challenge/module exams 2021

TRANSCRIPT

PASS

CHALLENGE/MODULE

EXAMS

2021

TECHNICAL

BINDER

© Professional Accounting Supplementary School (PASS) 2021 Technical Binder for Module/Challenge Exams

INTRODUCTION TO PASS TECHNICAL BINDER

2021 MODULE/CHALLENGE EXAMS

The PASS Technical Binder for the Module/Challenge exams is arranged as follows. For each

competency, it provides a summary of the technical matter for which students are responsible, as

well as simulated multiple choice and other objective format questions.

This binder does not include cases, material for case take-ups or material for the Assurance

Technique sessions. This material is included in a separate case binder.

Content of Technical Binder

The binder includes material which covers all of the 6 competencies listed in the CPA

Competency Map. These include:

I Strategy and Governance

II Financial Reporting

III Audit and Assurance

IV Finance

V Management Accounting

VI Taxation

Areas in financial reporting not covered in the binder include minor financial reporting topics

that are easy for students to learn on their own

For minor topics (listed on the 3rd

page of the introduction), simulated multiple choice questions

are provided in the last tab of the binder. As these questions are not reviewed in class, detailed

solutions to each question are also provided. After reviewing each of these subject areas,

students can use these questions to test their knowledge of the minor accounting topics.

Core 1 versus Electives

This binder includes all of the technical material necessary for the core 1 and core 2 modules as

well as for the electives for both Assurance and Taxation. The material necessary for the

electives is not generally broken out separately from that required for the core exams, as there is

a lot of overlap between the two sets of exams and in many cases the same topic is required for

both sets of exams, with the only difference being that the topic is examinable at a higher level

© Professional Accounting Supplementary School (PASS) 2021 Technical Binder for Module/Challenge Exams

for the elective exam than for core 1. For all of these “overlap” topics the material is covered at

the level required for the elective exams.

In the event that you are writing Core 1 before the Assurance/Tax Elective exams (or will

not be writing Assurance/Tax Elective exams) a discussion of the level at which you need to

learn assurance and taxation for the Core 1 versus elective exams is provided below.

Please note that Information and Information Technology (IT) is not a separate competency in

the CPA Competency Map. Rather IT topics are incorporated into the various competencies

listed above. The IT section of the binder will cover the IT elements of the various competencies

which include an IT component.

Taxation

The taxation notes in Tab 10 provide all of the material that a student studying for the Taxation

Elective would require. Students who are writing Core 1 will only need to focus on a portion of

the material as they require less tax knowledge than those writing the taxation elective. Please

read the preface to the Taxation notes at the beginning of Tab 10 before reading the taxation

material as the preface provides instruction on what students writing core 1 should focus on.

Assurance

Similar to the case of Taxation, the Assurance notes include all of the material for which you are

responsible for the Core 1 exam as well as additional material which is only important for

students who will be choosing assurance as one of their electives. The distinction between the

knowledge level required for the Core 1 and Assurance elective exams is however not as

significant as it is for Taxation.

For the case of assurance you will note that most topics are at the A or B level for both exams.

The one area however, which is far less important for Core 1 (i.e. most topics in this area are

level C) is special engagements - as opposed to topics relating to engagements in connection

with general purpose financial statements which are generally level A or B for the Core exam.

Very minimal time should be spent on the materials that deal with special engagements unrelated

to general purpose financial statements.

Information for Students who Acquired Binder and will also be Watching Videos

Financial Accounting - Videos

Most of the major technical topics covered in the binder are also covered in the videos. There

are however a few topics which are not covered in the videos. These include:

© Professional Accounting Supplementary School (PASS) 2021 Technical Binder for Module/Challenge Exams

1) Technical topics that are covered by CPA Canada through videos

A list of these topics is provided on page 4.

2) Topics that students can learn on their own

These topics include: Earnings per Share (EPS) and Employer Future Benefits

Please note that for the above topics, although no video is provided, extensive technical notes

along with objective format questions are included in the binder.

Management Accounting and Finance

Certain topics which are self-explanatory are not covered in videos. Please watch the

introduction videos for management accounting and finance before watching the other videos for

these competencies. The introductory videos indicate which topics will not be covered by video.

MINOR TOPICS

ASPE

Generally Accepted Accounting Principals (Section 1100)

Unincorporated businesses (Section 1800)

Contractual obligations (Section 3280)

Investment tax credits (Section 3805)

Economic dependence (Section 3841)

Public sector accounting*

IFRS

Operating segments – IFRS 8

Interim financial statements – IAS 34

*Based upon the Competency Map this topic only required at level “C” proficiency.

© Professional Accounting Supplementary School (PASS) 2021 Technical Binder for Module/Challenge Exams

TABLE OF CONTENTS

1 FINANCIAL REPORTING – LEASES, RELATED PARTIES, NON MONETARY

TRANSACTIONS, DISPOSAL OF LONG LIVED ASSETS AND DISCONTINUED

OPERATIONS, IMPAIRMENT OF ASSETS

2 FINANCIAL REPORTING – MISCELLANEOUS ACCOUNTING TOPICS (E.G.

CONCEPTUAL FRAMEWORK, PPE, INTANGIBLES, ARO, AGRICULTURE ETC.)

