competitiveness of poultry sector in east and south africa

TRANSCRIPT

Competitiveness of poultry sector in East and South Africa

Peter van Horne

Wageningen University and Research

Webinar, 1 September 2021

Project: Support Agri-Economic Analysis for Africa

Funding by EU / European Commission

▪ Lead by BFAP, South Africa (Tracy Davids)

• Bureau for Food & agricultural Policy

▪ Cooperation with Wageningen UR, Netherlands

▪ Wageningen Economic Research (peter van Horne

▪ Tanzania: Sokoine University of Agriculture

▪ Ghana: University of Ghana

▪ Kenya: Egerton University

Support Agri-Economic Analysis for Africa

Focus:

▪ Support model framework

▪ International Cooperation (research)

▪ Literature review

▪ Poultry production / infra structure

▪ Linkage livestock and feed products

▪ Outlook study

▪

Countries:

- South Africa: details economics

- Tanzania: details economics

- Kenya

- Ghana

Sub Sahara region: poultry meat

• Consumption

+5.4% per year

• Production

+4.2% per year

• Growth in

imports

• In recent years

50% of imports

by SAF, Angola

and Ghana.

Poultry imports: in 4 focus countries

EU-27 exports Imports Exporters of poultry meat:

- Low costs countries

• USA and Brazil

- Leg meat

/USA and EU

2018 2019 2020

Ghana 163 184 214

Philippines 160 216 196

Ukraine 177 178 146

Congo 75 78 101

HongKong 112 94 89

South Africa 84 130 89

Saudi Arabia 82 67 76

Benin 91 69 61

EU-27 export of poultry meat (1000 tonnes)

Consumer preference: poultry

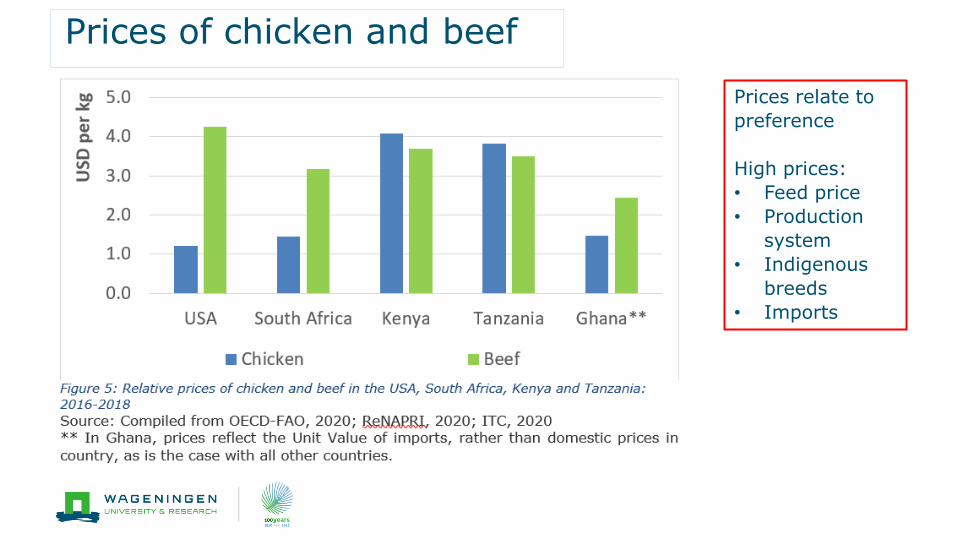

Prices of chicken and beef

Prices relate to

preference

High prices:

