comparison of motor insurance in india and china

TRANSCRIPT

COMPARISON OF MOTOR

INSURANCE IN INDIA AND

CHINA

PREETHI.A

II MBA

BANKING & INSURANCE

INTRODUCTION

Focus of insurers in 2015, it is “technology.”

Investing in digital platforms

Consumers to better shop for insurance

Making products more transparent

Easier-to-understand and compare.

capitalizing on data analytics, cloud computing and

modeling techniques

Consumers in Asia-

willing to shift to digital channels than

consumers in any other region globally,

according to EY’s Global Consumer

Insurance Survey 2014.

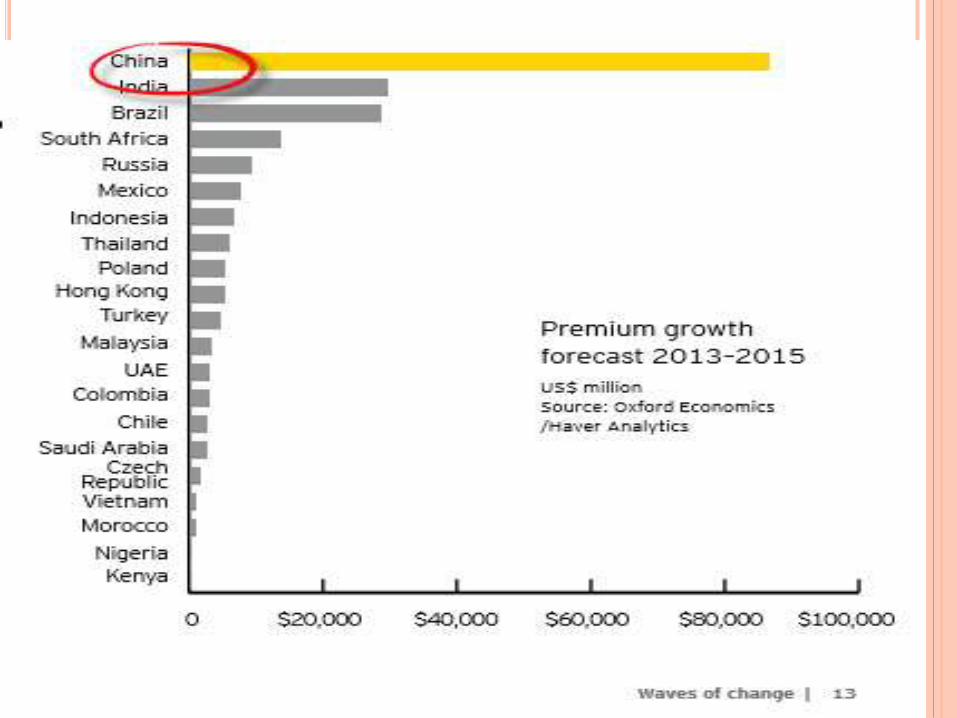

ASIA PACIFIC REGION

For life and non-life insurance products, with GDP

projected to be 5.5%.

The growth of the middle class population,

increased the sales of personal lines insurance.

Commercial lines insurance prospects remain

strong.

increasingly technologically sophisticated

population.

