complying with the dodd-frank diversity and inclusion · pdf filecomplying with the dodd-frank...

TRANSCRIPT

Complying with the Dodd-Frank Diversity and Inclusion Standards

Association of Corporate Counsel

Arizona Chapter Tuesday, November 17, 2015

Dee Spagnuolo Partner

Ballard Spahr LLP

2

Agenda

• Introduction

• Section 342 of the Dodd-Frank Act

• Overview of the Standards

• Focus Areas and Compliance Approaches

• Voluntary Nature of the Standards – Why Comply?

• Questions and Answers

DMEAST #23316894

3

Dee Spagnuolo, Esquire Partner, White Collar Defense/Internal Investigations Ballard Spahr LLP [email protected] | 215.864.8312

Dee Spagnuolo’s practice focuses on internal investigations and compliance and regulatory matters. She represents clients in the development and implementation of their diversity and inclusion programs, and is a member of Ballard Spahr’s Diversity Council.

DMEAST #23316894

4

Section 342 of Dodd-Frank

DMEAST #23316894

5

Section 342 of Dodd-Frank: Background

• The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 Pub.L.No. 111-203 (2010) was signed into law July 21, 2010, in the wake of the 2008 financial crisis

• Dodd-Frank’s regulatory and compliance objectives are to: - Increase financial marketplace transparency and stability - Identify, monitor, and reduce systemic risks

• Section 342 contains Dodd Frank’s Diversity and Inclusion Objectives

DMEAST #23316894

6

Section 342 of Dodd Frank: Objectives

• Objectives of Section 342 Address the under-representation of women and minorities in the financial services industries and public companies by focusing on transparency and awareness of diversity and inclusion policies within: - Federal financial services agencies, including the SEC - Entities that are regulated by these agencies - Entities that contract with these agencies

DMEAST #23316894

7

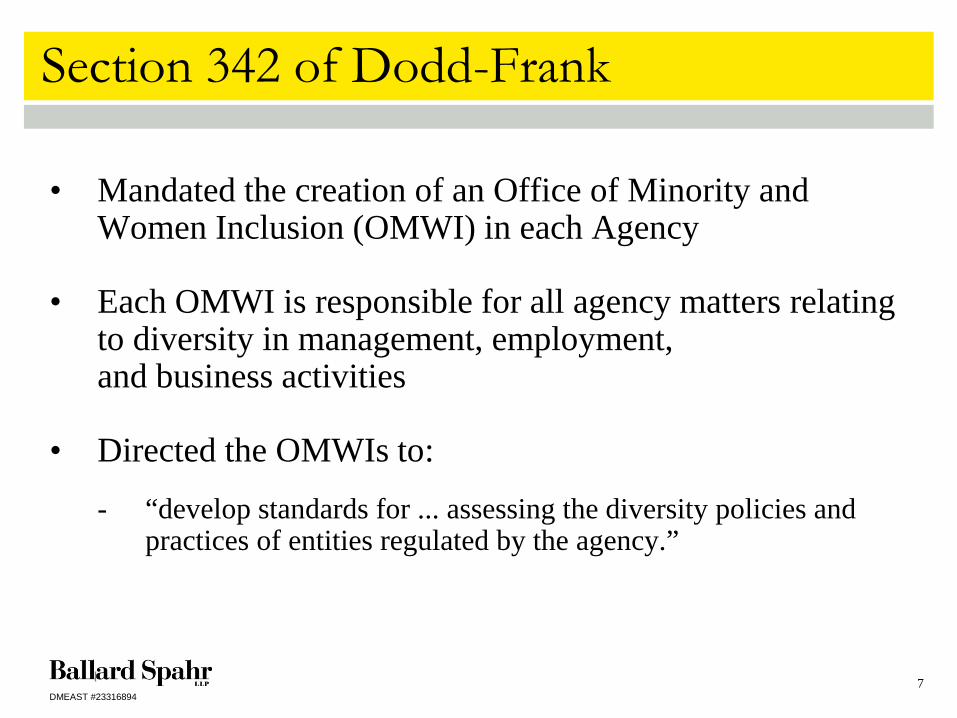

Section 342 of Dodd-Frank

• Mandated the creation of an Office of Minority and Women Inclusion (OMWI) in each Agency

• Each OMWI is responsible for all agency matters relating to diversity in management, employment, and business activities

• Directed the OMWIs to: - “develop standards for ... assessing the diversity policies and

practices of entities regulated by the agency.”