• Feed price

• Production

system

• Indigenous

breeds

• Imports

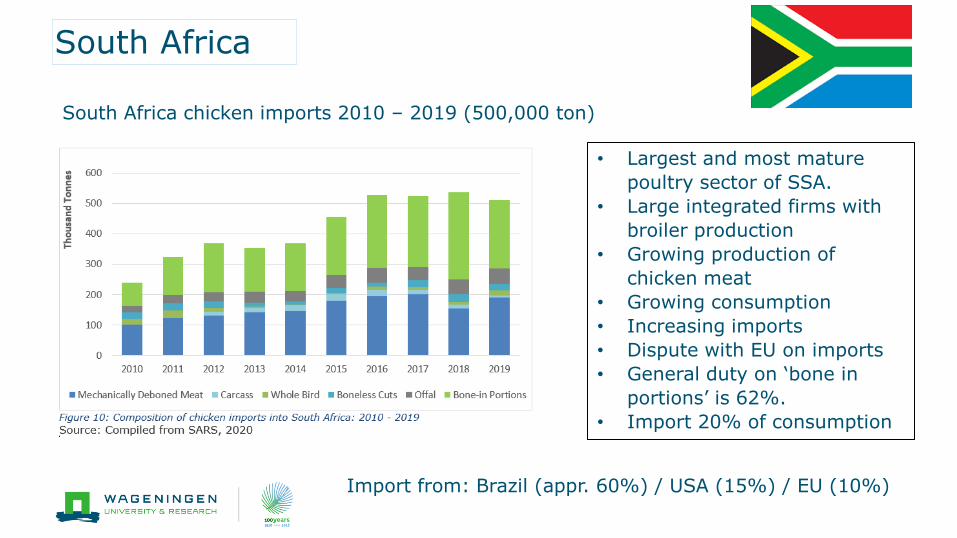

South Africa

• Largest and most mature

poultry sector of SSA.

• Large integrated firms with

broiler production

• Growing production of

chicken meat

• Growing consumption

• Increasing imports

• Dispute with EU on imports

• General duty on ‘bone in

portions’ is 62%.

• Import 20% of consumption

South Africa chicken imports 2010 – 2019 (500,000 ton)

Import from: Brazil (appr. 60%) / USA (15%) / EU (10%)

Kenya

• Poultry is 55% of the

livestock sector

• Poultry is widespread in rural

and peri-urban areas

• Indigenous poultry is main

production system

• Chicken production around

80,000 ton.

• Import low amounts from

Brazil and Uganda.

• General duty is 25%, Duty

free import from EAC (East

Africa community)

Kenya chicken imports 2001 – 2019 (1,500 ton)

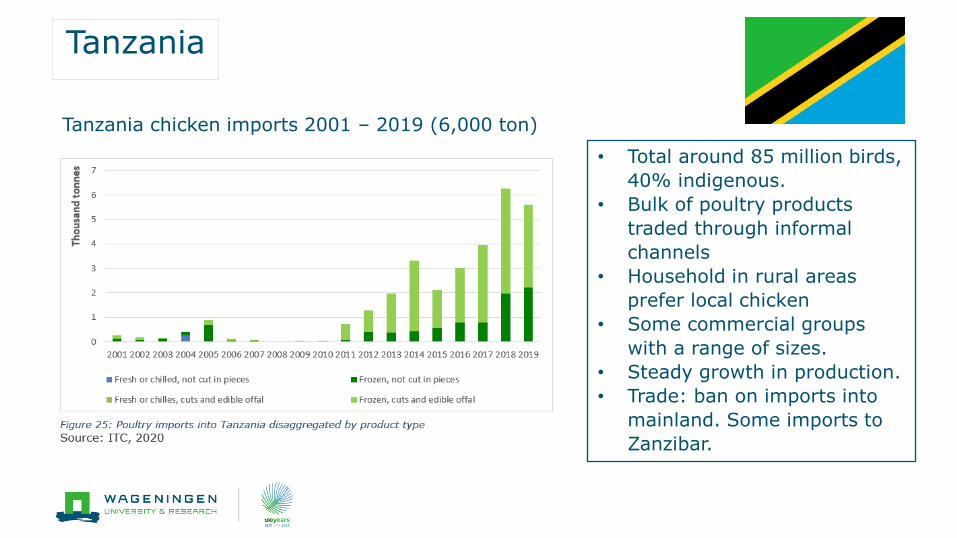

Tanzania

• Total around 85 million birds,

40% indigenous.

• Bulk of poultry products

traded through informal

channels

• Household in rural areas

prefer local chicken

• Some commercial groups

with a range of sizes.

• Steady growth in production.

• Trade: ban on imports into

mainland. Some imports to

Zanzibar.

Tanzania chicken imports 2001 – 2019 (6,000 ton)

Ghana

• In poultry extensive system

dominates production.

• Commercial poultry with two

segments; layers and

broilers.

• In Poultry meat high

competition with imports

• Increasing local production /

increasing imports.

• Imports from USA and EU

• General duty is 35%. Free

trade ECOWAS (econ. Com. of

west Africa states).

