comprehensive cost management ccm - c.ymcdn.com · –ccm unit cost development case study...

TRANSCRIPT

page 1

M

Comprehensive Cost Management

CCInstitute – 2016

page 2

•Business Performance Management Model

•Developing & Administering an CCM Information Database

–CCM Responsibility Center Classifications

–CCM Cost Distribution Techniques for Integrated Profitability

–CCM Unit Cost Development Techniques

–CCM Unit Cost Development Case Study

Comprehensive Cost Management Agenda

Session I

Session II

•Cost Deployment – Integrated Resource Management–CCM Unit Cost Deployment Case Study

•Cost Deployment – Integrated Profitability Measurement

•Establishing Business Performance Management Targets

•Strategic Analyses and Pricing

page 3

Business Performance Management

(BPM) Model

Fostering the dialogue between

Service Provider and Service Receiver

page 4

Phase 1 - Budgeting and Responsibility Center Reporting

Phase 2 - Expense Pooling and Allocations

Phase 3 – Organization/Line of Business Profitability

Phase 4 - Product and Customer Value Estimates

Phase 5 - Comprehensive Cost Management

Phase 7 - Integration – Resource Mgmt. and Profitability Measurement

Business

Information

Value

Business Information Requirements

Financial Information

directly linked to

Business Events

and Customer

Interactions

Accounting

Integration

Performance Measurement Continuum

Phase 10 - Strategic Management

Phase 8 – Integrated and InformedPlanning and Forecasting

Phase 6 - Integration – Financial and Non-Financial Performance Metrics

Phase 9 – Strategic Business Analysis

Business Performance Management

page 5

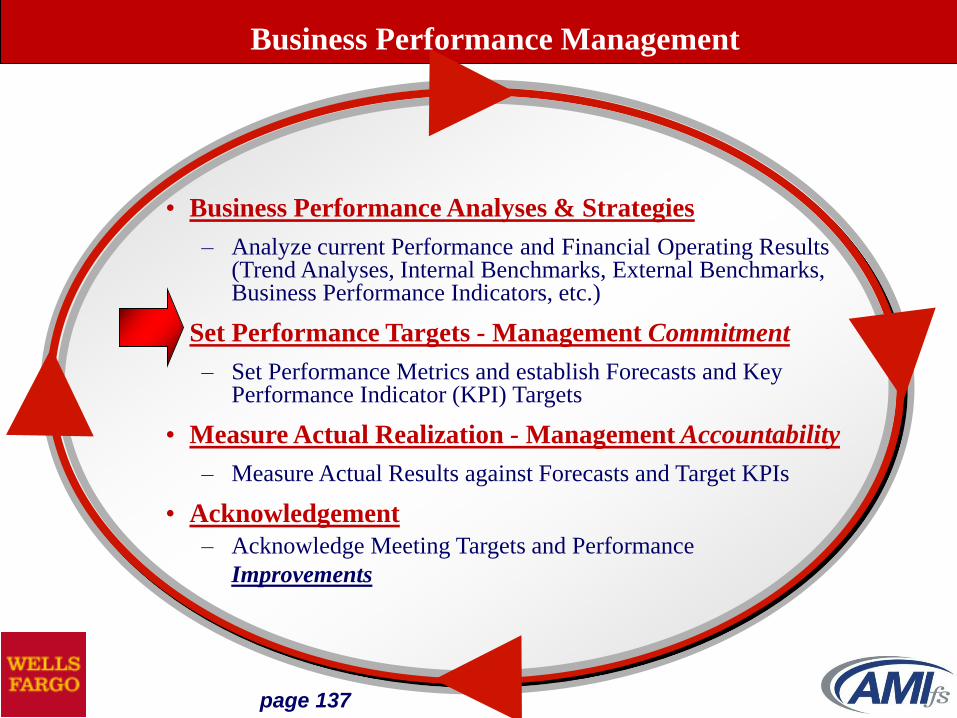

• Business Performance Analyses & Strategies

– Analyze current Performance and Financial Operating Results (Trend Analyses, Internal Benchmarks, External Benchmarks, Business Performance Indicators, etc.)

• Set Performance Targets - Management Commitment

– Set Performance Metrics and establish Forecasts and Key Performance Indicator (KPI) Targets

• Measure Actual Realization - Management Accountability

– Measure Actual Results against Forecasts and Target KPIs

• Acknowledgement

– Acknowledge Meeting Targets and Performance

Improvements

Business Performance Management

page 6

Comprehensive Cost Management (CCM) Background:

•CCM includes the Activity-Based Costing methodology

(Capacity- Based and Allocation-Based Unit Costing), in

addition to other costing methodologies where appropriate, to

account for 100% of Non-Interest expenses.

•CCM also includes cost distribution rules and techniques, as

well as cost deployment criteria.

•CCM provides a linkage to non-financial performance metrics.

•CCM promotes the comprehensive performance aspects of

the Management Accounting processes.

•CCM provides for Integrated Profitability and Integrated

Resource Management.

Business Performance Management

page 7

Integrated

Resource

Management

Scorecard

Integrated Performance

Measurement Architecture

Strategic Management

Strategic

Analyses,

Pricing &

Forecasting

Integrated

Profitability

Measurement

Scorecard

Analyze Performance Results

Set Performance Targets

Measure Actual PerformanceResults vs. Targets

Acknowledge PerformanceImprovements

Integrated CCM

InformationDatabase

Business Performance Management

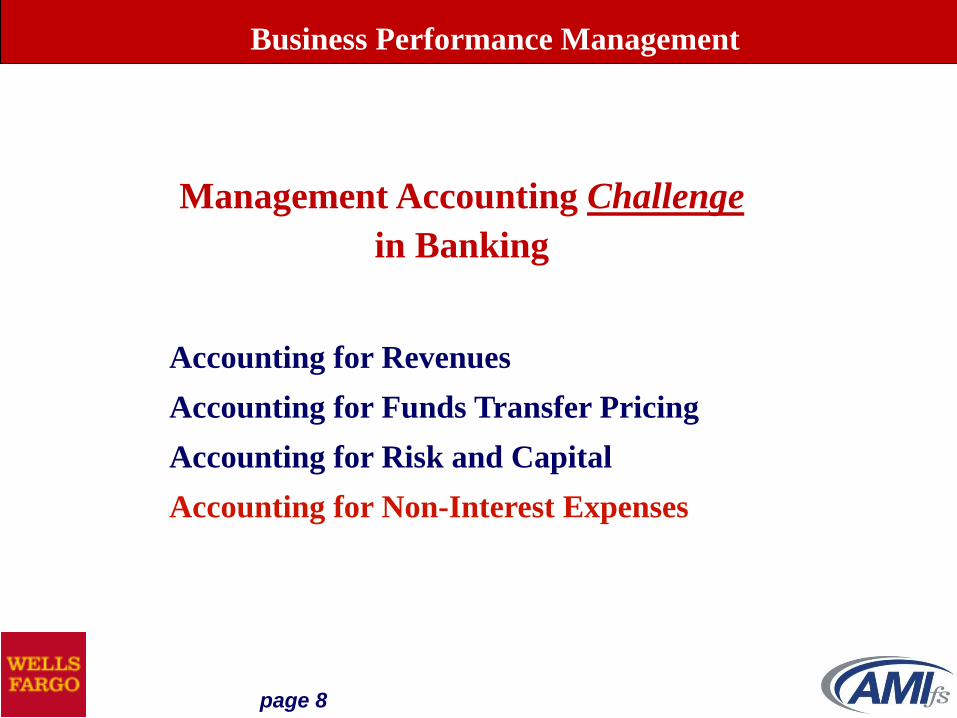

page 8

Accounting for Revenues

Accounting for Funds Transfer Pricing

Accounting for Risk and Capital

Accounting for Non-Interest Expenses

Management Accounting Challenge

in Banking

Business Performance Management

page 9

Business Performance Management

Activity Based Costing - Benchmarking Common Practices IISponsored by ALG Software, September 21, 2004 11:00 AM EST

# Questions and Answewrs # %

1 What is the current stage of ABC at your organization?

Exploratory - evaluation and review of the concept and it's potential need and impact 1 9%

Infancy - beginning cost studies to collect information and training staff 1 9%

Intermediate - continuing cost studies starting some maintenance and determining how to use 8 72%

Mature - Moved from ABC to ABM - maintaining and using data to support organizational decisions 1 9%

8 What BEST describes how your organization uses ABC?

Not currently implementing any cost allocations or other 0 0%

Using to evaluate organizational product & customer profitability 11 84%

Using it as a tool for cost control and cost management 1 7%

Using it for Budgeting and planning 0 0%

Using it for Incentive Compensation 0 0%

All of the above except for A 1 7%

8B What is your next planned use of ABC?

Not currently implementing any cost allocations or other 0 0%

Using to evaluate organizational product & customer profitability 1 9%

Using it as a tool for cost control and cost management 7 63%

Using it for Budgeting and planning 2 18%

Using it for Incentive Compensation 1 9%

All of the above except for A 0 0%

page 10

Integrated Profitability Measurement:

•Customer by Product

•Organization or LOB by Product

•Product by Organization

Integrated Resource Management:

•Delivery Channel by Resource Group

•Resource Group by Delivery Channel

•Business Process

Management Accounting Scorecards

Business Performance Management

page 11

Financial Accounting

vs.

Management Accounting

Expenses vs. Costs

Business Performance Management

page 12

Expenses (Incurred)

– to become liable for or subject to, within

an accounting period (i.e. month/quarter)

Costs (Derived)

– an outlay (i.e. $/effort) made to achieve

an object or unit of measure

Expenses vs. Costs

Business Performance Management

page 13

Product

Revenues

Expenses

Incurred

Net

Income

Top of the Institution

Financial Accounting View

Business Performance Management

page 14

Product

RevenuesProcessing

Credits

Distributed

Costs

Expenses

Incurred

Cost

Recovery

Residual

Management Accounting View

Product

Margins

Business Performance Management

(Customer, Product and LOB Profitability/Integrated Resource Management)

page 15

Product

Revenues

Cost

Recovery

Distributed

Costs

Expenses

Incurred

Product

Margins

Cost

Recovery

Residual

Recovery

Residual

Product

Revenues

DistributedCosts

Product

Margins

Net

Income

Expenses

Incurred

Management Accounting View Reconciliation

Business Performance Management

page 16

Linking

Integrated Profitability

and

Integrated Resource Management

Information

Business Performance Management

page 17

Product Cost

Drivers (PCDs)

Integrated Resource

Management

Integrated ProfitabilityMeasurement

Integrated

CCM

Information

DatabaseResource Cost

Drivers (RCDs)

Unit Costs for Integrated Profitability

and Integrated Resource Management

(e.g. Item Capture

in Check Processing)

(e.g. Deposit less Cash -

Basic Checking for

Customer X at Branch Y)

(Product, Customer,

Line of Business)

(Business Process,Delivery Channel,Resource Group)

Business Performance Management

page 18

Product

Revenues

Product

Margin

Analyses

Processing

Credits

Expenses

Incurred

CostRecoveryResidualAnalyses

Actual vs. Plan

Actual vs. Forecast

Forecast vs. Plan

Processing

Charges

Integrated

Profitability

IntegratedResource

Management

$ D

imen

sion

-Product

-Customer

-LOB/Org.

Business Performance Management

RCDs

PCDs

-Resource Group

-Delivery Channel

-Business Process

page 19

BRANCH

e.g. Customer Deposits

Costs and Usage along Processing Path – End-to-End View

COURIER

Operations

CHECK

PROC.

Automation

IT

POSTINGTOTAL

Branch Banking

ATM Banking

Internet Banking

Smart Phone Banking

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

e.g. Virtual Capture

PCDs

RCDs

XXXX

XXXXXXXX

XXXX

XXXX

Product Transaction View

Delivery Channel View, Integrated by Resource Group

Business Performance Management

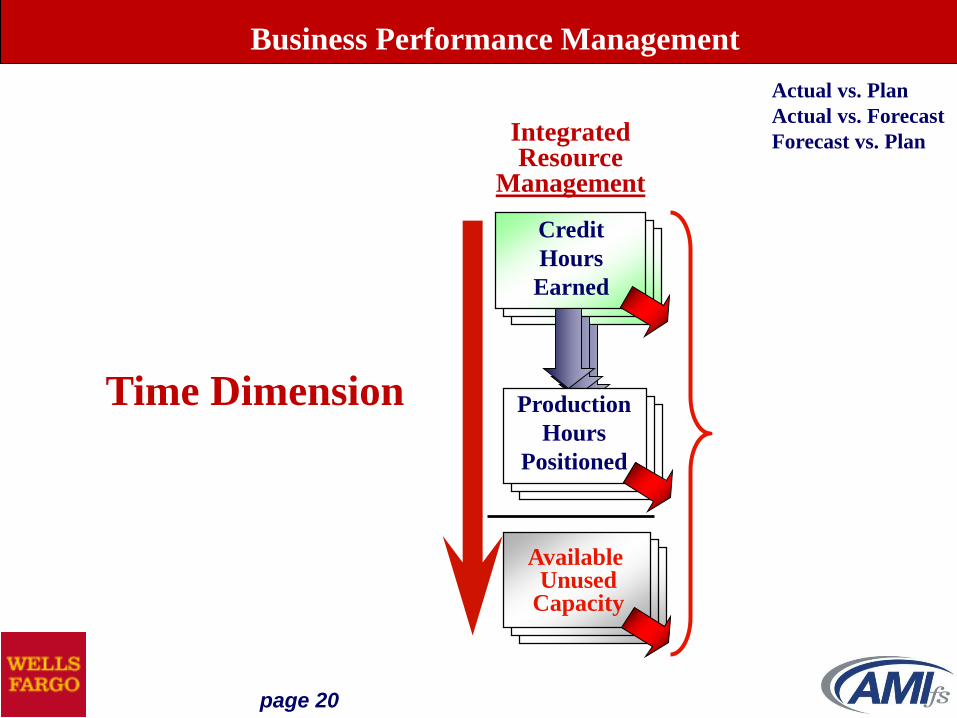

page 20

Credit

Hours

Earned

Production

Hours

Positioned

Available Unused

Capacity

IntegratedResource

Management

Time Dimension

Business Performance Management

Actual vs. Plan

Actual vs. Forecast

Forecast vs. Plan

page 21

Integrated Profitability Measurement

Integration Points

Business Performance Management

page 22

Product

Revenues

LOB

Customer

Distributed

Costs

Product

Margins

Del. Chan.

