continuing education certificate participant directory ...€¦ · continuing education certificate...

TRANSCRIPT

Finance and Business Skills for Nurse Leaders September 1, 2016

Continuing Education Certificate Participant Directory PowerPoint Presentation

The American Organization of Nurse Executives

CONTINUING EDUCATION CERTIFICATE

The American Organization of Nurse Executives (AONE) is accredited as a provider of continuing nursing education by the American Nurses Credentialing Center’s Commission on Accreditation. Program: Finance and Business Skills for Nurse Leaders Date: September 1, 2016 Place: American Organization of Nurse Executives (AONE)

155 N. Wacker Drive, Suite 400 Chicago, IL 60606

Provider: American Organization of Nurse Executives (AONE) 155 N. Wacker Drive, Suite 400 Chicago, IL 60606

This is to certify that:

__________________________________________(Name of Learner) has attended and completed a continuing professional education program and earned a total of 7.0 Continuing Education Contact Hours. The American Organization of Nurse Executives is accredited as a provider of continuing nursing education by the American Nurses Credentialing Center's Commission on Accreditation. .

Finance & Business Skills for Nurse Leaders September 1, 2016 – Chicago, IL

Participant Directory Denise Banton

Rush University Medical Center

Chicago, IL

Jason Bauer

Clinical Manager

SwedishAmerican ‐ A Division of UW Health

Rockford, IL

Mary Becker‐Roth

Patient Care Manager

Aurora St. Luke's Medical Center

Whitefish Bay, WI

mary.becker‐[email protected]

Jennifer Beyer

Centegra Hospital ‐ McHenry

McHenry, IL

Jennifer Blissitt

Nurse Manager, Access and Coordination

Froedtert Health

Milwaukee, WI

Beth Bradley

MSN, RN

Penn State Hershey Medical Center

Hershey, PA

Christopher Callahan

Nurse Manager

Massachusetts General Hospital

North Reading, MA

Cristina Canaria

Aliso Viejo, CA

Ann Caughron

Dir, Nursing

Presbyterian Homes

Evanston, IL

Scott Christensen

University of Utah Health Care ‐ Hospital and

Clinics

Salt Lake City, UT

Dawn Clayburn

Morris Hospital & Healthcare Centers

Coal City, IL

Kimberly Cleveland

Canal Fulton, OH

George Daly

Nurse Manager

The University of Chicago Medicine

Chicago, IL

Ashley Davis

Clinical Manager

Riley Hospital for Children at Indiana University

Health

Indianapolis, IN

Teresa De Los Santos

Chicago, IL

Belinda Frazee

Rushville, IN

Finance & Business Skills for Nurse Leaders September 1, 2016 – Chicago, IL

Participant Directory Nicole Geist

Registered Nurse Associate Partner,

Supplemental Associate Administrator

Riley Hospital for Children at Indiana University

Health

Westfield, IN

Matthew Getsinger

OHSU Hospital

Newberg, OR

Jane Gustafson

Manager

Aurora Medical Center

Kenosha, WI

Karen Hardin

Assistant Professor, School of Nursing

Anderson University

Anderson, SC

Joey Hollis

Franklin, IN

Denise Hong

Chicago, IL

Belinda Hopper

Janesville, WI

Rebekah Hopper

Dir, Med/Surg

SwedishAmerican ‐ A Division of UW Health

Rockford, IL

Karen Hunt

Nurse Manager

Franciscan St Francis Health

Indianapolis, IN

Lynn Lawson

Carmel, IN

Kelly Magee

Manager

Aurora Medical Center

Kenosha, WI

Cara Marco

Morris Hospital & Healthcare Centers

Morris, IL

Jennifer McMillan

Manager

Aurora Medical Center

Kenosha, WI

Julie Monville

Ironwood, MI

Cathleen Mullane

NorthShore University Health System

Park Ridge, IL

Kate ONeill

CNO and VP of Quality Patient Safety

Springfield, PA

Yolanda Penny

Director of Nursing

St. Bernard Hospital and Health Care Center

Chicago, IL

Finance & Business Skills for Nurse Leaders September 1, 2016 – Chicago, IL

Participant Directory Tracey Peterson

Penn State Hershey Health System

Lebanon, PA

Nancy Pope‐Angulo

Walnut Creek, CA

nancy.pope‐[email protected]

Kathryn Roberts

Children's Hospital of Philadelphia

Philadelphia, PA

James Sturtevant

Truckee, CA

Roberta Szumski

Manager Nursing Education

Riley Hospital for Children Indiana University

Health

Avon, IN

Greg Taylor

Patient Care Manager

Aurora Health Care

Milwaukee, WI

Ann Vallone

Nurse Manager, Cancer Center Clinics

Froedtert Health

Milwaukee, WI

Ron Yolo

Long Beach, CA

1

©AONE

Finance and

Business Skills for

Nurse Leaders

Jan Phillips, DNP, RN, CENP

Director, Nursing‐ Adult Acute Care, Emergency Services & Care Transitions

PennState Hershey Medical Center

Chuck Alsdurf, MAcc, CPA

Director, Healthcare Finance Policy, Operational Initiatives

Healthcare Financial Management Association (HFMA) September 1, 2016

©AONE©AONE

The pressure is too much to bear alone

2

©AONE©AONE

Together we can get through this and succeed!

©AONE©AONE

Realignment Is Erasing Traditional Healthcare Boundaries

Driven by demands for care transformation, the healthcare industry is realigning at an an unprecedented pace.

The Triple Aim framework was developed by the Institute for Healthcare Improvement in Cambridge, Mass. (www.ihi.org).

SHARED GOAL

3

©AONE©AONE

Collaboration required for quality care

©AONE©AONE

Collaboration required for success

Nursing controls substantial resources and related costs

+Resource and cost management is critical part of value based model

Nursing and Finance need to become BFFs

$

4

©AONE

Open Questions

Now that we’ve answered the “why” collaboration is necessary, here

are a few questions to think about:

– What obstacles exist within your organization that prevent or

inhibit collaboration? How can those be overcome?

– What can finance do to better support the clinicians?

– What can clinicians do to better communicate their needs and

challenges to finance?

– What gaps still exist?

©AONE

Healthcare Reform Update

5

©AONE

Survey Question

When you read or hear ‘Healthcare Reform’ what initially comes to mind?

A. The Affordable Care Act

B. Opportunity to improve healthcare

C. Not sure what to think

D. Feels like we’re shuffling deck chairs on the Titanic

©AONE

Uninsured rates are decreasing…

6

©AONE

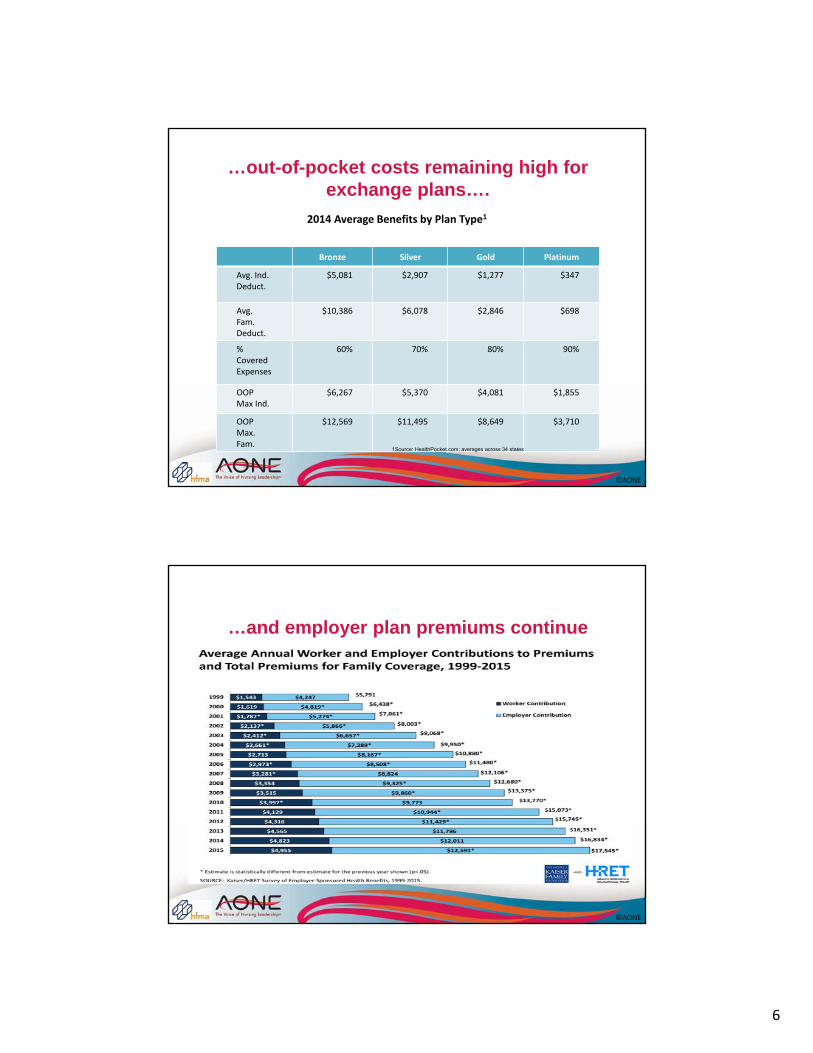

…out-of-pocket costs remaining high for exchange plans….