• Policy to reduce imports

Ghana chicken imports 2001 – 2019 (250,000 ton)

Competitiveness of Africa poultry sector

• Rising import of poultry products

• Calculation tool of Wageningen UR:

• Production costs at farm level

• Cost of slaughter

• Cost of transport

• Impact of import levies

• Countries in Wageningen model:

• EU countries: NL, Germany, Poland

• Brazil

• USA

• South Africa

• Tanzania (example)

Production cost at farm level (2018) (euro/kg LW)

Production cost after slaughter (2018) (euro/kg CW)

Offer price of the WHOLE BIRD to SAF (euro/kg CW)

No import of whole birds. Only Brazil competitive

Offer price of mixed portions in SAF and TZA (euro/kg product)

SAF is IQF

mixed portion

EU/USA and

Brazil offer leg

meat / bone-

in products

SAF: scenario 1, import levy of 35% (euro/kg product)

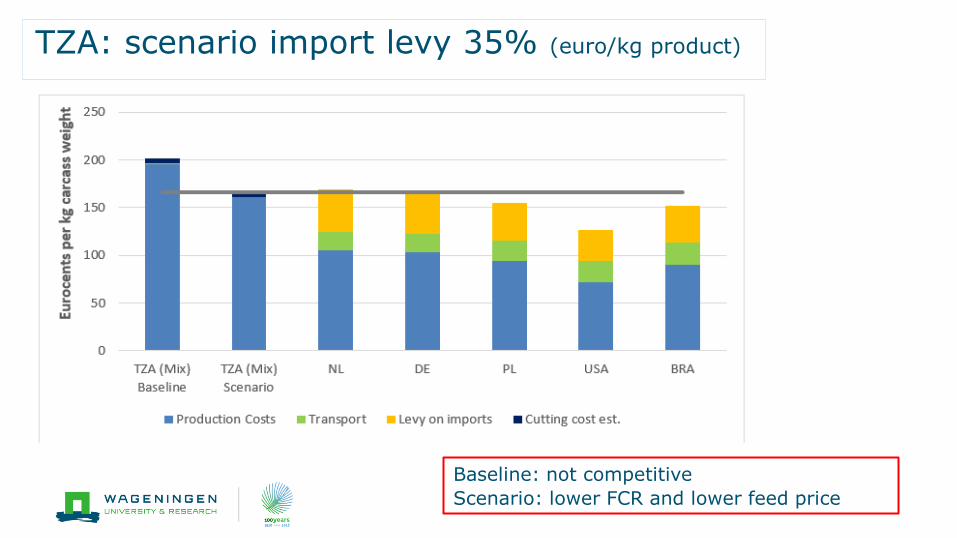

TZA: scenario import levy 35% (euro/kg product)

Baseline: not competitive

Scenario: lower FCR and lower feed price

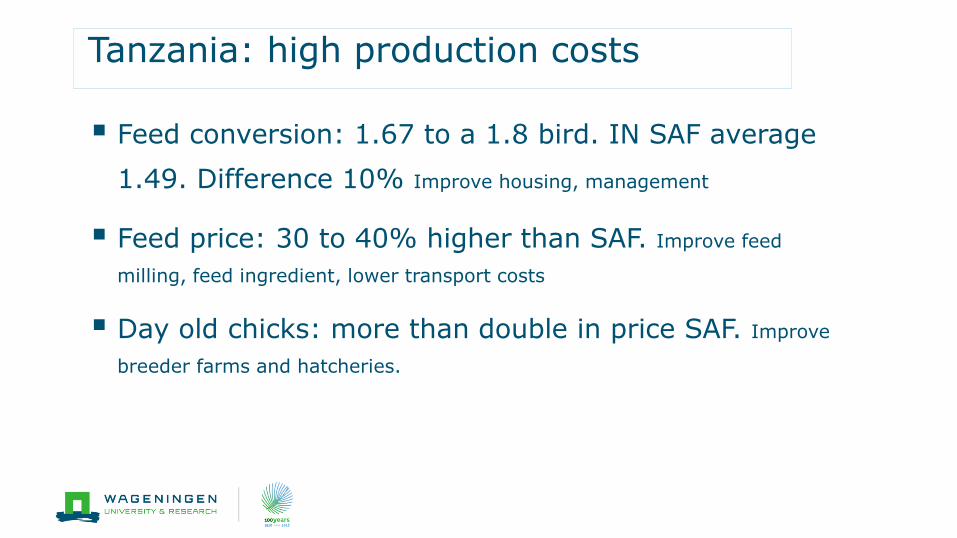

Tanzania: high production costs

▪ Feed conversion: 1.67 to a 1.8 bird. IN SAF average

1.49. Difference 10% Improve housing, management

▪ Feed price: 30 to 40% higher than SAF. Improve feed

milling, feed ingredient, lower transport costs

▪ Day old chicks: more than double in price SAF. Improve

breeder farms and hatcheries.

