chapter 12: sources of funds 1 copyright 2005 prentice hall inc. a pearson education company sources...

TRANSCRIPT

Chapter 12: Sources of FundsChapter 12: Sources of Funds 11Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Sources of Funds:Equity and Debt

Sources of Funds:Equity and Debt

Chapter 12: Sources of FundsChapter 12: Sources of Funds 22Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

The “Secrets” to Successful The “Secrets” to Successful FinancingFinancing

1. Choosing the right sources of capital is a 1. Choosing the right sources of capital is a decision that will influence a company for a decision that will influence a company for a lifetime.lifetime.

2. The money is out there; the key is knowing 2. The money is out there; the key is knowing where to look.where to look.

3. Raising money takes time and effort. 3. Raising money takes time and effort. 4. Creativity counts. Entrepreneurs have to be as 4. Creativity counts. Entrepreneurs have to be as

creative in their searches for capital as they are creative in their searches for capital as they are in developing their business ideas.in developing their business ideas.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 33Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

The “Secrets” to Successful The “Secrets” to Successful FinancingFinancing

(continued)(continued)

5. The World Wide Web puts at entrepreneurs’ 5. The World Wide Web puts at entrepreneurs’ fingertips vast resources of information that fingertips vast resources of information that can lead to financing. can lead to financing.

6. Be thoroughly prepared before approaching 6. Be thoroughly prepared before approaching lenders and investors. lenders and investors.

7. Entrepreneurs should not underestimate the 7. Entrepreneurs should not underestimate the importance of making sure that the importance of making sure that the “chemistry” among themselves, their “chemistry” among themselves, their companies, and their funding sources is a good companies, and their funding sources is a good one. one.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 44Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Three Types of CapitalThree Types of Capital

FixedFixed - used to purchase the the permanent or - used to purchase the the permanent or fixed assets of the business (e.g. buildings, land, fixed assets of the business (e.g. buildings, land, equipment, etc.).equipment, etc.).

WorkingWorking - used to support the small company's - used to support the small company's normal short-term operations (e.g. buy normal short-term operations (e.g. buy inventory, pay bills, wages, or salaries, etc.).inventory, pay bills, wages, or salaries, etc.).

GrowthGrowth - used to help the small business - used to help the small business expand or change its primary direction.expand or change its primary direction.

CapitalCapital is any form of wealth employed to is any form of wealth employed to produce more wealth for a firm.produce more wealth for a firm.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 55Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Equity CapitalEquity Capital

Represents the personal investment of the Represents the personal investment of the owner(s) in the business.owner(s) in the business.

Is called Is called risk capital risk capital because investors assume the because investors assume the risk of losing their money if the business fails.risk of losing their money if the business fails.

Does Does notnot have to be repaid with interest like a have to be repaid with interest like a loan does.loan does.

Means that an entrepreneur must give up some Means that an entrepreneur must give up some ownership in the company to outside investors.ownership in the company to outside investors.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 66Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Debt CapitalDebt Capital

Must be repaid with interest.Must be repaid with interest. Is carried as a liability on the Is carried as a liability on the

company’s balance sheet.company’s balance sheet. Can be just as difficult to secure as Can be just as difficult to secure as

equity financing, even though sources equity financing, even though sources of debt financing are more numerous.of debt financing are more numerous.

Can be expensive, especially for small Can be expensive, especially for small companies, because of the risk/return companies, because of the risk/return tradeoff.tradeoff.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 77Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Sources of Equity Sources of Equity FinancingFinancing

Personal savingsPersonal savingsFriends and family membersFriends and family membersAngelsAngelsPartnersPartnersCorporationsCorporationsVenture capital companiesVenture capital companiesPublic stock salePublic stock sale

Chapter 12: Sources of FundsChapter 12: Sources of Funds 88Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Personal SavingsPersonal Savings

The The firstfirst place an entrepreneur place an entrepreneur should look for money. should look for money.

The most common source of equity The most common source of equity capital for starting a business.capital for starting a business.

