consumer protection in the telecommunication markets …

TRANSCRIPT

CONSUMER PROTECTION IN THE

TELECOMMUNICATION MARKETS IN THE POST

LIBERALIZATION ERA – THE CASE OF TANZANIA

MARCH 2017

HILDA MWAKATUMBULA

PhD Thesis 4014S0181

GRADUATE SCHOOL OF ASIA-PACIFIC STUDIES,

WASEDA UNIVERSITY

i

DEDICATION

This work is dedicated to my darling husband Dr. Goodiel Moshi and my beloved children Jadon and

Joan

ii

ACKNOWLEDGEMENT

I would like to extend my gratitude to my Chief Supervisor, Professor Hitoshi Mitomo, for offering me

the opportunity to study under his leadership. His tireless support and leadership throughout the PhD

Program have led this work to fruition. Under his leadership, I have learned to perceive social problems

as an opportunity for improvement. Furthermore, I am thankful for every encouraging word from him,

especially at times when the road ahead seemed dark.

Moreover, I would like to extend my gratitude to my deputy supervisor Professor Yasushi Katsuma and

other member of my examination committee, Professor Kato Atsushi and Professor Akihiro Nakamura.

Thank you very much for taking the time to read the draft of my thesis, and to offer your

recommendations and input. Looking at this thesis, your input has made the difference.

This thesis was also shaped during seminar presentations, where most of my colleagues offered their

inputs for improvement. A number of my colleagues used their precious time to go through my work and

help me shape it accordingly. I would not be able to mention every one of you, but I am appreciative to

each one.

I would not have been able to write this thesis without the great support of my darling husband and

children, and their sacrifices, patience, and understanding. I am thankful to my husband for sacrificing to

live far away from his family for almost two years, to give me the chance to finalize my PhD studies.

Furthermore, living in a foreign country with two children and studying was sometimes very challenging,

but I am indebted to my family supporters Mr and Mrs Tajiri, for taking care of children in my absence.

They made me a home in Japan.

I am also grateful to my beloved parents Jacob Mwakatumbula and Sekela Mwakatumbula for their

continuous support and prayers. Their moral and financial support throughout my academic journey will

forever be appreciated.

iii

This journey would not have been completed without the two-year scholarship the government of Japan

extended to me through the Ministry of Education, Culture, Sports, Science, and Technology (MEXT). In

the same vein, I am appreciative to the Waseda University for Young Doctoral scholarship. These

scholarships have enabled me to live financially relax and offered me supplementary time to concentrate

on my studies. Furthermore, I feel indebted to GSAPS office staff for their continuous support and advice

throughout my studies.

Last, but not least, I would like to extend my heartfelt gratitude to my heavenly Father and Almighty

GOD. Through it all, His mighty hand anchored and strengthened me. To Him and Him alone the praise

and honor is due now and forevermore.

iv

TABLE OF CONTENTS

DEDICATION ............................................................................................................................................... i

ACKNOWLEDGEMENT ............................................................................................................................ ii

TABLE OF CONTENTS ............................................................................................................................. iv

LIST OF TABLES ..................................................................................................................................... viii

LIST OF FIGURES ..................................................................................................................................... ix

ABBREVIATIONS ...................................................................................................................................... x

EXECUTIVE SUMMARY ....................................................................................................................... xiv

CHAPTER 1 : INTRODUCTION ................................................................................................................ 1

1.1 Background ................................................................................................................................... 1

1.2 Problem Statement ........................................................................................................................ 3

1.2.1 Ideal Situation ....................................................................................................................... 3

1.2.2 Background of Consumer Protection .................................................................................... 5

1.2.3 Challenges Facing Consumers in the Markets ...................................................................... 6

1.3 Purpose .......................................................................................................................................... 7

1.4 Research Questions ....................................................................................................................... 9

1.5 Contribution ................................................................................................................................ 11

1.5.1 Academic Contribution ....................................................................................................... 11

1.5.2 Social Contribution ............................................................................................................. 11

1.6 Thesis Overview ......................................................................................................................... 12

1.7 Summary ..................................................................................................................................... 14

CHAPTER 2 THE OVERVIEW OF THE TANZANIA TELECOMMUNICATIONS MARKET .......... 15

2.1 Introduction ................................................................................................................................. 15

2.2 Prior to the Liberalization Era ..................................................................................................... 15

2.2.1 History of Tanzania ............................................................................................................. 15

2.2.2 History of the telecommunication in Tanzania ................................................................... 16

2.2.3 Policies ................................................................................................................................ 16

2.3 The Liberalization-process Era ................................................................................................... 18

2.3.1 Introduction ......................................................................................................................... 18

2.3.2 The Regulator: Tanzania Communication Commission (TCC) .......................................... 18

2.3.3 Policy and regulations ................................................................................................................ 19

v

2.3.4 Market Structure during the Liberalization Process ............................................................ 23

2.4 Post-liberalization Era ....................................................................................................................... 30

2.4.1 Overview of the era .................................................................................................................... 30

2.4.2 Legislations and regulations ....................................................................................................... 30

2.4.3 Major Operators ......................................................................................................................... 34

2.5 Consumer Protection ......................................................................................................................... 38

2.5.1 Introduction ................................................................................................................................ 38

2.5.2 Consumer Challenges ................................................................................................................ 39

2.6 Conclusion ........................................................................................................................................ 40

CHAPTER 3 CONSUMER PROTECTION LITERATURE AND THE THEORETICAL FRAMEWORK

.................................................................................................................................................................... 42

3.1 Introduction to Consumer Protection .......................................................................................... 42

3.1.1 Definition of Consumer Protection ..................................................................................... 42

3.1.2 Organizations responsible for consumer protection ............................................................ 43

3.1.3 Ways to achieve consumer protection................................................................................. 48

3.2 International Organizations and Consumer Protection ............................................................... 51

3.2.1 UNCTAD and Consumer Protection .................................................................................. 51

3.2.2 WTO and Consumer Protection .......................................................................................... 52

3.2.3 ITU and Consumer Protection ............................................................................................ 53

3.3 Consumer Protection literature based on the telecommunication markets ................................. 56

3.3.1 Consumer knowledge .......................................................................................................... 56

3.3.2 Consumer awareness about the complaint procedure ........................................................ 59

3.4 Consumer Protection in Tanzania ............................................................................................... 66

3.5 Conceptual and Theoretical Perspective ........................................................................................... 69

3.5.1 Theory of Reasoned Action ................................................................................................ 70

3.5.2 Theory of planned behaviour .............................................................................................. 70

3.5.3 Information Motivation Behaviour Skills (IMB) theory ..................................................... 71

3.5.4 Adopted Study Model and Conceptual Framework ............................................................ 75

CHAPTER 4 METHODOLOGY ............................................................................................................... 77

4.1 Introduction ................................................................................................................................. 77

4.2 Study design ................................................................................................................................ 78

4.3 Sampling technique ..................................................................................................................... 80

4.4 Data Collection ........................................................................................................................... 82

vi

4.4.1 Collection of Data Samples ................................................................................................. 82

4.4.2 The questionnaire ................................................................................................................ 84

4.5 Approaches to Data Analysis ...................................................................................................... 86

4.5.1 Discrete-choice modelling ................................................................................................. 86

4.6 Summary ..................................................................................................................................... 94

CHAPTER 5 DETERMINANTS OF CONSUMER KNOWLEDGE ON THEIR RIGHTS ..................... 95

5.1 Introduction ................................................................................................................................. 95

5.2 Background of the consumer rights ............................................................................................ 97

5.2.1 History of consumer rights ................................................................................................. 97

5.2.2 Consumer rights in the telecommunication sector ............................................................. 98

5.3 Methodology ............................................................................................................................. 101

5.4 Results ....................................................................................................................................... 113

5.5 Conclusion ................................................................................................................................ 118

CHAPTER 6 : CONSUMER AWARENESS OF THE COMPLAINTS PROCEDURE ......................... 121

6.1 Introduction ............................................................................................................................... 121

6.2 Complaints Procedure and Institutions. .................................................................................... 123

6.3 Methodology ............................................................................................................................. 125

6.3.1 Data ................................................................................................................................... 125

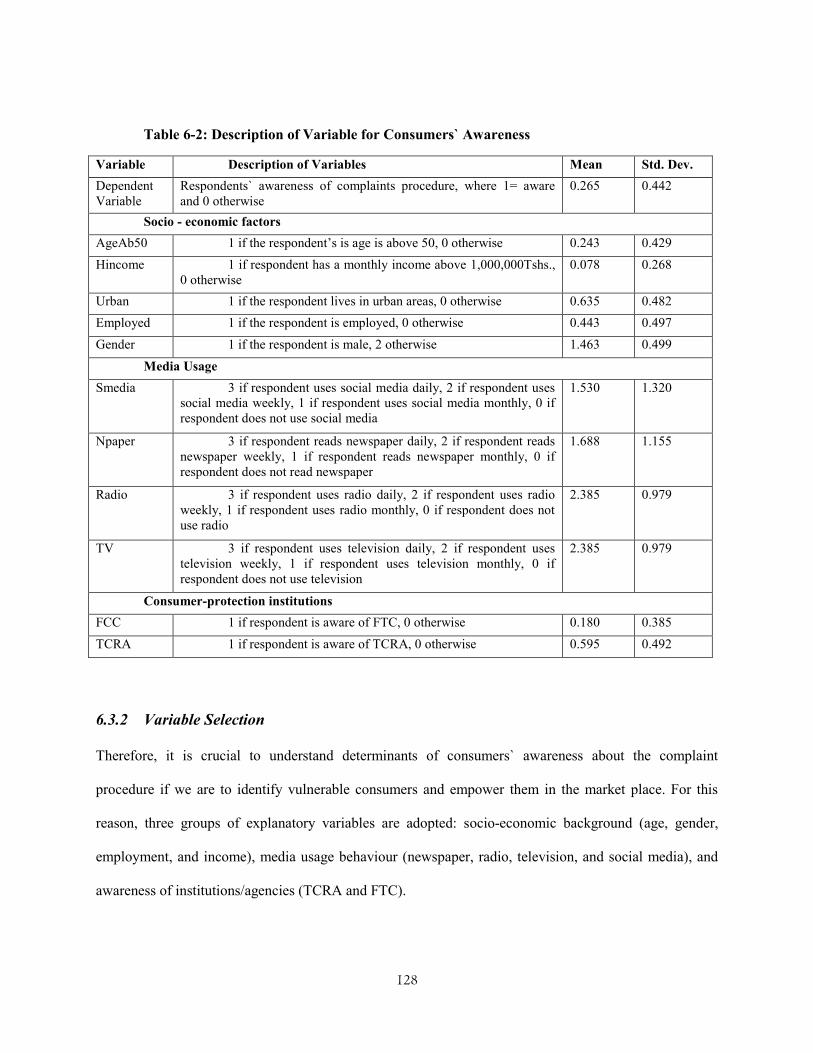

6.3.2 Variable Selection ............................................................................................................. 128

