compliance online ppt format 2015 anti manipulation rules concerning securities offerings 8.12.2015

TRANSCRIPT

www.complianceonlie.com©2010 Copyright

© 2015 ComplianceOnline

This training session is sponsored by

1

Anti Manipulation Rules Concerning Securities Offerings

This Training is Brought to you by ComplianceOnline.

Presenter: Craig M. Taggart

www.complianceonline.com©2015 Copyright

2

Instructor Profile: Craig Taggart has almost a decade of experience in the fields of mergers and acquisitions and

business financing. Mr. Taggart works strategically with his clients to achieve the highest value for their business within the capital markets. His experience with BCC Capital Partners in the M&A industry has greatly contributed to his understanding of transaction structure, strategic

placement of buyers, and the attainment of maximum market value for his clients. He has represented and sold many businesses in a number of different industries and has significant experience working with companies in: continuing education, transportation, software and professional services. Mr. Taggart is currently working in the clean energy sector that covers multiple initiatives within M&A and corporate development.

He is a certified merger and acquisition advisor, accredited valuation analyst as well as an active member of Alliance of Mergers and Acquisition, and The National Association of Certified Valuators and Analysts (NACVA). Mr. Taggart has been a certified fraud examiner since 2011 and has owned an investigative franchise business, which focused on fraud based cases involving insurance, asset searches, surveillance, witness statements

He earned his MBA from the San Diego State University specializing in financial management. Mr. Taggart graduated from the California State University Northridge with a bachelor’s degree majoring in organizational psychology.

www.complianceonline.com©2015 Copyright

Areas Covered in the Webinar: CFTC Proposes Rules to Expand Prohibition on Market

Manipulation Prohibition of Price Manipulation SEC Proposes Rule 9j-1 under the Exchange Act for

Security-based Swaps The red flags of securities fraud The four fundamental categories of securities fraud The monetary scope of securities fraud

3

www.complianceonline.com©2015 Copyright

4

Investment-fraud terminology Investigative resources and examination strategies SEC Regulation M-Related Notice Requirements What is a distribution and magnitude of the offering

under this regulation Rule 5190

www.complianceonline.com©2015 Copyright

Agenda

5

The Securities and Exchange Commission (Commission) is proposing amendments to Regulation M under the Securities Exchange Act of 1934 (Exchange Act), which governs the activities of underwriters, issuers, selling security holders, and others in connection with offerings of securities. The proposed amendments are intended to prohibit certain activities by underwriters and other distribution participants that can undermine the integrity and fairness of the offering process, particularly with respect to allocations of offered securities.

www.complianceonline.com©2015 Copyright

The proposal also seeks to enhance the transparency of syndicate covering bids, which may affect the aftermarket price and trading of an offered security, and prohibit the use of penalty bids. The amendments also are intended to update certain definitional and operational provisions in light of market developments since Regulation M's adoption. As a consequence of these proposed amendments to Regulation M, we are also recommending corresponding changes to disclosure rules under the Securities Act of 1933 ("Securities Act") as well as changes to certain recordkeeping rules under the Exchange Act.

6

www.complianceonline.com©2015 Copyright

Definition of Manipulation source Securities and Exchange Commission

Manipulation interferes with the securities markets’ fundamental function as an independent pricing mechanism and undermines the markets’ integrity and fairness. Under the securities laws, Congress granted the Commission broad authority to combat manipulative conduct. The Commission, in turn, has recognized that special opportunities and incentives for manipulation arise in securities offerings and has determined that certain offerings require specific regulation.

7

www.complianceonline.com©2015 Copyright

8

Consequently, the Commission has focused its regulation on market activities that could artificially facilitate an offering. Because price integrity is essential during a securities offering, the Commission adopted rules to proscribe and regulate activities that offering participants could use to manipulate the price of the offered security. The anti-manipulation rules were first codified in 1955, and today, Regulation M incorporates these provisions.3 Regulation M, among other things, prohibits issuers, selling security holders, underwriters, broker-dealers,

www.complianceonline.com©2015 Copyright

and other distribution participants4 from directly or indirectly bidding for, purchasing, or attempting to induce any person to bid for or purchase any security that is the subject of the distribution during the applicable restricted period.5 Regulation M proscribes activities that may increase a security’s offering price, and so increase the offering proceeds; or may stabilize the market price of an offered security in order to avoid a price decline during the sales period or in the immediate aftermarket, or to induce or attempt to induce prospective investors to buy in the aftermarket.