3 FINANCIAL REPORTING – ACCOUNTING FOR INCOME TAXES

4 FINANCIAL REPORTING – EARNINGS PER SHARE (EPS) AND EMPLOYER

FUTURE BENEFITS

5 FINANCIAL REPORTING – CONSOLIDATIONS, EQUITY METHOD, INTERESTS

IN JOINT VENTURES AND JOINT ARRANGEMENTS, FINANCIAL

INSTRUMENTS, ACCOUNTING FOR NPO, FOREIGN CURRENCY

TRANSLATION

6 MANAGEMENT ACCOUNTING

7 STRATEGY AND GOVERNANCE & INFORMATION AND INFORMATION

TECHNOLOGY

8 FINANCE

9 AUDIT AND ASSURANCE

10 TAXATION

11 SIMULATED MULTIPLE CHOICE QUESTIONS AND SOLUTIONS ON MINOR

TOPICS

PASS

EXCERPT

NON-MONETARY TRANSACTIONS

3) NON-MONETARY TRANSACTIONS

Introduction

Under ASPE, non-monetary transactions is covered under Section 3831 Non- Monetary

Transactions

Under IFRS there is no specific standard on non-monetary transactions; it however comes up in a

number of standards including

IAS 16 Property, Plant and Equipment

IFRS 15 Revenue from Contracts with Customers

IAS 40 Investment Properties

IAS 20 Accounting for Government Grants and Disclosure of Government Assistance,

IAS 38 Intangibles and in SIC 31 which deals with barter transactions involving advertising.

The summary below is based on section 3831; any differences between 3831 and IFRS are

highlighted

DEFINITIONS*

Monetary assets and liabilities.

Money or claims to future cash flows, that are fixed or determinable in amounts and timing by

contract or other arrangement.

Non-Monetary Assets and Liabilities

Assets and liabilities that are not monetary.

Non-Monetary Transactions

Includes:

Non -Monetary Exchanges

Exchange of Non-Monetary items for other Non-Monetary items with little or no monetary

consideration involved.

i.e. Some amount of cash involved in transaction does not necessarily indicate monetary

transaction.

Non-Monetary Non-Reciprocal Transfers

Transfers of Non-Monetary items without consideration

Would include for example:

• Donations of non -monetary asset or service

• Payment of dividend in kind

• Stock dividend (when the shareholder has option of receiving cash or shares)

• Distribution of assets to owners in liquidation of all or part of business

* The above definitions are based on section 3831

Non-Monetary Transactions - General Rules

If both the item given up and received can be equally reliably determined, the fair value of the

item given up should be used to measure the asset received.

If one item’s fair value is more reliable than the other, use that item.

If the value of the asset given up can not be reliably measured and the value of the asset received

can be reliably measured, the exchange should be measured based upon the value of the asset

received.

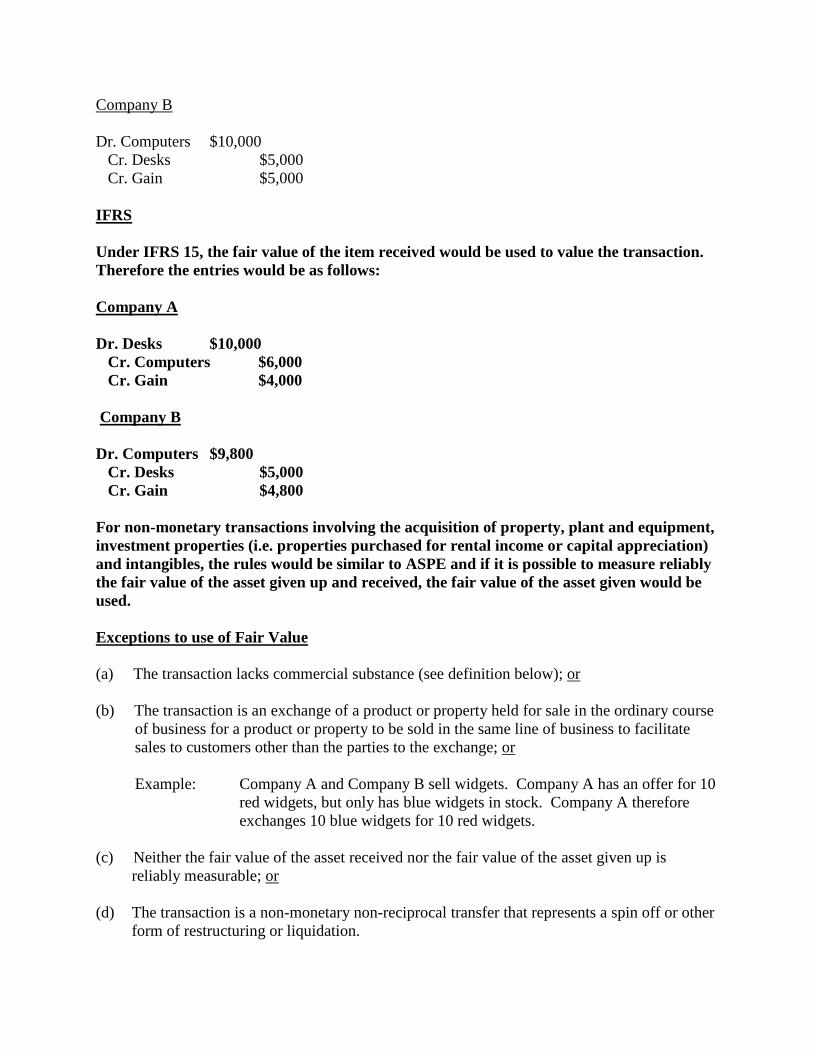

Under IFRS the rule is generally the same except under IFRS 15 Revenue; under this IFRS

revenue is measured at the fair value of the goods or services received, when both the goods

given up and received can be measured equally reliably. If the entity cannot reliably measure

the fair value of the asset received, the entity would look at the selling price of the goods

received.