6.4 Results ....................................................................................................................................... 134

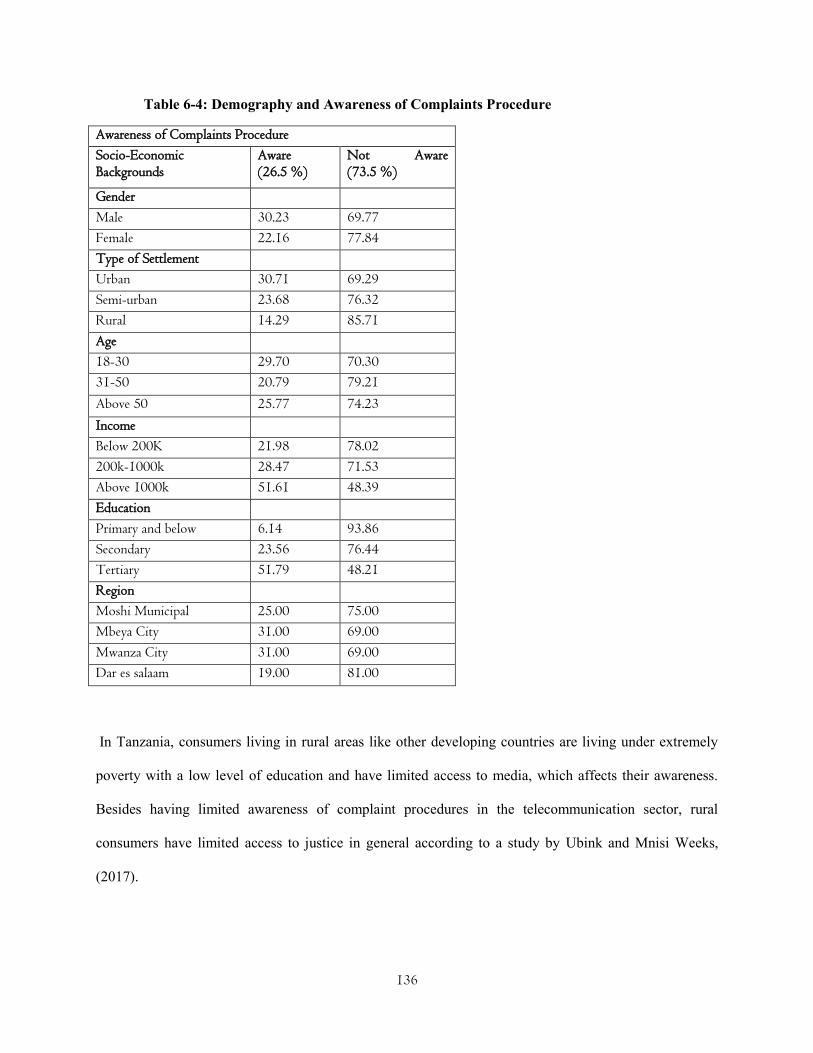

6.4.1 Cross tabulation................................................................................................................. 134

6.5 Empirical results ....................................................................................................................... 135

6.6 Conclusion ................................................................................................................................ 140

CHAPTER 7 CONSUMER COMPLAINT BEHAVIOR ........................................................................ 142

7.1: Introduction .................................................................................................................................... 142

7.2 Methodology ............................................................................................................................. 144

7.2.1 Data ................................................................................................................................... 144

7.2.2 Socioeconomic backgrounds and consumer complaint behavior ..................................... 146

7.2.3 Variables Selection ........................................................................................................... 147

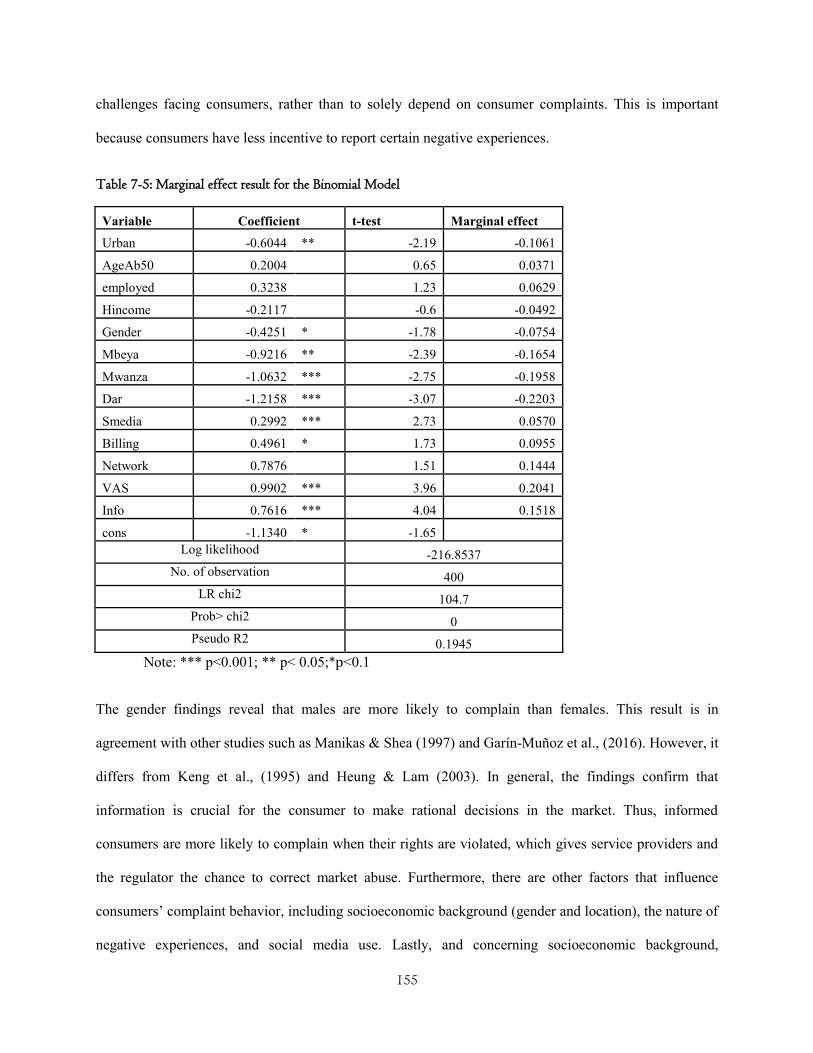

7.3 Results and discussion ............................................................................................................. 153

7.4 Conclusion ............................................................................................................................... 156

CHAPTER 8 KEY FINDINGS, IMPLICATIONS, AND FUTURE RESEARCH ................................. 159

8. 1 Key findings .............................................................................................................................. 159

vii

8.2 Policy Implications and Managerial Recommendations ........................................................... 164

8.2.1 Policy recommendations ................................................................................................... 164

8.2.2 Managerial Implication ..................................................................................................... 166

8.3 Limitation and Direction for Future Studies ............................................................................. 167

CHAPTER 9 : CONCLUSION................................................................................................................. 169

REFERENCES ......................................................................................................................................... 174

viii

LIST OF TABLES

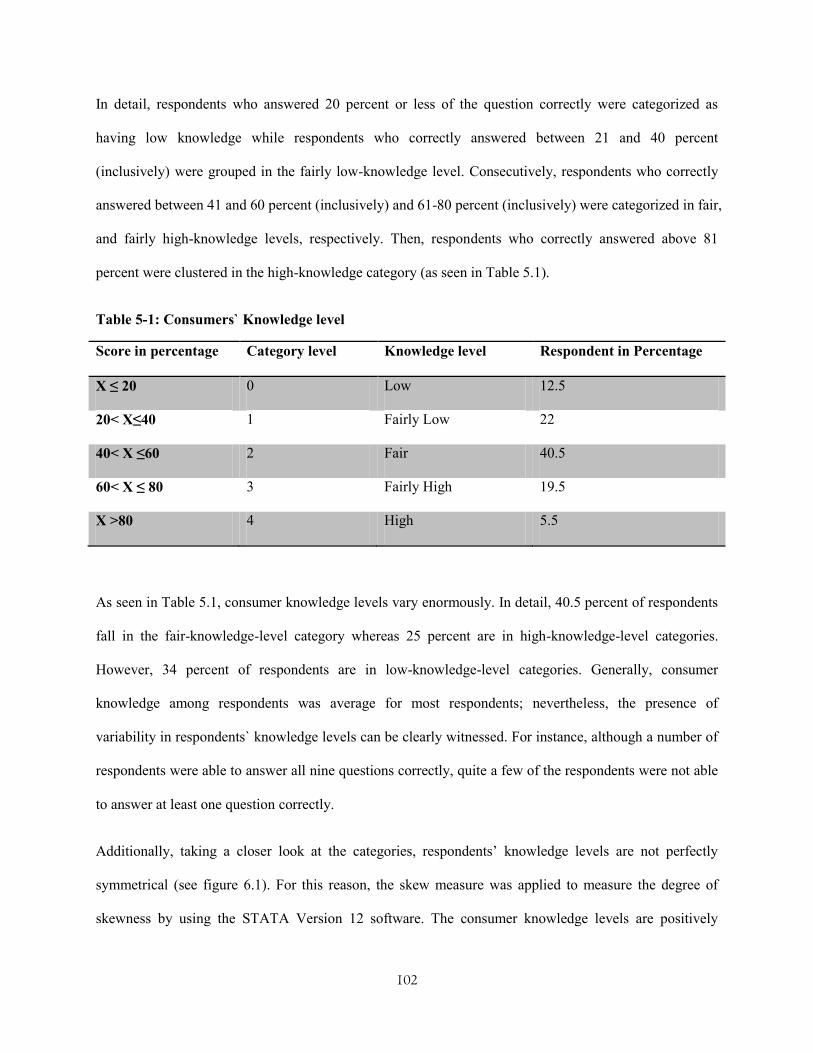

Table 5-1: Consumers` Knowledge level .................................................................................................. 102