Distributed

Credits

Bus. Proc.

Proc. Group

Del. Chan.

Expenses

Incurred

Cost

Recovery

Residual

Integrated Profitability Information

Business Performance Management

page 23

• Customer/

Relationship

• Organization/

Location/LOB

• Product

Integration

Integrated Profitability Information

Business Performance Management

page 24

Delivery Channel

Decisions

Customer Access Point

Decisions

ProductOfferings

ServiceOfferings

Access Point Offerings

Access Point Locations

Access Points to Promote

Customer Behaviors

Diversion Strategies

Performance Measurement

Product Pricing

DecisionsProduct Feature

Decisions

Product Offerings

Product Features

Products to Promote

Products to Discourage

Competitive Information

Performance Measurement

Product Pricing

Relationship Pricing

Volume Discounts

Market Prices

Compensation Strategies

Performance Measurement

Delivery Channel Costs

Delivery Channel Usage

Delivery Channel Capacity

Del. Channel Capacity Utl.

Process Improvement

Performance Measurement

Strategic Management

Integrated Profitability Measurement

Analyze Performance Results

Set Performance Targets

Measure Actual Performance

Results vs. Targets

Acknowledge Performance

Improvements

Business Performance Management

page 25

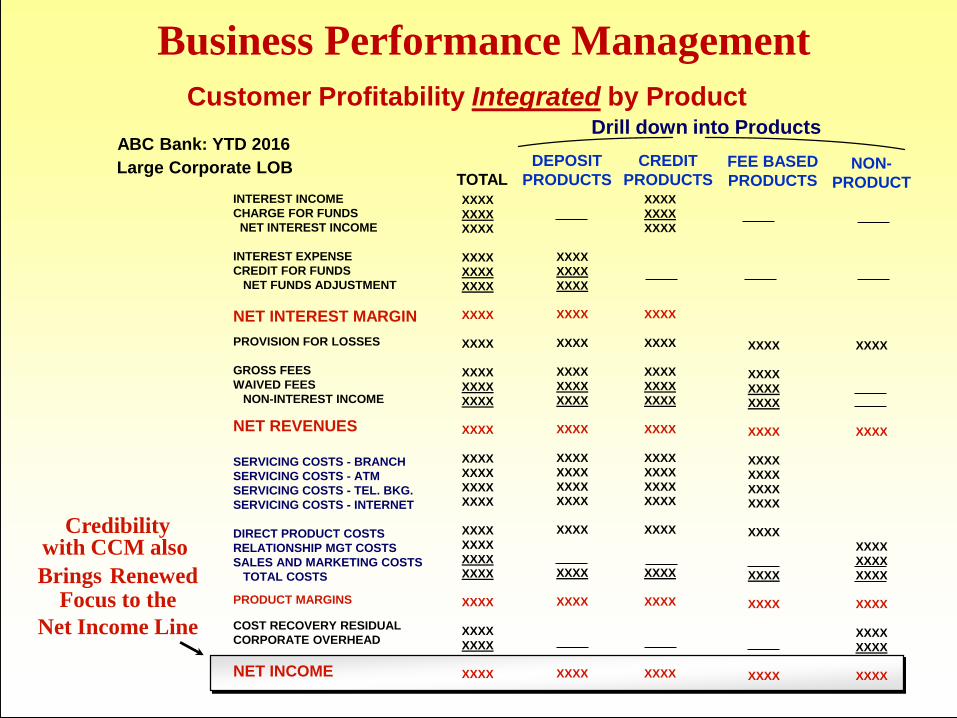

Customer: R. McDonald

ABC Bank: YTD 2016Drill down into Products

Customer Profitability Integrated by Product

TOTAL

DEPOSIT

PRODUCTS

CREDIT

PRODUCTSFEE BASED

PRODUCTS

Cost of Servicing

Customers

INTEREST INCOME

CHARGE FOR FUNDS

NET INTEREST INCOME

INTEREST EXPENSE

CREDIT FOR FUNDS

NET FUNDS ADJUSTMENT

NET INTEREST MARGIN

PROVISION FOR LOSSES

GROSS FEES

WAIVED FEES

NON-INTEREST INCOME

NET REVENUES

SERVICING COSTS - BRANCH

SERVICING COSTS - ATM

SERVICING COSTS - TEL. BKG.

SERVICING COSTS - INTERNET

DIRECT PRODUCT COSTS

RELATIONSHIP MGT COSTS

SALES AND MARKETING COSTS

TOTAL COSTS

PRODUCT MARGINS

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

Business Performance Management

page 26

Integrated Resource Management

Integration Points

Business Performance Management

page 27

Product

Revenues

Location

Customer

Distributed

Costs

Product

Margins

Del. Chan.

Distributed

Credits

Bus. Proc.

Proc. Group

Del. Chan.

Expenses

Incurred

Cost

Recovery

Residual

Integrated Resource Management

Business Performance Management

page 28

• Business Process• Delivery Channel

• Resource Group

Integration

Integrated Resource Management

Business Performance Management

page 29

FinancialManagement

Fixed, Variable, Semi-V Costs

Targeted Unit Costs

Hourly Rate Analyses

Unit Time Analyses

Throughput Analyses

Process Improvements

Performance Measurement

Fixed, Variable, Semi-V Exp.

Targeted Expenses

Targeted Recoveries

Actual Expenses

Actual Recoveries

Expense Residual Analyses

Performance Measurement

ExpenseManagement

CostManagement

ResourceManagement

Targeted Productivity

Actual Productivity

Productivity Improvements

Incentive Compensation

Integrated Productivity Mgmt.

Performance Measurement

Targeted Capacity

Targeted Capacity Utilization

Actual Capacity

Actual Capacity Utilization

Integrated Capacity Mgmt.

Performance Measurement

CapacityManagement

ProductivityManagement

Integrated Resource Management

Strategic Management

Analyze Performance Results

Set Performance Targets

Measure Actual Performance

Results vs. Targets

Acknowledge Performance

Improvements

Business Performance Management

page 30

DIRECT EXPENSES

SALARIES

BENEFITS

OCCUPANCY

EQUIPMENT

SUPPLIES

TOTAL DIRECT EXP.

INDIRECT EXPENSES

HUMAN RESOURCES

TECHNOLOGY

OTHER INDIRECT

TOTAL INDIRECT EXP.

TOTAL EXPENSES

COST RECOVERY RESIDUAL

TOTAL

PLAN

ABC Bank

YTD 2016

Site: Maitland

Center: 123

Integrated Resource Management(One Example of New Management Information Dimension)

Cost

Recovery

Residual

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

PROCESSING CREDITS

PROCESSING RCD #1

PROCESSING RCD #2

PROCESSING RCD #3

PROCESSING REJECT ITEMS

PROCESSING OFFLINE ITEMS

TOTAL PROCESSING CREDITS

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

Cost Recovery

Expenses

Incurred

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

TOTAL

ACTUAL

TOTAL

VARIANCE

Business Performance Management

Resource

Cost

Drivers

page 31

Developing and Administering a

Comprehensive Cost Management (CCM)

Information Database

Business Performance Management

page 32

Product

Revenues

Processing

Credits

Distributed

“Expenses”

Expenses

Incurred

Cost

Recovery

Residual

Expense Allocation View

of P&Ls for Lines of Business

Product

Margins

X

Little Information

Value For the

Expense Center

Managers

Business Performance Management

page 33

INTEREST INCOME

CHARGE FOR FUNDS

NET INTEREST INCOME

INTEREST EXPENSE

CREDIT FOR FUNDS

NET FUNDS ADJUSTMENT

PROVISION FOR LOSSES

GROSS FEES

WAIVED FEES

NON-INTEREST INCOME

ALLOCATED EXPENSES

NET CONTRIBUTION

INCOME TAX

NET EARNINGS

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

Customer: R. McDonald

ABC Bank: YTD 2015

TOTAL

Customer Value Estimate

This P&L is

driven by balances

and

not reflective of

customer transaction

behavior

These are usually

fixed amounts

per account and

not usage based

Could also be

Net Funds

Used/Provided

Business Performance Management

page 34

CostRecovery

Bus. Proc.

Res. Group

Cost

Recovery

Residual

Product

Revenues

LOB

Customer

Distributed

Costs

Product

Margins

Expenses

Incurred

Business Performance Management

page 35

•Create a Shared Vision for the Business Information Value of a CCM

Cost Development and Deployment initiative

•Conduct Cost Information Requirements meetings with Line of Business

Management Partners:

–Service Receivers

–Service Providers

•Establish Management Accounting Policies and Standards for NIE

in Integrated Profitability Measurement and Integrated Resource

Management

•Develop Maintenance and Administration processes for the CCM

Information database

Developing and Administering a CCM Information Database

Business Performance Management

page 36

Expense Classifications &

Cost Distribution Techniques

for

Integrated Profitability Measurement

Business Performance Management

page 37

Responsibility Center Classifications:

•Centralized Expense Centers

•Service Centers

•Local Overhead Centers

•Processing Centers

•Profit CentersProduct Management

Sales & Marketing

Relationship Management

•Corporate Overhead Centers

Business Performance Management

page 38

•Unit Cost Rate “X” Volume

•Fixed Percentage

•Dynamic Percentage

•Fixed Dollar Amount

•Expense to Expense Ratio

•Expense to FTE Ratio

•Expense to Revenue Ratio

•Expense to Equity Ratio

•Rate “X” Customer Classification

CCM Cost Distribution Techniques for Integrated Profitability Measurement

Cost Distribution

Rates & Rules

Business Performance Management

page 39

•Centralized Expense Centers•Service Centers•Local Overhead Centers

•Processing Centers

•Profit Centers

Product Management

Sales & Marketing

Relationship Management

•Corporate Overhead Centers

Product

Revenues

LOB

Customer

Non-Interest Expenses

Distributed

Costs

Product

Margins

Business Performance Management

page 40

•Centralized Expense Centers•Service Centers•Local Overhead Centers

•Processing Centers

•Profit Centers

Product Management

Sales & Marketing

Relationship Management

•Corporate Overhead Centers

Product

Revenues

LOB

Customer

Non-Interest Expenses

Distributed

Costs

CCM Cost Development

& Distribution Rules

for Indirect ExpensesCenter

to Center

Distributions

Business Performance Management

Product

Margins

page 41

Center Classification:

Certain types of institution operating expenses are often managed centrally to obtain

purchasing efficiencies or improved controls (for example: occupancy, utilities, bulk

office supplies, etc.). Typically these expenses are accounted for in separate

responsibility centers to facilitate ease of analysis and reporting from the general

ledger. If these expenses are centrally recorded, material and not distributed in the

GL, consideration should be given to distributing these expenses to the specific centers

that consume the resources.

•Service CentersService Center expenses are for resources positioned to provide internal support

services to other organizational units throughout the institution. Examples include

Human Resources, Procurement Services, certain IT services such as Network and PC

support, etc. Service Centers do not process for bank Customers or bank Products

directly.

•Local Overhead CentersLocal overhead centers are those centers that are responsible for the administration of

a specific group of centers. Examples of local overhead centers include Branch

Administration and Operations Administration.

•Centralized Expense Centers

Business Performance Management

page 42

The Funds Transfer Pricing rate applied to non-earning Fixed Assets

(e.g. Facilities, Leasehold Improvements, Equipment, etc.) is often

called the Cost to Carry that asset. The calculation results are

reported as an Income Statement line item and classified as part of

Indirect Expenses for the period.