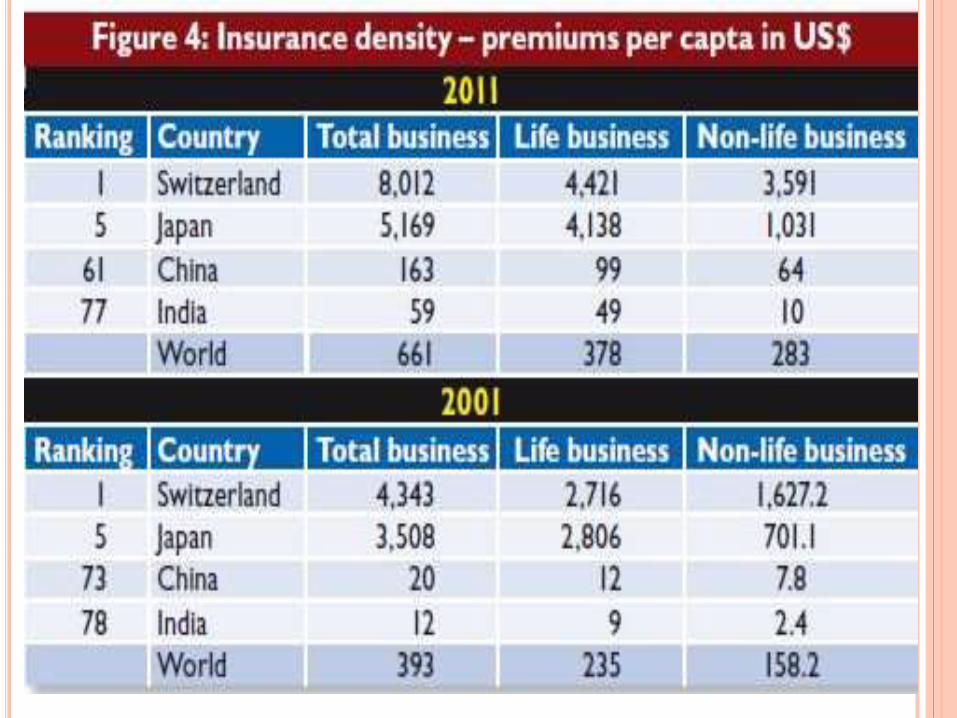

MOTOR INSURANCE IN INDIA

After liberalisation of the Indian insurance industry

in the year 1999- 2000, the Indian general

insurance industry has witnessed rapid growth.

GDP has grown from INR 11,446 crore in FY02 to

INR 57,964 crore in FY12.

Compounded annual growth rate (CAGR) of 17.6

percent.

Changes in the regulatory environment

substantially impacted the industry dynamics.

Coverage of underlying risks has increased

considerably.

CONTINUES……

the general insurance industry has set a target of crossing Rs 1 trillion mark in annual premium income this fiscal, up from Rs 84,715 crore in 2014-15.

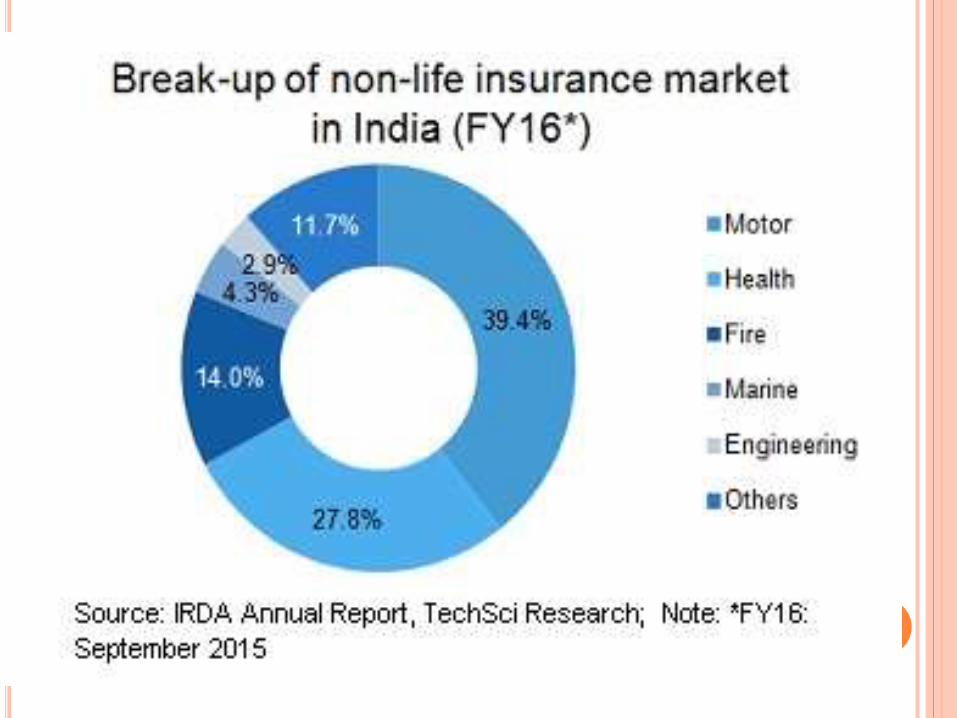

motor insurance has grown by 11-12 percent during 2014-15.

Motor insurance with a share of around 46 per cent in the total gross premium is the largest business.

A slowdown in new motor car sales has hit motor insurance business.

Car sales in India fell for the second consecutive fiscal in 2013-14 with a drop of 4.65 per cent.

GROWTH AND PROFITABILITY TRENDS

Motor insurance stands tall in growing general

insurance sector.

Motor insurance including both ' own damage' and '

third party' categories has maximum share of 44

percent in the general insurance business .

The third-party insurance category of motor

insurance is mandatory in India.

