Bossa Ticaret ve Sanayi İşletmeleri T.A.Ş and a subsidiary of which shares and control belongs to Bossa. Akkardan Sanayi and Ticaret A.Ş. (“Akkardan”) whose activities are stopped, owns 93,75% of the shares of Bossa as of December 31,2016. (31 December 2015 93,75%). Akkardan’s paid in capital is 62.000.000 TL and all of the shares belong to Serap Kantül. Average number of personnel is 1.834 (December 31, 2015: 1.902).

The Company is registered in Turkey and the address of the registered office is Adana Hacı Sabancı

Organize Sanayi Bölgesi Turgut Özal Bulvarı No:2 Sarıçam – Adana (*).

(*)All the necessary procedures for this process was fulfilled and legislation related announcement was published in Turkey Trade Registry Gazette dated July 15, 2016. In the United States, in order to support marketing activities, a company titled as Bossa International Inc. with a US Dollar 200.000 (Two Hundred Thousand US Dollar) capital with 100% shareholding was established. Capital payment transaction has been completed on December 7, 2015. The name of the subsidiary of Bossa Ticaret ve Sanayi İşletmeleri T.A.Ş., its main activity and direct and indirect capital shares owned by Bossa as of December 31, 2016 are as follows: 31 December 2016 31 December 2015

Affiliated Company Main activity Direct

ownership rate (%)

Indirect ownership rate

(%)

Direct ownership rate (%)

Indirect ownership rate

(%) Bossa International Inc. Marketing Activities 100 100 100 100

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(9)

2. Basis of presentation of financial statements

2.1 Basis of presentation

The financial statements and disclosures have been prepared in accordance with the communiqué numbered II-14.1 “Communiqué on the Principles of Financial Reporting In Capital Markets” (the Communiqué) announced by the Capital Markets Board (“CMB”) (hereinafter will be referred to as “the CMB Reporting Standards”) on June 13, 2013 which is published on Official Gazette numbered 28676. In accordance with article 5th of the CMB Reporting Standards, companies should apply Turkish Accounting Standards/Turkish Financial Reporting Standards and interpretations regarding these standards as adopted by the Public Oversight Accounting and Auditing Standards Authority of Turkey (“POA”).

According to decision which was made by CMB on March 17, 2005, from the date of January 1, 2005 there is no need for inflation accounting application for the listed companies performing in Turkey. The Company has prepared the financial statements according to this decision. Functional and representative currency of the Company is TL. The financial statements are based on the statutory records, with adjustments and reclassifications for the purpose of fair presentation in accordance with the Accounting Standards of the POA. Main adjustments and reclassifications are deferred tax effects, income and expense accruals, and retirement benefit obligations in accordance with Turkish Accounting Standard (“TAS”) 19.

Basis of consolidation

Consolidated financial statements include accounts of parent company, Bossa, and its subsidiary (hereinafter referred to as “Group” as a whole). Financial statements of the subsidiary, mentioned in scope of consolidation, have been prepared in accordance with Turkish Financial Reporting Standards through making required adjustments and classifications taking accounting principles and implementations into consideration as of date of consolidated financial statements. The operating results of the affiliate have been included and excluded on expiry dates of transactions in question according to acquisition and disposal transactions. Going concern

The financial statements including the accounts have been prepared assuming that the Company will continue its operations.

Basis of preparation of financial statements The accompanying financial statements of the Company have been prepared in accordance 2016 TAS Taxonomy which is developed by POA based on (b) subparagraph of article 9 of Statutory Decree numbered 660 and approved by resolution of the Board dated 2/6/2016 and numbered 30. Approval of financial statements The consolidated financial statements have been approved for publication by the Company Management on February 15, 2017. The General Assembly has the power to make changes in the financial statements. 2.2 Amendments in accounting policies The new standards and interpretations The accounting policies adopted in preparation of the consolidated financial statements as at December 31, 2016 are consistent with those of the previous financial year, except for the adoption of new and amended TFRS and TFRIC interpretations effective as of January 1, 2016. The effects of these standards and interpretations on the Group’s financial position and performance have been disclosed in the related paragraphs.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(10)