Expense Classification:

•Cost to Carry Fixed Assets

Business Performance Management

page 43

HRService Center

ITService Center

UnderwritingProcessing Center

Lending UnitProfit Center

Centerto

Center

Distributions

Distribution Sequencing and Cascading

Business Performance Management

page 44

Direct Expenses

Compensation

Occupancy

Equipment

Supplies

Other

Indirect Expenses

IT Distribution

HR DistributionLOH DistributionCost to Carry FAOther Indirect

Product

Revenues

LOB

Customer

Indirect ExpensesDistributed

Costs

•Processing Centers

•Profit Centers

•Corporate Overhead Centers

for

Non-Interest Expenses

•Centralized Expense Centers

•Service Centers

•Local Overhead Centers

•Cost of Carry Fixed Assets

Business Performance Management

Product

Margins

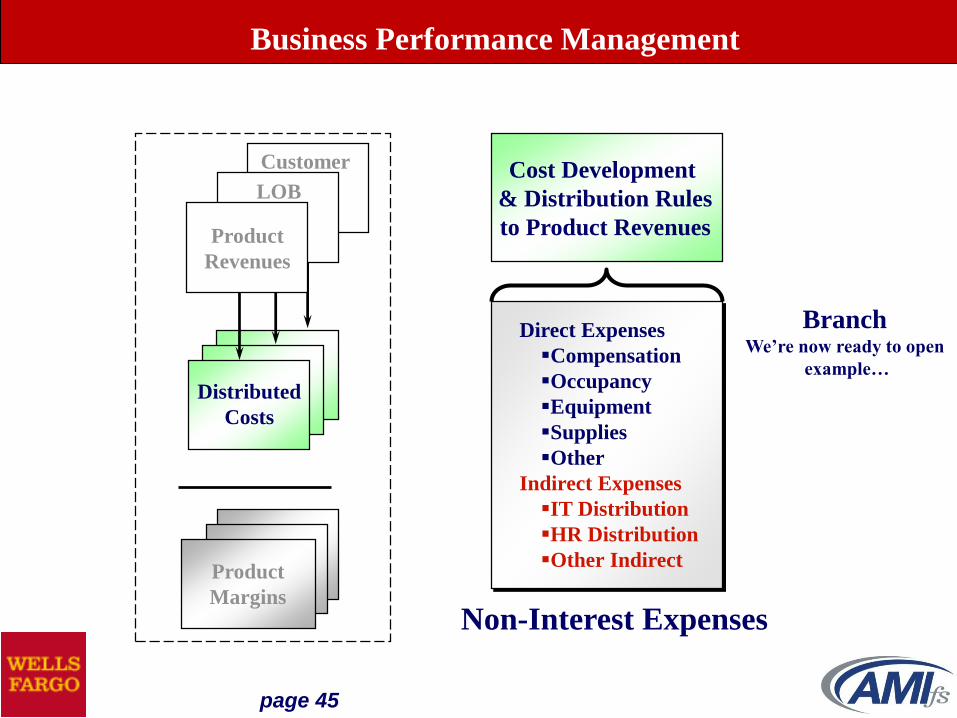

page 45

Direct Expenses

Compensation

Occupancy

Equipment

Supplies

Other

Indirect Expenses

IT Distribution

HR Distribution

Other Indirect

Product

Revenues

LOB

Customer

Non-Interest Expenses

Cost Development

& Distribution Rules

to Product Revenues

Distributed

Costs

BranchWe’re now ready to open

example…

Business Performance Management

Product

Margins

page 46

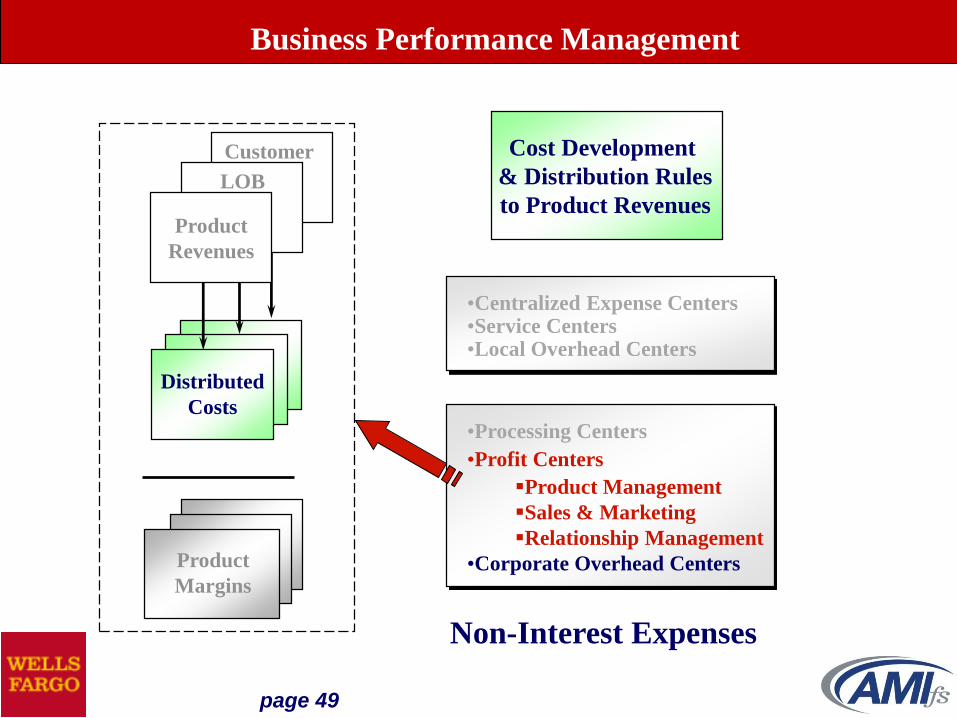

•Centralized Expense Centers•Service Centers•Local Overhead Centers

•Processing Centers

•Profit Centers

Product Management

Sales & Marketing

Relationship Management

•Corporate Overhead Centers

Product

Revenues

LOB

Customer

Non-Interest Expenses

Distributed

Costs

Cost Development

& Distribution Rules

to Product Revenues

Business Performance Management

Product

Margins

page 47

Center Classification:

•Processing Centers

Processing Center Expenses are resources positioned to process

activities for bank Customers and the Products that they purchase.

Examples include Branch Tellers, Bank Operations and certain IT

related functions.

The distribution of Processing Center expenses is typically usage-

driven (rate X volume) and classified as Processing Costs or

Servicing Costs on the P&Ls for Integrated Profitability

measurement.

Business Performance Management

page 48

•Typically Unit Cost Rate “X” Volume

–Capacity-Based Unit Costing

–Allocation-Based Unit Costing

Cost Distribution Techniques:

•Processing Centers

Distribution

Rates & Rules:

Unit Cost Development Techniques

Business Performance Management

page 49

•Centralized Expense Centers•Service Centers•Local Overhead Centers

•Processing Centers

•Profit Centers

Product Management

Sales & Marketing

Relationship Management

•Corporate Overhead Centers

Product

Revenues

LOB

Customer

Non-Interest Expenses

Distributed

Costs

Cost Development

& Distribution Rules

to Product Revenues

Business Performance Management

Product

Margins

page 50

Center Classification:

•Profit CentersProduct Management

Sales & Marketing

Relationship Management

Profit Centers are Responsibility Centers that have a GL booking of

Product Revenues and Product Balances, in addition to their own

Non-Interest Expenses and positioning of resources to perform

activities.

The distribution of Profit Center expenses is typically a re-

classification to the P&L view as Direct Product Costs, Sales &

Marketing Costs and Relationship Management Costs – how much

and why the expenses are incurred.

Business Performance Management

page 51

Product

RevenuesProcessing

Credits

Distributed

Costs

Expenses

Incurred

Cost

Recovery

Residual

Management Accounting View

Product

Margins

Reclassification

of

Expenses Incurred

to

Costs and Purpose ID

Business Performance Management

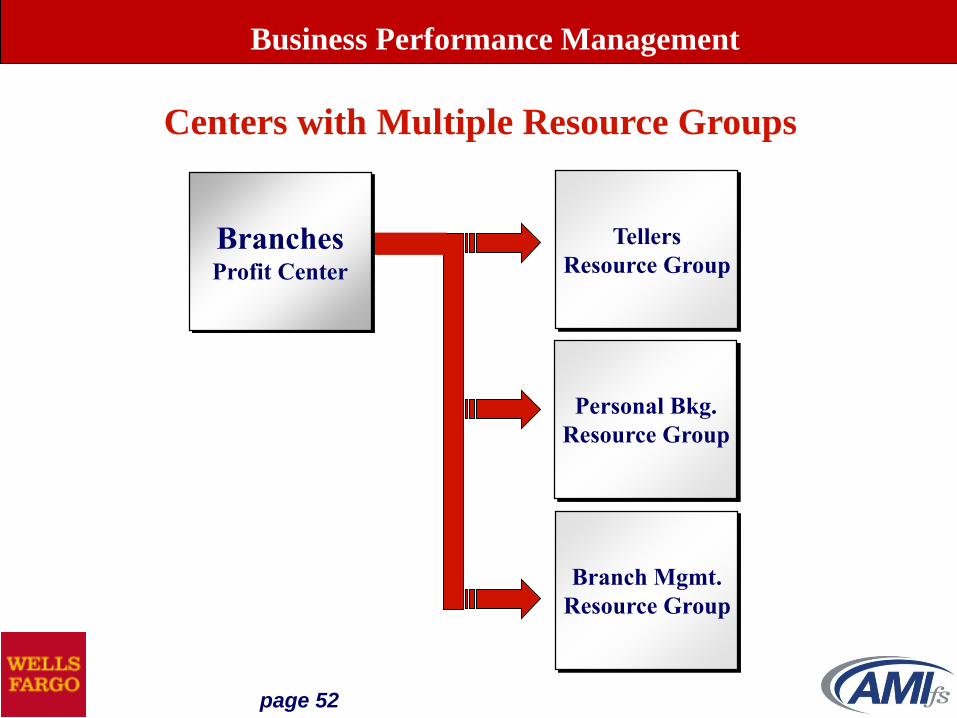

page 52

BranchesProfit Center

Tellers

Resource Group

Personal Bkg.

Resource Group

Branch Mgmt.

Resource Group

Centers with Multiple Resource Groups

Business Performance Management

page 53

•Centralized Expense Centers•Service Centers•Local Overhead Centers

•Processing Centers

•Profit Centers

Product Management

Sales & Marketing

Relationship Management

•Corporate Overhead Centers

Product

Revenues

LOB

Customer

Non-Interest Expenses

Distributed

Costs

Cost Development

& Distribution Rules

to Product Revenues

Business Performance Management

Product

Margins

page 54

Center Classification:

•Corporate Overhead Centers

Corporate Overhead Center expenses are those expenses that cannot be

directly aligned to a specific Product or group of Products, Customer

Segments, or Organizational Units. Therefore, they are aligned to all

Products, Customer Segments and Organizational Units. Examples

include office of the CEO, enterprise level advertising, directors fees,

external reporting, etc.

The distribution technique is typically an expense to expense ratio, but

could also be expense to revenues or equity or some combination

Business Performance Management

page 55

•Centralized Expense Centers•Service Centers•Local Overhead Centers

•Processing Centers

•Profit Centers

Product Management

Sales & Marketing

Relationship Management

•Corporate Overhead Centers

•Cost Recovery Residual

Product

Revenues

LOB

Customer

Non-Interest Expenses

Distributed

Costs

Cost Development

& Distribution Rules

to Product Revenues

Business Performance Management

Product

Margins

page 56

The Cost Recovery Residual is the difference between processing credits

and expenses incurred for the period. This could be the result of a rate/

utilization variance for Capacity-Based cost studies or a volume/spending

variance for Allocation-Based-based studies. The Management

Accounting Policies & Standards will define the management accounting

treatment. One option is to leave the residual with the processing centers.

Another option is to distribute the residual based on the processing charge

distributions. However, this should be to a dedicated line item on the

P&L, along with Corporate Overhead, in order to maintain the

management information value of the contribution margin on the P&L.

Distributions Techniques:

•Cost Recovery Residual– Markup on Processing Charges

Business Performance Management

page 57

Product

Revenues

Cost

Recovery

Distributed

Costs

Expenses

Incurred

Product

Margins

Cost

Recovery

Residual

RecoveryResidual/

COH

Product

Revenues

DistributedCosts

Product

Margins

Net

Income

Expenses

Incurred

Accounting for the Cost Recovery Residual

Business Performance Management

page 58

•Centralized Expense Centers

•Service Centers

•Local Overhead Centers

•Cost to Carry Fixed Assets

•Processing Centers

•Profit Centers

Product Management

Sales & Marketing

Relationship Management

•Corporate Overhead Centers

•Cost Recovery Residual

•Fixed Dollar, Fixed %, Dynamic %

•All

•Expense to Expense or to FTE Ratio

•FTP Rate

•All

•Fixed Dollar, Fixed %, Dynamic %

•Fixed Dollar, Fixed %, Dynamic %

•Rate “X” Customer Classification

•Expense to Expense or to Other Ratio

•Markup on Processing Cost Distributions

Center Classification Distribution Technique Guidelines

Recap

Business Performance Management

page 59

•Centralized Expense Centers•Service Centers

•Local Overhead Centers•Processing Centers

•Profit Centers

Product Management

Sales & Marketing

Relationship Management

•Corporate Overhead Centers

•Cost Recovery Residual

Product

Revenues

LOB

Customer

Non-Interest Expenses

Distributed

Costs

100% of NIE

Business Performance Management

Product

Margins

page 60

Large Corporate LOB

ABC Bank: YTD 2016Drill down into Products

Integrated Profitability Measurement

TOTAL

DEPOSIT

PRODUCTS

CREDIT

PRODUCTSFEE BASED

PRODUCTS

INTEREST INCOME

CHARGE FOR FUNDS

NET INTEREST INCOME

INTEREST EXPENSE

CREDIT FOR FUNDS

NET FUNDS ADJUSTMENT

NET INTEREST MARGIN

PROVISION FOR LOSSES

GROSS FEES

WAIVED FEES

NON-INTEREST INCOME

NET REVENUES

SERVICING COSTS - BRANCH

SERVICING COSTS - ATM

SERVICING COSTS - TEL. BKG.