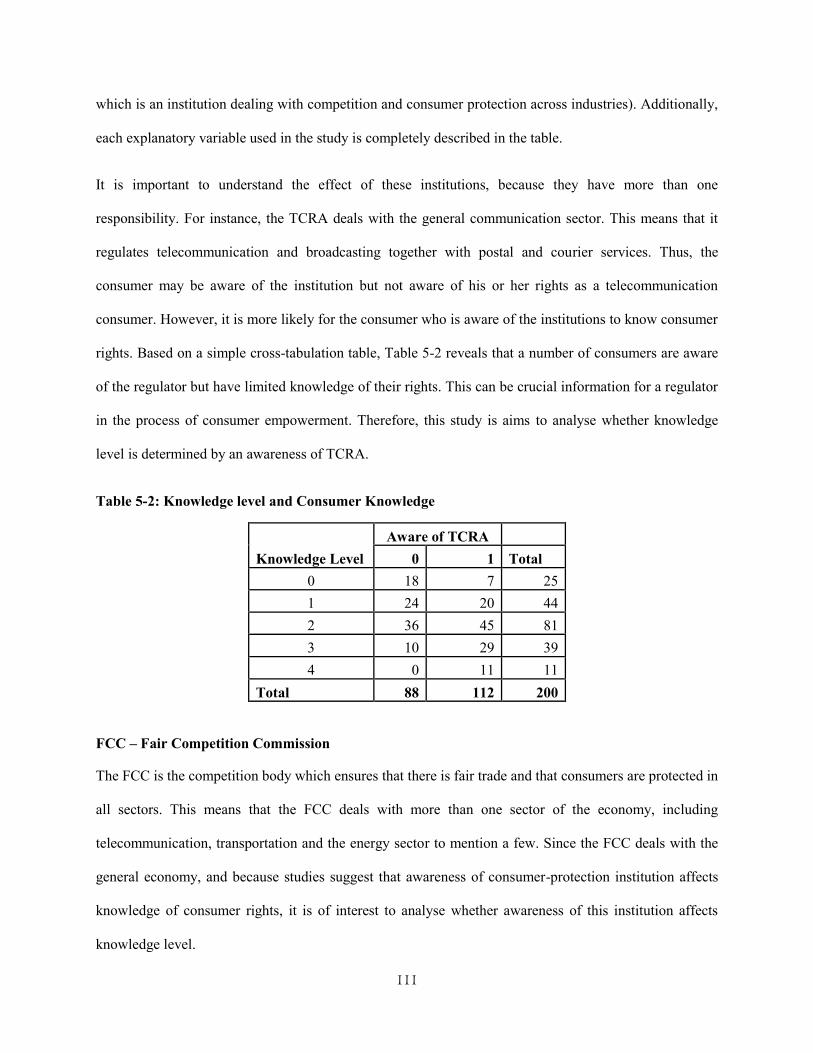

Table 5-2: Knowledge level and Consumer Knowledge .......................................................................... 111

Table 5-3: Cross tabulation FCC and Consumer Knowledge ................................................................... 112

Table 5-4: Correlation result for Knowledge ............................................................................................ 112

Table 5-5: Descriptive analysis ................................................................................................................. 113

Table 5-6: Demography and Knowledge levels ........................................................................................ 115

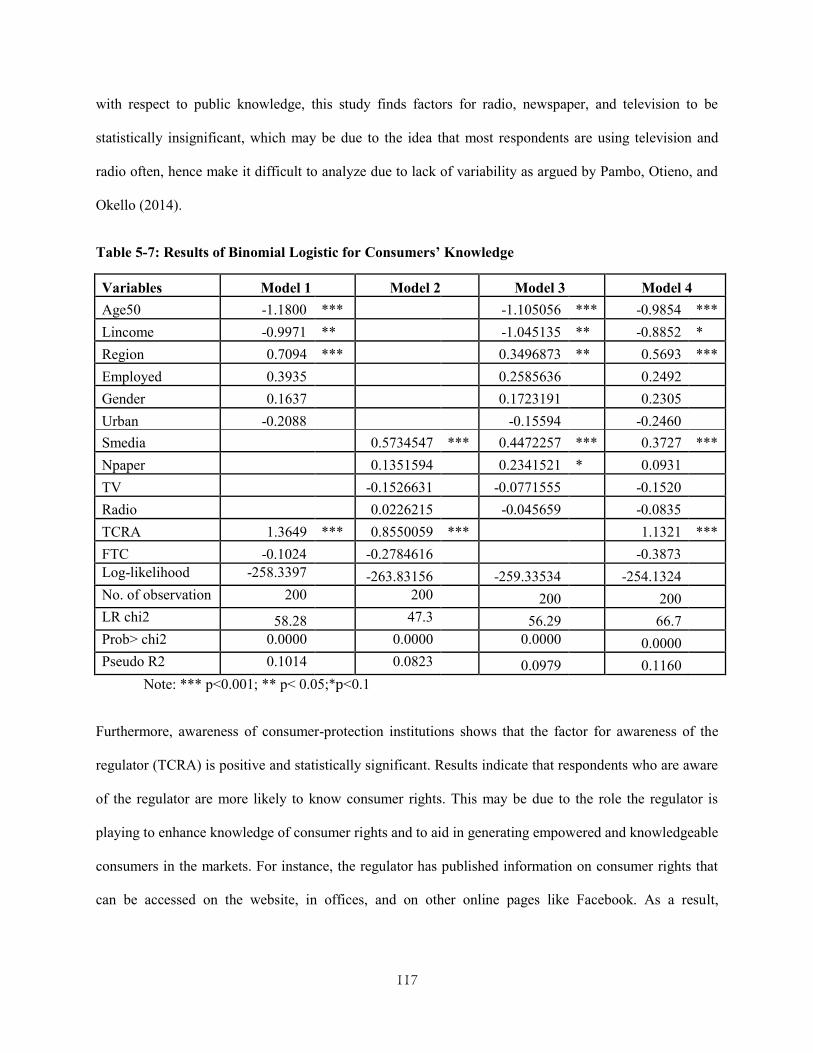

Table 5-7: Results of Binomial Logistic for Consumers’ Knowledge ...................................................... 117

Table 5-8: The result for marginal effects for each category .................................................................... 118

Table 6-1: Consumers` awareness categories ........................................................................................... 126

Table 6-2: Description of Variable for Consumers` Awareness ............................................................... 128

Table 6-3: Correlation matrix of variables ................................................................................................ 134

Table 7-1 Socioeconomic Background and Consumer Complaint Behavior ........................................... 147

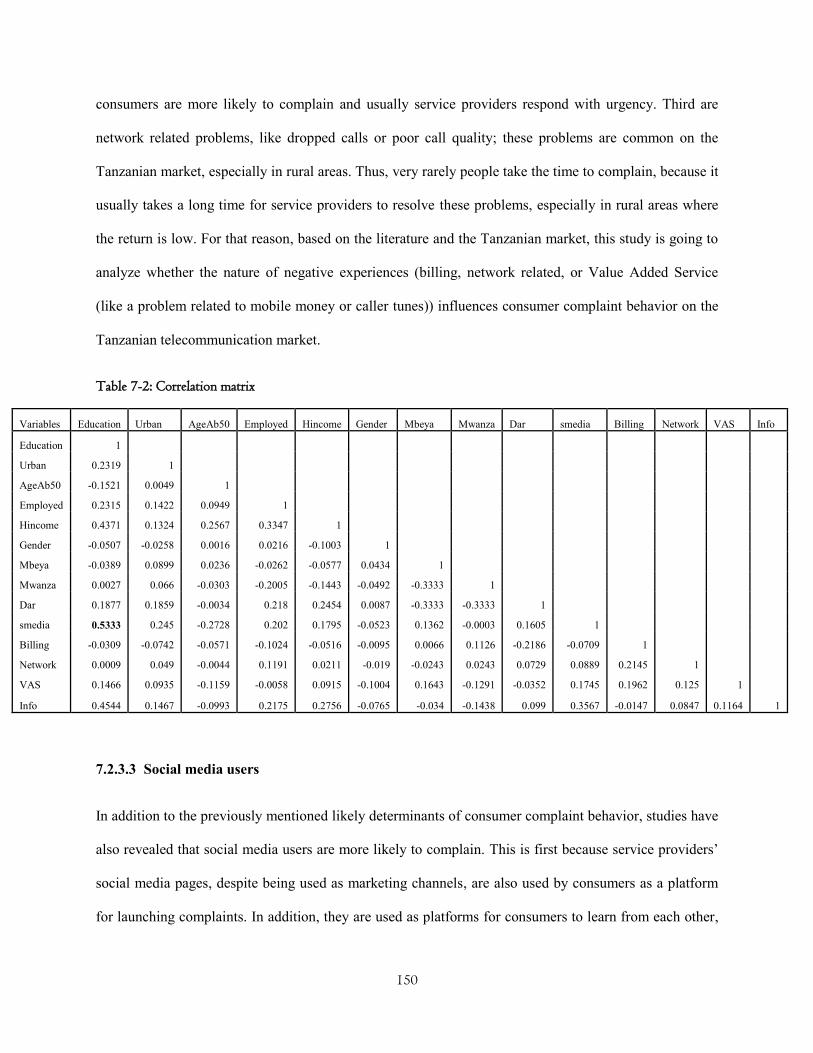

Table 7-2: Correlation matrix ................................................................................................................... 150

