companies act 2013 : loans, advances and related party transactions (sec. 185, 186, 188)

TRANSCRIPT

COMPANIES ACT 2013

Loans, Advances & RPTs

CA Chintan N. Patel

Naresh J. Patel & Co.

Chartered Accountants

Ahmedabad

www.nareshco.com

LOANS &

INVESTMENTS

CA Chintan Patel

Sec. 185 : Loan to Directors

Sec. 186 : Loan and Investment by Company

Loans by Company

To

Directors

OR

To

Any Other OR

Company in which

director are interested

Sec. 185

Company

Sec. 186

CA Chintan Patel

Section 185:

A company cannot, directly or indirectly, give any loan,

including loan represented by a book debt, to any of its

directors or to any other person in whom the director is

interested or give any guarantee or provide any security in

CA Chintan Patel

interested or give any guarantee or provide any security in

connection with any loan taken by him or such other

person.

Loan:

A loan is defined by the Oxford English Dictionery as ‘a thing lent,

something the use of which is allowed for a time, on the

understanding that it shall be returned or an equivalent given; esp.,

a sum of money lent on these conditions and usually with interest.’

The essential requirement of a loan is the advance of money (or of

some article) upon the understanding that it shall be returned, and

it may or may not carry interest.

CA Chintan Patel

Indirect:

The word ‘indirect’ used means that the co should not give a loan

to director through the agency of one or more intermediaries.

However the word ‘indirect’ cannot be read as converting what is

not a loan into a loan.

[Dr. Fredie Ardeshir Mehta v Union of India [1991] 70 Comp. Cas

210 (Bom.)

‘any other person in whom director is interested’ :

(a) any director of the lending company, or of a company which is its

holding company or any partner or relative of any such director;

(b) any firm in which any such director or relative is a partner;

(c) any private company of which any such director is a director or

member;

(d) any body corporate at a general meeting of which not less than

25% of the total voting power may be exercised or controlled by any

CA Chintan Patel

25% of the total voting power may be exercised or controlled by any

such director, or by two or more such directors, together; or

(e) any body corporate, the Board of directors, managing director or

manager, whereof is accustomed to act in accordance with the

directions or instructions of the Board, or of any director or directors,

of the lending company.

Body Corporate :Section 2(11) of 2013 Act:

It includes a company incorporated outside India but does not include a co-operative

society and any other as specified by CG.

Characterstics

Incorporated under some law, Perpetual succession, Ability to hold property in its own

name , Legal entity apart from the members

Examples:

• All companies registered under Indian Companies Act

• All companies registered under any Act outside India

• Any Corporation registered under any special law in India or abroad

CA Chintan Patel

• Any Corporation registered under any special law in India or abroad

• Public financial institutions u/s 2(72) of Companies Act 2013

• Nationalised banks incorporated under Banking Companies (Acquisition & Transfer

of Undertakings) Act 1970

• LLPs (LLP Act 2008)

Not Body Corporates:

• Proprietorship concerns

• Partnership firms (other than LLPs)

• HUFs

• Societies registered under Societies Registration Act

• Mutual funds managed by trustees (UTI is a body corporate)

Prohibition on Loan

by Company To

Director

Partnership Firm(If Director or Relative

of Director is a partner)

IndividualOther than

Individual

Body Corporate(If BOD, MD or manager

Sec. 185

Summary

CA Chintan Patel

Any Partner

of Director

Any Relative

of Director

Director of

Holding Co.

Pvt. Ltd. Co.(If Director is a director

or member)

Body Corporate(If Director/s having

atleast 25% voting power)

(If BOD, MD or manager

accustomed to act as per

directions of director/s,

board of lending co.

Subject to EXCEPTIONS

Exceptionsof Sec. 185

Loan to

Managing or

Whole time

Director

LGS by a company

in the ordinary

course of business

LGS by Holding

Co. to Wholly

Owned

Subsidiary Co.

