competitiveness: a new economic strategy for peru files/20091130_peru_7abdf2f2-94cc... · latin...

TRANSCRIPT

1 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Professor Michael E. PorterHarvard Business School

Lima, Peru November 30, 2009

This presentation draws on ideas from Professor Porter’s books and articles, in particular, Competitive Strategy (The Free Press, 1980); CompetitiveAdvantage (The Free Press, 1985); “What is Strategy?” (Harvard Business Review, Nov/Dec 1996); “Strategy and the Internet” (Harvard BusinessReview, March 2001); and a forthcoming book. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form orby any means—electronic, mechanical, photocopying, recording, or otherwise—without the permission of Michael E. Porter. Additional information maybe found at the website of the Institute for Strategy and Competitiveness, www.isc.hbs.edu. Version: November 27, 2009

Competitiveness: A New Economic Strategy for Peru

2 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

$0

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

0% 2% 4% 6% 8% 10% 12% 14%

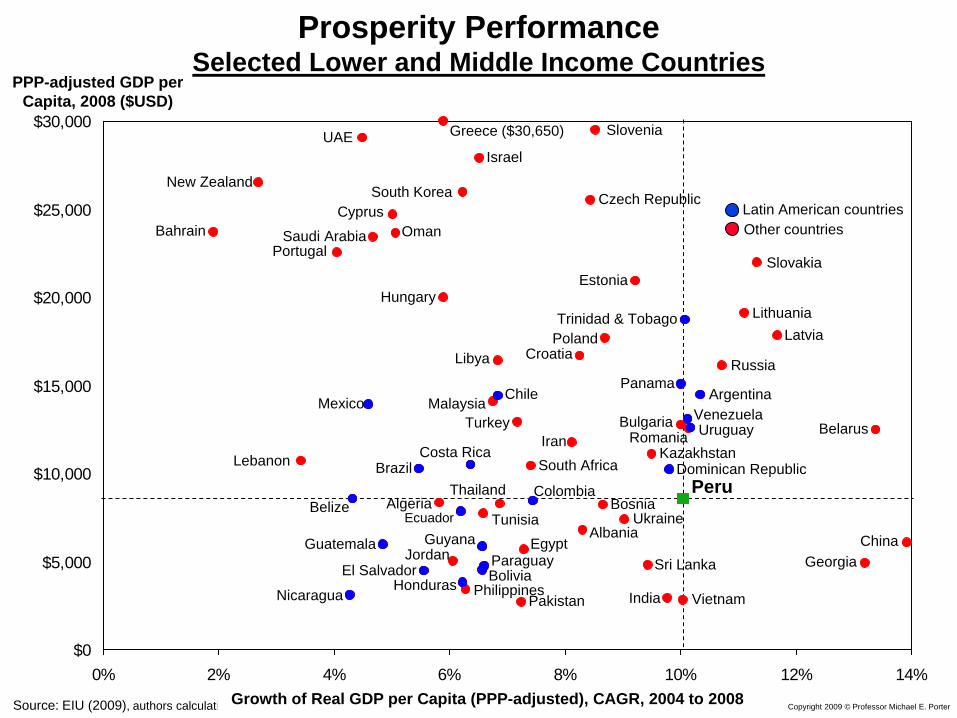

Source: EIU (2009), authors calculations

PPP-adjusted GDP per Capita, 2008 ($USD)

Growth of Real GDP per Capita (PPP-adjusted), CAGR, 2004 to 2008

Bahrain

China

Vietnam

South Africa

Latvia

Oman

Croatia

Czech Republic

Saudi Arabia

Thailand

Estonia

Russia

Costa RicaBrazil

HondurasIndia

Turkey

Egypt

Lithuania

Israel

Slovakia

Hungary

Mexico

Slovenia

Belize

Chile

Other countriesLatin American countries

Prosperity PerformanceSelected Lower and Middle Income Countries

Argentina

South Korea

Poland

Malaysia

Philippines

Sri Lanka

New Zealand

Bulgaria

Dominican RepublicColombia

Romania Uruguay

Ukraine

GuatemalaGeorgia

Bosnia

Jordan

Peru

Paraguay

Nicaragua

Guyana

Panama

BoliviaEl Salvador

Venezuela

KazakhstanBelarus

UAE Greece ($30,650)

Cyprus

Portugal

Libya

Lebanon

Albania

Trinidad & Tobago

Ecuador TunisiaAlgeria

Iran

Pakistan

3 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Peru’s Prosperity Performance

Note: PPP using Geary Khamis calculation methodology. Source: Groningen Growth and Development Centre, Total Economy Database (June 2009)

GDP per Capita(in 1990 PPP US$)

CAGR:

+2.07%

CAGR:

+5.19%

CAGR:

- 0.65%

2008

4 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

0%

2%

4%

6%

8%

10%

12%

14%

-6% -5% -4% -3% -2% -1% 0% 1% 2%

Unemployment PerformanceSelected CountriesUnemployment

Rate, 2008

Change of Unemployment Rate in Percentage Points, 2004 to 2008

Source: EIU (2009)

Improving Deteriorating

Greece

Syria

Tunisia

El Salvador

Ukraine

LithuaniaCzech Rep.

Poland (-8.4%)

Estonia

Mexico

Slovenia

Malaysia

Portugal HungaryPhilippines

China

Turkey

Slovakia

Vietnam

Indonesia

Albania

Thailand

Brazil

RussiaIndia

Chile

Romania

Bulgaria

Egypt

South Africa (22.9%)

Croatia

Saudi Arabia

Costa RicaLatvia

PakistanArgentina

IrelandIsrael

Iran

Other countriesLatin American countries

Colombia

PeruBoliviaEcuadorVenezuela

NicaraguaPanama T&TParaguay

Honduras

Dominican Republic (15.5%)

JordanAlgeria

Kazakhstan

Sri Lanka

CyprusKorea

Uruguay

5 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Poverty RatesPeru, 2001 to 2007% of Population Under

the Poverty Line

0%

10%

20%

30%

40%

50%

60%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Source: Informacion Socio Demografica, from El Instituto Nacional de Estadistica e Informatica (INEI), 2009

6 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

-15% -10% -5% 0% 5% 10% 15% 20%

Export PerformanceSelected Countries

Exports of Goods and Services (% of GDP), 2008

Change in Exports of Goods and Services (% of GDP), 2004 to 2008

Russia

Thailand

Jordan

Saudi Arabia

China

MacedoniaChile

Philippines South Africa

Ireland

India

Bolivia

Brazil

Cambodia

Indonesia

Czech Republic

Slovakia

Turkey

MexicoSri Lanka

Pakistan

Argentina

Vietnam

Malaysia (103.5%)

