consolidated half -year financial report as of 30 … · consolidated half -year financial report...

TRANSCRIPT

1

CONSOLIDATED HALF-YEAR FINANCIAL REPORT AS OF 30 JUNE 2016 OF THE TERNIENERGIA GROUP

2

CORPORATE INFORMATION

TerniEnergia S.p.A.

Registered office in Strada dello Stabilimento 1, 05035 Narni (TR)

Authorised, issued and paid-up share capital: Euro 57,007,230

Terni Register of Companies No. 01339010553

Branches and Offices

Narni – Strada dello Stabilimento 1

Milan – Corso Magenta, 85

Lecce – Via Costadura, 3

Athens – 52, Akadimias Street

Cape Town - Boulevard Office Park, 2nd floor, Block D, Searle. District of Woodstock

Warsaw - Sw. Krolewska 16, 00-103

Bucharest - Str. Popa Petre 5

Board of Directors

Chairman and CEO

Stefano Neri

Directors

Massimiliano Salvi

Fabrizio Venturi

Monica Federici

Laura Bizarri

Paolo Ottone Migliavacca

Mario Marco Molteni

Domenico De Marinis

Laura Rossi

Board of Statutory Auditors

Ernesto Santaniello (Chairman)

Marco Chieruzzi (*)

Simonetta Magni

(*) replaces Vittorio Pellegrini as from 7 June 2016

Independent auditors

PriceWaterhouseCoopers S.p.A.

3

Contents

1. REPORT ON OPERATIONS ............................................................................................................................... 5

1.1 THE GROUP’S BUSINESS AND MISSION ......................................................................................... 5

1.2 THE GROUP’S STRUCTURE ............................................................................................................ 6

1.3 MAIN EVENTS DURING THE FINANCIAL PERIOD ENDED 30 JUNE 2016 .......................................... 7

1.4 PERFORMANCE OF OPERATIONS ................................................................................................ 13

1.5 GROUP ECONOMIC RESULTS ...................................................................................................... 15

1.6 OVERVIEW OF STATEMENT OF FINANCIAL POSITION .................................................................. 17

1.7 STATEMENT OF RECONCILIATION OF THE PARENT COMPANY’S OPERATING RESULT AND

SHAREHOLDERS’ EQUITY WITH THE CONSOLIDATED RESULTS AS AT 30 JUNE 2016 ............................... 21

1.8 INVESTMENTS ............................................................................................................................ 22

1.9 HUMAN RESOURCES .................................................................................................................. 22

1.10 RISK FACTORS RELATED TO THE REFERENCE SECTOR .................................................................. 23

1.11 RELATIONS WITH RELATED PARTIES ........................................................................................... 24

1.12 INFORMATION REQUIRED BY ART. 123 BIS OF THE T.U.F. (CONSOLIDATED FINANCIAL ACT) ........ 24

1.13 OTHER INFORMATION................................................................................................................ 26

1.14 SIGNIFICANT EVENTS AFTER THE END OF THE PERIOD CLOSED AS AT 30 JUNE 2016 ................... 29

1.15 BUSINESS OUTLOOK ................................................................................................................... 29

2 FINANCIAL STATEMENTS ....................................................................................................................... 31

2.1 CONSOLIDATED STATEMENT OF FINANCIAL POSITION ................................................................ 31

2.2 CONSOLIDATED INCOME STATEMENT ........................................................................................ 31

2.3 CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME ....................................................... 33

2.4 STATEMENT OF CHANGES IN CONSOLIDATED SHAREHOLDERS’ EQUITY ...................................... 34

2.5 CONSOLIDATED CASH FLOW STATEMENT ................................................................................... 35

3 EXPLANATORY NOTES TO THE CONSOLIDATED INTERIM FINANCIAL STATEMENTS AS AT 30 JUNE 2016 . 36

3.1 GENERAL INFORMATION ............................................................................................................ 36

3.2 SEGMENT REPORTING ................................................................................................................ 36

3.3 FORM, CONTENT AND APPLIED ACCOUNTING PRINCIPLES .......................................................... 38

3.4 COMMENTS ON THE MAIN STATEMENT OF FINANCIAL POSITION ITEMS .................................... 43

3.4.1 INTANGIBLE FIXED ASSETS.......................................................................................................... 43

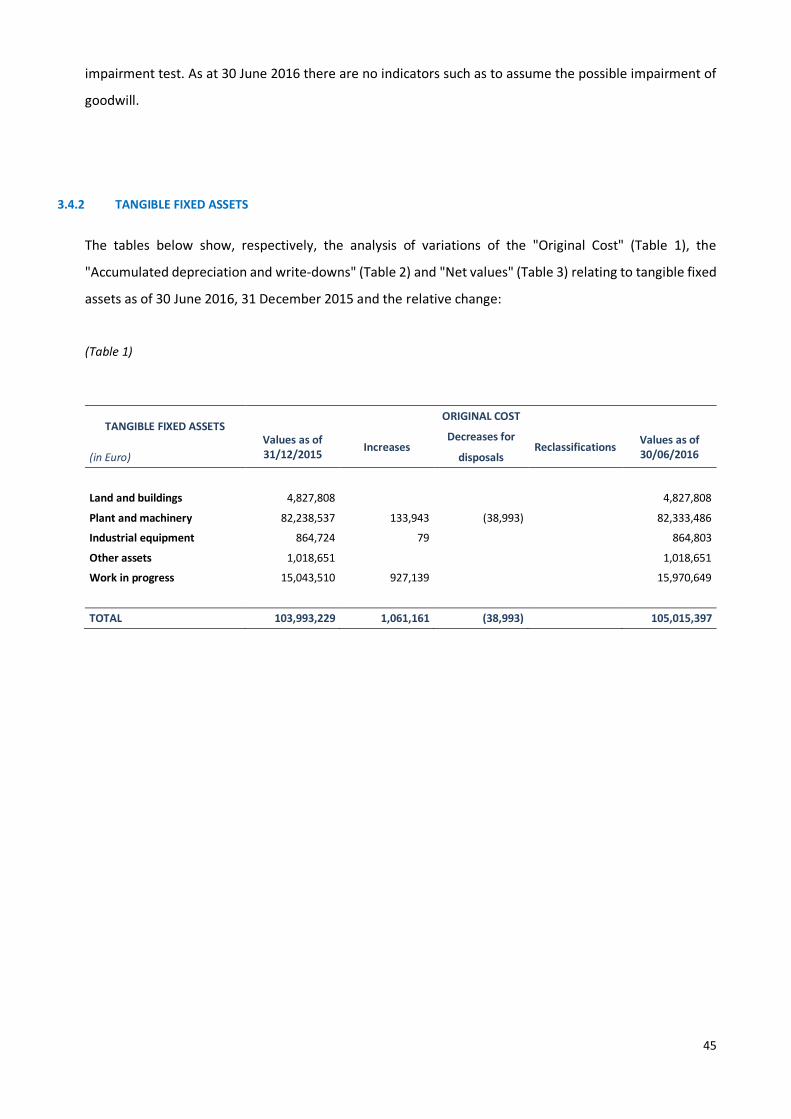

3.4.2 TANGIBLE FIXED ASSETS ............................................................................................................. 45

3.4.3 EQUITY INVESTMENTS ............................................................................................................... 47

3.4.4 DEFERRED TAX ASSET .............................................................. Errore. Il segnalibro non è definito.

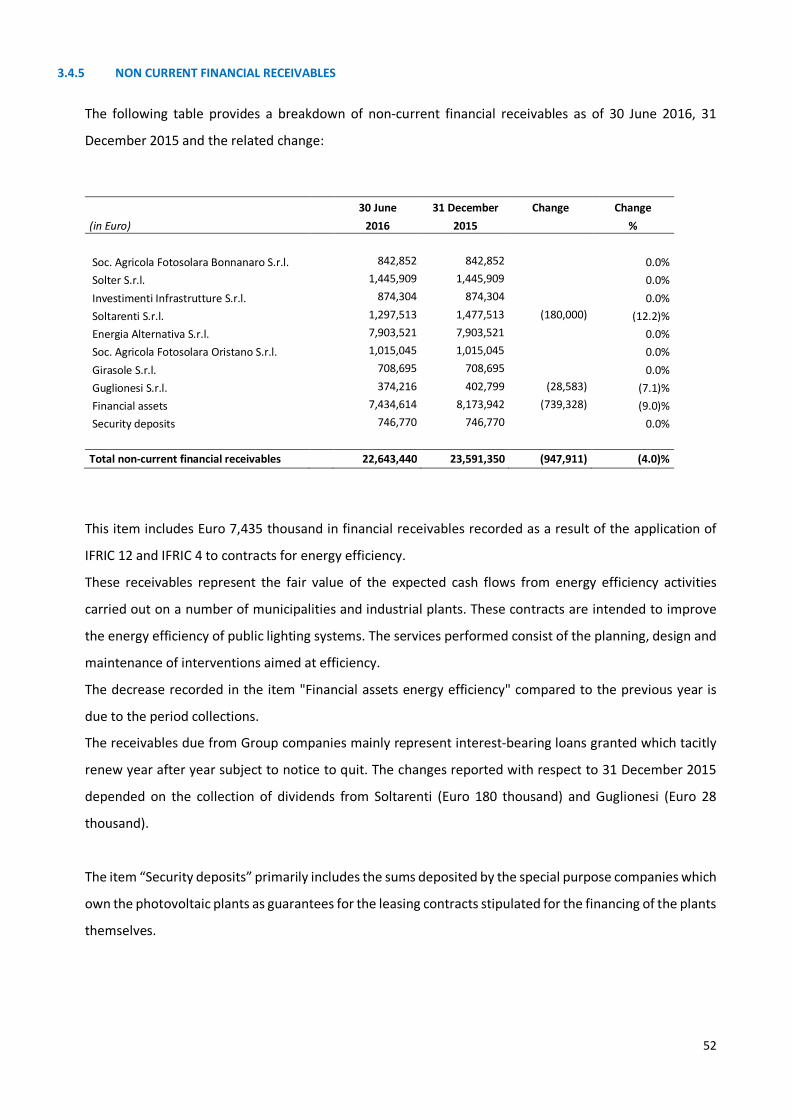

3.4.5 NON CURRENT FINANCIAL RECEIVABLES .................................................................................... 52

3.4.6 INVENTORIES ............................................................................................................................. 53

3.4.7 TRADE RECEIVABLES .................................................................................................................. 53

3.4.8 OTHER CURRENT ASSETS ............................................................................................................ 54

