city of la board book 11-15-11 the previous twelve months most securitized products have u.s....

TRANSCRIPT

City of Los Angeles

November 15, 2011

Presenters:Mike NormanSenior Principal

Robert CrandallSenior Associate

Experience Performance Consistency

GalliardCapital Management, Inc.

Experience. Performance. Consistency.

City of Los Angeles Stable Value Fund

Galliard ContactsRelationship Management

Mike NormanSenior [email protected]

Section I: Galliard Capital Management Update

Section II: A Brief Refresher: What is Stable Value?

Andy ApostolSenior [email protected]

Portfolio Analyst

Section III: Stable Value Market Update Economic Overview

Section IV: City of Los Angeles 3Q’11 Portfolio Update

Robert CrandallSenior [email protected]

Other Contact(s)

John Caswell, CFAManaging [email protected]

Karl TourvilleKarl TourvilleManaging [email protected]

Galliard Client Service

612 667 3220

City of Los Angeles

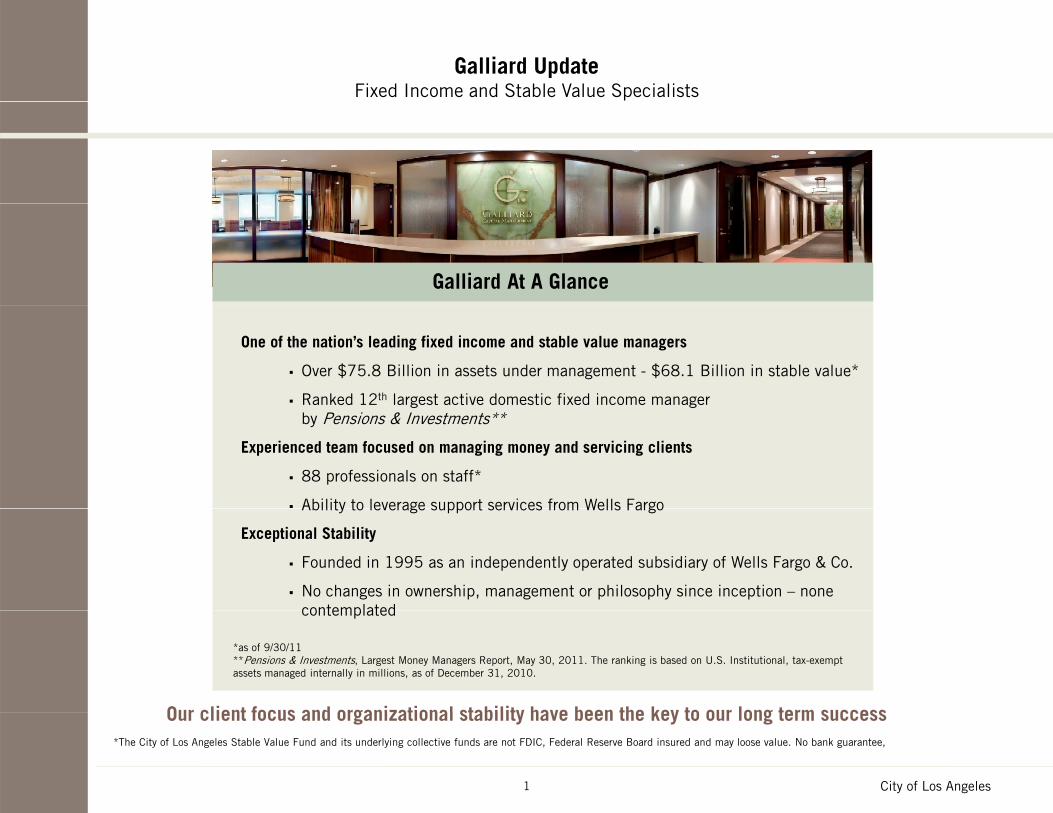

Galliard UpdateFixed Income and Stable Value Specialists

Galliard At A Glance

One of the nation’s leading fixed income and stable value managers

Over $75.8 Billion in assets under management - $68.1 Billion in stable value*

Ranked 12th largest active domestic fixed income managerg gby Pensions & Investments**

Experienced team focused on managing money and servicing clients

88 professionals on staff*

Ability to leverage support services from Wells FargoAbility to leverage support services from Wells Fargo

Exceptional Stability

Founded in 1995 as an independently operated subsidiary of Wells Fargo & Co.

No changes in ownership, management or philosophy since inception – none contemplated

Our client focus and organizational stability have been the key to our long term success

contemplated

*as of 9/30/11**Pensions & Investments, Largest Money Managers Report, May 30, 2011. The ranking is based on U.S. Institutional, tax-exempt assets managed internally in millions, as of December 31, 2010.

1 City of Los Angeles

Our client focus and organizational stability have been the key to our long term success*The City of Los Angeles Stable Value Fund and its underlying collective funds are not FDIC, Federal Reserve Board insured and may loose value. No bank guarantee,