2. Basis of presentation of financial statements (continued) 2.2 Amendments in accounting policies The new standards and interpretations The accounting policies adopted in preparation of the consolidated financial statements as at December 31, 2016 are consistent with those of the previous financial year, except for the adoption of new and amended TFRS and TFRIC interpretations effective as of January 1, 2016. The effects of these standards and interpretations on the Group’s financial position and performance have been disclosed in the related paragraphs. i) The new standards, amendments and interpretations which are effective as at January 1, 2016 are as follows: TFRS 11 Acquisition of an Interest in a Joint Operation (Amendment) TFRS 11 is amended to provide guidance on the accounting for acquisitions of interests in joint operations in which the activity constitutes a business. This amendment requires the acquirer of an interest in a joint operation in which the activity constitutes a business, as defined in TFRS 3 Business Combinations, to apply all of the principles on business combinations accounting in TFRS 3 and other TFRSs except for those principles that conflict with the guidance in this TFRS. In addition, the acquirer shall disclose the information required by TFRS 3 and other TFRSs for business combinations. The amendments did not have an impact on the financial position or performance of the Group. TAS 16 and TAS 38 - Clarification of Acceptable Methods of Depreciation and Amortisation (Amendments to TAS 16 and TAS 38) The amendments to TAS 16 and TAS 38, have prohibited the use of revenue-based depreciation for property, plant and equipment and significantly limiting the use of revenue-based amortisation for intangible assets. The amendments did not have an impact on the financial position or performance of the Group. TAS 16 Property, Plant and Equipment and TAS 41 Agriculture (Amendment) – Bearer Plants TAS 16 is amended to provide guidance that bearer plants, such as grape vines, rubber trees and oil palms should be accounted for in the same way as property, plant and equipment in TAS 16. Once a bearer plant is mature, apart from bearing produce, its biological transformation is no longer significant in generating future economic benefits. The only significant future economic benefits it generates come from the agricultural produce that it creates. Because their operation is similar to that of manufacturing, either the cost model or revaluation model should be applied. The produce growing on bearer plants will remain within the scope of TAS 41, measured at fair value less costs to sell. The amendment is not applicable for the Group and did not have an impact on the financial position or performance of the Group.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(11)

2. Basis of presentation of financial statements (continued) 2.2 Amendments in accounting policies (continued) TAS 27 Equity Method in Separate Financial Statements (Amendments to TAS 27) Public Oversight Accounting and Auditing Standards Authority (POA) of Turkey issued an amendment to TAS 27 to restore the option to use the equity method to account for investments in subsidiaries and associates in an entity’s separate financial statements. Therefore, an entity must account for these investments either: • At cost • In accordance with IFRS 9, Or • Using the equity method defined in TAS 28 The entity must apply the same accounting for each category of investments The amendment is not applicable for the Group and did not have an impact on the financial position or performance of the Group. TFRS 10 and TAS 28: Sale or Contribution of Assets between an Investor and its Associate or Joint Venture (Amendments) Amendments issued to TFRS 10 and TAS 28, to address the acknowledged inconsistency between the requirements in TFRS 10 and TAS 28 in dealing with the loss of control of a subsidiary that is contributed to an associate or a joint venture, to clarify that an investor recognises a full gain or loss on the sale or contribution of assets that constitute a business, as defined in TFRS 3, between an investor and its associate or joint venture. The gain or loss resulting from the re-measurement at fair value of an investment retained in a former subsidiary should be recognised only to the extent of unrelated investors’ interests in that former subsidiary. The amendment is not applicable for the Group and did not have an impact on the financial position or performance of the Group. TFRS 10, TFRS 12 and TAS 28: Investment Entities: Applying the Consolidation Exception (Amendments to IFRS 10 and IAS 28)

In February 2015, amendments issued to TFRS 10, TFRS 12 and TAS 28, to address the issues that have arisen in applying the investment entities exception under TFRS 10 Consolidated Financial Statements. The amendment is not applicable for the Group and did not have an impact on the financial position or performance of the Group. TAS 1: Disclosure Initiative (Amendments to TAS 1)

The amendments issued to TAS 1. Those amendments include narrow-focus improvements in the following five areas: Materiality, Disaggregation and subtotals, Notes structure, Disclosure of accounting policies, Presentation of items of other comprehensive income (OCI) arising from equity accounted investments. These amendments did not have significant impact on the notes to the interim condensed consolidated financial statements of the Group.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(12)

2. Basis of presentation of financial statements (continued) 2.2 Amendments in accounting policies (continued)

Annual Improvements to TFRSs - 2012-2014 Cycle POA issued, Annual Improvements to TFRSs 2012-2014 Cycle. The document sets out five amendments to four standards, excluding those standards that are consequentially amended, and the related Basis for Conclusions. The standards affected and the subjects of the amendments are: - IFRS 5 Non-current Assets Held for Sale and Discontinued Operations – clarifies that changes

in methods of disposal (through sale or distribution to owners) would not be considered a new plan of disposal, rather it is a continuation of the original plan

- IFRS 7 Financial Instruments: Disclosures – clarifies that i) the assessment of servicing contracts that includes a fee for the continuing involvement of financial assets in accordance with IFRS 7; ii) the offsetting disclosure requirements do not apply to condensed interim financial statements, unless such disclosures provide a significant update to the information reported in the most recent annual report

- IAS 19 Employee Benefits – clarifies that market depth of high quality corporate bonds is assessed based on the currency in which the obligation is denominated, rather than the country where the obligation is located

- IAS 34 Interim Financial Reporting –clarifies that the required interim disclosures must either be in the interim financial statements or incorporated by cross-reference between the interim financial statements and wherever they are included within the interim financial report