Bronze Silver Gold Platinum

Avg. Ind. Deduct.

$5,081 $2,907 $1,277 $347

Avg.Fam. Deduct.

$10,386 $6,078 $2,846 $698

% Covered Expenses

60% 70% 80% 90%

OOP Max Ind.

$6,267 $5,370 $4,081 $1,855

OOP Max. Fam.

$12,569 $11,495 $8,649 $3,710

2014 Average Benefits by Plan Type1

1Source: HealthPocket.com; averages across 34 states

©AONE

…and employer plan premiums continue to climb…

7

©AONE

…and even those insured are challenged to pay bills…

©AONE

…with varying levels of knowledge…

Nongroup Uninsured

84%60%

Very or Somewhat Confident in Understanding of the Term:

“Deductible”

Nongroup: Nonelderly adults currently purchasing individual coverage and not eligible to buy health insurance through an employer or other group.Source: Urban Institute Health Policy Center ‐ Health Reform Monitoring Survey, 2013

8

©AONE

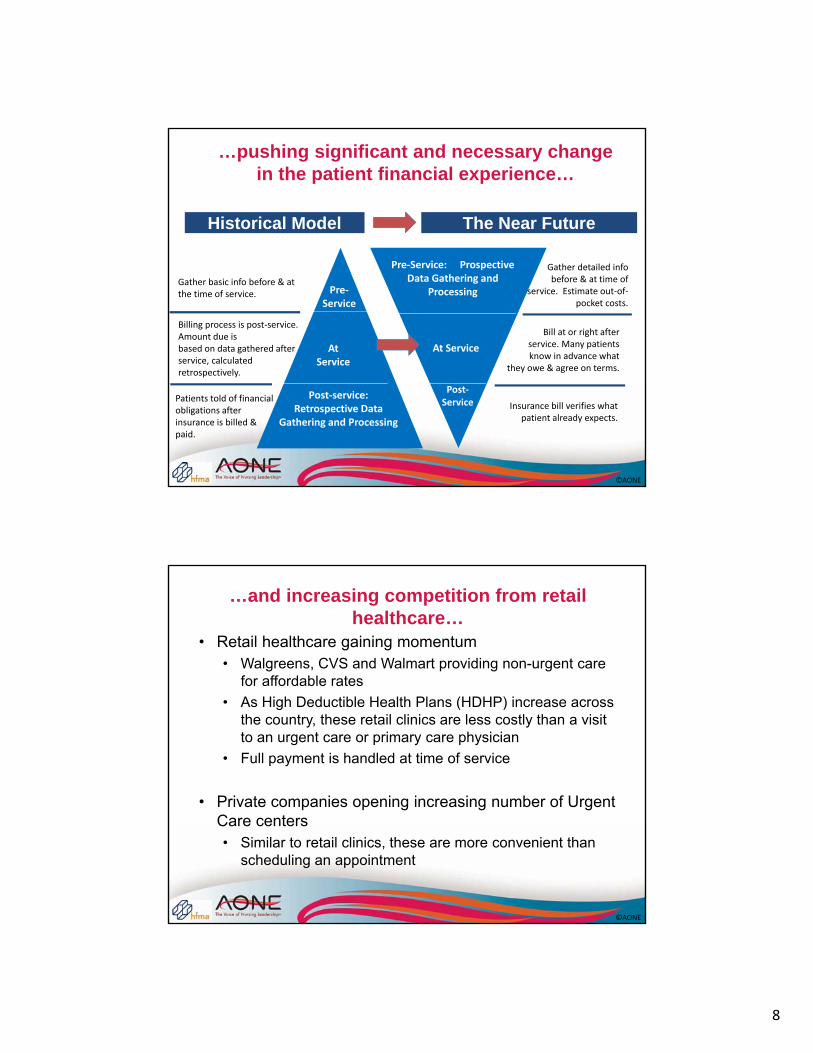

…pushing significant and necessary change in the patient financial experience…

Historical Model The Near Future

Gather basic info before & at the time of service.

Billing process is post‐service. Amount due isbased on data gathered after service, calculated retrospectively.

Patients told of financial obligations after insurance is billed & paid.

Pre‐Service

At Service

Post‐service: Retrospective Data

Gathering and Processing

Pre‐Service: Prospective Data Gathering and

Processing

At Service

Post‐Service

Gather detailed infobefore & at time of

service. Estimate out‐of‐pocket costs.

Bill at or right afterservice. Many patientsknow in advance what

they owe & agree on terms.

Insurance bill verifies whatpatient already expects.

©AONE

…and increasing competition from retail healthcare…

• Retail healthcare gaining momentum• Walgreens, CVS and Walmart providing non-urgent care

for affordable rates

• As High Deductible Health Plans (HDHP) increase across the country, these retail clinics are less costly than a visit to an urgent care or primary care physician

• Full payment is handled at time of service

• Private companies opening increasing number of Urgent Care centers• Similar to retail clinics, these are more convenient than

scheduling an appointment

9

©AONE

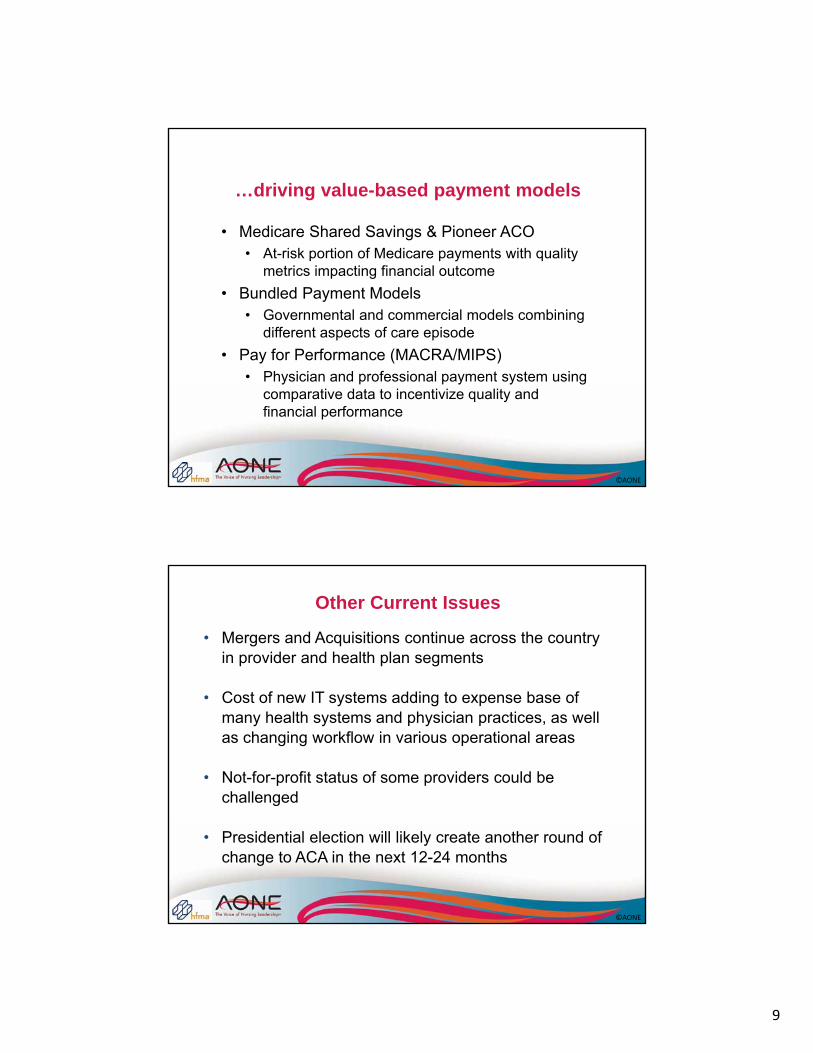

…driving value-based payment models

• Medicare Shared Savings & Pioneer ACO• At-risk portion of Medicare payments with quality

metrics impacting financial outcome

• Bundled Payment Models• Governmental and commercial models combining

different aspects of care episode

• Pay for Performance (MACRA/MIPS)• Physician and professional payment system using

comparative data to incentivize quality and financial performance

©AONE

Other Current Issues

• Mergers and Acquisitions continue across the country in provider and health plan segments

• Cost of new IT systems adding to expense base of many health systems and physician practices, as well as changing workflow in various operational areas

• Not-for-profit status of some providers could be challenged

• Presidential election will likely create another round of change to ACA in the next 12-24 months

10

©AONE

Items to Consider

• Healthcare reform has impacted uninsured rates as well as out-of-pocket costs for consumers

• Education and communication are critical for both providers and patients

• The payment models will evolve and vary depending on payer, providers and type of service

• Managing the efficient delivery, cost, and quality of care will be key to success as additional risk shifts to providers

©AONE

Challenges Ahead

• Aligning goals amongst providers delivering services

• Measuring current cost of delivering services

• Delivering care at a lower cost

• Changes in risk pool of patients receiving bundled services

• Accuracy and timeliness of performance data

11

©AONE

Volume to Value

Does Not Mean Volume is Bad

©AONE

Overview

• Trend Drivers

• FFS to Outcomes Based Payment

• ACO and Bundled Payment Contracts

• Impact on Nursing

12

©AONE

The Federal Deficit is Impacting FFS Payment Growth

Long‐Term Federal Fiscal Imbalances Are Driven by Healthcare and Retirement Programs…

…the CBO Projects Input Prices Will Grow Faster than Medicare Payments

‐19.0%

‐17.0%

‐15.0%

‐13.0%

‐11.0%

‐9.0%

‐7.0%

‐5.0%

‐3.0%

‐1.0%

1.0%

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Illustrative Hospital Medicare Margin Impact:CBO Projections of Growth in Medicare Pymt and Input Prices

Sources:1) 2014 Margin: MedPAC; Assessing Payment Adequacy and Updating Payments: Hospital Inpatient and Outpatient Services; December 10, 20152) Growth in Medicare Revenue and Input Prices: The Congressional Budget Office Economic Outlook: 2016 – 2026, pg 673) HFMA Analysis

CBO Projection

©AONE©AONE

Health Costs Eating into Wages

$1,071

$4,955$5,179

$12,591

Single Coverage Family Coverage

Employer Contribution

Worker ContributionSOURCE: Kaiser/HRET Survey of Employer‐Sponsored Health Benefits, 1999‐2015. Bureau of Labor Statistics, Consumer Price Index, U.S. City Average of Annual Inflation (April to April), 1999‐2015; Bureau of Labor Statistics, Seasonally Adjusted Data from the Current Employment Statistics Survey, 1999‐2015 (April to April).

