conducted by vanson bourne research - dell emc · pdf filedelay in product/ service ... the...

TRANSCRIPT

1 © Copyright 2013 EMC Corporation. All rights reserved.

Conducted by Vanson Bourne Research

N o v e m b e r 2 0 1 3

2 © Copyright 2013 EMC Corporation. All rights reserved.

3200

INTERVIEWS ALTOGETHER, 1600 IT & 1600

BUSINESS DECISION-MAKERS

50/50 SPLIT BETWEEN ORGANIZATIONS WITH

100–1000 EMPLOYEES & MORE THAN 1000 EMPLOYEES

10 VERTICALS

COUNTRIES USA CANADA BRAZIL UK FRANCE GERMANY ITALY SPAIN NORDICS BENELUX RUSSIA INDIA SOUTH AFRICA AUSTRALIA JAPAN CHINA

100 IT

DECISION- MAKERS & 100

BUSINESS DECISION- MAKERS

3 © Copyright 2013 EMC Corporation. All rights reserved.

THE FOUR BIG MEGATRENDS IN INFORMATION TECHNOLOGY TODAY

ARE CLOUD COMPUTING, BIG DATA, SOCIAL NETWORKING AND

MOBILE DEVICES. ADOPTION AND MATURITY OF THESE TRENDS

MUST FLOAT UPON A SEA OF TRUST — TRUST THAT MY

INFORMATION IS SECURE IN THE CLOUD, TRUST THAT MY DATA

WON’T BE LOST OR STOLEN, TRUST THAT MY IT WILL BE

OPERATIONAL WHEN IT NEEDS TO BE — WHICH, THESE DAYS, IS

ALL THE TIME. THE MORE TRUST THAT CAN BE EARNED AND

GUARANTEED, THE BIGGER AND FASTER THE IMPACT OF THESE

TRENDS. CONVERSELY, THE LESS TRUST THAT IS ESTABLISHED, THE

MORE LIMITED THESE TRENDS WILL BE.

DAVID GOULDEN

4 © Copyright 2013 EMC Corporation. All rights reserved.

OVERALL MATURITY

LAGGARDS EVALUATORS ADOPTERS LEADERS

0

10

20

30

40

50

60

70

0 25 50 75 100

NU

MBER O

F R

ESPO

ND

EN

TS

MATURITY SCORE (OUT OF 100)

17% 8% 40% 36%

OVERALL MATURITY DISTRIBUTION

5 © Copyright 2013 EMC Corporation. All rights reserved.

MATURITY PILLARS

LAGGARDS EVALUATORS ADOPTERS LEADERS

0

10

20

30

40

50

60

70

0 25 50 75 100

NU

MBER O

F R

ESPO

ND

EN

TS

MATURITY SCORE (OUT OF 100)

17% 8% 40% 36%

OVERALL MATURITY DISTRIBUTION

6 © Copyright 2013 EMC Corporation. All rights reserved.

SCORING METHODOLOGY The study focuses on attributes of IT

– information availability, backup, &

security – that contribute most to

the ability to withstand & quickly

recover from disruptive IT incidents.

Those organizations with more

progressive strategies & those

using more advanced technology

achieved higher ratings.

1,600 IT responses were used to

rank their organizations’ maturity

levels, ranging from lowest to

highest – Laggard, Evaluator,

Adopter, & Leader.

7 © Copyright 2013 EMC Corporation. All rights reserved.

MATURITY SCORE BY COUNTRY

65.2

61.8

60.9

53.8

52.8

51.6

51.4

49.7

49.5

49.5

49.4

49.1

48.7

48.4

43.0

38.8

China

USA

South Africa

Brazil

Australia

Spain

France

UK

Canada

Benelux

India

Italy

Russia

Germany

Nordics

Japan

(OUT OF 100)

CHINA IS THE MOST MATURE COUNTRY—JUST AHEAD OF AHEAD OF THE USA

3 OF THE 4 MOST MATURE COUNTRIES ARE

B R I C S

JAPAN L A G S A S T H E L E A S T MATURE

8 © Copyright 2013 EMC Corporation. All rights reserved.