Table 7-3 Description of variables for Consumer Complaints behavior .................................................. 152

Table 7-4: Binomial regression Model ..................................................................................................... 154

Table 7-5: Marginal effect result for the Binomial Model ........................................................................ 155

ix

LIST OF FIGURES

Figure 1-1: Telecommunication market ........................................................................................................ 4

Figure 1-2: Liberalized telecommunication markets .................................................................................... 4

Figure 3-1: Information Motivation and Behaviour Skills Theory ............................................................. 73

Figure 3-2: Adopted study model ............................................................................................................... 76

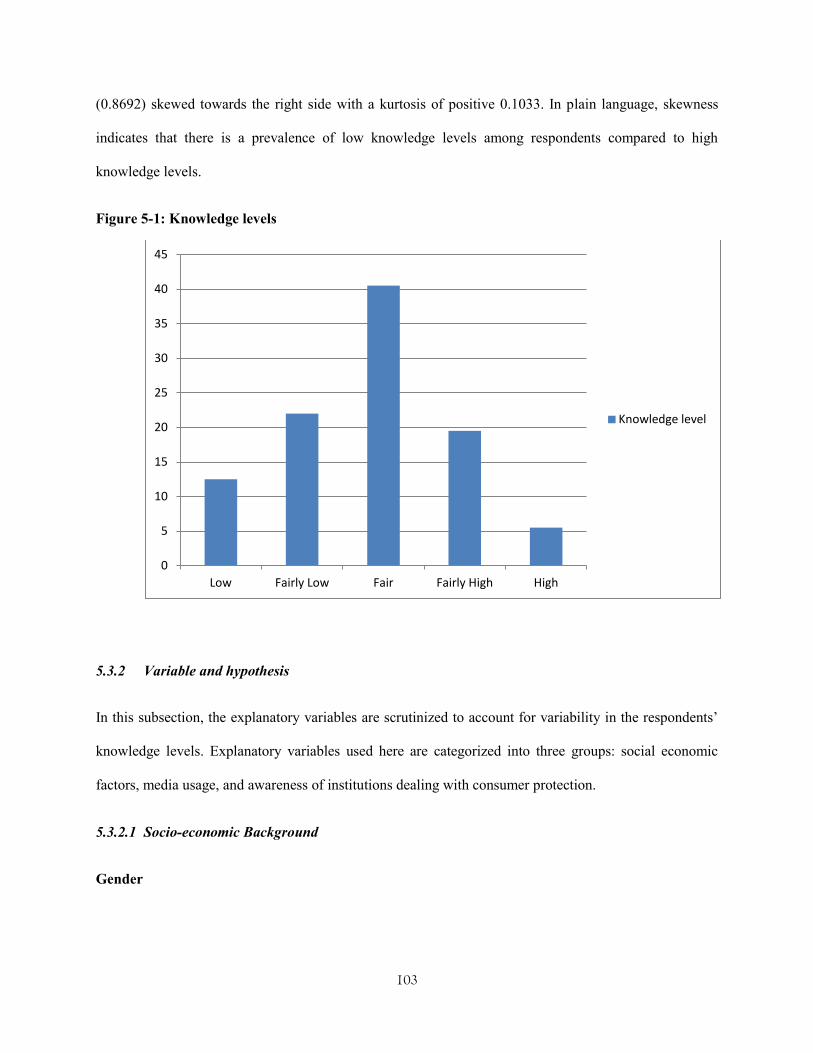

Figure 5-1: Knowledge levels ................................................................................................................... 103

Figure 6-1: Consumer Awareness Levels in percentage ........................................................................... 127

Figure 6-2: Consumer Awareness in Percentage ...................................................................................... 127

Figure 7-1: Study Framework ................................................................................................................... 145

x

ABBREVIATIONS

AAPOR – American Association for Public Opinion Research

AKFED – Aga Khan Fund for Economic Development

ADR – Alternative Dispute Resolution

APCON – Advertising Practitioners of Nigeria

ARICEA – The Association of Regulators of Information and Communications for Eastern and

Southern Africa

AU – African Union

CC – Complaint Committee, Tanzania

CCU – Consumer Complaint Unit, Tanzania

CDR – Consumer Dispute Resolution

CEIR – Central Equipment Identification Register

CERT – Computer Emergency Response Team

CI – Consumer International

CLF – Converged Licensing Framework

COMESA – Common Market for Eastern and Southern Africa

CPA – Consumer Protection Act, Nigeria

CPC – Consumer Protection Council, Nigeria

EAC – East Africa Community

EC – European Commission

ECOSOC – Economic and Social Council

EIR – Equipment Identification Register

EPOCA – Electronic and Postal Communications Act

EU – European Union

FCT – Tanzania Fair Competition Tribunal

xi

GMSS – Global Maritime Distress safety and System

GSM – Global System for Mobile communication

GSMA – GSM Association

HSDPA – High Speed Downlink Packet Access

HTT – Helios Towers Tanzania

ICASA – Independent Communications Authority of South Africa (ICASA)

ICT – Information and Communication Technology

IMB – Information Motivation Behavior

IMEI – International Mobile Equipment Identity

IPO – Initial Public Offer

IP-PoP – Internet Protocol Point of Presence

IPS – Industrial Promotional Services

ISO – International Standards Organization

ISP – Internet Service Provider

ITU – International Telecommunication Union

KCC – Kenya Communications Commission

KPI – Key Performance Indicator

LTE – Long Term Evaluation

MEK – Minimum Economic Knowledge

MIC – Millicom International Cellular

MNP – Mobile Number Portability

MoA – Memorandum of Agreement

MoU – Memorandum of Understanding

MST – Ministry of Science and Technology

NCA – National Communications Agency

xii

NCC – National Communications Commission

NF – National Facility

NGO – Non Governmental Organization

NICTBB – National ICT Broadband Backbone

NLRC – National Lottery Regulatory Commission, Nigeria

NSN – Nokia Siemens Networks

NTP – National Telecommunications Policy, Tanzania

ODR – Online Dispute Resolution

OECD – Organization for Economic Co-operation and Development

OFCOM – Office of Communications, United Kingdom

RIO – Reference Interconnection Offer

SADC – Southern African Development Community

SDG – Sustainable Development Goals

SIM – Subscriber Identity Module

SMS – Short Message Service

SR – Self Regulation

TAEC – Tanzania Atomic Energy Commission

TBC1 – Tanzania Broadcasting Commission

TBC2 – Tanzania Broadcasting Corporation

TBS – Tanzania Bureau of Standards

TCC – Tanzania Communications Commission

TCRA – Tanzania Communication Regulatory Authority

TCRA-CCC – Tanzania Communications Regulatory Authority – Consumer Consultative

Council

TD-LTE – Time Division Long Term Evolution

xiii

TPB – Theory of Planned Behavior

TPC – Tanzania Posts Corporation

TPTC – Tanzania Portal Telecommunications Corporation

TRA1 – Tanzania Revenue Authority

TRA2 – Theory of Planned Behavior

TRI – Technology Resources Industries, Berhad

TTCL – Tanzania Telecommunication Company Limited

TTMS – Telecommunication Traffic Monitoring System

UAE – United Arab Emirates

UMTS – Universal Mobile Telecommunications Service

UN – United Nations

UNCTAD – United Nations Conference on Trade and Development

UNGCP – United Nations Guidelines for Consumer Protection

USD – United States Dollar

VAS – Value Added Services

V-SAT – Very Small Aperture Terminal

WGTCP – Working Group for Trade and Competition Policy

WOM – Word of Mouth

WTO – World Trade Organization

xiv

EXECUTIVE SUMMARY

The telecommunications sector has grown tremendously since the turn of the century (ITU, 2015). This

growth has been attributed to massive policy reforms such as the liberalization of markets and the

subsequent technological developments. The policy rationales for liberalization include the improvement

of consumer choices, sovereignty and bargaining power, which should in turn lead to higher perceived

consumer satisfaction (Hulsink, 2012; Togan, 2010). However, even with the presence of liberalized

markets, consumer satisfaction in the telecommunications sector is still low, both in developing and

developed countries (Lopez, Amaral, Garín-Muñoz, & Gijón, 2015). Furthermore, it is now evident that

competitive markets alone do not necessarily translate to better services, as research shows that even in

competitive markets, there can be low quality service providers (Lopez, Amaral, Garín-Muñoz, & Gijón,

2015). This is because as competition becomes stiff and profit margins are eroded, service providers have

little incentive to increase their investments in providing better quality services, if such decisions do not

lead to comparable financial gains. Consequently, consumers are more likely to be exploited in the

telecommunication markets, which has raised the need for consumer protection to ensure consumers get

value for money and have bargaining power.

The Tanzanian market is not different from the rest of the world where consumers are prone to multiple

challenges, from billing problems to poor network quality. For example, parliamentary sessions on

consumer complaints have revealed that some mobile service providers charge their users automatically,

without their consent. Similarly, there have been accusations of collusion among the service providers, as

in February 2015 all major operators decided to increase their data prices within the same week, a practice

that is against competitive markets. Although the Tanzanian regulatory authority has regulations to

uphold consumer protection, in most cases regulations are offered ex-post, thus evoked after the consumer

has filed his complaints to the responsible entities in accordance with the procedure instituted by the

Tanzanian regulator. Thus, consumer protection is pegged against the ability of consumers to discern

xv

when their rights have been abused, aware of the complaints procedures and entities that can enable them

to pursue redress, and lastly actually file the complaints in accordance with the complaints procedure.