The amendment did not have significant impact on the financial position or performance of the Group. ii) Standards issued but not yet effective and not early adopted Standards, interpretations and amendments to existing standards that are issued but not yet effective up to the date of issuance of the consolidated financial statements are as follows. The Group will make the necessary changes if not indicated otherwise, which will be affecting the consolidated financial statements and disclosures, when the new standards and interpretations become effective. TFRS 15 Revenue from Contracts with Customers In September 2016, POA issued TFRS 15 Revenue from Contracts with Customers. The new standard issued includes the clarifying amendments to IFRS 15 made by IASB in April 2016. The new five-step model in the standard provides the recognition and measurement requirements of revenue. The standard applies to revenue from contracts with customers and provides a model for the sale of some non-financial assets that are not an output of the entity’s ordinary activities (e.g., the sale of property, plant and equipment or intangibles). TFRS 15 effective date is January 1, 2018, with early adoption permitted. Entities will transition to the new standard following either a full retrospective approach or a modified retrospective approach. The modified retrospective approach would allow the standard to be applied beginning with the current period, with no restatement of the comparative periods, but additional disclosures are required. The Group is in the process of assessing the impact of the standard on financial position or performance of the Group.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(13)

2. Basis of presentation of financial statements (continued) 2.2 Amendments in accounting policies (continued) TFRS 9 Financial Instruments In January 2017, POA issued the final version of TFRS 9 Financial Instruments. The final version of TFRS 9 brings together all three aspects of the accounting for financial instruments project: classification and measurement, impairment and hedge accounting. TFRS 9 is built on a logical, single classification and measurement approach for financial assets that reflects the business model in which they are managed and their cash flow characteristics. Built upon this is a forward-looking expected credit loss model that will result in more timely recognition of loan losses and is a single model that is applicable to all financial instruments subject to impairment accounting. In addition, TFRS 9 addresses the so-called ‘own credit’ issue, whereby banks and others book gains through profit or loss as a result of the value of their own debt falling due to a decrease in credit worthiness when they have elected to measure that debt at fair value. The Standard also includes an improved hedge accounting model to better link the economics of risk management with its accounting treatment. TFRS 9 is effective for annual periods beginning on or after 1 January 2018, with early application permitted by applying all requirements of the standard. Alternatively, entities may elect to early apply only the requirements for the presentation of gains and losses on financial liabilities designated as FVTPL without applying the other requirements in the standard. The Group is in the process of assessing the impact of the standard on financial position or performance of the Group iii) The new standards, amendments and interpretations that are issued by the International

Accounting Standards Board (IASB) but not issued by Public Oversight Authority (POA) The following standards, interpretations and amendments to existing IFRS standards are issued by the IASB but not yet effective up to the date of issuance of the financial statements. However, these standards, interpretations and amendments to existing IFRS standards are not yet adapted/issued by the POA, thus they do not constitute part of TFRS. The Group will make the necessary changes to its consolidated financial statements after the new standards and interpretations are issued and become effective under TFRS. IFRS 10 and IAS 28: Sale or Contribution of Assets between an Investor and its Associate or Joint Venture (Amendments) In December 2015, the IASB postponed the effective date of this amendment indefinitely pending the outcome of its research project on the equity method of accounting. Early application of the amendments is still permitted. Annual Improvements – 2010–2012 Cycle IFRS 13 Fair Value Measurement

As clarified in the Basis for Conclusions short-term receivables and payables with no stated interest rates can be held at invoice amounts when the effect of discounting is immaterial. The amendment is effective immediately.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(14)

2. Basis of presentation of financial statements (continued) 2.2 Amendments in accounting policies (continued) Annual Improvements – 2011–2013 Cycle IFRS 16 Leases The IASB has published a new standard, IFRS 16 'Leases'. The new standard brings most leases on-balance sheet for lessees under a single model, eliminating the distinction between operating and finance leases. Lessor accounting however remains largely unchanged and the distinction between operating and finance leases is retained. IFRS 16 supersedes IAS 17 'Leases' and related interpretations and is effective for periods beginning on or after January 1, 2019, with earlier adoption permitted if IFRS 15 'Revenue from Contracts with Customers' has also been applied. The Group is in the process of assessing the impact of the standard on financial position or performance of the Group. IAS 12 Income Taxes: Recognition of Deferred Tax Assets for Unrealised Losses (Amendments) The IASB issued amendments to IAS 12 Income Taxes. The amendments clarify how to account for deferred tax assets related to debt instruments measured at fair value. The amendments clarify the requirements on recognition of deferred tax assets for unrealised losses, to address diversity in practice. These amendments are to be retrospectively applied for annual periods beginning on or after January 1, 2017 with earlier application permitted. However, on initial application of the amendment, the change in the opening equity of the earliest comparative period may be recognised in opening retained earnings (or in another component of equity, as appropriate), without allocating the change between opening retained earnings and other components of equity. If the Group applies this relief, it shall disclose that fact. The Group is in the process of assessing the impact of the amendments on financial position or performance of the Group. IAS 7 Statement of Cash Flows (Amendments) The IASB issued amendments to IAS 7 'Statement of Cash Flows'. The amendments are intended to clarify IAS 7 to improve information provided to users of financial statements about an entity's financing activities. The improvements to disclosures require companies to provide information about changes in their financing liabilities. These amendments are to be applied for annual periods beginning on or after January 1, 2017 with earlier application permitted. When the Group first applies those amendments, it is not required to provide comparative information for preceding periods. The Group is in the process of assessing the impact of the amendments on financial position or performance of the Group.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(15)