$6,251

$17,545

Health Insurance Costs Have Grown at an Unsustainable Rate, Depressing Employee Wages

Trends ‐ Employers

0%

200%

400%

1999 2003 2007 2011 2015

Health InsurancePremiums

Workers' Contribution toPremiums

221%

203%

56%

42%

13

©AONE©AONE

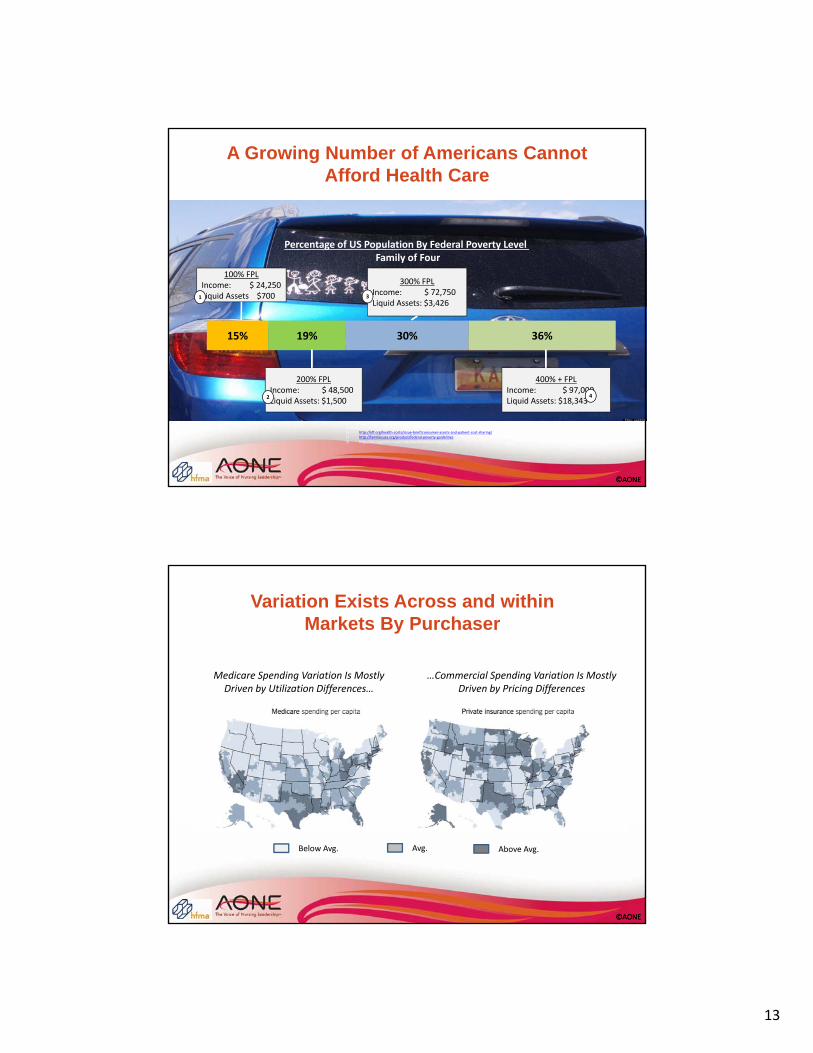

A Growing Number of Americans Cannot Afford Health Care

15% 19% 30% 36%

100% FPLIncome: $ 24,250 Liquid Assets $700

200% FPLIncome: $ 48,500 Liquid Assets: $1,500

300% FPLIncome: $ 72,750 Liquid Assets: $3,426

400% + FPLIncome: $ 97,000 Liquid Assets: $18,343

Percentage of US Population By Federal Poverty Level Family of Four

11

22

33

44

Sources:1) http://kff.org/health‐costs/issue‐brief/consumer‐assets‐and‐patient‐cost‐sharing/2) http://familiesusa.org/product/federal‐poverty‐guidelines3) http://kff.org/other/state‐indicator/distribution‐by‐fpl/

Trends ‐Families

©AONE©AONE

Trends ‐Variation

Below Avg. Avg. Above Avg.

Medicare Spending Variation Is Mostly Driven by Utilization Differences…

…Commercial Spending Variation Is Mostly Driven by Pricing Differences

Variation Exists Across and within Markets By Purchaser

14

©AONE©AONE

Implications

• Governmental Health Expenditures Are Crowding Out Investments in Other Areas Valued By Society

• Fee for Service in the Public Sector Is Unsustainable

• Even Insured “Middle Class” Families Would Struggle Financially if They Had a Significant Medical Event

• As a Result, Purchasers Are Looking to Reduce Both Unnecessary Utilization and Payment Rates

©AONE

Overview

• Trend Drivers

• FFS to Outcomes Based Payment

• ACO and Bundled Payment Contracts

• Impact on Nursing

15

©AONE

CMS’s Long‐Term Goal Is to Shift Providers to Prospective Population Based Payments

FFS to Outcomes

CMS’s Glide-Path to Outcomes Payment

©AONE

FFS to Outcomes

0%

20%

40%

Capitation

Partial Capitation

Shared Risk

FFS ‐ Shared Savings

Nationally, Only 20% of Commercial Payments Are Outcomes Based

Source: http://www.catalyzepaymentreform.org/news‐and‐publications/publications

% of Commercial Health Plan Revenue by Payment Mechanism

Slow Transition to Risk Based Payments

16

©AONE

FFS to Outcomes

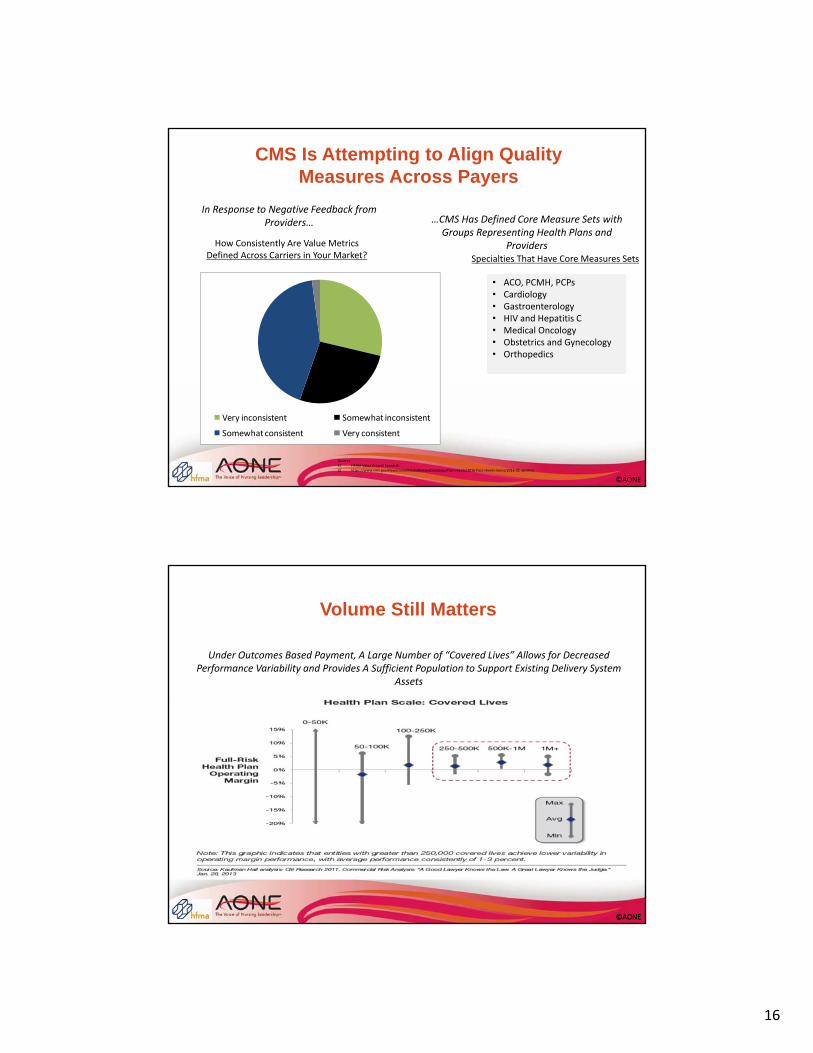

CMS Is Attempting to Align Quality Measures Across Payers

Very inconsistent Somewhat inconsistent

Somewhat consistent Very consistent

How Consistently Are Value Metrics Defined Across Carriers in Your Market?