GS by Holding Co.

to Subsidiary Co. in

respect of loan by

Bank or FI

CA Chintan Patel

Provided that such Loans are utilised by the

subsidiary for its principal business activitiesInterest is charged at a rate

not less than bank rate

As a part of condition of service to all employees

OR

Pursuant to scheme approved by members in SR

Section 185 : Practical Solutions

Convert Lender

& Borrower to

LLP

Convert Borrower

Company to Limited

Company

(If Common Directors

hold Less Than 25% of

Borrowing company)

Change in

Directorship/

Shareholding

1) Appoint New i.e Uncommon Director

2) Resign Common Director from either Company

(in which Director is not share holder)

3) Change the Shareholding in such a way that no Director of

Borrower / Lender are shareholder of other company.(i.e.

Director Should hold the share in which they are director.)

4) Shares/Directorship Held by Relatives of the Directors not

considered.

CA Chintan Patel

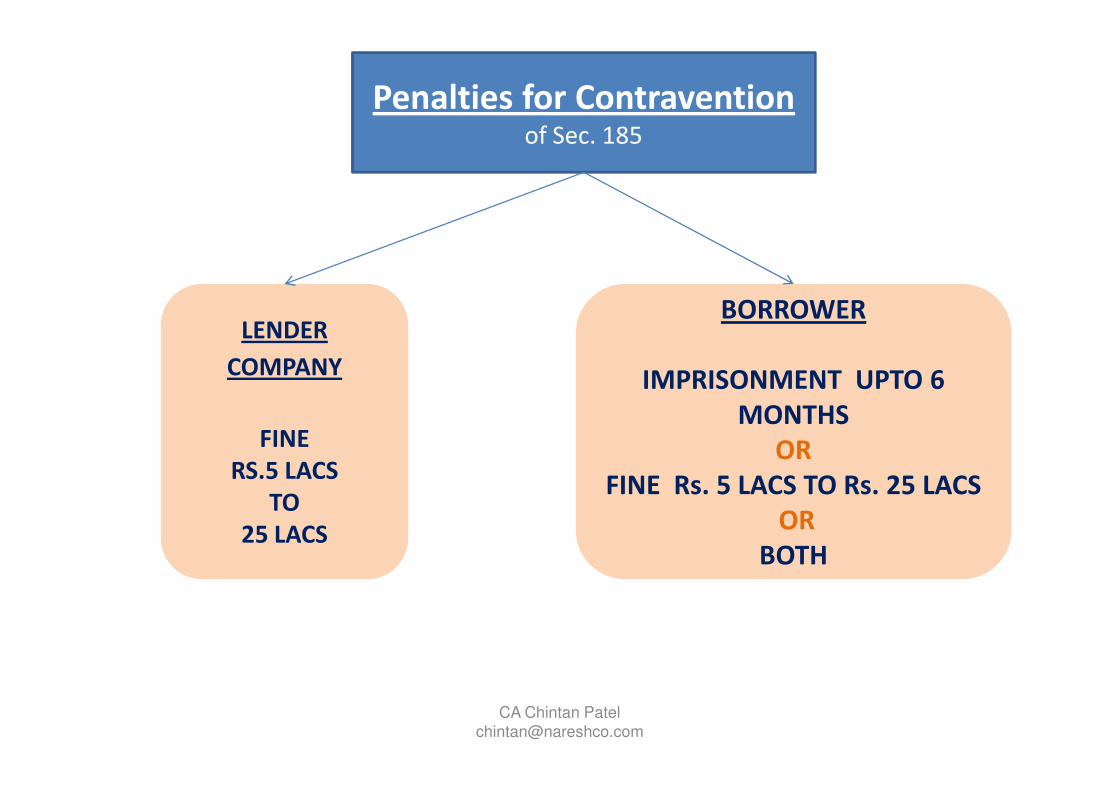

Penalties for Contraventionof Sec. 185

LENDER

COMPANY

BORROWER

IMPRISONMENT UPTO 6

CA Chintan Patel

FINE

RS.5 LACS

TO

25 LACS

MONTHS

OR

FINE Rs. 5 LACS TO Rs. 25 LACS

OR

BOTH

Sec 186 – Loan & Investment by company(corresponding to sec 372A of Act,1956)