Outside investors and lenders Outside investors and lenders expect entrepreneurs to put some expect entrepreneurs to put some of their own capital into the of their own capital into the business business beforebefore investing theirs. investing theirs.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 99Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Friends and Family MembersFriends and Family Members

Three out of four entrepreneurs start Three out of four entrepreneurs start their businesses with capital from their businesses with capital from outside sources.outside sources.

After emptying her own pockets, an After emptying her own pockets, an entrepreneur should turn to those entrepreneur should turn to those most likely to invest in the business: most likely to invest in the business: friends and family members.friends and family members.

Careful!!! Inherent dangers lurk in Careful!!! Inherent dangers lurk in family/friendly business deals, family/friendly business deals, especiallyespecially those that flop. those that flop.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 1010Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Friends and Family MembersFriends and Family Members(continued)(continued)

Guidelines for Family and Friendship Guidelines for Family and Friendship Financing Deals:Financing Deals: Consider the impact of the investment on Consider the impact of the investment on

everyone involved. Keep the arrangement everyone involved. Keep the arrangement “strictly business.”“strictly business.”

Settle the details up front.Settle the details up front. Create a written contract.Create a written contract. Treat the money as “bridge financing.” Treat the money as “bridge financing.” Develop a payment schedule that suits both Develop a payment schedule that suits both

parties. parties.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 1111Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

AngelsAngels

Angels - private investors who back Angels - private investors who back emerging entrepreneurial companies emerging entrepreneurial companies with their own money.with their own money.

Fastest growing segment of the small Fastest growing segment of the small business capital market. business capital market.

An excellent source of “patient money” An excellent source of “patient money” for investors needing relatively small for investors needing relatively small amounts of capital – often less than amounts of capital – often less than $500,000.$500,000.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 1212Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

AngelsAngels(continued)(continued)

An estimated 400,000 angels across the An estimated 400,000 angels across the U.S. invest $50 billion a year in 30,000 to U.S. invest $50 billion a year in 30,000 to 60,000 small companies. 60,000 small companies.

Dwarf investments of venture capital Dwarf investments of venture capital firms, providing two to five times as firms, providing two to five times as much capital to 20 to 30 times as many much capital to 20 to 30 times as many companies.companies.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 1313Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

AngelsAngels(continued)(continued)

Key: finding them! Key: finding them! Angels almost always invest their money locally Angels almost always invest their money locally

and can be found through “networks.”and can be found through “networks.” The typical angel:The typical angel:

Invests in companies at the startup or infant growth Invests in companies at the startup or infant growth stages.stages.

Accepts 24% of the proposals presented to him.Accepts 24% of the proposals presented to him. Makes an average of two investments every three Makes an average of two investments every three

years.years. Has invested an average of $80,000 in 3.5 businesses. Has invested an average of $80,000 in 3.5 businesses.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 1414Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Corporate Venture CapitalCorporate Venture Capital

20% of all venture capital investments 20% of all venture capital investments come from corporations.come from corporations.

About 300 large corporations across the About 300 large corporations across the globe invest in start-up companies.globe invest in start-up companies.

Capital infusions are just one benefit; Capital infusions are just one benefit; corporate partners may share marketing corporate partners may share marketing and technical expertise. and technical expertise.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 1515Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Venture Capital CompaniesVenture Capital Companies

More than 1,300 venture capital firms More than 1,300 venture capital firms operate across the U.S. operate across the U.S.

Most venture capitalists seek investments Most venture capitalists seek investments in the $3,000,000 to $10,00,000 range in in the $3,000,000 to $10,00,000 range in companies with high-growth and high-companies with high-growth and high-profit potential. profit potential.

Business plans are subjected to an Business plans are subjected to an extremelyextremely rigorous review - less than 1% rigorous review - less than 1% accepted.accepted.