In Response to Negative Feedback from Providers…

Sources:1) HFMA Value Project Research2) https://www.cms.gov/Newsroom/MediaReleaseDatabase/Fact‐sheets/2016‐Fact‐sheets‐items/2016‐02‐16.html

…CMS Has Defined Core Measure Sets with Groups Representing Health Plans and

Providers

• ACO, PCMH, PCPs• Cardiology• Gastroenterology• HIV and Hepatitis C• Medical Oncology• Obstetrics and Gynecology• Orthopedics

Specialties That Have Core Measures Sets

©AONE©AONE

FFS to Outcomes

Under Outcomes Based Payment, A Large Number of “Covered Lives” Allows for Decreased Performance Variability and Provides A Sufficient Population to Support Existing Delivery System

Assets

Volume Still Matters

17

©AONE©AONE

Implications

• Outcomes Risk Is Being Pushed to Delivery Systems, though It’s Occurring Slowing

• Many of the Models for Transferring Risk to Delivery Systems Are Experimental

• CMS Recognizes the Need to Align Efforts with the Private Sector but Hasn’t Done so on a Broad Scale Yet

• Volume (Lives under Management) Will Still Drive Profitability

©AONE

Overview

• Trend Drivers

• FFS to Outcomes Based Payment

• ACO and Bundled Payment Contracts

• Impact on Nursing

18

©AONE©AONE

From a Structural Perspective ACOs Can Include A Variety of Provider Types

Source: The Brookings Institute; Issue Brief: Accountable Care Organizations; March 2009

Examples of Different Combination of ACO Components

ACOs and Bundled Payment Contracts What is an ACO?

©AONE©AONE

Payment Models - Risk Varies

As ACOs Assume More Outcomes Risk, the Incentive to Redesign Care Delivery Increases

Risk Bearing Payment Models vs. Incentive to Redesign Care

Ince

nti

ve t

o R

edes

ign

C

are

De

live

ry

Degree of Risk Assumed by ACO

High

Low

Fee for Service w/

P4P

Shared Savings

Shared Savings/

Loss

Partial Capitation

Full Capitation

http://healthaffairs.org/blog/2015/06/16/the‐revised‐medicare‐aco‐program‐more‐options‐and‐more‐work‐ahead/

19

©AONE©AONE

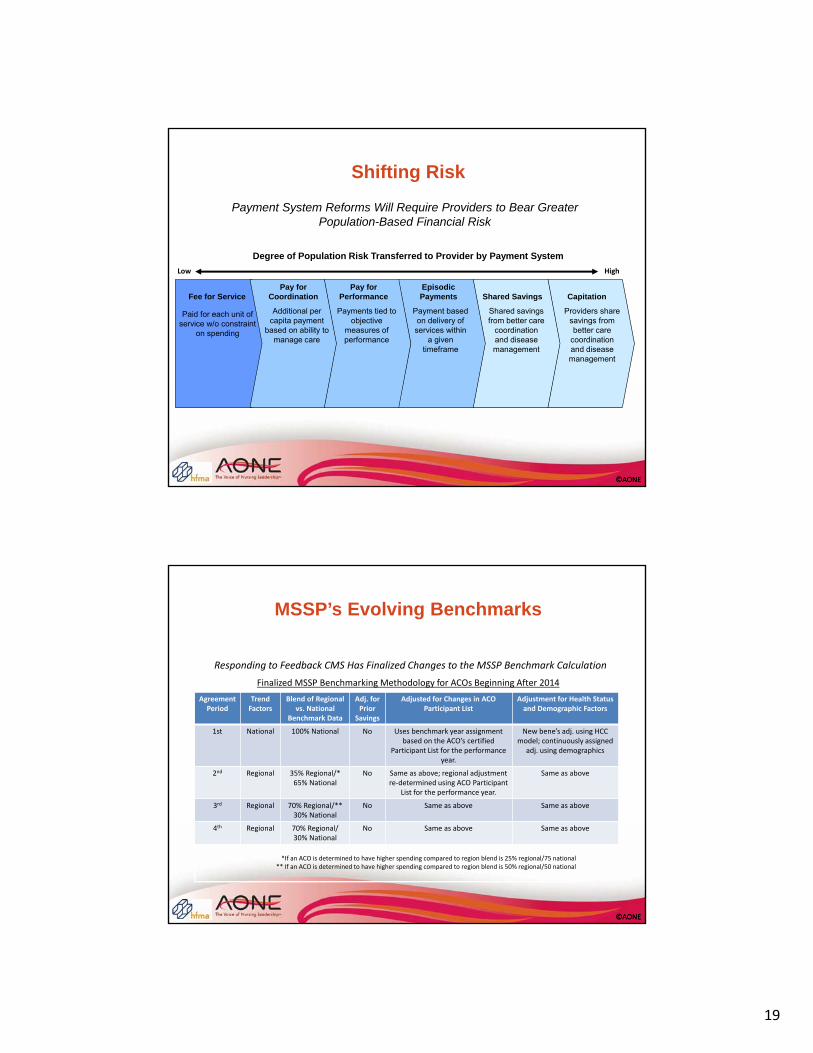

Shifting Risk

Capitation

Low

Pay forCoordination

Pay forPerformance

Episodic Payments Shared SavingsFee for Service

Additional per capita payment

based on ability to manage care

Payments tied to objective

measures of performance

Payment based on delivery of services within

a given timeframe

Shared savings from better care

coordination and disease management

Providers share savings from better care

coordination and disease management

High

Paid for each unit of service w/o constraint

on spending

Payment System Reforms Will Require Providers to Bear Greater Population-Based Financial Risk

Degree of Population Risk Transferred to Provider by Payment System

©AONE©AONE

MSSP’s Evolving Benchmarks

*If an ACO is determined to have higher spending compared to region blend is 25% regional/75 national ** If an ACO is determined to have higher spending compared to region blend is 50% regional/50 national

Responding to Feedback CMS Has Finalized Changes to the MSSP Benchmark Calculation

Finalized MSSP Benchmarking Methodology for ACOs Beginning After 2014

AgreementPeriod

Trend Factors

Blend of Regionalvs. National

Benchmark Data

Adj. for Prior

Savings

Adjusted for Changes in ACO Participant List

Adjustment for Health Status and Demographic Factors

1st National 100% National No Uses benchmark year assignment based on the ACO’s certified

Participant List for the performance year.

New bene’s adj. using HCC model; continuously assigned

adj. using demographics

2nd Regional 35% Regional/* 65% National

No Same as above; regional adjustment re‐determined using ACO Participant

List for the performance year.

Same as above

3rd Regional 70% Regional/** 30% National

No Same as above Same as above

4th Regional 70% Regional/ 30% National

No Same as above Same as above

20

©AONE©AONE

Definition and Purpose of Bundled Payments

Single payment for all services provided during the defined episode of care

• Typically less than the sum of the individual services

Creates a package for patient and payer simplifying billing and cost for these parties

Incent reduction in provider cost by shifting risk

• Should result in lower patient cost as well

Increase collaboration across hospitals, physicians, and post-acute providers

Improve patient outcomes and experience

©AONE

Current Models

• Reconciliation Model

• Billing practices remain the same

• Total savings or overages are determined after ‘performance period’

• If savings target achieved, payer sends payment to provider(s)

• If target not achieved, provider(s) send payment to payer

• Example: Comprehensive Joint Replacement (CJR) model

• Global Payment Model

• Consolidated claim/bill submitted

• Single episodic payment received by primary provider or ACO and then distributed amongst all providers for that episode