9

www.complianceonline.com©2015 Copyright

Commodity Futures Trading Commission(CFTC) Proposed Rules Q:Would the proposed rules impose margin requirements on

commercial end users? A: No. The rule requires a swap dealer (SD) or major swap

participant (MSP) to collect margin if its counterparty is another SD/MSP or a financial entity other than an SD/MSP. An SD/MSP would collect initial and variation margin from a nonfinancial end user only to the extent the parties had mutually agreed to this in their privately-negotiated credit support arrangements.

Q:What products would the proposed rules cover? A: The rules would apply to uncleared swaps entered into after

the effective date of the regulation. The proposal would not apply retroactively

10

www.complianceonline.com©2015 Copyright

Q: Did the Commission consult with other US authorities in developing these rules?

A: Yes. Staff of the Commission consulted with staff of the Federal Reserve Board, the Office of the Comptroller of the Currency, the Federal Deposit Insurance Corporation, the Farm Credit Administration, and the Federal Housing Finance Agency (collectively, the Prudential Regulators) in developing these rules. Staff of the Securities and Exchange Commission also participated in these consultations. The proposed rules of the Commission and the Prudential Regulators are very similar.

Q: Are the proposed rules similar to international standards? A: Yes. The proposed rules are very similar to the standards issued by the

Basel Committee on Banking Supervision and the International Organization of Securities Commissions in September of 2013. In a few instances the Commission and the Prudential Regulators are stricter. For example the international standards would permit limited rehypothecation of initial margin. The proposed rules would prohibit it.

11

www.complianceonline.com©2015 Copyright

Agenda

12

Why Should You Attend:Education is power! There are not many other industries, that this concept could not be truer. The securities industry is the most regulated, compliance, governance driven industry in the country. This is actually for good reason, this is also one of the most lucrative fields a person can pursue regarding their overall career path. Here in lies the key reasons, with more rules and regulations, comes more securities exams and what you don’t know can be severely destructive to your company, firm, practice at many levels. As we have read the more monetary gain a person has, that same person has more inclination to break the rules or commit fraud as fear and greed come in to play more often than not in Wall Street based careers.

www.complianceonline.com©2015 Copyright

We will review how these new rules and laws can make you aware of what to look for in the workplace, a key skill set if you are part of any compliance or risk management departments. Perpetrators of securities fraud are responsible for not only a loss of assets, but also the devastation of investor confidence, which can carve away at the respect people have for the global financial markets. The destruction caused by their actions, both emotional and financial, is staggering. In fact, one respected academic study from Stanford Law School reported an annual damage estimate of nearly $700 billion for 2007. In a time when headlines are filled with the stories of Madoff and Stanford, preventing and investigating securities fraud is now more important than ever.

