comparative analysis and implication for the next phase … vol1 part 1 comparative ana… ·...

TRANSCRIPT

Part 1Comparative Analysis and Implication for the Next Phase of ABMF Sub-Forum 1 (2012–2013)

ASEAN+3 Bond Market Guide | Volume 1 | Part 1

i

Contents

Economies Covered in the Comparative Analysis ....................................................................................1

Summary of Findings ...............................................................................................................................2A. Overall Assessment – Sound and Robust Market Infrastructure ................................................................2B. Sub-Forum 1: Summary of Findings ........................................................................................................10

Implications for the Next Phase of the ASEAN+3 Bond Market Forum Sub-Forum 1 (2012–2013) .......21

Details of SF1 Contents of Findings .......................................................................................................29I. Legal Tradition in the Domestic Capital Markets ....................................................................................30II. Governing Law for Domestic Bond Issuance ..........................................................................................30III. Competent Authority (Regulator) and Self-Regulatory Organizations of

Domestic Bond Markets ........................................................................................................................35IV. Role of the Self-Regulatory Organizations in Domestic Bond Markets ...................................................36V. Definition of Securities (Bonds) .............................................................................................................44VI. Event of Default and Payment Default ....................................................................................................48VII. Existence of the Meeting of Bondholders System ....................................................................................51VIII. The System of Commissioned Company, Bond Representative and Trustee .............................................52IX. Bankruptcy Procedures ...........................................................................................................................53X. Form of Bonds (Settlement Method) and Status (Bearer/Registered) ......................................................56XI. Exchangeability of Scripless Bonds to Physical Bonds .............................................................................57XII. Transfer of Securities (or Property Rights) and Finality of Settlement of Scripless Bonds ........................58XIII. Legal Basis and Definition of “Settlement and Clearing” .......................................................................63XIV. Registration and Issuing Approval Procedures of Bonds .........................................................................66XV. Necessity of Disclosure of Ultimate Beneficial Owner ...........................................................................77XVI. Foreign Exchange and Currency-Related Restrictions .............................................................................78XVII. Omnibus Securities Account and Nominee Concept ..............................................................................79XVIII. Main Trading Places (Over the Counter or Exchange) and Existence of Exchange trading .....................80XIX. Listing of Bonds and Obligation for Market Listing (Domestic Market) ..................................................80XX. Necessity of Credit Rating for the Issuing of Bonds ................................................................................81XXI. Documentation Language .......................................................................................................................82XXII. Concept/Definition of Professional or Institutional investors .................................................................83XXIII.Definition of Public Offering (and Private Placement or Exempt Regime) ...............................................86

ii

ASEAN+3 Bond Market Guide | Volume 1 | Part 1

XXIV. Existence of Professional Investors-Only Market ....................................................................................89XXV. Market Capitalization – Size of the Local Currency Bond Market (as of March 2011) ............................90XXVI. Size of Foreign Currency Bond Market (as of March 2011) ....................................................................90XXVII. Islamic Finance related Issues ................................................................................................................90

Appendix ...............................................................................................................................................93

Reference ..............................................................................................................................................94

Figures and TableFigures

Figure 2.1 ASEAN+3 Government Bond Market Infrastructure Diagram .....................................................11Figure 2.2 Regional Standardization of Documentation ............................................................................22Figure 2.3 Exempted Market versus Full Disclosure Market ......................................................................22Figure 2.4 Comparative Structure of US Domestic and Offshore Markets ...................................................23Figure 2.5 Status Quo of Asean+3 Bond Markets ...................................................................................24Figure 2.6 Connecting the Professional Market Elements in the Region .....................................................24Figure 2.7 Creation of an Intra-Regional Bond Market ..............................................................................25Figure 2.8 Mutual Recognition Examples (1), (2), (3) ..............................................................................26

TablesTable 1.1 Economies Covered in the Comparative Analysis ........................................................................1Table 1.2 Existence of a Clear Definition of Securities (Bonds) ..................................................................2Table 1.4 Forms and Status of Bonds across Economies ..........................................................................4Table 1.5 Exchangeability of Scripless Bonds to Physical Bonds .................................................................5Table 1.6 Existence of a Concept of Bondholder Meeting ..........................................................................6Table 1.7 Existence of Concepts of Commissioned Company, .....................................................................

Bond Representative and Trustee ............................................................................................6Table 1.8 Obligation to Acquire Credit Rating upon Bond Issuance .............................................................6Table 1.9 Main Market Authorities across covered Economies ...................................................................7Table 1.10 Self-Regulatory Organizations across ASEAN+3 Bond Markets ....................................................7Table 1.12 Foreign Exchange and Currency-Related Restrictions ..................................................................8Table 2.1 Over-the-Counter Market versus Exchange Market ...................................................................10Table 2.2 Existence of Exempt Regimes ................................................................................................12Table 2.3 Status of Concepts of Commissioned Company, Bondholder Representative and Trustee ............12Table 2.4 Legal Tradition .....................................................................................................................13Table 2.5 Requirements for Identifying Investors and Beneficial Owners ....................................................14Table 2.6 Existence of Omnibus Accounts or Nominee Concept ...............................................................14Table 2.7 Existence of Exempt Regimes ................................................................................................15Table 2.8 Existence of the Concept of Professional Investor ...................................................................16Table 2.9 Existence of Professional Investor-Only Market ........................................................................17Table 2.10 Definitions of Self-Regulatory Organizations ............................................................................17Table 2.11 Existence of the Islamic Finance Market .................................................................................20

iii

ASEAN+3 Bond Market Guide | Volume 1 | Part 1 ASEAN+3 Bond Market Guide | Volume 1 | Part 1

Details of SF1 Contents of Findings: Tables Table 1. Legal Tradition in the Domestic Capital Markets .......................................................................30Table 2. Governing Law for Domestic Bond Issuance ............................................................................30Table 3. Competent Authority (Regulator) and Self-Regulatory Organizations of Domestic Bond Markets ....35Table 4. Role of Self-Regulatory Organizations in Domestic Bond Markets ...............................................36Table 5. Definition of Securities (Bonds) ..............................................................................................44Table 6. Event of Default and Payment Default ....................................................................................48Table 7. Existence of Bondholders Meeting System ..............................................................................51Table 8. The System of Commissioned Company, Bond Representative and Trustee .................................52Table 9. Bankruptcy Procedures .........................................................................................................53Table 10. Form of Bonds (Settlement Method) and Status (Bearer/Registered) .........................................56Table 11. Exchangeability of Scripless Bonds to Physical Bonds ...............................................................57Table 12. Transfer of Securities (or Property Rights) and Finality of Settlement of Scripless Bonds ...............58Table 13. Legal Basis and Definition of “Settlement and Clearing” ...........................................................63Table 14. Registration and Issuing Approval Procedures of Bonds ............................................................66Table 15. Necessity of Disclosure of Ultimate Beneficial Owner................................................................77Table 16. Foreign Exchange and Currency-Related Restrictions ................................................................78Table 17. Omnibus Securities Account and Nominee Concept .................................................................79Table 18. Main Trading Places (Over the Counter or Exchange) and Existence of Exchange Trading ..............80Table 19. Listing of Bonds and Obligation for Market Listing (Domestic Market) .........................................80Table 20. Necessity of Credit Rating for the Issuing of Bonds ..................................................................81Table 21 Documentation Language .....................................................................................................82Table 22. Concept and Definition of Professional or Institutional investors ................................................83Table 23. Definition of Public Offering (and Private Placement or Exempt Regime) .....................................86Table 24. Existence of Professional Investors-Only Market ......................................................................89Table 25. Market Capitalization – Size of Local Currency Bond Market (as of March 2011) ($ billion) .........90Table 26. Size of Foreign Currency Bond Market (as of March 2011) ($ billion) .........................................90Table 27. Islamic Finance-Related Issues ..............................................................................................90

ASEAN+3 Bond Market Guide | Volume 1 | Part 1

1

This report mainly discusses the harmonization and standardization of bond markets of 10 economies with existing bond markets in the Association of Southeast Asian Nations, People’s Republic of China, Japan and Republic of Korea (ASEAN+3).

Table 1.1 Economies Covered in the Comparative Analysis

Economy

Economies Subject to Comparative Analysis

(Ten Scripless Securities Markets)Economies Covered Under

Bond Market Guides 1 China, People’s Rep. of ü ü

2 Hong Kong, China ü ü

3 Indonesia ü ü

4 Japan ü ü

5 Korea, Rep. of ü ü

6 Malaysia ü ü

7 Philippines ü ü

8 Singapore ü ü

9 Thailand ü ü

10 Viet Nam ü ü

11 Lao PDR – ü (voluntary submission for reference)aa At the outset, it is understood that the bond markets of Brunei Darussalam, Cambodia, Lao People’s Democratic Republic (PDR),

and Myanmar are in the planning stage for creation or in the early stages of development; therefore, as discussed in the ASEAN+3 Bond Market Forum (ABMF) in the past, the ADB secretariat did not ask these developing markets to provide market information. Instead, ABMF members and experts focused on sharing the information collected from these developing markets to support their initiatives to establish or develop their respective bond markets. This is the reason the ABMF secretariat held workshops in Brunei Darussalam and Lao PDR in May and June 2011. However, this did not entirely prevent the two economies from providing any market information to be included in the market guides. Lao PDR proactively and voluntarily submitted their bond market guide as reference.