• Would require agreement with other providers in advance of care being provided

• System mechanics would need to be revised

Example: Medicare Acute Care Episode (ACE) model

21

©AONE

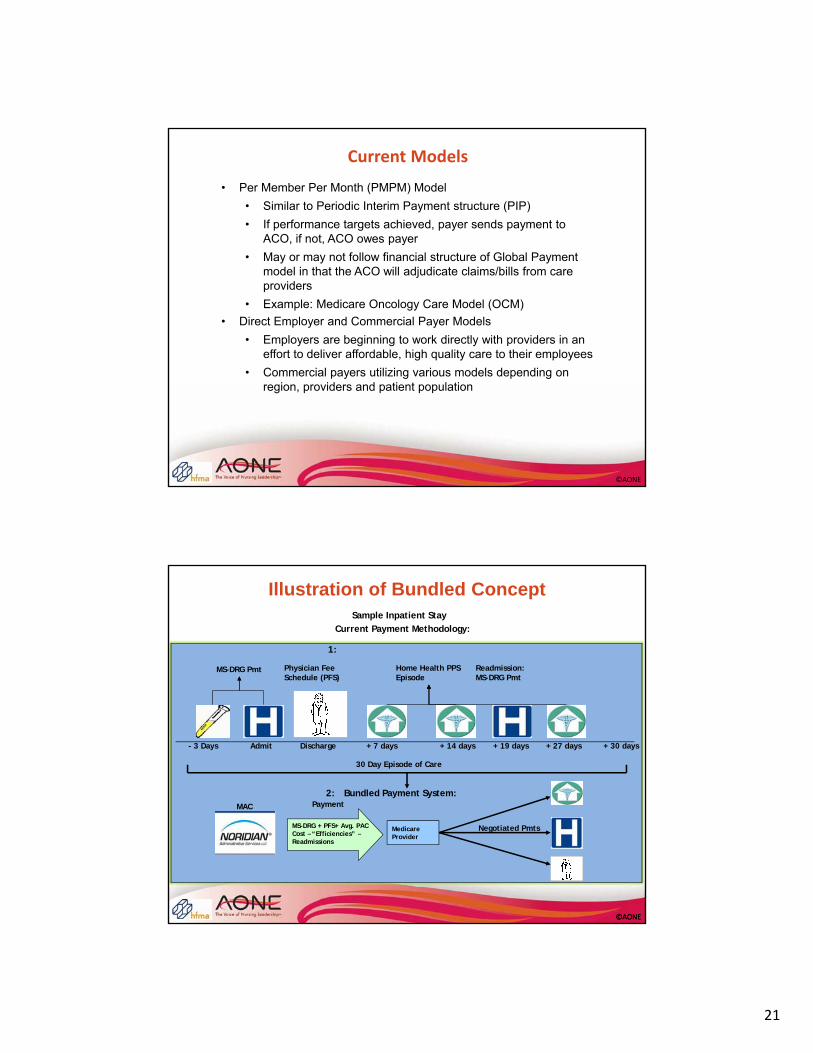

Current Models

• Per Member Per Month (PMPM) Model

• Similar to Periodic Interim Payment structure (PIP)

• If performance targets achieved, payer sends payment to ACO, if not, ACO owes payer

• May or may not follow financial structure of Global Payment model in that the ACO will adjudicate claims/bills from care providers

• Example: Medicare Oncology Care Model (OCM)

• Direct Employer and Commercial Payer Models

• Employers are beginning to work directly with providers in an effort to deliver affordable, high quality care to their employees

• Commercial payers utilizing various models depending on region, providers and patient population

©AONE©AONE

Bundled Payment System:

Current Payment Methodology:

1:

2:

- 3 Days Admit Discharge + 7 days + 14 days + 19 days + 30 days

MS-DRG Pmt Physician Fee Schedule (PFS)

Home Health PPS Episode

Readmission:MS-DRG Pmt

+ 27 days

30 Day Episode of Care

Sample Inpatient Stay

MAC

MS-DRG + PFS+ Avg. PAC Cost – “Efficiencies” –Readmissions

Negotiated Pmts

Payment

Medicare Provider

Illustration of Bundled Concept

22

©AONE©AONE

Volume Remains an Important Factor

Value: Public Payers

Not Surprisingly, the Bundled Payments for Care Improvement (BPCI) Episodes Including the Most Common MS‐DRGs Are the Most Prevalent

Source: CMS Innovation and Health Care Delivery System Reform, Amy Bassano, Director Patient Care Models Group, CMMI, Presentation to HFMA’s BPCI Council, June 22, 2015

©AONE©AONE

Direct Contracting with Centers of Excellence

Transplants

Cardiac Surgery

Spine Surgery

Cardiac Surgery

Sources:1) http://thehealthcareblog.com/blog/2012/10/18/walmart‐moves‐health‐care‐forward‐again/2) http://my.clevelandclinic.org/about‐cleveland‐clinic/newsroom/releases‐videos‐newsletters/lowes_expands_heart_healthcare_benefits

23

©AONE

Collaboration

• Relationships and agreements will need to be established for compliant and efficient operational and financial structures

• Need for infrastructure investments to support operational model necessary for high performance

• All providers involved in episode of care must work together to increase coordination and efficiency

• In addition, areas like finance, revenue cycle, and IT need to understand the challenges facing the clinicians to better support increased efficiency and innovation

©AONE

Impact on Nursing

• Innovation in nursing will be required for the industry to overcome the financial and operational challenges

• Short-term it will be painful for all as the primary resource in healthcare is labor and nursing comprises a large portion of this resource

• Long-term nursing will play a huge part in creating solutions

24

©AONE©AONE

Finance Fundamentals

©AONE

Discussion topics

• Hospital Financial Management

• Speaking the language

• Accounting & Financial Reporting

• Labor Budget Interactive Exercise

• Budgeting

• Financial Decision Support & Systems

• Key Takeaways

25

©AONE

Why do you need to know this?

• Developing nursing leaders/champions drive a culture of performance improvement

• Applying a shared language to discuss data

• Extending a business acumen that support strategies to convert financial and clinical data into action

• Helping support physicians to drive care delivery changes involving varying degrees of risk assumption

©AONE

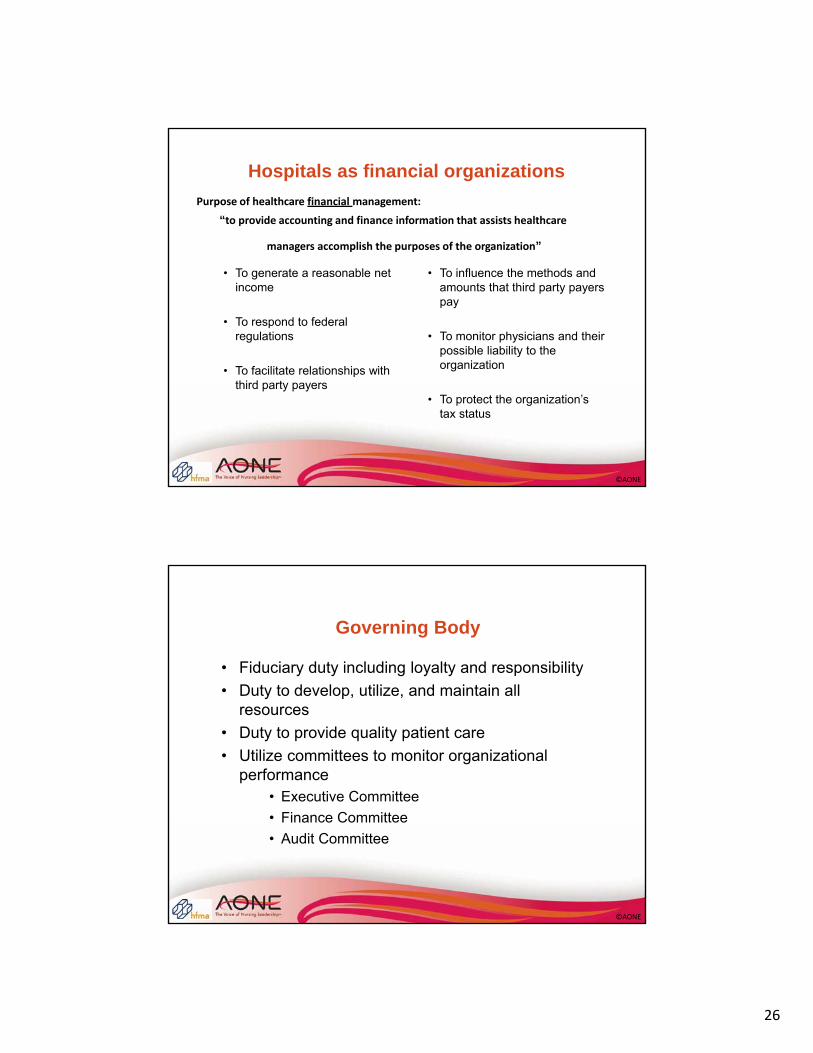

Hospitals as financial organizations

Purpose of healthcare management:

“to provide the community with the services it needs, at a clinically acceptable level of quality, at a publicly responsive level of amenity, at the least possible cost”

26

©AONE

Hospitals as financial organizations

• To generate a reasonable net income

• To respond to federal regulations

• To facilitate relationships with third party payers

• To influence the methods and amounts that third party payers pay

• To monitor physicians and their possible liability to the organization

• To protect the organization’s tax status

Purpose of healthcare financial management:

“to provide accounting and finance information that assists healthcare

managers accomplish the purposes of the organization”