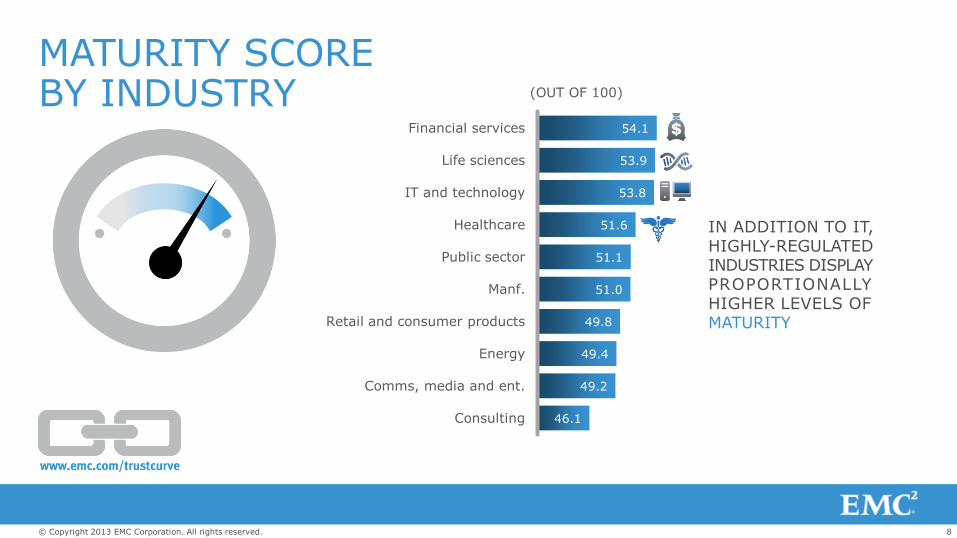

MATURITY SCORE BY INDUSTRY

54.1

53.9

53.8

51.6

51.1

51.0

49.8

49.4

49.2

46.1

Financial services

Life sciences

IT and technology

Healthcare

Public sector

Manf.

Retail and consumer products

Energy

Comms, media and ent.

Consulting

(OUT OF 100)

IN ADDITION TO IT, HIGHLY-REGULATED INDUSTRIES DISPLAY PROPORTIONALLY HIGHER LEVELS OF MATURITY

9 © Copyright 2013 EMC Corporation. All rights reserved.

THE CRISIS Widespread unplanned downtime, security breaches, & data loss

of respondents’ companies have

suffered at least one of the

following: unplanned downtime

(37%), security breach (23%) or

data loss (29%) in the last 12

months.

61% Nearly half—

45% —of respondents report that their senior

executives are not confident that their

organization has adequate data

protection, security, & IT availability.

10 © Copyright 2013 EMC Corporation. All rights reserved.

81%

65%

51%

39%

Leaders

Adopters

Evaluators

Laggards

SENIOR EXECUTIVES’ CONFIDENCE IN THEIR ORGANIZATION’S IT MATURITY

On average, only 55% of respondents report their senior executives have any confidence in their data protection, security, & availability. This rises significantly with each level of maturity. Conversely, 45% cited no confidence.

Do you think your senior executives are confident they currently have adequate data protection, security, & availability?

Only showing percentage for “yes, they already are”, by overall maturity (Asked to all 3200 respondents)

11 © Copyright 2013 EMC Corporation. All rights reserved.

SENIOR EXECUTIVES’ CONFIDENCE IN THEIR ORGANIZATION’S IT MATURITY (COUNTRY)

Japan—the least mature country—has the smallest percentage of respondents reporting that their senior teams have trust in IT. Interestingly, the BRICS countries are scattered throughout the centre—neither leading or lagging in this regard.