Source: ADB Consultants, based on research materials and market visit information.

Economies Covered in the Comparative Analysis

ASEAN+3 Bond Market Guide | Volume 1 | Part 1ASEAN+3 Bond Market Guide | Volume 1 | Part 1

2

A. Overall Assessment – Sound and Robust Market Infrastructure

All of the 10 securities markets covered under this research project have built robust market infrastructures, including legal and operational systems to secure transactions in the domestic bond market over the past 10 years.

In almost all markets, key legal and regulatory frameworks and related systems are in place. The following tables detail some of the features of these key bond-market infrastructures.

For instance, a clear definition of securities (bonds) is considered to be a fundamental base and condition for the sound development of the bond market. Most of the jurisdictions have a specific definition of securities, or are striving to further improve or clarify the definition of securities.

Table 1.2 Existence of a Clear Definition of Securities (Bonds)

Jurisdiction Existence of a Clear Definition of Securities (Bonds)

People’s Republic of China

Securities concepts may differ by industry or by competent authority in China. The Corporation Law and Enterprise Law co-exist and, hence, either may set rules for issuance of securities, depending on the industry, issuer, and type of security.

The official definition of securities is provided in the Securities Law of PRC, which was revised in 2005.

The present law shall be applied to the issuance of and transactions in stocks, corporate bonds, as well as any other securities lawfully recognized by the State Council within the territory of the PRC. However, some bonds do not fall under the Securities Law.In case where there is no such provision in the present law, the provisions of the Corporation Law and other relevant laws and administrative regulations shall be applied.

Hong Kong, China For bonds to be listed on the Hong Kong Stock Exchange or cleared through the Central Moneymarkets Unit (CMU), they must satisfy the criteria as set out in, among others, the Listing Rules and CMU Service Reference Manual (which is accessible to CMU members only), respectively. Also, a definition of securities is laid down in the Securities and Futures Ordinance (SFO) of the Securities and Futures Commission (SFC).

Indonesia The definition of securities is not confined to a single law. Original relevant definitions found in the commercial code left by the Dutch, and remaining in force are the following: Promissory note (PN), cheque, and bill of exchange.

There is no mention of corporate bonds and debt instruments in the Company Law; however, they are often described or covered in the Articles of Association of companies.

Summary of Findings

continued on next page

3

ASEAN+3 Bond Market Guide | Volume 1 | Part 1 ASEAN+3 Bond Market Guide | Volume 1 | Part 1ASEAN+3 Bond Market Guide | Volume 1 | Part 1

Jurisdiction Existence of a Clear Definition of Securities (Bonds)The clearest definition of securities can be found in the Capital Market Law No. 8 (1995). Pursuant to the Capital Market Law, securities are classified as PNs, commercial paper (CP), shares, bonds, evidences of indebtedness, participation units of collective investment contracts, futures contracts related to securities, and all derivatives of securities. Today, the distinction of debt instruments can be divided into the capital market and the money market: (1) the capital market covers bonds, (2) the money market covers PN, medium-term notes (MTN), CP, Certificate of Central Bank (SBI, Sertifikat Bank Indonesia); most instruments have been introduced by foreign bank participants in recent years. MTN and CP are synonymous for all intents and purposes; legal treatises exist but there are no statutory definitions of these instruments.

Japan The Companies Act defines corporate bonds.

A uniform legal framework for all types of securities exists.

Distinctions between dematerialization or immobilization and physical securities are clear.

Legal ownership structure of dematerialized or immobilized securities is clearly stipulated.

Republic of Korea The revised Commercial Act (to take effect in 2012) provides a basis for corporate bonds diversity.

This should resolve the discrepancy in the definition of securities between the Commercial Act and the Financial Investment Services and Capital Markets Act (FSCMA).

Malaysia Under section 2(1) of the Capital Markets and Services Act 2007, securities are defined as: (a) debentures, stocks or bonds issued or proposed to be issued by any government; (b) shares in or debentures of, a body corporate or an unincorporated body; or (c) unit trusts or prescribed investments, and includes any right, option or interest in respect thereof, but does not include futures contracts.

Debentures are also stipulated in article 125 of the Companies Act 1965.

Philippines Under section 3 of the Securities Regulation Code (SRC), securities are shares; participation or interests in a corporation or in a commercial enterprise or profit-making venture and evidenced by a certificate; contract; or instrument, whether written or electronic in character.

The Philippine Dealing and Exchange (PDEx) Rules for the Fixed Income Securities Market, as amended (PDEX Rules), define securities as fixed-income securities, including government securities.

Singapore Securities are defined in the Securities and Futures Act (SFA) in sections 2(1), 196A, 214, and 239.

Thailand Section 4 of the Securities and Exchange Act B.E. 2535 stipulates the definition of securities.

Viet Nam Pursuant to article 3 of the amended and supplemented Securities Law No. 62/2010/QH12 and article 6 of Securities Law No. 70/2006/QHll, securities mean evidence from an issuing organization certifying the lawful rights and interest of an owner with respect to assets or capital portion. Securities may take the form of certificates, book entries or electronic data, and shall comprise the following types: 1) shares, bonds and investment fund certificates; 2) share purchase rights (rights issue), warrants, call options, put options, future contracts, groups of securities and securities indices; 3) investment capital contribution contracts; and 4) other types of securities stipulated by the Ministry of Finance.

Source: ADB Consultants, based on research materials and market visit information.

Trades can be executed efficiently in a secure manner; operations and practices in the markets are comparable to other developed bond markets. All of the 10 securities markets now have a scripless securities system. Notwithstanding, some still have room for further improvement in maximizing the benefits available from such systems.

Table 1.3 Existence of Scripless Securities System

Jurisdiction Existence of Scripless Securities SystemPeople’s Republic of China Yes

Hong Kong, China Yes

Indonesia Yes

Japan Yes

Republic of Korea Yes

Malaysia Yes

Table 1.2 continuation

continued on next page

4

ASEAN+3 Bond Market Guide | Volume 1 | Part 1

Jurisdiction Existence of Scripless Securities SystemPhilippines Yes

Singapore Yes

Thailand Yes

Viet Nam YesSource: ADB Consultants, based on research materials and market visit information.

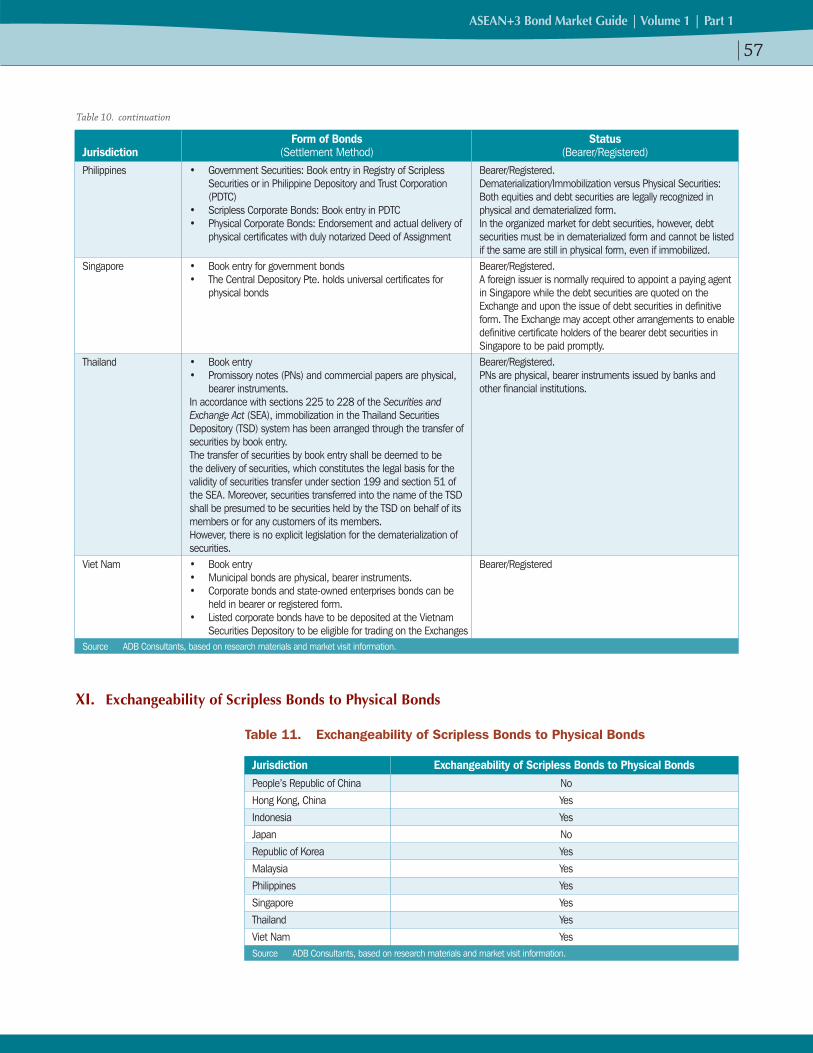

The introduction of scripless securities led to the issuance, keeping and transfer of bonds on a book-entry basis in these markets. This reduces operational risk significantly. In this context, it is noteworthy that the People’s Republic of China (China) and Japan have implemented a ‘registered notes only’ policy. In addition, from the viewpoint of exchangeability of scripless bonds to physical bonds, it is observed that scripless bonds can no longer be exchanged to physical bonds in China and Japan. It seems that these two countries are pursuing the same policy direction.