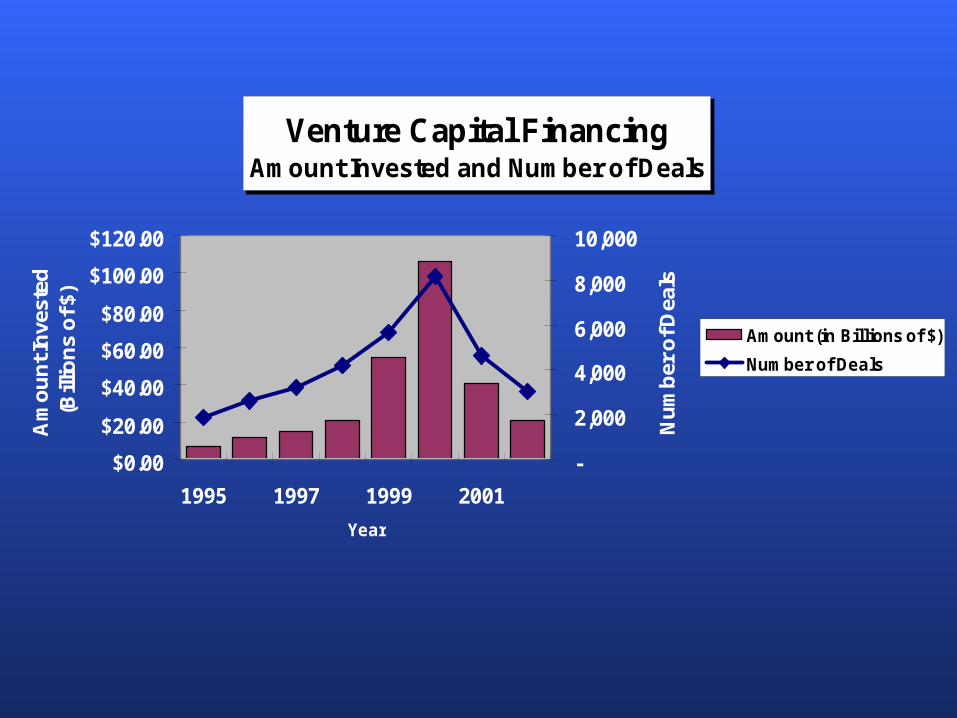

Venture Capital FinancingAmount Invested and Number of Deals

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

1995 1997 1999 2001

Year

Am

ou

nt I

nve

sted

(B

illio

ns

of $

)

-

2,000

4,000

6,000

8,000

10,000

Nu

mb

er o

f Dea

ls

Amount (in Billions of $)

Number of Deals

Chapter 12: Sources of FundsChapter 12: Sources of Funds 1717Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Venture Capital CompaniesVenture Capital Companies(continued)(continued)

Most venture capitalists take an active Most venture capitalists take an active role in managing the companies in which role in managing the companies in which they invest.they invest.

Many venture capitalists focus their Many venture capitalists focus their investments in specific industries with investments in specific industries with which they are familiar.which they are familiar.

Venture capitalists typically purchase Venture capitalists typically purchase between 20% and 40% of a company but between 20% and 40% of a company but in some cases will buy 70% or more. in some cases will buy 70% or more.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 1818Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Venture Capital CompaniesVenture Capital Companies(continued)(continued)

Most often, venture capitalists invest in a Most often, venture capitalists invest in a company across several stages.company across several stages.

On average, 91% of venture capital goes On average, 91% of venture capital goes to:to: Early stage investments (companies in the Early stage investments (companies in the

early stages of development).early stages of development). Expansion stage investments (companies in Expansion stage investments (companies in

the rapid growth phase).the rapid growth phase).Only 9% of venture capital goes to Only 9% of venture capital goes to

businesses in the startup phase. businesses in the startup phase.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 1919Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

What Do Venture CapitalWhat Do Venture CapitalCompanies Look For?Companies Look For?

Competent managementCompetent managementCompetitive edgeCompetitive edgeGrowth industryGrowth industryViable exit strategyViable exit strategy““Intangibles”Intangibles”

Average Returns on Venture Capital Investments

Total loss11%

Partial loss23%

1 to 2 times the initial investment

30%

2 to 5 time the initial investment

20%

5 to 10 times the initial investment

9%

10+ times the initial invesment

7%

Chapter 12: Sources of FundsChapter 12: Sources of Funds 2121Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Going PublicGoing Public

Initial public offering (IPO) - when a Initial public offering (IPO) - when a company raises capital by selling shares company raises capital by selling shares of its stock to the public for the first time. of its stock to the public for the first time.