66%

64%

64%

63%

62%

61%

59%

58%

56%

55%

54%

50%

49%

49%

46%

31%

Germany

France

Benelux

Spain

India

USA

Australia

Canada

China

South Africa

UK

Brazil

Italy

Russia

Nordics

Japan

Do you think your senior executives are confident they currently have adequate data protection, security, & availability?

Only showing percentage for “yes, they already are”, by country (Asked to all 3200 respondents)

12 © Copyright 2013 EMC Corporation. All rights reserved.

SENIOR EXECUTIVES’ CONFIDENCE IN THEIR ORGANIZATION’S IT MATURITY (INDUSTRY)

Life sciences, seen previously to be among the most mature in terms of the IT Trust Curve, is the vertical least likely to report their senior teams are confident in their organization’s IT. 10% of those in the public sector don’t think their senior teams will ever have this confidence (compared to 6% on average).

59%

58%

57%

57%

55%

55%

55%

51%

50%

48%

Financial services

IT and technology

Consulting

Retail and consumer …

Energy

Manf.

Comms, media and ent.

Healthcare

Public sector

Life sciences

Do you think your senior executives are confident they currently have adequate data protection, security, & availability?

Only showing percentage for “yes, they already are”, by vertical (Asked to all 3200 respondents)

13 © Copyright 2013 EMC Corporation. All rights reserved.

CONSEQUENCES OF INCIDENTS IN THE LAST 12 MONTHS (COUNTRY) Of the 61% of organizations who have experienced either unplanned downtime, a security breach or data loss at least once in the last 12 months, the top 3 consequences are a loss of employee productivity (45%), loss of revenue (39%), and loss of customer confidence/loyalty (32%).

Top consequence in each country:

• Loss of employee productivity: USA (58%), Canada (58%), Brazil (46%), UK (61%), France (36%), Nordics (48%), Russia (48%), Benelux (34%), South Africa (59%), Australia (47%)

• Loss of revenue: China (59%), Spain (46%), Italy (40%), Germany (40%), Russia (48%), Benelux (34%)

• Loss of an incremental business opportunity: Japan (38%)

• Loss of business to a competitor: India (47%)

45%

39%

32%

27%

27%

26%

26%

26%

23%

20%

16%

10%

1%

4%

Loss of employee productivity

Loss of revenue

Loss of customer confidence/loyalty

Loss of an incremental business …

Loss of business to a competitor

Delay in product/ service …

Loss of a new business opportunity

Loss of customers

Damage to company brand and …

Loss of repeat business

Delay in getting products/ …

Damage to company stock price …

Other

None of these

What were the consequences of the incident(s) your organization experienced in the last 12 months?

(Asked to those who have experienced downtime, security breach(es) and/or data loss in the last 12 months 1956/3200)

14 © Copyright 2013 EMC Corporation. All rights reserved.

MATURITY MATTERS.

THE IMPACT 53% of organizations in the highest maturity

segment reported data recovery time

measured in minutes or less for their most mission-

critical applications compared with only

27% across all respondents who reported

data recovery in minutes or less The more advanced the organization’s maturity, the less they suffer when it comes to data loss, downtime, & security breaches.

of companies in the highest maturity

segment believe they are able to recover

100% of their lost data in every instance versus only

in the lowest maturity segment

76%

44% Organizations in the lowest maturity segment

(Laggards) lost one and a half times more

money over the last 12 months as a result of

downtime than those in the highest maturity

segment (Leader). Average annual financial loss

from downtime across all respondents is

$494,037.

65%

15 © Copyright 2013 EMC Corporation. All rights reserved.

“If you had adequate controls to protect data and breaches were stopped before impact, how would your organization benefit?” (Asked to respondents who have experienced a security breach/breaches in the last 12 months 734/3200)

THE UPSIDE

42%

43%

45%

48%

49%

Reduced cost of application

deployment / time to market

More time for innovation &

analysis

Lower cost of investigation &

response

Lower barrier to information

sharing

Expedited audits & lower

compliance reporting cost

16 © Copyright 2013 EMC Corporation. All rights reserved.

