chapter 14 special tax computation methods, tax credits, and payment of tax

TRANSCRIPT

Chapter 14Special Tax Computation Methods, Tax Credits, and

Payment of Tax

Learning Objectives

• Calculate the Alternative Minimum Tax• Describe what constitutes self-employment

income and compute the self-employment tax• Describe the various business and personal

tax credits• Understand the mechanics of the federal

withholding tax system and the requirements for making estimated payments

Alternative Minimum Tax

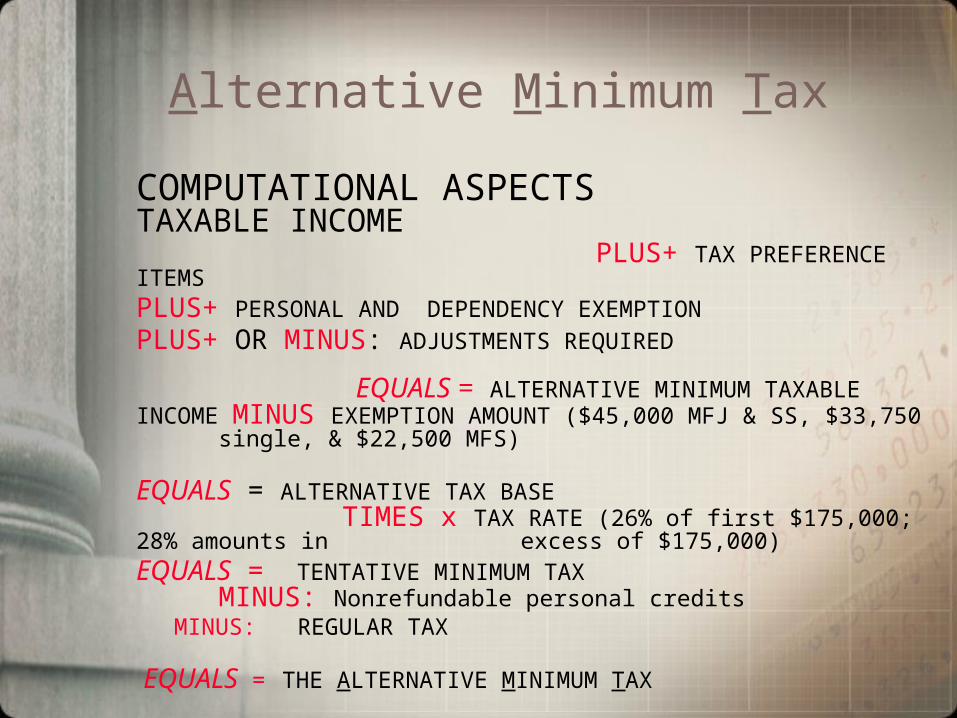

COMPUTATIONAL ASPECTS TAXABLE INCOME PLUS+ TAX PREFERENCE ITEMS

PLUS+ PERSONAL AND DEPENDENCY EXEMPTION

PLUS+ OR MINUS: ADJUSTMENTS REQUIRED EQUALS = ALTERNATIVE MINIMUM TAXABLE INCOME MINUS EXEMPTION AMOUNT ($45,000 MFJ & SS, $33,750 single, & $22,500 MFS) EQUALS = ALTERNATIVE TAX BASE TIMES x TAX RATE (26% of first $175,000; 28% amounts in excess of $175,000) EQUALS = TENTATIVE MINIMUM TAX MINUS: Nonrefundable personal credits