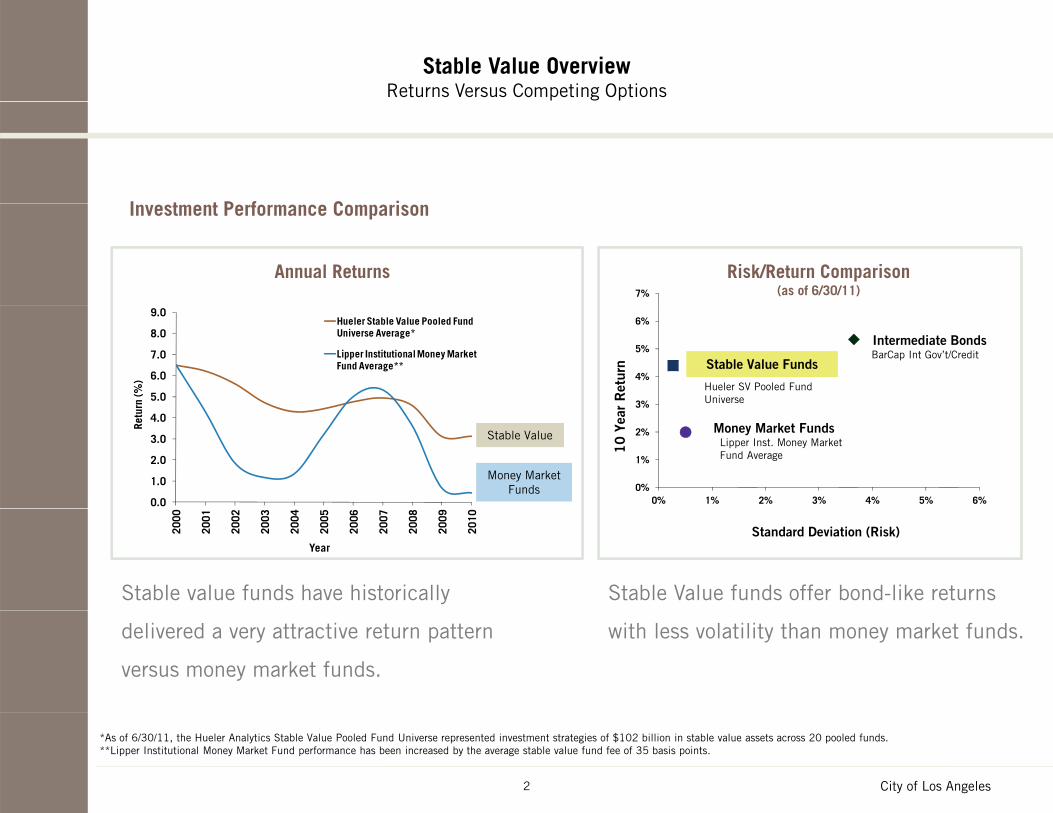

Stable Value OverviewReturns Versus Competing Options

I t t P f C iInvestment Performance Comparison

Annual Returns Risk/Return Comparison(as of 6/30/11)7%

3%

4%

5%

6%

Stable Value Funds

Intermediate Bonds

Hueler SV Pooled Fund Universe

BarCap Int Gov’t/Credit

r R

etur

n

5.0

6.0

7.0

8.0

9.0

rn (%

)

Hueler Stable Value Pooled Fund Universe Average*

Lipper Institutional Money Market Fund Average**

Stable Value

Money MarketFunds 0%

1%

2%

3%

0% 1% 2% 3% 4% 5% 6%

Money Market FundsLipper Inst. Money Market Fund Average1

0 Y

ear

0.0

1.0

2.0

3.0

4.0

Retu

r

Stable Value funds offer bond-like returns Stable value funds have historically

Standard Deviation (Risk)2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

Year

with less volatility than money market funds.delivered a very attractive return pattern

versus money market funds.

City of Los Angeles

*As of 6/30/11, the Hueler Analytics Stable Value Pooled Fund Universe represented investment strategies of $102 billion in stable value assets across 20 pooled funds.**Lipper Institutional Money Market Fund performance has been increased by the average stable value fund fee of 35 basis points.

2

Stable Value OverviewWhat Does the Fund Invest In?

Security Backed Contract (Wrap Contract)A fixed income (bond) portfolio combined withA fixed income (bond) portfolio combined with an investment contract issued from a bank or

insurance company

Investment Contracts (wrap contracts)

• Issued by banks and insurance companies

Book Value Contract

insurance companies

Underlying Fixed Income Portfolio

U.S. Gov't/Agency

Commercial Mortgage Backed

Securities 8%

Residential Mortgage Backed

Securities 35%

Sovereign/ Supranational

2%

Cash 4%

Portfoliog y9%

Other U.S. Gov't 11%

Taxable Municipal

5%

Corporates26%

8%

Underlying fixed income portfolio managed by a company different than the bank or insurance company providing the investment (wrap) contract

Th i d i d f ili i i ’ bili

3 City of Los Angeles

The wrap contract is designed to facilitate participants’ abilityto transact at book value (principal plus accrued interest)

