chapter 4: personal financial statements chapter 4 personal financial statements (preparation and...

TRANSCRIPT

Chapter 4: Personal Financial Statements

Chapter 4

Personal Financial Statements(Preparation and Analysis)

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

2

Financial Statements Provide Information About:

Financial resources available to client

How resources were acquired What the client has accomplished

financially utilizing these resources

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

3

Personal Financial Statements

Balance Sheet Income Statement Statement of Changes in Net

Worth

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

4

Financial Statements are Used:

By clients to benchmark goal achievement

By planners to help clients set financial direction

By creditors & lenders to make decisions to extend, continue, or call indebtedness

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

5

Balance Sheet Terms

Asset Liability Net Worth

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

6

Asset Categories & Classifications

Cash and Cash Equivalents Liquid – easily converted to cash Convert to cash within a year

Investment Assets Held for growth or income

Personal-Use Assets Long-lived assets Used to maintain quality of life

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

7

Liability Categories & Classifications

Current Liabilities Credit card debt & unpaid bills

Long-Term Liabilities Debts of larger assets

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

8

Valuation of Assets & Liabilities

Assets valued at FMV Liabilities represent principal owed

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

9

Sample Balance Sheet

Assets LiabilitiesCash/Cash Equivalents Current Liabilities

JT Checking 2,100 JT Credit Cards 10,000 JT Savings 48,000 JT Home Mortgage 4,200

Total Cash/Cash Equiv. 50,100 Total Current Liabilities 14,200

Invested Assets Long-term LiabilitesJT Stock Portfolio 15,000 JT Mortgage on Home 288,000 W 401(k) 9,000 Total Long-term Liabilities 288,000 H IRA 14,500

Total Invested Assets 38,500 Total Liabilities $292,200

Personal-Use Assets Net Worth $223,900

JT Home 420,000 W Jewelry 5,000 JT Automobile 2,500

Total Personal-Use Assets 427,500

Total Assets $516,100 Total Liabilities & Net Worth $516,100

Balance Sheetas of 12/31/2006

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

10

The Income and Expense Statement

Summary of client’s income and expenses over a period of time, usually one year

May focus on realized transactions, and if so, helps compare to budgeted financial goals

May be prepared in advance and used for budgeting or projections

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

11

Income Statement Terms

Income Employment Investment Other

Savings Expenses

Fixed Variable Discretionary

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

12

Sample Income Statement

INCOMEEmployment

Husband 85,000 Wife 60,000 145,000

Investment Income 500 Total Inflow $145,500

SavingsReinvestment 500 401(k) Deferral 7,200 Total Savings $7,700

Available for Expenses $137,800

EXPENSESFixed Expenses

Necessities 25,000 Debt Payments 36,000 Total Fixed Expenses $61,000

Variable ExpensesEntertainment 1,200 Clothing 3,600 Total Variable Expenses $4,800Total Expenses $65,800

Discretionary Cash Flow $72,000

Income StatementFor the Year 2006

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

13

The Statement of Changes in Net Worth

Summarizes noncash flow changes in net worth not recorded on the income statement.

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

14

Statement of Changes in Net Worth Transactions

Changes in value for assets due to appreciation or depreciation

If an asset other than cash is exchanged for some other assets

If assets other than cash are received by gift or inheritance

If assets other than cash are given to charities or noncharitable donees

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

15

Sample Statement of Changes in Net Worth

Additions to Net WorthAdd (Noncash Flow Adjustments)

Increases in Assets:Appreciation of Assets

Home 5,000 Increase in Investment Contributions

401(k) Employer Contribution 2,000 Decrease in Liabilities:

Home Mortgage 12,000 Credit Card Debt 2,000

Total $21,000

Reductions in Net WorthSubtract (Noncash Flow Adjustments)

Decrease in Assets:Depreciation of Assets

Automobile (500) Total ($500)

Net - Noncash Flow Change in Net Worth $20,500

Statement of Changes in Net WorthFor the Year Ending 12/31/06

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

16

Ratio Analysis

The key to ratio analysis is: Does the ratio get to the answer for

the question asked? Is there some standard or benchmark

to determine whether the result is appropriate for this particular client?