SERVICING COSTS - INTERNET

DIRECT PRODUCT COSTS

RELATIONSHIP MGT COSTS

SALES AND MARKETING COSTS

TOTAL COSTS

CONTRIBUTION

COST RECOVERY RESIDUAL

CORPORATE OVERHEAD

NET INCOME

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

_____

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

_____

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

_____

_____

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

_____

XXXX

XXXX

XXXX

_____

_____

_____

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

_____

_____

_____

XXXX

_____

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

NON-

PRODUCT

100% Association

of Expenses

to Revenues

in the form of

Various Cost

Distribution

Techniques

page 61

Unit Cost Development Techniques

Capacity-Based Unit Costing

Allocation-Based Unit Costing

Business Performance Management

page 62

A very interesting question asked was about the most important determinant in choosing a

cost distribution methodology. The participants were asked to rank from the following list

in order from 1 to 5 with 1 being the most important:

•Fairness

•User Comprehension

•Cost Effectiveness

•Consistency

•Information Integrity

For the tier 1 and tier 3 institutions, information integrity was the most important. For the

tier 2 institutions, it was fairness [Graph 9]. User comprehension was last across the

board.

Graph 9

50%

42%

45%

36%

38%

40%

42%

44%

46%

48%

50%

Tier 1 - Info Integrity Tier 2 - Fairness Tier 3 - Info Integrity

Most Important Derterminant for Cost Distribution Methodology

Best Practice Costing – Treasury Management

page 63

Loan Products Deposit Products

Product Cost Drivers# of Active Accounts by Loan

Account Type (e.g. Home Equity

Loans, Commercial Loans)

# of Transactions (e.g. Installment

Loan Payments, Line of Credit

Draws)

Product Cost Drivers# of Active Accounts by Deposit

Account Type (e.g. Student

Checking, Commercial DDA)

# of Transactions (e.g. ATM

Withdrawals, Branch Deposits)

Business Performance Management

page 64

Capacity-Based and Allocation-Based Costing:

Unit Cost Development Techniques

•Provide stable and consistent Product and Resource

Cost Driver rates from period to period

•Provide for an end-to-end view of unit costs with

Study Group contributions along a Processing Path

•Provide for Integrated views of the Cost Information:

–by Product

–by Customer

–by Location

•Provide for Integrated views of the Cost Information:

–by Resource Group

–by Delivery Channel

–by Business Process

Business Performance Management

page 65

Support Costing Information Analyses, such as:

•Pricing Analyses

•Productivity Analyses

•Capacity Analyses

•Fixed vs. Variable and Semi-Variable Analyses

•Breakeven Analyses

•Location Analyses

•Delivery Channel Alternatives

•Marketing Strategies

The management information value of both the Capacity-Based

and Allocation-Based cost development approaches:

Business Performance Management

page 66

Capacity-Based Approach:

Build unit rates with a unit time and an hourly rate calculation

Allocation-Based Approach:

Full absorption expense pools divided by relevant volumes

- unit rate calculation

GL line items distributions to expense pools:

Management Estimate/Survey – Fixed %/Fixed $

Volume Based – Dynamic %

Relative Value Technique – Dynamic %

Two Unit Cost Development Techniques

Business Performance Management

page 67

Financial Data

Resource Production HoursVolume Statistical Data

Business

Performance

Management

Capacity-Based Approach

Business Performance Management

page 68

Pooling:

Expenses Statistical Volumes = Pooled Expense per Item

Time Statistical Volumes = Throughput Rate per Unit

Expenses Available Production Hours =

Resource Group Hourly Rate

Measure: Activity or Transaction “Unit Times”

Build: Measured “Unit Time” X Resource Group

“Hourly Rate” = Capacity-Based Unit Cost

Capacity-Based Costing

Business Performance Management

page 69

Capacity-Based Costing

Example:

Total Expenses = $500,000

Total FTE = 7

Total Production Hours = 12,768 (7 * 152 * 12)

Hourly Rate = $39.16 ($500,000/12,768)

RCD #1 takes 1 minute to process

RCD #2 takes 3 minutes to process

Unit Cost for RCD #1 = 1/60 * 39.16 = $0.6527

Unit Cost for RCD #2 = 3/60 * 39.16 = $1.9580

Business Performance Management

page 70

Capacity-Based Cost Study Execution

June 2016

Credit

Hours

Monthly

Volumes

Decimal

Hours

Calculation Fixed

Semi-

Variable Variable

Total Unit

Costs

Cost Recovery

Calculation

RCD 1 101.93 30,010 0.003397 0.0738$ 0.0777$ 0.0467$ 0.1982$ 5,947.52$

RCD 2 387.37 33,442 0.011583 0.2518$ 0.2649$ 0.1592$ 0.6759$ 22,602.33$

RCD 3 7.38 510 0.014472 0.3146$ 0.3309$ 0.1989$ 0.8444$ 430.64$

RCD 4 49.69 13,879 0.003580 0.0778$ 0.0819$ 0.0492$ 0.2089$ 2,899.41$

RCD 5 609.41 3,697,281 0.000165 0.0036$ 0.0038$ 0.0023$ 0.0096$ 35,557.50$

RCD 6 33.89 410,809 0.000083 0.0018$ 0.0019$ 0.0011$ 0.0048$ 1,977.54$

RCD 8 292.73 79,117 0.003700 0.0804$ 0.0846$ 0.0509$ 0.2159$ 17,080.27$

RCD 9 13.53 2,697 0.005017 0.1090$ 0.1147$ 0.0690$ 0.2927$ 789.42$

RCD 10 34.75 1,298 0.026774 0.5820$ 0.6122$ 0.3680$ 1.5622$ 2,027.71$

RCD 11 74.77 672,906 0.000111 0.0024$ 0.0025$ 0.0015$ 0.0065$ 4,362.49$

RCD 13 5.24 191 0.027450 0.5967$ 0.6277$ 0.3773$ 1.6016$ 305.91$

RCD 14 1.00 NA NA 21.74$ 22.87$ 13.75$ 58.35$ 58.35$

RCD 15 264.00 4,319 0.061125 1.3286$ 1.3976$ 0.8402$ 3.5665$ 15,403.61$

1,875.70 Total Cost Recovery 109,442.71$

Total Hours 2,061.56 Hourly Rate 58.35$ Total Expenses 120,286.99$

90.98% 90.98%

Capacity Utilization % = Total Cost Recovery Ratio

Capcity-Based Unit Costs

Business Performance Management

page 71

RCD/PCDAccount Classifications Total 1 2 3 4

Direct ExpensesSalaries & BenefitsOccupancyEquipmentSuppliesOther

Indirect ExpensesIT DistributionHR DistributionOther Indirect

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

X

Allocation-Based Approach

Expense Pooling: Fixed %, Dynamic %

Business Performance Management

page 72

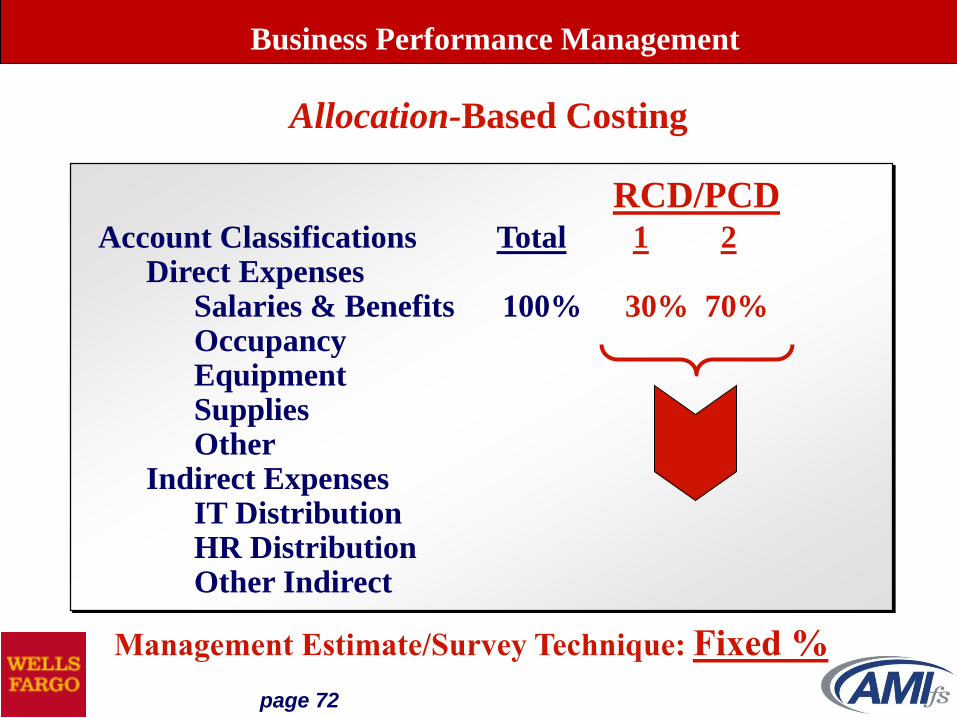

RCD/PCDAccount Classifications Total 1 2

Direct ExpensesSalaries & Benefits 100% 30% 70% OccupancyEquipmentSuppliesOther

Indirect ExpensesIT DistributionHR DistributionOther Indirect

Management Estimate/Survey Technique: Fixed %

Allocation-Based Costing

Business Performance Management

page 73

Example:

Total Expenses = $500,000

RCD #1 Volume = 100,000

RCD #2 Volume = 300,000

Total Volume = 400,000

Distribution % for RCD #1 = 25% (100,000/400,000)

Distribution % for RCD #2 = 75% (300,000/400,000)

Unit Cost for RCD #1 = 500,000*25%/100,000 = $1.25

Unit Cost for RCD #2 = 500,000*75%/300,000 = $1.25

Allocation-Based Costing

Volume Based Distribution Technique: Dynamic%

Business Performance Management

page 74

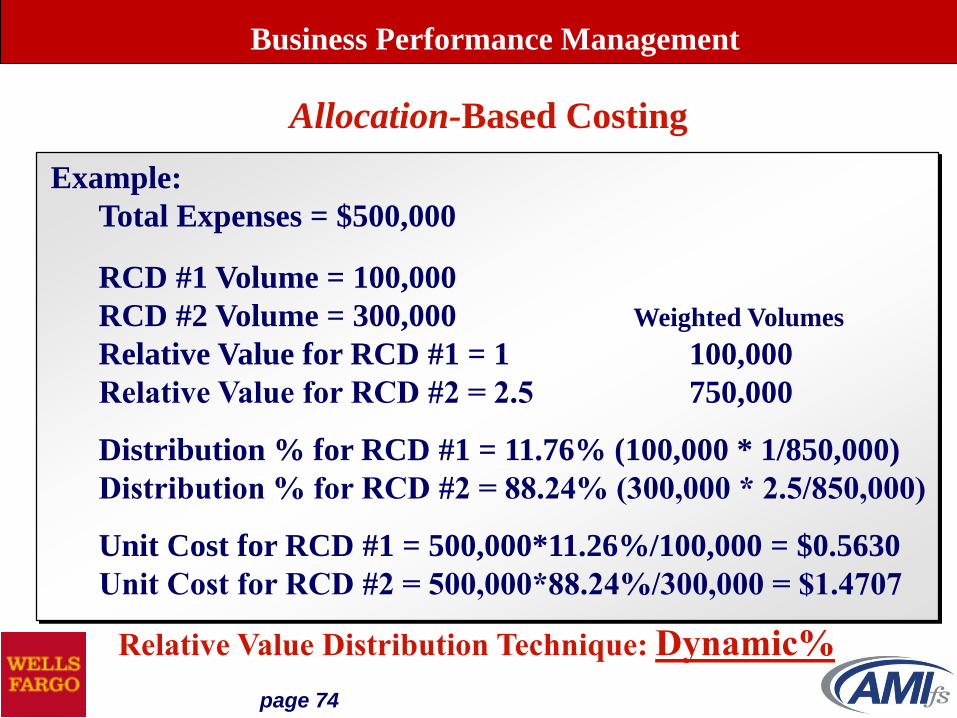

Example:

Total Expenses = $500,000

RCD #1 Volume = 100,000

RCD #2 Volume = 300,000 Weighted Volumes

Relative Value for RCD #1 = 1 100,000

Relative Value for RCD #2 = 2.5 750,000

Distribution % for RCD #1 = 11.76% (100,000 * 1/850,000)

Distribution % for RCD #2 = 88.24% (300,000 * 2.5/850,000)