Table 1.4 Forms and Status of Bonds across Economies

JurisdictionForm of the Bonds(Settlement Method)

Status (Bearer/Registered)

People’s Republic of China

• Book-entry Registered.(Bonds are generally getting scripless in a central register and registered in an account holder’s or bondholder’s name; some older bearer bonds may still exist. As for China Central Depository and Clearing (CCDC)-settled bonds in the China Inter-bank Bond Market, CDCC centralized the management of the bearer bond library in 1998, and 2001 saw the end of bearer bonds in this market.)

Hong Kong, China • Book-entryform(dematerialized)forExchangeFundpaper,and• Globalnoteformforcorporatebonds

Bearer/Registered

Indonesia • Bookentry(from2000)• Physicalcertificatestillexist(issuedpriorto2000)

Bearer/Registered

Japan • Book-entry(Completelydematerialized,exceptforafewnon-centralsecurities depository [CSD] settled private placed notes)

Registered

Republic of Korea • Book-entry Dematerialized securities: Securities which are not issued in paper

form and where ownership is held and is transferable by book entry in a ledger maintained by a CSD or account management institution.

Immobilized securities: Physical securities and non-certificated securities held and transferred by book entry in a ledger maintained by a CSD or account management institution.

Bearer/Registered

Malaysia • Listedbonds:BookentryatBursaMalaysiaDepository• Unlisteddebtsecurities:BookentryatBankNegaraMalaysia(BNM)

Basically, registered.Cagamas papers are unsecured bearer bonds issued by Cagamas, the national mortgage corporation established in 1986 to promote the secondary mortgage market in Malaysia.

Philippines • GovernmentSecurities:BookentryintheRegistryofScriplessSecurities (RoSS) or in the Philippine Depository and Trust Corporation (PDTC)

• ScriplessCorporateBonds:BookentryinPDTC• PhysicalCorporateBonds:Endorsementandactualdeliveryof

physical certificates with duly notarized Deed of Assignment

Bearer/Registered. Dematerialization/immobilization versus physical securities: both equities and debt securities are legally recognized in physical and dematerialized forms. In the organized market for debt securities, however, debt securities must be in dematerialized form and cannot be listed if the same are still in physical form, even if immobilized.

Table 1.3 continuation

continued on next page

5

ASEAN+3 Bond Market Guide | Volume 1 | Part 1 ASEAN+3 Bond Market Guide | Volume 1 | Part 1

JurisdictionForm of the Bonds(Settlement Method)

Status (Bearer/Registered)

Singapore • Bookentryforgovernmentbonds• TheCentralDepositoryPte.(CDP)holdsuniversalcertificatesfor

physical bonds

Bearer/Registered.A foreign issuer is normally required to appoint a paying agent in Singapore while debt securities are quoted on the Exchange and upon the issue of debt securities in definitive form. The Exchange may accept other arrangements to enable definitive certificate holders of the bearer debt securities in Singapore to be paid promptly.

Thailand • Bookentry• Promissorynotes(PNs)andcommercialpapersarephysical,bearer

instruments

In accordance with sections 225 to 228 of the Securities and Exchange Act (SEA), immobilization in the Thailand Securities Depository (TSD) system has been arranged through the transfer of securities by book entry.

The transfer of securities by book entry shall be deemed to be the delivery of securities, which constitutes the legal basis for the validity of securities transfer under section 199 and section 51 of the SEA. Moreover, securities transferred into the name of the TSD shall be presumed to be securities held by the TSD on behalf of its members or for any customers of its members.

However, there is no explicit legislation for the dematerialization of securities.

Bearer/Registered.PNs are physical, bearer instruments issued by banks and other financial institutions.

Viet Nam • Bookentry• Municipalbondsarephysical,bearerinstruments.• Corporatebondsandstate-ownedenterprises(SOE)bondscanbe

held in bearer or registered form.• ListedcorporatebondshavetobedepositedattheVietnam

Securities Depository to be eligible for trading on the Exchanges.

Bearer/Registered

Source: ADB Consultants, based on research materials and market visit information.

Table 1.5 Exchangeability of Scripless Bonds to Physical Bonds

Jurisdiction Exchangeability of Scripless Bonds to Physical BondsPeople’s Republic of China No

Hong Kong, China Yes

Indonesia Yes

Japan No

Republic of Korea Yes

Malaysia Yes

Philippines Yes

Singapore Yes

Thailand Yes

Viet Nam YesSource: ADB Consultants, based on research materials and market visit information.

A bondholder meeting concept is one of the typical indicators of the maturity of a bond market. Ten out of Eleven jurisdictions already feature the bondholder-meeting concept as a basic infrastructure of their respective bond markets.

Table 1.4 continuation

6

ASEAN+3 Bond Market Guide | Volume 1 | Part 1

Table 1.6 Existence of a Concept of Bondholder Meeting

Jurisdiction Existence of a Concept of Bondholder Meeting People’s Republic of China YesHong Kong, China YesIndonesia YesJapan YesRepublic of Korea YesMalaysia YesPhilippines YesSingapore YesThailand YesViet Nam Meeting concept may be existent, but has not been established as a system.Source: ADB Consultants, based on research materials and market visit information.

In addition, the existence of concepts of commissioned company, bond representative and trustee is important for investor protection in the bond markets. Most of the jurisdictions have such concepts in place, even though they may vary in name and individual features.

Table 1.7 Existence of Concepts of Commissioned Company, Bond Representative and Trustee

JurisdictionExistence of

Commissioned Company/Bond Representative/Trustee ConceptPeople’s Republic of China YesHong Kong, China YesIndonesia YesJapan YesRepublic of Korea YesMalaysia YesPhilippines YesSingapore YesThailand YesViet Nam -Source: ADB Consultants, based on research materials and market visit information.

At the same time, a credit rating system also plays an important role in the bond market. Particularly, it is considered that developing markets generally require a compulsory credit rating system for investor protection. Many of the developing markets in the region have such system.

Table 1.8 Obligation to Acquire Credit Rating upon Bond Issuance

Jurisdiction Obligation to Acquire Credit Rating upon Bond IssuancePeople’s Republic of China

Yes.

Hong Kong, China No.

Indonesia Yes.

Japan No. But, TOKYO PRO-BOND Market Listing requires a credit rating.

Republic of Korea Yes.

Malaysia Yes.

continued on next page

7

ASEAN+3 Bond Market Guide | Volume 1 | Part 1 ASEAN+3 Bond Market Guide | Volume 1 | Part 1

Jurisdiction Obligation to Acquire Credit Rating upon Bond IssuancePhilippines Yes.

Singapore No. But, as a foreign debt-securities listing requirement of the Singapore Exchange (SGX), the issue of debt securities must have a credit rating of investment grade and above.

Thailand Yes.

Viet Nam No.Source: ADB Consultants, based on research materials and market visit information.

Regulators in these markets are encouraged to further eliminate legal and regulatory uncertainties, and to maintain transparency of rules and practices in each domestic market.

Table 1.9 Main Market Authorities across covered Economies

Jurisdiction Main Market AuthorityPeople’s Republic of China • Inter-bankBondMarket(OvertheCounter):People’sBankofChina(PBOC)

• ExchangeMarket(ShanghaiStockExchangeandShenzhenStockExchange):China Securities Regulatory Commission (CSRC)

• ForeignCurrencyPolicy:PBOC,StateAdministrationofForeignExchange

Hong Kong, China Hong Kong Monetary Authority

Indonesia Capital Market and Non-Bank Financial Service Supervisory Agency

Japan Financial Services Agency

Republic of Korea Financial Services CommissionFinancial Supervisory Service

Malaysia Securities Commission Malaysia

Philippines Securities and Exchange Commission

Singapore Monetary Authority of Singapore

Thailand Ministry of Finance Securities and Exchange Commission

Viet Nam State Securities Commission (SSC) (Since March 2004, the SSC is under the jurisdiction of the Ministry of Finance of Viet Nam)

Source: ADB Consultants, based on research materials and market visit information.