2. Basis of presentation of financial statements (continued) 2.2 Amendments in accounting policies (continued) IFRS 2 Classification and Measurement of Share-based Payment Transactions (Amendments) The IASB issued amendments to IFRS 2 Share-based Payment, clarifying how to account for certain types of share-based payment transactions. The amendments, provide requirements on the accounting for: a. the effects of vesting and non-vesting conditions on the measurement of cash-settled share-based payments; b. share-based payment transactions with a net settlement feature for withholding tax obligations; and c. a modification to the terms and conditions of a share-based payment that changes the classification of the transaction from cash-settled to equity-settled. These amendments are to be applied for annual periods beginning on or after 1 January 2018. Earlier application is permitted. The amendment are not applicable for the Group and will not have an impact on the financial position or performance of the Group. IFRS 4 Insurance Contracts (Amendments)

In September 2016, the IASB issued amendments to IFRS 4 Insurance Contracts. The amendments introduce two approaches: an overlay approach and a deferral approach. The amended Standard will: - give all companies that issue insurance contracts the option to recognise in other comprehensive income, rather than profit or loss, the volatility that could arise when IFRS 9 Financial instruments is applied before the new insurance contracts Standard is issued; and - give companies whose activities are predominantly connected with insurance an optional temporary exemption from applying IFRS 9 Financial instruments until 2021. The entities that defer the application of IFRS 9 Financial instruments will continue to apply the existing financial instruments Standard—IAS 39. These amendments are to be applied for annual periods beginning on or after 1 January 2018. Earlier application is permitted. The amendment are not applicable for the Group and will not have an impact on the financial position or performance of the Group. IAS 40 Investment Property: Transfers of Investment Property (Amendments)

The IASB issued amendments to IAS 40 'Investment Property '. The amendments state that a change in use occurs when the property meets, or ceases to meet, the definition of investment property and there is evidence of the change in use. These amendments are to be applied for annual periods beginning on or after 1 January 2018. Earlier application is permitted. The Group is in the process of assessing the impact of the amendments on financial position or performance of the Group.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(16)

2. Basis of presentation of financial statements (continued) 2.2 Amendments in accounting policies (continued) IFRIC 22 Foreign Currency Transactions and Advance Consideration The interpretation clarifies the accounting for transactions that include the receipt or payment of advance consideration in a foreign currency. The Interpretation states that the date of the transaction for the purpose of determining the exchange rate to use on initial recognition of the related asset, expense or income is the date on which an entity initially recognises the non-monetary asset or non-monetary liability arising from the payment or receipt of advance consideration. An entity is not required to apply this Interpretation to income taxes; or insurance contracts (including reinsurance contracts) it issues or reinsurance contracts that it holds. The interpretation is effective for annual reporting periods beginning on or after 1 January 2018. Earlier application is permitted. The Group is in the process of assessing the impact of the amendments on financial position or performance of the Group.

Annual Improvements to IFRSs - 2014-2016 Cycle The IASB issued Annual Improvements to IFRS Standards 2014–2016 Cycle, amending the following standards: - IFRS 1 First-time Adoption of International Financial Reporting Standards: This amendment

deletes the short-term exemptions about some IFRS 7 disclosures, IAS 19 transition provisions and IFRS 10 Investment Entities. These amendments are to be applied for annual periods beginning on or after 1 January 2018.

- IFRS 12 Disclosure of Interests in Other Entities: This amendment clarifies that an entity is not

required to disclose summarised financial information for interests in subsidiaries, associates or joint ventures that is classified, or included in a disposal group that is classified, as held for sale in accordance with IFRS 5 Non-current Assets Held for Sale and Discontinued Operations. These amendments are to be applied for annual periods beginning on or after 1 January 2017.

- IAS 28 Investments in Associates and Joint Ventures: This amendment clarifies that the election

to measure an investment in an associate or a joint venture held by, or indirectly through, a venture capital organisation or other qualifying entity at fair value through profit or loss applying IFRS 9 Financial Instruments is available for each associate or joint venture, at the initial recognition of the associate or joint venture. These amendments are to be applied for annual periods beginning on or after 1 January 2018. Earlier application is permitted.