In all other IFRS standards in which non-monetary transactions is dealt with, similar to

ASPE if both the value of the asset given up and received can be measured equally reliably,

the fair value of the asset given up is used

Example of Accounting for Non Monetary Transaction Using Fair Value

Company A provides 10 computers to Company B in exchange for 10 desks. The fair values of

the computers and desks can be reliably determined. The carrying values and fair values of the

assets are as follows:

Carrying Value Fair value

Computers $6,000 $9,800

Desks $5,000 $10,000

The entries are as follows:

Company A

Dr. Desks $9,800

Cr. Computers $6,000

Cr. Gain $3,800

Company B

Dr. Computers $10,000

Cr. Desks $5,000

Cr. Gain $5,000

IFRS

Under IFRS 15, the fair value of the item received would be used to value the transaction.

Therefore the entries would be as follows:

Company A

Dr. Desks $10,000

Cr. Computers $6,000

Cr. Gain $4,000

Company B

Dr. Computers $9,800

Cr. Desks $5,000

Cr. Gain $4,800

For non-monetary transactions involving the acquisition of property, plant and equipment,

investment properties (i.e. properties purchased for rental income or capital appreciation)

and intangibles, the rules would be similar to ASPE and if it is possible to measure reliably

the fair value of the asset given up and received, the fair value of the asset given would be

used.

Exceptions to use of Fair Value

(a) The transaction lacks commercial substance (see definition below); or

(b) The transaction is an exchange of a product or property held for sale in the ordinary course

of business for a product or property to be sold in the same line of business to facilitate

sales to customers other than the parties to the exchange; or

Example: Company A and Company B sell widgets. Company A has an offer for 10

red widgets, but only has blue widgets in stock. Company A therefore

exchanges 10 blue widgets for 10 red widgets.

(c) Neither the fair value of the asset received nor the fair value of the asset given up is

reliably measurable; or

(d) The transaction is a non-monetary non-reciprocal transfer that represents a spin off or other

form of restructuring or liquidation.

Under IFRS, similar to ASPE, fair value would not be used in conditions (a) and (c).

Condition (b) is outside the scope of IFRS 15 Revenue.

Commercial Substance

A transaction has commercial substance if it causes an identifiable and measurable change in

the economic circumstances of the entity.

More specifically, commercial substance exists when the entity’s future cash flows are expected

to change significantly as a result of a transaction.

This will occur when:

(A) The risk, timing or amount of the cash flows, of the asset received (referred to as the

“configuration”), differs significantly from the configuration of the cash flows of the asset

given up

Example: A company exchanges computer equipment for trucks

or

(B) The present value of the cash flows from the continuing use and disposal at the end of its

life (referred to as the “entity specific value”) differs from the entity specific value of the

asset given up and the difference is significant relative to the fair value of the assets

exchanged

Example: A company owns an apartment building in Toronto. They exchange that

building for an apartment building in Montreal that is next store to an apartment building

the company already owns. The company’s plan following the exchange is to use the same

management and maintenance staff for both buildings in Montreal leading to synergistic

cost savings. Condition B above, would be met if the present value of the cost savings is

significant relative to the fair value of the buildings exchanged.

Under IFRS the concept of “entity specific value” also comes up and is defined in a similar

way to ASPE; however IFRS explicitly states that the cash flows must be after tax