Aiding the functioning of the bond markets, the role of self-regulatory organizations (SROs) in each domestic market is critically important. In the region, many of the jurisdictions have established SROs.

Table 1.10 Self-Regulatory Organizations across ASEAN+3 Bond Markets

Jurisdiction Name of SRO Membership Sets Rules Enforcement People’s Republic of China NAFMII Yes Yes Yes

Hong Kong, China N/A N/A N/A N/A

Indonesia IDXKPEIKSEI

YesYesYes

YesYesYes

YesYesYes

Japan JSDATSETOKYO AIM

YesYesYes

YesYesYes

YesYesYes

Republic of Korea KOFIAKRX

YesYes

YesYes

YesYes

continued on next page

Table 1.8 continuation

8

ASEAN+3 Bond Market Guide | Volume 1 | Part 1

Jurisdiction Name of SRO Membership Sets Rules Enforcement Malaysia Bursa Malaysia

ACI Malaysia (quasi)YesYes

YesYes

YesYes

Philippines PDS Group (PDEx) Yes Yes Yes

Singapore SGX Yes Yes YesThailand ThaiBMA

ExchangesYesYes

YesYes

YesYes

Viet Nam VBMA Yes Yes –ACI = Persatuan Pasaran Kewangan Malaysia; IDX = Indonesia Stock Exchange; JSDA = Japan Securities Dealers Association; KOFIA = Korea Financial Investment Association; KPEI = Indonesia Clearing and Guarantee Corporation; KRX = Korea Exchange; KSEI = Indonesian Central Securities Depository, Kustodian Sentral Efek Indonesia; NAFMII = National Association of Financial Market Institutional Investors; PDEx = Philippine Dealing and Exchange; SGX = Singapore Exchange; SRO = self-regulatory organization; ThaiBMA = Thailand Bond Market Association; TSE = Tokyo Stock Exchange; VBMA = Vietnam Bond Market AssociationSource: ADB Consultants, based on research materials and market visit information

Bond markets in the region are distinct in many ways, such as in governing laws and responsible regulators based on their legal tradition and their own market needs, including documentation languages.

Table 1.11 Documentation Languages

Jurisdiction Main Language Alternative LanguagePeople’s Republic of China ChineseHong Kong, China English ChineseIndonesia Bahasa Indonesia EnglishJapan Japanese* English for TOKYO-PRO BOND Market ListingRepublic of Korea Korean (Hangul) English for Qualified Institutional Buyer MarketMalaysia EnglishPhilippines EnglishSingapore EnglishThailand Thai EnglishViet Nam Vietnamese* Japan is in the course of introducing a partial English based documentation for disclosure from April 2012; Although the information

for securities should be submitted in Japanese, most part of the disclosure information for issuer (including already disclosed reference information) can be submitted in English, except for a certain information. (Non-resident issuers’ burden will be reduced)

Source: ADB Consultants, based on research materials and market visit information.

Foreign institutional investors are already able to access all ASEAN+3 active markets for bond investments in local currency, with the exception of the People’s Republic of China. Having said so, the renminbi bond market in Hong Kong has been growing. Investors can access one or many ASEAN+3 markets, and buy corporate or government bonds, if they prefer, in local currency.

Table 1.12 Foreign Exchange and Currency-Related Restrictions

JurisdictionForeign Exchange Rate

Floating

Restrictions on Foreign Remittance(1. Own currency)

(2. Investment principal)(3. Coupons or dividends)

Currencies eligible for CLS

SettlementPeople’s Republic of China

Government-controlled floating, rate referring to currency basket

1. Restricted –2. Restricted for a certain period of time after investment3. Restricted for a certain period of time after investment

Hong Kong, China Link to US dollar (Currency Board System)

1. No restriction Yes2. No restriction3. No restriction

Table 1.10 continuation

continued on next page

9

ASEAN+3 Bond Market Guide | Volume 1 | Part 1 ASEAN+3 Bond Market Guide | Volume 1 | Part 1

JurisdictionForeign Exchange Rate

Floating

Restrictions on Foreign Remittance(1. Own currency)

(2. Investment principal)(3. Coupons or dividends)

Currencies eligible for CLS

SettlementIndonesia Floating 1. Restricted. (Rupiah foreign exchange trades must be done by Indonesian

domestic banks; rupiah remittance between foreign banks is prohibited)–

2. No reporting required for repatriation of benefits. 3. Reporting required(*) Real-demand principle applies to inbound foreign exchange or buying

Indonesian rupiah only.Japan Floating 1. No restriction Yes

2. No restriction. (ex post facto report required)3. No restriction. (ex post facto report required)

Republic of Korea Floating 1. Restricted Yes2. No restriction3. No restriction

Malaysia Managed float against a basket of currencies, following the de-pegging of the ringgit

1. Restricted (All remittances out of the country must be made in foreign currency). Real-demand principle applies to inbound FX only.

–

2. No restriction for non-resident investors to repatriate in foreign currency3. No restriction for non-resident investors to repatriate in foreign currency

Philippines Floating 1. Restricted. Registration with the Bangko Sentral ng Pilipinas (BSP) for issuance of Bangko Sentral Registration Document (BSRD) on per transaction basis is required to qualify for automatic conversion of peso sale or interest into foreign exchange for outward repatriation.

–

2. Registration with BSP for issuance of BSRD on per transaction basis is required to qualify for automatic conversion of peso sale or interest into foreign exchange for outward repatriation.

3. Interest automatically qualifies for outward repatriation if principal investment has BSRD.

Singapore Floating against basket of currencies

1. No restrictions (investor can hold Singapore dollar in Tokyo, for example) Yes2. No restriction3. No restriction

Thailand Managed Floating 1. Restricted –2. Reporting is required.3. Reporting is required.

Viet Nam Controlled Floating 1. Restricted –2. Restricted for certain period of time after investment3. No restriction(Viet Nam issue is based on availability of foreign currency)

Source: ADB Consultants, based on research materials and market visit information.

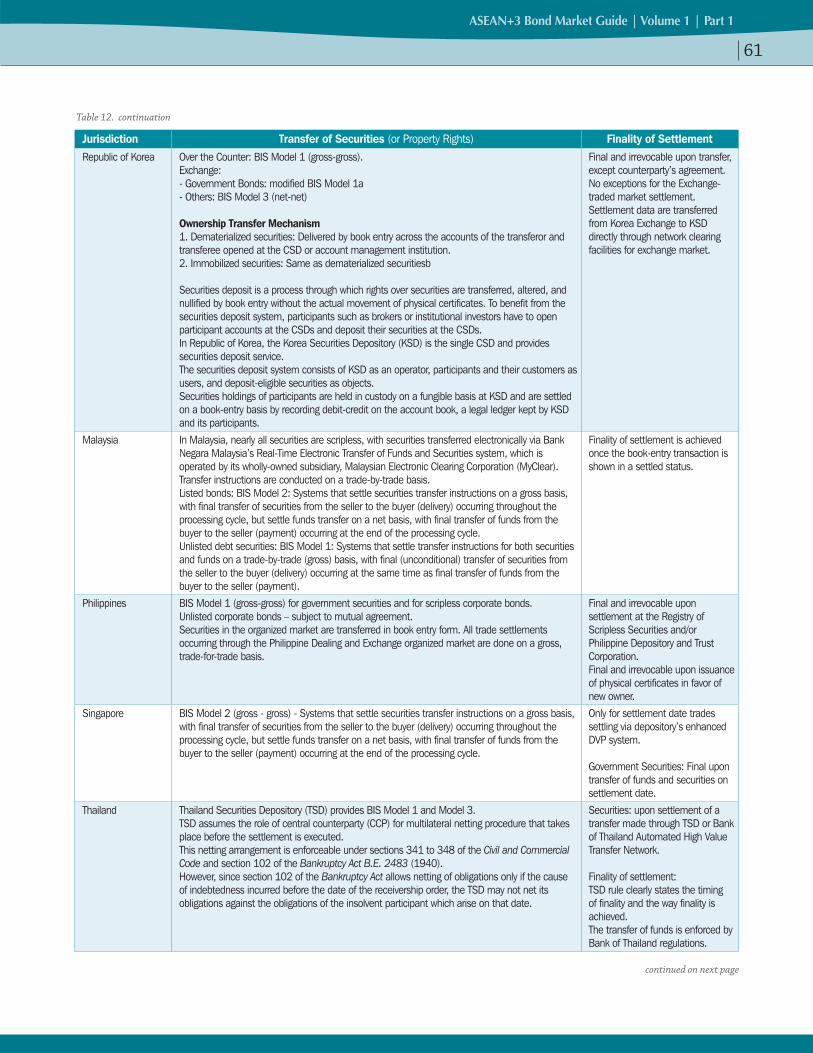

To illustrate such distinction, the transfer of ownership of bonds may not be the same as in the rules governing the finality of settlement; almost all of the markets have established their specific market practices. For details, please refer to “SF1: Contents of Findings, XII. Transfer of Securities (or Property rights) and Finality of Settlement of Scripless Bonds.”