Unit Cost for RCD #1 = 500,000*11.26%/100,000 = $0.5630

Unit Cost for RCD #2 = 500,000*88.24%/300,000 = $1.4707

Allocation-Based Costing

Relative Value Distribution Technique: Dynamic%

Business Performance Management

page 75

Allocation-Based Cost Study Execution2016 Forecast

Total RCD 1 RCD 2 TOTAL

Total Personnel 866,992 Survey 216,748 650,244 866,992$

Total Equipment 1,376,579 Direct Association 166,667$ 166,667$

- Weighting Factor 126,433$ 1,083,480$ 1,209,912$

Total Occupancy 170,892 Volume 14,591$ 156,301$ 170,892$ -

IT SUPPORT EXPENSE 2,630,302 Volume 224,582$ 2,405,720$ 2,630,302$

PRINTING & OFFICE EXPENSE 97,843 Volume 8,354$ 89,489$ 97,843$

TRAVEL & ENTERTAINMENT 40,404 Weighting Factor 4,222$ 36,182$ 40,404$

MISC PROFESSIONAL FEES 850,000 Volume 72,575$ 777,425$ 850,000$

HIRING EXPENSE 800 Weighting Factor 84$ 716$ 800$

FREIGHT & EXPRESS EXPENSE 6,600 Volume 564 6,036 6,600$

OPERATING LOSSES/RECOV 400,000 Volume 34,153$ 365,847$ 400,000$

TOTAL IT INTERNAL 1,105,201 Volume 94,365$ 1,010,837$ 1,105,201$

Total Other Operating 5,131,150 438,898 4,692,252 5,131,150

Total Direct Expenses 7,545,613 963,336 6,582,277 7,545,613

Total Indirect Expenses 622,783 Direct Controllable 79,510 543,273 622,783

Total Expenses 8,168,396 1,042,846 7,125,550 8,168,396

Total Unit Costs 0.0272$ 0.0174$

RCD 1 @ 1.25 RCD 2 @ 1 Total

Weighting Factor Distribution 47,903,170 410,511,402 458,414,572.2

10.45% 89.55% 100.00%

RCD 1 RCD 2 Total

Volume Base Distribution 38,322,536 410,511,402 448,833,938.2

8.54% 91.46% 100.00%

Business Performance Management

page 76

Fixed, Semi-Variable

and

Variable Classifications

Business Performance Management

page 77

A calculated contribution margin is the difference between price and the variable cost. It

represents how much is left to contribute to fixed costs and profits after covering variable

costs only. The number of institutions reporting contribution margins was 59% for the tier

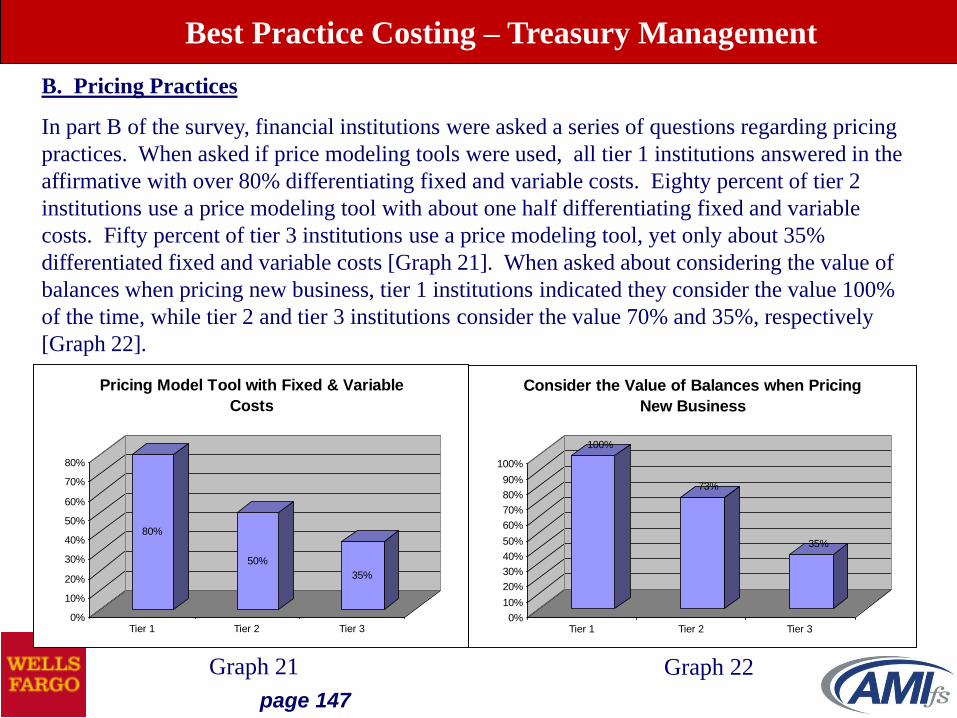

1 institutions, 27% for tier 2 and 25% for tier 3 [Graph 15]. Less than 1/3 of the

respondents also have a semi-variable component, which is designed to account for

personnel related expenses. Of those respondents, 1/3 took associated semi-variable with

the variable classification for the contribution margin calculation and 2/3 split it into both

variable and fixed [Graph 16].

Semi-Variable Cost Treatment

SV to V

9%

SV to F

0%

SV to V and F

18%

No SV

73%

Graph 15 Graph 16

59%

27%25%

0%

10%

20%

30%

40%

50%

60%

Tier 1 Tier 2 Tier 3

% of Respondents who Report Contribution Margin

Best Practice Costing – Treasury Management

page 78

Fixed/Variable/Semi-Variable Analysis

Volumes

Expenses

Run

Rise

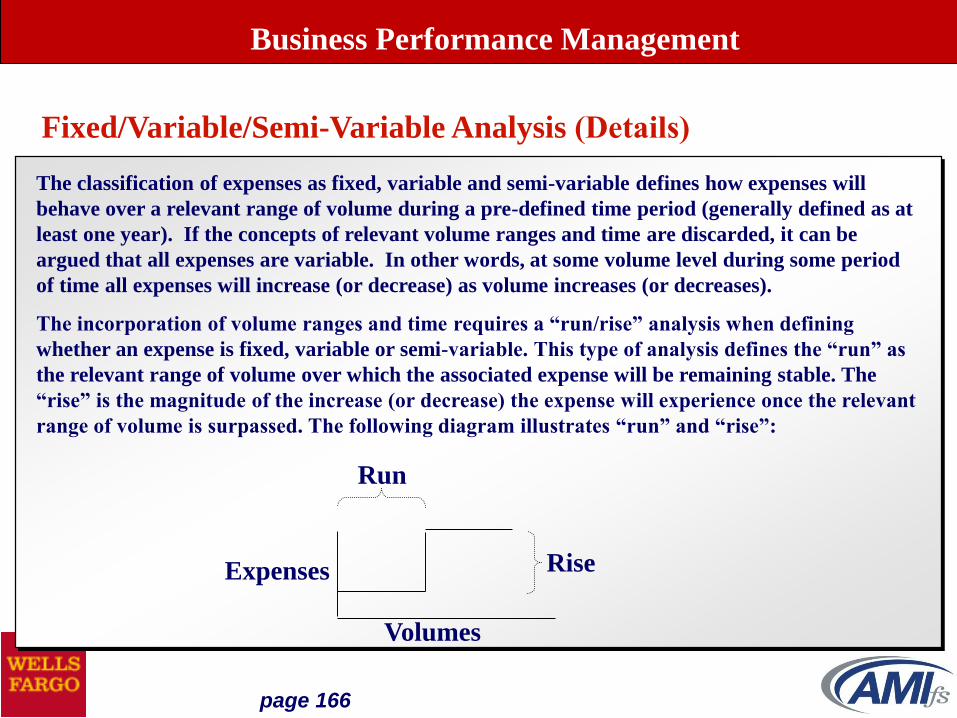

The classification of expenses as fixed, variable and semi-variable defines

how expenses will behave over a relevant range of volume during a pre-

defined time period (typically defined as at least one year). The

incorporation of volume ranges and time requires a “run/rise” analysis

when defining whether an expense is fixed, variable or semi-variable.

This type of analysis defines the “run” as the relevant range of volume

over which the associated expense will be remaining stable. The “rise” is

the magnitude of the increase (or decrease) the expenses will experience

once the relevant range of volume is surpassed. The following diagram

illustrates “run” and “rise”:

Business Performance Management

page 79

Fixed/Variable/Semi-Variable Analysis

Volumes

Expenses

Yr 2Yr 1

Volumes

Expenses

Yr 2Yr 1

Volumes

Expenses

Yr 2Yr 1

Fixed Variable

Semi-Variable

Business Performance Management

page 80

Account Classifications: Fixed Variable Semi-VDirect Expenses

PersonnelOccupancyEquipmentSuppliesPostageOther

Indirect ExpensesIT DistributionHR DistributionCost to Carry FAOther Indirect

X

XX

X

X

X

X

X

X

Fixed/Variable/Semi-Variable Analysis

X

Business Performance Management

page 81

•Centralized Expense and Service Center Distributions;

•Local Overhead Distributions;

•Cost to Carry Fixed Assets;

•Fixed/Variable/Semi-Variable Components;

-Applied to Hourly Rates for the Capacity-Based

unit cost development approach.

-Applied directly to Expense Pools for Allocation-Based

unit cost development approach.

Unit Cost Development Techniques

Business Performance Management

page 82

Treasury Management Cost Structure at Wells Fargo

Business Performance Management

TM Variable costs are charged to the LOBs using a consumption based

rate X volume methodology at the Account Analysis billing element

level.

TM Direct Fixed costs are associated to TM Products and are charged

to the LOBs using a fixed $ methodology (plan/12) for services at a TM

Product level such as Cash Vault Occupancy to the Cash Services

Product.

TM Indirect Fixed expenses are incurred on behalf of all TM (not

associated to TM Products) and are charged to the LOBs using a fixed

$ methodology (plan/12) for services such as TM Marketing and TM

Risk Management.

TM Sales costs are charged to LOBs based geographic assignments or

industry specific support using a fixed $ methodology (plan/12).

page 83

CCM unit cost development is a structured project approach

designed to streamline the costing effort, while maximizing the

information value

StudyPreparation

StudyExecution

StudyApproval

Study Information

Rollout

CCM Unit Cost Development Techniques

Business Performance Management

page 84

StudyPreparation

•Leverage and optimize the skill sets of the cost analyst team

•Analyze and classify processing centers

•Establish study group IDs

•Determine study period

•Communicate expectations with study group management

•Look for quick management information wins

Cost Study Process

CCM Unit Cost Development Techniques

Business Performance Management

page 85

StudyExecution

Activity

Definition

Activity Time

Development

Expense

Analysis

Calculate

Component

Rates

Define

Activities

Develop

Activity

Unit

Times

Develop

Resource

Hourly

Rate(s)

Calculate

Capacity-

Based

Costs

Statistical

Volume

Analysis

RCD &

PCD

Unit Rates

Capacity-Based Cost

Study Execution

Processes

CCM Unit Cost Development Techniques

Business Performance Management

page 86

StudyExecution

Activity

Definition

Distribution

Techniques

To Cost Pools

Expense &

RCD Analysis

Calculate

Unit

Rates

Define

Activities

Determine

GL Line

ItemDistribution

Bases

ExecuteDistributions

to

Expense

Pools

Calculate

Fully

Absorbed

Costs

Statistical

Volume

Analysis

RCD &

PCD

Unit Rates

CCM Unit Cost Development Techniques

Allocation-Based Cost

Study Execution

Processes

Business Performance Management

page 87

StudyApproval

•Communicate study period results with Study Group management

•Obtain approval (sign-off) for results

•Reinforce the role of the rates representing the Study Group and

Study Period in Integrated Profitability

• Reinforce the role of the Study Period results as a new balance type

for Integrated Resource Management reporting

Cost Study Process

CCM Unit Cost Development Techniques

Business Performance Management

page 88

Study Information

Rollout

•Use the cost information database to support ongoing business

ad hoc analyses, such as pricing, capacity, fixed vs. variable, etc.

•Deploy the Product Cost Driver (PCD) rates and business logic in

Integrated Profitability measurement.

•Deploy the Resource Cost Driver (RCD) rates and business logic in

Integrated Resource Management.

Cost Study Process

CCM Unit Cost Development Techniques

Business Performance Management

page 89

Comprehensive Cost Management

Case Study

Development - Capacity-Based Methodology

Vs.