Typical year: about 440 companies make Typical year: about 440 companies make IPOs.IPOs.

Few companies with sales below $20 Few companies with sales below $20 million in annual sales make IPOs. million in annual sales make IPOs.

Initial Public Offerings (IPOs)

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

1981 1986 1991 1996 2001

Year

Am

ou

nt

Rai

sed

(B

illi

on

s o

f $)

01002003004005006007008009001000

Nu

mb

r o

f IP

Os

$ Raised (Billions)

Number

Chapter 12: Sources of FundsChapter 12: Sources of Funds 2323Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Successful IPO CandidatesSuccessful IPO Candidates

Consistently high growth ratesConsistently high growth rates Strong record of earningsStrong record of earnings 3 to 5 years of audited financial statements 3 to 5 years of audited financial statements

that meet or exceed SEC standardsthat meet or exceed SEC standards Solid position in a rapidly-growing industrySolid position in a rapidly-growing industry Sound management team with experience Sound management team with experience

and a strong board of directorsand a strong board of directors

Chapter 12: Sources of FundsChapter 12: Sources of Funds 2424Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Advantages of “Going Public”Advantages of “Going Public”

Ability to raise large amounts of Ability to raise large amounts of capitalcapital

Improved corporate imageImproved corporate image Improved access to future financingImproved access to future financing Attracting and retaining key Attracting and retaining key

employeesemployees Using stock for acquisitionsUsing stock for acquisitions Listing on a stock exchangeListing on a stock exchange

Chapter 12: Sources of FundsChapter 12: Sources of Funds 2525Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Disadvantages of “Going Public”Disadvantages of “Going Public”

Dilution of founder’s ownershipDilution of founder’s ownership Loss of controlLoss of control Loss of privacyLoss of privacy Reporting to the SECReporting to the SEC Filing expensesFiling expenses Accountability to shareholdersAccountability to shareholders Pressure for short-term Pressure for short-term

performanceperformance TimingTiming

Chapter 12: Sources of FundsChapter 12: Sources of Funds 2626Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

The Registration ProcessThe Registration Process

Choose the underwriterChoose the underwriterNegotiate a letter of intentNegotiate a letter of intentPrepare the registration statementPrepare the registration statementFile with the SECFile with the SECWait to “go effective” and road showWait to “go effective” and road showMeet state requirementsMeet state requirements

TimeTime ActionAction

Week 1Week 1 Conduct organizational meeting with IPO team, including underwriter, attorneys, Conduct organizational meeting with IPO team, including underwriter, attorneys, accountants, and others. Begin drafting registration statement.accountants, and others. Begin drafting registration statement.

Week 5Week 5 Distribute first draft of registration statement to IPO team and make revisions. Distribute first draft of registration statement to IPO team and make revisions.

Week 6Week 6 Distribute second draft of registration statement and make revisions. Distribute second draft of registration statement and make revisions.

Week 7Week 7 Distribute third draft of registration statement and make revisions. Distribute third draft of registration statement and make revisions.

Week 8Week 8 File registration statement with the SEC. Begin preparing presentations for road show File registration statement with the SEC. Begin preparing presentations for road show to attract other investment bankers to the syndicate. Comply with Blue Sky laws in to attract other investment bankers to the syndicate. Comply with Blue Sky laws in states where offering will be sold. states where offering will be sold.

Week 12Week 12 Receive comment letter on registration statement from SEC. Amend registration Receive comment letter on registration statement from SEC. Amend registration statement to satisfy SEC comments. statement to satisfy SEC comments.

Week 13Week 13 File amended registration statement with SEC. Prepare and distribute preliminary File amended registration statement with SEC. Prepare and distribute preliminary offering prospectus (called a “red herring”) to members of underwriting syndicate. offering prospectus (called a “red herring”) to members of underwriting syndicate. Begin road show meetings.Begin road show meetings.

Week 15Week 15 Receive approval for offering from SEC (unless further amendments are required). Receive approval for offering from SEC (unless further amendments are required). Issuing company and lead underwriter agree on final offering price. Prepare, file, and Issuing company and lead underwriter agree on final offering price. Prepare, file, and distribute final offering prospectus.distribute final offering prospectus.