©AONE

Governing Body

• Fiduciary duty including loyalty and responsibility

• Duty to develop, utilize, and maintain all resources

• Duty to provide quality patient care

• Utilize committees to monitor organizational performance

• Executive Committee

• Finance Committee

• Audit Committee

27

©AONE

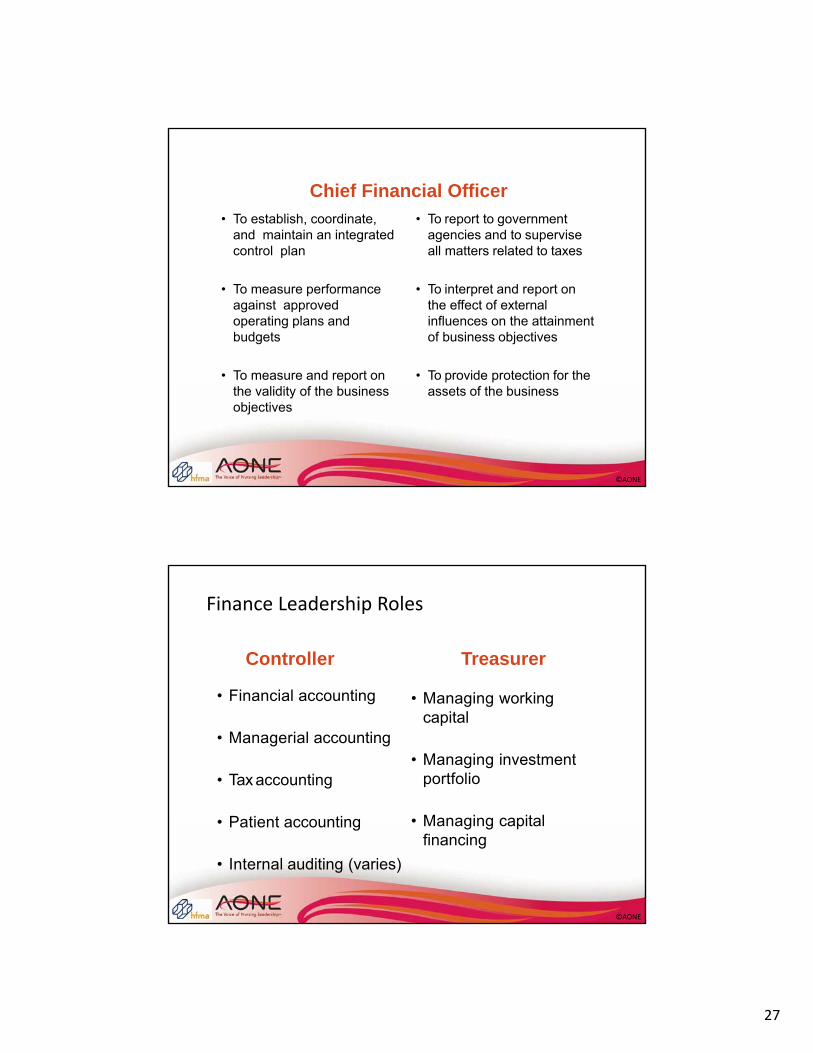

Chief Financial Officer

• To establish, coordinate, and maintain an integrated control plan

• To measure performance against approved operating plans and budgets

• To measure and report on the validity of the business objectives

10

• To report to government agencies and to supervise all matters related to taxes

• To interpret and report on the effect of external influences on the attainment of business objectives

• To provide protection for theassets of the business

©AONE

54

Controller Treasurer

Finance Leadership Roles

• Financial accounting

• Managerial accounting

• Tax accounting

• Patient accounting

• Internal auditing (varies)

• Managing workingcapital

• Managing investmentportfolio

• Managing capitalfinancing

28

©AONE

55

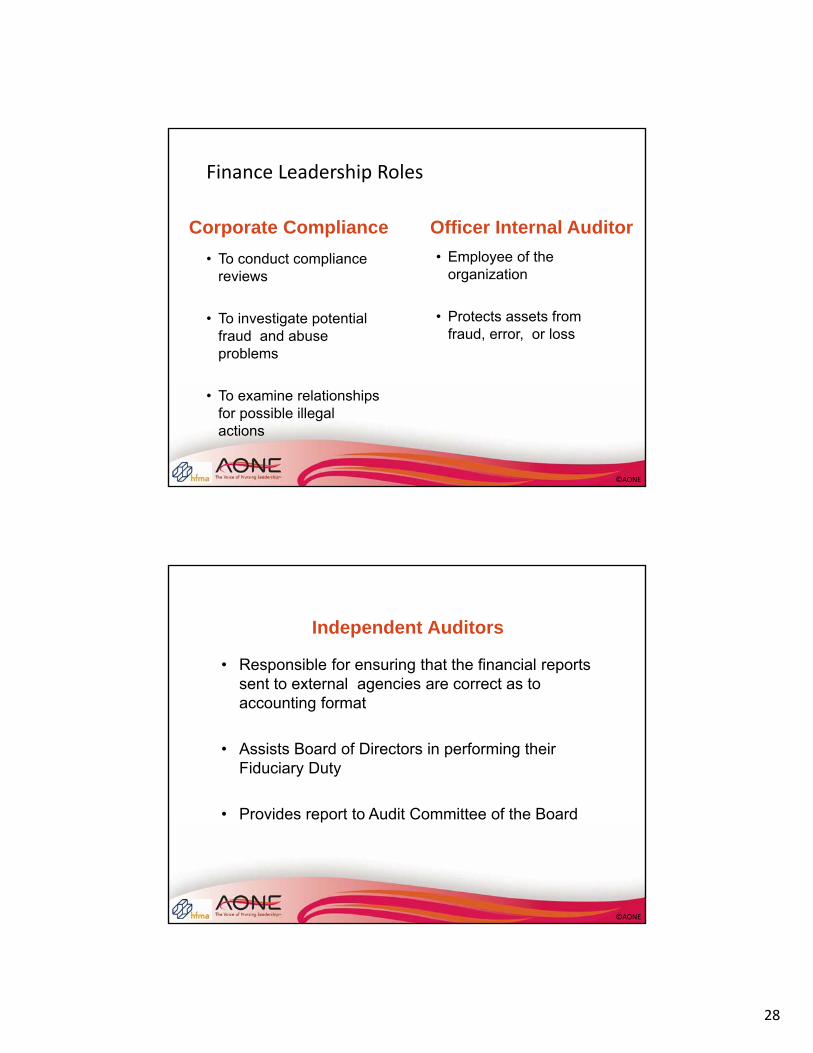

Corporate Compliance Officer Internal Auditor

• To conduct compliance reviews

• To investigate potential fraud and abuse problems

• To examine relationships for possible illegal actions

• Employee of the organization

• Protects assets from fraud, error, or loss

Finance Leadership Roles

©AONE

Independent Auditors

• Responsible for ensuring that the financial reports sent to external agencies are correct as to accounting format

• Assists Board of Directors in performing their Fiduciary Duty

• Provides report to Audit Committee of the Board

56

29

©AONE

Why all these Finance Positions?

"There are risks and costs to a program of action, but they are far less than the long-range risks

and costs of comfortable

inaction."

President John F. Kennedy

57

©AONE

Orange Jumpsuits & Silver Bracelets are

not a good look for anyone…

58

30

©AONE

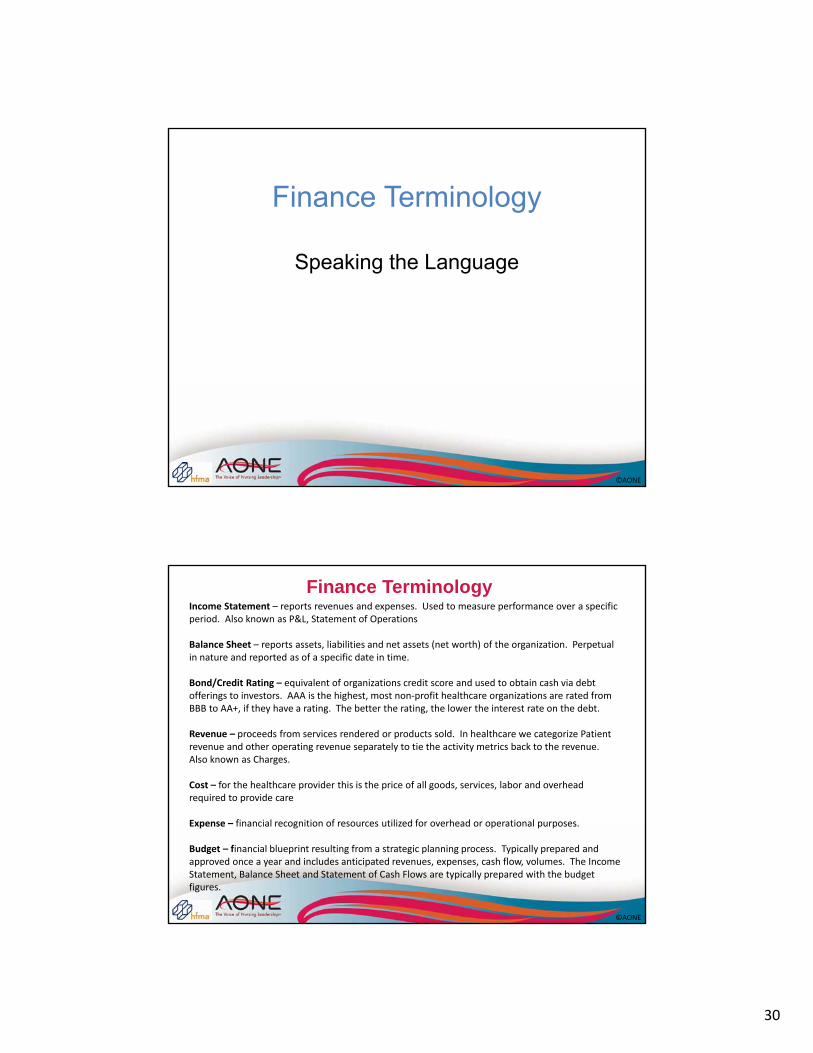

Finance Terminology

Speaking the Language

©AONE

Income Statement – reports revenues and expenses. Used to measure performance over a specific period. Also known as P&L, Statement of Operations

Balance Sheet – reports assets, liabilities and net assets (net worth) of the organization. Perpetual in nature and reported as of a specific date in time.

Bond/Credit Rating – equivalent of organizations credit score and used to obtain cash via debt offerings to investors. AAA is the highest, most non‐profit healthcare organizations are rated from BBB to AA+, if they have a rating. The better the rating, the lower the interest rate on the debt.