The Group is in the process of assessing the impact of the amendments on financial position or performance of the Group.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(17)

2. Basis of presentation of financial statements (continued) 2.3 Summary of significant accounting policies Offsetting Financial assets and liabilities are offset and the net amount reported in the balance sheet when there is a legally enforceable right to set off the recognized amounts and there is an intention to settle on a net basis, or realize the asset and settle the liability simultaneously. Assets used in operational leasing In the case of the operating lease the economic ownership of the object of the lease remains with the lessor. Assets used in operational lease, which consist of chemical tankers, are carried at cost less straight-line depreciation. Depreciation is calculated on a pro rata basis at rates based on the fair value (30 years) of assets after deducting the residual value (15%) of the assets. The depreciable amount of an asset used in operational lease is the cost of the asset less its residual value, which is determined as the expected market value at the end of the leasing period. The residual value represents the net amount which the enterprise expects to obtain from an asset at the end of its useful life after deducting the expected costs of disposal. Residual values are initially recorded based on appraisals and estimates. Realisation of the residual values is dependent on the Group’s future ability to market the vehicles under the prevailing market conditions. Management reviews residual values periodically to determine that recorded amounts are appropriate and if expectations differ from previous estimates, the change is accounted for as a change in accounting estimate. Cash and cash equivalents Cash and cash equivalents comprise cash on hand and demand deposits and other short-term highly liquid investments which their maturities are three months or less from date of acquisition and readily convertible to a known amount of cash and are subject to an insignificant risk of changes in value. If the amount of impairment decreases subsequent to a write-down, the amount of impairment reversal is reflected in other income in the current period. Inventories Inventories are stated at the lower of cost and net realizable value. Expenses incurred to bring the inventories to their present conditions are recognized in accordance with the following method. Raw materials and supplies - The cost of raw materials and supplies, is determined by the weighted average method. Finished and semi-finished products - Direct material and labour costs, variable and fixed production overheads in certain proportions (considering normal operating capacity) were included. Inventory valuation is determined using the weighted average method. Net realizable value is the estimated via determination of selling price in the ordinary course of business, less the estimated costs of completion and estimated costs necessary to make the sale.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(18)

2. Basis of presentation of financial statements (continued) 2.3 Summary of significant accounting policies Tangible assets Except for the land and buildings held for use, property, plant and equipment are carried at cost deducted by accumulated depreciation. The Company recognized land and buildings in the financial statements according to their fair values determined by the CMB approved real estate valuation experts. Increases resulting from the revaluation of assets held for use held at carrying values are classified under "revaluation funds” in shareholders' equity, impairments of the same assets’ value following the increase in value in prior years due to revaluation are netted off from revaluation funds and any other remaining decreases in value are reflected to the income statement. For each reporting period, the difference between depreciation expense calculated over restated value of assets and the depreciation expense calculated over the assets’ value prior to revaluation (charged to the income statement), is transferred from revaluation fund to retained earnings. Depreciation is recognized, either, over the adjusted costs of property, plant and equipment or restated balances on a straight-line basis over the economic useful lives. The estimated economic useful lives for property, plant and equipment are as follows: Years Land improvements 10-30 Buildings 10-50 Machinery and equipment 3-20 Vehicles 4-10 Fixture and furnitures 3-19 In the event of circumstances indicating that impairment has occurred in the tangible assets, an inspection is performed with the purpose of determining a possible impairment, and if the registered value of the tangible asset is higher than its recoverable value, the registered value is reduced to its recoverable value by reserving a provision. Gains/loss due to disposal of tangible assets are accounted in income statement in the event of revalued property disposal, the balance booked under “revaluation fund” is transferred to retained earnings account.(Note 11). Non-current assets held for sale Tangible assets or group of assets, meeting the criteria to be classified as held for sale, are measured at the lower of cost or fair value less costs to sell.Non current assets held for sale are not depreciated. Intangible assets Intangible assets comprise acquired intellectual property and computer software. They are recorded at acquisition cost and amortized on a straight-line basis over their estimated economic lives for a period not exceeding 5 years from the date of acquisition. Where an indication of impairment exists, the carrying amount of any intangible asset is assessed and written down immediately to its recoverable amount (Note 12).

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(19)

2. Basis of presentation of financial statements (continued) 2.3 Summary of significant accounting policies Research and development expenses Research expenses are recognized in comprehensive income statement in the period they are incurred. Intangible assets resulting from development activities (or within the development of a project within the group as a by-product) are recognized in the financial statements, only if all of the following criteria are met.

• It is technically possible for the fixed asset to be finalized and made ready for sale.

• There is an intention of completing, utilizing and disposing the fixed asset • Whether the fixed asset is usable and merchantable.

• It is foreseeable that fixed asset is capable of providing a possible future gross economic benefit.

• There is a technical, financial and other resource that is suitable fort the completion, usage and trade of the fixed asset

• Whether the development cost is properly measurable during the development phase. Other development costs are recognized as expenses as they occur. Development costs that are recognized as expense within the prior period cannot be capitalised within the following year.