Ethiopia

Croatia

Source: EIU (2008), authors’ analysis

Egypt

Poland

Slovenia

Peru

Israel

BulgariaBelarus Belize

Romania

Greece

Estonia

Hungary

Lithuania

LatviaUkraine (-17.5%)

Other countriesLatin American Countries

Nicaragua

Honduras

Costa Rica

Trinidad & TobagoParaguay

Panama

Ecuador

Guatemala

Venezuela Uruguay

El Salvador

ColombiaAlbania

AlgeriaCyprus

Kazakhstan

IranLebanon

LibyaMalta

MoroccoPortugalSyria

Tunisia

Georgia

7 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Peru’s Exports By Type of Industry

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

0.70%

0.80%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Processed GoodsSemi-processed GoodsUnprocessed GoodsServicesTOTAL

Source: UNComTrade, WTO (2009)

World Export Market Share (current USD)

8 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

0

2,000

4,000

6,000

8,000

10,000

12,000

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 20070

50

100

150

200

250

300

350Unprocessed Goods Exports (current prices)

Unprocessed Goods Exports (1997 prices)

Price of Copper (current price, $.01/pound)

Peru’s Exports By Type of IndustryPeruvian

Export, $US Commodity Price (US$)

9 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

0%

10%

20%

30%

40%

50%

60%

70%

80%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

Inbound Foreign Investment PerformanceStocks and Flows, Selected Countries

Source: UNCTAD, World Investment Report (2009)

Inward FDI Stocks as % of GDP, Average 2003 - 2007

FDI Inflows as % of Gross Fixed Capital Formation, Average 2003 - 2007

Iran

Russia

Saudi ArabiaTurkey

Slovenia

HungaryVietnam

SlovakiaCzech Republic

Chile

PolandColombia

Estonia

Malaysia

ThailandSouth Africa

Indonesia

Lithuania

India

Brazil

Pakistan

Croatia

El Salvador

Latvia

Nicaragua

Tunisia

China

Mexico

Portugal

Ecuador

Cambodia

Cyprus

Jordan (46.5%, 81.8%)

Paraguay

Costa RicaRomania

Uruguay

Macedonia

Guatemala

BoliviaKazakhstan

Honduras

Other countriesLatin American countries

Bulgaria (69%)

Egypt

Dominican Republic

Belize

Peru

ArgentinaVenezuela

Panama (48.2%)

Trinidad & Tobago

Israel

Libya

Morocco

UAE

Lebanon (6.7%)

Sri Lanka

Georgia

Ukraine

Bosnia

Malaysia

10 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

-30% -20% -10% 0% 10% 20% 30% 40% 50% 60%

Source: USPTO (2009), EIU (2009)

Average U.S. patents per 1 million population, 2004-2008

CAGR of US-registered patents, 2004 – 2008

Innovative CapacityInnovation Output of Selected Countries

Saudi Arabia

RussiaPortugal

Turkey

India

Poland

Czech Republic

China

South Africa

Greece

120 patents =

Argentina

Brazil

Croatia

Bulgaria

PhilippinesEcuador

Chile

ThailandRomania

Peru

VenezuelaMexico

ColombiaUkraine

11 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

The Peruvian Economy in 2009

• Peru has had a long history of instability • Since 2001, Peru has experienced high rates of economic growth

– Recent surge in FDI and exports has been driven by commodities

• Implementation of sound macroeconomic policies has allowed Peru to weather the current global crisis

– Peru’s economy has been one of the most resilient in Latin America

BUT

• Prosperity remains low and large segments of the population lack access to basic needs

• High unemployment and inequality persist• Peru is overly dependent on commodity exports with limited potential to drive job growth

and economic diversification

• Returning to 8 to 9% growth is possible only if Peru can substantially improve competitiveness

• Peru will need an ambitious economic and social strategy, building on the country’s unique competitive advantages

12 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

What is Competitiveness?

• Only competitive businesses can create wealth and jobs

• Nations compete to offer the most productive environment for business

• The public and private sectors play different but interrelated roles in creating a productive economy

• Competitiveness depends on the productivity with which a nation uses its human, capital, and natural resources.

– Productivity sets the sustainable standard of living (wages, returns on capital, returns on natural resources)

– It is not what industries a nation competes in that matters for prosperity, but how productively it competes in those industries

– Productivity in a national economy arises from a combination of domestic and foreign firms

– The productivity of “local” or domestic industries is fundamental to competitiveness, not just that of export industries

13 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

-3% 0% 3% 6% 9%

Comparative Labor ProductivitySelected Countries

Growth of real GDP per employee (PPP-adjusted), 1990 to 2008

Real GDP per employee (PPP adjusted US$), 2008

Source: authors calculation Groningen Growth and Development Centre (2009), EIU (2009)

Peru (Avg. growth 2001to 2008)

Mexico

New Zealand

Australia

Iran

Slovakia

Pakistan

Brazil

Malaysia

Germany

Poland

Slovenia

Argentina

ChinaPhilippines

Russia

Indonesia

Bosnia

Korea

India

Thailand

Japan

Egypt

Belarus

Czech Republic

Georgia

Romania

Saudi Arabia

South Africa

Syria

Spain

Croatia

Chile

Oman

Cambodia

Kazakhstan

UAE

Ukraine

PortugalLithuania

Kuwait

Israel

Jordan

Greece

Hungary

Azerbaijan

Cyprus

Armenia

Albania

Macedonia

Austria

Malta

Estonia

Singapore

Bulgaria

Switzerland

Latvia

Vietnam

Serbia

Turkey

Peru

14 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Macroeconomic Competitiveness

Microeconomic Competitiveness

Sophisticationof Company

Operations andStrategy

Quality of the NationalBusiness

Environment

MacroeconomicPolicies

SocialInfrastructure and PoliticalInstitutions

State of Cluster Development

• Macroeconomic competitiveness creates the potential for high productivity, but is not sufficient

• Productivity ultimately depends on improving the microeconomic capability of the economy and the sophistication of local competition

Determinants of Competitiveness

Natural Endowments

15 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Macroeconomic Competitiveness

Microeconomic CompetitivenessSophistication

of CompanyOperations and

Strategy

Quality of the NationalBusiness

Environment

SocialInfrastructure and PoliticalInstitutions

State of Cluster Development

Natural Endowments

MacroeconomicPolicies

Determinants of Competitiveness

• Fiscal policy: public spending aligned with revenues over time

• Monetary policy: low levels of inflation

• Macroeconomic management: avoiding structural imbalances and cyclical overheating