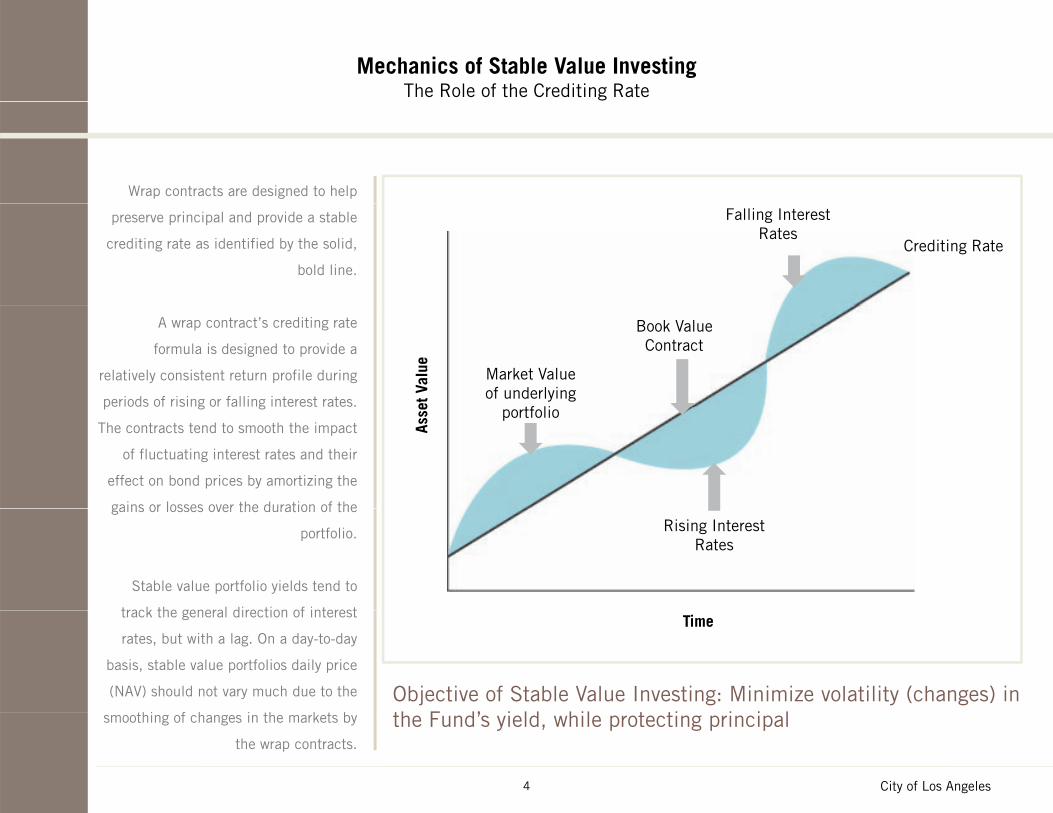

Mechanics of Stable Value Investing The Role of the Crediting Rate

Wrap contracts are designed to help

preserve principal and provide a stable

crediting rate as identified by the solid,

bold line.

Falling Interest Rates

Crediting Rate

A wrap contract’s crediting rate

formula is designed to provide a

relatively consistent return profile during

periods of rising or falling interest rates.

Market Valueof underlying

tf li

Book Value Contract

et V

alue

p g g

The contracts tend to smooth the impact

of fluctuating interest rates and their

effect on bond prices by amortizing the

gains or losses over the duration of the

portfolioAs

se

gains or losses over the duration of the

portfolio.

Stable value portfolio yields tend to

track the general direction of interest

Rising Interest Rates

track the general direction of interest

rates, but with a lag. On a day-to-day

basis, stable value portfolios daily price

(NAV) should not vary much due to the

hi f h i h k b

Time

Objective of Stable Value Investing: Minimize volatility (changes) in th F d’ i ld hil t ti i i l

4 City of Los Angeles

smoothing of changes in the markets by

the wrap contracts.

the Fund’s yield, while protecting principal

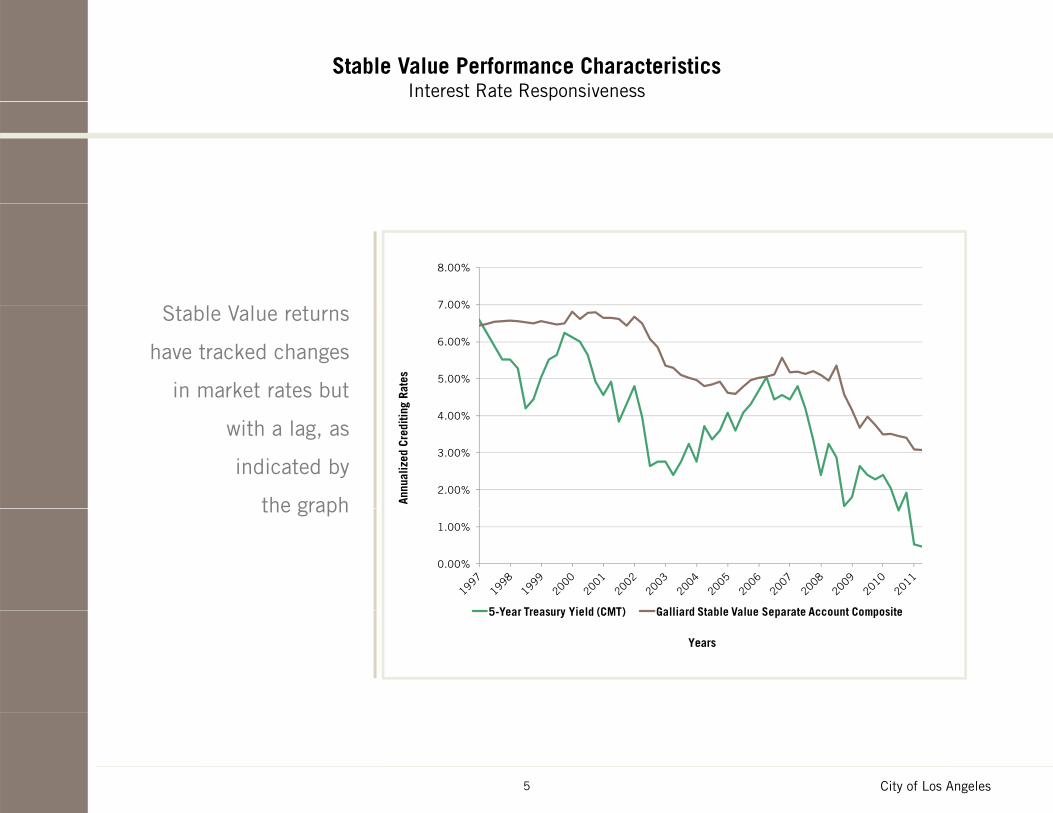

Stable Value Performance CharacteristicsInterest Rate Responsiveness

7 00%

8.00%

S

5.00%

6.00%

7.00%Stable Value returns

have tracked changes

in market rates but g

Rate

s

2.00%

3.00%

4.00%

with a lag, as

indicated by

the graph Annu

aliz

ed C

redi

ting

0.00%

1.00%

5 Year Treasury Yield (CMT) Galliard Stable Value Separate Account Composite

the graph

5-Year Treasury Yield (CMT) Galliard Stable Value Separate Account Composite

Years

5 City of Los Angeles

Stable Value Market UpdateWrap Capacity

Wrap Market Update

• Existing providers are increasing capacity

• New providers entering market

• Shift in market providers from banking and insurance entities to predominantly insurance providers