The thesis is guided by the Information Motivation Behavior (IMB) theory by Fisher and Fisher (1992) to

understand the consumer behavior of telecommunication users in Tanzania. The IMB theory suggests that

information is an important agent, with the ability to alter consumer behavior. Thus, consumers having

the correct information are more likely to behave in a positive way and according to social norms. Since

consumer protection is offered ex-post, it is crucial that consumers have proper information, to be able to

discern negative experiences. In other words, information may offer consumers the ability to discern

challenges in the markets, and hence provides operators and/or the regulator with the opportunity to

correct market abuse. The underlining belief is that properly handled consumer complaints have benefits

for the industry, as they offer a feedback mechanism to service providers and regulators alike, and thus

can be used to improve the service design, management and delivery (Tronvell, 2008). Accordingly, this

thesis has three specific objectives; first to analyze the level of information among telecommunication

consumers; second to determine the antecedent of the level of information among consumers; and third to

investigate the effect of information on consumer complaint behavior. To achieve this objective, the thesis

aim to respond three research questions:

What is the level of consumers’ knowledge about their rights and its determinants in the

telecommunication markets?

What is the level of consumers’ awareness of the complaints procedure and its determinants in

the telecommunication markets?

What is the effect of information on consumer complaint behavior?

Thesis uses three empirical analyses in response to the research problems. The first empirical analysis

tackled the first research question. The study found that the level of consumer knowledge varies

significantly among consumers and is skewed toward low knowledge. Furthermore, the study showed that

xvi

the respondents’ knowledge levels are determined by socioeconomic background, media use (social

media), and institutional awareness (the regulator-TCRA).

The second empirical analysis addressed the second research question. The study revealed that the level

of consumer awareness on complaints procedure is low. Furthermore, the study demonstrated that

awareness of the complaints procedure is determined by socioeconomic background, whereby urban

consumers are more likely to be aware. Moreover, the use of newspapers and social media increases

individuals’ propensity toward awareness of complaints procedures in the telecommunications market.

The last research question was answered by the third empirical study. The study suggested that 40% of

aggrieved consumers are not likely to complain. Furthermore, the study elucidated that the level of

information influences consumers’ complaint behavior. Thus, better informed consumers are more likely

to complain. In addition, the study suggested that while information is the basic agent to consumer

behavior, there are other factors that influence consumer complaint behavior in the telecommunication

markets. Those factors include socioeconomic background, social media use, and the nature of the

unpleasant experience.

Based on the results of each case study, this thesis has offered an academic contribution and implications

for policy makers as well as service providers’ management with respect to consumer protection in

developing countries, particularly in Tanzania.

Academic contribution

• The thesis has contributed to literature by introducing new determinants of consumer complaint

behavior in the telecommunication markets. Previous studies suggested that socioeconomic

factors, the level of dissatisfaction and the nature of the unpleasant experience influence

consumer complaint behavior. This thesis does not nullify previous studies that analyzed the

determinants of consumer complaint behavior (CCB) in the telecommunication market, but rather

xvii

extended the level of information as another factor that is likely to affect CCB. In addition, the

thesis suggests that social media use also influence consumers’ behavior.

Implications for policy makers

Education

o As informed consumers - consumers who know their rights and are aware of complaints

procedure are likely to complain when having unpleasant experiences, and thus eliminate

a risk of consumer exploitation, informed consumers are vehicles toward a healthier

telecommunication sector. Therefore, policy makers are recommended to offer consumer

education programs targeting consumers in all socioeconomic groups, including

vulnerable ones.

Demand side based survey

o As 40% of aggrieved consumers are not likely to complain, the policy makers are advised

to conduct a demand side survey. This survey will aid policy makers and enable them to

device better policies for consumer protection, by providing insights into challenges

facing consumers in the telecommunication markets.

Social media

o The regulator is recommended to take social media more seriously, as one means of

interacting with the consumers. Social media can be used by the regulator to provide

information to consumers, and also as a means for obtaining feedback from consumer

experiences in the market, which may be useful insights for consumer protection policy.

Implications for service providers’ management

Offer information

xviii

o While the regulator has the main responsibility of offering information to

consumers, service providers also have a role to play. For instance, the consumers

must be well informed by their service providers concerning complaints

procedures to follow when having unpleasant experiences. Therefore, and due to

the limited awareness of complaints procedures among consumers, service

providers are recommended to offer information to consumers, including

vulnerable ones.

Improve quality of service

o All respondents have reported to have had at least one unpleasant experience

related to telecommunications; this can be minimized, even though service failure

is inevitable. Therefore, service providers are advised to minimize service failures

and eliminate them where technically possible.

1

CHAPTER 1 : INTRODUCTION

1.1 Background

The telecommunication sector has grown tremendously since the turn of the 21st century, in both

developed and developing countries. Penetration of mobile services had reached 7 billion (equivalent to

95% of the global population) in 2015, from less than 1 billion in 2000, worldwide (ITU, 2016). The

same trend of growth has been witnessed in the Tanzanian telecommunication sector: penetration of

mobile services had reached 39.9 million (equivalent to 79% of the population) in 2015, from only 0.28

million (less than 1%) in 2000 (TCRA, 2015).

Rapid growth in the telecommunications sector is attributed to sector reforms, and mainly the

liberalization of markets (Batuo, 2015). Liberalization of telecommunications markets started around

1980 and 1990 in most developed and developing countries, respectively (Chowdary, 1998). The

Tanzanian telecommunication markets were partially liberalized in 1993 and fully liberalized in 2005. As

a result of liberalization, investments in the telecommunication sector grew (Lestage, Flacher, Kim, Kim,

& Kim, 2013; Kang, Hauge, & Lu, 2012; Garrone & Zaccagnino, 2015); this in turn encouraged

technological advancements, which led to innovative services and products. For instance, most operators

in Tanzania are currently offering 4G LTE services (Kitundu, 2016).

Furthermore, due to technological advancements, the telecommunication sector has become intertwined

with and plays a major role in other sectors such as education, commerce, agriculture, and health. For

instance, mobile money systems such as M-Pesa are important in the financial sectors of developing

countries (Alampay and Moshi, forthcoming). The link between the telecommunication sector and other

sectors explains the former’s vitality and its potential to foster economic growth in the modern world,

thereby playing a crucial role in attaining the Sustainable Development Goals (SDG) (ITU, 2016).

2

Apart from contributing to the growth of the telecommunication sector, liberalization was expected to

improve consumer sovereignty by creating choices in the markets through competition, hence leading to

higher consumer satisfaction (OECD, 2007; Jordana & Levi-Faur, 2004). However, according to Lopez et

al. (2015), consumer satisfaction is still low in both developed and developing countries. In particular, the

situation is worse in developing countries, where the quality of service (QoS) is persistently poor ("A

growing number", 2013; Appiah, 2011; Fripp, 2012; Mumo, 2016; TCRA, 2015). This persistence of

poor QoS and low consumer satisfaction in the telecommunication markets suggests that liberalization

alone does not guarantee consumer sovereignty (Lopez, et al. 2015; Smith, 2010; Cherry 2010).

Moreover, Averitt and Lande (1997) suggest that competition may lead to consumer sovereignty only

when consumers are able to make rational decisions in competitive markets based on the information

offered. Thus, information is a crucial factor for consumers to make sound decisions, hence reaping the

competitive advantages of the liberalized markets. In addition, Sappington (2005) and Xavier and

Ypsilanti (2010) posit that even in competitive markets, consumers are faced with challenges such as

incomplete information and behavioral biases. In a similar vein, the consumer protection manual prepared

by UNCTAD (2016) elucidates that there is a disparity between consumer and supplier in the marketplace

in terms of bargain power, knowledge, and resources, and suggests that consumers are more likely to

be vulnerable in that relationship. Thus, studies (Ofcom, 2007; Xavier, & Ypsilanti, 2008) emphasize that

consumer protection is crucial in the markets to improve consumer welfare, as well as to deliver the

potential benefits of competition.

Consumer protection is becoming a common topic of discussion among policymakers, researchers, and

other stakeholders worldwide. For example, international organizations such as the United Nations (UN),

the Organization for Economic Co-operation and Development OECD, and the European Union (EU)

have directives, manuals, or guidelines for consumer protection (UNCTAD, 2016). Consumer protection

in the telecommunication markets has been adopted mainly to strike the right balance between

consumers and service providers by first, protecting consumers against unfair business practices; second,

3

providing information and education to consumers; and third, helping the aggrieved consumer in the

process of complaining and seeking redress. In addition to consumer welfare benefits, consumer

protection is expected to oblige suppliers or service providers to offer a high quality of services and

refrain from unfair business practices, thereby increasing efficiency in the marketplace (Hogarth &

English, 2002).

1.2 Problem Statement

1.2.1 Ideal Situation

In Tanzania, the task of consumer protection in the telecommunication markets is mainly left to the

regulator: Tanzania Communication Regulatory Authority (TCRA). Specifically, the regulator is the

overseer of the telecommunication markets with the responsibility of controlling the market failure by

first, ensuring a level plain field among service providers; second, offering consumer protection; and third,

managing scarce national resources such as spectrum. The regulator takes this responsibility by passing

regulations for the market (as seen in Figure 1.1), where both consumers and service providers have to

adhere to them for the telecommunication markets to operate efficiently.

For instance, to ensure that liberalized telecommunication markets operate optimally, the regulator and

policymakers have set regulations to ensure that both the demand and supply sides are protected by law.

As figure 1-2 depicts, competition regulations have been enacted to guide the supply side by ensuring a

level playing field among service providers, thus ensuring that all operators are protected and treated

equally under the law. On the other side, consumer protection has been enacted to ensure consumers are

empowered to make rational decisions and protected to obtain value for money. In other words,

competition regulations offer protection to service providers, and consumer protection regulations offer

protection and empowerment to consumers. Hence, these two regulations offer the desired balance in the

market and eliminate the possibility of market failure.

4

Figure 1-1: Telecommunication market

Multiple scholars have researched on the supply side, thus competition policy (competition and anti-trust

regulations). International Telecommunication Union (ITU) reported that competition policy is successful

in most countries; however most countries were still working on developing consumer protection. Thus,

ITU suggest that there is still a gap to be filled in the consumer protection. Therefore, this thesis will be

based on the demand side, thus consumer protection and empowerment.