MacroeconomicPolicy

16 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Determinants of Competitiveness

Macroeconomic Competitiveness

Microeconomic CompetitivenessSophistication

of CompanyOperations and

Strategy

Quality of the NationalBusiness

Environment

SocialInfrastructure and PoliticalInstitutions

State of Cluster Development

Natural Endowments

• Human Development: basic education and health care

• Rule of Law: property rights and due process

• Political Institutions: stable and effective political and governmental processes and organizations

SocialInfrastructure and PoliticalInstitutions

MacroeconomicPolicies

17 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Macroeconomic Competitiveness

Microeconomic CompetitivenessSophistication

of CompanyOperations and

Strategy

Quality of the NationalBusiness

Environment

SocialInfrastructure and PoliticalInstitutions

State of Cluster Development

Natural Endowments

MacroeconomicPolicies

Determinants of Competitiveness

• The internal company skills, capabilities,and managementpractices needed to attain the highest level of productivity and innovation possible

Sophisticationof Company

Operations andStrategy

18 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Determinants of Competitiveness

• The external business environment conditions that allow companies to reach high levels of productivity and innovation

Quality of the National Business

Environment Macroeconomic Competitiveness

Microeconomic CompetitivenessSophistication

of CompanyOperations and

Strategy

Quality of the NationalBusiness

Environment

SocialInfrastructure and PoliticalInstitutions

State of Cluster Development

Natural Endowments

MacroeconomicPolicies

19 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Determinants of Competitiveness

• A critical mass of firms in particular fields,together with specialized skills, infrastructure, and supporting institutions, to support high productivity through efficiencies and synergies

State of Cluster Development

Macroeconomic Competitiveness

Microeconomic CompetitivenessSophistication

of CompanyOperations and

Strategy

Quality of the NationalBusiness

Environment

SocialInfrastructure and PoliticalInstitutions

State of Cluster Development

Natural Endowments

MacroeconomicPolicies

20 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Competitiveness and Poverty Reduction

Social Development

• There is a strong connection between economic and socialdevelopment

• Improving competitiveness and decreasing poverty requires improving the economic and social context simultaneously

Economic Development

21 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Peru’s Competitiveness Profile, 2009ISC Country Competitiveness Model

Macroeconomic Competitiveness (82)

MicroeconomicCompetitiveness (73)

Social Infra-structure and Pol. Institutions (90)

Macroeconomic Policy (69)

Business Environment Quality

(74)

Company Sophistication

(70)

Note: Rank versus 133 countries; overall, Peru ranks 71st in 2008 PPP adjusted GDP per capita and 75th in 2009 Global CompetitivenessSource: Country Competitiveness Model (CCM), Institute for Strategy and Competitiveness, Harvard University (2009)

Peru’s GDP per capita rank is 71st versus 133 countries

22 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Peru’s Macroeconomic Competitiveness

Macroeconomic Policy

• Conservative fiscal policy

23 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Government Budget BalancesSelected Countries

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

1996 1998 2000 2002 2004 2006 2008

Chile

Peru

Argentina

Colombia

Mexico

Brazil

Source: EIU, 2009

Budget Balance(% of GDP)

Ranked by Surplus, 2008

24 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Peru’s Macroeconomic Competitiveness

Macroeconomic Policy

• Conservative fiscal policy

• Sound macroeconomic management

• Stabilization fund

However

• Peru’s macroeconomic position remains overly dependent on commodities and commodity prices

25 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Peru’s Macroeconomic Competitiveness

Macroeconomic Policy

• Conservative fiscal policy

• Sound macroeconomic management

• Stabilization fund

However

• Peru’s macroeconomic position remains overly dependent on commodities and commodity prices

Social Infrastructure and Political Institutions

• Continued problems with corruption

26 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

-20 -15 -10 -5 0 5 10 15 20

Corruption Perception Index, 2007

Note: Ranks only countries available in both years (91 countries total)Source: Global Corruption Report, 2008

Change in Rank, Global Corruption Report, 2007 versus 2001

Rank in Global

CorruptionIndex,2007

91

1 Finland

Canada

Bangladesh

Indonesia

Ireland

Portugal

Egypt

Iceland

Czech Republic

SlovakiaSouth Korea

Latvia

India

Slovenia

Thailand

Switzerland

France

RomaniaTurkey

Estonia

Austria GermanyJapan

Vietnam

China

NorwayUK

MalaysiaLithuania

Colombia

HungaryTaiwan

Spain

Hong Kong

ChileUnited States

South Africa

Mexico

Croatia

Italy

Poland

Brazil

Argentina

Israel

Venezuela

Russia

Uruguay

New ZealandSweden

Tunisia

Peru

Tanzania

Uganda

Senegal

Philippines

Zimbabwe Cote d’Ivoire NigeriaPakistan

GreeceJordan

Ukraine

Panama

Worsening Improving

High corruption

Low corruption

Belgium

Singapore

Netherlands

Botswana

Mauritius

El SalvadorGhana

Dominican RepublicGuatemala

Uzbekistan

Kazakhstan

Honduras

Malawi

Namibia

Kenya

CameroonNicaragua

Moldova

Ecuador

Costa Rica

Bolivia

27 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Peru’s Macroeconomic Competitiveness

Macroeconomic Policy

• Conservative fiscal policy

• Sound macroeconomic management

• Stabilization fund

However

• Peru’s macroeconomic position remains overly dependent on commodities and commodity prices

Social Infrastructure and Political Institutions

• Continued problems with corruption

• Sharp inequality between indigenous groups and other citizens

• Weak education system

• Inadequate health care system, despite some improvements

• Weak legal system and effectiveness of property rights

• Unstable political processes andinstitutions

• Government institutions are inefficient and held in low esteem by the public

28 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Macroeconomic Policy

• Maintain macroeconomic stability

• Broaden the tax base andimprove collections

Social Infrastructure and Political Institutions

• Modernize political and governmental institutions to improve policy formulation and execution

• Tackle corruption at every level of government

• Improve the effectiveness of the legal system

• Improve property rights

• Improve human development– Rapid improvements in education,

health, and nutrition are needed

• Create equal opportunity for all groups

Peru’s Macroeconomic CompetitivenessAction Priorities

29 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Microeconomic Competitiveness: Quality of the Business Environment

Context for Firm

Strategy and Rivalry

Related and Supporting Industries

Factor(Input)