• JP Morgan indication of exit

• Contract terms predominantly redefined

• Fees settling in 20-25 bps range

• Overall cooperation on S&P downgrade and guidelines being adjusted as necessary

Galliard continues to successfully transition Stable Value Portfolios in this environment:

• Since 1/1/08, transitioned $31.5 billion in new assets for 84 clients*

• In 2010, $11 billion transitioned for 30 clients

Galliard’s conservative approach, proven track record and strong relationships within the wrap market have allowed us to deliver client solutions in a challenging market

6

allowed us to deliver client solutions in a challenging market

*As of 9/30/11City of Los Angeles

Third Quarter 2011 Economic OverviewThird Quarter 2011

Confidence Crisis Threatens Economic Recovery! Consumer Confidence continued to erode during the third quarter,

falling to its lowest level since 2009 (Fig.1). Consumers and

700,000

Fig. 2: Initial Weekly Unemployment Claims

falling to its lowest level since 2009 (Fig.1). Consumers and businesses are leery about spending in the wake of political gridlock in the United States and the looming European debt crisis.

Initial unemployment claims fell below 400,000 at the end of the quarter (Fig. 2), signaling potential economic expansion. However, job creation remains stagnant and national unemployment remains above

500,000

600,000

tial Claim

s

Contraction (above 400k in claims)

9.0%.

Tepid ISM data suggest that manufacturing and non-manufacturing businesses alike are signaling weak expansion despite better-than-expected data for September (Fig. 3).

200 000

300,000

400,000Init

Expansion (below 400k in claims)

Current Level

200,000

Current Level Initial Claims (4-week moving average)

65

Fig. 3: ISM Manufacturing Index140 Fig. 1: Conference Board Consumer Confidence Index

45

50

55

60

65

ndex

Value

(%)

80

100

120

ndex

Valu

e

30

35

40

45

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

In

20

40

60

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

In

7

ISM Manufacturing Index ISM Non-Manufacturing Index2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Third Quarter 2011 Economic OverviewThird Quarter 2011

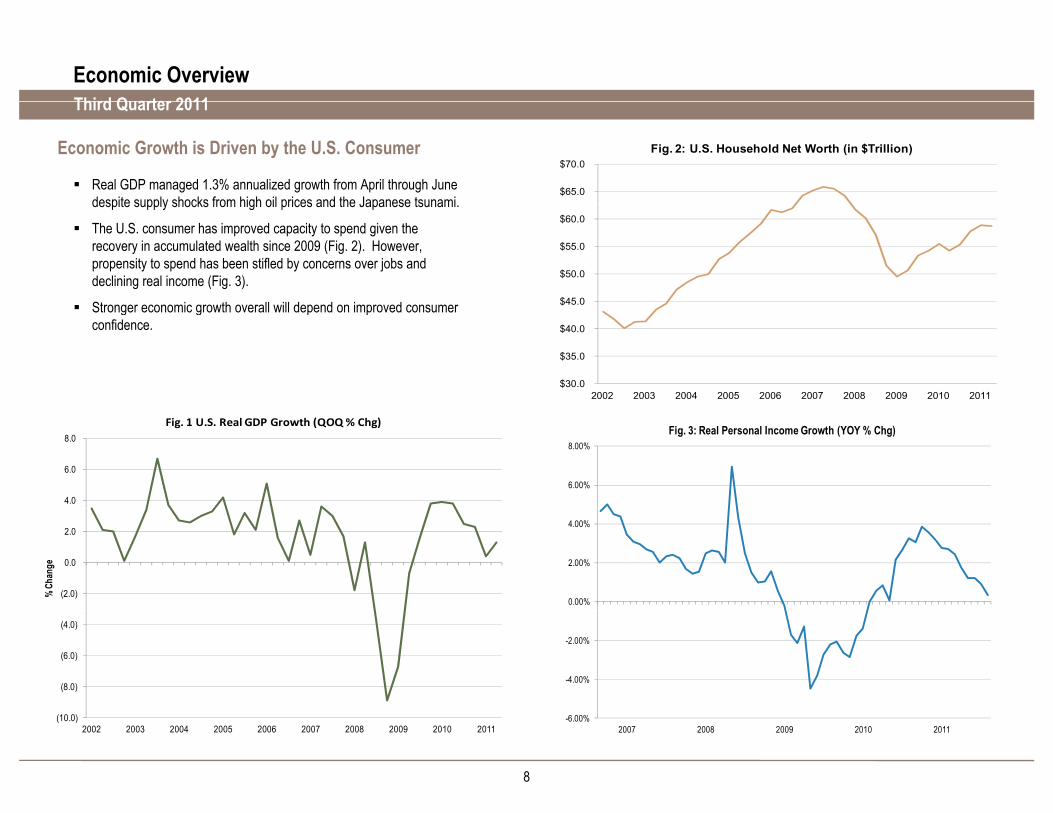

Economic Growth is Driven by the U.S. Consumer

Real GDP managed 1.3% annualized growth from April through June despite supply shocks from high oil prices and the Japanese tsunami

$65.0

$70.0 Fig. 2: U.S. Household Net Worth (in $Trillion)

despite supply shocks from high oil prices and the Japanese tsunami.

The U.S. consumer has improved capacity to spend given the recovery in accumulated wealth since 2009 (Fig. 2). However, propensity to spend has been stifled by concerns over jobs and declining real income (Fig. 3).

Stronger economic growth overall will depend on improved consumer $45.0

$50.0

$55.0

$60.0

Stronger economic growth overall will depend on improved consumer confidence.