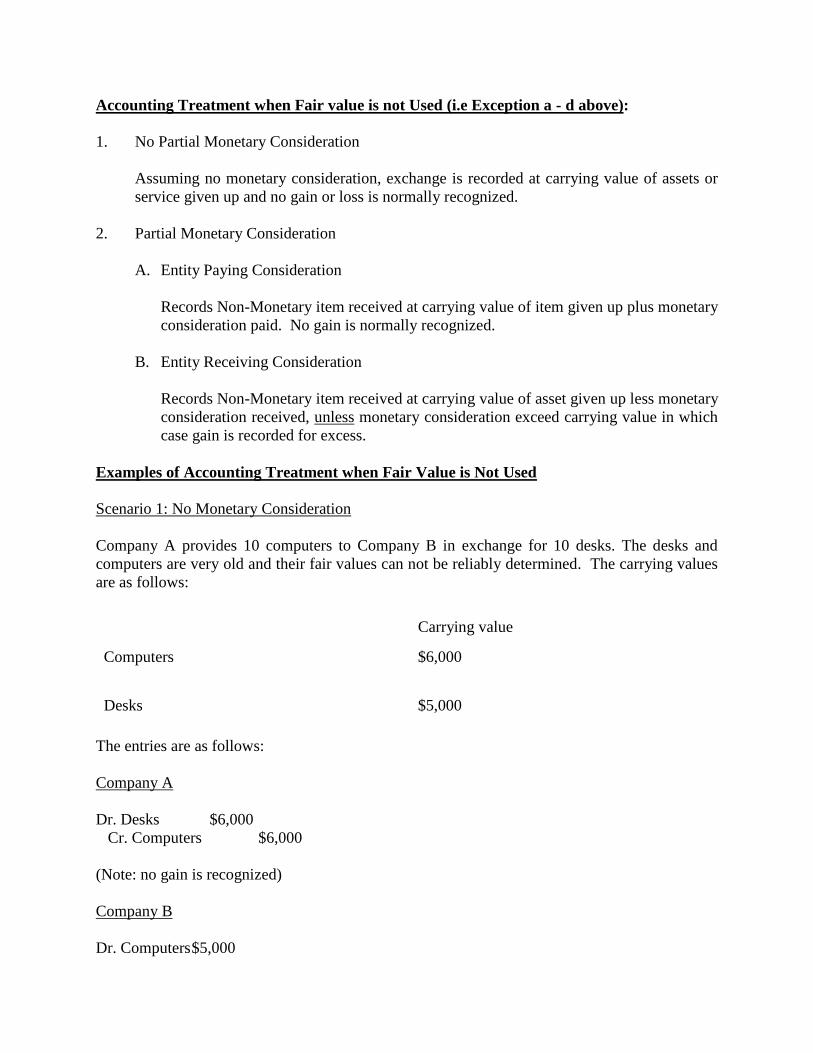

Accounting Treatment when Fair value is not Used (i.e Exception a - d above):

1. No Partial Monetary Consideration

Assuming no monetary consideration, exchange is recorded at carrying value of assets or

service given up and no gain or loss is normally recognized.

2. Partial Monetary Consideration

A. Entity Paying Consideration

Records Non-Monetary item received at carrying value of item given up plus monetary

consideration paid. No gain is normally recognized.

B. Entity Receiving Consideration

Records Non-Monetary item received at carrying value of asset given up less monetary

consideration received, unless monetary consideration exceed carrying value in which

case gain is recorded for excess.

Examples of Accounting Treatment when Fair Value is Not Used

Scenario 1: No Monetary Consideration

Company A provides 10 computers to Company B in exchange for 10 desks. The desks and

computers are very old and their fair values can not be reliably determined. The carrying values

are as follows:

Carrying value

Computers $6,000

Desks $5,000

The entries are as follows:

Company A

Dr. Desks $6,000

Cr. Computers $6,000

(Note: no gain is recognized)

Company B

Dr. Computers $5,000

Cr. Desks $5,000

(Note: no gain is recognized)

Scenario 2: Partial Monetary Consideration

Company A gives Company B 10 computers plus $200 cash in exchange for 10 desks. The desks

and computers are very old and their fair values can not be reliably determined. The carrying

values are as follows (same as last example):

Carrying value

Computers $6,000

Desks $5,000

The entries are as follows:

Company A

Dr. Desks $6,200 ($6,000 + $200)

Cr. Computers $6,000

Cr. Cash $200

(Note: no gain is recognized)

Company B

Dr. Computers $4,800 ($5,000 - $200)

Dr. Cash $200

Cr. Desks $5,000

(Note: no gain is recognized)

Treatment is similar under IFRS

Restructuring or Liquidation

Non-Monetary Non-Reciprocal transfer to owners that represents spin-off or other form of

restructuring or liquidation should be recorded at carrying value of items transferred.

e.g. - Entity distributes operating division to owners.

- Parent company distributes shares of subsidiary directly to shareholders.

Under IFRS there is an Interpretation IFRIC 17 which deals with the distribution of non-

cash assets to owners. See summary of IFRIC in Appendix 1

Government Grants

A government grant may take the form of a transfer of a non-monetary asset, such as land or

other resources, for the use of the entity.

The CICA Handbook Section on Governance assistance (Section 3800) does not address this

situation; it is however assumed that the grant and the asset would be valued at fair value

IFRS 20 Accounting for Government Grants and Disclosure does address this issue and

offers two alternatives:

(1) Record both asset and grant at fair value

(2) Record both asset and grant at a nominal amount

Presentation and Disclosure

Section 3831 requires the following disclosure relating to non-monetary transactions:

(i) nature

(ii) basis of measurement

(iii) amount and

(iv) related gains and losses.