ConditionsDemand

Conditions

• Demanding and sophisticated local customers and needs

– e.g., Strict quality, safety, and environmental standards

– Consumer protection laws

• Many things matter for competitiveness• Successful economic development is a process of successive upgrading, in which the

business environment improves to enable increasingly sophisticated ways of competing

• Efficient access to high quality business inputs

– Human resources– Capital availability– Physical infrastructure– Administrative infrastructure (e.g.

registration, permitting, transparency)– Scientific and technological

infrastructure– Efficient utilization of natural

endowments

• Availability of suppliers, related industries, and supporting institutions

Open and vigorous local competition

– Openness to foreign competition– Competition laws

• Local rules and incentives that encourage investment and productivity

– e.g. incentives for capital investment, intellectual property protection, corporate governance standards

30 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

WEAKNESSESSTRENGTHS

Peru’s Business Environment Overall Strengths and Weaknesses

Trade and Investment Liberalization• Openness to foreign investment• Low restrictions on capital flows• Simplification of custom procedures• Low trade barriers• Improvements in investor protectionsImproving Financial Markets• Soundness of banks• Improving financial marketIT Infrastructure• Good quality of telecom infrastructure• Sound IT policiesOther• Good management training• Improving sophistication of local buyers• Efforts to strengthen competition policy

Physical Infrastructure• Low quality of air, transport and port

infrastructure• Inadequate electricity supplyWorkforce Development and Training• Poor quality of the higher education system• Low skill level of the labor force • Limited availability of scientists and

engineers Competitive Context• Low intensity of local competition• Difficulty in business formation• Burdensome government regulations• Rigidity of employment• Weak intellectual property protection• High informality in the economyInnovation Infrastructure• Limited technological capacity• Weak university-industry research

collaboration• Low patenting rates

31 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

0

20

40

60

80

100

120

Ease ofDoing

Business

GettingCredit

ProtectingInvestors

RegisteringProperty

PayingTaxes

TradingAcrossBorders

Closing aBusiness

EmployingWorkers

Starting aBusiness

EnforcingContracts

Dealingwith

Licenses

Ease of Doing BusinessPeru, 2009

Ranking, 2009 (of 183 countries)

Source: World Bank Report, Doing Business (2009/10)

Favorable Unfavorable

Peru’s per capita GDP rank: 72

32 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Peru’s Business EnvironmentAction Priorities

• Improve physical infrastructure

• Create an effective system for workforce training

• Upgrade higher education

• Encourage entrepreneurship and SME business formation

– Simplify business formation

– Reduce tax burden and labor market rigidities

– Address other causes of informality

– Strengthen financing for SMEs

• Improve environmental standards

• Develop innovation infrastructure

– Upgrade technology standards in key clusters of the economy

33 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Sources: HBS student team research (2003) - Peter Tynan, Chai McConnell, Alexandra West, Jean Hayden

Hotels

Attractions andActivities

e.g., theme parks, casinos, sports

Airlines, Cruise Ships

Travel agents Tour operators

Restaurants

PropertyServices

MaintenanceServices

Government agenciese.g. Australian Tourism Commission,

Great Barrier Reef Authority

Educational Institutionse.g. James Cook University,

Cairns College of TAFE

Industry Groupse.g. Queensland Tourism

Industry Council

FoodSuppliers

Public Relations & Market Research

Services

Local retail, health care, andother services

Souvenirs, Duty Free

Banks,Foreign

Exchange

Local Transportation

Microeconomic Competitiveness: Cluster DevelopmentTourism Cluster in Cairns, Australia

34 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Government Agencies, NGOs & Industry Associations

Education, Research & Quality Standards Organizations

FlowerFarming

Post-HarvestHandling;

Transport toMarket

FreightForwarders

Clearing andForwarding

Agents

Air Carriers(Commercial /

Charters)

PlantstockTrade & Industry Associations

Kenya Flower Council (KFC)Fresh Produce Exporters Association of Kenya (FPEAK)

Regional Growers Associations e.g., North & South Kinangop; Lake Naivasha, etcGreenhouse;Shading

Structures

Pre-CoolingTechnology

Irrigationtechnology

Grading /Packaging Sheds

Post-HarvestCooling

Technology

AgriculturalCluster

HorticulturalCluster

(Fruits & Vegetables)

Public universities with post graduate degrees inhorticulture:

University of Nairobi; Jomo Kenyatta University of Agriculture & Technology

Horticultural Crops Development Authority (HCDA)Government Export Policies targeting Horticulture

Government Policy for Revitalizing Agriculture; National Export Strategy; ExportPromotion Council (EPC)

Fertilizers,pesticides,herbicides

Research Institutions:Kenya Agricultural Research Institute (KARI)

International Center for Insect Physiology and Ecology (ICIPE)

RefrigeratedTrucks

Quality & Standards:EUREGAP Standard (UK & Dutch Supermarkets)

Kenya Plant Health Inspectorate Services (KEPHIS)

Non-Governmental OrganizationsThe Rural Enterprise Agri-Business Promotion Project (USAID, CARE, IFAD)

Horticultural Produce Handling Facilities Project (JBIC)

Packaging &LabelingMaterials

TourismCluster

Cluster in Developing CountriesKenya’s Cut Flower Cluster

Sources: Student team research by Kusi Hornberger, Nick Ndiritu, Lalo Ponce-Brito, Melesse Tashu, and Tijan Watt, Microeconomics of Competitiveness Course, 2007

35 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

The Australian Wine ClusterHistory

1955

Australian Wine Research Institute founded

1970

Winemaking school at Charles Sturt University founded

1980

Australian Wine and Brandy Corporation established

1965

Australian Wine Bureau established

1930

First oenology course at Roseworthy Agricultural College

1950s

Import of European winery technology

1960s

Recruiting of experienced foreign investors, e.g. Wolf Bass

1990s

Surge in exports and international acquisitions

1980s

Creation of large number of new wineries

1970s

Continued inflow of foreign capital and management

1990

Winemaker’s Federation of Australia established

1991 to 1998

New organizations created for education, research, market information, and export promotions

Source: Michael E. Porter and Örjan Sölvell, The Australian Wine Cluster – Supplement, Harvard Business School Case Study, 2002

36 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

The Evolution of Regional EconomiesSan Diego

U.S. Military

CommunicationsEquipment

Sporting Goods

Analytical Instruments

Power Generation

Aerospace Vehiclesand Defense

Transportationand Logistics

Information Technology

1910 1930 1950 19901970

Bioscience Research Centers

Climate and

Geography

Hospitality and Tourism

Medical Devices

Biotech / Pharmaceuticals

Education andKnowledge Creation

37 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

FurnitureBuilding Fixtures,

Equipment & Services

Fishing & Fishing Products

Hospitality & TourismAgricultural

Products

Transportation & Logistics

Clusters and Economic DiversificationLinkages Across Clusters

Plastics

Oil & Gas

Chemical Products

Biopharma-ceuticals

Power Generation

Aerospace Vehicles &

Defense

Lightning & ElectricalEquipment

Financial Services

Publishing & Printing

Entertainment

Information Tech.

