construction defect claims: horizontal vs....

TRANSCRIPT

Construction Defect Claims: Horizontal vs. Vertical

Exhaustion of Insurance Coverage Navigating Exhaustion of Primary Policies, Triggers for Excess

Carriers and Additional Insured Coverage

Today’s faculty features:

1pm Eastern | 12pm Central | 11am Mountain | 10am Pacific

The audio portion of the conference may be accessed via the telephone or by using your computer's

speakers. Please refer to the instructions emailed to registrants for additional information. If you

have any questions, please contact Customer Service at 1-800-926-7926 ext. 10.

TUESDAY, SEPTEMBER 24, 2013

Presenting a live 90-minute webinar with interactive Q&A

Richard B. Friedman, Partner, McKenna Long & Aldridge, New York

David G. Jordan, Associate, Saxe Doernberger & Vita, Hamden, Conn.

Rebecca DiMasi, Partner, Van Osselaer & Buchanan, Austin, Texas

Sound Quality

If you are listening via your computer speakers, please note that the quality of

your sound will vary depending on the speed and quality of your internet

connection.

If the sound quality is not satisfactory and you are listening via your computer

speakers, you may listen via the phone: dial 1-866-927-5568 and enter your PIN

when prompted. Otherwise, please send us a chat or e-mail

[email protected] immediately so we can address the problem.

If you dialed in and have any difficulties during the call, press *0 for assistance.

Viewing Quality

To maximize your screen, press the F11 key on your keyboard. To exit full screen,

press the F11 key again.

FOR LIVE EVENT ONLY

For CLE purposes, please let us know how many people are listening at your

location by completing each of the following steps:

• In the chat box, type (1) your company name and (2) the number of

attendees at your location

• Click the SEND button beside the box

If you have purchased Strafford CLE processing services, you must confirm your

participation by completing and submitting an Official Record of Attendance (CLE

Form).

You may obtain your CLE form by going to the program page and selecting the

appropriate form in the PROGRAM MATERIALS box at the top right corner.

If you'd like to purchase CLE credit processing, it is available for a fee. For

additional information about CLE credit processing, go to our website or call us at

1-800-926-7926 ext. 35.

FOR LIVE EVENT ONLY

If you have not printed the conference materials for this program, please

complete the following steps:

• Click on the ^ sign next to “Conference Materials” in the middle of the left-

hand column on your screen.

• Click on the tab labeled “Handouts” that appears, and there you will see a

PDF of the slides for today's program.

• Double click on the PDF and a separate page will open.

• Print the slides by clicking on the printer icon.

FOR LIVE EVENT ONLY

Richard B. Friedman

McKenna Long & Aldridge LLP, New York, New York

David G. Jordan

Saxe Doernberger & Vita, P.C., Hamden, Connecticut

Rebecca DiMasi

Van Osselaer & Buchanan, LLP, Austin, Texas

Strafford Webinar

September 24. 2013

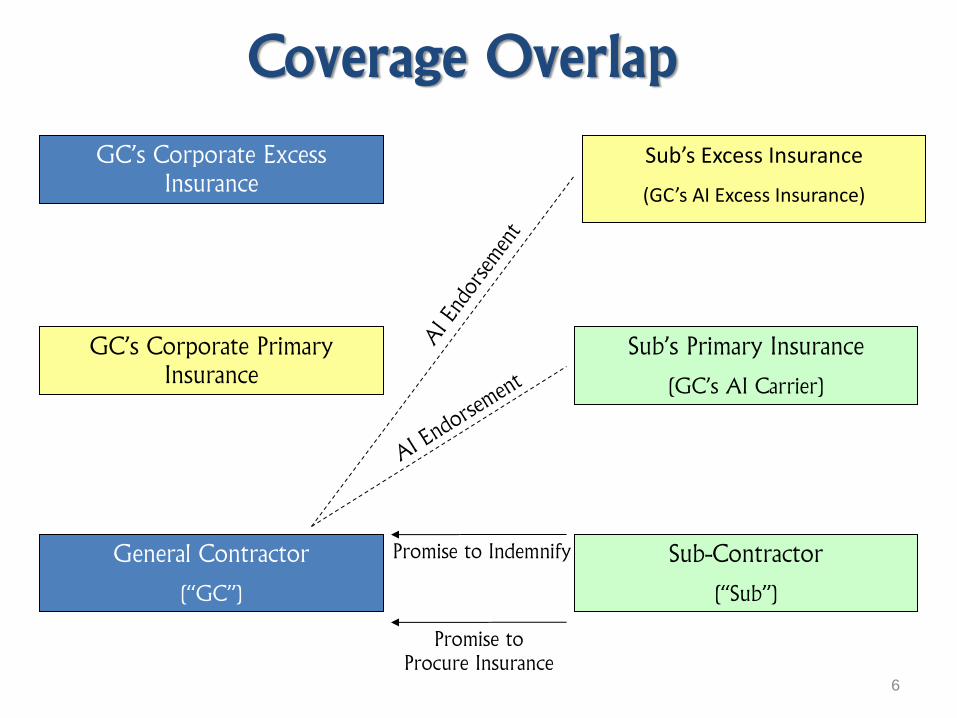

Coverage Overlap

General Contractor

(“GC”)

GC’s Corporate Primary

Insurance

GC’s Corporate Excess

Insurance

Sub-Contractor

(“Sub”)

Sub’s Primary Insurance

(GC’s AI Carrier)

Sub’s Excess Insurance

(GC’s AI Excess Insurance)

Promise to Indemnify

Promise to

Procure Insurance

www.sdvlaw.com 6

Relevant Issues

Multiple parties

Multiple layers of coverage in AI context

Loss exceeds limits of a single primary

policy

7

Which Insurer Responds First?