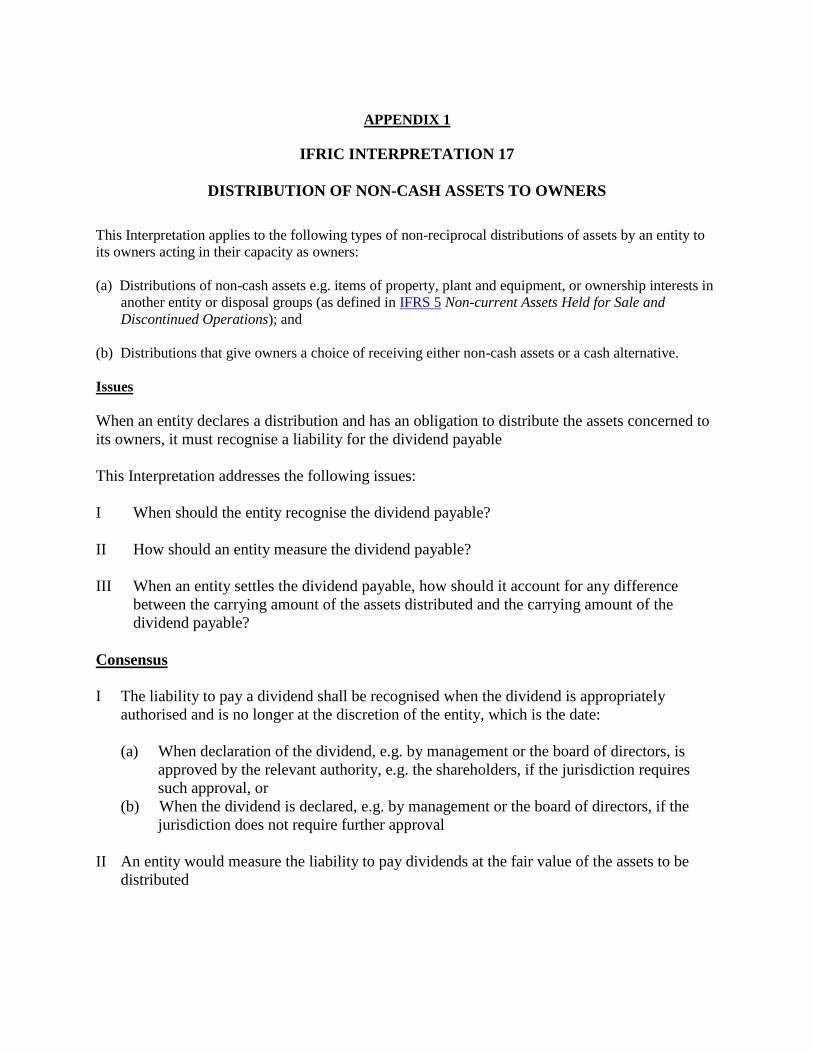

APPENDIX 1

IFRIC INTERPRETATION 17

DISTRIBUTION OF NON-CASH ASSETS TO OWNERS

This Interpretation applies to the following types of non-reciprocal distributions of assets by an entity to

its owners acting in their capacity as owners:

(a) Distributions of non-cash assets e.g. items of property, plant and equipment, or ownership interests in

another entity or disposal groups (as defined in IFRS 5 Non-current Assets Held for Sale and

Discontinued Operations); and

(b) Distributions that give owners a choice of receiving either non-cash assets or a cash alternative.

Issues

When an entity declares a distribution and has an obligation to distribute the assets concerned to

its owners, it must recognise a liability for the dividend payable

This Interpretation addresses the following issues:

I When should the entity recognise the dividend payable?

II How should an entity measure the dividend payable?

III When an entity settles the dividend payable, how should it account for any difference

between the carrying amount of the assets distributed and the carrying amount of the

dividend payable?

Consensus

I The liability to pay a dividend shall be recognised when the dividend is appropriately

authorised and is no longer at the discretion of the entity, which is the date:

(a) When declaration of the dividend, e.g. by management or the board of directors, is

approved by the relevant authority, e.g. the shareholders, if the jurisdiction requires

such approval, or

(b) When the dividend is declared, e.g. by management or the board of directors, if the

jurisdiction does not require further approval

II An entity would measure the liability to pay dividends at the fair value of the assets to be

distributed

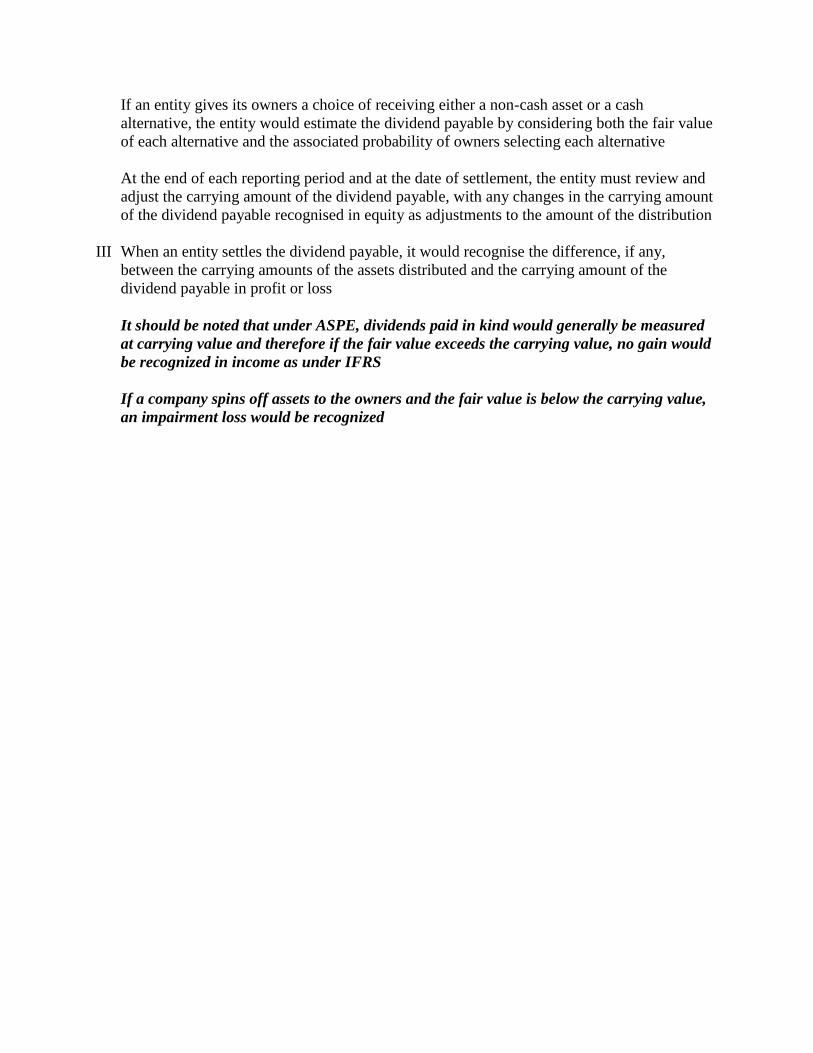

If an entity gives its owners a choice of receiving either a non-cash asset or a cash

alternative, the entity would estimate the dividend payable by considering both the fair value

of each alternative and the associated probability of owners selecting each alternative