Communi-cations

Equipment

Aerospace Engines

Business Services

DistributionServices

Forest Products

Heavy Construction

Services

ConstructionMaterials

Prefabricated Enclosures

Heavy Machinery

Sporting & Recreation

Goods

Automotive

Production Technology

Motor Driven Products

Mining & Metal Manufacturing

Apparel

Leather & Related Products

Jewelry & Precious Metals

Textiles

Footwear

Processed Food

Tobacco

Medical Devices

Analytical InstrumentsEducation &

Knowledge Creation

Note: Clusters with overlapping borders or identical shading have at least 20% overlap(by number of industries) in both directions.

38 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

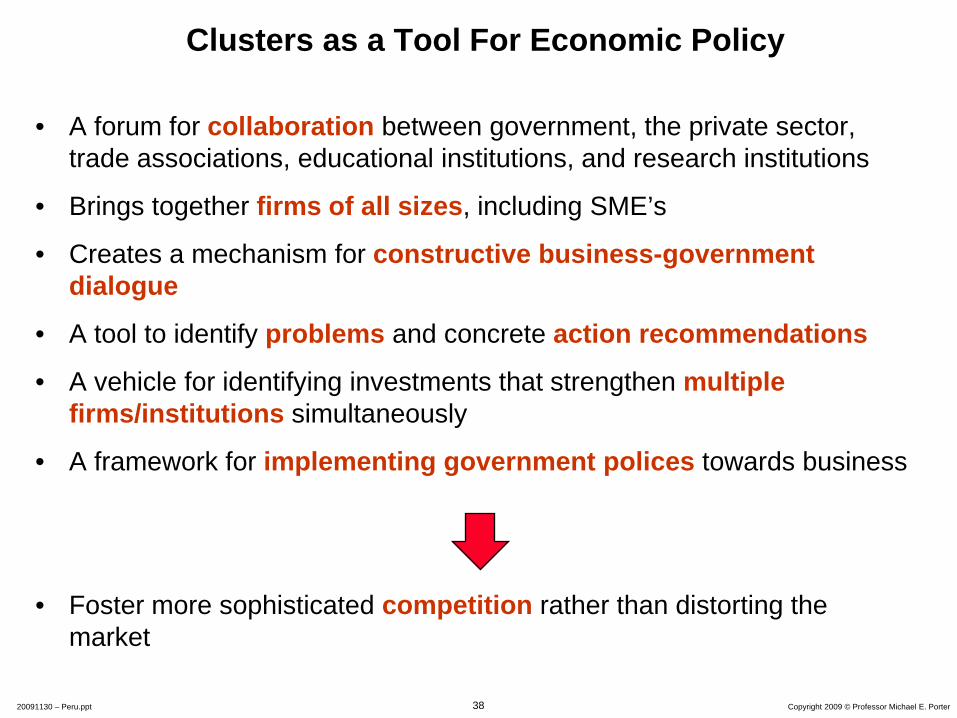

Clusters as a Tool For Economic Policy

• A forum for collaboration between government, the private sector, trade associations, educational institutions, and research institutions

• Brings together firms of all sizes, including SME’s

• Creates a mechanism for constructive business-government dialogue

• A tool to identify problems and concrete action recommendations

• A vehicle for identifying investments that strengthen multiple firms/institutions simultaneously

• A framework for implementing government polices towards business

• Foster more sophisticated competition rather than distorting the market

39 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

-0.4% -0.2% 0.0% 0.2% 0.4% 0.6%

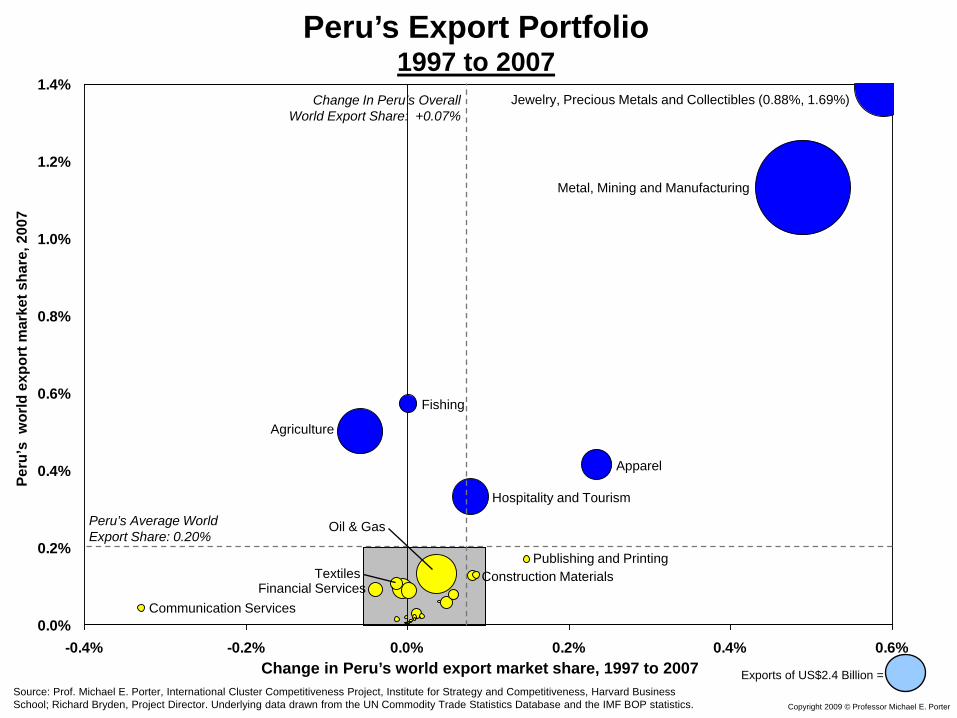

Peru’s Export Portfolio1997 to 2007

Change in Peru’s world export market share, 1997 to 2007Source: Prof. Michael E. Porter, International Cluster Competitiveness Project, Institute for Strategy and Competitiveness, Harvard Business School; Richard Bryden, Project Director. Underlying data drawn from the UN Commodity Trade Statistics Database and the IMF BOP statistics.