(1) Without prejudice to the provisions contained in this Act, a co shall unless otherwise prescribed, make investment through not more than two layers of investment co’s :

Provided that the provisions of this sub-section shall not affect, -

(i) a co from acquiring any other co incorporated in a (i) a co from acquiring any other co incorporated in a country outside India if such other co has investment subsidiaries beyond two layers as per the laws of such country ;

(ii) a subsidiary co from having any investment subsidiary for the purpose of meeting the requirements under any law or under any rule or regulation framed under any law for the time being in force.

CA Chintan Patel

LOANS & INVESTMENTS

BY COMPANIES

Section 186

NO

Investments through

more than two layers

of Investment Co.

Upto

1.Give loan to any person OR body corporate

2. Give guarantee or provide security in connection with

loan

3. Purchase subscription, purchase securities

Upto

Higher of 60% of

Paid up Capital

(+) Free Reserves

(+) Security Premium

100% of

Free reserves

(+) Security Premium

Alternate Route :

If Loan Exceeds the above threshold limit, then Prior Approval by Special Resolution at

General meeting is MUST . (Subject to Exceptions)

OR

CA Chintan Patel

Exceptions to Prior Approval

No Prior Approval required:

- L G S to WOS

- L G S to Joint Venture

- Investment (Acquisition) by holding company by way

of subscription, purchase or otherwise of securities of subscription, purchase or otherwise of securities

of WOS

CA Chintan Patel

Exception to Sec. 186(a) L G S by a banking company or insurance company or a

housing finance company in the ordinary course of its

business or a company engaged in the business of financing of

companies or of providing infrastructural facilities ;

(b) to any acquisition –

(i) made by a non-banking financial company registered

under chapter III-B of the RBI Act 1934 and whose principal under chapter III-B of the RBI Act 1934 and whose principal

business is acquisition of securities ;

Provided that exemption to non-banking financial company

shall be in respect of its investment and lending activities

(ii) made by a company whose principal business is the

acquisition of securities ;

(iii) of shares allotted in pursuance of clause (a) of sub-section

(1) of section 62.

CA Chintan Patel

Disclosure in Financial Statement

• Full particulars of the L G S I and

• Purpose for which it is proposed to be utilised by

the borrower - L G S (Not I) .