Allocation-Based

If you can do cost accounting for financial institutions,

you can do it for ANY industry…

Business Performance Management

page 90

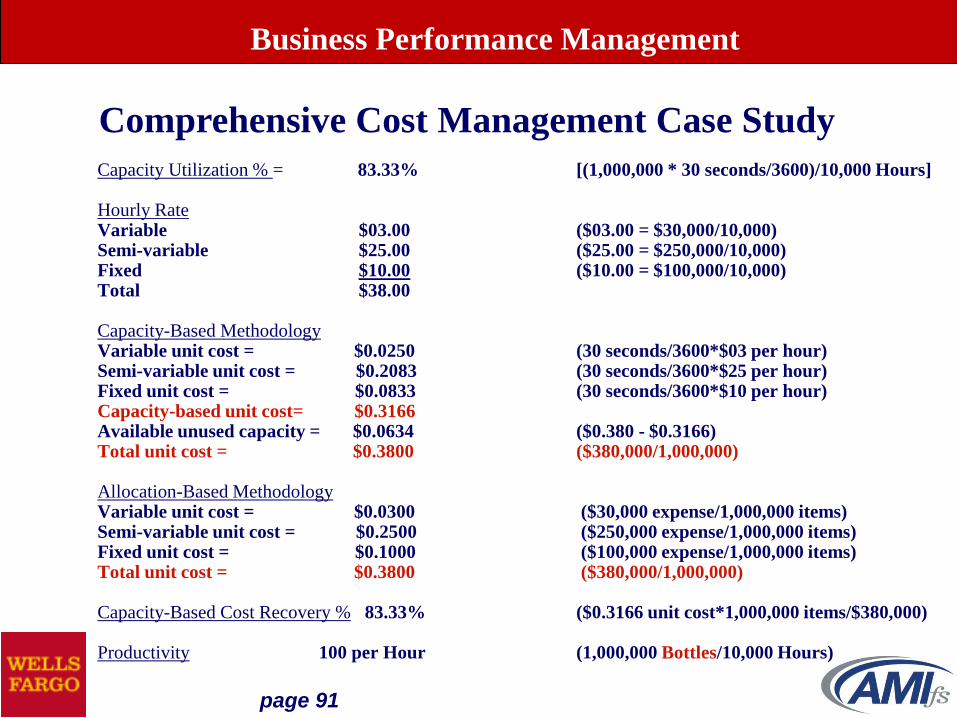

Study Period Data Assumptions

Personnel Expense $250,000

Equip. Depreciation Expense $ 35,000

Occupancy Expense $ 65,000

Raw Materials Expense $ 30,000

Total Expenses $380,000

Calculate the following:

Capacity Utilization %

Hourly Rates (Fixed, Semi-Variable, Variable)

Capacity-Based unit cost

Allocation-Based Fully Absorbed unit cost

Capacity-Based Cost Recovery %

Productivity

Hours worked 10,000

Bottles processed 1,000,000

Unit time per Bottle 30 seconds

Comprehensive Cost Management Case Study

Business Performance Management

page 91

Capacity Utilization % = 83.33% [(1,000,000 * 30 seconds/3600)/10,000 Hours]

Hourly RateVariable $03.00 ($03.00 = $30,000/10,000)Semi-variable $25.00 ($25.00 = $250,000/10,000)Fixed $10.00 ($10.00 = $100,000/10,000)Total $38.00

Capacity-Based MethodologyVariable unit cost = $0.0250 (30 seconds/3600*$03 per hour)Semi-variable unit cost = $0.2083 (30 seconds/3600*$25 per hour)Fixed unit cost = $0.0833 (30 seconds/3600*$10 per hour)Capacity-based unit cost= $0.3166Available unused capacity = $0.0634 ($0.380 - $0.3166)Total unit cost = $0.3800 ($380,000/1,000,000)

Allocation-Based Methodology Variable unit cost = $0.0300 ($30,000 expense/1,000,000 items)Semi-variable unit cost = $0.2500 ($250,000 expense/1,000,000 items)Fixed unit cost = $0.1000 ($100,000 expense/1,000,000 items)Total unit cost = $0.3800 ($380,000/1,000,000)

Capacity-Based Cost Recovery % 83.33% ($0.3166 unit cost*1,000,000 items/$380,000)

Productivity 100 per Hour (1,000,000 Bottles/10,000 Hours)

Comprehensive Cost Management Case Study

Business Performance Management

page 92

Cost Deployment

for

Integrated Resource Management

Business Performance Management

page 93

Product

Revenues

LOB

Customer

Distributed

Costs

Del. Chan.

Distributed

Credits

Bus. Proc.

Proc. Group

Del. Chan.

Expenses

Incurred

Cost

Recovery

Residual

CCM Deployment for Integrated Resource Management

Business Performance Management

Product

Margins

page 94

•NIE Financial Data

•Statistical Volume Data

•FTE (Production Hours) Data

Linking involves the Integration of:

Business Performance Management

page 95

by Balance Type to generate New Performance Measurement

criteria, including:

•Statistical Volumes in Budgeting & Forecasting

•The dimension of Production Time and FTEs in

Integrated Costing

•Comprehensive Variance Analyses – Actual

Performance results vs. Performance Targets

Business Performance Management

page 96

•Actual

•Budget

•Forecast (Multiple Forecasts)

•Study Period (if Applicable)

Balance Type Comparisons

Financial Data

Business Performance Management

page 97

Plaza 48 Hour Processing

0

2

4

6

8

10

12

14

16

0:00

2:00

4:00

6:00

8:00

10:0

0

12:0

0

14:0

0

16:0

0

18:0

0

20:0

0

22:0

00:

002:

004:

006:

008:

00

10:0

0

12:0

0

14:0

0

16:0

0

18:0

0

20:0

0

22:0

0

Time

So

rters

@54,0

42 ite

m p

er/

ho

ur

IBFS

Capture

Available Unused capacity versus Excess capacity

- no Available Unused capacity at 2:00, therefore no Excess capacity overall

Window Capacity By Time of Day

Business Performance Management

Excess Capacity

Available Unused

page 98

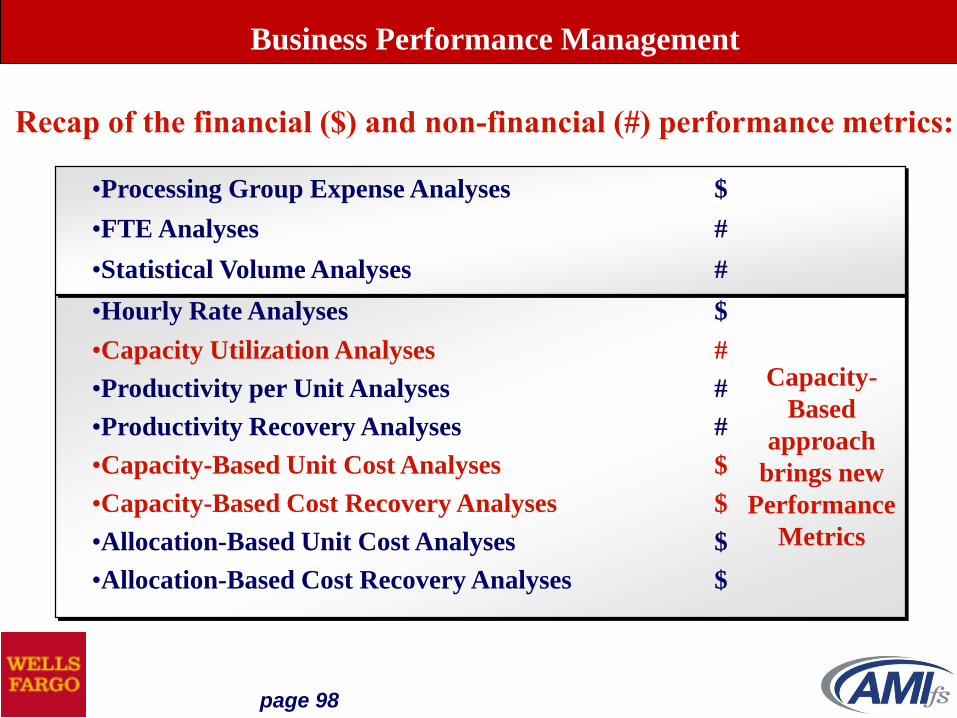

•Processing Group Expense Analyses $

•FTE Analyses #

•Statistical Volume Analyses #

•Hourly Rate Analyses $

•Capacity Utilization Analyses #

•Productivity per Unit Analyses #

•Productivity Recovery Analyses #

•Capacity-Based Unit Cost Analyses $

•Capacity-Based Cost Recovery Analyses $

•Allocation-Based Unit Cost Analyses $

•Allocation-Based Cost Recovery Analyses $

Recap of the financial ($) and non-financial (#) performance metrics:

Capacity-

Based

approach

brings new

Performance

Metrics

Business Performance Management

page 99

•Error Rates

•Reject Rates

•Turnaround Time

•Response Time

•Customer Satisfaction

•Employee Tenure

•Employee Turnover

In addition, the analyses should align certain quality

indicators and other relevant information against the

performance metrics to look for patterns and/or trends

against the performance results. Examples include:

Business Performance Management

page 100

Performance Metrics can also be presented across

multiple balance types. Comprehensive Variance Analyses

across balance type comparisons include:

•Actual vs. Budget

•Actual vs. Forecast (Multiple Forecasts)

•Budget vs. Forecast

•Actual vs. Study Period (if Different from

Budget/Forecast)

Business Performance Management

page 101

Analysis

Module

Analysis Outputs

Monthly Performance Metrics

• Monthly Results by Balance Type

• Balance Type Comparatives

Comprehensive Variance Analyses

• Performance Variance Calculations

• Variance Explanations

Analysis Inputs

Costing Information Database:•Unit Costs by Study Group•Unit Times by Study Group•HR FTE/Production Hours by Study Group •Study Period Hourly Rates•Study Period Performance Ratios

Monthly Production Values:

•RCD Volumes by Proc. Center

•PCD Volumes

•GL $ by Processing Center

•FTE/Hours by Processing Center•Quality Indicators by Processing Center

Monthly Analysis Balance Types:

•Budget by Period

•Forecast by Period

•Actual by Period

•Study Period Results

CCM Deployment for Integrated Resource Management

Business Performance Management

page 102

Treasury Operations

January February March April May June

$ 365,060 $ 334,842 $ 353,857 $ 358,986 $ 369,217 $ 377,349

$ 366,200 $ 366,200 $ 374,200 $ 366,200 $ 366,200 $ 366,200

$ 375,858 $ 375,858 $ 375,858 $ 375,858 $ 375,858 $ 375,858

Strategic Business Analysis

January February March April May June

36.91 34.95 39.28 35.00 37.00 40.00

40.00 40.00 40.00 40.00 40.00 40.00

37.50 37.50 37.50 37.50 37.50 37.50

Treasury Operations

1 2 3 4 5 6

Actual

Study Period$310,000

$320,000

$330,000

$340,000

$350,000

$360,000

$370,000

$380,000

Month

Expense Analysis

Actual

Forecast

Study Period

1 2 3 4 5 6

Actual

Study Period32

33

34

35

36

37

38

39

40

Month

FTE Analysis

Actual

Forecast

Study Period

Business Performance Management

page 103

January February March April May June

$ 65.07 $ 63.03 $ 59.27 $ 67.48 $ 65.65 $ 62.06

$ 60.23 $ 60.23 $ 61.55 $ 60.23 $ 60.23 $ 60.23

$ 65.94 $ 65.94 $ 65.94 $ 65.94 $ 65.94 $ 65.94

Treasury Operations

Strategic Business Analysis

January February March April May June

95.22% 96.01% 87.73% 102.15% 92.54% 94.30%

85.54% 85.54% 85.54% 85.54% 85.54% 85.54%

90.00% 90.00% 90.00% 90.00% 90.00% 90.00%

Treasury Operations

1 2 3 4 5 6

Actual

Study Period54

56

58

60

62

64

66

68

Month

Hourly Rate Analysis

Actual

Forecast

Study Period

1 2 3 4 5 6

Actual

Study Period75%

80%

85%

90%

95%

100%

105%

Month

Capacity Utilization Analysis

Actual

Forecast

Study Period

Business Performance Management

page 104

Analysis

Module

Analysis Outputs

Monthly Performance Metrics

• Monthly Results by Balance Type

• Balance Type Comparatives

Comprehensive Variance Analyses

• Performance Variance Calculations

• Variance Explanations

Analysis Inputs

Costing Information Database:•Unit Costs by Study Group•Unit Times by Study Group•HR FTE/Production Hours by Study Group •Study Period Hourly Rates•Study Period Performance Ratios

Monthly Production Values:

•RCD Volumes by Proc. Center

•PCD Volumes

•GL $ by Processing Center

•FTE/Hours by Processing Center•Quality Indicators by Processing Center

Monthly Analysis Balance Types:

•Budget by Period

•Forecast by Period

•Actual by Period

•Study Period Results

CCM Deployment for Integrated Resource Management

Business Performance Management

page 105

Processing

Credits

Expenses

Incurred

CostRecoveryResidual

IntegratedResource

Management

$ Dimension

Residual

Analysis

By Ledger Type:

•Actual

•Budget

•Forecast•Multiple Forecast

Business Performance Management

page 106

When using standard or published costs for cost allocations, a residual is created each

period. As a result, the cost pools will either be over-allocated or under-allocated. For the

tier 1 financial institutions, 67% create a residual when running cost allocations. For tier 2

institutions responding, 50% create a residual and for tier 3, less than 30% [Graph 5].

When asked whether calculated residuals are distributed, two thirds of the tier 1

institutions said yes, 57% of the tier 2 institutions and half of the tier 3 institutions said yes

[Graph 6].

Graph 5 Graph 6

67%

50%

32%

0%

10%

20%

30%

40%

50%

60%

70%

Tier 1 Tier 2 Tier 3

% of Respondents Creating Residuals

67%

57%

50%

0%

10%

20%

30%

40%

50%

60%

70%

Tier 1 Tier 2 Tier 3

% of Respondents Allocating Residuals

Best Practice Costing – Treasury Management

page 107

A follow up question for those institutions that allocate the residual each period was to

what level, including:

•Line of Business (LOB)

•Product

•Customer

•Customer Account

Across all three tiers, 13% allocate to LOB only, 21% to Product only and nearly 2/3 to

both LOB and product. None of the respondents allocate residuals to a customer or

customer account level. [Graph 8].