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

17

Ratio Analysis—The Objective

The objective of ratio analysis is twofold: To gain additional insight into the

financial situation and behavior of the client

To generate questions for the client to answer to further gain such insight

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

18

Types of Ratio Analysis

Liquidity ratios – emergency fund ratio and current ratio

Debt ratios – total debt to net worth, long-term debt to net worth, debt to total assets, long-term debt to total assets, housing costs to gross income, housing and debt payments to gross income

Performance ratios – savings ratios and investment performance ratios

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

19

Emergency Fund Ratio

EFR = Current Assets Monthly Nondiscretionary

Expenses

Target of 3 to 6 months

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

20

Current Ratio

CR = Current Assets Current Liabilities

Target of 1.0 to 2.0

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

21

Lending Ratios

Housing Costs (Mortgage payment + Property tax + Homeowners insurance) to Gross Income Target of ≤ 28%

Housing and Debt Payments (i.e. credit card, auto loan) to Gross Income Target of ≤ 36%

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

22

Savings Ratios

Rate of Savings = Annual Savings Annual Gross IncomeTarget of ≥ 10% (age dependent)

Discretionary Cash Flow + Savings to Gross Income

Target of ≥ 10%

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

23

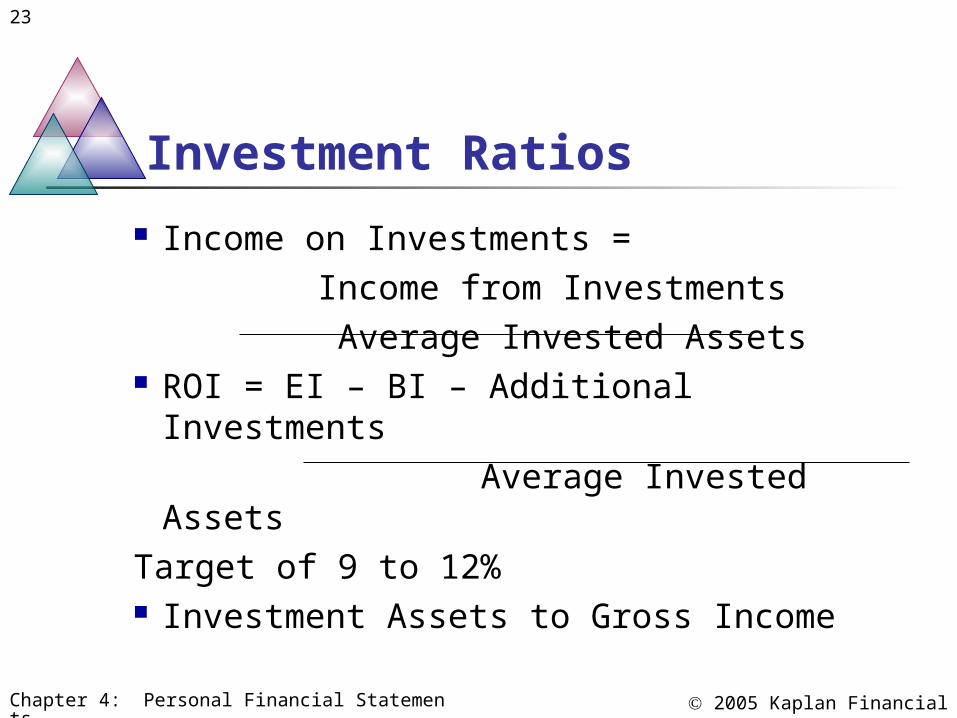

Investment Ratios

Income on Investments = Income from Investments Average Invested Assets ROI = EI – BI – Additional Investments Average Invested Assets Target of 9 to 12% Investment Assets to Gross Income

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

24

Vertical & Growth Analysis

Vertical analysis: Balance sheet – each item presented

as a percent of total assets Income statement – each item

presented as a percent of total income Growth analysis:

Calculates the growth rate of certain financial variables over time using TVM tools

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

25

Limitations of Financial Statement Analysis

Inflation Use of estimates Few benchmarks for individuals

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

26

Sensitivity Analysis & Risk Analysis

Sensitivity analysis allows manipulation of input variables by small increments to determine the impact on the ratio

Risk analysis examines the uncertainty of cash flows to the individual Business or investment risk Financial risk

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

27

Budgeting

A process of projecting, monitoring, adjusting and controlling future income and expenditures. Savings and Consumption Habits

Chapter 4: Personal Financial Statements 2005 Kaplan Financial

28

Debt Management

Home Mortgages Fixed-Rule Mortgages Variable-Rate Mortgages or

Adjustable-Rate Mortgages (ARMs) Balloon Mortgages