CA Chintan Patel

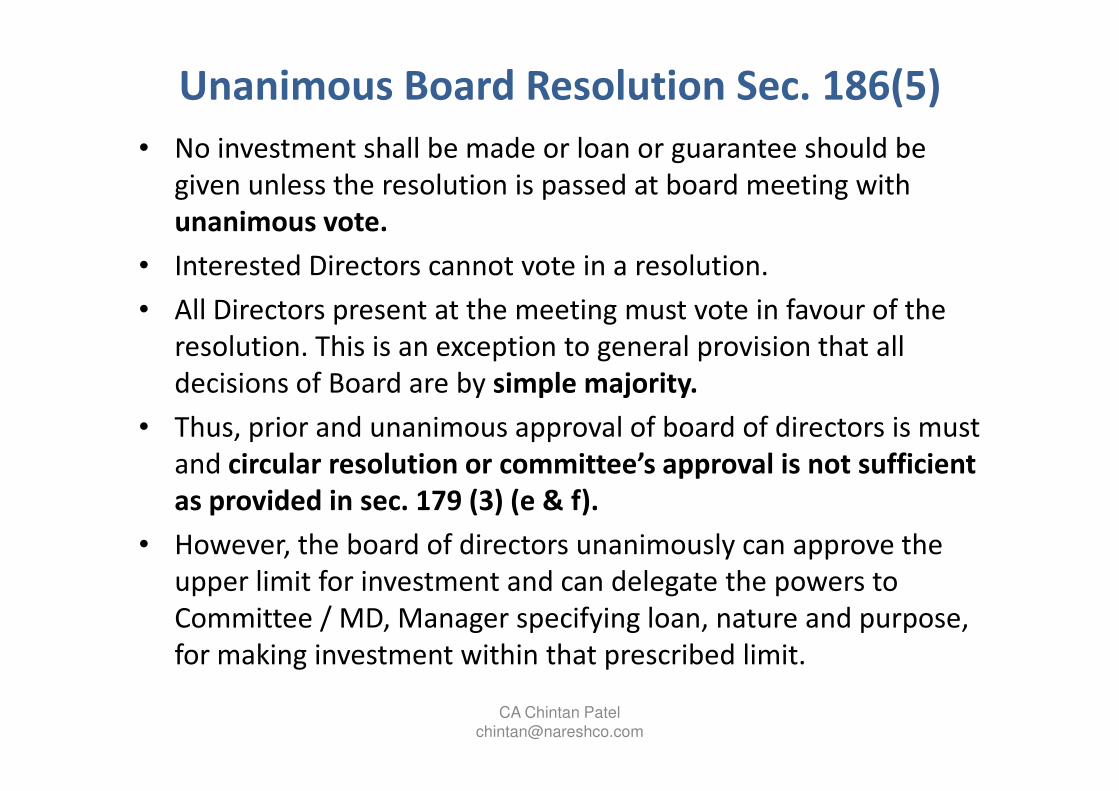

Unanimous Board Resolution Sec. 186(5)

• No investment shall be made or loan or guarantee should be

given unless the resolution is passed at board meeting with

unanimous vote.

• Interested Directors cannot vote in a resolution.

• All Directors present at the meeting must vote in favour of the

resolution. This is an exception to general provision that all

decisions of Board are by simple majority. decisions of Board are by simple majority.

• Thus, prior and unanimous approval of board of directors is must

and circular resolution or committee’s approval is not sufficient

as provided in sec. 179 (3) (e & f).

• However, the board of directors unanimously can approve the

upper limit for investment and can delegate the powers to

Committee / MD, Manager specifying loan, nature and purpose,

for making investment within that prescribed limit.

CA Chintan Patel

Prior approval of Public Financial Insti. (PFI)

• Prior approval of Public Financial Institution where

any tem loan is subsisting if

(i) Company has made default in repayment of loan

or interest to PFI OR

(ii)The aggregate of LGSI along with proposed

exceeds the limit prescribed in sec. 186 (2)

CA Chintan Patel

SEC 186 – Loan & Investment by company

• No company, which is registered under section 12 of the

SEBI Act 1992 and covered under such class or classes of

companies as may be prescribed, shall take inter-

corporate loan or deposits exceeding the prescribed

limit and such company shall furnish in its financial

statements the details of the loan or deposits.statements the details of the loan or deposits.

• No loan shall be given under this section at a rate of

interest lower than the prevailing yield of one year,

three year, five year or ten year government security

closet to the tenure of the loan..

CA Chintan Patel

Defaulter in Repayment

No company which is in default in the repayment of

deposits accepted before or after the commencement

of this Act or in payment of interest thereon, shall give

any loan or give any guarantee or provide any security or

make an acquisition till such default is subsisting.make an acquisition till such default is subsisting.

CA Chintan Patel

Register of L G S I

• Every company to keep a register which shall contain

the particulars.

• To keep register at the registered office of the company

and

(a) shall be open for inspection at such office ; and

(b) extracts may be taken therefrom by any member,

and copies thereof may be furnished to any member of

the company on payment of fees as prescribed in the

Articles not exceeding Rs. 10 per page.