4

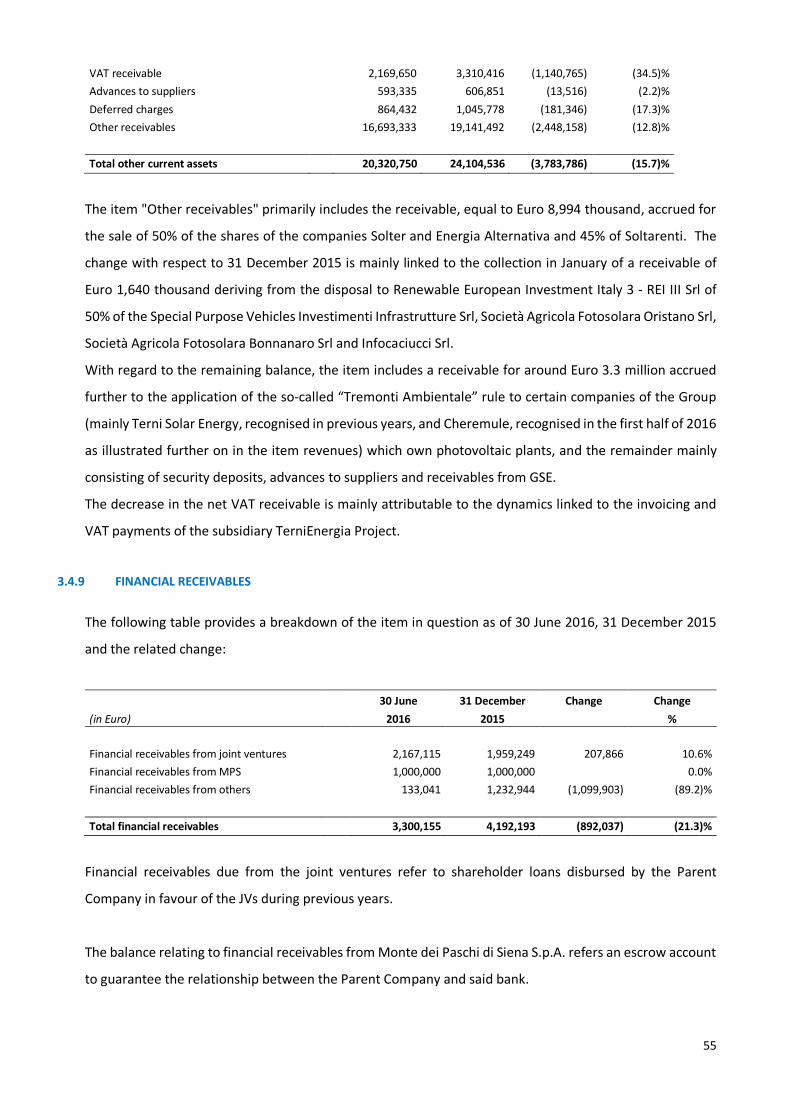

3.4.9 FINANCIAL RECEIVABLES ............................................................................................................ 55

3.4.10 CASH AND CASH EQUIVALENTS ............................................................................................. 56

3.5 COMMENTS ON THE MAIN LIABILITY AND EQUITY ITEMS ........................................................... 57

3.5.1 SHAREHOLDERS’ EQUITY ............................................................................................................ 57

3.5.2 PROVISIONS FOR EMPLOYEE BENEFITS ....................................................................................... 57

3.5.3 PROVISIONS FOR DEFERRED TAXES ............................................................................................ 58

3.5.4 NON CURRENT FINANCIAL PAYABLES ......................................................................................... 58

3.5.5 OTHER NON CURRENT LIABILITIES .............................................................................................. 59

3.5.6 DERIVATIVES .............................................................................................................................. 60

3.5.7 TRADE PAYABLES ....................................................................................................................... 60

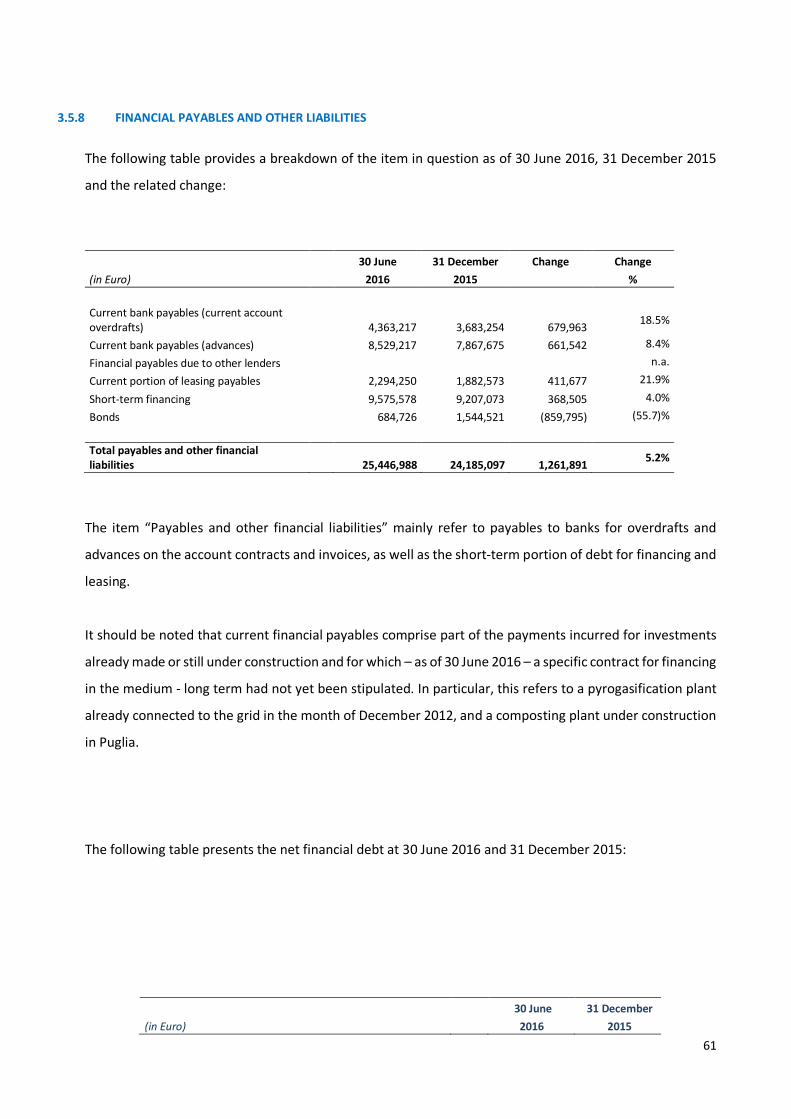

3.5.8 FINANCIAL PAYABLES AND OTHER LIABILITIES ............................................................................ 61

3.5.9 INCOME TAX PAYABLES .............................................................................................................. 62

3.5.10 OTHER CURRENT LIABILITIES ................................................................................................. 63

3.5.11 COMMITMENTS AND GUARANTEES ISSUED AND POTENTIAL LIABILITIES ............................... 63

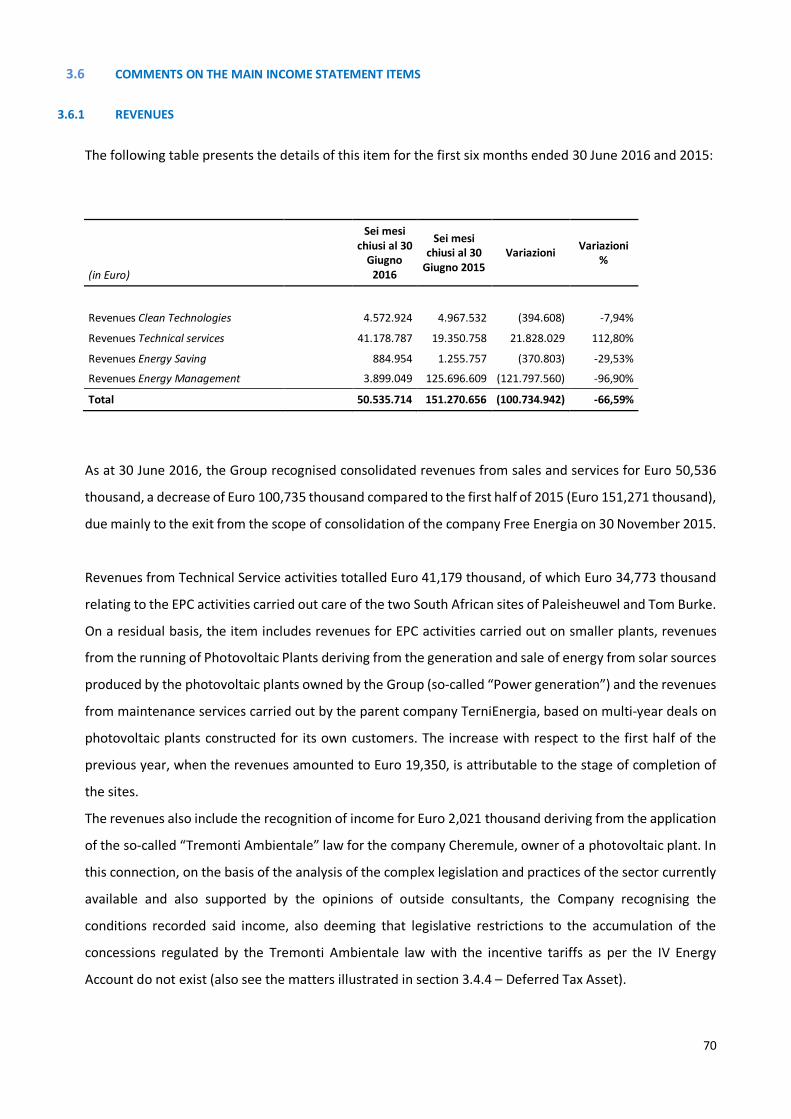

3.6 COMMENTS ON THE MAIN INCOME STATEMENT ITEMS............................................................. 70

3.6.1 REVENUES.................................................................................................................................. 70