Peru

’s w

orld

exp

ort m

arke

t sha

re, 2

007

Change In Peru’s Overall World Export Share: +0.07%

Peru’s Average World Export Share: 0.20%

Exports of US$2.4 Billion =

Hospitality and Tourism

Fishing

Agriculture

Construction MaterialsFinancial Services

Publishing and Printing

Jewelry, Precious Metals and Collectibles (0.88%, 1.69%)

Metal, Mining and Manufacturing

Apparel

Textiles

Communication Services

Oil & Gas

40 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

0.00%

0.05%

0.10%

0.15%

0.20%

-0.06% -0.04% -0.02% 0.00% 0.02% 0.04% 0.06% 0.08% 0.10%

Peru’s Export Portfolio1997 to 2007

Change in Peru’s world export market share, 1997 to 2007Source: Prof. Michael E. Porter, International Cluster Competitiveness Project, Institute for Strategy and Competitiveness, Harvard Business School; Richard Bryden, Project Director. Underlying data drawn from the UN Commodity Trade Statistics Database and the IMF BOP statistics.

Peru

’s w

orld

exp

ort m

arke

t sha

re, 2

007

Construction Materials

Transportation and Logistics

Biopharmaceuticals

Production Technology

Chemical Products

Oil and Gas

Prefabricated Enclosures and StructuresSport

Business Services

Financial Services

Heavy MachineryMotor Driven Products

Communications Equipment

Furniture

Footwear

Leather and Related Products

Forest ProductsBuilding Fixtures and Equipment

Plastics

Processed Foods

Textiles

Exports of US$2.4 Billion =

Power and Power Generation Equipment

41 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

-1.5% -1.0% -0.5% 0.0% 0.5% 1.0%

Malaysia’s Export Portfolio1997 to 2007

Change in Malaysia’s world export market share, 1997 to 2007Source: Prof. Michael E. Porter, International Cluster Competitiveness Project, Institute for Strategy and Competitiveness, Harvard Business School; Richard Bryden, Project Director. Underlying data drawn from the UN Commodity Trade Statistics Database and the IMF BOP statistics.

Mal

aysi

a’s

wor

ld e

xpor

t mar

ket s

hare

, 200

7

Change In Malaysia’s Overall World Export Share: -0.20%

Malaysia’s Average World Export Share: 1.24%

Exports of US$9.3 Billion =

Hospitality and Tourism

Fishing & Fish Products

Agriculture

Construction Materials

Publishing and Printing

Jewelry, Precious Metals and CollectiblesMetal, Mining and Manufacturing

Apparel

Textiles

Communication Services

Oil & Gas

Transportation and Logistics

Biopharmaceuticals

Production Technology

Chemical Products

Prefabricated Enclosures and Structures

SportBusiness Services (-2.36%)

Financial Services

Heavy Machinery

Motor Driven Products

Communications Equipment

Furniture

Footwear

Forest Products

Building Fixtures and Equipment

Plastics

Processed Foods

Power and Power Generation Equipment

Information Technology (6.46%)

Analytical Instruments

Lighting and Electrical Equipment

Entertainment and Reproduction Equipment (2.19%, 3.09%)

Construction Services

Medical Devices

Marine Equipment

Aerospace Vehicles and Defense

Automotive

42 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

FurnitureBuilding Fixtures,

Equipment & Services

Fishing & Fishing Products Hospitality

& TourismAgricultural

ProductsTransportation

& Logistics

Share of World Exports by ClusterPeru, 2007

Plastics

Oil & Gas

Chemical Products

Biopharma-ceuticals

Power Generation

Aerospace Vehicles &

Defense

Lightning & ElectricalEquipment

Financial Services

Publishing & Printing

Information Tech.

Communi-cations

Equipment

Business Services

DistributionServices

Forest Products

Heavy Construction

Services

ConstructionMaterials

Prefabricated Enclosures

Apparel

Leather & Related Products

Jewelry & Precious

Metals

Textiles

Footwear

Processed Food

Tobacco

Medical Devices

Analytical InstrumentsEducation &

Knowledge Creation

Note: Clusters with overlapping borders have at least 20% overlap (by number of industries) in both directions.

Marine Equipment

Aerospace Engines

Heavy Machinery

Sporting & Recreation

Goods

Automotive

Production Technology

Motor Driven Products

Mining & Metal Manufacturing

0.2% - 0.5%

0.5% - 1.0%

> 1.0%

Enter-tainment

World Market Share

43 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

FurnitureBuilding Fixtures,

Equipment & Services

Fishing & Fishing Products Hospitality

& TourismAgricultural

ProductsTransportation

& Logistics

Share of World Exports by ClusterMalaysia, 2007

Plastics

Oil & Gas

Chemical Products

Biopharma-ceuticals

Power Generation

Aerospace Vehicles &

Defense

Lightning & ElectricalEquipment

Financial Services

Publishing & Printing

Information Tech.

Communi-cations

Equipment

Business Services

DistributionServices

Forest Products

Heavy Construction

Services

ConstructionMaterials

Prefabricated Enclosures

Apparel

Leather & Related Products

Jewelry & Precious Metals

Textiles

Footwear

Processed Food

Tobacco

Medical Devices

Analytical InstrumentsEducation &

Knowledge Creation

Note: Clusters with overlapping borders have at least 20% overlap (by number of industries) in both directions.

Marine Equipment

Aerospace Engines

Heavy Machinery

Sporting & Recreation

Goods

Automotive

Production Technology

Motor Driven Products

Mining & Metal Manufacturing

1.24% - 1.75%

1.75% - 2.25%

> 2.25%

Enter-tainment

World Market Share

44 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

State of Cluster Development in Peru

• Peru has strengths in several clusters, including mining, fishing, agribusiness, tourism, jewelry and apparel

• Peru’s clusters are based heavily on natural endowments, with limited further upgrading

• Peru’s clusters are shallow, with weak supplier bases and supporting institutions

• The limited cluster development efforts underway in Peru suffer from poor coordination between the private and public sectors

• Clusters are so far an unexploited dimension of economic policy at the national and regional levels

45 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Cluster Development in PeruAction Priorities

• Adopt cluster development as a central tool for organizing business development and implementation of economic policies supporting businesses

• Use cluster development to encourage value-add upgrading within existing clusters