Typically primary insurer of downstream party (Additional Insured Carrier) has initial

obligation to defend and indemnify the claim.

Priority is established by “Other Insurance” language commonly found in most CGL Policies

e.g. This insurance is excess over: Any other primary insurance available to you covering you for damages … for which you have been added as an additional insured by attachment of an endorsement.

When such language is not present, primary carriers of Upstream and Downstream Parties

may dispute priority. See e.g. Briarwoods Farm, Inc. v. Cent. Mut. Ins. Co., 22 Misc. 3d

427, 428, 866 N.Y.S.2d 847, 848 (Sup. Ct. 2008).

Which Insurer Responds Second?

The AI Excess carrier OR the corporate primary policy?

Disputes arise when, as is often the case, the subcontractor’s

primary CGL policy is insufficient to cover the loss to the injured party.

8

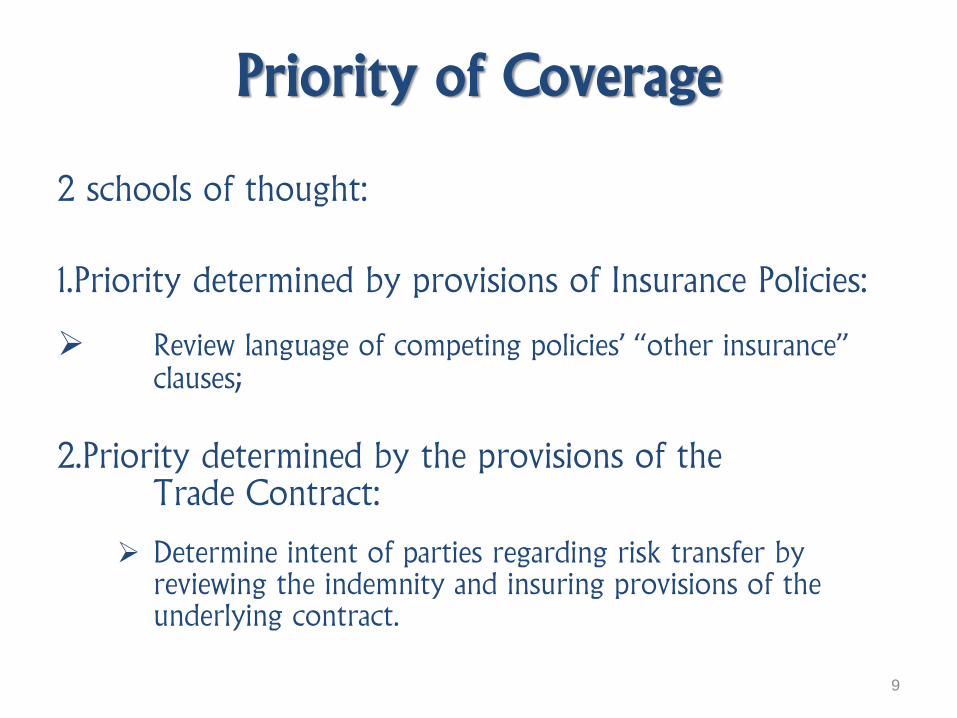

Priority of Coverage

2 schools of thought:

1.Priority determined by provisions of Insurance Policies:

Review language of competing policies’ “other insurance” clauses;

2.Priority determined by the provisions of the Trade Contract:

Determine intent of parties regarding risk transfer by reviewing the indemnity and insuring provisions of the underlying contract.