Although actual condition regarding default recognition may be different by the terms and conditions of the bonds and by jurisdiction, default procedures are usually well disclosed in the bonds issuance documentation in many jurisdictions in the region. In many jurisdictions and bonds issuance documentation, these default procedures do not usually deviate from the documentation standards of international bond issues. In some cases, however, there are still uncertainties regarding default recognition and procedures. On the other hand, the status of development of bankruptcy-related legislation in the region differs between jurisdictions.

Table 1.12 continuation

10

ASEAN+3 Bond Market Guide | Volume 1 | Part 1

Generally, the companies act and/or bankruptcy law and/or related laws, where applicable, will be quoted in the trust deed or similar documents to guide investors in making informed decisions. But in some jurisdictions in the region, bankruptcy-related law and procedures are still in the development stage. A greater understanding and further analysis of bankruptcy-related law and procedures across regional markets is important for future consideration.

For details, please refer to “SF1: Contents of Findings, VI. Event of Default/Payment Default” and “SF1: Contents of Findings, IX. Bankruptcy Procedures”

B. Sub-Forum 1: Summary of Findings

1. Over-the-Counter Market and Exchange MarketBonds can be listed on the stock exchanges in many markets, but most of the instruments are traded on the over-the-counter (OTC) market. The OTC market remains the main trading place for bond markets, but selected exchanges in Republic of Korea and China have begun to establish significant market segments. For instance, transactions in China’s Inter-bank Bond Market involve the trade system of the China Foreign Exchange Trade System (CFETS) and money-brokers, while exchange-market trading is done through the Shanghai Stock Exchange (SSE) and Shenzhen Stock Exchange (SZSE). In addition, since July 2011, Singapore government securities (SGS) can be traded on the Singapore Exchange (SGX), with particular focus for retail investors. On the other hand, Republic of Korea will launch the Qualified Institutional Buyer (QIB) market in May 2012 for professional investors, using the OTC trading platform of the Republic of Korea Financial Investment Association (KOFIA); the market will provide for exemption from the full-disclosure regime in Republic of Korea.

Table 2.1 Over-the-Counter Market versus Exchange Market

Jurisdiction OTC Market as a Main Trading Place Exchange-Market TradingChina Yes. Inter-bank Bond Market, not directly available to foreign investors.

Domestic institutions are permitted to trade in OTC market.Yes (SSE and SZSE).

Hong Kong, China Yes Yes (HKEx). But only accounts for a relatively small portion of all the trading in bonds.

Indonesia Yes Possible but not observed.Japan Yes No.Republic of Korea Yes Yes (KRX). Government Bonds.Malaysia Yes (Only for unlisted debt securities) No.

Philippines Yes (Regulated OTC) No.Singapore Yes Yes. (Government bonds, mainly for retail investors, since

July 2011)

Thailand Yes. BEX provides electronic platform for OTC fixed-income trading named Fixed Income and Related Securities Trading System (FIRST)

No.

Viet Nam Yes. But not yet regulated. No.BEX = Bond Electronic Exchange; SZSE = Shenzhen Stock Exchange; HKEx = Hong Kong Exchanges and Clearing; KRX = Korea Exchange; OTC = over the counter; SSE = Shanghai Stock ExchangeSource: ADB Consultants, based on research materials and market visit information.

The following diagram provides further illustration on the trading to settlement infrastructure across the observed economies.

11

ASEAN+3 Bond Market Guide | Volume 1 | Part 1 ASEAN+3 Bond Market Guide | Volume 1 | Part 1

Figu

re 2

.1

ASEA

N+

3 G

over

nmen

t B

ond

Mar

ket

Infr

astr

uctu

re D

iagr

am

Trad

e

Trad

e m

atch

ing

CCP

Sett

lem

ent

mat

chin

g

Bond

se

ttle

men

t

Cash

se

ttle

men

t

Viet

Nam

OTC

VSD

KSD

CCDC

CSDC

C

PDTC

PDEx

Ross

STP

Facil

ity

BTBT

r-ROS

S

PDEx

eDVP

JASD

ECPS

MS

JASD

ECPS

MS

CFET

SHK

MA

CMU

TCH

PTI

TSD

PTI

HNX

BIDV

Com

mer

cial

Bank

BOT

BAHT

NET

MAS

MEP

S+

RTGS

BSP

PhilP

ass

BOK

BOK-

Wire

+

BOJ

BOJ-

NET

BIBI

-RTG

SHK

MA

CHAT

SPB

OCHV

PS

CNAP

S

BOJ

BOJ-

NET

BNM

RENT

AS-

IFTS

TCH

PTI

BMS

ETP

Toky

oOT

CM

anila

OTC

PRC

OTC

Inte

r-ban

kBo

nd M

arke

t

Thai

land

OTC

Indo

nesia

OTC

Mal

aysia

OTC

MAS

MEP

S+

SGS

BNM

RENT

AS-

SSDS

BIBI

-SSS

SHK

MA

CMU

Hong

Kon

gOT

CSe

oul

OTC

KRX

SSE

and

SZSE

BRU,

CAM

, LAO

, MYA

VIE

MAL

SIN

JPN

PRC

THA

KOR

HKG

PHI

INO

Brun

ei

Daru

ssal

amCa

mbo

dia

Lao

PDR

Mya

nmar

(Net

ting)

Note

:

Exch

ange

Mar

ket

Dire

ct in

ters

yste

m c

onne

ctio

n

Cent

ral B

ank

Indi

rect

con

nect

ion.

Trad

e da

ta (b

ond

settl

emen

t ins

truct

ions

) are

ent

ered

to C

SD b

y ag

ent c

usto

dian

s.

Com

mer

cial B

ank

BAHT

NET

= B

ank

of T

haila

nd A

utom

ated

High

Val

ue T

rans

fer N

etwo

rk; B

I = B

ank

Indo

nesia

; BID

V =

Ban

k fo

r Inv

estm

ent a

nd D

evel

opm

ent o

f Vie

tnam

; BI-S

SSS

= B

ank

Indo

nesia

-Scr

iple

ss S

ecur

ities

Set

tlem

ent S

yste

m; B

MS

=

Burs

a M

alay

sia S

ecur

ities

; BNM

= B

ank

Nega

ra M

alay

sia; B

OJ =

Ban

k of

Japa

n; B

OJ-N

ET =

BOJ

-Fin

ancia

l Net

work

Sys

tem

; BOK

= B

ank

of K

orea

; BOK

-Wire

+ =

New

Ban

k of

Kor

ea F

inan

cial W

ire N

etwo

rk S

yste

m; B

OT =

Ban

k of

Th

aila

nd; B

SP =

Ban

gko

Sent

ral n

g Pi

lipin

as; B

Tr =

Bur

eau

of Tr

easu

ry; C

CDC

= C

hina

Cen

tral D

epos

itory

and

Cle

arin

g; C

CP =

Cen

tral C

ount

erpa

rty; C

FETS

= C

hina

For

eign

Exc

hang

e Tra

de S

yste

m; C

HATS

= C

lear

ing

Hous

e Au

tom

ated

Tra

nsfe

r Sys

tem

; CM

U =

Cen

tral M

oney

mar

kets

Uni

t; CN

APS

= C

hina

Nat

iona

l Aut

omat

ic Pa

ymen

t Sys

tem

; CSD

CC =

Chi

na S

ecur

ities

Dep

osito

ry a

nd C

lear

ing

Corp

orat

ion;

eDV

P =

ele

ctro

nic

deliv

ery v

ersu

s pa

ymen

t; ET

P =

ele

ctro

nic

tradi

ng p

latfo

rm; H

KMA

= H

ong

Kong

Mon

etar

y Au

thor

ity; H

NX =

Han

oi S

tock

Exc

hang

e; H

VPS

= H

igh V

alue

Pay

men

t Sys

tem

; IFT

S =

Inte

rban

k Fu

nds

Trans

fer S

yste

m; J

ASDE

C =

Japa

n Se

curit

ies

Depo

sitor

y Ce

nter

; JGB

CC =

Japa

n Go

vern

men

t Bon

d Cl

earin

g Co

rpor

atio

n; K

RX =

Kor

ea E

xcha

nge;

KSD

= K

orea

Sec

uriti

es D

epos

itory

; MAS

= M

onet

ary A

utho

rity o

f Sin

gapo

re; M

EPS

= M

AS E

lect

roni

c Pa

ymen

t Sys

tem

; OTC

= o

ver t

he c

ount

er; P

BOC

= P

eopl

e’s

Bank

of

Chi

na; P

DEx =

Phi

lippi

ne D

ealin

g an

d Ex

chan

ge; P

DTC

= P

hilip

pine

Dep

osito

ry a

nd Tr

ust C

orpo

ratio

n; P

hilP

aSS

= P

hilip

pine

Pay

men

ts a

nd S

ettle

men

t Sys

tem

; PSM

S =

Pre

-Set

tlem

ent M

atch

ing

Syst

em; P

TI =

pos

t-tra

de in

tegr

atio

n;

RENT

AS =

Rea

l-tim

e El

ectro

nic

Trans

fer o

f Fun

ds a

nd S

ecur

ities

; RoS

S =

Reg

istry

of S

crip

less

Sec

uriti

es; R

TGS

= re

al-ti

me

gros

s se

ttlem

ent;

SGS

= S

inga

pore

gov

ernm

ent s

ecur

ities

; SSD

S =

Scr

iple

ss S

ecur

ities

Dep

osito

ry S

yste

m;

SSE

= S

hang

hai S

tock

Exc

hang

e; S

TP =

stra

ight-t

hrou

gh p

roce

ssin

g; S

ZSE

= S

henz

hen

Stoc

k Ex

chan

ge; T

CH =

Tha

iland

Cle

arin

g Ho

use;

TSD

= T

haila

nd S

ecur

ities

Dep

osito

ry; V

SD =

Vie

tnam

Sec

uriti

es D

epos

itory

Sour

ce:

ABM

F SF

2.