Figure 1-2: Liberalized telecommunication markets

5

1.2.2 Background of Consumer Protection

Ideally, the presence of competition and consumer protection regulations should guarantee optimum

yields in the telecommunication markets. However, this is not always the case in Tanzania. This is

because while the regulator has the responsibility to ensure consumer protection, regulatory intervention

in the market is non-desirable and must be kept to a minimum. For that reason, consumer protection is

mostly offered ex-post. As a result, in case of an unpleasant experience in the market, the aggrieved

consumer is expected to act as a whistleblower. Thus, for the regulator to intervene in the market, this

consumer must first, understand that his or her rights have been violated; second, be aware of the

complaint procedure; and third, actually complain to his or her service provider, and then escalate the

complaint to the regulator if unsatisfied by the resolution offered by the service provider. This means that

unless consumers voice their complaint, the regulator cannot intervene in the market and offer the

required protection.

Consumer complaints are sometimes considered negatively, but when properly managed can be used as

feedback to improve the quality of service, thereby promoting growth in the sector. For instance, in the

case of Tanzania, consumer complaints represent chances for the regulator to intervene in the market and

offer consumer protection in two ways: first, service providers are required to submit all complaints filed

by consumers and their resolution to the regulator; and second, consumers have the chance to escalate

their complaints to the regulator when they are dissatisfied with the resolution offered by their service

provider. Thus, through the reporting of complaints by service providers and escalated complaints by

consumers, the regulator receives feedback on the challenges that consumers face. Based on complaints,

the regulator can then intervenes in the market, investigate the reported unpleasant experience, protect

consumers where necessary, and correct market abuse. For example, this was the response from the

TCRA’s Head of Corporate and Communication following an unpleasant experience that raised public

query, as reported by Tambwe (2015): “Following the number of complaints we have received from

6

numerous people and the public outcry on social media, by law we have a duty to follow up on the matter

and will only make a public statement after thorough investigations.” Of note in this response is that due

to the number of complaints, the regulator was allowed by law to intervene, investigate the matter, and

make a public statement. Thus, the ability of the consumer to complain is crucial for consumer protection.

1.2.3 Challenges Facing Consumers in the Markets

As mentioned in the previous section, consumer protection is important as it gives the regulator a chance

to intervene in the markets in the case of unpleasant experiences. The present section demonstrates some

of the challenges encountered by consumers in the telecommunication markets and why consumer

protection is important.

First, poor quality of telecommunication services still persists among service providers in African

countries including Tanzania (Appiah, 2011; Fripp, 2012; Mumo, 2016; Osuagwu, 2012; TCRA, 2015).

One of the reasons for this is an intensification of competition and technological advancements in the

sector, so that service providers are forced to simultaneously reduce the cost of services and invest

CAPEX into new technologies. Therefore, service providers sometimes have low incentives to improve

QoS in places that offer them low return (such as rural areas), as high QoS imposes more costs for

operators. Thus, unless the return on offering high QoS exceeds its cost, service providers’ incentive to do

so may be jeopardized (GSMA, 2016; Wu and Lo, 2012). In the long run, low incentive to improve QoS

among service providers may retard the growth of the telecommunication sector especially in developing

countries where the majority of the populace lives in rural areas (GSMA, 2016).

For example, the regulator in Tanzania conducted a QoS test in December 2015 (in Dar es Salaam), and

in February and March 2016 (in Dare s Salaam, Mwanza, Arusha, and Zanzibar). This revealed that the

majority of service providers were offering poor QoS compared to the required standard parameters.

However, while this offered insight to the regulator, such tests are rarely conducted. For instance, the last

published QoS test was conducted in February and March 2016 (more than a year ago). Furthermore,

7

previous QoS tests covered only four large cities. Therefore, for the most part, consumer complaints are

vital as they offer better feedback since QoS tests are not conducted periodically and do not cover the

whole country (or even rural areas).

Secondly, because QoS test is not conducted periodically and throughout the whole country, due to lack

of monitoring service providers tend not to adhere to the regulations stipulated by the regulator (Ofcom,

2009; TCRA, 2015). For instance, in February 2015, within a period of one week, three major operators

in Tanzania raised their internet prices abruptly against the tariff regulations of 2011 (TCRA, 2015). The

matter raised public concern among consumers. The regulator’s Head of Corporate and Communication,

Mr. Mungy, acknowledged receiving multiple complaints from consumers. Mr. Mungy elaborated that the

regulator does not regulate retail prices. However, because consumers complained, that by law gave the

organization the power to intervene in and investigate the matter. Following the investigation, three major

service providers were penalized for failing to adhere to regulations (Tambwe, 2015). In addition, during

the third session of the 41st parliamentary meeting on 13 June 2016, Hon. Cosato D. Chumi alleged that

service providers are conducting a great deal of unfair business practices in the telecommunication

markets.1 Due to the persistence of these unfair business practices, it is crucial for consumers to complain,

thereby bestowing power to the regulator for intervention.

In summary, consumer complaints are crucial as they give the regulator the chance to intervene in the

market and offer the required protection to consumers. However, it is also important to analyze whether

consumers have the basic information necessary to file their complaints –in other words, whether

consumers know their rights and are aware of complaint procedures.

1.3 Purpose

The problem statement section has demonstrated the importance of offering information to consumers to

empower consumer complaint behavior in the process of consumer protection in telecommunication

1 http://parliament.go.tz/polis/uploads/documents/1476712142-13JUNI,%202016.pdf

8

markets. According to information, motivation, and behavior skills (IMB) theory, conceived to

understand and explain social behaviors; information is one of the crucial aspects to attain the desirable

behavior (Fisher and Fisher’s 1992, 1993, 1999, and 2000). Moreover, Ong and Teh (2016) suggest that

consumers who are informed on what, where, and how to complain are more likely to do so or seek

redress compared to the uninformed. Similarly, Usman, Yaacob, and Rahman (2016) suggest that

consumers who are informed about consumer rights and enforcement or complaint procedures are more

likely to complain when they encounter unpleasant experiences in the marketplace. In other words,

information gives consumers the ability to communicate dissatisfaction in the market, which is crucial for

consumer protection (Brennan & Ritters, 2004).

However, to the best of the present author’s knowledge, at the time of this writing neither study has

analyzed the level of information and its determinants among consumers, nor the effect of information

(that is, consumers who knows consumer rights and are aware of the complaint procedure) on consumer

complaint behavior in the Tanzanian telecommunication markets. Studies (including (Chinedu, Haron, &

Osman, 2017; Garín-Muñoz, Pérez-Amaral, Gijón, & López, 2016)) have made contributions on

consumer complaint behavior in the telecommunication markets but have not considered the effect of

information as another factor in this behavior.

Hence, the main purpose of this thesis is to protect and empower consumers in the Tanzanian

telecommunication markets through information. Based on the IMB theory, information is an important

aspect for consumers to exhibit desired behavior. Thus, informed consumers are expected to act rationally

in the markets compared to those who are uninformed. Consequently, to protect consumers, it is vital to

equip them with basic and necessary information for them to make sound decisions. However, the level of

information among consumers, the factors affecting this level of information, and the effect of

information on consumer complaint behavior in the telecommunication market are unknown. Thus, this

thesis analyzes three subjects:

9

The level of information among telecommunication consumers,

Factors affecting the level of information among consumers, and

The effect of information on consumer complaint behavior.

Based on the findings, the thesis addresses the implications for policymakers, including the regulator,

with regard to consumer empowerment and protection.

1.4 Research Questions

Research questions have been formulated in accordance with the stipulated specific research objectives.

These questions closely examine consumers as key stakeholders in upholding consumer protection

practices in the market. In total, this thesis aims to respond to the following three research questions by

conducting in-depth analyses.

1) What is the level of consumers’ knowledge about their rights in

telecommunication markets, and what factors determine this?

Consumers’ knowledge, together with other psychological and social factors, plays an

important role in altering consumers’ behavior (Onel & Mukherjee, 2016). When

consumers have limited knowledge in the market concerning their rights, unpleasant

experiences become tenacious (CPC, 2014). A low knowledge level affects the ability of

the aggrieved consumer to file complaints, thereby lowering the opportunity for operators

and/or policymakers to correct unpleasant experiences in the market.

Knowledgeable consumers can engage more confidently and are more likely to consume

services from the markets. Thus, these consumers are the vehicle towards sustainable

competitive markets, hence growth in the sector and economy at large. Therefore, to

empower consumers, it is crucial to understand the level of consumer knowledge and

factors that determine it. As the result, the study will profile consumers and identify

10

vulnerable ones. Consequently, the recommendation for regulator and managerial policy

implication consumer protection will be drawn.

2) What is the level of consumers’ awareness of the complaint procedure in the

telecommunication markets, and what factors determine this?

In addition to knowledge of consumer rights, a proper understanding of the complaints

procedure is crucial to empower consumer complaint behavior. The Tanzanian regulator

has published the procedure to be followed by the aggrieved consumer when seeking

redress or complaining about unpleasant experiences. Ong and Teh (2016) suggest that

consumers who are aware of complaint procedures are more likely to complain when

they encounter unpleasant experiences in the market.

Thus, to empower consumer complaint behavior, it is vital to understand factors that

determine their awareness of the complaint procedure in the telecommunication market.

To this end, this research question analyzes these factors. As a result, vulnerable

consumers can be identified. Further, the results of this study deepen policymakers’

understanding of attaining the regulatory goal of empowering and protecting consumers.

Finally, the results offer useful consumers insights to managers.

3) What is the effect of information on consumer complaint behavior?

Consumer complaints are vital for consumer protection in the Tanzanian

telecommunication markets since they give the regulator the chance to intervene.

Moreover, consumer complaints offer feedback to service providers, which may lead to

improvements in QoS. The present research question analyzes the effect of information

on the consumer complaint behavior. In other words, this research question is expected to

unveil the likelihood of highly informed consumers complaining compared to those who

are less informed.

11

1.5 Contribution

Through three case studies, this thesis makes both academic and social contributions in the Tanzanian

telecommunication markets. Moreover, the results may be applicable to other countries with similar

market structures. The contributions are as follows.

1.5.1 Academic Contribution

This thesis makes an academic contribution by investigating the effect of providing information to

consumers, and how this information affects consumer behavior in the markets. To the best of the author's

knowledge, this is the first study to investigate this in the Tanzanian telecommunication markets.