Financial assets Investments intended to be held for an indefinite period of time and which may be sold in response to needs for liquidity or changes in interest rates are classified as available-for-sale. These are included in non-current assets unless management has the expressed intention of holding the investments for less than 12 months from the balance sheet date or unless they will need to be sold to raise operating capital, in which case they are included in current assets. Management reviews the classification of these financial assets on a regular basis. All financial assets are initially carried at cost including acquisition costs related with investments. Financial assets are initially measured at cost values including the acquisition costs related to investment, which is the fair value of the cost. Financial instruments classified as assets held for sale after their recognition in the financial statements and have been valued at fair value as long as their fair value could be calculated reliably. Borrowings Fixed or determinable payments, which are not traded loans, are classified in this category. Loans are measured at amortized cost using the effective interest method, less any impairment losses.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(20)

2. Basis of presentation of financial statements (continued) 2.3 Summary of significant accounting policies Trade Receivables Trade receivables are recognized at invoice value and, subsequently, at amortized cost, with the deduction of provision for doubtful receivables, if present, determined by the effective interest rate method. Notes and checks that are classified under trade receivables are discounted using the effective interest rate method and carried at amortized cost. Provision for doubtful receivables is accounted, if there is a concrete indication that overdue receivables cannot be collected. The provision is the amount reserved which the Company’s management considers that it covers the risk due to economic conditions forecasted or possible future losses due to the nature of account. Collection of receivables that are determined to be completely impossible is completely written off from the records. Impairments in financial assets Financial asset are assessed, at each balance sheet date, to determine if there is any objective evidence that a financial asset or a group of financial assets is impaired. A financial asset or a group of financial assets is deemed to be impaired, if, and only if, there is objective evidence of impairment as a result of one or more events that had occurred after the initial recognition of the asset and that loss event has an impact on the estimated future cash flows of the financial asset or the group of financial assets that can be reliably estimated. For loans and receivables, impairment loss is measured as the difference between present value calculated via the discount of possible future cash flows using the financial asset’s effective rate of interest and the asset’s carrying amount. The Company monitors its receivables individually. In case, if it is realised that financial asset is uncollectable, the amount corresponding is written off as it is written of from the allowances, simultaneously. Changes in provisions are recognized in income statement. In case the fair value of available for sale financial assets are decreased beyond the cost value due to market fluctuations. While the Company considers whether there is an impairment of financial assets that should be related to the corresponding financial period’s results, it also considers whether impairments are substantial, permanent or not possible to be reverted in the long term and the performance of similar financial assets in the market. According to the accounting estimates and policies of the Company, in order for the financial assets’ impairments to be considered permanent or not possible to be reverted in the long term, a year must be past following the decrease of the market value of financial asset beyond the cost value. Trade and settlement date accounting All regular way financial asset purchase and sales are recognized at the date of the transaction, in other terms, the date the Company committed to purchase or sell. The mentioned purchases or sales are transactions which require the delivery of the financial assets within the time interval identified with the established practices and regulations in the market.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(21)

2. Basis of presentation of financial statements (continued) 2.3 Summary of significant accounting policies Financial liabilities Financial liabilities are recognized initially at fair value less their transaction costs and subsequently measured at their amortized cost determined via the interest expense calculated using effective interest rate. Effective interest rate method is the determination of amortized cost of financial liabilities and allocation of related interest expenses to corresponding period. Effective interest rate is the rate reducing the long term, or short term if conditions allow, expected cash payments to present value of the current financial liability within an expected life of the financial instrument.

Borrowings

Short and long term bank loans are stated at the value computed through addition of the principal amount and the interest expenses accrued as of the balance sheet date. Borrowings are recognized initially at proceeds received, net of transaction costs incurred. Borrowings are subsequently stated at amortized cost using the effective yield method; any difference between the proceeds and redemption value is recognized in the comprehensive income statement over the period of the borrowings. Borrowing costs arising from bank loans are charged to the comprehensive income statement when they are incurred unless they are incurred for acquisition of a qualifying asset.

Trade payables

Trade payables are recognized initially at fair value of and subsequently measured at amortized cost using the effective interest method. Financial lease operations

Lease – Company as Lessor

Leases which a significant portion of the risk and rewards of ownership belongs to the lessee are classified as financial leases but other leases are classified as operating leases. Financial lease receivables are recorded under the Company’s net investment item. Financial lease income is distributed to accounting periods as providing a fixed interest rate of return on the Company’s net financial leases investment. Operating leases incomes are recorded the income statement to use straight-line basis during the lease period. Initial direct costs that are incurred on realization and negotiation of leasing are included the cost of leased asset and they are amortized to use straight-line basis during the lease term. Lease – Company as Tenant