At the end of each reporting period and at the date of settlement, the entity must review and

adjust the carrying amount of the dividend payable, with any changes in the carrying amount

of the dividend payable recognised in equity as adjustments to the amount of the distribution

III When an entity settles the dividend payable, it would recognise the difference, if any,

between the carrying amounts of the assets distributed and the carrying amount of the

dividend payable in profit or loss

It should be noted that under ASPE, dividends paid in kind would generally be measured

at carrying value and therefore if the fair value exceeds the carrying value, no gain would

be recognized in income as under IFRS

If a company spins off assets to the owners and the fair value is below the carrying value,

an impairment loss would be recognized

© Professional Accounting Supplementary School (PASS) 1

Non Monetary Items

Multiple Choice Questions

1. Which of the following would qualify as a non-monetary transaction under ASPE?

(a) An auto manufacturer enters into a transaction with equipment manufacturer to exchange

an automobile in return for manufacturing equipment. The FMV and carrying value of the

automobile are $35,000 and $15,000 respectively. The carrying value of the manufacturing

equipment is $20,000. As the manufacturing equipment is worth $150 less than the

automobile the equipment manufacturer also pays $150 in addition to giving up the

equipment.

(b) Company A transfers to company B a 5% investment in Laidlaw Inc in exchange for

mandatorily redeemable preferred shares in GM.

(c) Company A, a bank, allows company B, a furniture manufacturer in financial distress, to

settle its loan with the bank by giving the bank furniture in lieu of paying off their loan.

(d) None of the above

2. Jackal Inc. (JI) decides to purchase a rental property. As they have insufficient cash

available and can not get financing, they decided to purchase the property through a barter

transaction. The company owned a piece of land they purchased very recently, which they

were originally planning to use to build a new plant, but they then decided not to go ahead

with building the plant. The company therefore decided to give up the land in return for

the rental property. The rental property is in an area of London Ontario, in which similar

properties have turned over quite frequently in the recent past. Which of the following

correctly describes the accounting for the transaction under IFRS?

(a) The company should measure the value of the new building on its balance sheet at date of

acquisition, based upon the fair value of the land given up.

(b) The company should measure the value of the new building on its balance sheet at date of

acquisition, based upon the fair value of the building received.

(c) The company should measure the value of the new building on its balance sheet at date of

acquisition, based upon the carrying value of the land given up.

© Professional Accounting Supplementary School (PASS) 2

(d) The company should measure the value of the new building on its balance sheet at date of

acquisition, based upon the carrying value of the building received..

The following scenario relates to questions 3 and 4

GN Inc. an auto manufacturer has committed to a plan to sell the manufacturing equipment in

one of its plants and has found a buyer. It is planning to replace the equipment with new high

technology robotics equipment. The carrying value of the equipment is $500,000. The cost of

selling the equipment includes a brokerage fee of $25,000 and internal charges of $5,000 based

on a proration of salary of those individuals who spent time negotiating and arranging the sale.

The sales price is $520,000.

3. Assuming that GN stipulates that they will not transfer the equipment to the buyer until the

new robotics equipment is manufactured, delivered and installed at GN, which of the

following most accurately describes the presentation of the existing equipment?

(a) It would be presented as held for sale

(b) It would not be presented as held for sale

(c) It would not be presented as held for sale as long as there is a commitment from the

manufacturer of the new equipment to deliver and install the equipment with 1 year.

(d) It would not be presented as held for sale unless there is an expectation that the

manufacturer of the new equipment will deliver and install the new equipment within 1

year.

4. Assuming that GN agrees to transfer the existing equipment to the buyer as soon as the

buyer can find a shipper to ship the equipment, regardless of when the new equipment is

manufactured, delivered and installed, which of the following is the amount at which the

equipment would be valued in the financial statements.