MINUS: REGULAR TAX EQUALS = THE ALTERNATIVE MINIMUM TAX

Alternative Minimum Tax

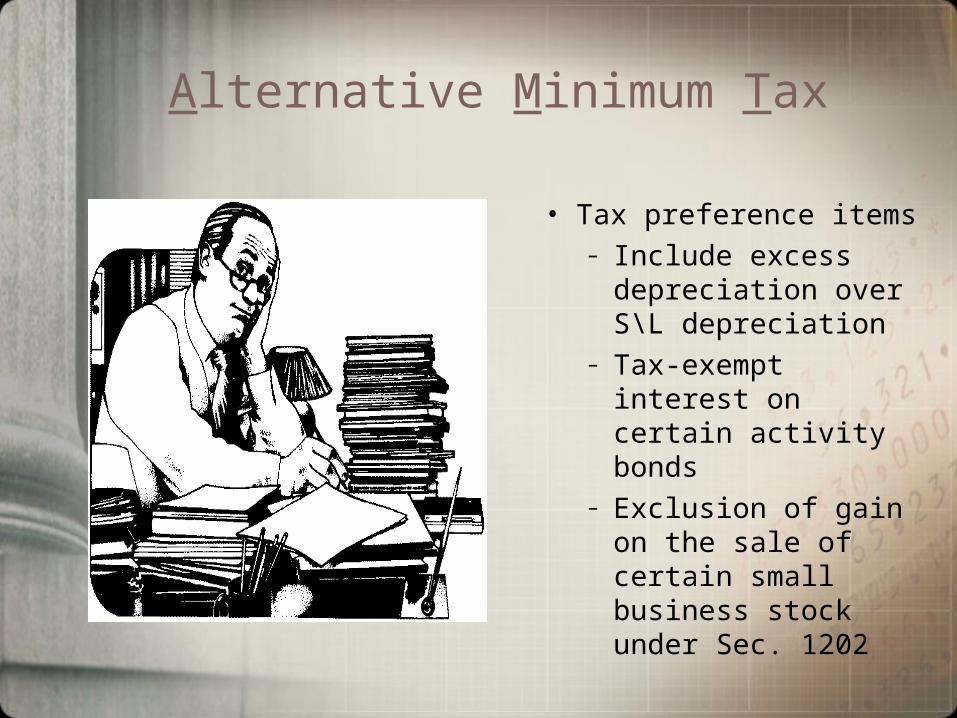

• Tax preference items– Include excess

depreciation over S\L depreciation

– Tax-exempt interest on certain activity bonds

– Exclusion of gain on the sale of certain small business stock under Sec. 1202

Alternative Minimum Tax

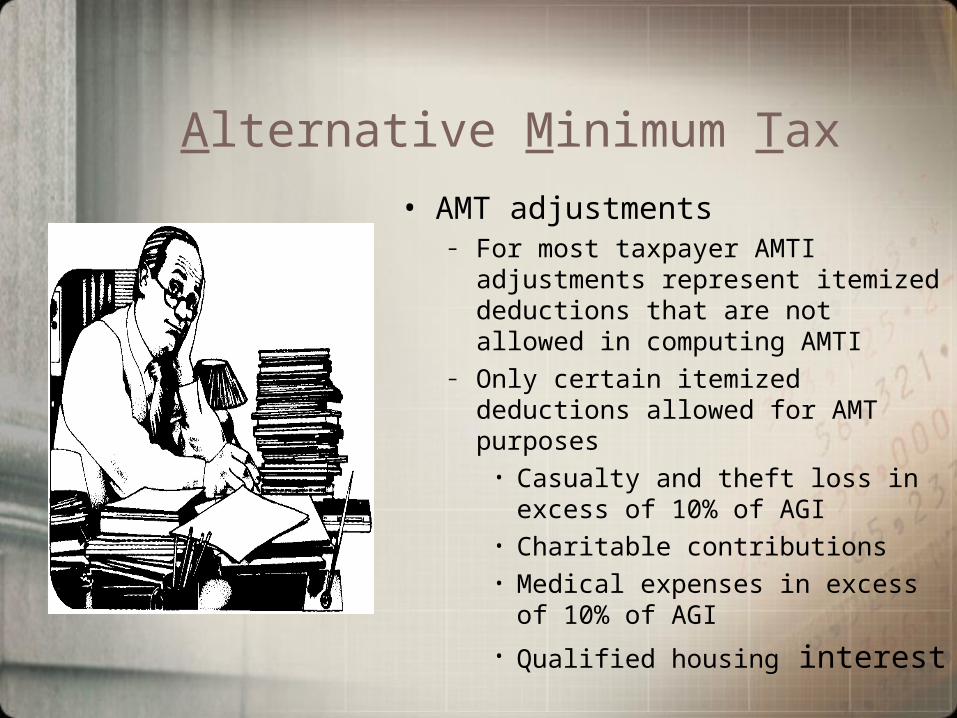

• AMT adjustments– For most taxpayer AMTI adjustments

represent itemized deductions that are not allowed in computing AMTI

– Only certain itemized deductions allowed for AMT purposes

• Casualty and theft loss in excess of 10% of AGI

• Charitable contributions• Medical expenses in excess of 10%

of AGI

• Qualified housing interest

Alternative Minimum Tax

• AMT adjustments due to timing differences– For real property

placed in service after 1986 and before 1999

Alternative Minimum Tax

• AMT adjustments due to timing differences– For personal

property placed in service after 1986, difference between MACRS deduction and the amount determined by using 150% DB method

Self-employment Tax• Distinction between

independent contractor and an employee is important

• Self-employed individuals are subject to self-employment tax on the amount of net earnings from the self-employment

• Employees who have a small business in addition to regular employment may also be subject to the self-employment tax

Self-employment Tax

• Computing the tax– Individuals having net

earnings from self-employment of $400 or more are subject to the self-employment tax

– The self-employment tax is 15.3%. This consist of 12.4% for OASDI and 2.9% for Medicare. The limit for 2004 on OASDI is $90,000 and there is no limit on the Medicare portion of the self-employment tax

Self-employment Tax

• Computing amount subject to the self-employment tax– To compute the amount

that is subject to self-employment tax. Multiply self-employment income by 92.35% (100%-7.65%) this equals the net earnings from self-employment

Self-employment Tax

– One-half of self-employment tax imposed is allowed as a for AGI deduction

Self-employment Tax

• What constitutes self-employment

– Net earnings from a sole proprietorship

– Director’s fees– Taxable research grant– Distributive share of partnership

income plus guaranteed payments

• The self-employment tax is computed on Schedule SE

Overview Of Tax Credits