FACTORS THAT LIMIT TECHNOLOGICAL PROGRESS

92% of all respondents experience inhibitors to their technology project success.

China is the only country where budget is not the main inhibitor. Instead resources and/or workload constraints tops the list here (50%), followed by planning and anticipation (46%), knowledge and skills (44%) and then budget (41%).

A lack of confidence in technology impacts one in five, & a lack of executive/management support inhibits one in seven.

8%

14%

19%

25%

32%

33%

35%

52%

We have no limits to our technology

project success

Lack of executive/management

support

Lack of trust in technology/IT

Culture (flexibility, acceptance)

Knowledge & skills

Planning and anticipation

Resources and/or workload

constraints

Budget

What most limits your organization's technology project success in relation to data protection, security, & availability?

(Asked to all 3200 respondents)

17 © Copyright 2013 EMC Corporation. All rights reserved.

DIFFERING VIEWS

Where is the motivation/drive for future plans/projects to deliver resilient & secure IT infrastructure coming from?

Percentage that selected “internal: IT department”, by respondent type (Asked to all 3200 respondents

70%

50%

ITDMs

BDMs

Just 50% of BDMs (business decision makers) consider the IT department to be a driver of a resilient & secure infrastructure—compared to 70% of ITDMs (IT decision makers) themselves.

18 © Copyright 2013 EMC Corporation. All rights reserved.

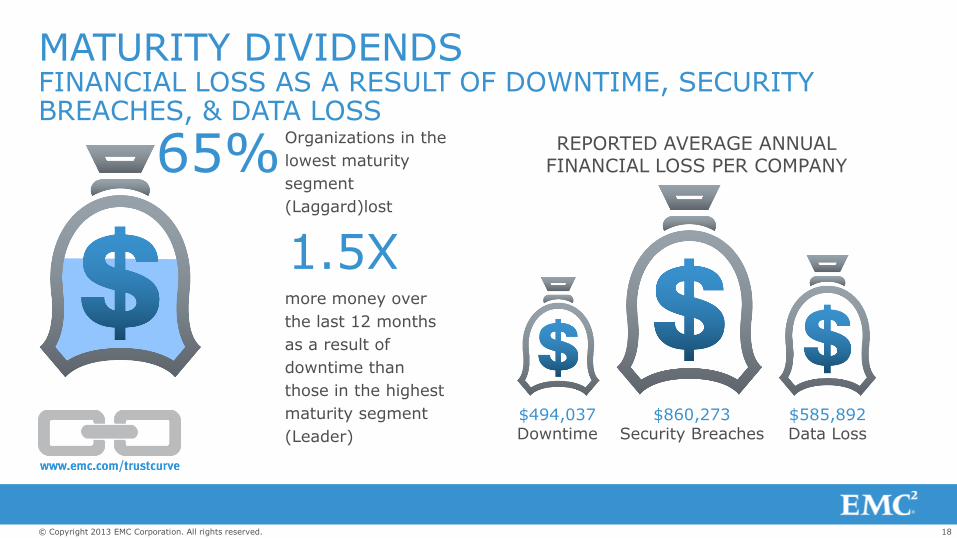

MATURITY DIVIDENDS FINANCIAL LOSS AS A RESULT OF DOWNTIME, SECURITY BREACHES, & DATA LOSS

$585,892 Data Loss

Organizations in the

lowest maturity

segment

(Laggard)lost

more money over

the last 12 months

as a result of

downtime than

those in the highest

maturity segment

(Leader)

1.5X

REPORTED AVERAGE ANNUAL FINANCIAL LOSS PER COMPANY

$860,273 Security Breaches

$494,037 Downtime

65%

19 © Copyright 2013 EMC Corporation. All rights reserved.

MATURITY DIVIDENDS ONLY AROUND A QUARTER OF SURVEYED ORGANIZATIONS CAN RECOVERY DATA IN MINUTES OR LESS

During an unexpected event causing downtime to our most critical applications.