KRX

JGBC

C

PDEx

PDEx

Sing

apor

eOT

C

12

ASEAN+3 Bond Market Guide | Volume 1 | Part 1

continued on next page

2. Regulatory Vacuum in Private PlacementThe regulatory vacuum in private placement in some of the domestic markets can be seen as a place of future improvement of the securities laws to be put properly as a regulated and an exempted private placement market to be taken up in tandem with their development stages.

That sort of clearly stipulated private placement scheme will be an opportunity to propose a regional self-regulatory framework for qualified market participants in the future.

Table 2.2 Existence of Exempt Regimes

Jurisdiction Existence of Exempt Regimes

Exempt securities/Exempt transactions (Private Placement)People’s Republic of China

-

Hong Kong, China Yes.

Indonesia No. Private placement (to less than 100) is not regulated in Indonesia.

Japan Yes.

Republic of Korea The Qualified Institutional Buyer system (and professional only market) will be launched in May 2012 under the revised Financial Services Commission Regulation on Issuance, Public Disclosure, etc. of Securities.

Malaysia Yes.

Philippines Yes.

Singapore Yes.

Thailand Yes.

Viet Nam No. Private placement (to less than 100) or sale to professional investors is clearly stipulated in the amended Securities Law. However, private placement is not regulated as an exempted scheme.

Source: ADB Consultants, based on research materials and market visit information.

3. Bondholder Representative and/or TrusteeThe concepts of bondholder representative, commissioned bank, and trustee are gaining popularity and are evolving. For example, the new Commercial Code in Republic of Korea, which will come into effect in 2012, is re-defining the role of commissioned banks.

Table 2.3 Status of Concepts of Commissioned Company, Bondholder Representative and Trustee

Jurisdiction Name of the systemStatus of Concepts

of Commissioned Company, Bondholder Representative and Trustee People’s Republic of China

Commissioned company • Enterprisebondshavethisconcept;whetheritworksisuntested.

Hong Kong, China Trustee • TheappointmentofatrusteeisdoneunderprovisionsoftheTrustIndenture.• Theappointmentofatrusteeisnotmandatory.• Norecentissuesorprogramsfeaturedtheconceptoftrustee.

Indonesia wali amanat (Trustee) • Bapepam-LKhasguidelinesforregistrationandthedutiesastrustee.• Trusteesmustmakeacontract,perwaliamanatan, with the corporate issuer in accordance with the

conditions set out by Bapepam-LK.

Japan Commissioned person or Commissioned company

• StipulatedinCompanies Act.• ItshallnotbeappliedincasebondminimumunitisJPY100millionormore.

13

ASEAN+3 Bond Market Guide | Volume 1 | Part 1 ASEAN+3 Bond Market Guide | Volume 1 | Part 1

Jurisdiction Name of the systemStatus of Concepts

of Commissioned Company, Bondholder Representative and Trustee Republic of Korea Commissioned company

(Revised Commercial Law which will take effect in 2012)/(Old Commercial Act)

• StipulatedintherevisedCommercial Act.• Theappointmentofacommissionedcompanyisnotmandatory.• TheappointmentofacommissionedcompanyisdoneunderprovisionsoftheTrustIndenture.

Malaysia Trustee • Trustdeedandtrusteeisrequired;basedonTrustee Corporation Act.• TrusteesshouldbeapprovedbytheSecuritiesCommission(SC)andlistedontheSCwebsite.• AAAissuersmaynotneedatrustee,butsuchissuesneedtobeapprovedbySC,anddefault

definitions need to be included in bond issue documentation.

Philippines Trustee - for Public offering.Facility Agent (FA) - for Private placement

• Publicofferingofbondissuestypicallyhasatrustee.• Corporatebondissuersmustappointatrustee.• PrivateplacementsrequireanFA,whichfunctionsasatrusteeandfiscalagent;intheabsenceof

specific regulations, issue documentation would indicate that the FA works on behalf of investors.

Singapore Trustee • AnissuermustappointasuitabletrusteetorepresenttheholdersofitsdebtsecuritieslistedontheExchange. However, a trustee is not required for a debt issue that is offered only to sophisticated or institutional investors and is traded in a minimum board lot size of SGD200,000 or its equivalent in foreign currencies following listing. (Refer to article 308 “Part IV Trustee and Trust Deed” of Chapter 3 (Debt Securities) of the Singapore Exchange Main Board Listing Rules for detailed information on the suitability of the trustee and the provisions to be included in the trust deed.)

Thailand Bondholder Representative or Trustee

• Notrusteeconceptforbonds;butbondholderrepresentative(BR).• BRhasfiduciaryduty,plusanydutyandliabilitysetoutinthetermsandconditions;both

appointment of BR and actual terms and conditions need to be registered with the Securities and Exchange Commission.

• IndentureagreementsinbondissuescanspecifyatrusteeorBR.Thetrusteeoverseesbondholderrights, including the filing of claims and demand payments from the issuer or guarantors. Bondholders can sue and claim for damages from the trustee in case the trustee acts in bad faith or causes damages to bondholders.

Viet Nam • InVietNam,thereisnoofficialconceptofthemeetingsofbondholdersyet.Source ADB Consultants, based on research materials and market visit information.

4. Common Law and Civil Law TraditionsAlthough market regulations in the region vary in many ways, this does not mean that harmonization is impossible. Markets can be categorized into different groups if regulations are viewed from certain angles. For instance, markets with common law tradition, such as Singapore, Malaysia and Hong Kong share the same trustee concept. Markets with civil law tradition like China, Indonesia, Japan, Republic of Korea, Thailand, and Viet Nam, while they may not have the concept of trustee, support the concept of an entity acting for bondholders; names, roles, fiduciary duties and type of institutions, though, may differ (i.e., bondholders representative or commissioned bank, etc.). Generally, if the details are examined, the differences may not be as significant.

Table 2.4 Legal Tradition

Jurisdiction Original Legal Tradition InfluencesPeople’s Republic of China Civil law or civil law system English law, United States (US) law, Japanese law

Hong Kong, China UK law, Common law

Indonesia Islamic law, Dutch law, Civil law or civil law system US law

Japan Civil law or civil law system English law, US law, European Union law

Republic of Korea Civil law or civil law system English law, US law, Japanese law

Malaysia English law, Common law, Islamic law

Philippines Spanish law US law

Table 2.3 continuation

continued on next page

14

ASEAN+3 Bond Market Guide | Volume 1 | Part 1

Jurisdiction Original Legal Tradition InfluencesSingapore English law, Common law (Australian law)

Thailand Civil law or civil law system English law, US law, Islamic law

Viet Nam Civil law or civil law system French lawSource: ADB Consultants, based on research materials and market visit information.

5. DifferentRequirementsforIdentifyingInvestorsandBeneficialOwnersRequirements for identifying investors and beneficial owners are different in several countries or jurisdictions. For instance, China does not allow omnibus accounts, even for International Central Securities Depositories (ICSD), while the Republic of Korea recently revised its regulation to allow omnibus accounts for ICSDs only. This, on the other hand, is allowed in Japan and in ASEAN markets. However, there is a growing tendency or desire among regional regulators to increase monitoring.

Table 2.5 Requirements for Identifying Investors and Beneficial Owners

Jurisdiction

Regulators’ Policy related to the Necessity of Disclosure of Ultimate

Beneficial OwnerDirect or indirect Account

Holding SystemPeople’s Republic of China Yes. Beneficial owner to be disclosed.

Hong Kong, China No policy Both

Indonesia No requirement by law.Typically grouped by tax rate or domicile.

Japan No policy Direct. (Account holders have the rights directly against issuers)

Republic of Korea No policy Direct

Malaysia No policy

Philippines No policy Registered holders have legal rights against the Issuer.