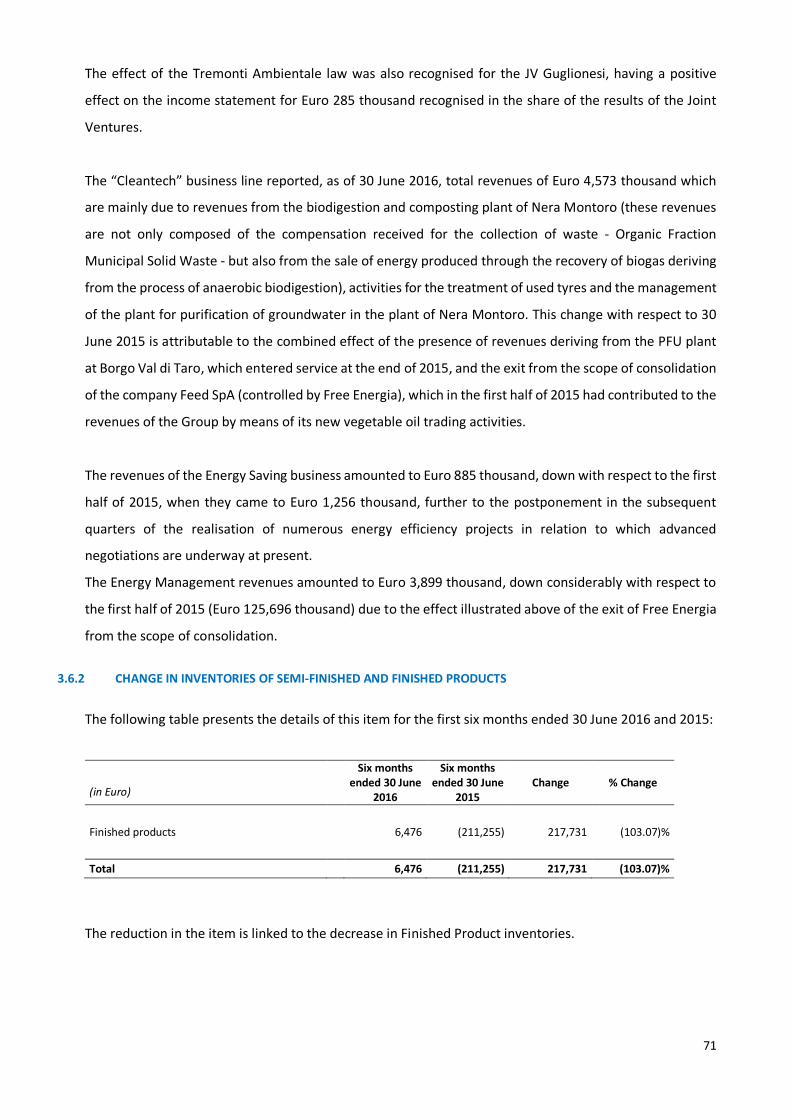

3.6.2 CHANGE IN INVENTORIES OF SEMI-FINISHED AND FINISHED PRODUCTS ..................................... 71

3.6.3 COST OF RAW MATERIALS, CONSUMABLES AND GOODS ............................................................ 72

3.6.4 COSTS FOR SERVICES .................................................................................................................. 72

3.6.5 PERSONNEL COSTS ..................................................................................................................... 73

3.6.6 OTHER OPERATING COSTS.......................................................................................................... 73

3.6.7 AMORTISATION, DEPRECIATION, ALLOCATIONS AND WRITE-DOWNS ......................................... 74

3.6.8 FINANCIAL INCOME AND EXPENSES ........................................................................................... 74

3.6.9 PROFIT SHARE FROM JOINT VENTURES ...................................................................................... 75

3.6.10 TAXES ................................................................................................................................... 76

3.7 RELATIONS WITH RELATED PARTIES ........................................................................................... 77

3.8 ATYPICAL AND/OR UNUSUAL TRANSACTIONS............................................................................. 83

3.9 OTHER INFORMATION................................................................................................................ 83

Agreement for the without recourse factoring of receivables for around Euro 1.2 million ................... 84

4 CERTIFICATION OF THE CONSOLIDATED INTERIM FINANCIAL STATEMENTS OF THE TERNIENERGIA GROUP AS

AT 30 JUNE 2016 PURSUANT TO ARTICLE 154 BIS OF LEGISLATIVE DECREE 58/98 AND ART. 81 TER OF CONSOB

REGULATION NO. 11971/99, AND SUBSEQUENT AMENDMENTS AND SUPPLEMENTS ....................................... 89

5

1. REPORT ON OPERATIONS

1.1 THE GROUP’S BUSINESS AND MISSION

TerniEnergia aims to establish itself as the first independent Italian “smart energy company” operating in

the sectors of renewable energies, energy efficiency, and waste and Energy management through its

individual business model.

The Industrial Plan as of February 2015, “Fast on the smart energy road”, was updated and approved by

the previous TerniEnergia Board of Directors on 29 October 2015. In particular, the plan is based on the

following business assumptions:

- backlog of work orders in the photovoltaic sector, both acquired and those in the process of being acquired

abroad;

- development of significant commercial cross-selling opportunities in the sectors of energy efficiency

(strong growth) and in gas & power management;

- strong diversification of the TerniEnergia business within anti-cyclical sectors and completion of core

activities of the Group along the entire value chain of energy, ranging from the design of plants to advanced

post-sales services;

- search for potential corporate and business partnerships in the environmental sector, including the

possibility of spinning off the waste management sector in a “newco”, which may represent a “national

leader” industrial platform open to the investment of new investors focused on the green & circular

economy sector.

The overall number of photovoltaic plants constructed by TerniEnergia since the start of operations is equal

to 274, with cumulative capacity of around 366.6 MWp (including 13.2 MWp held 100% by the company

and 30 MWp in joint venture, allocated to power generation activities). In addition, biomass plants for a

total of 1.5 MWe and 2 MWt are connected to the grid.

The overall production of energy in full ownership and joint venture plants for Power generation activities

was equal to around 30.85 million kWh.

Within the environmental sector, plants for the treatment and recovery of unused tires in Nera Montoro

and Borgo Val di Taro, as well as for biodigestion and GreenAsm composting are operational, as are the

Nera Montoro groundwater purification plants.

TerniEnergia Gas&Power managed around 14,200,000 of standard cubic metres of gas, equivalent to

150,250 MWh.

During the period, it launched lighting energy efficiency work on an industrial scale for a leading cement

manufacturing group. The Group undertook initiatives for 5,150 lighting points, with expected savings of

more than 9,760 million KWh of 0.55 million kWh and 1,842 TEP.

6

1.2 THE GROUP’S STRUCTURE

TERNIENERGIA S.P.A.

100%

NEWCOENERGY S.R.L.

REBIS POWER S.R.L.

CAPITAL SOLAR S.R.L.

INVESTIMENTI INFRASTRUTTURE S.R.L.

CAPITAL ENERGY S.R.L.

SOC AGR FOTOSOLARA BONNANARO S.R.L.

ENERGIA NUOVA S.R.L.

SOC AGR FOTOSOLARA ORISTANO S.R.L.

MEET SOLAR S.R.L.

INFOCACIUCCI S.R.L.

RINNOVA S.R.L. 50% ENERGIA ALTERNATIVA S.R.L.

ENERGIA BASILICATA S.R.L.

SOLTER S.R.L.

ENERGIA LUCANA S.R.L.

GIRASOLE S.R.L.

VERDE ENERGIA S.R.L.

GUGLIONESI S.R.L.

FESTINA S.R.L.

GREEN ASM S.R.L.

SOCIETA' AGRICOLA PADRIA SRL

SOC AGR FOTOSOLARA CHEREMULE S.R.L.

SOC AGR FOTOSOLARA ITTIREDDU S.R.L.

80% TEVASA L.t.d.

TECI S.R.L. TERNIENERGIA PROJECT L.t.d.

MEET GREEN ITALIA S.R.L. 70%

IGREEN PATROL S.R.L.

LYTENERGY S.R.L.

TERNIENERGIA POLSKA Sp.z.o.o. 49%

TERNIENERGIA SOLAR SOUTH AFRICA L.t.d.

TERNIENERGIA MIDDLE EAST POWER

TERNIENERGIA S.p.A. HELLAS M.E.P.E.

TERNIENERGIAROMANIA S.R.L.

T.E.R.N.I. SOLARENERGY S.R.L. 5% SOL TARENTI S.R.L.

ALCHIMIA ENERGY 3 S.R.L.

TERNIENERGIA GAS&POWER S.P.A.

GREENLED INDUSTRY S.P.A.

VAL DI TARO TYRE SRL

TERNIENERGIA MOCAMBIQUE LIMITADA

7

1.3 MAIN EVENTS DURING THE FINANCIAL PERIOD ENDED 30 JUNE 2016

Establishment of the subsidiary TerniEnergia Middle East Power LLC in Abu Dhabi

In January 2016, as part of the global growth strategy, TerniEnergia S.p.A. established the company

TerniEnergia Middle East Power LLC in Abu Dhabi, governed under UAE law, with a 51% investment by

Khalid Al Hamed Group LLC and 49% by TerniEnergia. The subsidiary will operate in Middle Eastern

countries and within the Gulf Cooperation Council (GCC), with share capital of 50 thousand dirham.

In particular, TerniEnergia and Al Hamed Group signed a shareholders’ agreement governing the company’s

operations, which was the subject of a strategic agreement previously signed by the parties and announced

to the market on 29 April 2014. The Board of Directors of TerniEnergia Middle East Power LLC will have a

Board of Directors consisting of two members, Chairman and CEO of Khalid Al Hamed Group LLC, Sheik

Khalid Bin Ahmed Al Hamed, and Chairman and CEO of TerniEnergia S.p.A., Stefano Neri. The profits from

the company’s operations will be divided as follows: 75% to TerniEnergia S.p.A. and 25% to Khalid Al Hamed

Group LLC.

The agreement envisages that Khalid Al Hamed Group LLC will primarily be involved in the management of

relations with the local government authorities as well as the facilitation of authorisation processes, the

acquisition of operational requirements and support during negotiations with financial partners and with

banking institutions supporting business operations, while TerniEnergia will be responsible for managing

the operational and industrial component. By means of this managerial model, the parties aim to unite and

enhance the value of the know-how and technological competencies of TerniEnergia in the energy and

environmental sectors, with the financial endowment and business development skills of the Al Hamed

Group, thereby ensuring rapid growth for TerniEnergia Middle East Power LLC.

“TerniEnergia Hub” presented, the new operating formula for the Group’s Energy Saving business line

On 11 February 2016, TerniEnergia presented the “HUB” project, a new operating method to open up the

industrial energy efficiency market through “third party financing” in Italy.

The objective of “TerniEnergia Hub” is to form a strategic alliance between all players in the value chain to

meet the needs of capital markets. The formula that the Group uses in the renewables and Energy

management sectors can also bring advantages to the industrial energy efficiency sector, as was explained

in a presentation to a select audience of partners and suppliers during a workshop held in the conference

room of the Hotel Principe di Savoia in Milan. In the three-year plan “Fast on the smart energy road”,

TerniEnergia paid particular attention to developing the Energy saving business line, by defining a new

business model.

8

Among the applicable methods, TerniEnergia added:

1) Financial leasing:

The action was completed and accepted by the end user. The Hub assesses the intervention and assumes

ownership, absorbing the business risk, and finances it through financial leasing. TerniEnergia is responsible

for performance guarantees, assuming the role of ESco, compensates the partner for the investment made

for technology costs and for the O&M assets. The partner recovers the invested equity, making it available

for new interventions, while TerniEnergia Hub is compensated through the savings generated and

guarantees the expected return to the investor. At the conclusion of the contract, TerniEnergia redeems

the plant and transfers ownership to the end user.