$30.0

$35.0

$40.0

$

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

4.0

6.0

8.0 Fig. 1 U.S. Real GDP Growth (QOQ % Chg)

6.00%

8.00%Fig. 3: Real Personal Income Growth (YOY % Chg)

(2.0)

0.0

2.0

% Ch

ange

0.00%

2.00%

4.00%

(8.0)

(6.0)

(4.0)

-4.00%

-2.00%

8

(10.0)2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

-6.00%2007 2008 2009 2010 2011

Third Quarter 2011 Economic OverviewThird Quarter 2011

Economic Outlook – Slow Growth Recovery Continues

We expect final real GDP growth in the 1% to 2% range for 2011 and a slow growth p g g genvironment to begin 2012 in the face of mixed economic conditions. Businesses and consumers have taken a continued wait-and-see approach while politicians work to resolve economic and debt concerns in the United States and Europe. The consequence has been apathetic spending, despite improving capacity to do so.

The Federal Reserve remains committed to keeping interest rates low and liquidity abundant, as it instituted Operation Twist at the end of the third quarter. The result has been a flattening yield curve, as longer interest rates declined. The program’s desired outcome is to encourage consumer-based loans and spending. However, the program’s effectiveness remains to be seen.

The effects of QE2, which wrapped up in June, and Operation Twist, which began in September will ideally stimulate economic growth in the near term Looking forward and September, will ideally stimulate economic growth in the near term. Looking forward, and presuming economic growth materializes, the Fed may consider interest rate increases as keeping interest rates at historic lows risks a deflationary spiral.

In the meantime, economic growth will depend on job creation and income growth, the key determinants of consumer spending.

9

Third Quarter 2011 Fixed Income Market ReviewThird Quarter 2011

Interest rates fell across the yield curve in the third quarter (Fig.1). Paradoxically Treasury yields plummeted despite a rating downgrade

Fig. 2: Fixed Income Total Return By Sector (%)(Barclays Capital Intermediate & Long Indices)

Interest Rates Moved Lower In the Quarter

Paradoxically, Treasury yields plummeted despite a rating downgrade of the U.S. Government from AAA to AA+ by Standard and Poor’s, as a “flight to quality” buoyed Treasury prices.

Credit spreads widened notably during the third quarter creating negative returns in the high yield sector (Fig. 2).

Over the previous twelve months most securitized products have

(Barclays Capital Intermediate & Long Indices)U.S. Treasury Govt. Related Corporate High Yield

QTR 1 YR QTR 1 YR QTR 1 YR QTR 1 YRIntermediate 3.54 3.94 1.50 2.66 0.78 2.92 -6.05 1.56Long 24.66 17.14 11.20 11.48 8.95 8.73 -6.18 4.21

Over the previous twelve months, most securitized products have modestly outperformed Treasuries despite the recent flight to quality (Fig. 3).

MBS ABS CMBSQTR 1 YR QTR 1 YR QTR 1 YR

Securitized 2.36 5.56 2.42 3.34 -0.86 3.76

Fi 1 U S T Yi ld C Fig. 3: Barclays Capital

3.54.04.55.0

Fig. 1: U.S. Treasury Yield Curve

0.00 0.56 0.53 0.55

(0.52)(1 0)

0.0

1.0

)

Fig. 3: Barclays Capital Excess Returns versus Treasuries

1.01.52.02.53.0

Yiel

d (%

)

(2.21)

(3.51)

(1.62)

(2.51)

( )

(4.0)

(3.0)

(2.0)

(1.0)

Exce

ss R

etur

n (%

)

0.00.5

3 Mon

th6 M

onth

1 Yea

r2 Y

ear

3 Yea

r

5 Yea

r

7 Yea

r

10 Ye

ar

30 Ye

ar

6/30/2011 9/30/2011

(5.11)(6.0)

(5.0)

Corporate MBS CMBS ABS Govt. Related

QTR 1-Year

10

Stable Value PhilosophyInvestment Approach and Objectives

Consistent with the role of stable value as the “safe option,” we manage stable value portfolios conservatively seeking to consistently outperform our benchmarks while

K I Obj i

portfolios conservatively, seeking to consistently outperform our benchmarks while minimizing crediting rate volatility

Key Investment Objectives:

• Capital preservation

• Maintain sufficient liquidity

• Consistently outperform benchmarks and peer groupConsistently outperform benchmarks and peer group

Hallmarks of Our Investment Approach:

• High quality and broad diversificationg q y

• Disciplined value investing

• Stringent risk control

• Minimal crediting rate volatility

Our investment approach is ideally suited to stable value

11 City of Los Angeles

Third Quarter 2011 City of Los Angeles Stable Value FundThird Quarter 2011

Galliard Inception Date July 1, 1999

Investment Objective

Benchmark

Stable Value Portfolio Components Components Allocation Range

To provide safety of principal and consistency of returns with minimal volatility, while maintaining a stable credited rate of interest.

3 Year Constant Maturity Treasury Yield + 50 basis points

p p g

Cash Equivalents 2-50%

Security Backed Contracts 50-98%

Key Portfolio Guidelines P tf li D ti 2 0 3 5 Y T t f 3 0 Y Portfolio Duration 2.0 - 3.5 Years, Target of 3.0 Years

Minimum Portfolio Quality AA/Aa2 (underlying asset level)Minimum Portfolio Issue Quality Investment grade at the time of purchase

12 City of Los Angeles Stable Value Fund

***

***

13 City of Los Angeles Stable Value Fund

Third Quarter 2011

Periods Ending September 30, 2011Annualized Investment Performance*

3Q'11 YTD 1 Yr 3 Yr 5 Yr 10 YrSince

Inception**

Calendar Year Performance

2010 2009 2008 2007 2006

Returns for periods of less than one year are not annualized.Prior to July 1, 2008, the portfolio was invested exclusively in the Wells Fargo Stable Return Fund, a stable value collective fund. Since inception returns only include separate account returns.50% Citigroup 3 Month T-Bill/50% Merrill Lynch 1-3 Year Treasury Index through 6/30/2008 linked with 3 Year Constant Maturity Treasury Yield + 50 basis points from 7/1/2008.

