chapter 12 legal forms of organization. copyright © houghton mifflin company12-2 overview how to...

TRANSCRIPT

Chapter 12

Legal Formsof Organization

Copyright © Houghton Mifflin Company 12-2

Overview

• How to make the decision

• Legal forms of organization– Sole proprietorship– Partnership– Corporation– Limited liability company– Professional corporations– Nonprofit corporations

Copyright © Houghton Mifflin Company 12-3

How Would You Decide?

Copyright © Houghton Mifflin Company 12-4

Criteria for Choice

• Who will be the owners?

• Level of liability protection required

• Operating requirements and costs

• Effect on the tax strategy of the company & the founders– When do you expect to earn a profit?– How do you want to distribute earnings?

• Effect on financing plans

Copyright © Houghton Mifflin Company 12-5

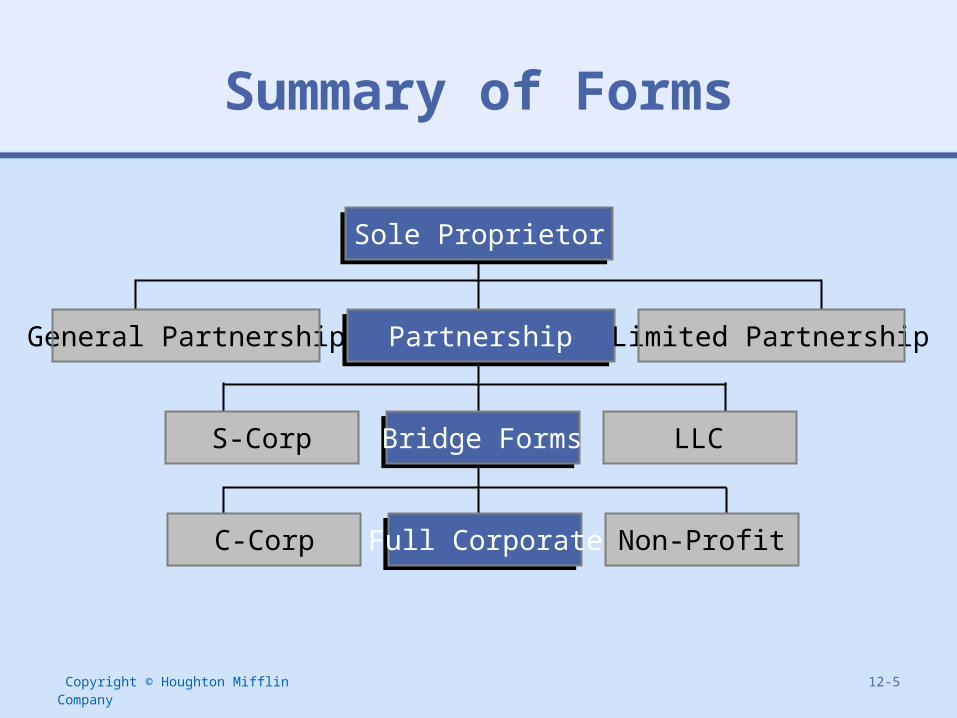

Summary of Forms

General Partnership

S-Corp

C-Corp Full Corporate Non-Profit

Bridge Forms LLC

Partnership Limited Partnership

Sole Proprietor

Copyright © Houghton Mifflin Company 12-6

Sole Proprietorship

• 76% of all businesses

• Flexible, easy, inexpensive

• Does not exist apart from the owner, so pays no tax

• Salary or draw not deductible as expense

• Hobby rule (3 of 5 years)

Copyright © Houghton Mifflin Company 12-7

Sole Proprietorship: Disadvantages

• Unlimited liability

• Difficult to raise debt capital

• Lacks advantage of team

• Survival dependent on owner

Copyright © Houghton Mifflin Company 12-8

Partnership

• Association of two or more persons as a business

• Doctrine of ostensible authority– One partner can bind the partnership

• Specific property rights

• Share in profit/loss according to contribution

Copyright © Houghton Mifflin Company 12-9

Partnership Agreement

• Duties and responsibilities

• Profit/loss distribution

• Transfer of interest

• Duration and dissolution

• Arbitration and dispute resolution

• Type of partnership– general versus limited– secret, silent, dormant

Copyright © Houghton Mifflin Company 12-10

C-Corporation

• Legal entity

• Survival of death and separation

• Limited liability of shareholders

• Issue different classes of stock

• Raise capital by selling stock

• More status

• Benefit from retirement funds, profit sharing, stock options

• Owners can lease their assets to the corp

Copyright © Houghton Mifflin Company 12-11

Disadvantages of Corporation

• Complex and costs more

• Stockholders do not have benefit of writing off losses

• Double taxation (earnings and dividends)

• Pay taxes on profits whether or not distributed as dividends

• Accountable to board of directors

Copyright © Houghton Mifflin Company 12-12

S-Corporation

• Not a tax-paying entity• Owners taxed on

corporate earnings• Deduct losses on

personal income tax up to amount invested

• No more than 75 stockholders, US citizens or legal residents

• One class of stock

Copyright © Houghton Mifflin Company 12-13

Disadvantages of S-Corp

• Difficult to get loans if distributes earnings

• No deductions based on medical reimbursements or health insurance plans

• If not a cash business, may not be able to pay taxes out of business

• Must convert to C for IPO

Copyright © Houghton Mifflin Company 12-14

Limited Liability Company

• Limited liability of corporation with pass-through tax advantages of partnership

• Members and interests

• Articles of organization

• Managers, officers, members not personally liable

• Most organize for tax purposes as partnership

• No limitation to membership, more than one class of stock

Copyright © Houghton Mifflin Company 12-15

Non-Profit

• Established for charitable, public, religious, or mutual benefit

• IRS 501(c)(3) tax exempt

• Limited liability

• Owners give up proprietary interest

• Perpetual existence

• Apply for grants

Copyright © Houghton Mifflin Company 12-16

Take-Aways

• List what students took away from the discussion in real time