2) Securitisation of receivables

This action was also completed and accepted by the end user. The Hub assesses the intervention and uses

a special purpose vehicle to purchase the energy efficiency plant, compensating the partner for the

investment made in technology costs and the O&M asset. The SPV transfers the plant and discounted

receivable to the investor. The securitisation can also be applied to portfolios of similar transactions, if there

is not one single high-value project.

3) Financing from the contract signing

This intervention is only in the planning stage and the end user has signed the contract for installation and

management. TerniEnergia Hub will acquire the contract and activate the procedures to finance the project

through the FTT formula. The possibility of issuing guarantees, the track record and the TerniEnergia

governance system will release the necessary capital for the investment. Once the contact is acquired,

depending on the type, entity, business plan and quality of the intervention, TerniEnergia will decided

whether to activate the leasing option or the securitisation of receivables option.

Establishment of the subsidiary TerniEnergia Moçambique Limitada in Mozambique

TerniEnergia SpA finalised the establishment of TerniEnergia Moçambique Limitada, wholly-owned, in

Maputo (Mozambique) in March 2016. The Mozambique subsidiary will operate with the utmost efficiency

for the performance of the consistent programme of activities which the Group envisages to develop in

African countries, considered strategic in terms of trend for the growth of the businesses linked to

renewable energy and smart energy. In detail, operations are underway preliminary for participation in

projects in the energy sector, by means of the construction of industrial-size photovoltaic plants.

9

Connection to the network of the giant photovoltaic plant in Paleisheuwel

The first of the two giant sites active in South Africa was connected on 26 April to the national transmission

network of the distributor Eskom. This Paleisheuwel site, whose overall installed power capacity came to

82.5 MWp, was connected in advance with respect to the timeline envisaged by the EPC contracts. The site

covers an area of 240 hectares and employs more than 500 workers in the various functions for the

installation of a good 611,000 photovoltaic panels with a power capacity ranging between 125Wp and

140Wp. 101,850 frames were mounted in total, 7 million Kg of metalwork used and 3,000 km of electrical

cables laid. During the work, TerniEnergia collaborated with 6 subcontractors and operated in compliance

with the policies for furthering the participation of coloured people in economic life. As at the date of this

consolidated half year report, accessory work remains to be completed for the purpose of final delivery of

the plant to the customer.

Approval of the 2015 financial statements and renewal of the corporate bodies

On 26 April, the Ordinary Shareholders' Meeting of TerniEnergia SpA approved the draft financial

statements and acknowledged the presentation of the consolidated financial statements at 31 December

2015, resolving the distribution of a dividend of Euro 0.025 per share (gross of tax), to be withdrawn from

the net profit (loss) of the individual financial statements and corresponding to a pay-out ratio of 43% of

the net profit (loss) of the consolidated financial statements with dividend coupon No. 7 registered on 23

May 2015 and dividend payment on 25 May 2016.

The shareholders’ meeting also approved the Company and Group policy with regard to remuneration and

incentives, which envisages: (a) the total annual taxable emolument of the Board of Directors as Euro 490

thousand plus legal contributions and charges, as well as the reimbursement of the costs incurred as a

result of the appointment; (b) a maximum annual variable component equal to 15% of the emolument due

to the individual executive director in the event of exceeding an amount equal to at least 15% of the EBITDA

forecast by the business plan approved, deferring the payment of 50% of the variable component accrued

solely as of the natural expiry of the mandate; (c) to establish the total gross annual emolument for the

Board of Statutory Auditors as Euro 70 thousand plus the reimbursement of the expenses incurred as a

result of the appointment.

In conclusion, the Shareholders’ Meeting appointed the members of the Board of Directors who will remain

in office for the years 2016, 2017 and 2018, until the date of the meeting called to approve the financial

statements as of 31 December 2018, whose number of members has been established as 9. The directors,

proposed in the list presented by the majority shareholder Italeaf SpA, and voted for unanimously, are

Stefano Neri, who undertakes the office of Chairman, Monica Federici, Fabrizio Venturi, Massimiliano Salvi,

10

Laura Bizzarri, Mario Marco Molteni, Paolo Ottone Migliavacca, Domenico De Marinis and Laura Rossi.

Mario Marco Molteni, Paolo Migliavacca, Domenico De Marinis and Laura Rossi have declared that they are

in possession of the independence requisites envisaged by current provisions, including the Consolidated

Financial Act and the Corporate Governance Code.

Three members of the Board of Statutory Auditors and two alternate auditors were also appointed, who

will remain in office for the years 2016, 2017 and 2018, i.e. Ernesto Santaniello, who undertakes the office

of Chairman of the Board of Statutory Auditors, Vittorio Pellegrini, elected as standing auditor, Simonetta

Magni elected as standing auditor, Marco Chieruzzi and Caterina Brescia elected as alternative auditors. On

7 June, Marco Chieruzzi replaced Vittorio Pellegrini, who handed in his resignation for personal reasons,

from the office of standing auditor.

Merger by incorporation of the wholly-owned company TerniEnergia Gas&Power in TerniEnergia SpA

On 2 May, TerniEnergia SpA communicated the filing care of its head offices, in the “Investor relations”

section of the company website, as well as care of the authorised storage mechanism 1Info, at the address

www.1info.it, of the Project for the merger via incorporation of the wholly-owned company TerniEnergia

Gas & Power SpA in TerniEnergia SpA, together with the balance sheets of TerniEnergia Gas & Power SpA

and TerniEnergia SpA as of 31 December 2015, drawn up in accordance with Article 2501 quater of the

Italian Civil Code.

Acquisition of a contract for the construction in Egypt of a photovoltaic plant and a lighting energy

efficiency contract

On 19 May 2016, TerniEnergia disclosed that it has been awarded a contract for a value of around US$ 19.2

million relating to the construction in Egypt of an industrial size photovoltaic plant with total power of 47

MWp on behalf of a leading Italian utility company.

The plant will be installed in Benban around 900 km from Cairo and cover an area of roughly 150 hectares.

The contract envisaged EPC activities (engineering, procurement and construction) without the supply of

photovoltaic modules and inverters. More than 250 workers will be employed at the site when fully up and

running. The project envisaged the use of 3Sun panels (manufactured in Italy at the Catania plants),

mounted on traditional steel structures.

Furthermore, TerniEnergia has entered into a lighting energy efficiency agreement, featuring the FTT

formula (financing via third parties) of a shared saving type, for a value of around Euro 0.6 million on behalf

of a leading Italian cement manufacturer. The project, with regard to which TerniEnergia will also see to

the “turnkey” EPC aspect, will be carried out on a plant in Lombardy and will envisage the replacement of

11

4,497 traditional lighting points with 2,853 new latest generation LED lighting points produced using the

Group’s own technology, with an expected savings of around 1GWh/year.

Agreement entered into for the construction of two important water treatment plants care of the Nera

Montoro production site

On 27 May 2016, TerniEnergia revealed that it had entered into an agreement for the construction of two

important water treatment plants care of the Nera Montoro (TR) production site, for an equivalent value

of around Euro 6 million with Saceccav, a Bona Dea S.r.l. Group company, active in the sector involved in

construction and management of industrial plants for the treatment of waste water.

The work, launched in June 2016, will allow TerniEnergia to complete the scheduled investments on the

biological and chemical/physical plants that are already operational in Umbria, so as to comply with the

provisions for the restoration project of the groundwater of Nera Montoro and for the construction of a

new treatment plant intended for the special liquid waste treatment business (e.g. agricultural, industrial,

organic and inorganic chemical, etc.).

The agreement will make it possible to achieve new high quality plant engineering equipment within the green

industry hub of Nera Montoro (TR). In detail, the first plant is functional for environmental redevelopment via the

implementation of a hydraulic barrier, the creation of new plant engineering sections and the modernisation of the

existing parts; the treatment potential of the groundwater, polluted over the years by previous uses of the site, will

be equal to 50,000 litres an hour. Thanks to the experience and expertise of Saceccav, the enhancement of the

treatment activities will be guaranteed, preventing the pollutants from reaching the river Nera, returning water with

a more or less drinkable quality, as envisaged in the Operational Restoration Plan and requested by the Bodies

involved.

The second plant treats liquid waste originating from production activities whose treatment requires

solutions with a high technologic content, permitting TerniEnergia to intercept flows of materials currently

destined for plants positioned outside Umbria and at the same time meet the industrial demand of Central

Italy. The plant, which represents the state of the art of the treatment and purification technologies, with

have an intake capacity of 58,000 tons/year of waste with different matrixes and will therefore have the

twofold objective of upholding the requests of the Authorities and establishing a resource for TerniEnergia’s

activities in the circular economy sector and for the development of the area.

The measures have been approved by means of Executive Resolution of the Province of Terni No.

11458/2015 “Integrated Environmental Authorisation (IEA)” relating to the “Operational plan for

restoration of the groundwater of the industrial site of Nera Montoro (TR) – adjustment to provisions and

implementation of current plants with the introduction of new sections for liquid waste treatment with

third parties”.

12

Connection to the network of the giant photovoltaic plant in Tom Burke

On 8 June 2016, TerniEnergia revealed that also the second of the two giant sites active in South Africa on

behalf of a leading Italian utility company was connected, by means of a new stretch of high voltage line,

to the national transmission network of the distributor Eskom. In detail, TerniEnergia Projects PTY Ltd, the

South African subsidiary of TerniEnergia S.p.A., connected the Tom Burke plant to the network (for an

overall installed power capacity of 66 MWp), in advance with respect to the timeline envisaged by the final

EPC (engineering, procurement and construction) and O&M (operation and maintenance) contracts which

have a four-year duration and are renewable, in observance of the estimated economic results.

The Tom Burke site, which covers an area of 200 hectares in the Limpopo region close to the border with

Botswana, employed more than 350 workers in the various functions for the installation of around 500,000

photovoltaic panels with a power capacity ranging between 125Wp and 140Wp. 82,700 metalwork frames

were mounted in total and 2,550 km of electrical cables laid. During the work, TerniEnergia operated in

compliance with the policies for furthering the participation of coloured people in economic life.

Acquisition of a contract for the construction in Zambia of a photovoltaic plant

On 15 June 2016, within the sphere of the process for the insourcing of the photovoltaic EPC business

(engineering, procurement and construction), TerniEnergia disclosed that it has been awarded a contract

for a value of around US$ 8 million relating to the construction in Zambia of an industrial size photovoltaic

plant with total power of 34 MWp on behalf of a leading Italian utility company.

By means of this new industrial agreement, TerniEnergia strengthened its leadership role in the

construction of large plants for the production of energy from solar sources in Africa.

The Zambia plant will be installed in Lusaka in the province of the same name and cover an area of around

50 hectares. The contract envisages EPC activities without the supply of photovoltaic modules and inverters.

Around 150 workers will be employed at the site when fully up and running, for the installation of roughly

106,260 poly modules with 320 Wp of power. The use of 2,550 kg of steel metalwork frames is envisaged

along with the laying of 960 km of electrical cables.