9

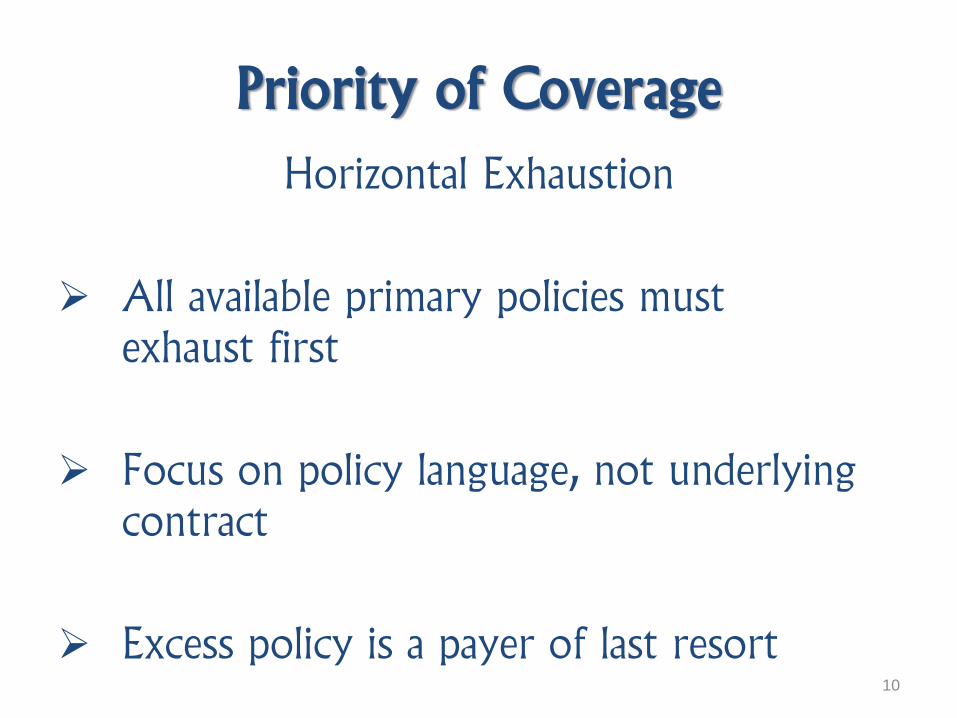

Priority of Coverage

Horizontal Exhaustion

All available primary policies must

exhaust first

Focus on policy language, not underlying

contract

Excess policy is a payer of last resort 10

Priority of Coverage Vertical Exhaustion

AI policies (primary & excess) exhaust before upstream party’s primary policy

Focus on underlying contract’s indemnity obligation, not policy language

Reflects intent of parties

Avoids circuity of litigation 11

Priority of Coverage

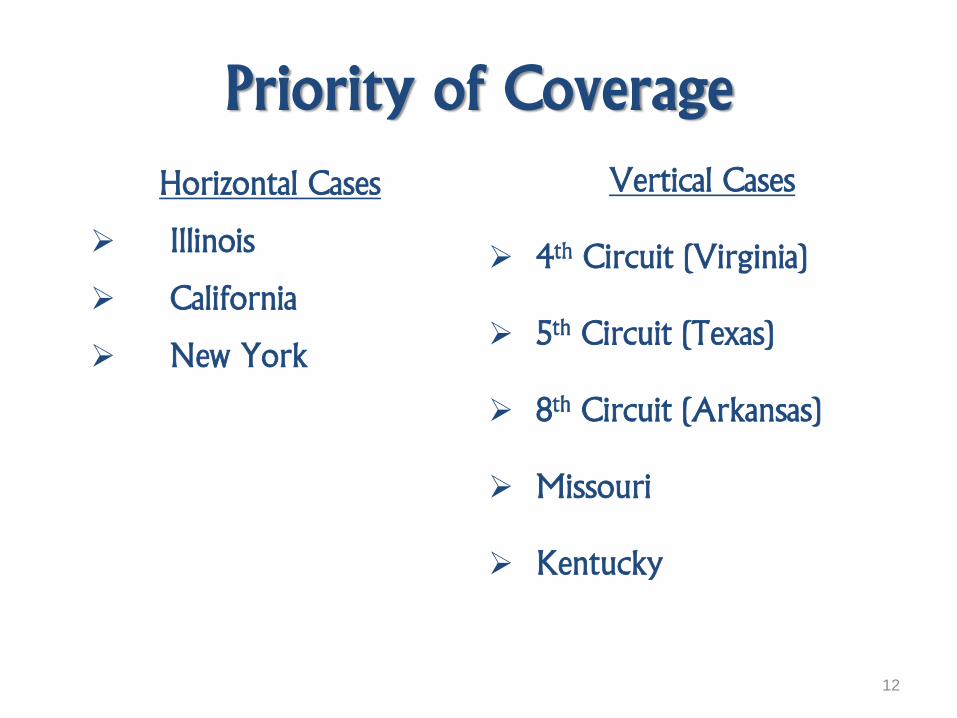

12

Horizontal Cases

Illinois

California

New York

Vertical Cases

4th Circuit (Virginia)

5th Circuit (Texas)

8th Circuit (Arkansas)

Missouri

Kentucky

12

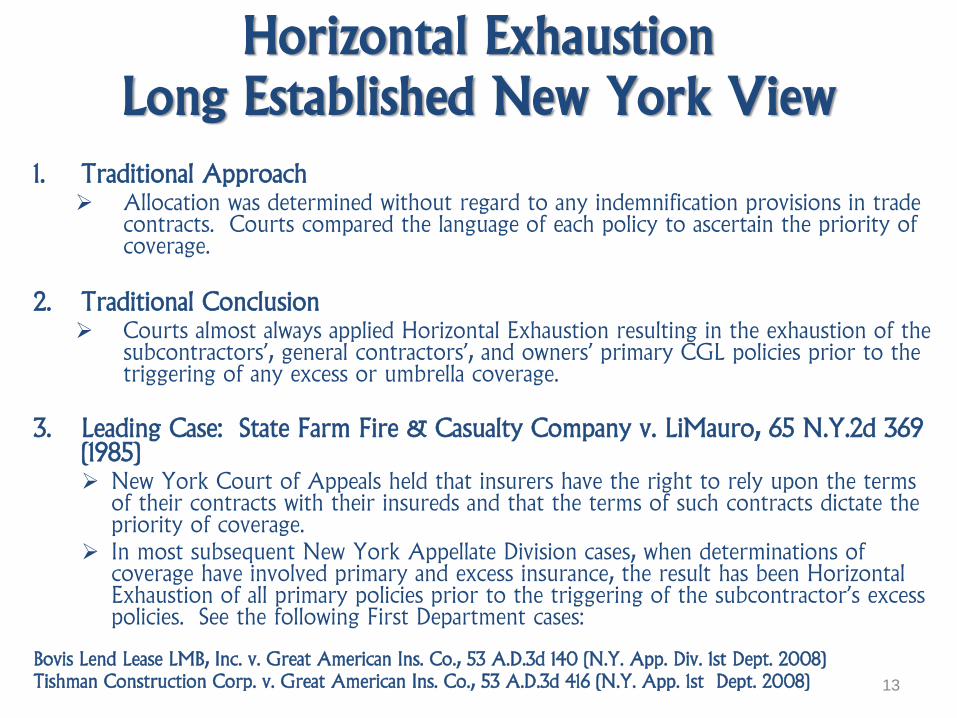

1. Traditional Approach Allocation was determined without regard to any indemnification provisions in trade

contracts. Courts compared the language of each policy to ascertain the priority of coverage.

2. Traditional Conclusion Courts almost always applied Horizontal Exhaustion resulting in the exhaustion of the

subcontractors’, general contractors’, and owners’ primary CGL policies prior to the triggering of any excess or umbrella coverage.

3. Leading Case: State Farm Fire & Casualty Company v. LiMauro, 65 N.Y.2d 369 (1985) New York Court of Appeals held that insurers have the right to rely upon the terms

of their contracts with their insureds and that the terms of such contracts dictate the priority of coverage.

