chapter seventeen - ridgeview high schoolrvhs.redmond.k12.or.us/files/2013/12/chap017.pdf · ......

TRANSCRIPT

*

* Chapter

Seventeen

Understanding

Accounting

and Financial

Information

Copyright © 2010 by the McGraw-Hill Companies, Inc. All rights reserved. McGraw-Hill/Irwin

*

*

• A lifelong weightlifter who

wanted a protein-packed

cookie to take to the gym.

• Due to accounting

troubles, his Bakery Barn

business was in trouble.

• Became a supplier for

another company and

hired a comptroller and a

new CEO.

SEAN PERICH Bakery Barn

Profile

17-2

*

*

• Accounting -- Recording, classifying, summarizing

and interpreting of financial events and transactions

in an organization to provide interested parties

needed financial information.

• Outside parties - like employees, owners,

creditors, unions, investors and the government -

make use of a firm’s accounting information.

WHAT’S ACCOUNTING? What is

Accounting?

LG1

17-3

*

* The ACCOUNTING SYSTEM

What is

Accounting?

LG1

17-4

*

* ACCOUNTANTS’

RESPONSIBILITIES

What is

Accounting?

LG1

17-5

*

*

• Managerial Accounting -- Provides information

and analysis to managers inside the organization to

assist them in decision making.

• Managerial accounting is involved with:

- Costs of production

- Costs of marketing

- Preparation and control of budgets

- Minimizing tax liabilities

MANAGERIAL ACCOUNTING Managerial

Accounting

LG2

17-6

*

* USERS of ACCOUNTING

INFORMATION

Managerial

Accounting

Users Type of Report

Government tax authority Tax reports

Government regulatory

agencies

Required reports

People interested in the

organization’s income

Financial statements found in

annual reports

Managers of the firm Financial statements and

internally distributed financial

reports

LG2

17-7

*

*

• Financial Accounting -- Financial information and

analyses are generated for people primarily outside

the organization. Outside users are interested in

these questions:

- Is the organization profitable?

- Is it able to pay its bills?

- How much debt does it owe?

• Annual Report -- A yearly statement of the financial

condition, progress, and expectations of the firm.

FINANCIAL ACCOUNTING Financial

Accounting

LG2

17-8

*

*

• Key things to watch for and read:

HOW to READ

an ANNUAL REPORT

Financial

Accounting

LG2

- Management’s

discussion and

analysis of operations

- Balance sheet

- Income statement

- Statement of cash

flows

- Auditor’s opinion

17-9

*

*

• Private Accountants -- Work in a single firm,

government agency, or nonprofit organization.

• Public Accountants -- Provide accounting

services to individuals or businesses.

• Certified Public Accountants (CPAs) -- Accountants who have passed a series of

examinations established by the American Institute of

Certified Public Accountants (AICPA) and met a

states requirements for education and experience.

PUBLIC vs. PRIVATE

ACCOUNTANTS

Financial

Accounting

LG2

17-10

*

• When a company is suspected of fraud or other

accounting wrongdoings a court will commission

a forensic accountant to search for foul play.

• Forensic accountants look for proof a company is

“cooking the books.”

• Problems within Enron, WorldCom, and our

federal government were found by forensic

accountants.

BALANCE SHEETS SHERLOCKS Legal Briefcase

*

17-11

*

* STEPS to CONTROL

ACCOUNTING PRACTICES

Financial

Accounting

LG2

17-12

*

*

• Auditing -- Reviewing and evaluating the

information used to prepare a company’s financial

statements.

• Independent Audit -- An evaluation and unbiased

opinion about the accuracy of a company’s financial

statements.

• Certified Internal Auditors (CIAs) -- Accountants

who have a bachelor’s degree and two years of

experience in internal auditing and pass an exam

administered by the Institute of Internal Auditors.

AUDITING CHECKS ACCURACY Auditing

LG2

17-13

*

*

• Tax Accountants -- Accountants

trained in tax law and are

responsible for preparing tax

returns or developing tax

strategies.

• Government and Not-for-

Profit Accounting -- Support for

organizations whose purpose is

not generating a profit, but serving

others according to a duly

approved budget.

SPECIALIZED ACCOUNTANTS Tax

Accounting

LG2

17-14

*

*

• What’s the key difference between managerial

and financial accounting?

• How’s the job of a private accountant different

from that of a public accountant?

• What’s the job of an auditor?