13

1.4 PERFORMANCE OF OPERATIONS

Below are summarised the main economic and financial highlights of the TerniEnergia Group as at 30 June

2016 compared with the corresponding figures for the previous year.

The financial results of the Group are summarised below:

Six months ended 30 June

2016

Six months ended 30 June

2015

Change Change

(in Euro) %

Income Statement Net revenues from sales and services 50,535,713 151,270,656 (100,734,942) (66.59)% EBITDA 9,503,452 10,735,543 (1,232,092) (11.48)% EBIT 5,948,923 7,865,932 (1,917,009) (24.37)% Result for the period 1,107,682 1,484,340 (376,658) (25.38)% Ebitda Margin 18.8% 7.1% 11.7% n.a.

30 June 31 December Change Change

(in Euro) 2016 2015 %

Financial data Fixed assets 124,484,721 125,960,176 (1,475,455) (1.17)% Net working capital, excluding provisions and other liabilities 9,550,490 17,202,726 (7,652,236) (44.48)% Net financial position 79,361,677 87,371,548 (8,009,871) (9.17)% Shareholders’ equity 54,673,534 55,791,353 (1,117,819) (2.00)%

14

Performance indicators

Performance indicators 30 June 30 June

2016 2015

PROFITABILITY RATIOS

ROE 2.1% 10.1% ROI 4.3% 5.8% ROS 11.8% 4.6%

FINANCIAL RATIOS Fixed asset coverage 1.61 1.51 Short-term NFP / Shareholders’ equity (0.02) 0.20 NFP / Shareholders’ equity 1.45 1.44 NFP / Net invested capital 0.59 0.59 Shareholders’ equity / Net invested capital 0.41 0.41 NFP / EBITDA 8.35 5.36

NET WORKING CAPITAL ROTATION Net working capital / Revenues 28.80% 12.60%

(a) ROE: Normalised net earnings for the period/Total Shareholder’s Equity net of the net profit for the period; (b) ROI: Normalised EBIT/ average of the Net invested capital at the beginning of the reference period and the Net invested capital at the end of the reference period; (c) ROS: Normalised operating result/Normalised revenues net of sales and services; (d) Fixed asset coverage: Total tangible and intangible fixed assets/Shareholder’s Equity

15

1.5 GROUP ECONOMIC RESULTS

Six months ended 30 June

2016

Six months ended 30 June

2015 Change

Change

(in Euro) %

Net revenues from sales and services 50,535,713 151,270,656 (100,734,942) (66.59)% Cost of production (38,857,759) (137,032,633) 98,174,873 (71.64)% Added value 11,677,954 14,238,023 (2,560,069) (17.98)% Personnel costs (2,174,503) (3,502,480) 1,327,977 (37.92)% EBITDA 9,503,452 10,735,543 (1,232,092) (11.48)% Amortisation, depreciation, allocations and write-downs (3,554,529) (2,869,611) (684,918) 23.87% Operating result 5,948,923 7,865,932 (1,917,009) (24.37)% Financial income and expenses (3,603,971) (5,211,808) 1,607,836 (30.85)% Profit share from joint ventures 619,659 49,532 570,127 n.a. Pre-tax result 2,964,611 2,703,657 260,954 9.65% Income taxes (1,856,929) (1,219,317) (637,612) 52.29%

Net result 1,107,682 1,484,340 (376,658) (25.38)%

The period in question in particular highlights the progress of the EPC activities care of two giant plants in

South Africa, linked to the network and by now close to completion. The comparison with the first half of

2015 highlights the repercussions of the contract for divestment in Free Energia, fully illustrated in the 2015

statutory and consolidated financial statements to which reference is made and which, despite not

determining essential changes in the business model, has led, for the moment, to a significant downsizing

in trading activities with a consequent reduction in revenues.

As at 30 June 2016, the Group recognised consolidated revenues from sales and services for Euro 50,536

thousand, a decrease of Euro 100,735 thousand compared to the first half of 2015 (Euro 151,271 thousand),

due mainly to the exit from the scope of consolidation of the company Free Energia on 30 November 2015.

Sei mesi

chiusi al 30 Giugno

2016

Sei mesi chiusi al 30

Giugno 2015 Variazioni Variazioni

% (in Euro)

Ricavi Clean Technologies 4.572.924 4.967.532 (394.608) -7,94%

Ricavi Technical services 41.178.787 19.350.758 21.828.029 112,80%

Ricavi Energy Saving 884.954 1.255.757 (370.803) -29,53%

Ricavi Energy Management 3.899.049 125.696.609 (121.797.560) -96,90%

Totale 50.535.714 151.270.656 (100.734.942) -66,59%

16

The revenues from the Technical Service activities came to Euro 41,179 thousand, of which Euro 34,773

thousand relating to the EPC activities carried out at the two South African sites of Paleisheuwel and Tom

Burke and the remaining balance relating to the power generation and maintenance activities; the item

also includes the recognition of tax-related income for Euro 2,021 thousand deriving from the application

of the so-called “Tremonti Ambientale”, in relation to which, for greater details, reference is made to the

matters indicated in the explanatory notes to the section commenting on the Revenues. The increase with

respect to the first half of the previous year, when the revenues amounted to Euro 19,351, is mainly

attributable to the stage of completion of the sites.

The Cleantech revenues amounted to about Euro 4,573 thousand, down with respect to the first half of

2015 (Euro 4,967 thousand). This change is essentially due to the combined effect of the presence, in the

first half of 2016, of revenues deriving from the PFU plant at Borgo Val di Taro, which entered service at the

end of 2015, and the exit from the scope of consolidation as of 30 November 2015 of the company Feed

SpA (controlled by Free Energia), which in the first half of 2015 had contributed to the revenues of the

Group by means of its vegetable oil trading activities.

The revenues of the Energy Saving business amounted to Euro 885 thousand, down with respect to the first

half of 2015, when they came to Euro 1,255 thousand, further to the postponement in the second half of

2016 of the realisation of numerous energy efficiency projects in relation to which advanced negotiations

are underway at present.

The Energy Management revenues amounted to Euro 3,899 thousand, down considerably with respect to

the first half of 2015 (Euro 125,697 thousand) due to the effect illustrated above of the exit of Free Energia

from the scope of consolidation.

Direct production costs, which are primarily variable in nature, totalled Euro 38,858 thousand, disclosing a

decrease of Euro 98,175 thousand compared to the first half of 2015 (Euro 137,033 thousand), essentially

reflecting the drop in revenues due to the cessation of the energy trading activities of Free Energia. With

respect to the first half of 2015, the EBITDA fell from Euro 10,736 to Euro 9,503 thousand, therefore

disclosing a decrease less than proportionate with respect to the drop in revenues, as confirmed by the

EBITDA margin trend which passed from around 7% to around 19%.

“Amortisation, depreciation, allocations and write-downs” in the reclassified income statement reported

an increase from Euro 2,870 thousand to Euro 3,555 thousand with respect to the first half of 2015 due, on

the one hand, to the write-downs of securities (Veneto Banca) reported in the first half of 2016 and, on the

other hand, the lower depreciation attributable to the fewer photovoltaic plants fully owned by the Group.

Financial operations, a negative balance of around Euro 3,604 thousand, disclosed a considerable increase

with respect to the first half of 2015, when the balance was negative for Euro 5,212 thousand, essentially

as a result of the minor average borrowing and the exit from the scope of consolidation, as from 30

November 2015, of the Free Energia Group.

17

The JV portion of result, increasing Euro 570 thousand compared with 30 June 2015, was mainly affected

by the recognition of the positive effects of the Tremonti Ambientale on the company Guglionesi (pro rata

Euro 285 thousand).

The item taxation shows an increase of Euro 638 thousand with respect to 30 June 2015, with a tax rate

which increased mainly due to the different incidence of the tax adjustments as well as further to the

adjustment of the estimates of the taxes for the same period in the previous year.

The net result for the period as at 30 June 2016 has a positive balance of Euro 1,108 thousand, with a

decrease in absolute terms of Euro 377 thousand compared to the figure in the same period last year (Euro

1,484 thousand), on account of the dynamics described above.

1.6 OVERVIEW OF STATEMENT OF FINANCIAL POSITION

Following is the summarised equity and income information.

30 June 31 December Change Change (in Euro) 2016 2015 %

Intangible fixed assets 5,309,242 4,460,745 848,497 19.02% Tangible fixed assets 81,280,641 82,616,544 (1,335,903) (1.62)% Financial fixed assets and other fixed assets 37,894,838 38,882,887 (988,049) (2.54)% Fixed assets 124,484,721 125,960,176 (1,475,455) (1.17)%

Inventories 13,893,554 23,329,978 (9,436,424) (40.45)% Trade receivables 31,843,192 52,361,935 (20,518,743) (39.19)% Other assets 20,320,750 24,104,536 (3,783,786) (15.70)% Trade payables (44,066,235) (63,543,245) 19,477,010 (30.65)% Other liabilities (6,029,224) (13,106,938) 7,077,714 (54.00)% Net working capital 15,962,037 23,146,266 (7,184,229) (31.04)%

Provisions and other non-trade liabilities (6,411,547) (5,943,540) (468,007) 7.87%

Net invested capital 134,035,211 143,162,902 (9,127,691) (6.38)%

Shareholders’ equity 54,673,534 55,791,353 (1,117,819) (2.00)%

Current net financial position (170,495) 8,099,515 (8,270,010) (102.11)% Non-current net financial position 79,532,172 79,272,033 260,139 0.33% Total net financial position 79,361,677 87,371,548 (8,009,871) (9.17)%

Total sources 134,035,211 143,162,901 (9,127,690) (6.38)%

18

Net invested capital

Net invested capital as at 30 June 2016 amounted to Euro 134,035 thousand consisting of Euro 124,485

thousand from fixed assets, Euro 15,962 thousand from net working capital and Euro 6,412 thousand from

provisions and other non-trade liabilities.

With respect to the financial statements for the period ended 31 December 2015, the net invested capital

reported a decrease of Euro 9,128 thousand attributable for Euro 1,475 thousand to the decrease in the

fixed assets, the significant decrease in the net working capital for Euro 7,184 thousand, attributable in

particular to (i) the collections of receivables received at the end of the first half of 2016 by TerniEnergia

Project relating to the milestones achieved at the sites in South Africa, (ii) the reduction in the value of

inventories for South Africa, comprising as of 31 December 2015 of panels which have been installed during

the first half of 2016 and (iii) the reduction in trade payables further to the payment of the first tranche of

the debt for the panels relating to the Tom Burke and Paleisheuwel plants. The remaining change in Net

invested capital is attributable to the increase of Euro 468 thousand in the item Provisions and other non-

trade liabilities.