Graph 8

Residual Distributions

LOB

13%

Product

21%

LOB & Product

66%

Customer

0%

Best Practice Costing – Treasury Management

page 108

Actual

Expenses

$135,425

Actual

Expenses

Forecast

Expenses

Forecast

Volumes

Forecast

Alloc-Based Unit Cost

“X”

Actual Volumes

Alloc.-Based

Cost Recovery

Residual

$144

Volume

Variance

$3,739

Spending

Variance

($3,595)

Actual

Volumes

Example: Allocation-Based Cost Recovery Analysis

$135,569

Volume Variance

“X”

Forecast

Alloc-Based Unit Cost

Forecast Expenses

Less

Actual Expenses

Business Performance Management

page 109

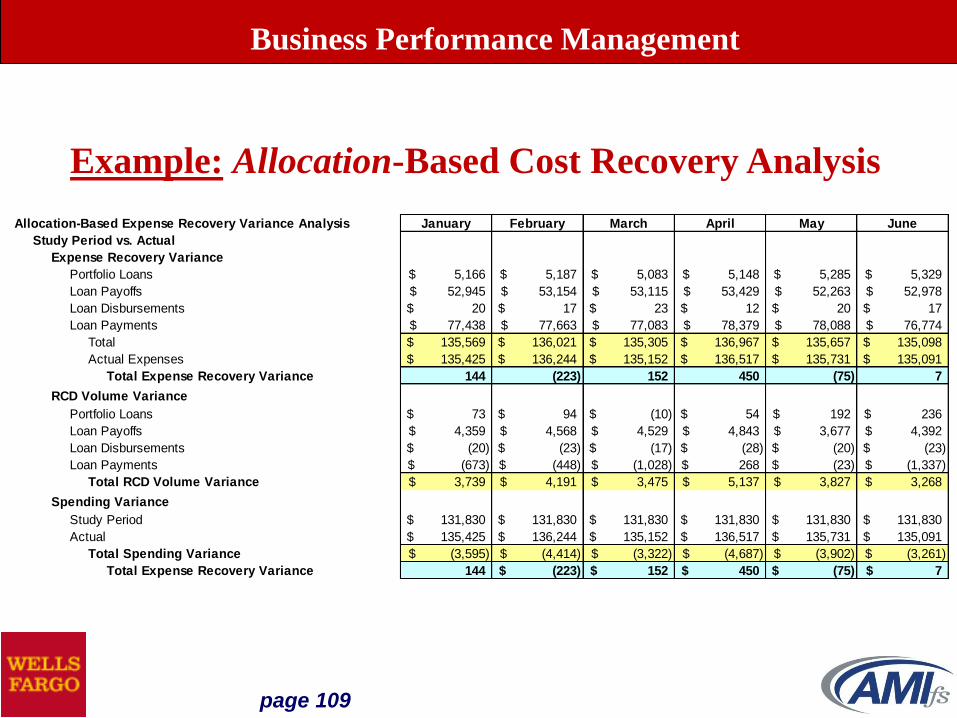

Business Performance Management

Example: Allocation-Based Cost Recovery Analysis

Allocation-Based Expense Recovery Variance Analysis January February March April May June

Study Period vs. Actual

Expense Recovery Variance

Portfolio Loans 5,166$ 5,187$ 5,083$ 5,148$ 5,285$ 5,329$

Loan Payoffs 52,945$ 53,154$ 53,115$ 53,429$ 52,263$ 52,978$

Loan Disbursements 20$ 17$ 23$ 12$ 20$ 17$

Loan Payments 77,438$ 77,663$ 77,083$ 78,379$ 78,088$ 76,774$

Total 135,569$ 136,021$ 135,305$ 136,967$ 135,657$ 135,098$

Actual Expenses 135,425$ 136,244$ 135,152$ 136,517$ 135,731$ 135,091$

Total Expense Recovery Variance 144 (223) 152 450 (75) 7

RCD Volume Variance

Portfolio Loans 73$ 94$ (10)$ 54$ 192$ 236$

Loan Payoffs 4,359$ 4,568$ 4,529$ 4,843$ 3,677$ 4,392$

Loan Disbursements (20)$ (23)$ (17)$ (28)$ (20)$ (23)$

Loan Payments (673)$ (448)$ (1,028)$ 268$ (23)$ (1,337)$

Total RCD Volume Variance 3,739$ 4,191$ 3,475$ 5,137$ 3,827$ 3,268$

Spending Variance

Study Period 131,830$ 131,830$ 131,830$ 131,830$ 131,830$ 131,830$

Actual 135,425$ 136,244$ 135,152$ 136,517$ 135,731$ 135,091$

Total Spending Variance (3,595)$ (4,414)$ (3,322)$ (4,687)$ (3,902)$ (3,261)$

Total Expense Recovery Variance 144 (223)$ 152$ 450$ (75)$ 7$

page 110

Business Performance Management

Example: Allocation-Based Cost Recovery Analysis

Allocation-Based Expense Recovery Variance Analysis January February March April May June

Study Period vs. Actual

Expense Recovery Variance

Portfolio Loans 5,166$ 5,569$ 5,684$ 5,791$ 5,791$ 5,813$

Loan Payoffs 51,246$ 52,604$ 53,665$ 53,978$ 53,912$ 52,681$

Loan Disbursements 17$ 20$ 23$ 17$ 20$ 20$

Loan Payments 73,688$ 77,663$ 84,583$ 89,629$ 89,338$ 93,649$

Total 130,117$ 135,856$ 143,956$ 149,416$ 149,062$ 152,163$

Actual Expenses 145,425$ 149,244$ 149,152$ 149,517$ 143,731$ 144,091$

Total Expense Recovery Variance (15,307) (13,388) (5,196) (101) 5,330 8,072

RCD Volume Variance

Portfolio Loans 73$ 476$ 591$ 698$ 698$ 719$

Loan Payoffs 2,660$ 4,018$ 5,079$ 5,392$ 5,326$ 4,095$

Loan Disbursements (23)$ (20)$ (17)$ (23)$ (20)$ (20)$

Loan Payments (4,423)$ (448)$ 6,473$ 11,518$ 11,228$ 15,538$

Total RCD Volume Variance (1,712)$ 4,026$ 12,126$ 17,586$ 17,232$ 20,333$

Spending Variance

Study Period 131,830$ 131,830$ 131,830$ 131,830$ 131,830$ 131,830$

Actual 145,425$ 149,244$ 149,152$ 149,517$ 143,731$ 144,091$

Total Spending Variance (13,595)$ (17,414)$ (17,322)$ (17,687)$ (11,902)$ (12,261)$

Total Expense Recovery Variance (15,307) (13,388)$ (5,196)$ (101)$ 5,330$ 8,072$

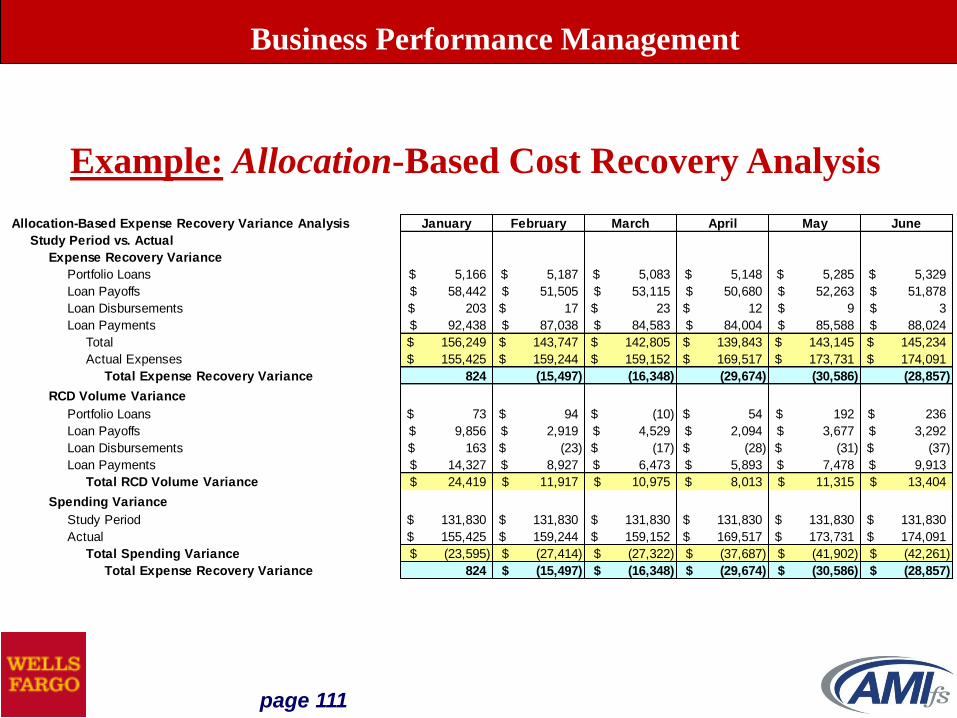

page 111

Business Performance Management

Example: Allocation-Based Cost Recovery Analysis

Allocation-Based Expense Recovery Variance Analysis January February March April May June

Study Period vs. Actual

Expense Recovery Variance

Portfolio Loans 5,166$ 5,187$ 5,083$ 5,148$ 5,285$ 5,329$

Loan Payoffs 58,442$ 51,505$ 53,115$ 50,680$ 52,263$ 51,878$

Loan Disbursements 203$ 17$ 23$ 12$ 9$ 3$

Loan Payments 92,438$ 87,038$ 84,583$ 84,004$ 85,588$ 88,024$

Total 156,249$ 143,747$ 142,805$ 139,843$ 143,145$ 145,234$

Actual Expenses 155,425$ 159,244$ 159,152$ 169,517$ 173,731$ 174,091$

Total Expense Recovery Variance 824 (15,497) (16,348) (29,674) (30,586) (28,857)

RCD Volume Variance

Portfolio Loans 73$ 94$ (10)$ 54$ 192$ 236$

Loan Payoffs 9,856$ 2,919$ 4,529$ 2,094$ 3,677$ 3,292$

Loan Disbursements 163$ (23)$ (17)$ (28)$ (31)$ (37)$

Loan Payments 14,327$ 8,927$ 6,473$ 5,893$ 7,478$ 9,913$

Total RCD Volume Variance 24,419$ 11,917$ 10,975$ 8,013$ 11,315$ 13,404$

Spending Variance

Study Period 131,830$ 131,830$ 131,830$ 131,830$ 131,830$ 131,830$

Actual 155,425$ 159,244$ 159,152$ 169,517$ 173,731$ 174,091$

Total Spending Variance (23,595)$ (27,414)$ (27,322)$ (37,687)$ (41,902)$ (42,261)$

Total Expense Recovery Variance 824 (15,497)$ (16,348)$ (29,674)$ (30,586)$ (28,857)$

page 112

Productivity Measurement

Links total Production Volumes to total

Production Hours (e.g., # of FTEs or # of CPU Hours)

to Calculate a Throughput Rate per Hour

Business Performance Management

page 113

With a plan commitment to increase Productivity

from 10,000 items per FTE to 12,000 items per FTE,

improvement can be represented as follows:

Total

Plan Volume

400,000

FTEs Required

at 10,000 per FTE

40.0

FTEs Required

at 12,000 per FTE

33.33

FTEs Required

at 12,000 per FTE

40.0

Potential

Plan Volume

480,000

Potential

FTE Re-Deployment

6.67

Business Performance Management

page 114

Actual

Expenses

$175,425

Actual

Expenses

Study Period

Expenses

Study Period

Volumes

Study Period

Cap-Based Unit Costs

“X”

Actual Volumes

Cap.-Based

Cost Recovery

Residual

($36,611)

Hourly Rt.