Revenue – proceeds from services rendered or products sold. In healthcare we categorize Patient revenue and other operating revenue separately to tie the activity metrics back to the revenue. Also known as Charges.

Cost – for the healthcare provider this is the price of all goods, services, labor and overhead required to provide care

Expense – financial recognition of resources utilized for overhead or operational purposes.

Budget – financial blueprint resulting from a strategic planning process. Typically prepared and approved once a year and includes anticipated revenues, expenses, cash flow, volumes. The Income Statement, Balance Sheet and Statement of Cash Flows are typically prepared with the budget figures.

Finance Terminology

31

©AONE

Finance Terminology (continued)FTE (Full Time Equivalent) – calculated by taking the hours worked or paid divided by the full time daily, weekly or monthly total. Example – 36 hour nursing position equates to a .9 FTE or 36/40 = .90.

Flexible or Variable Budget – tool that calculates the volume adjusted budget using an established hours or dollars per statistic. Example – Nursing unit’s volume is 10% over budget, so the hours per patient day X actual patient days = Flexible budgeted hours. This allows for a comparison to your budgeted expenses and hours based on the actual volume that will almost always be different than the budgeted volume.

Statistics – operational and financial metrics, activity indicators, volumes, acuity indicators. Examples include admissions, discharges, Case Mix Index, patient days, CT Scans, Lab Tests, etc.

Outpatient Equivalents – approximated calculation of outpatient activity into comparable inpatient activity or volumes.

Adjusted Admissions – approximated calculation accounting for outpatient activity and/or acuity using a Case Mix Index factor.

Patient Class – category of patient’s billing status. Examples include Inpatient Acute, Outpatient, Observation, Swing Bed, SNF, Inpatient Rehab, Bedded Outpatient, Inpatient Surgical, etc.

Financial Ratios – calculations drawn from financial statements for benchmarking and comparability amongst similar organizations. Example is Debt Service Coverage Ratio which measures an organization’s ability to repay their debt.

©AONE

Accounting Fundamentals

32

©AONE

Accounting Standards & Governance

• Generally Accepted Accounting Principles (GAAP) guide the uniform accumulation and communication of historical and projected economic data relating to the financial position and operating results of an enterprise. These principles are governed by the Financial Accounting Standards Board (FASB).

• The Financial Accounting Standards Board (FASB) mission is "to establish and improve standards of financial accounting and reporting that foster financial reporting by nongovernmental entities that provides decision-useful information to investors and other users of financial reports.“1

1 Facts about FASB

©AONE

Balance Sheet

• Assets

– Cash and Investments

– Accounts Receivable

– Inventory

– Property, Plant and Equipment

–

• Liabilities

– Accounts Payable

– Payroll Payable

– Bonds/Loans Payable

• Net Assets

– A.K.A. Fund Balance, Net Assets, Net Worth, Capital Equity, Stockholders’ Equity

– Assets – Liabilities = Net Assets

– Total of all capital infusions and earnings less all losses and dividends

Assets – Liabilities = Net Assets

33

©AONE

Statement of Operations aka Income Statement aka P&L

• Periodic statement produced to reflect operating performance

• Includes Revenue, Expenses and Income

• Revenue

• Receipts driven by delivery of product or service

• Expense

• Resources used to produce or deliver service. (Note: capital items such as equipment are expensed over a period of years of useful life, called depreciation)

• Net Income(Loss)

• Amount remaining(or not) for the reporting period

This is the consolidation of all activity within the individual department budgets

©AONE

Statement of Operations

Gross Patient Service Revenue─Deductions From Revenue

─Charity Care

─Bad Debt

Net Patient Service Revenue+ Other Operating Revenue

Total Operating Revenue- Operating Expenses

Operating Income(Loss)+ Non-Operating Income (i.e., investment income)

Excess of Revenue Over Expenses (or Total Income)

34

©AONE

Fee For Service (FFS) Payment Variation Example

DRG 234 CABG w/cc, LOS 9 days, Charge $48,350

• Medicare Weighted Case Rate Payment $33,019, Contractual Allowance $15,331

• Medicaid Weighted Case Rate Payment $28,587, Contractual Allowance $19,763

• Anthem Discount from Charge Payment $43,515, Contractual Allowance $4,835

• Free Care Payment $0, Free Care Allowance $48,350

67

©AONE

Statement of Operations (continued)

Other Operating Revenue

• Cafeteria

• Property Rental

• Value/Quality incentive payments

• Meaningful Use

68

35

©AONE

Statement of Operations (continued)

Non-Operating Revenue

• Investment Income, Interest, Dividends

• Gains(Losses) in Fair Value of Investments

• Donations/Gifts*

• Joint Venture Income

69*Sometimes recognized in Other Operating Revenue

©AONE

Fund Accounting

Unrestricted or General Funds

Restricted Funds• Temporarily Restricted or Specific Purpose

• Permanently Restricted or Endowment

Pension Funds

70

36

©AONE

Statement of Cash Flows• Important complimentary statement to the Balance Sheet and

Statement of Operations as it informs the reader of actual cash inflows, outflows and remaining balance for the reporting period

• Three sections include Operating, Investing and Financing activities

• Operating activities primarily represent Statement of Operations less a few non-cash expense items and changes in receivables and payables

• Investing activities primarily attributed to funds in stocks, bonds and other instruments as well as investments in building and equipment

• Financing activities relate to new or existing debt obligations (loans, issuance of bonds, repayments)

©AONE

Ratio Analysis

• Preferred approach for gaining an in depth understanding of financial statements

• Comparison of numbers to show a meaningful important to have context such as benchmarks or trends

• Allows external reviewers to quickly understand the current position, strengths, weaknesses and areas to watch.

37

©AONE

Categories of Ratios

• Liquidity-How well is the organization positioned to meet its short-term obligations?

• Activity- How efficiently is the organization using its assets to produce revenues?

• Profitability-How profitable is the organization?

• Capital structure- How are the organization’s assets financed and ability to take on new debt?

©AONE

Key Liquidity Ratios

• Current Ratio-proportion of all current assets to all current liabilities

• Days in Accounts Receivable Ratio-How quickly a hospital is converting its receivables into cash

• Days Cash on Hand Ratio-number of days worth of expenses an organization can cover with its most liquid assets

38

©AONE

Key Activity and Profitability Ratios• Operating revenue per adjusted discharge: measures total operating

revenues generated from the patient care line of business based on its adjusted inpatient discharges

• Operating Expense per Adjusted Discharge: measures total operating expenses incurred for providing its patient care services based on its adjusted inpatient discharges

• Salary and Benefit Expense as a Percentage of Total Operating Expenses: measures the total operating expenses that are attributed to labor costs

• Operating Margins: measures profits earned from the organizations main line of business

• Return on Net Assets: measures the rate of return for each dollar in net assets

©AONE

Capital Structure Ratios

• How are an organizations assets financed?

• How able is this organization to take on new debt?

• Examine the statement of cash flows to determine if significant long term debt has been acquired or paid off OR if there has been a sale or purchase of fixed assets

39

©AONE

Key Capital Structure Ratios

• Long term debt to net assets: measures the proportion of debt to net assets

• Net assets to total assets: reflects the proportion of total assets financed by equity

• Debt service Coverage: measures the ability to repay a loan

©AONE

Questions?

78

40

©AONE

Budgeting

The Crowd Favorite

Budgeting

©AONE

Interactive slide

When you hear budget, what’s the first word that pops into your head?

41

©AONE

Interactive slide

Managing my NHPPD is a priority for my institution.

A) Agree

B) Disagree

C) What is NHPPD?

©AONE

Interactive slide

I have a good grasp on what FTE means

A) Agree

B) Disagree

C) What’s FTE?

42

©AONE

Preparing a Personnel Budget

• Identify workload metric• Typical units of service

• Patient days or census

• Patient visits

• Number of cases

• Duration of hours for procedures

• Nursing Hours• Total hours worked by all RNs on the unit for a

defined time

• Nursing Hours per Patient Day=Nursing Hours/Census

©AONE

Understanding HPPD

• RNs worked 160 hours in the past 24 hours

• Unit census at midnight was 20 patients

• NHPPD = Nursing hours worked/census

• NHPPD = 160/20

• NHPPD = 8.0

43

©AONE

Practice

• Unit daily census 22 patients for the past 2 weeks

• Payroll review shows RNs worked 2,387 hours during the 2 weeks

• What is the NHPPD for the pay period?

©AONE

Understanding FTEs and Budgeting• Full Time Equivalent

• Amount of time worked in a week = 40 hours

• Business is 24/7

• Coverage needed for 168 hours weekly

• Staff needed for each assignment over a 24 hour period

• 168/40 = 4.2 FTEs

• 24 bed unit where each RN cares for 4 patients; how many FTEs are needed?

• 6 RNs X 4.2 FTEs = 25.2 FTEs

• Accounting for non-productive or non-patient care time

• 15% replacement factor (PTO, education, council, etc.)

• 25.2 X .15 = 3.78 + 25.2 = 28.98 FTEs

44

©AONE

Required FTEs using NHPPD

• Budgeted Census X Budgeted NHPPD =

• Required Hours/2080 =

• Required FTEs

• Practice: ADC is 22 and NHPPD is 10.0, how many FTEs are needed?

©AONE

Impact of Decrease in NHPPD

• ADC 22

• NHPPD decreased from 10.0 to 9.6

• What is the impact on your FTEs?