Previous studies have suggested determinants of consumer complaint behavior in this context (see Figure

1-3), but none have considered the effect of information. This thesis in no way nullifies previous findings,

but rather adds to the body of literature showing that basic information is crucial to empower consumer

complaint behavior, hence consumer protection in the telecommunication markets.

Another contribution of this study is an in-depth and general understanding of the telecommunication

markets before and after the liberalization era (from 1900 to 2016), which can be used by future studies to

understand the stages of growth of telecommunication sector in Tanzania. Furthermore, the thesis focuses

on consumer protection using the case of Tanzania, and thereby contributes to the limited body of

literature on developing countries.

1.5.2 Social Contribution

The thesis makes a social contribution by determining the level of information among consumers and

identifying vulnerable consumers (those who may require extra protection and empowerment in the

markets compared to so-called “average consumers”). Furthermore, the thesis suggests means that may be

used by policymakers to create information/knowledge-based consumers. Such consumers have the

12

ability to act rationally in the markets, and can thus challenge the markets to operate optimally. In turn,

this may drive the improvement of QoS.

In addition, this thesis contributes general market insight to service providers on ways to improve their

services. For instance, while the regulator has the basic responsibilities of providing information to

consumers, part of this information must be offered by service providers, such as complaint procedures.

Every service provider has a unique complaint procedure to be followed by its consumers. Moreover,

factors influencing consumer complaint behavior may be of interest to service providers, since studies

have proved that consumers who complain to their service providers are more likely to be loyal and less

likely to adopt negative behaviors when the complaint is properly managed. All in all, the present study

offers insights to service providers that may be used as competitive advantages.

1.6 Thesis Overview

This thesis comprises nine chapters. The second chapter provides an overview of the telecommunication

markets in Tanzania before and after the liberalization era. The telecommunication sector in Tanzania can

be traced back to 1900 during the Colonial Era, and has gradually developed over time. To increase

investment in the sector, it was partially liberalized in 1993 and fully liberalized in 2005. This was

accompanied by policy reforms, which resulted in a number of regulations and legislation. Prior to 2005,

policymakers focused mostly on the supply side, on issues such as spectrum management, anti-trust

regulations, numbering planning, and creating a conducive environment for investment. Subsequently, as

the consumer base grew over time, the need for demand-related policy rose. In 2005, the first consumer

protection regulations were enacted; they were later improved in 2010. As of February 2017, the

telecommunication sector is operated by seven mobile network operators. Penetration has reached 79%,

and most operators are now working on rolling out 4G-LTE and 4.5G-LTE-A.

Next, the third chapter provides insight into the consumer protection literature and theoretical framework.

This chapter is generally based on the consumer protection manual and United Nations Consumer

13

Protection Guidelines (UNCGP). The chapter elucidates the meaning of consumer protection,

organizations responsible for consumer protection, and ways to achieve consumer protection in

liberalized markets. Furthermore, it discusses selected literature on consumer protection based on case

studies included in this thesis. Lastly, the chapter concludes by presenting the general theoretical

framework of the thesis.

The fourth chapter elucidates the methodologies used to conduct different empirical studies during the

analysis phase. The chapter focuses on the discrete probabilistic models adopted in these studies.

Specifically, it focuses on the order logistic regression model and binomial logistic regression model

adopted in the case studies.

The fifth chapter determines consumers’ knowledge levels regarding their rights. The chapter analyzes the

level and antecedent of knowledge about consumer rights among telecommunication consumers. The

study profiles consumers according to their knowledge levels and analyzes factors contributing to these

knowledge levels using the ordered logistic regression model. Following the analysis, the results and

implications are discussed.

The sixth chapter is entitled “Consumer Awareness of Complaint Procedure.” The objective of this

chapter is to analyze the level and factors contributing to consumer awareness of complaint procedures in

the telecommunication market. To this end, consumers are clustered according to their awareness level,

and then contributing factors are analyzed. The study uses the binomial logit model to analyze the

likelihood of consumers being aware of complaint procedures. Subsequently, the last sections of the

chapter present the results and implications.

The seventh chapter is entitled “Consumer Complaint Behavior in the Telecommunication Market.” The

chapter seeks to determine how information and other factors influence consumer complaint behavior.

The study analyzes the likelihood of aggrieved consumers (those who have encountered at least one

unpleasant experience in the market) voicing complaints to their service providers, and the antecedent of

14

this behavior. To determine statistical significant factors that influence consumer complaint behavior, the

study uses the binomial logistic regression model. Subsequently, the results and implications are

discussed in the last sections of this chapter.

Next, the eighth chapter is entitled “Key Findings and Implications.” This chapter mainly synthesizes the

results of the three case studies (discussed in chapters 5, 6, and 7). Subsequently, the chapter offers

implication for regulators and other key stakeholders in the telecommunication markets with regard to

consumer protection. Lastly, chapter 9 concludes this thesis by summarizing the study, discussing its

limitations, and offering directions for future research.

1.7 Summary

This chapter has generally introduced this thesis. It first presented the background of the growth and

vitality of telecommunication markets in modern society. This demonstrated the disparity in the

relationship between the demand and supply sides, which raises the need for consumer protection.

Furthermore, the chapter presented the problem statement, along with the purpose, research questions,

contribution, and organization of the thesis.

15

CHAPTER 2 THE OVERVIEW OF THE TANZANIA TELECOMMUNICATIONS MARKET

2.1 Introduction

The previous chapter introduces the subject of consumer protection in the telecommunication sector. This

chapter offers an overview of the Tanzanian telecommunications sector. The growth of the

telecommunication sector in the post-liberalization era, prior to the liberalization era, and during the

liberalization era will be discussed in detail. The gradual growth of the sector has been traced from the

end of the nineteenth century (during the colonial period) until 2016 (Deutsch, 2002; Gann and Duignan,

1969; Gann and Duignan, 1977; Ngowi, 2009).

2.2 Prior to the Liberalization Era

2.2.1 History of Tanzania

The United Republic of Tanzania was formed after the union of two states: Tanganyika (the mainland)

and Zanzibar (a coastal archipelago) (Mwakikagile, 2008). Tanganyika was a colony and part of German

East Africa from the 1880s until 1919, after World War “I” (Schabel, 1990). After World War I, from

1920, Great Britain was mandated to take over Tanganyika as a trustee territory of the League of Nations

(which was later changed to United Nations in 1945) until December of 1961 when Tanganyika achieved

its independence (Dougherty, 1966; Taylor, 1963).

On the other side, Zanzibar was under Portuguese colonial power for about two centuries starting in the

sixteen century. Later Arabs took charge of the island under the sultan of Oman (Gray, 1958; Lofchie,

1965: 23-28). Consequently, Arabs ruled for about two centuries until 1890 when the British took over as

a protectorate of Zanzibar until Zanzibar’s independence in December of 1963 (Lofchie, 1965: 52-60;

Middleton and Campbell, 1965). Later, in 1964, Tanganyika and Zanzibar were united and The United

Republic of Tanzania was born (Noam, 1999: 114).

16

2.2.2 History of the telecommunication in Tanzania

During the colonial era, communication was vital for colonial masters who would carry out their day-to-

day administrative tasks. Following this, in 1885, a postal agency was first established as a stamp for

mail; later, telegraphy services were administered by the Germany East Africa. Until the First World War

I (WWI) in 1914, the German government set up 34 telegraphy offices and more than 2537 km of

landlines (Smith, 1971). Following WWI, the British took over Tanganyika (it became their territory).

During British rule, communication services were administered by the East African Post and Telegraph

Company, which operated until 1951in three countries: Kenya, Uganda, and Tanzania. In 1951, the East

African Posts and Telecommunication Act was enacted. Consequently, the East African Post and

Telecommunication Administration was born to replace the East African Post and Telegraphy Company

(Smith, 1971).

After regaining the independence in the 1960s, the East African Community was founded in 1967. The

community was founded by leaders from Tanzania, Kenya, and Uganda. Consequently, most sectors were

managed by the community. Therefore, the East African Post and Telecommunication administration was

replaced by the East Africa Post and Telecommunication Corporation under the EAC. The EAC collapsed

ten years later, in 1977. As a result, EAC member countries were left with no option but to establish their

own telecommunication companies. Consequently, in 1978, the Tanzania Post and Telecommunication

Corporation (TPTC) was established. The TPTC operated for about fifteen years, until 1993. After this,

telecommunication was liberalized (Gorp, 2008: 52-53).

2.2.3 Policies

On the policy side, prior to 1925, the postal and telecommunication services were used only for

administrative purposes, and the sector was financed by the government through commercial loans. The

financial dependence of the post and telecommunication sector on the government limited their autonomy.

17

According to Smith (1971), the lack of autonomy affected the business growth, which led to the

retardation of the sector.

From 1925, the need for technological advancements posed another threat to the sector's growth as the

need for heavy capital expenditure rose. The development of advanced services like the wireless telegraph

and telephone required higher capital. The capital required was far from what countries were willing to

invest. The 1929 depression in East Africa made the situation even worse, as capital became scarce. As a

result, the sector`s ability to keep up the pace with consumer demand and economic development was

limited (Smith, 1971).

However, during World War II (WWII), the need for telecommunication services played a vast role.

Consequently, this raised the need for sector reforms, which attracted more investment in high

technologies and led to growth in the telecommunication sector. Consequently, in 1949, the sector

became autonomous and free of government interference. Thus, the sector was able to plan and prioritize

according to its goals and revenue. The autonomy of the sector proved to be the better policy, as the

sector grew in five-fold between 1949 and 1966.

During the formation of the East African Community in 1967, member countries decided to change the

name of the corporation yet retain previous policies. After the collapse of the community in 1977, the

Tanzania telecommunication sector was handed back to the government as a parastatal until 1993, when

liberalization reforms took place.

In summary, prior to 1993, telecommunication services were mostly used by organizations and a few

individuals. The core service offered by the telecommunication companies was a fixed telephone. The

first mobile telecommunication was not licensed until November of 1993. The main challenge which

faced the telecommunication sector was the heavy capital expenditure required to invest in new

technologies like mobile telecommunication services and the Internet. Other challenges included the lack

18

of the technical and managerial capabilities needed to match up to consumer demands and technological

advancements worldwide.