Week 16Week 16 Company and underwriter sign the final agreement. Underwriter issues stock, collects Company and underwriter sign the final agreement. Underwriter issues stock, collects the proceeds from the sale, and delivers proceeds (less commission) to company.the proceeds from the sale, and delivers proceeds (less commission) to company.

Timetable for an IPOTimetable for an IPO

Chapter 12: Sources of FundsChapter 12: Sources of Funds 2828Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Simplified RegistrationsSimplified Registrationsand Exemptionsand Exemptions

GoalGoal: To give small companies easy access : To give small companies easy access to capital markets with simplified to capital markets with simplified registration requirements.registration requirements.

Regulation S-BRegulation S-BRegulation D: Rule 504 - Small Company Regulation D: Rule 504 - Small Company

Offering Registration (SCOR)Offering Registration (SCOR)Regulation D: Rule 505 and 506Regulation D: Rule 505 and 506

Chapter 12: Sources of FundsChapter 12: Sources of Funds 2929Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Simplified RegistrationsSimplified Registrationsand Exemptionsand Exemptions

(continued)(continued)

Section 4 (6)Section 4 (6)Rule 147 (Intrastate offerings)Rule 147 (Intrastate offerings)Regulation ARegulation ADirect Stock Offering on the Direct Stock Offering on the

World Wide Web (WWW)World Wide Web (WWW)

Chapter 12: Sources of FundsChapter 12: Sources of Funds 3030Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Sources of Debt CapitalSources of Debt Capital

Commercial banksCommercial banks

Chapter 12: Sources of FundsChapter 12: Sources of Funds 3131Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Commercial BanksCommercial Banks

Short-term loansShort-term loans Commercial loansCommercial loans Lines of creditLines of credit Floor planningFloor planning

Intermediate and long term Intermediate and long term loansloans Installment loans and contractsInstallment loans and contracts

...the heart of the financial market for small ...the heart of the financial market for small

businesses!businesses!

Chapter 12: Sources of FundsChapter 12: Sources of Funds 3232Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Six Most Common Reasons Bankers Six Most Common Reasons Bankers Reject Small Business LoansReject Small Business Loans

1.1. ““Our bank doesn’t make small business Our bank doesn’t make small business loans.” loans.” CureCure: Before applying for a loan, research : Before applying for a loan, research banks to find out which ones seek the type of banks to find out which ones seek the type of loan you need. loan you need.

2.2. ““I don’t know enough about you or your I don’t know enough about you or your business.”business.”CureCure: Develop a detailed business plan to : Develop a detailed business plan to present to the banker. present to the banker.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 3333Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Six Most Common Reasons Bankers Six Most Common Reasons Bankers Reject Small Business LoansReject Small Business Loans

3.3. “You haven’t told me why you need the “You haven’t told me why you need the money.” money.” CureCure: Your business plan should explain how : Your business plan should explain how much money you need and how you plan to much money you need and how you plan to use it. use it.

4.4. “Your numbers don’t support your loan “Your numbers don’t support your loan request.”request.”CureCure: Include a cash flow forecast in your : Include a cash flow forecast in your business plan. business plan.

(continued)(continued)

Chapter 12: Sources of FundsChapter 12: Sources of Funds 3434Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Six Most Common Reasons Bankers Six Most Common Reasons Bankers Reject Small Business LoansReject Small Business Loans

5.5. “You don’t have enough collateral.” “You don’t have enough collateral.” CureCure: Be prepared to pledge your company’s : Be prepared to pledge your company’s assets – and perhaps your personal assets – as assets – and perhaps your personal assets – as collateral for the loan. collateral for the loan.

6.6. “Your business does not support the loan on “Your business does not support the loan on its own.”its own.”CureCure: Be prepared to provide a personal : Be prepared to provide a personal guarantee on the loan. guarantee on the loan.