DMEAST #23316894

8

The Numbers

DMEAST #23316894

9

Section 342 of Dodd-Frank: The Numbers Underrepresentation of minorities and women at executive and senior level positions in finance/insurance industries:

• White Males: 31% of total workforce - but 64% of executive and senior level positions • Women: 59% of the total workforce - but only 29% of executive and senior level positions • African Americans: 12% of total workforce - but only 3% of the executive and senior level positions • Hispanics: 8% of total workforce - but only 3% of the executive and senior level positions

31%

59%

12% 8% 7%

2%

64%

29%

3% 3% 4% 1%

0%

10%

20%

30%

40%

50%

60%

70%

White Men Women African Americans Hispanics Asian Americans Other POC

Workforce and Executive/Senior Level Position Comparison by Race and Gender

Total Workforce

Executive/Senior Level PositionsOther: Other POC

Source: EEOC 2013 Job Patterns for Minorities and Women in Private Industry (EEO-1), 2013 EEO-1 National Aggregate Report by NAICS-2 Code (Finance and Insurance) (2013).

DMEAST #23316894

10

The Standards

DMEAST #23316894

11

The Standards

• Published June 10, 2015

• The Standards apply to all entities regulated by: - Board of Governors of the Federal Reserve System - Consumer Financial Protection Bureau (CFPB) - Department of the Treasury, Federal Deposit Insurance

Corporation (FDIC) - National Credit Union Administration (NCUA) - Officer of the Comptroller of the Currency (OCC) - Securities and Exchange Commission (SEC)

DMEAST #23316894

12

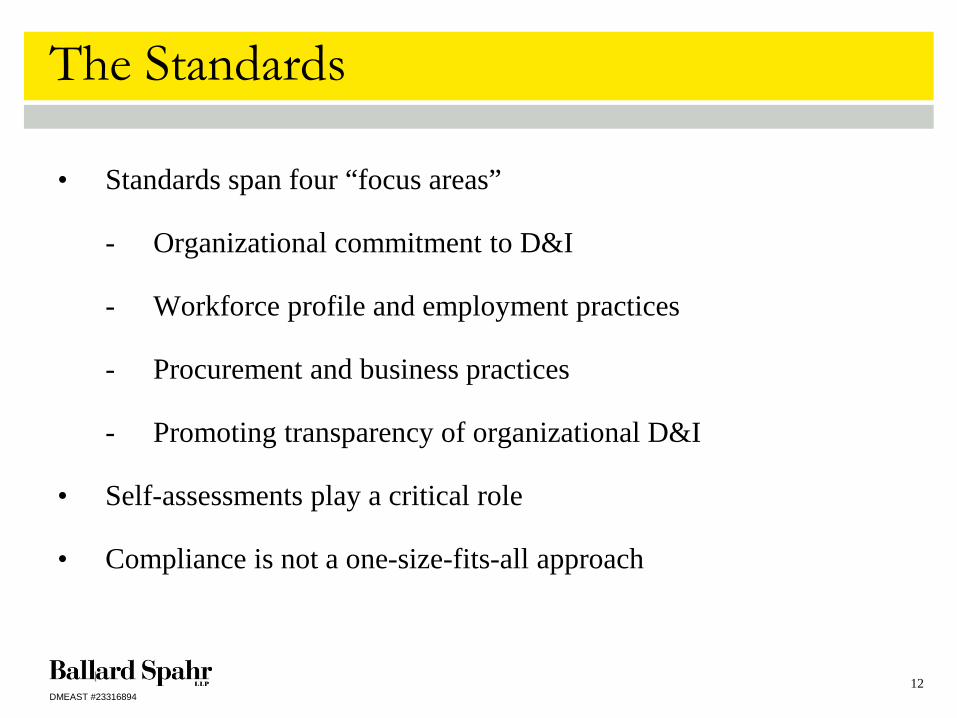

The Standards

• Standards span four “focus areas”

- Organizational commitment to D&I

- Workforce profile and employment practices

- Procurement and business practices

- Promoting transparency of organizational D&I

• Self-assessments play a critical role

• Compliance is not a one-size-fits-all approach

DMEAST #23316894

13

The Standards

• Standards address:

- Diversity of minorities and women, but may include other communities (e.g., veterans, people with disabilities, LGBT)

- Inclusion, defined as a process to create and maintain positive work environment that values individual similarities and differences

• Generally designed for companies of 100+ U.S. employees

DMEAST #23316894

14

Focus Areas

DMEAST #23316894

15

Organizational Commitment

Assessment Factors

Approaches

Strategic Plan • Supplier diversity and employment practices (hiring, recruiting, retention, and promotion)

D&I Policy • Approved and supported by senior leadership

Progress Reports • Board of directors • Senior management • Public report

Training • Regular training and educational opportunities on D&I

Senior Level Official • Chief Diversity Officer • Internal Diversity Council

Diverse candidate pools (including Board)

• Senior leadership pipeline – succession planning • Board pipeline – nominating criteria

DMEAST #23316894

16

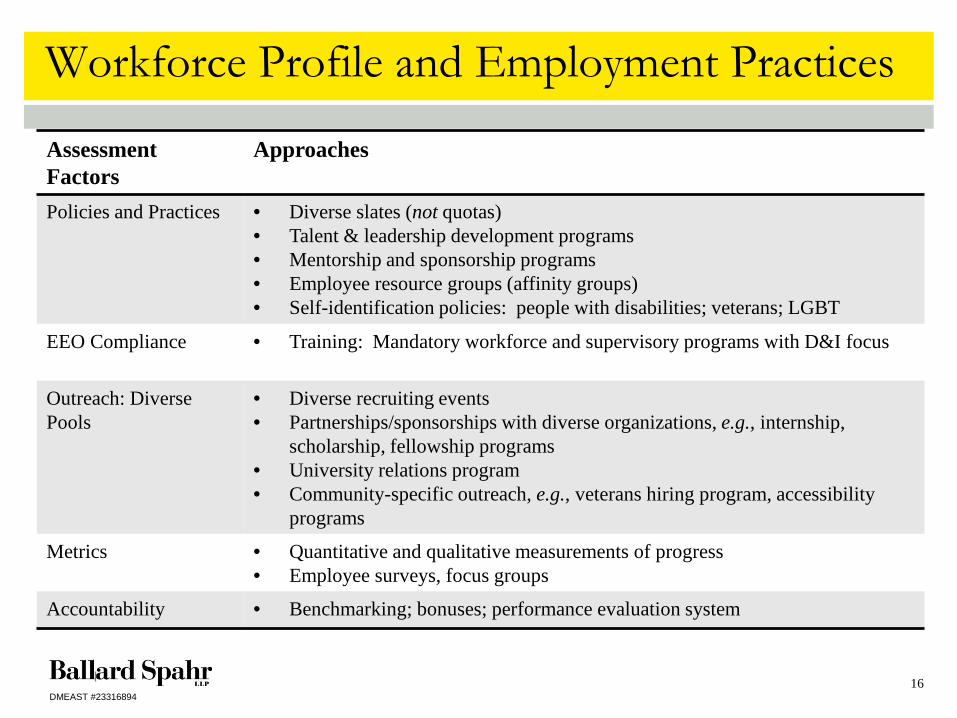

Workforce Profile and Employment Practices

Assessment Factors

Approaches

Policies and Practices • Diverse slates (not quotas) • Talent & leadership development programs • Mentorship and sponsorship programs • Employee resource groups (affinity groups) • Self-identification policies: people with disabilities; veterans; LGBT

EEO Compliance • Training: Mandatory workforce and supervisory programs with D&I focus

Outreach: Diverse Pools

• Diverse recruiting events • Partnerships/sponsorships with diverse organizations, e.g., internship,

scholarship, fellowship programs • University relations program • Community-specific outreach, e.g., veterans hiring program, accessibility

programs

Metrics • Quantitative and qualitative measurements of progress • Employee surveys, focus groups