(a) $490,000

(b) $500,000

(c) $495,000

(d) $520,000

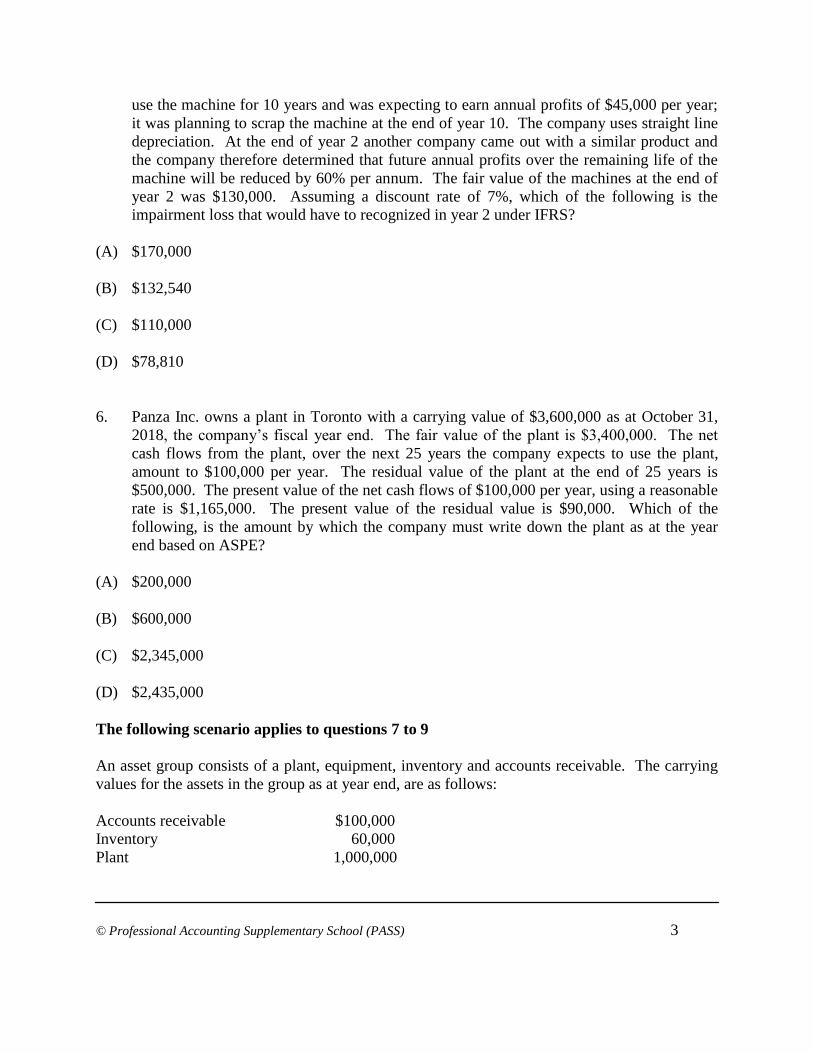

5. In year 1 Polygast Inc. (PI) purchased a machine to produce an MP3 player that is similar

to the Apple I-pod. The cost of the machine was $300,000. The company was planning to

© Professional Accounting Supplementary School (PASS) 3

use the machine for 10 years and was expecting to earn annual profits of $45,000 per year;

it was planning to scrap the machine at the end of year 10. The company uses straight line

depreciation. At the end of year 2 another company came out with a similar product and

the company therefore determined that future annual profits over the remaining life of the

machine will be reduced by 60% per annum. The fair value of the machines at the end of

year 2 was $130,000. Assuming a discount rate of 7%, which of the following is the

impairment loss that would have to recognized in year 2 under IFRS?

(A) $170,000

(B) $132,540

(C) $110,000

(D) $78,810

6. Panza Inc. owns a plant in Toronto with a carrying value of $3,600,000 as at October 31,

2018, the company’s fiscal year end. The fair value of the plant is $3,400,000. The net

cash flows from the plant, over the next 25 years the company expects to use the plant,

amount to $100,000 per year. The residual value of the plant at the end of 25 years is

$500,000. The present value of the net cash flows of $100,000 per year, using a reasonable

rate is $1,165,000. The present value of the residual value is $90,000. Which of the

following, is the amount by which the company must write down the plant as at the year

end based on ASPE?

(A) $200,000

(B) $600,000

(C) $2,345,000

(D) $2,435,000

The following scenario applies to questions 7 to 9

An asset group consists of a plant, equipment, inventory and accounts receivable. The carrying

values for the assets in the group as at year end, are as follows:

Accounts receivable $100,000

Inventory 60,000

Plant 1,000,000

© Professional Accounting Supplementary School (PASS) 4

Equipment 700,000

$1,860,000

The total aggregate carrying value is not recoverable and exceeds the fair value by $400,000.

The fair value of the inventory is $65,000.

7. Which of the following is the amount at which the inventory would be reflected, in the

financial statements at year end under ASPE?

(A) $60,000 (B) $65,000 (C) $48,000 (D) $50,000

8. Which of the following is the amount at which the equipment would be reflected, in the

financial statements at year end under ASPE, assuming that the fair value of the

equipment is not determinable?

(A) $548,000 (B) $536,000 (C) $526,000 (D) $562,000

9. Which of the following is the amount at which the plant would be reflected in the

financial statements at year end under ASPE, assuming that the fair value of the

equipment is known to be $550,000?