13

www.complianceonline.com©2015 Copyright

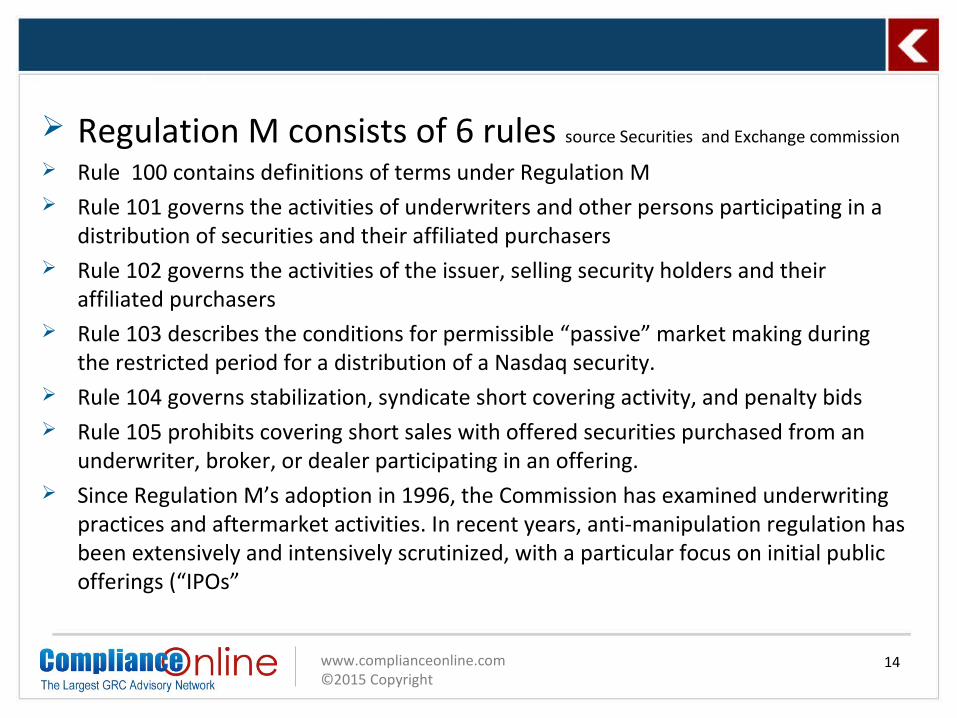

Regulation M consists of 6 rules source Securities and Exchange commission

Rule 100 contains definitions of terms under Regulation M Rule 101 governs the activities of underwriters and other persons participating in a

distribution of securities and their affiliated purchasers Rule 102 governs the activities of the issuer, selling security holders and their

affiliated purchasers Rule 103 describes the conditions for permissible “passive” market making during

the restricted period for a distribution of a Nasdaq security. Rule 104 governs stabilization, syndicate short covering activity, and penalty bids Rule 105 prohibits covering short sales with offered securities purchased from an

underwriter, broker, or dealer participating in an offering. Since Regulation M’s adoption in 1996, the Commission has examined underwriting

practices and aftermarket activities. In recent years, anti-manipulation regulation has been extensively and intensively scrutinized, with a particular focus on initial public offerings (“IPOs”

14

www.complianceonline.com©2015 Copyright

15

www.complianceonline.com©2015 Copyright

16

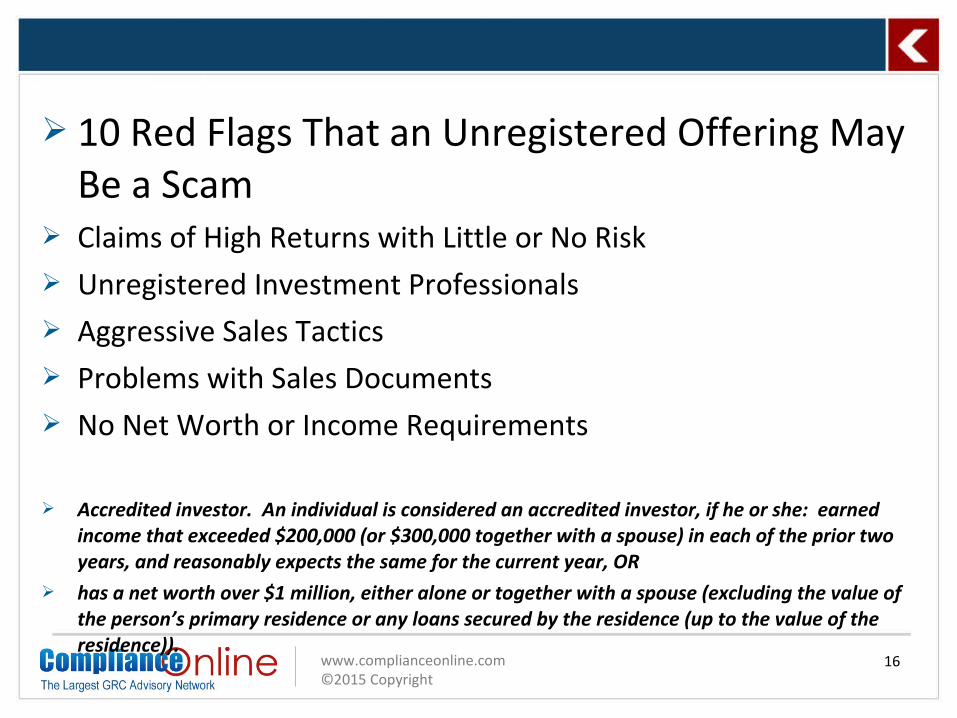

10 Red Flags That an Unregistered Offering May Be a Scam

Claims of High Returns with Little or No Risk Unregistered Investment Professionals Aggressive Sales Tactics Problems with Sales Documents No Net Worth or Income Requirements

Accredited investor. An individual is considered an accredited investor, if he or she: earned income that exceeded $200,000 (or $300,000 together with a spouse) in each of the prior two years, and reasonably expects the same for the current year, OR

has a net worth over $1 million, either alone or together with a spouse (excluding the value of the person’s primary residence or any loans secured by the residence (up to the value of the residence)).