In most subsequent New York Appellate Division cases, when determinations of coverage have involved primary and excess insurance, the result has been Horizontal Exhaustion of all primary policies prior to the triggering of the subcontractor’s excess policies. See the following First Department cases:

Bovis Lend Lease LMB, Inc. v. Great American Ins. Co., 53 A.D.3d 140 (N.Y. App. Div. 1st Dept. 2008)

Tishman Construction Corp. v. Great American Ins. Co., 53 A.D.3d 416 (N.Y. App. 1st Dept. 2008)

Horizontal Exhaustion

Long Established New York View

13

Horizontal Exhaustion - Bovis

Elevator Sub.

(AJ MCNULTY)

Great American

Decedent

Const. Mgr.

(BOVIS)

Illinois $1M Primary Policy

Gen. Ctr.

(STONEWALL)

Liberty $1M Primary

Policy

Westchester $10M

Umbrella

Concrete Sub.

(J&A)

QBE $1M Primary

United $5M Umbrella

Steel Ctr.

(SMI-OWEN)

Owner

(DASNY)

Horizontal Exhaustion: The Bovis Case

14

Horizontal Exhaustion: The Bovis Case Trial Court Apportionment of AI Coverage for Bovis

QBE

$1,000,000

J&A Primary

ILLINOIS

$1,000,000

BOVIS Primary

WESTCHESTER

$10,000,000

Stonewall Umbrella

UNITED

$5,000,000

J&A Umbrella

LIBERTY

$1,000,000

Stonewall Primary

15

Appellate Court Apportionment of AI Coverage for Bovis

QBE

$1,000,000

J&A Primary

LIBERTY

$1,000,000

Stonewall Primary

ILLINOIS

$1,000,000

BOVIS Primary

UNITED

$5,000,000

J&A Umbrella

WESTCHESTER

$10,000,000

Stonewall Umbrella Sharing pro rata

Horizontal Exhaustion: The Bovis Case

16

Vertical Exhaustion

Indemnity/Circuity of Litigation

Wal-Mart Stores, Inc. v RLI Ins. Co., 292

F.3d 583 (8th Cir 2002)

American Indemnity Lloyds v Travelers

Property Casualty Ins. Co., 335 F.3d 429 (5th Cir 2003)

17

Vertical Exhaustion: The Wal-Mart Case

National Union

$10M Primary

Wal-Mart Retailer

RLI

$10M Excess

Cheyenne - Manuf.

Contract – required $2M Primary

Obtained - $1M Primary/$10M Excess

Settlement - $11M: St. Paul $1M/RLI $10M

DJ – Wal-Mart and National Union sought to avoid contributing to $10M paid by RLI

Result – St. Paul $1M/RLI $10M

2

1

AI Status

Indemnity

St. Paul

$1M Primary

3

18

Horizontal Approach

GC

Sued

GC

tenders to AI

primary and AI

Excess

carrier

AI primary pays but AI

Excess asserts GC’s

corporate primary must

pay next

GC’s primary

pays

AI excess

carrier pays (GC

corporate limits

replenished)

Subcontractor tenders indemnity lawsuit to its

excess carrier (b/c primary carrier

exhausted)

GC’s

primary subrogates

to GC’s interests

and sues

Subcontractor for

indemnity

Circuity of Litigation Vertical exhaustion avoids “Circuity of Litigation”:

unnecessary legal steps which result in AI excess carrier

paying for loss

19

Upstream insurers argue against “circuity of litigation”, i.e., that it is

a waste of judicial resources to require them to pay for their portion

of the allocated loss and then have to recoup, via subrogation, that

payment from the subcontractor’s excess carrier.

Vertical Approach

GC Sued GC tenders

to AI

primary and

AI Excess

AI primary

pays first,

then AI

Excess

carrier

pays

Circuity of Litigation

20

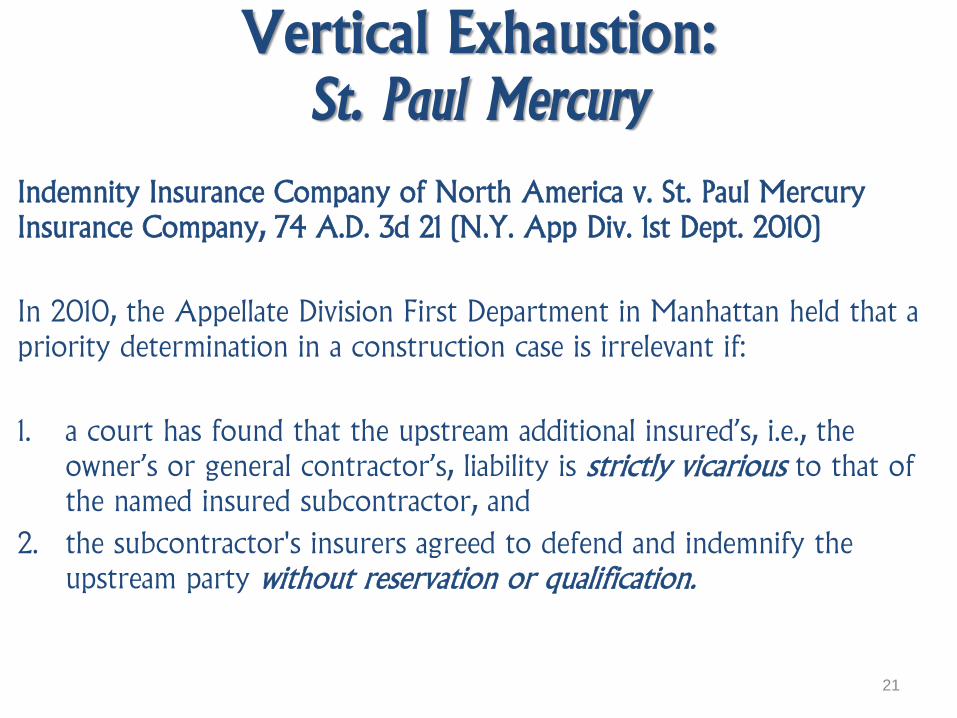

Indemnity Insurance Company of North America v. St. Paul Mercury

Insurance Company, 74 A.D. 3d 21 (N.Y. App Div. 1st Dept. 2010)

In 2010, the Appellate Division First Department in Manhattan held that a

priority determination in a construction case is irrelevant if:

1. a court has found that the upstream additional insured’s, i.e., the

owner’s or general contractor’s, liability is strictly vicarious to that of

the named insured subcontractor, and

2. the subcontractor's insurers agreed to defend and indemnify the

upstream party without reservation or qualification.