CA Chintan Patel

Penalty u/s. 186

• Company:

Fine : Rs. 25,000 to Rs. 5 lakhs

• Officers

Imprisonment : upto 2 years andImprisonment : upto 2 years and

fine Rs. 25,000 to Rs. 5 lakhs

CA Chintan Patel

Related PartyDefinition of Related Party : Sec. 2(76)

Director, KMP or their relative

Firm in which a director or manager or his relative is a partner

Private Company in which director or manager is a member or director

Public Company in which director or manager is a director AND holds along with his

relatives > 2% of its paid up share capital

Any Body Corporate whose BOD, MD or manager is accustomed to act in

accordance with advise, director or manager (Except in professional capacity)

Co. Act

13

CA Chintan Patel

accordance with advise, director or manager (Except in professional capacity)

Any person on whose advise, directions, or instructions, a director or manager is

accustomed to act. (Except in professional capacity)

Any Company which is H, S or A of Company or Subsidiary of H Co.

Director, KMP of the holding company or relative

2(77) : Relative :

Members of HUF, Husband or Wife,

As may be prescribed

Father(incld S-F), Mother (incld S-M), Brother (incld S-B), Sister (incld S-S)

Son (incld S-S), Son’s Wife, Daughter, Daughter’s Husband

Related Party(a) enterprises that directly, or indirectly through one or more intermediaries, control,

or are controlled by, or are under common control with, the reporting enterprise

(this includes holding companies, subsidiaries and fellow subsidiaries);

(b) associates and joint ventures of the reporting enterprise and the investing party or

venturer in respect of which the reporting enterprise is an associate or a joint

venture;

(c) individuals owning, directly or indirectly, an interest in the voting power of the

reporting enterprise that gives them control or significant influence over the

enterprise, and relatives of any such individual;

AS - 18

enterprise, and relatives of any such individual;

(d) key management personnel and relatives of such personnel;

(e) enterprises over which any person described in (c) or (d) is able to exercise

significant influence. This includes enterprises owned by directors or major

shareholders of the reporting enterprise and enterprises that have a member of

key management in common with the reporting enterprise.

CA Chintan Patel

Relative – in relation to an individual, means the spouse, son, daughter, brother, sister,

father and mother who may be expected to influence, or be influenced by, that

individual in his/her dealings with the reporting enterprise.

Related Party• Parties are considered to be related if one party has the ability to control

the other party or exercise significant influence over the other party,

directly or indirectly, in making financial and/or operating decisions and

includes the following :

SEBI

Individual (IND) Entity

- Related party u/s. 2(76)

CA Chintan Patel

- Related party u/s. 2(76)

- Control or joint control or

significant influence over Co.

(IC)

- KMP of company or parent

- Related party u/s. 2(76)

- Entity and company are members of same

group (each parent, subsidiary, fellow sub)

- One entity is Asso./JV of other entity or of a

member of a group of other entity

- Both entities are JV of same third party

- One entity is JV of third entity and other

entity is Asso. Of third entity

- Entity is post employment benefit for the

benefit of employees of co. Or related co.

- Entity Controlled/Jointly Conrolled by IND

- IC has significant infl. over entity or parent

Related Party

Transactions?

Is it Specified

Transaction?

Transactions in ordinary

course of business and Arms

Length Pricing?

Y

Y

N

Sec. 188 Not

Applicable

No Prior

Approval

Y

N

Sec. 188

N

CA Chintan Patel

Transaction >

Specified Amt or

PC > Rs. 10 Cr?

Approval of Sh. Holders by Sp. Resol.

AND

Board Approval

Prior Approval

of Board

Y

N

N

Director’s Report to disclose each Related Party Transaction (irrespective of its

arms length nature) along with justification for entering into same.

Prior Approval of Company by Special Resolution

for Specified but not Arms Length Transactions

Is the Company Having Paid up

share Capital > Rs. 10 Cr.?

Prior Approval

SR Required

YN

Prior Approval

SR Required

ONLY IFGoods or Material

Sale, purchase or Supply

Directly or through Agent Services

CA Chintan Patel

> 25% of Annual Turnover Availing or rendering

Directly or through Agent

> 10% of Net WorthProperty

Buying, selling, disposing

Directly or through Agent

> 10% of Net Worth

Leasing of Property

> 10% of Net Worth

Appointment

To office or place of profit

In Co., Subs, Asso

> Rs. 2.5 Lacs p.m.