Variance

$23,217

Utilization

Variance

($59,828)

Actual

Volumes

Example: Capacity-Based Cost Recovery Analysis

$138,814

Hourly Rate

Variance

“X”

Actual Hours

Actual Unused

Capacity

“X”

Study Period

Hourly Rate

Business Performance Management

page 115

Business Performance Management

Example: Capacity-Based Cost Recovery Analysis

Capacity-Based Cost Recovery Variance Analysis January February March April May June

Study Period vs. Actual

Cost Recovery Variance

Portfolio Loans 4,590$ 4,608$ 4,515$ 4,573$ 4,695$ 4,734$

Loan Payoffs 51,921$ 45,757$ 47,188$ 45,025$ 46,431$ 41,206$

Loan Disbursements 181$ 15$ 21$ 10$ 8$ 3$

Loan Payments 82,123$ 68,997$ 75,145$ 74,630$ 76,038$ 66,541$

Total Recovery 138,814$ 119,378$ 126,870$ 124,239$ 127,172$ 112,484$

Total Expenses 175,425$ 149,244$ 139,152$ 169,517$ 133,731$ 134,091$

% Recovery 79.13% 79.99% 91.17% 73.29% 95.10% 83.89%

Total Cost Recovery Variance (36,611)$ (29,866)$ (12,283)$ (45,278)$ (6,559)$ (21,607)$

Hourly Rate Variance

Study Period Hourly Rate 40.70$ 40.70$ 40.70$ 40.70$ 40.70$ 40.70$

Actual Hourly Rate 35.94$ 28.90$ 27.82$ 34.30$ 27.49$ 29.49$

Rate Variance per Hour 4.76$ 11.80$ 12.88$ 6.39$ 13.21$ 11.20$

Actual Hours 4,880.72 5,164.96 5,002.32 4,941.52 4,864.00 4,546.32

Total Hourly Rate Variance 23,217$ 60,966$ 64,439$ 31,599$ 64,230$ 50,941$

Utilization Variance

ABC Unit Times X Actual Volumes 3,411 2,933 3,117 3,053 3,125 2,764

Actual Hours 4,881 5,165 5,002 4,942 4,864 4,546

Utilization Variance (1,470) (2,232) (1,885) (1,889) (1,739) (1,783)

Study Period Hourly Rate 40.70$ 40.70$ 40.70$ 40.70$ 40.70$ 40.70$

Total Utilization Variance (59,828)$ (90,832)$ (76,721)$ (76,878)$ (70,789)$ (72,548)$

Total Cost Recovery Variance (36,611)$ (29,866)$ (12,283)$ (45,278)$ (6,559)$ (21,607)$

page 116

Capacity Utilization Measurement

Links total Production Volumes

Extended by Unit Times against

Practical Capacity, Expressed in Hours

Business Performance Management

page 117

With a plan commitment to increase Capacity

Utilization from 75% to 85%, improvement

can be represented as follows:

Total

Plan Capacity

400,000

Capacity Utilization

at 75%

300,000

Potential Reduction

to Total Plan Capacity

353,000

Potential Volume

Increase to Plan

40,000

Capacity Utilization

at 85%

340,000

Capacity Utilization

at 85%

300,000

Business Performance Management

page 118

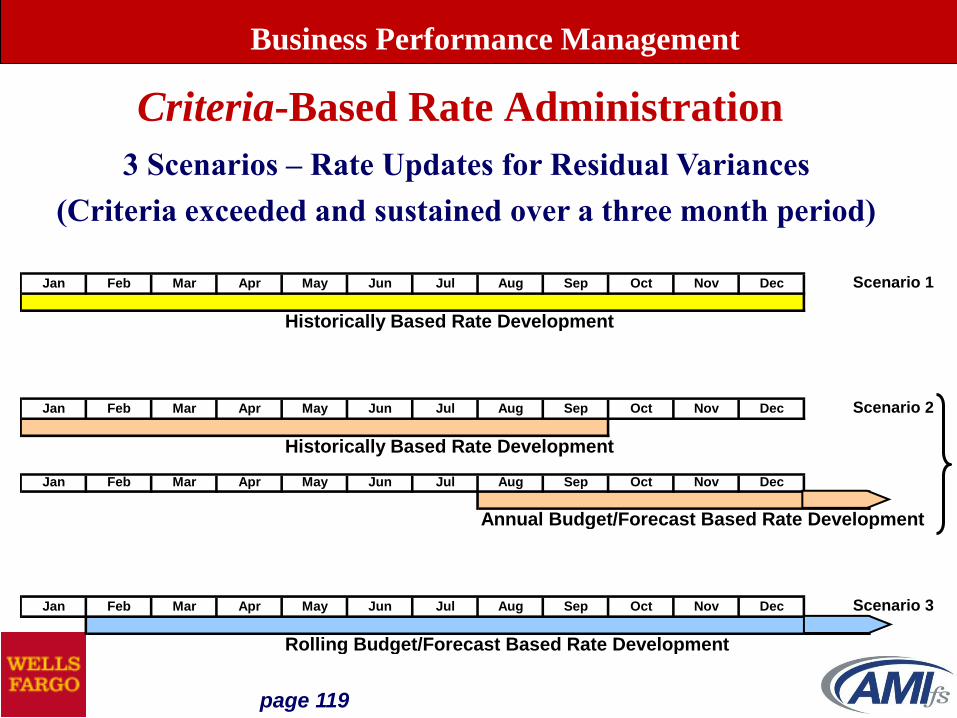

Criteria-Based Rate Administration

•Residual Variances (sustained over a three month period)

> 15% Cost Pools under $X MM

> 10% Cost Pools over $X MM

•Changes in forecasted expenses associated with strategic

efficiency or productivity initiatives

•Changes is projected volumes associated with significant new

business or the loss of key customers

•New Service / Drivers

•New Service (e.g. Image Cash Letter)

•New Drivers (e.g. Clearing Checks via ACH)

•Exceptions considered case-by-case

Business Performance Management

page 119

Criteria-Based Rate Administration

3 Scenarios – Rate Updates for Residual Variances

(Criteria exceeded and sustained over a three month period)

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Scenario 1

Historically Based Rate Development

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Scenario 2

Historically Based Rate Development

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Annual Budget/Forecast Based Rate Development

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Scenario 3

Rolling Budget/Forecast Based Rate Development

Business Performance Management

page 120

Comprehensive Cost Management

Case Study

Deployment - Capacity-Based Methodology

Vs.

Allocation-Based

If you can do cost accounting for financial services,

you can do it for ANY industry…

Business Performance Management

page 121

Monthly Production Data Assumptions:

Personnel Expense $ 31,000

Equip. Depreciation Expense $ 3,000

Occupancy Expense $ 6,000

Materials Expense $ 4,500

Total Expenses $ 44,500

Calculate the following:

Capacity Utilization %

Hourly Rates (Fixed, Semi-Variable, Variable)

Capacity-Based Cost Recovery %

Capacity-Based Cost Recovery Residual $

• Hourly Rate Component

• Utilization Component

Fully Absorbed Cost Recovery %

Fully Absorbed Cost Recovery Residual $

• Spending Component

• Volume Component

Productivity

Hours worked 1,000

Bottles processed 110,000

Comprehensive Cost Management Case Study

Business Performance Management

page 122

Capacity Utilization % = 91.67% [(110,000 * 30 seconds/3600)/1,000 Hours]Hourly RateVariable $ 4.50 ($ 4.50 = $4,500/1,000)Semi-variable $31.00 ($31.00 = $31,000/1,000)Fixed $ 9.00 ($ 9.00 = $9,000/1,000)Total $44.50

Full Capacity Unit Cost $0.3166Fully Absorbed Unit Cost $0.3800

Capacity-Based Cost Recovery% 78.26% ($0.3166 unit cost * 110,000 Bottles/$44,500)

Capacity-Based Cost Recovery Residual $(9,667) ($0.3166 unit cost * 110,000 Bottles = $34,833) less $44,500

-Hourly Rate Component $(6,500) (Study Period Hrly. Rate less Actual Hrly. Rate) * Actual Hours

-Utilization Component $(3,167) [(Unit Time * Actual Volume) – Actual Hours]

* Study Period Hourly Rate

Fully Absorbed Cost Recovery % 93.93% ($0.3800 unit cost * 110,000 Bottles/$44,500)

Fully Absorbed Cost Recovery Residual $(2,700) ($0.3800 unit cost * 110,000 Bottles = $41,800) less $44,500

-Spending Component $(12,833) ($380,000/12) less $44,500-Volume Component $10,133 [(110,000 - (1,000,000/12)] * $0.3800

Productivity 110 per Hour (110,000 Bottles/1,000 Hours)

Comprehensive Cost Management Case Study

Business Performance Management

page 123

Cost Deployment

for

Integrated Profitability

Business Performance Management

page 124

Product

Revenues

LOB

Customer

Distributed

Costs

Product

Margins

Del. Chan.

Distributed

Credits

Bus. Proc.

Res. Group

Expenses

Incurred

Cost

Recovery

Residual

CCM Deployment for Integrated Profitability

Business Performance Management

page 125

Usage –Driven

Transaction Costs by

Delivery Channel

Business Performance Management

page 126

They have to anticipate Resource Requirements every day:

Too many resources positioned today by Delivery Channel

Not enough resources positioned today by Delivery Channel

Resource Managers are frustrated without

Management Information:

What about tomorrow?

Customers of the Bank do not announce their

transaction intentions nor their

Delivery Channel preferences.

Delivery Channel Alternatives

Business Performance Management

page 127

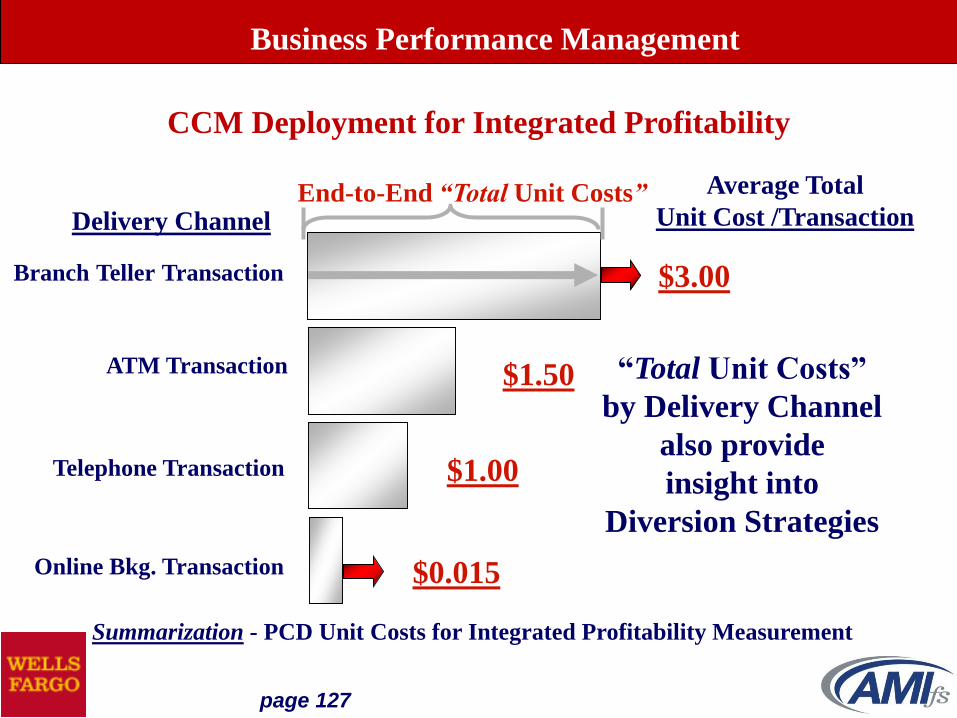

Branch Teller Transaction

Delivery Channel

ATM Transaction

Telephone Transaction

Online Bkg. Transaction

Average Total

Unit Cost /Transaction

$1.00

$3.00

$1.50

$0.015

“Total Unit Costs”

by Delivery Channel

also provide

insight into

Diversion Strategies

End-to-End “Total Unit Costs”

Summarization - PCD Unit Costs for Integrated Profitability Measurement

CCM Deployment for Integrated Profitability

Business Performance Management

page 128

Understanding Costs and Usage by Delivery Channel provides

insight into Integrated Profitability and Integrated Resource Management

Branch Teller Transactions

Delivery Channel

ATM Transactions

Telephone Banking Transactions

Online Banking Transactions

Utilization %

67%

72%

50%

10% Available Unused Capacity

Business Performance Management

page 129

Customer: R. McDonald

ABC Bank: YTD 2016Drill down into Products

TOTAL

DEPOSIT

PRODUCTS

CREDIT

PRODUCTSFEE BASED

PRODUCTS

INTEREST INCOME

CHARGE FOR FUNDS

NET INTEREST INCOME

INTEREST EXPENSE

CREDIT FOR FUNDS

NET FUNDS ADJUSTMENT

NET INTEREST MARGIN

PROVISION FOR LOSSES

GROSS FEES

WAIVED FEES

NON-INTEREST INCOME

NET REVENUES

SERVICING COSTS - BRANCH

SERVICING COSTS - ATM

SERVICING COSTS - TEL. BKG.

SERVICING COSTS - INTERNET

DIRECT PRODUCT COSTS

RELATIONSHIP MGT COSTS

SALES AND MARKETING COSTS

TOTAL COSTS

PRODUCT MARGINS

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

_____

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

_____

_____

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

_____

_____

_____

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

Usage-Driven Transaction Costs

Usage-Driven

Transaction

Costs by

Delivery Channel

CCM Deployment for Integrated Profitability

Delivery Channel

Alternatives:

•Same Customer

•Same Product

•Same Transaction

Different Costs

page 130

Customer: R. McDonald

ABC Bank: YTD 2016Drill down into Products

TOTAL

DEPOSIT

PRODUCTS

CREDIT

PRODUCTSFEE BASED

PRODUCTS

INTEREST INCOME

CHARGE FOR FUNDS

NET INTEREST INCOME

INTEREST EXPENSE

CREDIT FOR FUNDS

NET FUNDS ADJUSTMENT

NET INTEREST MARGIN

PROVISION FOR LOSSES

GROSS FEES

WAIVED FEES

NON-INTEREST INCOME

NET REVENUES

SERVICING COSTS - BRANCH

SERVICING COSTS - ATM

SERVICING COSTS - TEL. BKG.

SERVICING COSTS - INTERNET

DIRECT PRODUCT COSTS

RELATIONSHIP MGT COSTS

SALES AND MARKETING COSTS

TOTAL COSTS

PRODUCT MARGINS

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX

XXXX