19

Net financial position

30 June 31 December (in Euro) 2016 2015

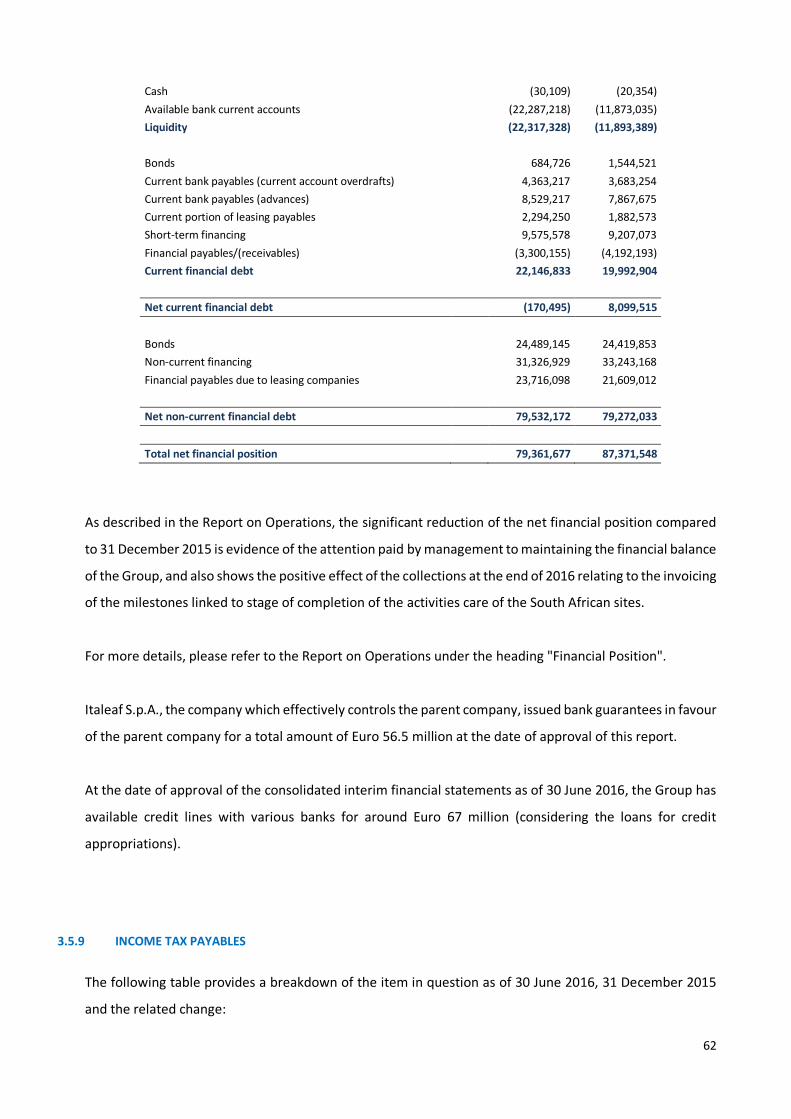

Cash (30,109) (20,354) Available bank current accounts (22,287,218) (11,873,035) Liquidity (22,317,328) (11,893,389)

Bonds 684,726 1,544,521 Current bank payables (current account overdrafts) 4,363,217 3,683,254 Current bank payables (advances) 8,529,217 7,867,675 Current portion of leasing payables 2,294,250 1,882,573 Short-term financing 9,575,578 9,207,073 Financial payables/(receivables) (3,300,155) (4,192,193) Current financial debt 22,146,833 19,992,904

Net current financial debt (170,495) 8,099,515

Bonds 24,489,145 24,419,853 Non-current financing 31,326,929 33,243,168 Financial payables due to leasing companies 23,716,098 21,609,012

Net non-current financial debt 79,532,172 79,272,033

Total net financial position 79,361,677 87,371,548

The significant reduction in the Net Financial Position, already highlighted during 2015, with respect to

previous periods, is proof of the attention paid by management to maintain the financial equilibrium of the

Group. Furthermore, the change with respect to 31 December 2015 was affected by the collections relating

to the invoicing of the milestones linked to the stage of completion of the activities care of the South African

sites, with benefits in particular reflected in the current Net Financial Position. In this connection, it is

highlighted that a significant part of this liquidity, around Euro 11 million, was used at the beginning of July

2016 to pay the second tranche of the debt for the purchase of the panels relating to the suppliers in South

Africa.

Net financial debt at 30 June 2016 amounted to Euro 79,362 thousand, divided into a short-term portion

which presented a negative imbalance of Euro 170 thousand and a long-term portion of Euro 79,532

thousand. The long-term portion is primarily attributable to leases entered into with major financial

institutions to cover the financial requirements necessary for the development of photovoltaic plants that

are fully available to the company and for the investments in the biodigestion plant and the used tire

treatment plants in Nera Montoro and, as from the second quarter of 2016, of Borgo Taro. Non-current

financial debt also includes the quota due beyond 12 months of the corporate financing granted to the

20

parent company TerniEnergia at the end of 2013, and mainly composed of an unsecured loan totalling Euro

10 million with a duration of 60 months and reimbursement in 20 quarterly instalments, as well as an

unsecured loan of Euro 5 million with a duration of 60 months and lump sum reimbursement at the

expiration date, both issued by Veneto Banca. Finally, the non-current financial debt also includes the bond

with a nominal value of Euro 25 million and a duration of 5 years, annual coupon of 6.875%, as well as

reimbursement in a lump sum at the expiration date (month of February 2019). The current quota includes

the accrual of the interest accrued in the first half of 2016, equal to around Euro 800 thousand, and relative

to the coupon to be paid in the month of February 2017.

It should be noted that current financial payables comprise part of the payments incurred for investments

already made or still under construction and for which – as of 30 June 2016 – a specific contract for financing

over the medium - long term had not yet been stipulated. In particular, they refer to the second treatment

plant of a pyrogasification plant and a composting plant under construction in Apulia.

The short-term financial position presents a negative imbalance of Euro 170 thousand and is basically made

up of short-term debt to banks for overdrafts totalling Euro 4,363 thousand or advances on invoices and/or

contracts for Euro 8,529 thousand, short-term financing from banks for Euro 9,576 thousand, short-term

portion of lease payables for Euro 2,294 thousand, cash for Euro 22,317 thousand, and the short-term

portion of financial receivables and securities for Euro 3,300 thousand.

Shareholders' equity

As at 30 June 2016, shareholders' equity, including income for the period, amounted to Euro 54,674

thousand, a decrease with respect to 31 December 2015 of Euro 1,118 thousand. This change is mainly due

to the combined effect of the distribution of the dividend in May, the change in the cash flow hedge reserve

and the positive result for the period.

21

1.7 STATEMENT OF RECONCILIATION OF THE PARENT COMPANY’S OPERATING RESULT AND SHAREHOLDERS’

EQUITY WITH THE CONSOLIDATED RESULTS AS AT 30 JUNE 2016

Following is the statement of reconciliation of the consolidated operating result and shareholders' equity

with the Parent Company's operating result and shareholders' equity, pursuant to Consob communication

no. 6064293 of 27 July 2006.

Amounts in Euro thousands

Jun-16

(in Euro/000) SE IS

Parent Company shareholders' equity and operating results 54,491 (1,119)

Capital and reserves of the consolidated companies 5,159

Consolidated companies' operating result for the period 1,695 1,695

Derecognition of the value of consolidated equity investments (8,339)

Net capital gains attributable to assets as at the investee acquisition date 1,771 (9)

JV recognition effect 503 503

Other adjustments to the consolidated income statement for the period 38 38

Deferred tax effects 51

Other effects (285)

JV Cash flow hedge reserve - derivatives (410)

Group shareholders' equity and operating results 54,673 1,108

22

1.8 INVESTMENTS

In the period ended on 30 June 2016, investments totalled Euro 3,366 thousand, mainly for plants under

construction by the Parent Company TerniEnergia SpA.

(in Euro) Direct investments

Increases from

purchases

Total investments

as of 30/06/2016

31-Dec-15 Change %

Software 535,795 535,795 310,810 224,985 72.4% Other intangible assets 426,106 426,106 1,075,603 (649,497) (60.4%) Plant and machinery 133,943 133,943 2,541,712 (2,407,769) (94.7%) Industrial equipment 79 79 45,599 (45,520) (99.8%)

Other assets 17,910 (17,910) (100.0%)

Fixed assets in progress 927,139 927,139 3,255,318 (2,328,179) (71.5%)

Total 2,023,062 2,023,062 7,246,952 (5,223,890) (72.08%)

For further details regarding investments made during the half year, please see the explanatory notes (note

3.4.1 and 3.4.2).

1.9 HUMAN RESOURCES

As at 30 June 2016, the Group had 138 employees classified as follows:

30-Jun-16 31-Dec-15 Actual Average Actual Average Executives 4 3.83 4 3.67 Middle managers 13 12.67 12 8.92

Office workers 40 37.5 43 40.67

Manual workers 81 76.33 72 64.08

Total 138 130.33 131 117.34

The Parent Company applied Italian Legislative Decree No. 81/08, appointing a security manager and

entrusting a qualified and experienced outsourcer with the analysis of risks and the related evaluation

report.

Procedures have been implemented in compliance with currently effective legislation and, in this regard,

medical examinations as well as training and refresher courses on safety at work and within the working

environment are regularly carried out for all the employees of the Company.

23

1.10 RISK FACTORS RELATED TO THE REFERENCE SECTOR

In order to comply with the provisions pursuant to Italian Legislative Decree no. 58 of 24 February 1998 and

specifically under article 154-ter as to the description of the main risks and uncertainties, below are

reported the risks and/or uncertainties and the related actions taken by the Company to neutralise their

effects on the economic-financial position and performance.

Activities pertaining to the construction and operation of plants for the production of energy from

renewable sources, similarly to new environmental activities, are extremely regulated; TerniEnergia

analyses in detail the regulations of reference in order to be constantly updated and to adopt, if possible,

optimal applicable solutions. During the implementation of its operations, TerniEnergia therefore is subject

to risks deriving respectively from external factors pertaining to the regulatory and macroeconomic context

of reference, including the legislative, financial and credit sectors where the Group operates or which result

from strategic choices adopted during operations and which expose the Group itself to specific risks as well

as internal risks deriving from ordinary operational management.

The Group is therefore significantly influenced by trends in scenario variables that are not controlled by

TerniEnergia itself, including the issue and/or revocation of administrative authorisations, developments in

the regulatory framework, the energy produced by photovoltaic, biomass and biogas plants, assumptions

made in relation to the price of sold electrical and thermal energy. In order to contain these risks,

TerniEnergia has diversified both the types of investment as well as the locations of the operational plants

in order to diversify risks across different enterprises. In addition, the sector is characterised by a high level

of competition as well as rapid and significant technological innovation with consequences in terms of

financial requirements.