Leases which a significant portion of the risk and rewards of ownership belongs to the lessee are classified as financial leases but other leases are classified as operating leases Assets acquired by financial lease are capitalized using the fair value of asset at the date of lease or the lower of the present value of the minimum lease payments. The liability to the lessor, which is the same amount as it is capitalized before is showed as financial lease liability in the balance sheet. Financial lease payments are seperated as financial expense and principal payment providing the decrease in financial lease obligation so the calculation of interest is made by using the fixed interest rate through the rest of principal balance.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(22)

2. Basis of presentation of financial statements (continued) 2.3 Summary of significant accounting policies Financial expenses are recorded in the income statement in accordance with the Group’s general policy on borrowing. Operating lease payments (incentive received or to be received to occur the lease process from tenant is recorded in the income statement using straight-line basis during the term of lease.) are recorded in the income statement on straight-line basis during the period of lease. Recognition and derecognition of financial assets and liabilities The Group recognizes a financial asset or financial liability in its balance sheet when only when it becomes a party to the contractual provisions of the instrument. The Group derecognizes a financial asset or a portion of it only when the control on rights under the contract is discharged. The Group derecognizes a financial liability when the obligation under the liability is discharged or cancelled or expires.

Tax calculated on the basis of the Group’s earnings Tax provision is the aggregate amount of current period and deferred tax of tax reserves included in the determination of net profit or loss.

Deferred tax is recognized taking into account balance sheet liability method and tax impacts arising from temporary differences between values of assets and liabilities reflected in financial reporting and their bases included in legal tax calculation. Deferred tax liability is calculated over all taxable temporary differences.

Deferred income tax assets are recognised for all deductible temporary differences and unused tax losses, to the extent that it is probable that taxable profit will be available against which the deductible temporary differences can be utilized. The carrying amount of deferred income tax assets is reviewed by the Group at each balance sheet date and reduced to the extent that it is no longer probable that sufficient taxable profit will be available to allow all or part of the deferred income tax asset to be utilized.

Tax rates, anticipated to occur in periods in which the asset in question shall be realized and the liability shall be met, is calculated based on valid tax rates as of balance sheet date during the calculation of deferred tax assets and liabilities. Current Tax Current tax liability is calculated on taxable current period income .Taxable profit and profit in the income statement is different because of taxable profit excludes tax deductible items and taxable items in other years and items can not be deducted from taxes. The Group’s current tax liability has been calculated by using legalized or considerably legalized tax rate as of balance sheet date.

As of January 1, 2006, therefore, in Turkey, the corporation tax rate is 20% as of 2016 (2015: 20%). Corporate tax rate is applied to tax base, which shall be determined as a result of addition of expenses not deducted according to lax laws to commercial income of entities and deduction of exceptions (affiliation privilege, investment discount exception etc.) and discounts (e.g. R & D discount) included in related tax laws. Dividends paid to the resident institutions and the institutions working through local offices or representatives are not subject to withholding tax. Withholding tax rate on the dividend payments other than the ones paid to the non-resident institutions generating income in Turkey through their operations or permanent representatives and the resident institutions is 15%. Appropriation of the retained earnings to capital is not considered as profit distribution and therefore is not subject to withholding tax.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(23)

2. Basis of presentation of financial statements (continued) 2.3 Summary of significant accounting policies Long-term employee benefits

(a) Provision for employee termination benefits

In accordance with existing social legislation in Turkey, the Group is required to make lump-sum termination indemnities to each employee who has completed over one year of service with the Group and whose employment is terminated due to retirement or for reasons other than resignation or misconduct.

Provisions for employee benefits are recognized as a separate item under long-term liabilities in the balance sheet. (b) Defined contribution plans:

The Group pays contributions to the Social Security Institution on a mandatory basis. The Group has no further payment obligations once the contributions have been paid. The contributions are recognized as an employee benefit expense when they are due.

Foreign currency transactions Transactions denominated in foreign currencies have been translated into TL at the exchange rate of the date of the transaction. Foreign currency denominated assets and liabilities are valued at the exchange rate of the date of balance sheet and its translation difference arising are recognized the related income and expense accounts. The exchange rates used in the end of periods are as follows:

Date TL / US Dollar TL / Euro 31 December 2016 3,5192 3,7099 31 December 2015 2,9076 3,1776 Revenue recognition

Revenue is recorded when the amount of revenue can be measured reliably and it is probable that the economic benefits will flow to the company. Revenues are stated as net after deduction of discounts and value-added tax. The following criteria must be fulfilled to occur the revenue. Sales Income is recognised when the risk and benefit of sales of goods are transferred to the buyer and the amount of income is measured reliably. Net sales consist of the invoiced amount of sales after deduction of discounts, value-added tax and commissions.

Interest

Interest income is recognised using the effective interest rate until maturity.