Vertical Exhaustion:

St. Paul Mercury

21

St. Paul Mercury

ROMANO (Sub)

YONKERS (GC)

Excess $10 M

Indemnity Ins.

Primary $1 M Royal

Excess $5 M

St. Paul

Primary $1 M

St. Paul

Contractual Indemnity

Additional Insured

Horizontal Exhaustion

CIRCUITY – Indemnity Ins. can force St. Paul Primary to pay first under principle of

horizontal exhaustion but Yonkers could then pass that liability back to Romano via

contractual indemnity, which would flow back to Indemnity Ins. Court shortcuts that result by simply holding that horizontal exhaustion does not apply. 22

1. General contractors and owners with contractual indemnity rights against

subcontractors should seek to establish as soon as possible their right to

contractual indemnity against subcontractors.

This can be done via a third party claim in the underlying action brought by the

injured party.

If a right to contractual indemnity is established prior to a determination regarding

the priority of coverage, the upstream insurers should argue that, under St. Paul

Mercury, the upstream parties’ liability passes to the subcontractors and its insurer,

and thus the priority of coverage is irrelevant.

2. Upstream insurers should also be aware that St. Paul Mercury is not binding in

New York other than in the First Appellate Department. And, even in the First

Department, Bovis and Tishman are still good law.

3. Although Horizontal Exhaustion remains generally the law In New York, St. Paul

Mercury provides insurers with the ammunition to argue for greater use of

Vertical Exhaustion in certain circumstances.