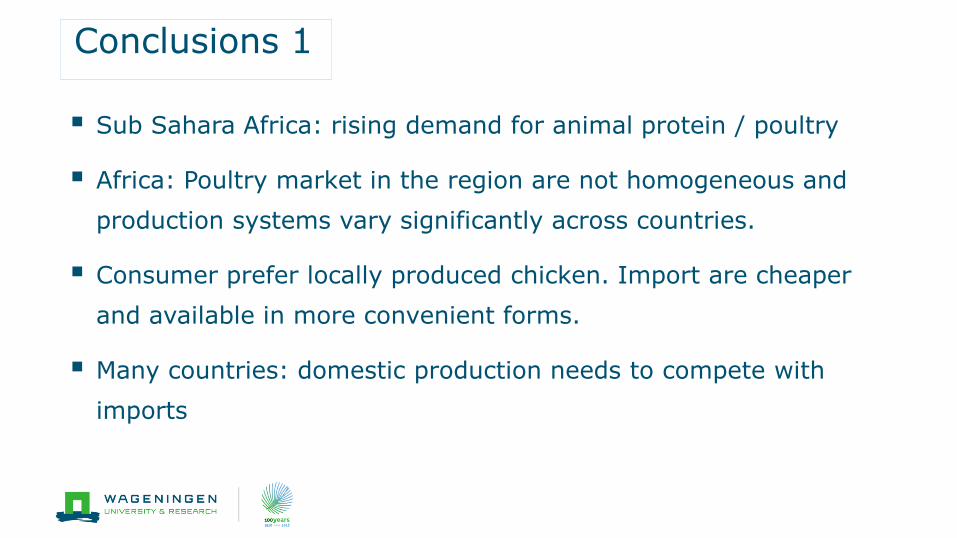

Conclusions 1

▪ Sub Sahara Africa: rising demand for animal protein / poultry

▪ Africa: Poultry market in the region are not homogeneous and

production systems vary significantly across countries.

▪ Consumer prefer locally produced chicken. Import are cheaper

and available in more convenient forms.

▪ Many countries: domestic production needs to compete with

imports

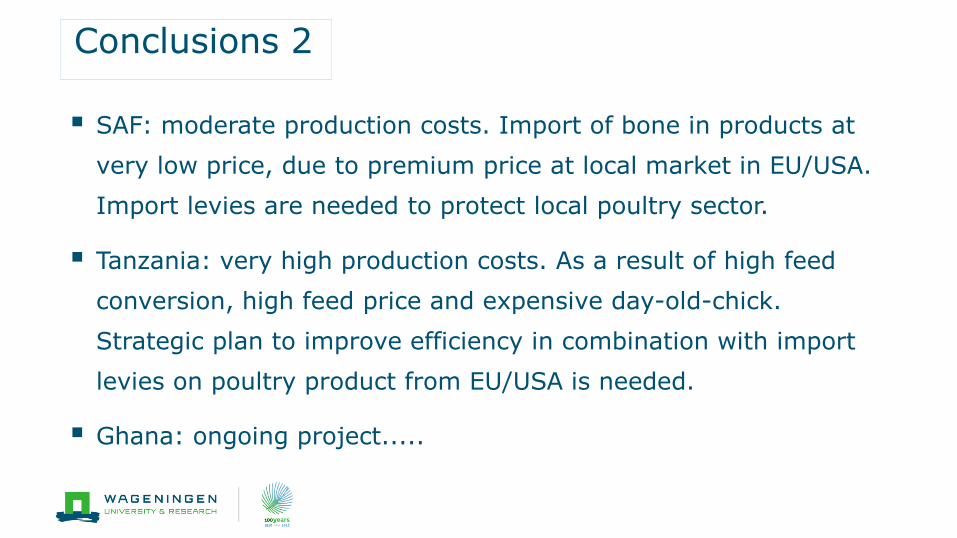

Conclusions 2

▪ SAF: moderate production costs. Import of bone in products at

very low price, due to premium price at local market in EU/USA.

Import levies are needed to protect local poultry sector.

▪ Tanzania: very high production costs. As a result of high feed

conversion, high feed price and expensive day-old-chick.

Strategic plan to improve efficiency in combination with import

levies on poultry product from EU/USA is needed.

▪ Ghana: ongoing project.....