complications in financing new nuclear power plants lynn rubow, director, business development...

TRANSCRIPT

Complications inFinancing New Nuclear Power Plants

Lynn Rubow, Director, Business DevelopmentLazarina Bataklieva, Lead Economic Analyst

BULATOM 2011

What we all know….

Large Capital Investment Complex Licensing and Permitting Process Long Term Implementation Nuclear is Exceptionally Safe Long Life with Very Low Production Cost Required Strong Regulatory Platform Required Large Community of Qualified Experts Small Community of Large Gen III or III+ NPP Suppliers Virtually No Air Quality Issues, including CO2 Special Public Sensitivities to Nuclear Technology

WorleyParsons Recent NPP Economic/ Financing Evaluation Experience

Kozloduy Modernization Belene NPP New-Build “Far East” NPP New-Build (Russia) Armenia NPP Unit Replacement Jordan First NPP New-Build Egypt First NPP New-Build Baltic NPP New-Build (Russia)

Historical Financing Approach

For many years, nuclear was a quite conservative investment:– Lower investment costs; – Monopoly (or Franchise) utility, guaranteed electricity offtake; – Long-term (30+ years), low-interest loans, on balance sheet; – Risks generally passed to consumers; – Sovereign financing or sovereign guarantees on financing; and – Generally, reasonable level of public support, or public not entering

the picture.

And now??

Recent Financing Complexities

Higher investment costs Significant impact on company rating and balance sheet Economic crisis Lending terms less attractive (for several reasons) Lack of security for electricity sales

– Secure PPA– No balance sheet– Competition

Governments desire to shed some risk Public opposition more “organized”

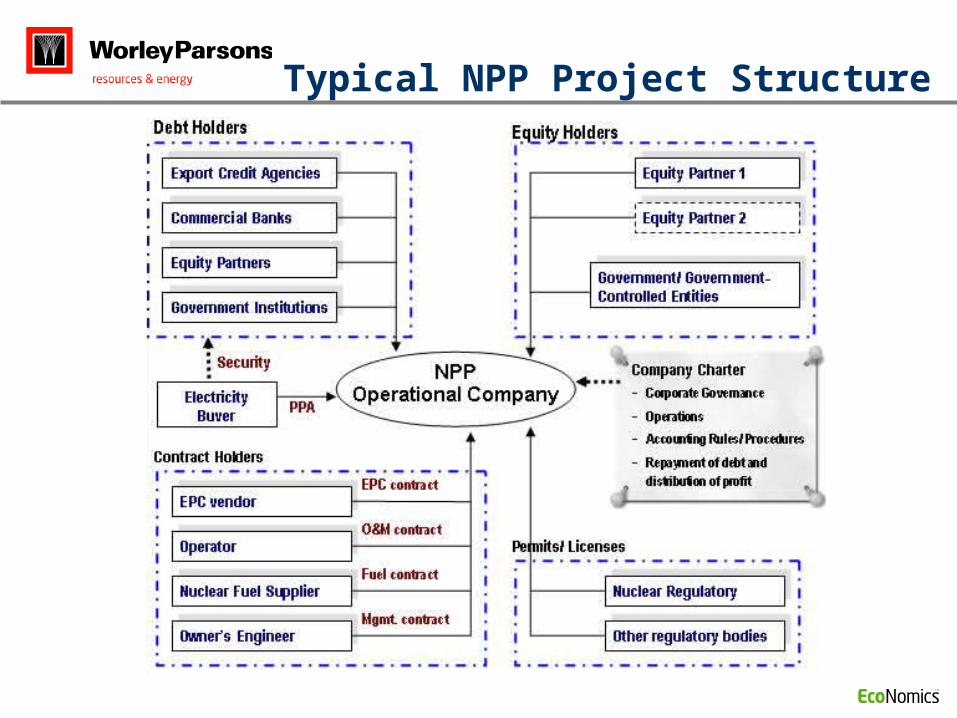

Typical NPP Project Structure

Project Funding

Government Domestic banks

Local investors Foreign banks/ Governments

Sources of Equity Sources of Debt

Investors, with Vendors Export credit agencies

Other large utility companies Development Finance Institutions

FinancingFinancing

structurestructure

Critical: Critical:

• Split of Equity (Majority In-Country)Split of Equity (Majority In-Country)

• Maximize ECA and Government LoansMaximize ECA and Government Loans

Technical Developments

50+ years “Lessons Learned” Multiple Redundant Active Safety Systems Extensive Passive Safety Design Continuing Materials Development Improved Operational Reliability/ Availability Long design life However……..