Action Points For General Contractors And Owners

and Their Insurers in light of St. Paul Mercury

23

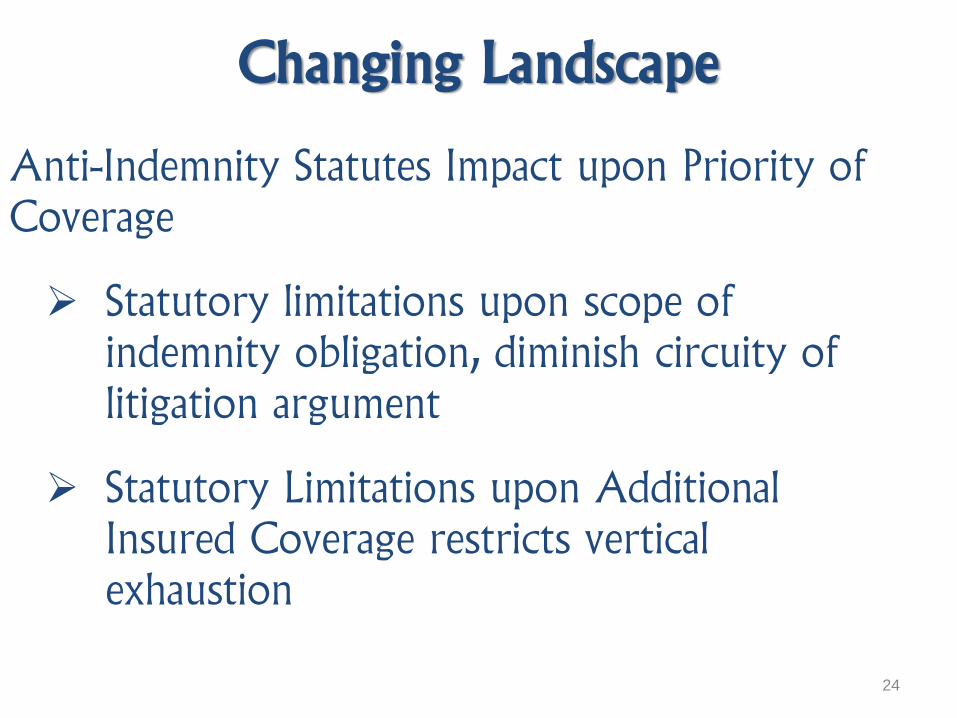

Changing Landscape

Anti-Indemnity Statutes Impact upon Priority of

Coverage

Statutory limitations upon scope of

indemnity obligation, diminish circuity of

litigation argument

Statutory Limitations upon Additional

Insured Coverage restricts vertical

exhaustion

24

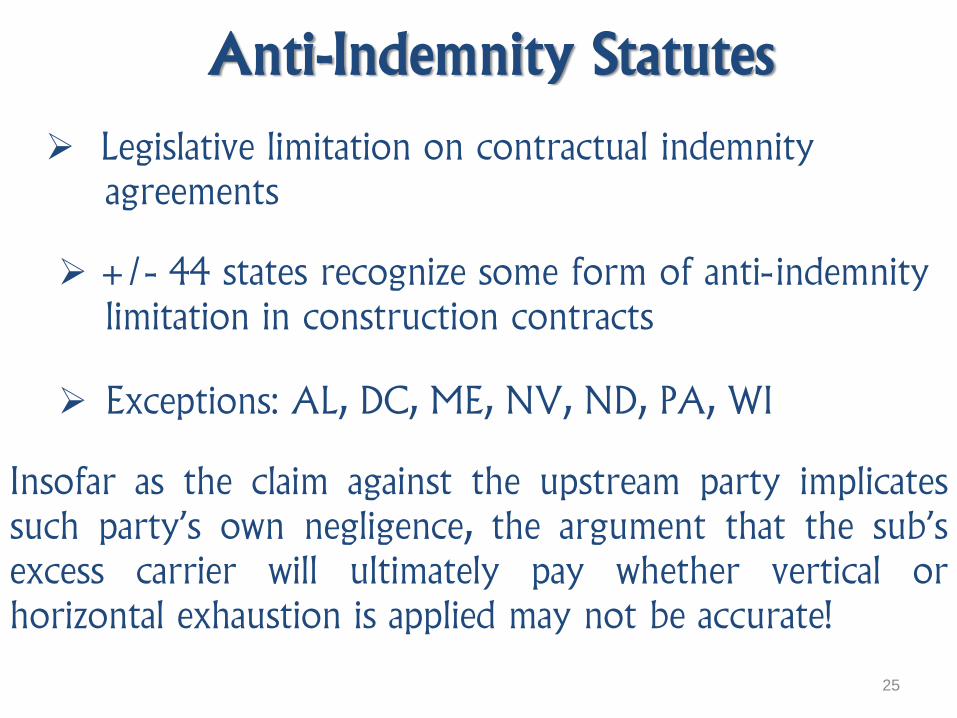

Anti-Indemnity Statutes

Legislative limitation on contractual indemnity

agreements

+/- 44 states recognize some form of anti- indemnity

limitation in construction contracts

Exceptions: AL, DC, ME, NV, ND, PA, WI

Insofar as the claim against the upstream party implicates

such party’s own negligence, the argument that the sub’s

excess carrier will ultimately pay whether vertical or

horizontal exhaustion is applied may not be accurate!

25

Anti-Indemnity Statutes:

Insurance Implications A number of states preclude GC from Requiring Sub to

obtain AI coverage which protects GC from its own negligence

e.g., California, Colorado, Kansas, Louisiana, Michigan, Montana, New Mexico, Oklahoma, Oregon and Texas

A few states have given some (but not a clear) indication that the anti-indemnity prohibition extends to insurance

e.g., Delaware, Georgia and Ohio

To the extent claims against the additional insured implicate its own negligence, the AI Coverage and GC’s own coverage may both be required to provide indemnity