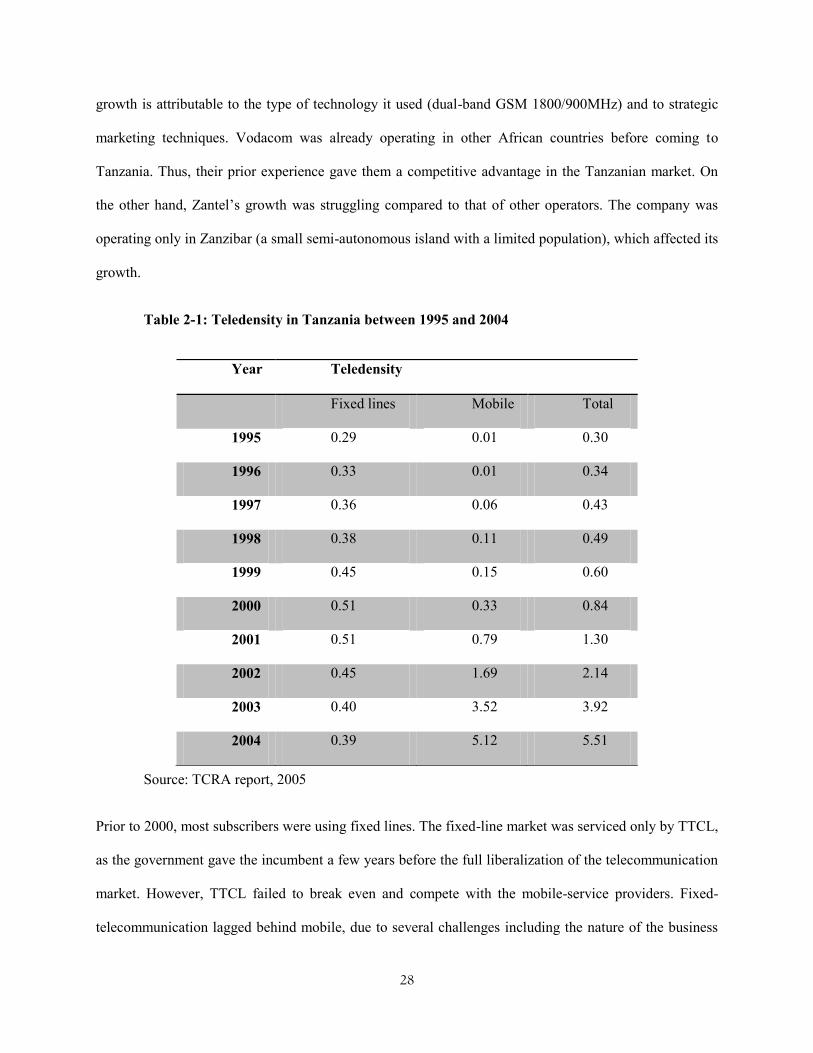

Due to the aforementioned challenges and the low penetration of electricity in the country, the

telecommunication sector was stagnant prior to liberalization. For example, there were fewer than 88,000

fixed-phone subscribers, and most of them lived in urban areas where electricity was accessible.

Therefore, to revamp the growth of the sector, the liberalization of the telecommunication sector was

inevitable.

2.3 The Liberalization-process Era

2.3.1 Introduction

The liberalization process of the telecommunication sector was a result of public sector reform, which

was part the liberalization of the general economy. This liberalization was the enactment of the

Communication Act No. 18 of 1993. Though the sector was officially liberalized in 1993, it was not fully

liberalized until 2005. This means that the liberalization process of the telecommunication sector took

twelve (12) year to be fully liberalized. Liberalization passed through several steps, which are discussed

in details in this section. The first step was to establish the regulator. The second was to commercialize

and privatize the incumbent operator. The third was partial liberalization, which was followed by full

liberalization. The liberalization process was not smooth. The process was challenging at times, because

technology was growing at high pace, the consumer base grew exponentially at a certain point, and the

business structure was changing. Therefore, the whole process required many policy reforms.

2.3.2 The Regulator: Tanzania Communication Commission (TCC)

Until 1993, the telecommunication sector was regulated by the Tanzania Postal and Telecommunication

Corporation. Following the Communication Act of 1993, Tanzania Postal and Telecommunication

Corporation was split to form the Tanzania Communication Commission (TCC), the Tanzania

19

Telecommunications Company Limited, and the Tanzania Posts Corporation. In 1994, the TCC was

established and mandated to be the overseer of the sector. In this respect, the commission had five major

functions (Noam, 1999: 118):

i. to offer licenses to operators of telecommunication services

ii. to uphold fair competition among operators

iii. to license and manage the use of satellites and spectra

iv. to endorse communication tariffs and equipment to be used to provide

telecommunication services, and

v. to promote telecommunication penetration in the rural areas.

Upon looking closely at the regulatory functions, we can see that most of them were keen on the supply

side. The main challenges ahead of this newly established commission were to create a conducive

environment for investors (operators) by managing scarce resources like spectra and aid penetration

especially in rural areas. In tackling the aforementioned challenges, the commission had to invest in

developing human resources and in improving its technical capabilities to catch up with growth of the

world. Also, the commission was geared to foster telecommunication penetration into rural areas.

Therefore, the commission set up the rural telecommunication development fund. As a result, all licensed

operators were obligated to contribute a certain amount of their profits to the fund.

2.3.3 Policy and regulations

2.3.3.1 National Telecommunication Policy 1997

Telecommunication policy reforms were pushed further in 1997 when the National Telecommunication

Policy (NTP) was launched. The National Telecommunication Policy set the action plan of the ICT in

Tanzania between 1997 and 2020. The plan outlined objectives and strategies during this time. The NTP

objectives were, first to ensure the growth of the telecommunication sector by improving the

20

telecommunication-network infrastructure and universal service access to the rest of the population, and

second, to encourage the use of telecommunication services by all sectors of the economy national wide.

The third, long-term objective was geared toward promoting public-private investment in the sector and

to improve the quality of and access to the service. The definite target was to reach a telephone density of

six phone lines per one-hundred inhabitants over a planned period.

Before the full liberalization of the telecommunication sector, Tanzania was lagging behind (with only

0.32 telephones per 100 inhabitants) in comparison to Kenya (0.92), Europe (35.36) and the world (10.49)

(MST, 1997:1). Many efforts were needed to boost the telecommunication sector, which was still in its

infancy. Consequently, considering the sectors` dynamics, the NTP suggested that the TCC should

collaborate in setting standards both with international organizations like World Trade Organization

(WTO) and International Telecommunication Union (ITU) and with local organizations like Tanzania

Bureau of Standard (TBS).

Furthermore, the NTP focused on the improving technical, business, and managerial skills. Therefore, for

management purposes, an institution framework was put forward. The framework was clearly emphasized

in the NTP, and the roles of the government, the regulator (TCC), and telecommunication operators were

explained. The legal framework was also made clear and transparent. Also, regulations concerning

competition and tariffs were made clear to ensure that all players could have equal rights in the market.

Furthermore, the policy insisted on a rural development telecommunication fund to ensure that all villages,

including those in rural areas, will be connected by the year 2020.

2.3.3.2 National Information and Communications Technologies Policy 2003

As a result of the NTP strategies, the teledensity grew to 1.2 per hundred inhabitants (MST, 2003:3),

though penetration was concentrated in the capital city (Dar es Salaam). This was the great achievement

for the sector. However, the demand for growth was to catch up with the world pace. At that point, the

main challenge was to penetrate services into rural areas.

21

Another challenge arose during the turn of the millennium as technological advancements in the world led

to the convergence of content, telecommunication computing, and broadcasting, thereby raising the need

for policy intervention and regulations (Henten, Falch, and Tadayoni 2002). Therefore, the new national

informational and communication technologies policy was put forward in 2003. The policy carried the

vision and mission of ICT Tanzania from 2003 to 2025.

The main vision was to make Tanzania the hub of ICT in the region. Another vision was to use ICT to

promote socio-economic growth, thereby to speed up the poverty-eradication rate. To attain the vision,

the strategy was to create an environment conducive to investment through capacity building by

promoting the use of ICT by the commercial sector (e-commerce) and public sectors (e-government) and

by encouraging partnership and knowledge sharing both locally and globally.

2.3.3.3 Tanzanian Communication Regulatory Authority (TCRA) Act 2003

The TCRA act was passed in April of 2003. The act gave provision to the enactment of the Tanzania

Communication Regulatory Authority (TCRA). The TCRA was formed after the Tanzania

Communication Commission (TCC) was merged with the Tanzania Broadcasting Commission (TBC).

The TCRA was formed in response to technological advancements which had eroded boundaries between

the telecommunication and broadcasting sectors. For instance, while traditionally the consumer was

required to have broadcast media like radio or television to watch the news, as technology evolved, the

consumer was able to stream broadcast content over the Internet. Therefore, to improve the efficiency of

the market economies and the effectiveness of regulations the need of having one authority to regulate

both media (broadcast) and telecommunication sector was high (Henten, Samarajiva, and Melody, 2003).

Therefore, in 2003, the TCRA Act No. 12 was enacted.

The TCRA act gave provision for the following:

i) functions and responsibilities of the authority,

ii) power and proceedings of the authority,

22

iii) content committee and its functions,

iv) roles and functions of Tanzania Broadcast Services as part of TCRA,

v) roles and functions of TCRA Consumer Consultative Council (TCRA-CCC)

vi) complaints and dispute resolution, and

vii) financial provision for the authority (TCRA).

Tanzania was among the earliest Sub-Saharan country to have the converged regulator. TCRA’s main

vision was to be a high-class regulator. The mission was to create a level playing field among players

(service providers), a pleasant environment for investors and accessible and affordable services to

consumers—including those living in underserved areas. In attaining their functions, the regulator's role

was to,

i. promote effective competition and economic efficiency;

ii. protect consumers` interest;