Accountability • Benchmarking; bonuses; performance evaluation system

DMEAST #23316894

17

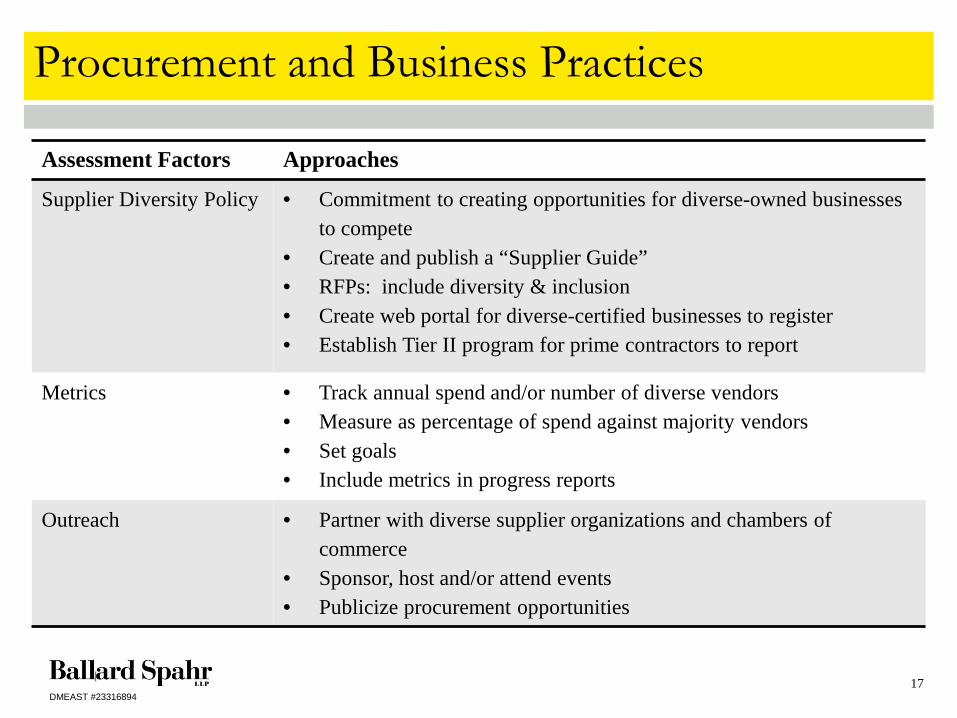

Procurement and Business Practices

Assessment Factors Approaches

Supplier Diversity Policy • Commitment to creating opportunities for diverse-owned businesses to compete

• Create and publish a “Supplier Guide” • RFPs: include diversity & inclusion • Create web portal for diverse-certified businesses to register • Establish Tier II program for prime contractors to report

Metrics • Track annual spend and/or number of diverse vendors • Measure as percentage of spend against majority vendors • Set goals • Include metrics in progress reports

Outreach • Partner with diverse supplier organizations and chambers of commerce

• Sponsor, host and/or attend events • Publicize procurement opportunities

DMEAST #23316894

18

Promoting Transparency

Assessment Factors

Approaches

Strategic Plan • Publish strategic objectives through D&I report

D&I Policy • Publish commitment to diversity through website • Create and disseminate public diversity report • Include D&I as part of Corporate Social Responsibility Report

Metrics • Include metrics in published reports on D&I to demonstrate progress

Opportunities • Promote opportunities for diversity both internally and externally: o Employment opportunities o Procurement opportunities o Availability of internship or mentorship programs o Leadership development opportunities