– Limited number of NPP suppliers– Limited number of large “qualified” international investors– Technological development actually restricted by the requirement for

extensive qualification and/ or reference plant support

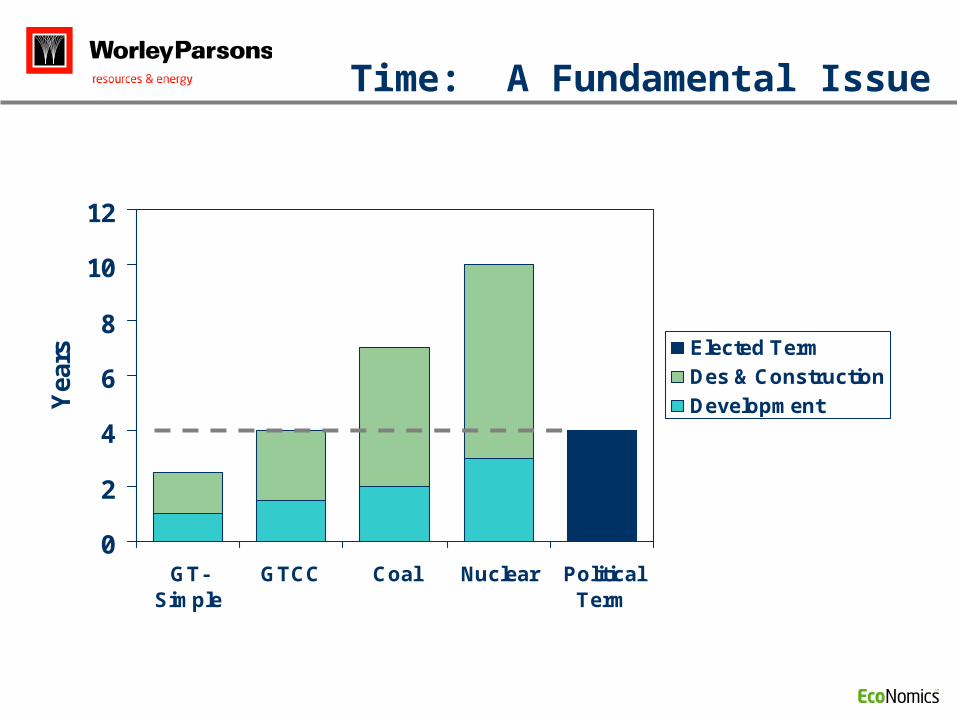

Time: A Fundamental Issue

0

2

4

6

8

10

12

GT-Simple

GTCC Coal Nuclear PoliticalTerm

Yea

rs Elected Term

Des & Construction

Development

Financing Drivers

Characteristics of a Project Finance (non-recourse) Model: – Reliance on strong PPA; however, in conflict with “free market” that

is theoretically open to competition– Reliance on fuel supply agreement, also somewhat in conflict with

“free market” concept (though less critical for nuclear)– Reliance on strong, more expensive, EPC-LSTK contract

Unbundled market, with associated free market for electricity purchase/ sale is not supportive of the Project Finance Model

Goal of NPP Financing is to strike a balance between free market principles, and the required security to achieve reasonable finance terms. How??

Conflicting Goals

Paths of Development:– Government only– Private entity only– Public-Private Partnerships (PPPs) as a Special Purpose Company

(SPC)…..today’s common approach

Issues of Nuclear Public-Private Partnerships (PPPs)– General difficulty to form PPPs – As a special purpose company, while effective for projects organized

under a “Project Finance” approach, secured by PPA, FSA, EPC-LSTK Agreement, it is more difficult for nuclear projects considering their need for stringent security, and their long-lead nature.