– Promote spillovers and synergies to upgrade local economies

• Apply a cluster based approach to economic diversification

46 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Develop Related Clusters

Upgrade Existing Export Products and Services

Clusters and Economic Diversification

Deepen Existing Clusters

Turn Products Into Clusters• Local firms• MNCs

47 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

-0.8% -0.6% -0.4% -0.2% 0.0% 0.2% 0.4% 0.6% 0.8%

Change in Subcluster’s share of World Exports, 1997 – 2007

Subc

lust

er’s

sha

re o

f Wor

ld e

xpor

ts, 2

007

Peru’s Agriculture Cluster, 1997 – 2007 Exports by Subcluster

Vegetables and Fruits

Subcluster Overall Export Share: 0.50%

Overall change in Subcluster World Export Share : - 0.06%

Source: Prof. Michael E. Porter, Cluster Mapping Project, Institute for Strategy and Competitiveness, Harvard Business School; Richard Bryden, Project Director.Exports of US$200 million =

Fertilizers

Coffee, Tea, Cocoa and Spices

Meat and Related Products

Miscellaneous Vegetable Materials (4.54%, 1.91%)

Crude Fertilizers

Oils and Fats

Sugars, Molasses and HoneyFeeding Materials

GrainsPlants and Flowers

Specialty Agricultural Products

48 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

-0.5% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5%

Change in Subcluster’s share of World Exports, 1997 – 2007

Subc

lust

er’s

sha

re o

f Wor

ld e

xpor

ts, 2

007

Peru’s Metal Mining and Manufacturing Cluster, 1997 – 2007 Exports by Subcluster

Other Metals

Subcluster Overall Export Share: 1.13%

Overall change in Subcluster World Export Share : + 0.49%

Source: Prof. Michael E. Porter, Cluster Mapping Project, Institute for Strategy and Competitiveness, Harvard Business School; Richard Bryden, Project Director.Exports of US$1.5 billion =

Iron and Steel

Copper

Wire and Springs

Iron and Steel Mill and Foundry Products

Nonferrous Metal Processing

Fabricated Metal Products

49 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Cluster Development in PeruAction Priorities

• Adopt cluster development as a central tool for organizing business development and implementation of economic policies supporting businesses

• Use cluster development to encourage value-add upgrading within existing clusters

– Promote spillovers and synergies to upgrade local economies

• Apply a cluster based approach to economic diversification

• Leverage clusters to attract FDI and facilitate integration with the global economy

• Use cluster initiatives to engage the private sector in more effective collaboration with government at the national and regional levels

– Cluster development is an effective approach to promote private sector-led growth

– Create Institutions for Collaboration (e.g., trade associations) to organize cluster participants

50 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Geographic Influences on Competitiveness

Regions and Cities

Nation

51 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Regions and Competitiveness

• Economic performance varies significantly across sub-national regions (e.g., provinces, states, metropolitan areas)

• Many essential levers of competitiveness reside at the regional level• Region’s specialize in different sets of clusters

52 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Specialization by Cluster, Turkish Regions 2007

Note: Source: European Cluster Observatory, 2009

IstanbulTextilesLeather and ApparelDistribution ServicesJewelry

Bati AnadoluFurnitureConstruction MaterialsDistribution ServicesAerospace

AkdenzizTextilesHospitality and TourismApparelDistribution Services

Orta AnadoluFurnitureTextilesAgricultural ProductsMetal Mining and Manufacturing

Bati KaradenizTobaccoApparelMetal Mining and ManufacturingForest Products

Dogu KaradenizFood ProcessingDistribution ServicesFurnitureForest Products

Ortadogu AnadoluTextilesAgricultural ProductsApparelDistribution Services

Guneydogu AnadoluTextilesTobaccoOil and GasFood Processing

Bati MarmaraApparelTextilesChemicalsConstruction Materials

Dogu MarmaraTextilesAutomotiveApparelFurniture

EgeTobaccoTextilesConstruction MaterialsApparel

Kuzeydogu AnadoluAgricultural ProductsFootwearDistribution ServicesHospitality and Tourism

53 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Regions and Competitiveness

• Economic performance varies significantly across sub-national regions (e.g., provinces, states, metropolitan areas)

• Many essential levers of competitiveness reside at the regional level• Region’s specialize in different sets of clusters• Cluster strength directly impacts regional performance• Each region requires its own distinctive competitiveness agenda• Improving competitiveness requires effective policy collaboration

between regions and the national government

• Decentralization of economic policy is especially important in larger countries to foster regional specialization, internal competition, and greater government accountability

54 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Competitiveness of Peru’s Regions

• Strong disparities exist across Peruvian regions in business environment, innovative capacity, and economic performance

55 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

0% 1% 2% 3% 4% 5% 6% 7% 8% 9% 10%

Prosperity PerformancePeru’s Regions

GDP per Capita, 2008 (1994 New Peruvian Soles)

Growth in GDP per Capital (CAGR), 2001 to 2008

Peru’s Weighted Average: 6.0%

Source: Fuente: Instituto Nacional de Estadistica e Informatica - Dirección Nacional de Cuentas Nacionales

Peru’s Weighted Average: 6,513

Ayachucho

Areguipa

HuancavelicaCusco

La Libertad

Lima

Moquegua

Ica

PiuraAmazonas

Apurimac

Ancash

San Martin

TumbesLambayeque

Madre de Dios

Ucayali

Puno

Tacna

Pasco

Loreto

Huanuco

Cajamarca

Junin

56 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Competitiveness of Peru’s Regions

• Strong disparities exist across Peruvian regions in business environment, innovative capacity, and economic performance

• Decentralization remains incomplete and has produced some social tension and unrest

• There is weak planning, design, andimplementation capacityat the local level

• Sub-national governments are highly dependent on transfers from the central government

57 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Peru’s RegionsAction Priorities

• Continue decentralization of responsibilities and resources to sub-national governments

• Improve the capacity of local governments to plan, design and implement development polices

• Improve national-regional collaboration to implement regional programs

• Adopt specific steps to reduce corruption at the regional level• Improve physical connections among regions to support

economic and social integration• Promote greater linkages between resource clusters and

regional economies• Address the underlying causes of inequality between the

highland, coastal and Amazon regions– Strengthen human development in the poorer highland regions

58 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Geographic Influences on Competitiveness

Neighboring Countries

Regions and Cities

Nation

59 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Economic Coordination with Neighboring Countries

60 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Competitiveness and the Neighborhood

• Opening trade and investment among neighbors fuels growth and specialization– A country’s neighbors are its most natural trading and investment partners

– The most natural path for internationalization by local firms is the neighborhood

– Open trade and investment make each country a more attractive location for foreign investment