Market Indices

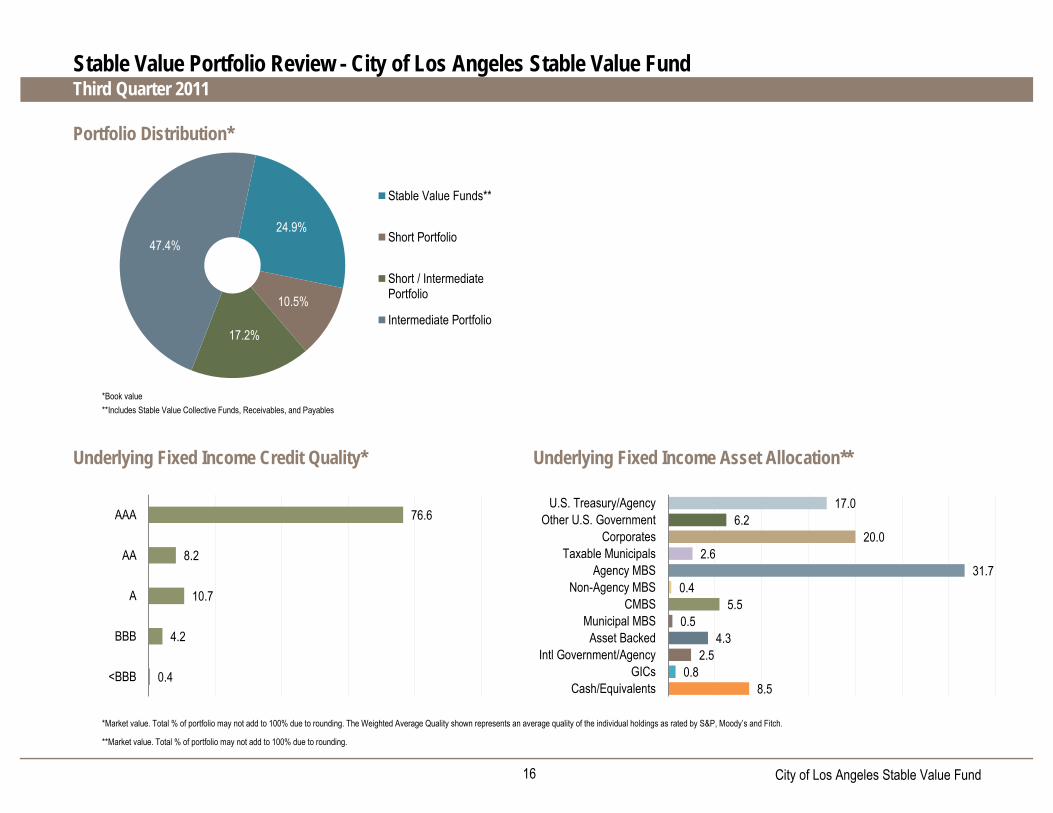

Stable Value Portfolio Review - City of Los Angeles Stable Value Fund

Merrill Lynch 3 Mo. T-Bill 0.13 0.21 2.06 5.03 4.83

Consumer Price Index 1.41 2.72 0.09 4.08 2.54

Portfolio (before inv. Mgmt. fees) 0.84 2.47 3.43 3.95 --- --- 4.04

Portfolio (net of inv. Mgmt. fees) 0.81 2.40 3.34 3.85 4.23 4.49 3.94

Benchmark*** 0.24 1.02 1.34 1.69 2.90 2.71 1.79

Portfolio (before inv. Mgmt. fees) 3.77 4.30 --- --- ---

Portfolio (net of inv. Mgmt. fees) 3.67 4.19 4.82 4.84 4.64

Benchmark*** 1.61 1.93 2.88 6.04 4.35

14 City of Los Angeles Stable Value Fund

Blended Yield (Before fees)* 3.29% Effective Duration 2.81 yearsMarket/Book Value Ratio 103.92%

Portfolio Distribution

192,434,103

581,626,323 81,633,736 133,077,080 366,915,507 $774,060,426

*Includes Stable Value Collective Funds, Receivables, and Payables **Total % of portfolio may not add to 100% due to rounding

*Gross yield is before investment management fees and after wrap fees.

Contract Value ($)

**The Weighted Average Quality of the portfolio has NOT been assessed by a nationally recognized statistical rating organization. The Weighted Average Quality shown represents an average quality of the individual holdings as rated by S&P and Moody’s.

75.1Short Portfolio 10.5 10.8Short / Intermediate Portfolio 17.2 17.6Intermediate Portfolio

Stable Value Portfolio Review - City of Los Angeles Stable Value FundThird Quarter 2011

Portfolio Characteristics

Total Assets $774,060,426Average Holdings Quality**Number of Contract Issuers 6

Aa3/AA-

09/30/2011% of Portfolio % of Portfolio

06/30/2011

Sector Distribution

Stable Value Funds* 24.9 24.9Security Backed Contracts 75.1

47.4 46.7Total 100.0%** 100.0%**

15 City of Los Angeles Stable Value Fund

Historical Crediting Rates*

*As of quarter end. Before fees.

Contract Quality Distribution*

*Total % of portfolio may not add to 100% due to rounding. The Weighted Average Quality shown represents an average quality of the individual holdings as rated by S&P, Moody’s and Fitch.**Total % of portfolio may not add to 100% due to rounding.