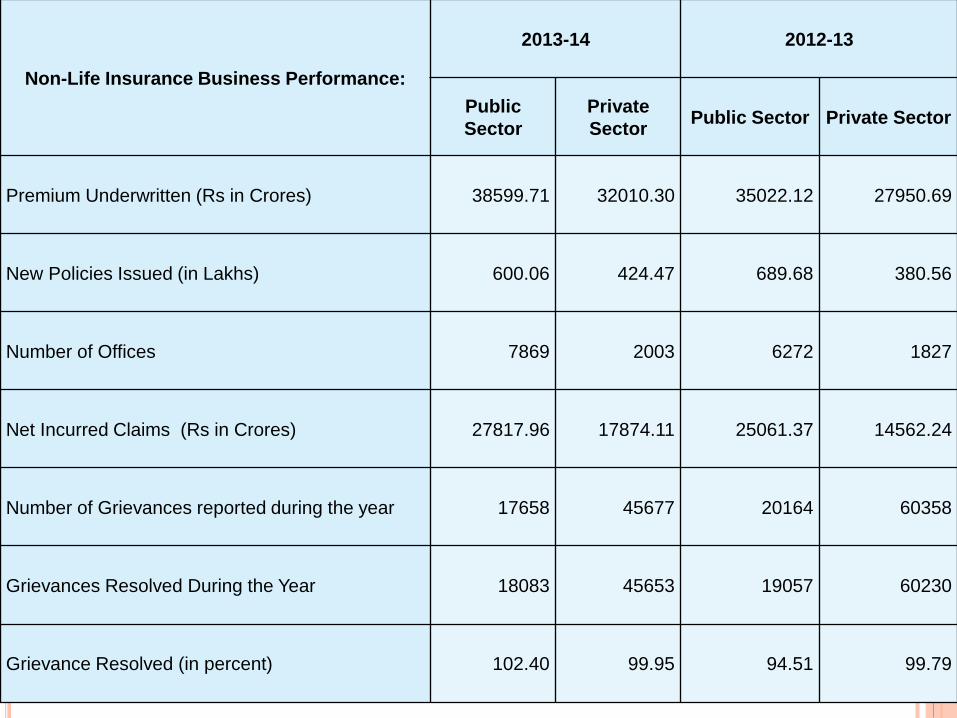

Non-Life Insurance Business Performance:

2013-14 2012-13

Public

Sector

Private

SectorPublic Sector Private Sector

Premium Underwritten (Rs in Crores) 38599.71 32010.30 35022.12 27950.69

New Policies Issued (in Lakhs) 600.06 424.47 689.68 380.56

Number of Offices 7869 2003 6272 1827

Net Incurred Claims (Rs in Crores) 27817.96 17874.11 25061.37 14562.24

Number of Grievances reported during the year 17658 45677 20164 60358

Grievances Resolved During the Year 18083 45653 19057 60230

Grievance Resolved (in percent) 102.40 99.95 94.51 99.79

MOTOR INSURANCE IN CHINA

China’s insurance market is one of the largest and fastest growing market.

the world’s second largest market.

10% GDP economy growth over the last 30 years.

The Chinese motor insurance market is expected to generate total gross premium income of $84,502.6m in 2014.

Compound annual growth rate (CAGR) of 14.1% between 2010 and 2014.

The personal segment is expected to be the market's most lucrative in 2014

Total gross premium income of $58,477.4m, equivalent to 69.2% of the market's overall value.

CONTINUES……

The performance of the market is forecast to

decelerate, with an anticipated CAGR of 10.2% for

the five-year period 2014 – 2019.

It is expected to drive the market to a value of

$137,313.5m by the end of 2019.

Despite new car sales slowing, auto insurance

continues to offer growth opportunities in the

property and casualty sector.

73.1% of the total property and casualty market

and 56.6% of the foreign companies’ business mix.

HIGHLIGHT OPPORTUNITIES IN MOTOR

INSURANCE

Over the next three years, foreign insurers

anticipate motor insurance will grow in the 10-15%

range.

Predicting growth of around 10% and a second

group around 25% between 2015-18.

Digital marketing will have a significant impact on

their business models over the next three years.

The motor insurance, which accounts for more than

70% of the total non-life premiums.

NON-LIFE INSURANCE –GAINING WEIGHT AND

DELIVERING STABLE GROWTH

Non-life market is even more concentrated than life,

with the top three insurers sharing 64.8% of the

market.

PICC 34.4% market share,

Ping An 17.8%

China Pacific 12.3%

o Non-life market is dominated by motor insurance,

which accounts for more than 70% of total non-life

premiums.

MOTOR INSURANCE

For motor insurance, the number of passenger cars has

jumped to 137.4 million by the end of 2013.

China the largest passenger car market in the world.

motor insurance maintains its dominance at least in the

medium term and to continue driving the growth for the

non-life sector.

Historically, the motor third party liability (MTPL) sector

was open only for domestic players.

In 2012 foreign insurers gain full access to compulsory

liability insurance for motor vehicle accidents.