26

Changing Landscape

Evolution of ISO AI Coverage

Limitations upon the Scope of AI coverage directly impact the

Horizontal / Vertical Exhaustion Debate. 27

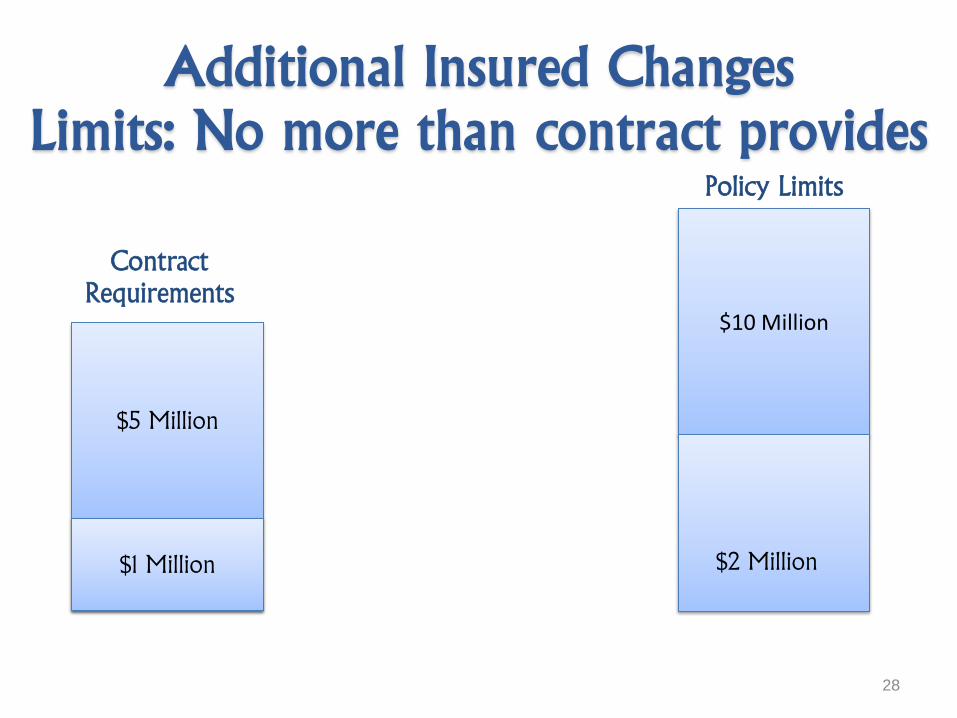

Additional Insured Changes

Limits: No more than contract provides

$10 Million

$2 Million

$5 Million

$1 Million $1 Million

Contract

Requirements

Policy Limits

28

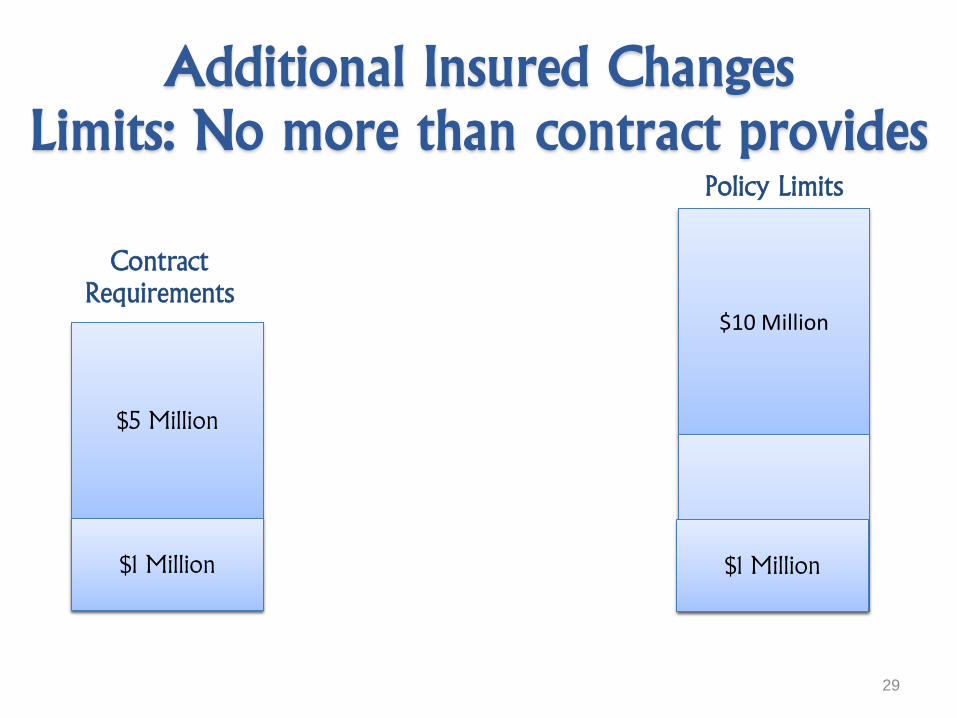

Additional Insured Changes

Limits: No more than contract provides

$10 Million

$2 Million

$5 Million

$1 Million $1 Million

Contract

Requirements

Policy Limits

29

$1 Million

$10 Million

Additional Insured Changes

Limits: No more than contract provides

$2 Million

$5 Million

$1 Million $1 Million

$1 Million GAP

Contract

Requirements

Policy Limits

30

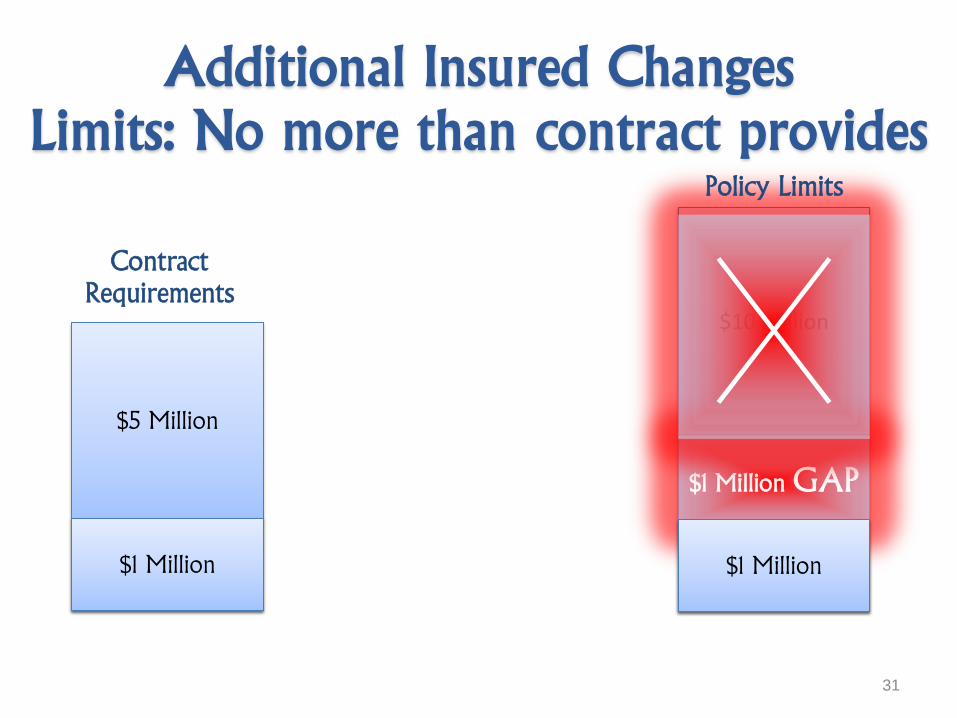

$1 Million

Additional Insured Changes

Limits: No more than contract provides

$10 Million

$2 Million

$5 Million

$1 Million $1 Million

$1 Million GAP

Contract

Requirements

Policy Limits

31

$1 Million

32

What happens when the insured settles with the

primary carrier for less than policy limits?

It depends on your jurisdiction and policy language . . .

33

Zeig v. Massachusetts Bonding & Ins. Co.,

23 F.2d 665 (2d Cir. 1928)

Settlement by insured with primary carrier did

not eliminate excess coverage

Excess carrier – no rational interest in whether

insured collected full primary limits

Public policy: delay, promotion of litigation,

chilling effect on settlements

But parties could impose conditions precedent if

they chose to do so…

34

Cases following the Zeig rationale:

Koppers Company, Inc. v. Aetna Casualty and Surety Company,

98 F.3d 1440 (3d Cir. 1996) (Pennsylvania law) (court did not focus

on policy language; settlement with primary carrier “functionally

exhausted” primary policy)

Trinity Homes, LLC v. Ohio Casualty Insurance Company, 629

F.3d 653 (7th Cir. 2010) (Indiana law) (policy was ambiguous; did

not clearly require payment of full CGL limit)

Rummel v. Lexington Insurance Company, 123 N.M. 752, 945 P.2d

970 (N.M. 1997) (policy language – “liability of the Company

under this policy shall not attach unless and until the Insured’s

Underlying insurance has been paid or has been held liable to pay

the total applicable underlying limits” – did not preclude

underlying insurer from settling for less than its limits and being

credited for the balance)

35

Comercia Inc. v. Zurich American Insurance Co.,

498 F.Supp.2d 1019 (E.D. Mich. 2007)

Distinguished Zeig - lack of specificity in excess

policy language

Different result with specific policy language

Public policy favors settlements, but can not

supersede unambiguous policy language

Policy required “actual payment of losses” by the

underlying insurer

36

Cases following the Comercia rationale:

Citigroup, Inc. v. Federal Insurance Company, 649 F.3d

367 (5th Cir. 2011) (excess policies not ambiguous; plain

language dictated primary carrier pay full limits before

excess coverage was triggered)

Qualcomm, Incorporated v. Certain Underwriters at

Lloyd’s, 161 Cal.App.4th 184, 73 Cal.Rptr.3d 770 (Cal.