Participation in policies for the support and strengthening of the sector reported a significant decrease that

culminated in the issue of Italian Legislative Decree No. 91 of 24 June 2014, the so-called “Spalmaincentivi

Decree”, containing “urgent provisions for the agricultural sector as well as for environmental protection,

energy efficiency of school and university buildings, the launching and growth of companies, the

containment of costs affecting electrical prices and the immediate fulfilment of obligations pursuant to

European regulations”.

Despite the introduction of legislative provisions for decreasing incentives relative to the production of

electrical energy (as of 2015) – and which involve an inevitable decrease in cash flows from investments –

the management of the Parent Company believes it can confirm the existence of a satisfactory level of

profitability from the completed investments.

24

For the purposes of diversifying and mitigating risk relative to the regulatory framework of reference,

TerniEnergia has for some time implemented an internationalisation strategy by conducting its activities

for the design and construction of major industrial plans for the production of electrical energy from

renewable sources in countries with regulations that are favourable to the development of such

investments.

The construction of plants from renewable energy sources is primarily financed through project financing,

leasing and/or financing sources of both public and private origin. There remains the risk, even in light of

the market situation and the regulatory norms, of collection of any financing which is necessary or sufficient

for the realisation of projects or whether favourable conditions are attained. In addition, these financing

contracts could provide for certain limitations, including in terms of timing, and relative to the construction

and operational start-up of the plants or may require the issuing of guarantees.

During its current phase of developing business, the Group must constantly monitor these risk factors in

order to evaluate, in advance, any potentially negative factors and initiate any opportune actions to

mitigate them.

With regard to risks pertaining to legal disputes that are underway, refer to note 3.5.11 of the Explanatory

Notes.

1.11 RELATIONS WITH RELATED PARTIES

With reference to relations with related parties, reference is made to the Explanatory Notes to the Financial

Statements (Note 3.7).

1.12 INFORMATION REQUIRED BY ART. 123 BIS OF THE T.U.F. (CONSOLIDATED FINANCIAL ACT)

Structure of share capital

Categories of shares composing the share capital of the Parent Company:

N° OF SHARES % OF LISTED SHARE CAPITAL RIGHTS AND OBLIGATIONS

Ordinary shares 44,089,550 100 The shares are registered and give the right to vote at ordinary and extraordinary shareholders’ meeting as well as the right to participate in profits

25

The amount of the capital subscribed and paid up on 30 June 2016 was equal to Euro 57,007,230.00, divided

into 44,089,550 ordinary shares, without par value. It should be noted that 3,767,095 shares, representing

unlisted (as at the reporting date) own shares deriving from the share capital increase of 13 October 2014

are marked by ISIN Code IT0005059230 and differ with respect to those of the TerniEnergia shares that are

currently in circulation.

The Group has not issued other financial instruments that give the right to underwrite newly issued shares.

Restrictions on the transfer of securities

At the date of this Report, there are no restrictions on the transfer of securities, such as limits on the

ownership of securities or the need to obtain approval by the Group or other holders of securities.

Significant shareholdings

As at 30 June 2016, significant shareholdings in the Group’s equity, as resulting from the notices given

pursuant to Article 120 of the TUF and from the findings in the Register of Shareholders, were the following:

Shareholder Investment No. of shares % of share capital

Stefano Neri Direct 125,697 0.29%

through Italeaf S.p.A. (*) 19,867,103 45.06%

TerniEnergia S.p.A. Direct (**) 4,012,998 9.10%

(*) Italeaf is controlled by Stefano Neri, who owns 2.67% of the share capital directly and 51.15% indirectly, through Skill & Trust Holding, of which

he holds 62.92% of the share capital directly.

(**) own shares

Stefano Neri, Fabrizio Venturi and Monica Federici are directors of the Parent Company and shareholders,

with investments held directly and indirectly. More precisely, the shareholdings are as follows:

31/12/2015 Changes 30/06/2016

Total No. of shares 44,089,550 44,089,550

Shares % Purchases Sales Shares %

Italeaf S.p.A. 20,717,103 46.99% 850,000 19,867,103 45.06%

Fabrizio Venturi 74,654 0.17% 74,654 0.17%

Monica Federici 10,240 0.02% 10,240 0.02%

Stefano Neri 120,697 0.27% 5,000 125,697 0.29%

26

Stefano Neri directly holds 0.29% of the share capital of the Parent Company and controls Italeaf SpA, of

which he holds 2.67% directly and 51.15% indirectly through Skill & Trust Holding, of which he owns a

controlling stake of 62.92% of the share capital.

Securities conferring special rights

At the date of this Report, the Group has not issued securities which confer special control rights.

Restrictions on voting rights

At the date of this Report, the By-laws do not provide for restrictions on the right to vote.

Shareholder agreements

At the date of this report, there are no shareholder agreements or agreements between significant

shareholders pursuant to Art. 122 of the TUF.

Own shares

As of 30 June 2016, the own shares in the portfolio totalled 4,012,998, corresponding to 9.10% of the

ordinary share capital.

1.13 OTHER INFORMATION

Litigation, investigations and judicial proceedings in progress

With respect to litigations, investigations and legal proceedings, please refer to what is stated in the

explanatory notes under note 3.5.11.

Legislative Decree 231/2001 and Code of Ethics

The Parent Company has a specific governance structure that is essentially geared to the objective of

creating value for shareholders, while acknowledging the importance of social activities, in which it is

engaged.

In addition, an organisational and management model in accordance with Legislative Decree 231/2001 is in

force. This model is composed of a General Section, a Special Section and the Code of Ethics.

In the general section, the main contents of the model, the essential components and adopted auditing

tools have been defined.

The Model has three external appendices:

- the Code of Ethics, which, designed as a "charter of values", sets out the general principles which the

company's activities must comply with and in some parts is more extensive than the Decree, as it describes

27

the “ethical” commitment of the company, regardless of any criminal and administrative liability (and hence

also stigmatised behaviours which in themselves could potentially breach or circumvent the provisions of

the Decree);

- the Disciplinary System, which acts as a penalty instrument based on the general national labour contract

category and integrates the missing requirement provided for by the Consolidated Labour Act (Art. 30,

Legislative Decree 81/08) for the protection of Health and Safety at Work (SSL);

- the Articles of Association (with the Operating Regulations) of the Supervisory Board, a body in charge of

overseeing the functioning and observance of the Model, which must receive specific disclosures on

corporate activities.

The Code of Ethics is an integral part of the System of Internal Control and Risk Management and expresses

the principles of business ethics which the Group recognises as its own and with which directors,

employees, consultants and partners must comply. This code was revised in December 2013 to further

enhance the importance of sustainable operations that take into account the legitimate interests of all

stakeholders.

The Company performs on-going activities to promote the Code with respect to all its interlocutors, while

at the same time carrying out initiatives to improve working life in the field of training and information to

its employees.

Italian Legislative Decree No. 196/2003

The Parent Company, in accordance with Italian Legislative Decree No. 196/2003, has developed ad hoc

procedures for management control and information technology, in order to protect the confidentiality of

data of any kind and in general the privacy, both outwards and within the company.

The norm is consistent with the ISO 9001 quality management system, which reduces, to the extent

possible, the risk of destruction or accidental loss of data from unauthorised access or handling. The aim is

to protect the organisation from committing offenses involving administrative liability, such as computer

crime and illegal data processing, pursuant to Art. 24-bis of Legislative Decree 231/2001.

28

Performance of the Parent Company on the stock exchange

During the first half of 2016 TerniEnergia stock saw a negative trend up until the end of the first quarter,

with a loss of around 24%, coinciding with a corresponding drop in the STAR index (up until February) and

with the same trend as the FTSE Small Cap. TerniEnergia stock suffered from the deconsolidation of Free

Energia, in a moment of difficulty for the Italian financial markets, which in the latter months was affected

by systemic agitation and problems. Another aspect is represented by the difficulties suffered by the

reference sector (renewable energy), also in relation to the drop in electricity demand coinciding with the

government decisions on incentive policies, which produced a phase of extreme legislative uncertainty over

the year and, in conclusion, a reduction of the benefits for the companies in the sector. Signals that were

interpreted as evidence of weakness in the economy were reflected in petroleum prices, which began a

negative trend, nearly reaching historic minimum levels. Above all else the companies in the energy and

utilities sector suffered the consequences, a sector level. In the second quarter, by contrast, the

TerniEnergia stock had a constant trend up until May, with a drop under the value of Euro 1 coinciding with

the dividend registration and a consequent drop to all-time lows coinciding with the serious Italian bank

securities crisis and with the negative trend of the European energy and utility companies, subject - in the

period - to bearish strategies at continental level.

The stock reported, during the course of the year, an average price of Euro 1.54 and average daily volumes

of 44,772 shares. On 4 January 2016, the price reported a maximum value of Euro 1.573; the peak in

29

volumes (252,760) occurred on 16 June 2016.

Since the IPO and following the admission into the STAR segment of Borsa Italiana at the end of 2010,

TerniEnergia maintains open and constant communications with investors and stakeholders through an

effective policy of communications implemented by the internal and external Investor Relations

department, which is entrusted with managing relations with the financial community.

During the first half of 2016, the Investor Relations team participated in requested one-to-one meetings

with analysts and investors in addition to taking part in public events such as:

- Presentation of the “HUB” - Turn on the energy saving project (Milan - Hotel Principe di Savoia) -

Presentation to the business and financial community: 11 February 2016.

The stock is followed by Intermonte Sim through coverage studies and notes published periodically.

1.14 SIGNIFICANT EVENTS AFTER THE END OF THE PERIOD CLOSED AS AT 30 JUNE 2016

For significant events occurred after the closing of the year, refer to the information in the explanatory

notes under note 3.9 "Other information".

1.15 BUSINESS OUTLOOK

TerniEnergia, as announced in the strategic development guidelines and in various press releases, has

developed scouting activities for the purpose of using the portfolio of own shares as payment within the

sphere of extraordinary transactions for the finalisation of alliances and industrial or strategic mergers. This

process concluded with the identification of two target companies in the digital energy sector, as illustrated

in the section “Subsequent events” in the explanatory notes, “Softeco-Sismat Srl and Selesoft Consulting

Srl”, while it is still underway with regard to a company in the Energy management sector. Including, as a

consequence, in the next half year the potential effects of the finalisation of the agreements for the

acquisition of controlling interests in Softeco-Sismat Srl and Selesoft Consulting Srl (whose contribution will

essentially materialise in the fourth quarter of the year), in the smart energy sector, and of a target company

already identified in the Energy management sector, a significant contribution to revenues is reasonably

estimated for the current year from as early as the second half of 2016 along with a significant strategic

repositioning of TerniEnergia.