(Asked to all 1600 respondents)

66% OUR RECOVERY TIME IS MEASURED IN HOURS

The most common response given overall is a recovery time of hours.

25% OUR RECOVERY TIME IS MEASURED IN MINUTES

A quarter of organizations have a recovery time of minutes for mission-critical applications. Therefore, 27% of organizations surveyed have a recovery time of minutes or less for their mission-critical applications.

2% OUR RECOVERY TIME IS ZERO

Only 2% of surveyed organizations report a recovery time of zero for their most critical applications.

3% OUR RECOVERY TIME IS 1 DAY OR MORE

Though a small minority report a recovery time of a day or more.

*

*Don’t know

20 © Copyright 2013 EMC Corporation. All rights reserved.

MATURITY DIVIDENDS BIG DATA ANALYTICS IS MORE LIKELY TO BE DEPLOYED BY THOSE WITH A HIGHER LEVEL OF TRUST MATURITY

74% of the leaders have already deployed Big Data analytics compared to just 8% of the laggards. However, less mature organizations are more likely to be in the planning stages.

8%

23%

42%

74%

74%

63%

50%

25%

18%

14%

8%

1%

Laggards

Evaluators

Adopters

Leaders

No plans

Deployment underway or in planning stages

Already deployed

Which of these strategic projects, requiring availability, data protection, & security do you have?

Looking at Big Data analytics only, by overall maturity (Asked to all 1600 IT respondents)

22 © Copyright 2013 EMC Corporation. All rights reserved.

Questions used to score Continuous Availability (i) IT only

Within each pillar section, respondents were asked questions that determine their technological maturity, the three used in Continuous Availability were (max score = 18):

Select which of the following best characterizes your current IT infrastructure:

Backup is the main component of our availability strategy – (2pt.)

Backup and replication are key components of our availability strategy – (2pt.)

Replication and standby servers are key components of our availability strategy – (3pts.)

Replication of virtual servers with restart capabilities are key components of our availability strategy - (4pts.)

Active-active instances of applications across data centers is key component of our availability strategy – (6pts.)

During an unexpected event causing downtime to our most critical applications:

Our recovery time is 1 day or more (please specify) – (2pt.)

Our recovery time is measured in hours – (3pts.)

Our recovery time is measured in minutes – (4pts.)

Our recovery time is zero – (6pts.)

Don’t know – no score

23 © Copyright 2013 EMC Corporation. All rights reserved.

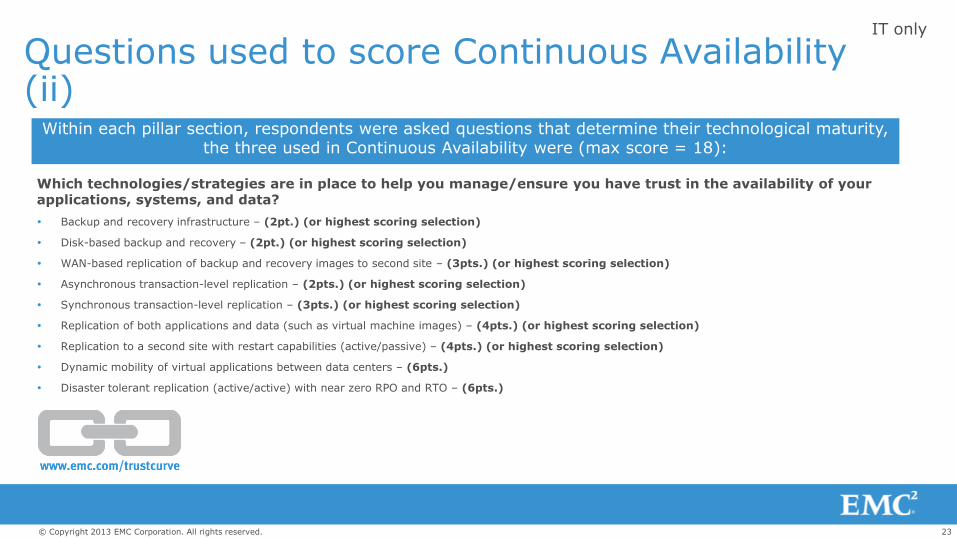

Questions used to score Continuous Availability (ii)