Dividend

Income is recognised as shareholders have right to receive dividend.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(24)

2. Basis of presentation of financial statements (continued) 2.3 Summary of significant accounting policies Provisions, contingent liabilities and assets

Provisions

Provisions are recognized when the Group has a present obligation (legal or constructive) as a result of a past event, it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation and a reliable estimate can be made of the amount of the obligation. The provision is reflected as present value of expenses which is likely to be in the future at the balance sheet date in case of the significant depreciation in money in time. The increase in the provision is recorded as interest expense when the present value is used. Contingent liabilities and assets

Contingent liabilities are disclosed in notes rather than being included in financial statements. On the other hand, contingent assets are not included in financial statements and disclosed in notes if there is a strong probability to generate an economic return. Government grants and incentives

Government grants are recognized where there is reasonable assurance that the grant will be received and all attaching conditions will be complied with. When the grant relates to an expense item, it is recognized as income over the period necessary to match the grant on a systemic basis to the costs that it is intended to compensate. The Government grants relates to intangible assets are recognized as deferred income under the short and long term liabilities and the intangible assets’ depreciations are recognized by using straight-line method of depreciation in income statement during useful economic life. Restricted reserves

Restricted reserves are reserved set aside from the profit of the prior period for certain purposes (such as acquiring tax advantage from sale of associates) except dividend distribution and due to obligations arising from the laws or contracts. These reserves are shown on their statutory amounts. (Note 17). Earnings per share

Basic earnings per share are calculated by dividing the net profit by the weighted average number of ordinary shares outstanding during the year. The companies can increase their share capital by making a pro-rata distribution of shares (“Bonus Shares”) to existing shareholders in Turkey. For the purpose of the earnings per share calculation such Bonus Share issues are regarded as stock dividends. Accordingly, the weighted average number of shares used in earnings per share calculation is derived by giving retroactive effect to the issue of such shares. There was no difference in basis and relative earnings per share any period. Subsequent events Subsequent events comprise all events occurred between the date of authorization of the financial statements for issuance and the balance sheet date. The subsequent events that does not require amendment are disclosed in notes based on materiality level.

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(25)

2. Basis of presentation of financial statements (continued) 2.3 Summary of significant accounting policies Impairment of financial assets At each reporting date, the Company assesses whether there is any indication that carrying value of assets except financial assets and deferred tax assets is impaired or not. When an indicator of impairment exists, the Company estimates the recoverable values of such assets. When individual recoverable value of assets cannot be measured, recoverable value of cash generating unit of that asset is measured. Recoverable amount is the higher of net selling price or value in use. The value in use is discounted to its present value using future cash flows and discount rate before tax that has risk about asset. The main assumptions used are inflation expectations of following years, expected increase in sales and costs and expected growth rate of country. When recoverable amount of an asset (or a cash generating unit) is lower than its carrying value, the asset’s carrying value is reduced to its recoverable amount. An impairment loss is recognized immediately in the comprehensive income statement. An impairment loss recognized in prior periods for an asset is reversed if the subsequent increase in the asset’s recoverable amount is caused by a specific event since the last impairment loss was recognized. Such a reversal amount cannot be higher than the previously recognized impairment and is recognized as income in the financial statements. Related parties a) A person or a close member of that person's family is related to a reporting entity if that person:

(i) has control or joint control over the reporting entity, (ii) has significant influence over the reporting entity; or (iii) is a member of the key management personnel of the reporting entity or of a parent of the

reporting entity. b) The entity and the reporting entity are members of the same group (which means that each

parent, subsidiary and fellow subsidiary is related to the others).

(i) Entity and the Company are the members of same group, (ii) One entity is an associate or joint venture of the other entity (or an associate or joint

venture of a member of a group of which the other entity is a member), (iii) Both entities are joint ventures of the same third party, (iv) One entity is a joint venture of a third entity and the other entity is an associate of the

third entity, (v) The entity is a post-employment benefit plan for the benefit of employees of either the

reporting entity or an entity related to the reporting entity. If the reporting entity is itself such a plan, the sponsoring employers are also related to the reporting entity.

(vi) The entity is controlled or jointly controlled by a person identified in (a). (vii) A person identified in (a) (i) has significant influence over the entity or is a member of the

key management personnel of the entity (or of a parent of the entity).

(Convenience translation of financial statements originally issued in Turkish (See Note 2))

Bossa Ticaret ve Sanayi İşletmeleri T. Anonim Şirketi

Notes to the financial statements as of December 31, 2016 (continued) (Currency –Turkish Lira (TL) unless otherwise indicated)

(26)

2. Basis of presentation of financial statements (continued) 2.3 Summary of significant accounting policies (continued)

Financial instruments A financial instrument is any contract that gives rise to both a financial asset of one enterprise and a financial liability or equity instrument of another enterprise. A financial asset is any asset that is:

cash, a contractual right to receive cash or another financial asset from another enterprise,

a contractual right to exchange financial instruments from another enterprise under conditions that are potentially favourable, or;

an equity instrument of another enterprise.

A financial liability that is a contractual obligation:

to deliver cash or another financial asset to another enterprise, or

to exchange financial instruments with another enterprise under conditions those are potentially

unfavourable.