Singapore No policy Both

Thailand No policy Indirect

Viet Nam No policy IndirectSource: ADB Consultants, based on research materials and market visit information.

Table 2.6 Existence of Omnibus Accounts or Nominee Concept

Jurisdiction Existence of Omnibus Securities Account Existence of Nominee ConceptPeople’s Republic of China No. Securities must be kept in the name of the beneficial owner. No.

Hong Kong, China Yes. Yes.

Indonesia Yes. Yes.

Japan Yes. Yes.

Republic of Korea Yes. But, the foreign exchange regulation in Republic of Korea does not allow omnibus accounts for payments for foreign investors. To avoid this, foreign investors who use International Central Securities Depositories can use their status as Qualified Foreign Investor and are, thus, allowed to make use of omnibus accounts.

Yes.But it cannot be applied to Foreign Investment in Bonds.

(See details “Contents of Findings, XVII. Omnibus Securities Account/Nominee Concept”)

Malaysia Yes. Yes.

Philippines Yes. Yes.

Table 2.3 continuation

continued on next page

15

ASEAN+3 Bond Market Guide | Volume 1 | Part 1 ASEAN+3 Bond Market Guide | Volume 1 | Part 1

Jurisdiction Existence of Omnibus Securities Account Existence of Nominee ConceptSingapore Yes. Yes.

Thailand Yes. Yes.

Viet Nam Yes. No.Source: ADB Consultants, based on research materials and market visit information.

6. Public Offering and Private PlacementTwo general approaches are observed in the markets when it comes to public offering:

(1) Full disclosure with specific exemptions and

(2) A clearly defined disclosure regime.

Markets are united in referring to public offerings as specified disclosure to all potential investors, whereas private placement or private offerings mean limited disclosure to only a specific investor group. However, a private offer does not mean no disclosure or no underlying regulations. In some markets, there exists a regulatory vacuum in private placement as mentioned previously. In the near future, a specific offering within professional market(s) could cover elements of both concepts of public and private offering.

Among the markets covered in the research, Hong Kong and Singapore are closer to international markets in terms of development; other ASEAN+3 markets are still developing.

Generally speaking, creating a common platform for issuance and investment of bonds among ASEAN+3 countries may not be that difficult since the necessary underlying concepts are already in place. This may also negate the discussion on whether to pursue onshore or offshore access to such a market.

Table 2.7 Existence of Exempt Regimes

JurisdictionExistence of Exempt Regimes

(Exempt Securities or Exempt Transactions in Private Placement)People’s Republic of China (PRC) “Self-regulatory Rules for Inter-bank Bond Market Non-financial Enterprise Debt Instrument on Private Placement”

provides for the process involved in private-placement instruments including issuance, registration, trading, and information disclosure, among others. Exempt regime is not applied in the PRC.

Hong Kong, China Yes.

Indonesia No. Private placement (to less than 100) is not regulated in Indonesia.

Japan Yes.

Republic of Korea Yes. The Qualified Institutional Buyer (QIB) system (and Professional only market) will be launched in May 2012 under the revised Financial Services Commission Regulation on Issuance, Public Disclosure, etc. of Securities. Korea Financial Investment Association regulation on management of the QIB system will be enacted before May 2012.

Malaysia Yes.

Philippines Yes.

Singapore Yes.

Thailand Yes.

Viet Nam No. Private placement (to less than 100) or sale to professional investors is stipulated in the amended Securities Law clearly. But private placement is not regulated as an exempted scheme.

Source: ADB Consultants, based on research materials and market visit information.

Table 2.6 continuation

16

ASEAN+3 Bond Market Guide | Volume 1 | Part 1

7. DefinitionofProfessionalInvestorsDefining professional investors is critically important to the next phase of ASEAN+3 Bond Market Forum (ABMF) discussions, as described in section C. Currently, there are varying definitions of professional investors where they exist. For instance, Indonesia acknowledges the concept but does not define it by law. In the case of Japan, the concept is clearly defined in recent legislation to create the TOKYO PRO-Bond Market. Malaysia does not have a direct definition, but the Capital Markets and Services Act of 2007 (CMSA) contains relevant provisions on how excluded offerings of bonds could be made to institutional and high net worth investors. Thailand has specific definitions for institutional investors.

Table 2.8 Existence of the Concept of Professional Investor

Jurisdiction Existence of a clear Definition of Professional Investor Concept People’s Republic of China

• Noconceptordefinitionof‘professional’(investor)isevidentinChineselaw.ThePeople’s Bank of China is mulling over the concept of Qualified Institutional Buyer (QIB).

Hong Kong, China • Professionalinvestorisdefinedinsection1ofPart1ofSchedule1totheSecurities and Futures Ordinance, etc.

Indonesia • Indonesiadoesnothavespecificdefinitionsonthistypeofprofessionalinvestors.Bapepam-LK is working on a definition of Professional Investor. Private placement (to less than 100) is not regulated in Indonesia.

Japan • TheFinancial Instruments and Exchange Act stipulates a definition for Specified (Professional) Investor and Qualified Institutional Investor.

Republic of Korea • TheFinancial Investment Services and Capital Markets Act classifies a Professional Investor. But the Republic of Korea so far does not have an exempt regime for Professional Investors. The Republic of Korea will launch the QIB market, which is an exempt regime for Professional Investors in May 2012.

Malaysia • SophisticatedInvestorisnotexplicitlydefinedintheCapital Market and Services Act 2007 (CMSA). However, the CMSA exempts sophisticated or professional investors from prospectus requirements.

Philippines • Securities Regulation Code (SRC), SRC Rules, Over-the-Counter Rules and Qualified Buyer Rules clearly define Qualified Buyer, Qualified Individual Buyer and Qualified Institutional Buyer. SRC specifies sale to Qualified Buyers as transaction exempt from registration.

Singapore • UnderSecurities and Futures Act, Accredited Investor and Institutional Investor are defined. Exemptions to prospectus requirements include exemptions for offers that are made only to institutional investors and accredited investors, etc.

Thailand • “NotificationofSecuritiesandExchangeCommission(SEC)”definesInstitutionalInvestors and High Net Worth Investors. Private Placement of corporate bond offers to institutional investors will be exempted from obligation to file disclosure documents to SEC.

Viet Nam • TheSecurities Law defines Professional Securities Investor. The Amended Securities Law defines Non-public offering of securities (Private placement) (to less than 100, etc.).

Source: ADB Consultants, based on research materials and market visit information.

17

ASEAN+3 Bond Market Guide | Volume 1 | Part 1 ASEAN+3 Bond Market Guide | Volume 1 | Part 1

Table 2.9 Existence of Professional Investor-Only Market

Jurisdiction Existence/Status Quo of the Professional Investors Only MarketPeople’s Republic of China

Does not exist. But the Inter-bank Bond Market consists of institutional participants only. The People’s Bank of China is considering the Qualified Institutional Buyer (QIB) concept.

Hong Kong, China The Hong Kong Exchanges and Clearing Limited has performed market consultation on some proposed changes to the requirements for the listing of debt issues to professional investors only in December 2010 and the Rule amendments were effected in November 2011.

Indonesia Does not exist.

Japan Exists. TOKYO PRO-BOND market with listing on the TOKYO AIM.

Korea The QIB market and trading system will be launched within 2012.

Malaysia TheSecuritiesCommissionandBankNegaraMalaysiaintroduced‘ExemptRegime.’

Philippines Exemptions are granted for particular securities and transactions.

Singapore Exists. There is a market for professionals which are exempted from prospectus requirements.

Thailand Private Placement is exempt from full filing requirement.

Viet Nam Does not exist. Source: ADB Consultants, based on research materials and market visit information.

8. Documentation LanguageWith regards to documentation language, there is a need to study this area in greater detail. Some jurisdictions have added other languages for documentation. One such case is in Hong Kong, China where Chinese is now an acceptable documentation language.

9. DefiningSelf-RegulatoryOrganizationsThe definitions of SROs may differ by market but their functions are comparable.

Table 2.10 Definitions of Self-Regulatory Organizations

Jurisdiction Name Main Functions People’s Republic of China

Inter-bank Bond Market (National Association of Financial Market Institutional Investors [NAFMII])In 2007, NAFMII was officially established.

NAFMII is mainly responsible for the self-regulatory management of the over-the-counter (OTC) market. The establishment of NAFMII fills in the void of a self-regulatory organization (SRO) in the OTC market, forming a market management mode that comprises both government supervision and market self-regulatory management. • Promoting investor protection mechanism. NAFMII is promoting the investor protection mechanism in

the non-financial enterprise debt capital market and formulated self-regulatory normative documents such as the “Rules for Meetings of Non-financial Enterprise Debt Holders in the Inter-bank Bond Market.”

1. Guiding and regulating market with the “Self-Governing Rules and Standardization of Management system of the Market.”

2. Further deregulation for issuance of bonds and notes in the inter-bank market.

Hong Kong, China -- No SROs in Hong Kong bond market.