• Use and importance of tax credits– Tax credits may be

used to implement tax policy objectives

• Example: provide tax relief for low income taxpayer - earned income credit

Overview Of Tax Credits

• Value of credit versus a deduction– The value of a

deduction is dependent on taxpayer’s marginal rate

– A tax credit reduces tax liability dollar for dollar

Overview Of Credits

• Classification of credits– Refundable– Nonrefundable

Overview Of Tax CreditsNon-refundable

• Personal tax credits • Child tax credit• Child and dependent care credit• Tax credit for the elderly & disabled• Adoption credit• Hope scholarship credit• Lifetime learning credit• Qualified Retirement Savings

Contribution Credit

Overview Of Tax CreditsNon-refundable

• Miscellaneous credits– Foreign tax credit

• General business credits– Credit for increasing research– Work opportunity credit– Empowerment zone employment – Disabled access credit– Rehabilitation expenditures– Business energy credit– Welfare to Work

Refundable Credits

• Earned Income Credit• Eligibility rules:

– Earned income and AGI thresholds met– Principal place of abode in the US for

more than ½ of the tax year.– The individual is at least 25 years old and

not more than 64 at the end of the year.– The individual is not a dependent of

another taxpayer for the tax year

Payment Of Taxes

• Withholding of taxes– Employers are required to

withhold federal income taxes and FICA tax from employee compensation

– Special rules are provided for more than one employer during the same year

– Exemptions for certain employment activities such as ministers and domestic servants

Payment Of Taxes

• Withholding allowances and methods– Every employee must

file an Employee’s Withholding Allowance Certificate (Form W-4)

Payments Of Taxes

• Estimated tax payments– Calendar year

taxpayers quarterly payments are due April 15, June 15, Sept 15 of the current year, and January 15 of the following year

Tax Planning Considerations

• Avoiding the Alternative Minimum Tax

• Avoiding the underpayment penalty for estimated tax

• Cash-flow considerations

• Use of credits

Compliance And Procedural Considerations

• Alternative minimum tax filing procedures Form 6251 or 4626

• Withholding and estimated payments Form W-2 and 1040ES

• General Business Credit Form 3800

• Personal tax credits– Form 2441– Schedule R– Schedule EIC– Form 1116– Form 8863