Underwriting

Remuneration for underwriting

subscription of Sec. or derivative

> 1% of Net Worth

Specified TransactionsCo. Act 1956 Co. Act 2013 SEBI Listing

Agreement

Sale, purchase or supply of

any goods, material or

services

-Sale, purchase or supply of any

goods or material

-Availing or rendering of any

services

Transfer of

resources, services

or obligations

between a

company and

a related party,

regardless, of

whether a price is

Underwriting the

subscription of any

shares in or debenture.

Underwriting the subscription of

any shares in or derivatives

thereof.whether a price is

charged.Selling or otherwise disposing of, or

buying, property of any kind

Leasing of property of any kind

Appointment of any agents for

purchase or sale of goods,

materials, services or property;

Related party’s appointment to

any office or place of profit in the

company, its subsidiary company or

associate companyCA Chintan Patel

Related Party

Transactions?

Is it Material?

Prior Approval of Audit

CommitteePrior Approval of

Audit Committee

Y

Y

No Action

N

SEBI

N

CA Chintan Patel

Committee

+

Prior Approval of Sh. Holders

by Sp. Resol. (Related Party

can not vote)

Audit Committee

Material :

if the transaction(s) to be entered into individually or collectively during a

financial year exceeds:

5% of the Annual Turnover; or 20% of the networth; Whichever is higher

Disclosure of RPT

• Details of all material transactions with

related parties shall be disclosed quarterly

along with the compliance report on

corporate governance.

SEBI

corporate governance.

• The company shall disclose the policy on

dealing with Related Party Transactions on its

website and also in the Annual Report.

CA Chintan Patel

Sec. 188 ExceptionsNot Apply to :

Any transactions entered into in its ordinary course of business other than

transactions which are not on an arm’s length basis.

Arm’s length transaction:

Transaction between 2 related parties that is conducted as if they were

unrelated, so that there is no conflict of interest.

Ordinary Course of business:Ordinary Course of business:

• SA 550 Related Party:

Examples of transactions outside the entity’s normal course of business:

– Complex equity transactions, such as corporate restructurings or acquisitions.

– Transactions with offshore entities in jurisdictions with weak corporate laws.

– The leasing of premises or the rendering of management services by the entity to another party if

no consideration is exchanged.

– Sales transactions with unusually large discounts or returns.

– Transactions with circular arrangements, for example, sales with a commitment to repurchase.

– Transactions under contracts whose terms are changed before expiry.CA Chintan Patel

Sec. 188 Related Party Transactions

office or place of profit :

i) where it is held by a director, if he receives anything by way of remuneration over & above remuneration to which he is entitled as director, by way of salary, fee, commission, perqs, rent free accommodation or otherwise;

ii) by any individual, other than director, or by any firm/ pvt co / body corporate holding it receives from the co anything by way of remuneration, salary, commission, perqs, any rent free accommodation or remuneration, salary, commission, perqs, any rent free accommodation or otherwise

If Not Approved:

Where entered without obtaining consent of board/ approval by special resolution in GM and if not ratified by Board/GM within 3 months, such contract voidable at the option of board and director concern (sanctioning) shall indemnify against any loss incurred by it.

Open to the co to proceed against director / any other employee for recovery of any loss

CA Chintan Patel

Listed Co.

- Imprisonment upto 1 year

- Fine not less than

Any Other Co.

Fine not less than Rs.25,000/-

may extend to Rs. 5 lacs

Penalty for Contravention of Sec. 188

Any director/ any other employee of co who entered into / authorized such contract/ arrangement in violation, shall

CA Chintan Patel

- Fine not less than

Rs.25,000/- may extend to Rs.

5 lacs

or

- Both

may extend to Rs. 5 lacs

CA Chintan N. Patel

+91-90999 21163

CA Chintan Patel

Naresh J. Patel & Co.

Chartered Accountants

www.nareshco.com