Indonesia 1. The Indonesia Stock Exchange (IDX)

2. The Indonesian Central Counterparty 3. The Indonesian Central Securities Depository

---Each regulates its own areas of operations, subject to Bapepam-LK approval.

As one of the three SROs of the capital market licensed by Bapepam-LK, IDX:(1) facilitates and regulates the Exchange. Specifically, it discusses, prepares, acquires approval from

Bapepam-LK, issues, and changes Listing Regulations, Trading Regulations and Membership Regulations;

(2) develops a mechanism for organizing and monitoring the Exchange; (3) implements Good Corporate Governance practice based on IDX’s Corporate Governance Principles;

and (4) develops infrastructure and technologies projects with other SROs.

To produce professional human resources that can encourage capital market growth, together with other SROs, IDX formed the Association of Indonesian Capital Market Education (P3MI). In 2010, P3MI, in cooperation with University of Indonesia (UI), founded Indonesia Capital Market Institute (TICMI). TICMI is focusing on giving education and training skills to candidates aspiring to become underwriters, investment managers and broker/dealers.

continued on next page

18

ASEAN+3 Bond Market Guide | Volume 1 | Part 1

Jurisdiction Name Main Functions Japan Japan Securities Dealers

Association (JSDA), Tokyo Stock Exchange Group (TSE), TOKYO AIM

JSDA is the full-fledged SRO for the securities industry in Japan. It issues a variety of rules and market practices/guidelines for bond market participants.

Rules: When JSDA members violate these rules, they are subject to disciplinary action by JSDA. JSDA takes into account market conditions and the practical reality of transactions in establishing, revising and abolishing rules for the purpose of achieving fair and smooth transactions in the Japanese market, thereby contributing to the protection of investors. During the rule-making procedure, a draft of rules is prepared first through deliberations mainly by JSDA members. The draft is then subjected to public comment and other processes, and finally approved by JSDA.

Guidelines: Guidelines are practical rules that JSDA requests participants in the bond market to comply with (thus recognized as “best practice”). As they are merely practices, those who do not comply are not penalized. However, as voluntary compliance with these guidelines by the overall market contributes to smooth and efficient transactions, most market participants observe the guidelines. Consequently, JSDA collects and considers the opinions of market participants when setting new guidelines or revising /abolishing old ones.

Standard Procedures, etc.: Besides the above, JSDA issues from time to time notices to members in advance regarding standard procedures, etc.

TSE’s role as a self-regulatory organization: It examines companies to assess their suitability as listed companies. It requires these companies to comply with disclosure requirements so that investors are able to make informed decisions, and it provides a market place for those companies’ securities to be traded. Pursuant to the Financial Instruments and Exchange Act (FIEA), TSE has self-regulatory functions to maintain a transparent, equitable and reliable market. The TSE has two units in relation to its self-regulatory function: (1) the Listing Regulation Unit deals with issues related to listing and (2) the Compliance Unit deals with issues related to trading participants.

Self-Regulation Punishment and Dealing with Offenders: TSE Regulation handles any trading participant that violates the law or stock exchange rules in accordance with article 34 of the official trading participant regulations. The “Disciplinary Committee” is an advisory body that, in addition to conducting inquiries, also handles penalty funds, censure, trading suspension, and limiting or canceling trading capabilities, etc.

TOKYO AIM’s Role as TOKYO PRO-BOND Market SRO: TOKYO PRO-BOND Market-related rules and regulations are provided by TOKYO AIM. TOKYO AIM is an SRO for the TOKYO PRO-BOND Market. Disclosure requirements under the FIEA such as Securities Registration Statements do not apply to the securities listed on the TOKYO PRO-BOND Market.

JSDA and TOKYO AIM: Trading on the OTC market is regulated under the JSDA’s Self-regulatory Rules and Guidelines for the Bond Market. “TOKYO AIM’s TOKYO PRO-BOND Market Listing Regulations and Enforcement Rules” and “JSDA’s Self-regulatory Rules and Guidelines for the Bond Market” have a mutually important and complimentary relationship.

Republic of Korea Korea Financial Investment Association (KOFIA),Korea Exchange (KRX)

KOFIA is an incorporated membership organization created to maintain business order between members, assuring fair trade, protecting investors, and promoting the sound development of financial investment services. Members of KOFIA are financial investment firms, general administration companies, collective investment scheme management companies, bond assessment companies and members under the conditions prescribed by the articles of KOFIA. KOFIA aims to promote fair business practices among member companies, create a fair business culture in the securities trading market, and maximize the function of investor protection. As such, KOFIA undertakes such activities as self-regulation to protect investors and maintain market order among member companies; dispute mediation between members regarding their business activities; registration and management of investment advisers and managers; management of OTC trading for non-listed stocks and non-listed and listed bonds; and establishment of dispute mediation rules for self-mediation of conflicts in the industry.

KRX aims to fix and stabilize fair prices in the transactions of securities and exchange-traded derivatives, and facilitate the stability and efficiency of other transactions. It established and operates the stock market, the KOSDAQ Market, and the derivative market. Under the Financial Investment Services and Capital Markets Act, the stock market is established for the trading of securities, such as debt securities, equity securities, beneficiary securities, investment contract securities, derivative-combined securities, and securities depositary receipts.

Table 2.10 continuation

continued on next page

19

ASEAN+3 Bond Market Guide | Volume 1 | Part 1 ASEAN+3 Bond Market Guide | Volume 1 | Part 1

Jurisdiction Name Main Functions Malaysia Bursa Malaysia,

Financial Market Association of Malaysia (ACI Malaysia, quasi SRO)

Bursa Malaysia (Exchange): Securities Commission Malaysia (SC) is the primary regulator of the Exchange. The SC relies on Bursa Malaysia to perform extensive regulatory functions that extend beyond their market operations, including regulating members’ business conduct. Bursa Malaysia is also responsible for marketplace surveillance. Bursa Malaysia, on behalf of the SC, supervises and enforces disclosure standards for listed companies. It adopts a thematic approach to achieve the goals and objectives of ensuring effective market regulation. Under this approach, in discharging its regulatory role, Bursa Malaysia will focus on certain key themes. These themes are regularly reviewed to ensure relevance in a progressive environment. The six themes are as follows: (1) Enhancing standards of corporate governance among listed issuers, (2) Improving standards of disclosure, (3) Promoting high standards of business conduct and self-regulation among brokers, (4) Enhancing the effectiveness of enforcement, (5) Elevating the level of education and awareness in the industry, and (6) Managing crisis in light of the global financial turmoil.

Financial Market Association of Malaysia (ACI Malaysia): The Bond Dealers Association was established in June 1996 to represent the industry’s views and work with regulatory authorities to promote the bond market. On the other hand, ACI Malaysia was established in 1974 to monitor, develop and improve industry standards, and to bring them in line with international best practice. ACI Malaysia, whose membership comprises staff from treasury operations of Malaysia’s financial institutions (including insurance companies), has adopted a Code of Conduct for the industry. To qualify as a member of ACI Malaysia, a rigorous qualifying examination must be passed. ACI Malaysia qualifies as an SRO in its function and actions; however, ACI Malaysia has not yet been conferred official SRO credentials.

Philippines PDS Group (Philippine Dealing and Exchange [PDEx])

The Securities and Exchange Commission granted PDEx the license to act as an SRO for the Inter-Dealer, Inter-Professional and Public Markets. As an SRO, PDEx has adopted the PDEx Rules that governs all transactions dealt on the PDEx Trading Platform for fixed-income securities.

Singapore Singapore Exchange (SGX)

Being a listed exchange and frontline regulator, SGX is considered an SRO. SGX serves as an SRO for the markets and clearing houses that it operates in Singapore. It works closely with relevant regulatory authorities, including the Monetary Authority of Singapore and the Criminal Affairs Department, to develop and enforce rules and regulations to build an enduring marketplace. SGX bears commercial responsibilities in addition to its regulatory duties. While this dual role may present conflicts, SGX has established a framework to manage such conflicts.SGX undertakes various regulatory functions to promote a fair, orderly and transparent marketplace as well as a safe and efficient clearing system. These functions are handled by the following regulatory departments: (1) Issuer Regulation, (2) Catalyst Regulation, (3) Member Supervision, (4) Market Surveillance, (5) Enforcement, (6) Risk Management, (7) Clearing Risk, and (8) Regulatory Development and Policy.

Thailand Thai Bond Market Association (ThaiBMA), Exchanges

ThaiBMA is an SRO licensed to run an efficient market and act as an information center for the secondary bond market. It is responsible for developing the market, establishing market conventions and standards, and acting as a bond pricing agency. It also provides a forum for market professionals to move towards a more mature and sophisticated Thai bond market.The membership of ThaiBMA can be classified into three types, each of which is subject to different membership fees and requirements:

(1) Ordinary members are dealers. (2) Extraordinary members are inter-dealer brokers. (3) Associate membership is provided for a dealer that has monthly average trading value in the past one year

of less than THB100 million per month.