PROGRESS ASSESSMENT Progress

Assessment

17-15

*

*

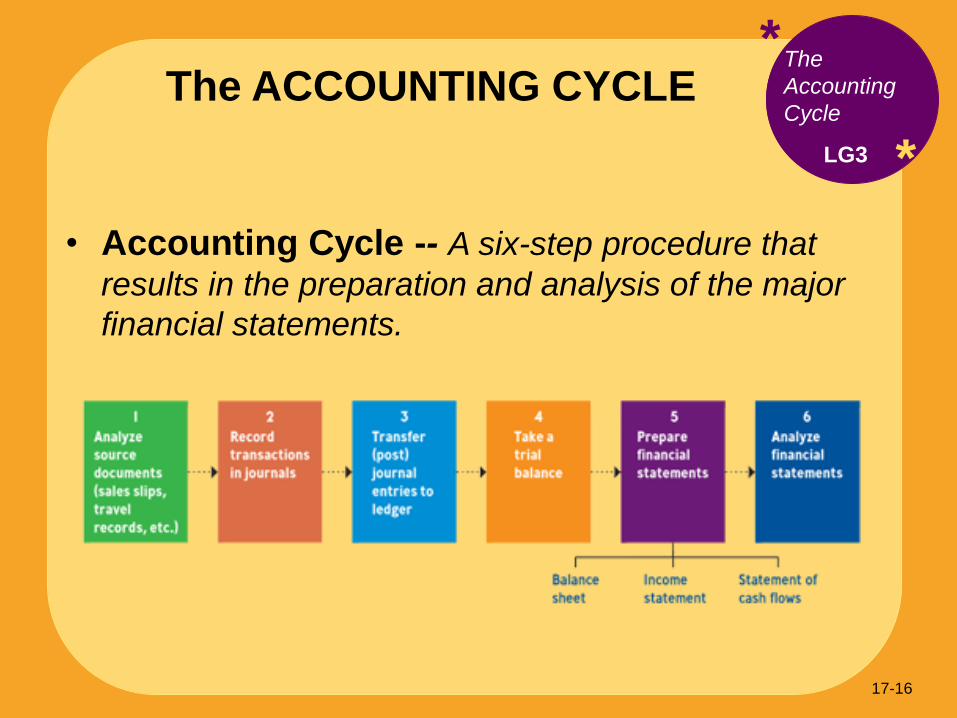

• Accounting Cycle -- A six-step procedure that

results in the preparation and analysis of the major

financial statements.

The ACCOUNTING CYCLE The

Accounting

Cycle

LG3

17-16

*

*

• Bookkeeping -- The recording of business

transactions. Bookkeepers divide a firm’s

transactions into meaningful categories and post

them into a record book or computer program called

a journal.

• Double-Entry Bookkeeping -- Bookkeepers

record all transactions in two places so they can

check one list of transactions against the other for

accuracy.

BOOKKEEPING’S ROLE The

Accounting

Cycle

LG3

17-17

*

*

• Ledger -- A specialized

accounting book or

program where all

information is in one

place.

• Trial Balance -- A

summary of all the

information in the account

ledgers.

BOOKKEEPING’S ROLE The

Accounting

Cycle

LG3

17-18

*

*

• Financial Statement -- A summary of all the

financial transactions that have occurred over a

particular period.

FINANCIAL STATEMENTS Understanding

Key Financial

Statements

LG3

• Key financial statements of

business are:

- Balance sheet

- Income statement

- Statement of cash flows

17-19

*

*

• Fundamental Accounting Equation -- The basis

for the balance sheet.

• The equation must always be balanced and

includes the formula:

o Assets = Liabilities + Owners Equity

The FUNDAMENTAL

ACCOUNTING EQUATION

The

Fundamental

Accounting

Equation

LG4

17-20

*

*

• Assets -- Economic resources owned by a firm.

Items can be tangible or intangible.

• Liquidity -- Ease with which assets can be

converted into cash.

ASSETS Classifying

Assets

LG4

17-21

*

*

• Current Assets -- Items that can or will be

converted to cash within one year.

• Fixed Assets -- Long-term assets that are relatively

permanent such as land, buildings, or equipment.

• Intangible Assets -- Long-term assets that have no

physical form but do have value such as patents,

trademarks, and goodwill.

CLASSIFYING ASSETS Classifying

Assets

LG4

17-22

*

*

• Liabilities -- What the business owes to others - its

debts.

• Accounts Payable -- Current liabilities a firm owes

for merchandise or services purchased on credit.

• Notes Payable -- Short or long-term liabilities a

business promises to pay by a certain date.

• Bonds Payable -- Long-term liabilities that the firm

must pay back.

CLASSIFYING LIABILITIES Liabilities and

Owners’

Equity

Accounts

LG4

17-23

*

*

• Owners’ Equity -- The

amount of the business that

belongs to the owners minus

any liabilities of the owners.

• Retained Earnings -- Accumulated earnings from

the firm’s profitable operations

that are reinvested in the

business.

OWNERS’ EQUITY ACCOUNTS Liabilities and

Owners’

Equity

Accounts

LG4

17-24

*

*

• What do we call the formula for the balance

sheet? What three accounts does it include?

• What does it mean to list assets according to

liquidity?

• What’s included in the liabilities account on the

balance sheet?

• What’s owners’ equity and how do we determine

it?

PROGRESS ASSESSMENT Progress

Assessment

17-25

*

*

• Income Statement -- The financial statement

that shows a firm’s bottom

line - that is, its profit after

costs, expenses, and

taxes.

• Net Income/Net Loss -- The revenue left over or

depleted.