Market Value to Book Value Ratio*

Stable Value Portfolio Review - City of Los Angeles Stable Value FundThird Quarter 2011

Underlying Duration Distribution**

4.09 3.87 3.78 3.78 3.73 3.663.29 3.27 3.29

0

1

2

3

4

5

6

Cred

iting R

ate (%

)

101.47 101.13102.09

103.22104.24

102.86 102.69103.37 103.92

94

96

98

100

102

104

106

MV/B

V Ra

tio (%

)

0.0 0.0

35.3

24.9

29.8

10.1

0.00

5

10

15

20

25

30

35

40

% o

f Por

tfolio

18.3

40.8

26.8

14.0

0

5

10

15

20

25

30

35

40

45

% o

f Por

tfolio

16 City of Los Angeles Stable Value Fund

Portfolio Distribution*

*Book value**Includes Stable Value Collective Funds, Receivables, and Payables

Underlying Fixed Income Credit Quality* Underlying Fixed Income Asset Allocation**

*Market value. Total % of portfolio may not add to 100% due to rounding. The Weighted Average Quality shown represents an average quality of the individual holdings as rated by S&P, Moody’s and Fitch.

**Market value. Total % of portfolio may not add to 100% due to rounding.

Stable Value Portfolio Review - City of Los Angeles Stable Value FundThird Quarter 2011

24.9%

10.5%

17.2%

47.4%

Stable Value Funds**

Short Portfolio

Short / Intermediate Portfolio

Intermediate Portfolio

17.06.2

20.02.6

31.70.4

5.50.5

4.32.5

0.88.5

U.S. Treasury/AgencyOther U.S. Government

CorporatesTaxable Municipals

Agency MBSNon-Agency MBS

CMBSMunicipal MBS

Asset BackedIntl Government/Agency

GICsCash/Equivalents

76.6

8.2

10.7

4.2

0.4

AAA

AA

A

BBB

<BBB

Third Quarter 2011 Stable Value Portfolio Review - City of Los Angeles Stable Value FundThird Quarter 2011

14

Historical Cashflows

02468

1012

t Cas

h Flo

w (M

illion

s $)

-6-4-20

Oct-0

8

Nov-0

8

Dec-0

8

Jan-

09

Feb-

09

Mar-0

9

Apr-0

9

May-0

9

Jun-

09*

Jul-0

9

Aug-

09

Sep-

09

Oct-0

9

Nov-0

9

Dec-0

9

Jan-

10

Feb-

10

Mar-1

0

Apr-1

0

May-1

0

Jun-

10

Jul-1

0

Aug-

10

Sep-

10

Oct-1

0

Nov-1

0

Dec-1

0

Jan-

11

Feb-

11

Mar-1

1

Apr-1

1

May-1

1

Jun-

11

Jul-1

1

Aug-

11

Sep-

11

Net

*P ti i t hfl l

YTD 2010 2009 2008 2007 2006

*Participant cashflows only

YTD 2010 2009 2008 2007 2006Beginning Assets $714.8 $655.7 $161.6 $121.7 $118.7 $115.6Net Cash Flow ($)* $41.7 $34.4 $477.8*** $33.3 -$2.7 -$2.4Net Cash Flow (%) 5.83% 5.25% 295.67% 27.36% -2.27% -2.08%Estimated Investment Earnings $17.6 $24.7 $16.2 $6.6 $5.7 $5.4

$ $ $ $ $ $Ending Assets** $774.1 $714.8 $655.7 $161.6 $121.7 $118.7

*Contributions, Withdraw als and Inv estment Transfers**Cashflow s may not net to final assets due to rounding***Includes cashflow s due to merger of inv estment options

17 City of Los Angeles Stable Value Fund

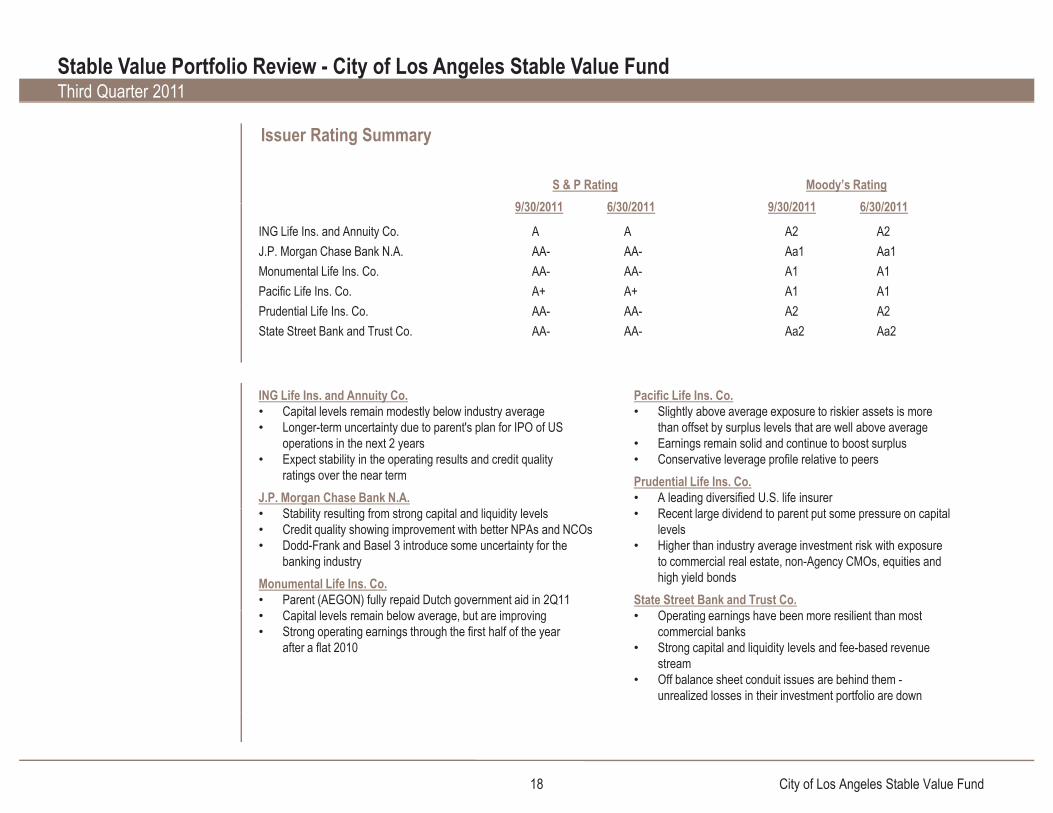

Stable Value Portfolio Review - City of Los Angeles Stable Value FundThird Quarter 2011

Issuer Rating Summary

S & P Rating Moody’s Rating9/30/2011 6/30/2011 9/30/2011 6/30/20119/30/2011 6/30/2011 9/30/2011 6/30/2011

ING Life Ins. and Annuity Co.J.P. Morgan Chase Bank N.A.Monumental Life Ins. Co.Pacific Life Ins. Co.