IT only

Within each pillar section, respondents were asked questions that determine their technological maturity, the three used in Continuous Availability were (max score = 18):

Which technologies/strategies are in place to help you manage/ensure you have trust in the availability of your applications, systems, and data?

Backup and recovery infrastructure – (2pt.) (or highest scoring selection)

Disk-based backup and recovery – (2pt.) (or highest scoring selection)

WAN-based replication of backup and recovery images to second site – (3pts.) (or highest scoring selection)

Asynchronous transaction-level replication – (2pts.) (or highest scoring selection)

Synchronous transaction-level replication – (3pts.) (or highest scoring selection)

Replication of both applications and data (such as virtual machine images) – (4pts.) (or highest scoring selection)

Replication to a second site with restart capabilities (active/passive) – (4pts.) (or highest scoring selection)

Dynamic mobility of virtual applications between data centers – (6pts.)

Disaster tolerant replication (active/active) with near zero RPO and RTO – (6pts.)

24 © Copyright 2013 EMC Corporation. All rights reserved.

Question used to score Advanced security IT only

Within each pillar section, respondents were asked questions that determine their technological maturity, the one used in Advanced Security was (max score = 18):

Which technologies/strategies do you have in place to help you trust your infrastructure and data is secure?

Strong authentication - 1pt.

Video surveillance – 0pts.

Governance, risk & compliance software – 2pt.

Anti-virus/anti-malware - 2pts.

Network firewalls/application firewalls/intrusion detection - 1pt.

Log/security monitoring - 1pt.

Identity & access management -1pt.

Encryption/tokenization - 1pt.

Digital forensics – 3pt.

Predictive analytics – 3pt.

Security operations center - 3pts.

25 © Copyright 2013 EMC Corporation. All rights reserved.

Questions used to score Integrated Backup and Recovery (i)

IT only

Within each pillar section, respondents were asked questions that determine their technological maturity, the two used in Integrated Backup and Recovery were (max score = 18):

Select which of the following best characterizes your current IT infrastructure’s information protection capabilities to prevent/minimize data loss due to site disasters or technical failures:

Backup is performed departmentally, as opposed to a centralized service, with independent backup tools requiring application downtime - (2pt.)

Multiple, separate application-specific backup tools are deployed across the organization regularly requiring application downtime during the backup process – (3pt.)

Backup is coordinated with storage features to minimize application downtime for the backup process and disk-based backup has been deployed – (5pts.)

Centralized disk-based backup systems exploit de-duplication efficiencies while providing comprehensive reporting of backup actives and protection status – (7pts.)

Comprehensive backup solutions include replication of backup images to secondary sites, enable archival storage, and ensure we meet our data retention and retrieval goals – (9pts.)

26 © Copyright 2013 EMC Corporation. All rights reserved.

Questions used to score Integrated Backup and Recovery (ii)

IT only

Within each pillar section, respondents were asked questions that determine their technological maturity, the two used in Integrated Backup and Recovery were (max score = 18):

Which technologies/strategies are you currently using to prevent data loss?

Tape-based backup and archive – (2pt.) (or highest scoring selection)

Disk-based backup and archive – (3pt.) (or highest scoring selection)

WAN-based replication of backups – (4pts.) (or highest scoring selection)

Software to assist in eDiscovery projects – (5pts.) (or highest scoring selection)

De-duplication of backup and archive data – (6pts.) (or highest scoring selection)

Consolidated backup and archive infrastructure – (7pts.) (or highest scoring selection)

Integrated backup and archive to meet data retention requirements – (9pts.) (or highest scoring selection)