• Economic coordination with neighbors drives improvements in the business environment– Capturing synergies in policy and infrastructure

– Gaining greater clout in international negotiations

• External agreements help overcome domestic political barriers to reform

61 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

• Eliminating trade and investment barriers within the region

• Simplifying and harmonizing cross-borderregulations and paperwork

• Coordinatinganti-monopoly and fair competition policies

• Opening governmentprocurementwithin the region Harmonizing environmental standards

• Harmonizing product safetystandards

• Establishing reciprocal consumerprotection laws

• Improving the efficiency of the regional transportationnetwork

• Creating an efficient energy network

• Enhancing regional communicationsand connectivity

• Harmonizing administrativerequirements for businesses

• Linking financialmarkets

• Facilitating the movement of students for higher education

• Facilitating cross-border cluster development

– e.g., Supplier networks

– Transport & Logistics

– Quality standards

Factor Conditions

Context for Strategy

and Rivalry

Related and Supporting Industries

Demand Conditions

Economic Integration Among NeighborsCapturing Synergies

Macroeconomic Competitiveness

• Coordinating macroeconomicpolicies

• Coordinating programs to improve securityand public safety

62 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Peru and the Neighborhood

Assessment• Peru remains a relatively isolated country for geographic reasons• Peru has weak relations with some of its neighbors• Peru has taken some positive steps to improve relations with some

neighbors• Peru’s recent trade liberalization program, including with the U.S. and

China, has created significant opportunities for new economic linkages with neighbors

Action Agenda• Economic coordination with neighboring countries is an important

tool in economic development• Peru can take a proactive leadership role in promoting trade

liberalization efforts with particular neighbors and the region• Peru can be a platform for South American firms seeking to access

the U.S. and Asian markets• Leverage inbound and outbound FDI with neighbors to upgrade

local competitiveness

63 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

• A prioritized agenda to create a uniquecompetitive position for a country or region

• Implementing best practices in each policy area

• There are a huge number of policy areas that matter

• No country can or should try to make progress in all areas simultaneously

PolicyImprovement

EconomicStrategy

The Need for an Economic Strategy

64 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

National Value Proposition

The Need for an Economic Strategy

Refining Unique Strengths Addressing Crucial Constraints

• What elements of the business environment and institutional context can be unique strengths relative to peers/neighbors?

• What existing and emerging clusterscan be developed?

• What are the crucial weaknesses and constraints that must be addressed to achieve parity with peer countries and allow the country to move to the next level?

• What are the distinctive competitive assets of the nation’s economy given its location, legacy, rate of progress, existing strengths, and potential strengths?

– What unique value as a business location?– In what types of fields / clusters?– What roles with neighbors, the broader region, and the wider world?

• Priorities and sequencing are a necessity in economic development

65 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Toward a Peruvian Economic StrategyImplications

Reduce and Eliminate Corruption

Implement Next Stage Regulatory Reforms to Improve the Business Environment

Improve the Quality of Education and Workforce Training

Unique Strengths

• Abundant natural endowments

• Vast biodiversity and ecosystems

• Central location in South America

• Young, hard working population

• Rich culture and history• Legacy of domestic

collaboration to overcome obstacles

• Open to FDI and capital flows

• Privileged access to major foreign markets (United States, China, etc.)

Foster Cluster Development Around Resource Strengths

Upgrade Ground, Air and Port Transportation Infrastructure to Connect Peruvian Regions with Neighbors and the World

Create New, More Stable Effective Political Institutions

• Upgrade Peru’s competitive assets to achieve high rates of sustainableeconomic growth while improving welfare of the poor

66 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Accelerating Poverty Reduction in Peru

Increase CompetitivenessReduce Poverty

67 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

The Process of Economic DevelopmentShifting Roles and Responsibilities

Old Model

• The central government drives economic development through policy decisions, spending and incentives

New Model

• Economic development is a collaborative process involving government at multiple levels, companies, educational and research institutions, and private sector organizations

• Competitiveness must be a bottom-up process in which many individuals, companies, and institutions take responsibility and act

68 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Organizing for Competitiveness in PeruAssessment

• Peru has weak coordination among government ministries and agencies responsible for improving competitiveness

– Across different ministries to align policies– Across geographic levels of government

• The National Council on Competitiveness was created in 2002, a positive step, but it has had limited impact

• There are few competitiveness initiatives at the regional level to mobilize strategic thinking and drive action

• The private sector has limited engagement in competitiveness development

69 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Revitalizing Peru’s Organization to Drive CompetitivenessAction Agenda

• Create an effective coordination structure within government across ministries and agencies

• Restart the National Council on Competitiveness to build consensus on an overall economic strategy and track implementation

– The council will require strong private sector leadership

• Create Regional Competitiveness Councils to drive consensus on state plans and monitor implementation

– Involve representatives from the private, public and academic sectors as well as federal government participation

• The private sector must assume a catalytic role in economic strategy formulation and implementation

70 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

• There is an inevitable link between business and society• A healthy business depends on a healthy community to create

demand for its products and provide a supportive business environment

• A healthy society depends on competitive companies that can create jobs, support high wages, build wealth, buy local goods, and pay taxes

• There is a long-term synergy between economic and social objectives

Integrating Business and the Society

Social Objectives

Economic Objectives

71 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Competitiveness and Social Issues

Company Productivity

Energy Use

Water Use

Employee Health

Gender Equity

Worker Safety

Worker Education and

SkillsPoverty in the Company’sCommunities

EnvironmentalImpact

72 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Corporate Role in CompetitivenessThe Concept of Shared Value

• Find the points of convergence between economic and social objectives, not assumed tradeoffs or the need for redistribution

– These points of convergence are growing

• Achieving shared value requires new thinking, new technologies, and new approaches to management

• Shared value opportunities are even greater in developing countries

• Shared value thinking applies equally to NGOs and governments

Shared Value: Policies and practices that enhance the competitiveness of a company while simultaneously advancing economic and social conditions in the communities in which it operates

73 Copyright 2009 © Professor Michael E. Porter20091130 – Peru.ppt

Corporate Role in CompetitivenessAction Agenda

• Organize the private sector to have a collective voice in competitiveness

• Participate actively in national and regional competitiveness initiatives

• Inform government on business needs and constraints bearing on company and cluster development

• Nurture local suppliers and attract foreign suppliers

• Work closely with local educational and research institutions to improve their quality and create specialized programs addressing the cluster’s needs

• Collaborate with other companies to enhance competitiveness through trade associations and other mechanisms

• Focus corporate social responsibility initiatives on enhancing the business environment