In detail, the Group intends to consolidate the entry into the sector of services and industrial production

and development of smart technologies and solutions for the transmission and distribution of energy (smart

grid), the flexible and prompt management of the energy production and consumption, the energy

efficiency, the management of the renewable energies and the Cleantechs (energy stations). The

transaction with the target companies Softeco-Sismat and Selesoft Consulting will make it possible to

supplement the activities in the renewables area, in energy efficiency and in Energy management with

30

innovative systems and solutions with high added value, which make it possible to introduce new

technologies in the chain capable of acting as a bridge between the industrial and “physical” bridge and

those digital and “virtual” ones.

Likewise, the integration transaction envisaged in the Gas&Power sector, will make it possible to strengthen

the Energy Management Business Line, developing the Power generation from renewable sources plants

and generating a wide array of strategic services and offers so as to pursue the validation on the dual fuel

market for industrial customers and public administration authorities.

In the Technical services sector, the Group is consolidating the commercial activities for the development

of new projects and for participation in new international tenders as “EPC contractor” for large utility

companies or investors of primary standing. Specifically, the opening of a site in Zambia is envisaged in the

second half of the year, for the construction of an industrial size photovoltaic plant with total power of 34

MWp on behalf of a leading Italian utility company. Furthermore, TerniEnergia aims to develop new growth

opportunities in countries with an ample growth potential, with the aim of consolidating its international

presence, as well as with a view to geographic diversification and maximisation of the value created with

the internationalisation strategy. In detail, in the photovoltaic sector, activities are underway preliminary

to the attainment of important contracts in emerging target countries characterised by abundant

renewable resources, stability of the regulatory systems and high economic growth. In this context,

negotiations are being finalised for the construction of a new giant photovoltaic plant using the EPC formula

(Engineering, procurement and construction) in South Africa, of a size similar to the two already recently

connected to the network.

Furthermore, TerniEnergia intends to enhance the Energy Saving Business Line activities. This objective,

pursued via the “Hub” project, operating formula to open up the industrial energy efficiency market

through “third party financing” in Italy, will see interesting growth prospects from the financial and

commercial partnership agreements entered into respectively with investment funds and with operators in

the Energy management sector, for cross-selling activities.

Within the sphere of the Cleantech business line activities, in the second half of the year the decision to

proceed with any sales of the assets will be assessed, according to operating methods to be defined, on a

consistent basis with the strategic choice of focusing on the smart energy business, deriving from the

expected positive outcome of the integration of the target companies.

31

2 FINANCIAL STATEMENTS

2.1 CONSOLIDATED STATEMENT OF FINANCIAL POSITION

Note 30 June 31 December (in Euro) 2016 2015 ASSETS Intangible fixed assets 3.4.1 5,309,242 4,460,745 Tangible fixed assets 3.4.2 81,280,641 82,616,544 Equity investments 3.4.3 1,188,986 2,157,923 Deferred tax asset 3.4.4 14,062,412 13,133,614 Non-current financial receivables 3.4.5 22,643,440 23,591,350

Total non-current financial assets 124,484,721 125,960,176

Inventories 3.4.6 13,893,554 23,329,978 Trade receivables 3.4.7 31,843,192 52,361,935 Other current assets 3.4.8 20,320,750 24,104,536 Financial receivables 3.4.9 3,300,155 4,192,193 Cash and cash equivalents 3.4.10 22,317,328 11,893,388

Total current financial assets 91,674,979 115,882,030

TOTAL ASSETS 216,159,700 241,842,206

LIABILITIES AND SHAREHOLDERS’ EQUITY Share capital 57,007,230 57,007,230 Reserves (4,158,425) (3,964,935) Result for the period 894,094 1,947,386

Total Group equity 53,742,899 54,989,681

Minority interests 717,047 191,614 Result of the period attributable to minority interests 213,588 610,058

Total equity 3.5.1 54,673,534 55,791,353

Provisions for employee benefits 3.5.2 1,386,500 1,149,966 Deferred taxes 3.5.3 1,208,935 1,294,323 Non-current financial payables 3.5.4 79,532,172 79,272,033 Other non-current liabilities 3.5.5 268,227 247,492 Derivatives 3.5.6 3,547,885 3,251,759

Total non-current liabilities 85,943,719 85,215,573

Trade payables 3.5.7 44,066,235 63,543,245 Payables and other financial liabilities 3.5.8 25,446,988 24,185,097 Taxes payable 3.5.9 3,270,671 1,330,322 Other current liabilities 3.5.10 2,758,553 11,776,616

Total current liabilities 75,542,447 100,835,280

TOTAL LIABILITIES 161,486,166 186,050,853

TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY 216,159,700 241,842,206

2.2 CONSOLIDATED INCOME STATEMENT

32

Note Six months ended 30 June

2016

Six months ended 30 June

2015 (in Euro)

Revenues 3.6.1 47,082,929 147,929,109

Other operating revenues 3.6.1 3,452,784 3,341,547

Change in inventories of semi-finished and finished products 3.6.2 6,476 (211,255)

Cost of raw materials, consumables and goods 3.6.3 (23,489,441) (57,219,816)

Costs for services 3.6.4 (14,585,423) (77,961,000)

Personnel costs 3.6.5 (2,174,503) (3,502,480)

Other operating costs 3.6.6 (789,372) (1,640,562)

Amortisation, depreciation, allocations and write-downs 3.6.7 (3,554,529) (2,869,611)

Operating result 5,948,923 7,865,932

Financial income 3.6.8 743,102 422,793

Financial charges 3.6.8 (4,347,073) (5,634,601)

Profit share from joint ventures 3.6.9 619,659 49,532

Pre-tax result 2,964,611 2,703,657

Taxes 3.6.10 (1,856,929) (1,219,317)

Net (profit)/loss of the year 1,107,682 1,484,340

- of which pertaining to the Group 894,094 1,359,326

- of which pertaining to minority interests 213,588 125,014

Earnings per share - base and diluted 0.021 0.031

33

2.3 CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

Note 30 June

(in Euro) 2016 2015

Net profit for the period 1,107,682 1,484,340

Change in cash flow hedge reserve (921,592) 947,542

Translation difference (478,759) (41,146)

Tax effect of charges/(income) recognised in equity 221,182 (260,574)

Total other income statement items of the period that will be recognised later in the income statement 3.5.1 (1,179,169) 645,822

Actuarial gains/(losses) from employee termination indemnities (114,989)

Tax effect of charges/(income) recognised in equity 27,597

Total other income statement items of the period that will not be recognised later in the income statement 3.5.1 (87,392)

Total comprehensive income for the period (158,879) 2,130,162

- of which pertaining to the Group (372,467) 2,005,149

- of which pertaining to minority interests 213,588 125,014

34

2.4 STATEMENT OF CHANGES IN CONSOLIDATED SHAREHOLDERS’ EQUITY

Description

Share capital

Reserves Total

reserves Result for the

period Total Group

equity Minority interests Total equity

(in Euro) Price

premium reserve

Legal reserve

Extraordinary reserve Other

Balance as of 31 December 2015 57,007,230 13,285,035 2,142,138 10,181,064 (29,573,172) (3,964,935) 1,947,387 54,989,682 801,672 55,791,353

Result for the period 105,276 1,842,110 1,947,387 (1,947,387)

Dividend distribution (1,001,814) (1,001,814) (1,001,814) (1,001,814)

Other movements 127,498 127,498 127,498 (84,624) 42,873

Transactions with shareholders 105,276 967,794 1,073,070 (1,947,387) (874,316) (84,624) (958,940)

Net profit for the period - - - - - - 894,094 894,094 213,588 1,107,682 Other items of the statement of comprehensive income - - - - (1,266,561) (1,266,561) (1,266,561) (1,266,561)

Total profit for the period (1,266,561) (1,266,561) 894,094 (372,467) 213,588 (158,879)

Balance as of 30 June 2016 57,007,230 13,285,035 2,247,414 10,181,064 (29,871,939) (4,158,425) 894,094 53,742,899 930,635 54,673,534

35

2.5 CONSOLIDATED CASH FLOW STATEMENT

30 June (in Euro) Note 2016 2015

Pre-tax profit 2,964,611 2,703,657

Amortisation/Depreciation 2,430,429 2,752,250 Write-downs of fixed assets and receivables 1,124,100 117,361 Allocations to the employee benefits fund 183,185 106,885 Result of joint ventures accounted for at equity and reversal of margin (619,659) (49,532) Effect of derivatives in income statement (273,507) Change in inventories 9,436,424 (37,724,503) Change in trade receivables 20,518,743 3,482,600 Change in other assets 3,515,044 (7,932,200) Change in trade payables (19,477,010) 33,465,371 Change in other liabilities (9,928,094) 13,694,648 Payment of employee benefits (34,043) (88,715)

Net cash flow (used in)/generated by operating activities 9,840,221 10,527,821

Investments in tangible fixed assets (983,222) (3,368,643) Investments in intangible fixed assets (959,800) (507,700) Equity investments 464,496 177,604 Change in receivables and other financial assets 1,839,948 3,669,127

Net cash flow used in investing activities 361,422 (29,612)

Change in payables and other financial assets 1,261,891 (2,224,218) Change in non-current financial payables (91,821) (2,208,352) Other changes in shareholders’ equity 54,041 (176,084) Payment of dividends (1,001,814) (2,865,821) Net cash flow generated by financing activities 222,297 (7,474,475)

Comprehensive cash flow for the period 10,423,940 3,023,735 Cash and cash equivalents at the beginning of the period 11,893,389 14,177,490 Cash and cash equivalents at the end of the period 22,317,328 17,201,225

Interest (paid)/collected (3,220,056) (4,476,829)

36

3 EXPLANATORY NOTES TO THE CONSOLIDATED INTERIM FINANCIAL STATEMENTS AS AT 30

JUNE 2016

3.1 GENERAL INFORMATION

TerniEnergia S.p.A. (“TerniEnergia”, “Company” or “Parent Company”) is a joint stock company with

registered office in Narni (Italy), Strada dello Stabilimento 1, listed on the Italian Stock Exchange on the Star

segment of MTA.

TerniEnergia, founded in the month of September 2005 and part of the Italeaf Group, is the first “Italian

smart energy company” and operates in the renewable energy field, in energy efficiency and in energy and

waste management. TerniEnergia acts as a system integrator, with a turnkey offer for industrial

photovoltaic plants, both on behalf of third parties and on its own, including through joint ventures with

primary national operators. The Company seeks to strengthen sales of solar energy. TerniEnergia operates

in waste management, in the recovery of material and energy and in the development and production of

technologies. In particular, the Company is active in the recovery of out-of-use tyres; in the treatment of

biodegradable waste through the implementation of biodigesters; in the production of energy from

biomass; in the management of biological depuration plants; in the decommissioning of industrial plants;

in the recovery of metals that must be demolished and the improvement of industrial plants; and in the

development and production of technological equipment. The Group is active in energy management, the

sale of energy to high energy-consuming customers, and is a provider of administrative, financial and credit

management services. In addition, TerniEnergia operates in the development of energy efficiency plants