(continued)(continued)

Chapter 12: Sources of FundsChapter 12: Sources of Funds 3535Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Sources of Debt CapitalSources of Debt Capital

Commercial banksCommercial banksAsset-based lendersAsset-based lenders

Chapter 12: Sources of FundsChapter 12: Sources of Funds 3636Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Asset-Based BorrowingAsset-Based Borrowing

Discounting accounts Discounting accounts receivablereceivable

AccountsReceivable

Inventory financingInventory financing

Chapter 12: Sources of FundsChapter 12: Sources of Funds 3737Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Sources of Debt CapitalSources of Debt Capital

Commercial banksCommercial banks

Trade creditTrade creditEquipment suppliersEquipment suppliersCommercial finance companiesCommercial finance companiesSaving and loan associationsSaving and loan associations

Asset-based lendersAsset-based lenders $$

Chapter 12: Sources of FundsChapter 12: Sources of Funds 3838Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Sources of Debt CapitalSources of Debt Capital

Stock brokerage housesStock brokerage houses Insurance companiesInsurance companies Credit unionsCredit unions BondsBonds Private placementsPrivate placements Small Business Investment Companies Small Business Investment Companies

(SBICs)(SBICs) Small Business Lending Companies (SBLCs)Small Business Lending Companies (SBLCs)

(continued)(continued)

Chapter 12: Sources of FundsChapter 12: Sources of Funds 3939Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Sources of Debt CapitalSources of Debt Capital

Economic Development Administration (EDA)Economic Development Administration (EDA) Department of Housing and Urban Development Department of Housing and Urban Development

(HUD)(HUD) U.S. Department of Agriculture’s Rural Business-U.S. Department of Agriculture’s Rural Business-

Cooperative ServiceCooperative Service Small Business Innovation Research (SBIR) Small Business Innovation Research (SBIR) Small Business Technology Transfer programsSmall Business Technology Transfer programs Small Business Administration (SBA)Small Business Administration (SBA)

(continued)(continued)

Federally Sponsored Programs:Federally Sponsored Programs:

Chapter 12: Sources of FundsChapter 12: Sources of Funds 4040Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Small Business Administration Small Business Administration Loan ProgramsLoan Programs

Low Doc Loan ProgramLow Doc Loan ProgramSBASBAExpressExpress Program Program7(A) Loan Guaranty Program – the most 7(A) Loan Guaranty Program – the most

popular SBA loan programpopular SBA loan program

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

Bill

ion

s o

f $

1976 1978 1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002

SBA 7(A) Guaranteed Loans

Chapter 12: Sources of FundsChapter 12: Sources of Funds 4242Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Small Business Administration Small Business Administration Loan ProgramsLoan Programs

Low Doc Loan ProgramLow Doc Loan ProgramSBASBAExpressExpress Program Program7(A) Loan Guaranty Program – the most 7(A) Loan Guaranty Program – the most

popular SBA loan programpopular SBA loan programCAPLine ProgramCAPLine Program International Trade ProgramsInternational Trade Programs

Export Working Capital ProgramExport Working Capital Program International Trade ProgramInternational Trade Program

Chapter 12: Sources of FundsChapter 12: Sources of Funds 4343Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

SBA Loan ProgramsSBA Loan Programs

Section 504 Certified Development Section 504 Certified Development Company ProgramCompany Program

Microloan ProgramMicroloan ProgramPrequalification Loan ProgramPrequalification Loan ProgramDisaster LoansDisaster Loans

Chapter 12: Sources of FundsChapter 12: Sources of Funds 4444Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

State and Local Loan ProgramsState and Local Loan Programs

Capital Access Programs (CAPs) –Capital Access Programs (CAPs) –designed to encourage lenders to make designed to encourage lenders to make loans to businesses that do not qualify for loans to businesses that do not qualify for traditional financing. traditional financing.

Revolving Loan Fund (RLFs) – combine Revolving Loan Fund (RLFs) – combine private and public funds to make small private and public funds to make small business loans. business loans.

Chapter 12: Sources of FundsChapter 12: Sources of Funds 4545Copyright 2005 Prentice Hall Inc. A Pearson Education CompanyCopyright 2005 Prentice Hall Inc. A Pearson Education Company

Internal Methods of FinancingInternal Methods of Financing

Factoring - selling accounts receivable Factoring - selling accounts receivable outrightoutright

Leasing - assets rather than buying themLeasing - assets rather than buying themCredit cardsCredit cards