– The SPCs must still have backing – Goals of partnerships can be in conflict

Different Motivation/ Values: Public vs. Private

Public (i.e. Government) Private

Expectation of Benefits over the Long Term;

Expectation of Investment Return in Short Period, signified by high Discount Rate in analysis, but also to capture “cash cow” benefits after debt is paid;

Electricity is a base need of the society. Responsibility to provide reliable electricity supply to population;

Electricity is a “market good”; Plant is responsible to satisfy terms of PPA, and also motivated to participate in the Market, as applicable, to maximize returns;

Highly motivated to achieve acceptable tariff, for Political, Social, and Economic reasons;

Interest is in setting maximum acceptable tariff to achieve return on investment;

Responsibility to Insure Safety, far above required insurance limit;

Responsible to meet insurance requirements;

Motivated to build technical expertise within country.

Satisfy contract requirements for “Capacity Building”.

In the end, there will likely be compromises on both sides to blend long- and short-term needs, and find agreement.

Consider Cash Flows through the Plant Life

Cost of Electricity Escalated and Not Discounted

When you reach year 15 or 20, the “revenue vs. cost” of the plant becomes insignificant

Cost of electricity by Components, annual basis

0

10

20

30

40

50

60

70

80

90

100

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

Year of plant operation

EU

R/M

Wh

Loan Repayment

Fuel Costs

O&M Costs

Cost of electricity by Components, annual basis

01020

3040506070

8090

100

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

Year of plant operation

EU

R/M

Wh

Loan Repayment

Fuel Costs

O&M Costs

Cost of Electricity Escalated and Discounted at 10%/year

Consider Cash Flows through the Plant Life Cost of electricity by Components, annual basis

01020

3040506070

8090

100

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

Year of plant operation

EU

R/M

Wh

Loan Repayment

Fuel Costs

O&M CostsCost of Electricity Escalated and Discounted at 10%/year

Cost of Electricity Escalated and Discounted at 4%/year

Cost of electricity by Components, annual basis

0

10

20

30

40

50

60

70

80

90

100

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29 31 33 35 37 39 41 43 45 47 49 51

Year of plant operation

EU

R/M

Wh

Loan Repayment

Fuel Costs

O&M Costs

Consider IRR Requirements

Higher IRR “Demands” will result in different required tariffs through the plant life

Tariff Path at Different IRR

0

50

100

150

200

250

2010 2015 2020 2025 2030 2035 2040

Ta

riff

, E

ur/

MW

h

IRR 15%

IRR 12%

IRR 10%

IRR 8%

The Case for In-Country Ownership

Many nuclear projects seeking “complex” arrangements involving foreign investment due to: – Lack of equity– Lack of borrowing capacity– Lack of development/ operational expertise

More Issues (in addition to Public-Private issues): – Ultimate responsibility lies within the Project Country– Criteria for quality of investment are different:

Country wants security of long-term power supply Investor wants return on investment as soon as possible BOO model quite expensive to consumer, generally

– Typically, “Earned Equity” is undervalued

100% In-Country Ownership retains both costs and benefits within the border.

Consider Small, Low GDP Country Issues

Many smaller countries are pursuing nuclear as their best option, and now interested in joining nuclear power “club”; however, it is a large undertaking without precedent

Financing security issues of smaller countries: – GDP– Cash– Lending limits– Country rating– Technical base (also a financing issue)

Generally, the primary issue is “affordability”

Some Possible things to Consider

Stronger involvement of Government Stronger involvement of offtakers as investors:

– Large industrial entities– Utilities/ Distribution companies– Smaller, aggregated industrial entities

Return to corporate finance model (e.g. balance sheet based on existing operating assets)

More creative BOO(T) structures EPCM project execution structures Better communication with outside stakeholders, i.e.,

why nuclear is best option

Discussion Items

Can nuclear plant financing be structured as a normal power project??

How to Simultaneously Satisfy Requirements of Public and Private Investors??

What kind of requirements should be imposed on outside investors in NPPs??

How can Lenders become more a part of the process??

How can Public become more a part of the process??

Thank you……