45

©AONE

Managing to Budgeted NHPPD

• Understanding organization’s metrics• Paid hours

• Worked hours

• Productive hours

• Impact of hours outside of direct patient care• Orientation

• Education

• Care models• Distribution to meet high demand times

• Use of full time and part-time

©AONE

Tightening the Budget Belt

• Organization makes the decision that all units must decrease their budget by 2%; where do you look to make this accommodation?

• What information do you need to know about your current budget performance?

• What line items would you go to first?

• How do you engage staff with prioritizing cuts?

46

©AONE

Innovative Care Models and Justification

• Understanding your work area flow• ADT times

• Understanding your staff strengths• Experience

• Education

• Adaptation

• Resilience

• Data needed for justification

• Nurse Incentives

©AONE

Clinical Efficiency

• What does clinical efficiency mean to you?

• Nurse Leader’s role in clinical efficiency

• Engaging clinical nurses in clinical efficiency• Impact to their practice

• Impact on quality patient outcomes

• Connection to value based reimbursement

47

©AONE

What is a Budget?

A budget is the financial blueprint or action plan for an organization. It translates strategic plans into measurable expenditures and anticipated performance over a certain period of time.

Budgeting is the process of creating and fine-tuning budgets. Budgeting activities include:

• Forecasting future business results, such as patient volume, revenues, capital investments, and expenses

• Reconciling those forecasts to organizational goals and financial constraints

• Obtaining organizational support for the proposed budget

• Managing subsequent business activities to achieve budgeted results93

©AONE

Budgeting Defined• Process of converting the operating plan into monetary terms.

• Budgets become the control standard against which performance is managed and measured.

• Budget process is an excellent opportunity for the financial manager to educate non-financial department managers on financial implications.

• Budget process is an excellent opportunity for the clinical and operating manager to educate the financial manager on quality and clinical outcomes implications.

94

48

©AONE

Why do Not-For-Profits need a profit?

• A reasonable profit is necessary to support demand for more and better services, continued investment in advanced technology, medical equipment, and facilities upkeep as well as meeting inflationary pressures.

• In addition, maintaining the credit rating allows for preferred rates and access to capital.

• Any profit is re-invested in the community via continued operations, access to care for those without financial resources.

95

©AONE

Budget Considerations

• Mission, Vision, Values, Culture

• Strengths, Weaknesses, Opportunities, Threats

• Economic Pressures

• Industry Trends

• Regulatory Issues

• Strategy96

49

©AONE

Budget Process Overview

97

©AONE

Key Steps in Creating a Budget

• Analysis of Current State

• Setting Goals

• Evaluating Options

• Identifying Budget Impacts

• Coordinating Department Budgets

• Creating Comprehensive Plan

• Executive and Board Level Approval98

50

©AONE

Budget Types

99

• Patient Days, Outpatient Visits

• Length of Stay

• Case Mix Index (CMI)

Statistical

• Patient Revenue

• Other Operating Revenue

• ExpensesOperating

• Buildings, Equipment, Software

• Other Investments, Cash Contributions, Loan/Debt Repayments,

Capital

©AONE

Steps in the Operating Budget Process

• Project volumes

• Convert volumes into revenue projections

• Convert volumes into expense requirements

• Adjust revenues and expenses as necessary

• Evaluate (monitor) budget performance100

51

©AONE

Operating Budget Process –Projecting Volumes

• Volume projection is the MOST important element in any planning process• Forecast content--description of specific situation

in question

• Forecast rationale--explanation of how the situation will progress from its current state to its forecasted state

101

©AONE

Operating Budget Process

Converting Volumes into Revenue

• Gross Revenues• Determine price increase

• Apply price increase to current price and multiply by specific volumes

• Net Revenues• Determine payer mix (extremely important planning

element)

• Determine rates by specific payer

• Apply payer mix and payer rates against payer volumes

102

52

©AONE

103

Operating Budget Process

Staffing expenses

– review staffing mix

– review skill mix

– review cost-of-living raise policy

– review merit raise policy

– review bonus policy

Non staffing expenses

– Determine variable expenses

• based on volumes

– Determine fixed expenses, using benchmarks

Converting Volumes into Expenses

©AONE

Operating Budget Process

Adjust revenues and expenses, as necessary

The adjustment will be based upon the requirements (targets) set forth by the Board and the Administration in its Strategic Plan and Strategic Financial Plan

• Operating Margin

• Excess Margin

• Days Cash on Hand

• Debt Service Coverage

• Return on Assets 104

53

©AONE

Variable Expenses

Variable expenses are those that change in direct proportion to changes in activity. Examples of variable expense include:

Direct labor

Supplies

Power and gas used in manufacturing

Shipping

Sales commissions

Income taxes 105

©AONE

Fixed Expenses

Fixed costs are those that remain fairly constant within a wide range of production or sales volumes. Examples of fixed costs include:

Rent

Basic utilities including electric and telephone service

Equipment leases

Depreciation

Interest payments

Marketing and advertising

Indirect labor, such as salaried supervisory employees 106

54

©AONE

Department Heads submit budgets

Department Heads submit budgets

VP/Division Leaders Review submissions

VP/Division Leaders Review submissions

Long Range Financial Plan

(3-5 years) completed

Long Range Financial Plan

(3-5 years) completed

Budget Committee Recommends

Budget

Budget Committee Recommends

Budget

CEO/President Endorses

CEO/President Endorses

Operating Budget Process Example

Board Approves Budget

Board Approves Budget

Budget Assumptions (Volume, New Services, Compensation

increases, Expense inflation/constraints)

disseminated

Budget Assumptions (Volume, New Services, Compensation

increases, Expense inflation/constraints)

disseminated

©AONE

Importance of Capital Budgeting

• Capital expenditures typically represent 6-10 % of operating expenses

• The healthcare organization has limited and scarce funding sources to maintain its fixed asset (capital) structure

• We have already seen that access to tax-exempt markets has become restricted

• The level of fixed asset acquisitions drive depreciation expenses on the income statement higher or lower

55

©AONE

109

Contingency Funds

• Due to the advanced timing of the budget, there could be significant unknown expenditures (Capital or Operating) that come up after its completion.

• Creation of a ‘contingency’ pool is a typical way of handling those types of expenses

• Usually the CEO, COO and/or CFO manage this pool of funds throughout the fiscal year

©AONE

Variance Analysis

• Comparisons of actual results to budgeted performance – variance analysis• Identify cause of variance

• Budget issue

• Fixed vs. variable cost drivers

• Review of trends

• Internal vs. external factors

• Consider possible interventions

110

56

©AONE

Variance Analysis

Common causes of variances in revenue and expenses

Example: Labor expense over budget by 5%; FTEs on budget

Reason: Staffing mix. Higher level/paid RN’s than budgeted.

Potential solution: Review Labor distribution report to determine which specific job/position codes were over compared to the budget. Use the Labor distribution or productivity reports to obtain detail. 111

©AONE

Variance Analysis

Example: Supply cost over budget, volume on budget

Reason: Supplies issued as ordered, budgeted based on volume. A large order occurred this month to stock up on necessary supplies which were not all used in this period.

Another reason could be that supplies were issued to your department in error.

Potential Solution: Check the inventory issued product using Inventory distribution report or AP distribution depending on whether supplies were ordered from outside vendor or internal supply room.

57

©AONE

Financial Decision Support

• Decreases in reimbursement have created a need for additional financial information

• This information is typically very detailed and is aggregated from the clinical, financial, supply chain and payroll systems

• Each organization utilizes this data differently, though calculating the provider’s cost of a specific service or procedure is a primary component

• Revenue, cost and profitability is often included in decision support information to better understand the financial perspective and implications of certain operations and/or strategies

113

©AONE

Financial Systems• Enterprise Resource Planning (ERP) systems include

modules for Human Resources, Payroll, Supply Chain, General Ledger, Fixed Assets

• Decision Support Systems (DSS) include modules for Labor Productivity Management, Cost Accounting, Variance Reporting, Benchmarking

• These systems interact with the clinical systems and/or Electronic Health/Medical Record (EHR/EMR)

114

58

©AONE

Key Takeaways• Financial Reporting is required function of healthcare

organizations and is overseen by regulators to ensure accuracy and integrity

• Ratios inform internal and external readers of ‘financial health’ of the organization

• The budgeting process is critical as it provides a financial plan each year to guide spending and maintain or improve the organization’s position

• Increased pressure on cost of care has led to additional tools integrating clinical and financial information

©AONE

Budget Committee ExerciseDriving the Process

59

©AONE

117

Budget Committee Executive Exercise

• Key assumptions

• Prioritizing initiatives for investment

• Communication to core leaders

• New position requests

• Capital investments

• Closing the remaining deficit

Each of you represents an executive on the budget committee of a large, stand alone hospital. Jan will play the CEO and Chuck will play the CFOWe’ll meet with each group as you process through this exerciseYou will work simultaneously in teams acting as the committee

There will be decisions made by your committee:

©AONE

Feedback and Insights

• What did you learn or realize that surprised you the most?

• How will this influence your approach to next year’s budget?

• What could we have done better to help you through this process? Was this helpful?

• Any unanswered questions?

60

©AONE

Feedback and Insights

• How did we do?

• What’s one thing you would change about today?

THANK YOU FOR BEING HERE!!