DMEAST #23316894

19

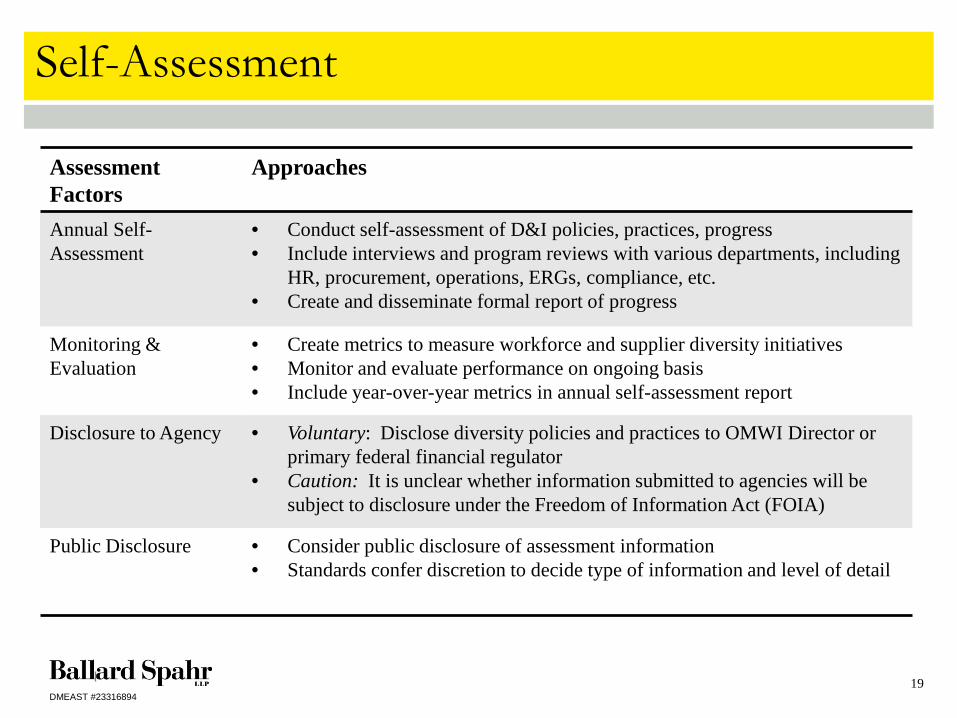

Self-Assessment

Assessment Factors

Approaches

Annual Self-Assessment

• Conduct self-assessment of D&I policies, practices, progress • Include interviews and program reviews with various departments, including

HR, procurement, operations, ERGs, compliance, etc. • Create and disseminate formal report of progress

Monitoring & Evaluation

• Create metrics to measure workforce and supplier diversity initiatives • Monitor and evaluate performance on ongoing basis • Include year-over-year metrics in annual self-assessment report

Disclosure to Agency • Voluntary: Disclose diversity policies and practices to OMWI Director or primary federal financial regulator

• Caution: It is unclear whether information submitted to agencies will be subject to disclosure under the Freedom of Information Act (FOIA)

Public Disclosure • Consider public disclosure of assessment information • Standards confer discretion to decide type of information and level of detail

DMEAST #23316894

20

Other Considerations: Community Engagement

• Not specifically addressed in the Standards • Track and analyze support of minority-led and minority-

serving organizations • Include data in D&I reporting • Opportunity to celebrate successes, but not a replacement

for other assessment factors

DMEAST #23316894

21

Why Comply?

DMEAST #23316894

22

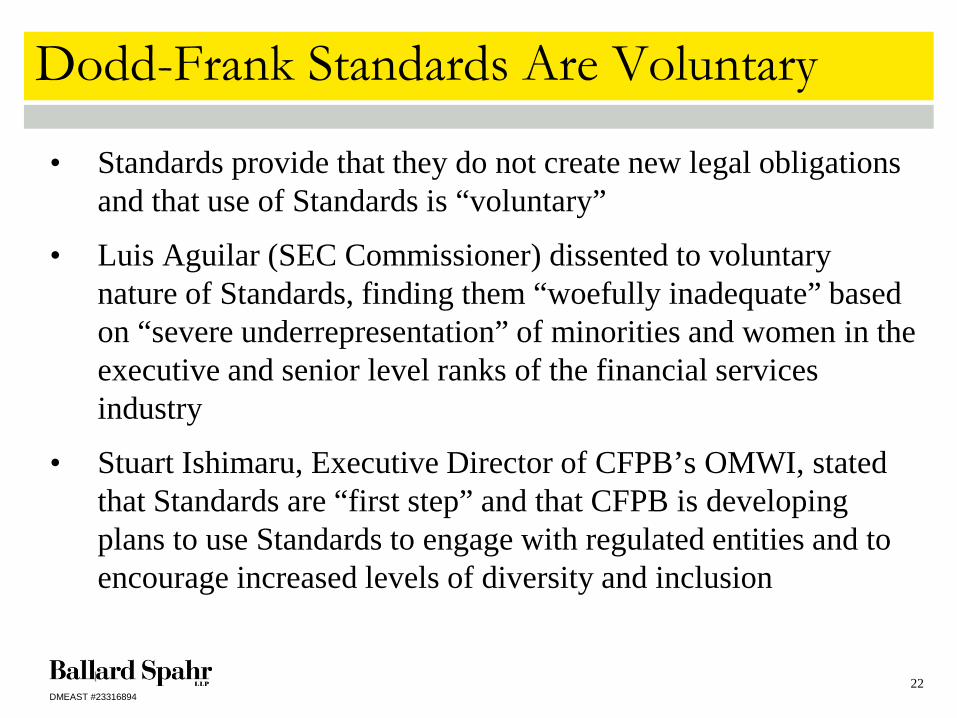

Dodd-Frank Standards Are Voluntary

• Standards provide that they do not create new legal obligations and that use of Standards is “voluntary”