The INCOME STATEMENT The Income

Statement

LG4

17-26

*

*

• The formula for the income statement:

o Revenue

o Minus Cost of Goods Sold

o Equals Gross Profit

o Minus Operating Expenses

o Equals Net Income before Taxes

o Minus Taxes

o Equals Net Income or Net Loss

The INCOME STATEMENT The Income

Statement

LG4

17-27

*

*

• Revenues is the monetary value a firm received

for goods sold, services rendered or other

payments.

• Cost of Goods Sold (or Manufactured) -- Measures the cost of merchandise the firms sells or

the cost of raw materials and supplies it used in

producing items for resale.

• Gross Profit -- How much a firm earned by buying

(or making) and selling merchandise.

ACCOUNTS of the INCOME

STATEMENT

The Income

Statement

LG4

(Continued) 17-28

*

*

• Operating Expenses -- Expenses a firm incurs in

selling goods and services

such as rent, salaries and

supplies.

• Depreciation -- The

systematic write-off of the cost

of a tangible asset over its

estimated useful life.

ACCOUNTS of the INCOME

STATEMENT (Continued)

The Income

Statement

LG4

17-29

*

*

• Generally Accepted Accounting Principles

(GAAP) sometimes permits accountants to use

different method of accounting for inventory.

• FIFO: First-In, First-Out

• LIFO: Last-In, Last-Out

• Each valuation can affect income and ending

inventory valuation.

ACCOUNTING for WHAT’S COMING

and GOING in SMALL BUSINESS Spotlight on Small Business

17-30

*

*

• Statement of Cash Flows -- Reports cash

receipts and cash disbursements related to the three

major activities of a firm:

1. Operations

2. Investments

3. Financing

The STATEMENT of CASH FLOWS The

Statement of

Cash Flows

LG4

17-31

*

*

• Cash Flow -- The difference between cash coming

in and cash going out of a business.

UNDERSTANDING CASH FLOW The Need for

Cash Flow

Analysis

LG4

• Managing cash flow is

a key consideration of

a business and can be

particularly challenging

for small and seasonal

businesses.

17-32

*

*

• You’re the only accountant employed by a small,

struggling firm.

• The firm requests a bank loan to keep operations

going and your boss suggests you record the

revenue early.

• This is against accounting principles, but you

know if you don’t get the loan, you may lose your

job. What do you do?

ON the ACCOUNTING HOT SEAT Making Ethical Decisions

17-33

*

*

• Ratio Analysis -- The assessment of a firm’s

financial condition using calculations and financial

ratios developed from the firm’s financial statements.

• Key ratios include:

- Liquidity ratios

- Leverage ratios

- Performance ratios

- Activity ratios

USING FINANCIAL RATIOS Analyzing

Financial

Performance

Using Ratios

LG5

17-34

*

*

• Liquidity ratios measure a firm’s ability to turn

assets into cash to pay its short-term debts.

• Two key ratios are:

- Current ratio

- Acid-test ratio

• This information is found on the firm’s balance

sheet.

COMMONLY USED

LIQUIDITY RATIOS

Liquidity

Ratios

LG5

17-35

*

*

• Leverage ratios measure the degree to which a

firm relies on borrowed funds in its operations.

• Key ratios include:

- Debt to Owner’s Equity Ratio

• This information is found on the firm’s balance

sheet.

LEVERAGE RATIOS Leverage

(Debt) Ratios

LG5

17-36

*

*

• Profitability ratios measure how effectively a

firm’s managers are using the firm’s various

resources to achieve profits.

• Key ratios include:

- Basic earnings per share

- Return on sales

- Return on equity

• This information is found on the firm’s balance

sheet and income statement.

PROFITABILITY RATIOS Profitability

(Performance)

Ratio

LG5

17-37

*

*

• Activity ratios measure how effectively

management is turning over inventory.

• Key ratios include:

- Inventory turnover ratio

ACTIVITY RATIOS Activity Ratio

LG5

• This information is

found on the firm’s

balance sheet and

income statement.

17-38

*

*

• Multinational companies must adapt their

accounting reporting to the rules of multiple

countries.

• Many countries have adopted International

Financial Reporting Standards (IFRS) and are

pushing to make them standard.

• The U.S. Securities & Exchange Commission

believes there should be such a standard.

The ACCOUNTING SHOT HEARD

AROUND the WORLD Reaching Beyond Our Borders

17-39

*

*

• 2008: SEC offers proposed timeline

• 2009: 110 large companies have the option of using

IFRS

• 2011: SEC assesses progress of IFRS

• 2013: Final decision on the move to IFRS

• 2014: Large public companies will be required to

report in IFRS (pending SEC decision)

• 2016: All companies will be required to report in

IFRS (pending SEC decision)

TIMELINE for the MOVE to IFRS Reaching

Beyond Our

Borders

LG5

17-40

*

*

• What’s the primary purpose of performing ratio

analysis using the firm’s financial statements?

• What are the four main categories of financial

ratios?

PROGRESS ASSESSMENT Progress

Assessment

17-41