www.complianceonline.com©2015 Copyright

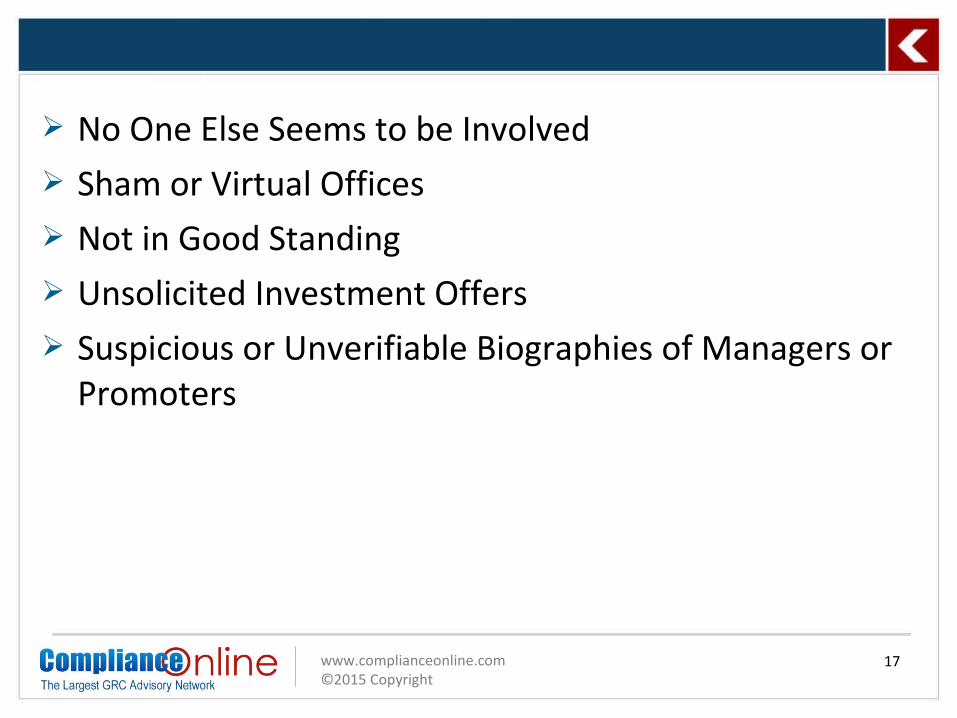

No One Else Seems to be Involved Sham or Virtual Offices Not in Good Standing Unsolicited Investment Offers Suspicious or Unverifiable Biographies of Managers or

Promoters

17

www.complianceonline.com©2015 Copyright

What You Can Do to Help Protect Yourself Check the background of the investment professional. Understand the Investment Strategy Be Aware of Tactics of Con Artists and Fraudsters Ask Questions Additional Resources Available on SEC.gov

For basic investment guidance, see our publication, Ask Questions.

For guidance on choosing an investment professional, review our Investor Bulletin, Top Tips for Selecting a Financial Professional.

To learn more about unregistered securities offerings, read:

Investor Alert: Advertising for Unregistered Securities Offerings Regulation D Offerings Investor Bulletin: Accredited Investors Investor Alert: Private Oil and Gas Offerings

18

www.complianceonline.com©2015 Copyright

Learning Objectives: Examine key information about the characteristics of

securities, securities markets, and securities fraud Demonstrate knowledge about the history of, and

basic concepts underlying, financial markets and investment securities

Recall key information about the development of securities regulation in the United States

Recognize securities fraud schemes that financial institutions or organizations commit against investors

19

www.complianceonline.com©2015 Copyright

Identify the different types of securities fraud schemes that financial advisors or employees commit against financial organizations

Recognize the ways investors commit securities fraud schemes against financial organizations

Identify securities fraud schemes that financial advisors commit against investors

Investigate incidences of securities fraud and report the results of such efforts

20

www.complianceonline.com©2015 Copyright

Who Will Benefit: Bank and financial institution auditors Controllers and corporate managers Forensic and management accountants, accounts

payable and financial analysts Governance, risk management and compliance officers Internal and external auditors, CPAs and CAs Certified fraud examiners and other anti-fraud

professionals Securities Attorneys

21

www.complianceonline.com©2015 Copyright

THANK YOU FOR YOUR ATTENTION

22

For more information on Live Webinars and any Other Training Requirements please email us [email protected] or Call us at this Toll Free Number: 1- 888-717-2436