AAA-AA-A+

AAA-AA-A+

A2Aa1A1A1

A2Aa1A1A1

ING Life Ins. and Annuity Co.C it l l l i d tl b l i d t

Pacific Life Ins. Co.Sli htl b t i ki t i

Prudential Life Ins. Co.State Street Bank and Trust Co.

AA-AA-

AA-AA-

A2Aa2

A2Aa2

• Capital levels remain modestly below industry average• Longer-term uncertainty due to parent's plan for IPO of US• operations in the next 2 years• Expect stability in the operating results and credit quality• ratings over the near termJ.P. Morgan Chase Bank N.A.

St bilit lti f t it l d li idit l l

• Slightly above average exposure to riskier assets is more• than offset by surplus levels that are well above average• Earnings remain solid and continue to boost surplus• Conservative leverage profile relative to peersPrudential Life Ins. Co.• A leading diversified U.S. life insurer

R t l di id d t t t it l• Stability resulting from strong capital and liquidity levels• Credit quality showing improvement with better NPAs and NCOs• Dodd-Frank and Basel 3 introduce some uncertainty for the• banking industryMonumental Life Ins. Co.• Parent (AEGON) fully repaid Dutch government aid in 2Q11

C

• Recent large dividend to parent put some pressure on capital• levels • Higher than industry average investment risk with exposure• to commercial real estate, non-Agency CMOs, equities and• high yield bondsState Street Bank and Trust Co.

O• Capital levels remain below average, but are improving• Strong operating earnings through the first half of the year• after a flat 2010

• Operating earnings have been more resilient than most• commercial banks• Strong capital and liquidity levels and fee-based revenue• stream• Off balance sheet conduit issues are behind them -• unrealized losses in their investment portfolio are down

City of Los Angeles Stable Value Fund18

Period: 7/1/2011 - 9/30/2011

Transaction ReportCity of Los Angeles Stable Value Fund Portfolio Review

S&PRating

TradeDate

SettleDate

Par AmountIssuerCUSIP Maturity Moody'sRating

*

PurchasesSecurity Backed Contracts

Intermediate Portfolio

744999AR4 14,000,000 N.S.M. 09/01/2011 09/01/2011 AA- A2Prudential Life Ins. Co.

Total Intermediate Portfolio 14,000,000

14,000,000Total Security Backed Contracts

Total Purchases 14,000,000

* N.S.M. = No Stated Maturity

Portfolio Holdings

MaturityContractValue ($)

S&PRating

Moody'sRating

EffectiveDuration (yrs)

CreditingRate / Yield (%)

% ofPortfolio

Portfolio Distribution

September 30, 2011

*

City of Los Angeles Stable Value Fund Portfolio Review

Money MarketCash Receivable / (Payable) -324,955 0.0 AAA Aaa0.102.37

Total Money Market -324,955 0.0 0.10 AaaAAA2.37

Stable Value FundsWells Fargo Stable Return Fund G 192,759,059 24.9 AA- Aa22.102.37

Total Stable Value Funds 192,759,059 24.9 2.10 Aa2AA-2.37

Security Backed Contracts

Short PortfolioPacific Life Ins. Co. 81,633,736 10.5 A+ A11.93N.S.M.2.81

Total Short Portfolio 81,633,736 10.5 1.93 A1A+2.81

Short / Intermediate PortfolioState Street Bank and Trust Co. 52,782,500 6.8 AA- Aa22.95N.S.M.3.53

J.P. Morgan Chase Bank N.A. 80,294,580 10.4 AA- Aa12.95N.S.M.3.14

Total Short / Intermediate Portfolio 133,077,080 17.2 2.95 Aa1AA-3.29

Intermediate PortfolioING Life Ins. and Annuity Co. 77,945,713 10.1 A A23.74N.S.M.4.48

Prudential Life Ins. Co. 149,318,952 19.3 AA- A23.14N.S.M.3.20

Monumental Life Ins. Co. 60,153,593 7.8 AA- A13.15N.S.M.4.08

Monumental Life Ins. Co. 79,497,249 10.3 AA- A13.40N.S.M.4.37

Total Intermediate Portfolio 366,915,507 47.4 3.32 A2AA-3.87

Total Security Backed Contracts 581,626,323 75.1 3.04 A1AA-3.59

Total Fund AA- Aa32.81100.0 3.29774,060,426

* N.S.M. = No Stated Maturity

City of Los AngelesAccount Overview

2010

• Migrated underlying broad market portfolio to an intermediate strategy to improve

i k/ t fil d dd id i trisk/return profile and address wrap provider requirements

• As wrap capacity improves, we will look to add additional external managers

20112011

• Working with wrap providers on equity wash needs due to brokerage window

• Looking to add new external manager to enhance diversification in the near future

Working with staff and Mercer on scenario analysis on the “what ifs” of various• Working with staff and Mercer on scenario analysis on the “what ifs” of various

Europe events

• Will be working with staff and Mercer on potential guideline updates

21 City of Los Angeles