• Luis Aguilar (SEC Commissioner) dissented to voluntary nature of Standards, finding them “woefully inadequate” based on “severe underrepresentation” of minorities and women in the executive and senior level ranks of the financial services industry

• Stuart Ishimaru, Executive Director of CFPB’s OMWI, stated that Standards are “first step” and that CFPB is developing plans to use Standards to engage with regulated entities and to encourage increased levels of diversity and inclusion

DMEAST #23316894

23

Why Comply?

Value Added • Companies that are more diverse regularly outperform

companies that are not - Correlation with financial performance, market share, relative

profits, stock prices, revenues, net income, and net profit margin - Key ingredient in a successful business strategy designed to

maintain and enhance competitive advantage

DMEAST #23316894

24

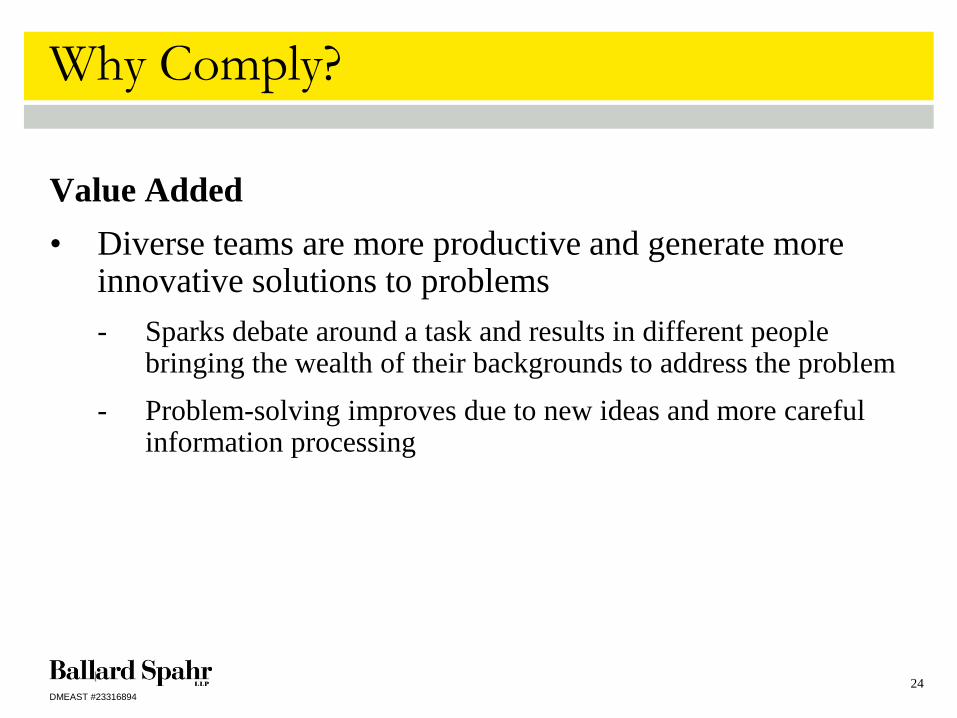

Why Comply?

Value Added • Diverse teams are more productive and generate more

innovative solutions to problems - Sparks debate around a task and results in different people

bringing the wealth of their backgrounds to address the problem - Problem-solving improves due to new ideas and more careful

information processing

DMEAST #23316894

25

Why Comply?

Talent Acquisition • Demographic changes are inevitable • Understanding those changes is critical to maintaining and

increasing market share • A diverse and inclusive workforce is key to attracting and

retaining top talent - Recruiting, retaining, and promoting diverse employees essential

to success - Workforce strategy must include measures aimed at attracting

and retaining the best, regardless of ethnicity, gender, or other diverse characteristics

DMEAST #23316894

26

Why Comply?

• Regulatory Perspective - Firms do not want to stand out as opting to ignore D&I when asked by

regulators

• It’s the Right Thing to Do - From a corporate social responsibility perspective in world that is increasingly

diverse and global

DMEAST #23316894

27

Questions and Answers

DMEAST #23316894