(A) $764,000 (B) $584,000

(C) $750,000 (D) $749,000

© Professional Accounting Supplementary School (PASS) 5

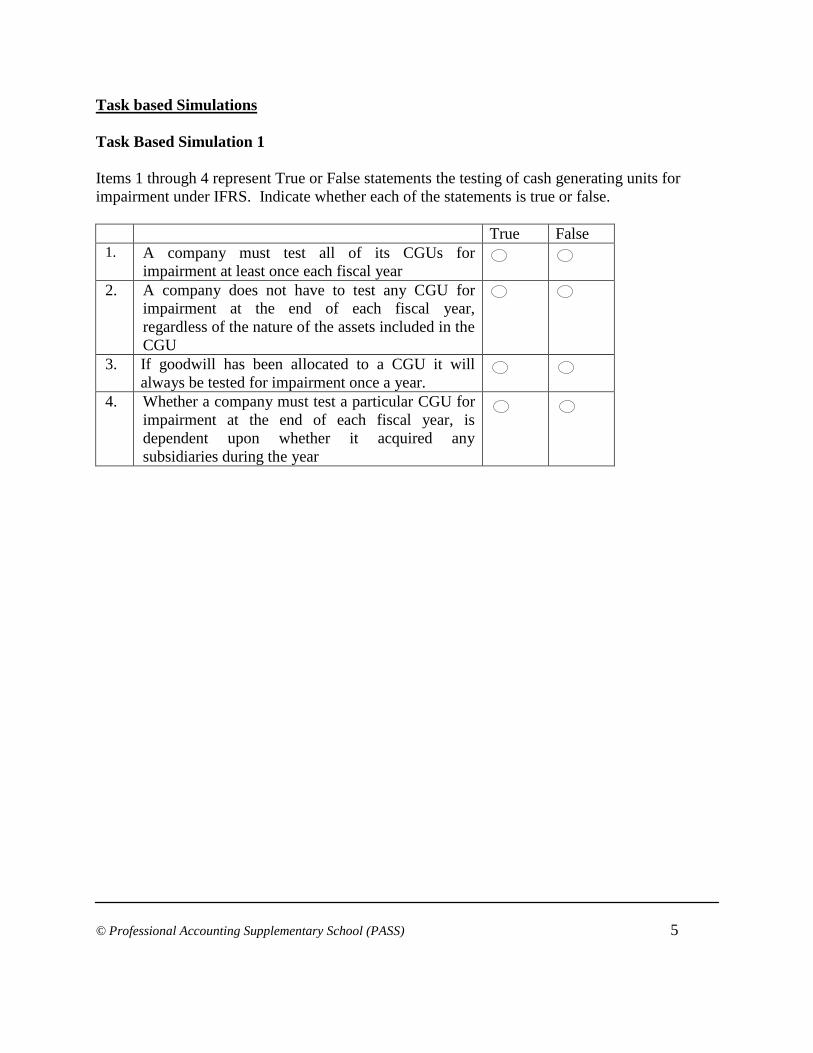

Task based Simulations

Task Based Simulation 1

Items 1 through 4 represent True or False statements the testing of cash generating units for

impairment under IFRS. Indicate whether each of the statements is true or false.

True False 1. A company must test all of its CGUs for

impairment at least once each fiscal year

2. A company does not have to test any CGU for

impairment at the end of each fiscal year,

regardless of the nature of the assets included in the

CGU

3. If goodwill has been allocated to a CGU it will

always be tested for impairment once a year.

4. Whether a company must test a particular CGU for

impairment at the end of each fiscal year, is

dependent upon whether it acquired any

subsidiaries during the year

© Professional Accounting Supplementary School (PASS) 6

Task Based simulation 2

Items 1 through 7 describe scenarios. For each item indicate whether the the item represents a

discontinued operation or would be included in continuing operations based on IFRS.

Discontinued

Operation

Continuing

Operations

1.

1.

Company sells 2 stores in a suburb of Calgary and replaces the

stores with a new large super store that will sell the same products

as the 2 stores which were sold.

2 2.

Manufacturer of soaps and shampoos and other hygiene products,

disposes of its Shampoo Division line, which accounts for 25% of

company sales. The operations and cash flows of the shampoo

product line, can be distinguished operationally and for financial

reporting purposes from the rest of the company.

3 3.

Company which manufactures bicycles and paint has committed to

a plan to close down its paint operation following year end. The

operations and cash flows of the paint business can be

distinguished operationally and for financial reporting purposes

from the rest of the company.

4. Company involved in residential and commercial construction

sold its commercial construction business which accounts for 40%

of company sales during the year. Separate records are kept for

each division. The company will continue to be significantly

involved in the commercial operation, as remuneration for the sale

is based upon the profitability of the business.

5. Company involved in manufacturing auto parts and motorcycle

parts decided to out source the manufacturing of motorcycle parts

and therefore sold the motorcycle plant. The operations and cash

flows of the motorcycle division can be distinguished

operationally and for financial reporting purposes from the rest of

the company

6. Company was involved in manufacturing hockey uniforms and

baseball uniforms. The manufacturing took place in the same

plant and the same machines were used for both hockey and

baseball uniforms. The same employees were involved in the

manufacture of both types of uniforms although there were

separate production runs for hockey versus baseball uniforms.

During the year the company discontinued the production of and

sale of baseball uniform, which accounted for 45% of sales

7. Company decided in the current year to dispose of a subsidiary

that was purchased 2 years ago

© Professional Accounting Supplementary School (PASS) 7

Task based Simulation 3

Farlinger Inc.(FI) is in the business of buying and selling land. (FI) owns a piece of land in

Toronto. The company was approached by a developer who is interested in buying their land

next year, provided FI can also sell them the plot of land adjacent to their own land, which is

owned by Maverick Inc (MI). FI therefore entered into a transaction with MI in which they

exchanged a piece of land they own in Vancouver for MI’s land which lies adjacent to their land

in Toronto, in order to be able to make the sale to the developer.

FI’s land located in Vancouver, was purchased in 1966 for only $500,000. Today the land is

worth $10 million. The land MI will provide to FI in exchange for the Vancouver land, is worth

$9,300,000. Therefore MI will give FI $700,000 in addition to giving up their land in Toronto,

in return for FI’s land in Vancouver. The carrying value of the land in Vancouver FI is giving

up, is equal to its historic cost of $500,000. The carrying value of the land MI is giving up is

$950,000.

Both FI and MI use ASPE to prepare their financial statements.

© Professional Accounting Supplementary School (PASS) 8

Items 1 through 4 below describe the items that would be reported in FI’s amd MI’s financial statements. For each item, select from

the following the correct numerical responses. An amount may be selected once, more than once or not at all.

A. $0 D. $600,000 G. $1,650,000 J. $10,000,000

B. $100,00 E. $500,000 H. $9,300,000

C. $200,000 F. $950,000 I. $8,350,000

Amount

A

B C D E F G H I J

1

1.

Carrying value of

land received in FI’s

F/S

2 Carrying value of

land received in

MI’s F/S

Items 3 and 4 require a second response. For each item indicate whether a gain or loss would be recognized

Amount Gain Loss

A

B C D E F G H I J

3 Gain or loss reported

on transaction in FI’s

F/S

4 Gain or loss reported

on transaction in

MI’s F/S