Ct. App. 2008) (policy language was not ambiguous;

did not apply Zeig because it placed policy

considerations above plain language, employed a

strained interpretation of “payment,” and stated that

parties could use express language)

37

Policy language supporting no excess coverage:

Citigroup, Inc. v. Federal Ins. Co., 649 F.3d 367, 372-73 (5th Cir.

2011) (emphasis added)

“(a) all Underlying Insurance carriers have paid in cash the full amount of their respective liabilities, (b) the full amount of the

Underlying Insurance policies have been collected by the plaintiffs,

the Insureds or the Insureds’ counsel, and (c) all Underlying

Insurance has been exhausted.”

“The insurer shall only be liable to make payment under this policy

after the total amount of the Underlying Limit of Liability has been

paid in legal currency by the insurers of the Underlying Insurance.”

“only after any Insurer subscribing to any Underlying Policy shall

have agreed to pay or have been held liable to pay the full amount of its respective limits . . .”

“in the event of the exhaustion of all of the limit(s) of liability of

such ‘Underlying Insurance’ solely as a result of payment of loss thereunder.”

Policy language supporting no excess coverage:

Qualcomm, Inc. v. Certain Underwriters at Lloyd’s, 161 Cal.App.4th 184, 73 Cal.Rptr.3d 770 (Cal. Ct. App. 2008)

“Underwriters shall be liable only after the insurers under each of the Underlying Policies have paid or have been held liable to pay the full amount of the Underlying Limit of Liability.”

Comercia Inc. v. Zurich American Insurance Co., 498 F.Supp.2d 1019 (E.D. Mich. 2007)

Policy required “actual payment of losses” by underlying insurer, and stated that the “policy does not provide coverage for any loss not covered by the ‘Underlying Insurance’ solely by reason of the reduction or exhaustion of the available ‘Underlying Insurance’ through payments of loss thereunder.”

38

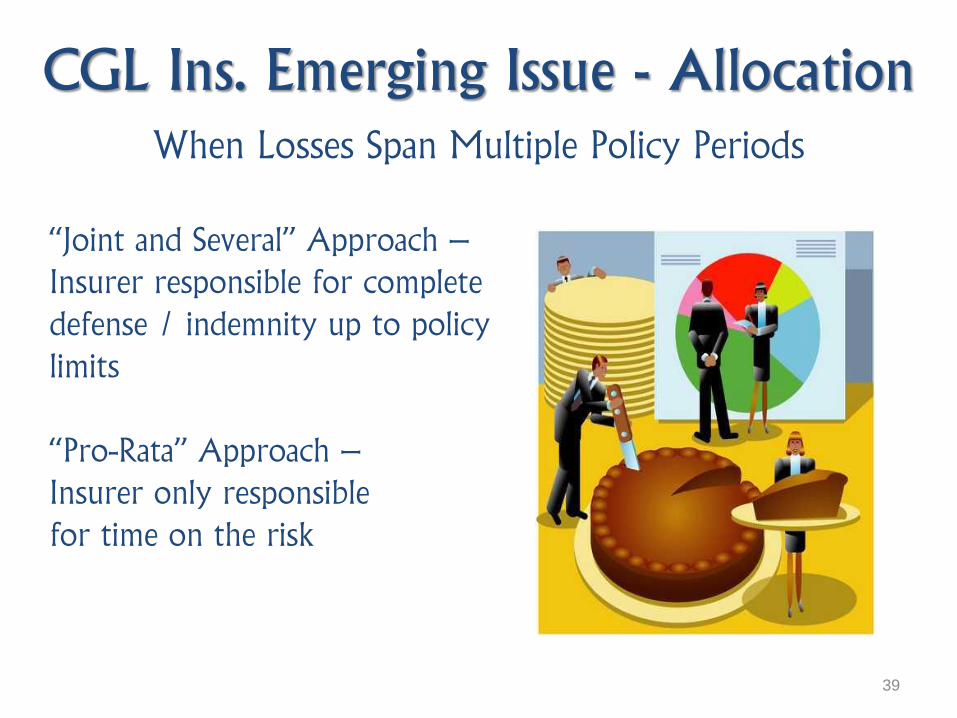

CGL Ins. Emerging Issue - Allocation

When Losses Span Multiple Policy Periods

“Joint and Several” Approach –

Insurer responsible for complete

defense / indemnity up to policy

limits

“Pro-Rata” Approach –

Insurer only responsible

for time on the risk

39

Consolidated Ins. Programs:

A.K.A “Wrap Ups”

Helps avoid much of the finger pointing and allocation arguments involved when projects are insured by traditional programs

40

Review all relevant policies to assess scope, limits, and “other

insurance” provisions

Determine applicable state/jurisdiction that may govern the

policies and the trade contract(s)

Upstream Parties (e.g., General Contractors and Owners) should

insist upon “primary and non-contributory” language in

downstream parties’ (e.g., Subcontractors’) insurance policies

Upstream Parties should seek to include a vertical exhaustion

provision in their own insurance policies

Consider whether a consolidated insurance (a/k/a “wrap-up”)

program is cost-effective and otherwise appropriate for your

project

TAKE AWAYS

41