ch.3 inventory management - iems 3/ch.3... · ch.3 inventory management edited by dr. seung hyun...

TRANSCRIPT

Module 3. Value Enhancement Strategies.

Ch.3 Inventory Management

Edited by Dr. Seung Hyun Lee (Ph.D., CPM)IEMS Research Center, E-mail : [email protected]

- 1 -

■ Functions of Inventory. [Task 304]

Functions of Inventory. ■ Uncertainty. ․ Uncertainty can take two forms, variation in quantity and variation in timing.

․ Quantity uncertainty can be caused by back ordering by the supplier, defects received for the supplier, or industry standard variable quantities. The usual method for dealing with quantity uncertainty is to use safety stock.

․ For timing uncertainty, the most appropriate tool is safety leadtime. Safety leadtime involves looking at the supplier's variation in leadtime and ordering far enough in advance to reduce the risk of late delivery.

- 2 -

■ Functions of Inventory. [Task 304]

Functions of Inventory. ■ Decoupling. ․ Decoupling is the use of inventory to isolate one internal process from another. By putting inventory between two processes, each process is unaffected by the performance of the other process.

■ Anticipation. ․ Anticipated inventories are created for a special purpose, such as seasonality, special promotions, anticipated of shortages, anticipated of strikes, political instabilities, end-of-life runs, or anticipated price increases.

- 3 -

■ Functions of Inventory. [Task 304]

Functions of Inventory. ■ Economies of Scale. ․ Economies of scale inventories are created by ordering or producing in quantities to obtain the lowest unit cost.

■ Transportation. ․ Transportation inventories, also called pipeline inventories, are the inventories that are in transit between supplier and purchaser.

- 4 -

■ Inventory Classification. [Task 304]

Inventory Classification. ■ Raw Materials. ․ Raw materials are input goods intended for combination and/or conversion through the manufacturing process into semi-finished or finished goods.

■ In-process Goods or Work-In-Process(WIP) ․ These are goods in the process of being manufactured and are only partially completed.

■ Finished Goods. ․ These represents the completed conversion of raw materials and components into the final product.

■ Maintenance, Repair, and Operating Supplies (MRO). ․ These inventories include parts, supplies, and materials used in or consumed by routine maintenance and repair of operating equipment.

- 5 -

■ Inventory Classification. [Task 304]

Inventory Classification. ■ Others. ․ Resales goods. These are goods acquired for resale. Such goods may be purchased by a wholesaler for resale to distributors, or by distributors for resale to consumers.

․ Capital goods. These are items that will not be used up or consumed during a single operation period. Tax laws require that such items be capitalized, and a predetermined percentage of their costs be recognized as an expense each operating period, over a predetermined timeframe, according to equipment classes.

․ Construction materials. These are raw materials and components for consideration projects.

- 6 -

■ Inventory Classification. [Task 304]

Inventory Classification. ■ Others. ․ Hard goods/soft goods. The definition of hard goods and soft goods will vary by industry. For example, in data processing hard goods include apparatus such as computers and terminals, while soft goods include software and data storage media. Hard goods in the retail sector include appliances, luggage, and electronics while soft goods include clothing, linens, and bedding.

․ Components. These are the "raw materials" of assembly operations. Just as raw materials are converted to finished goods in a manufacturing operation, components and parts are assembled into finished goods in an assembly operation.

- 7 -

■ Inventory Classification. [Task 304]

Inventory Classification. ■ Others. ․ Obsolete. Finished goods, raw materials, resale goods, or components are no longer needed when technically obsolete or when the product is no longer produced or sold. Equipment may also be considered obsolete inventory if it is no longer needed.

․ Defective. Items that have been rejected for use and are waiting to be returned to the supplier, or to be scraped, or reworked.

- 8 -

■ Inventory Management System. [Task 304]

Order Point System. ■ Economic Order Quantity (EOQ). ․ EOQ is the order quantity where the time period cost of ordering equals the time period cost of holding that inventory, thereby minimizing the sum of the total of these two costs.

․ EOQ =2DSH (where, D = annual demand, S = Cost to place an order.

H = Cost to hold one unit of the item)

- 9 -

■ Inventory Management System. [Task 304]

Order Point System. ■ EOQ with Simultaneous Usage. ․ There are cases when first produced units of an item on order may be used while the balance of that reorder quantity is still being produced, such as when a production department is supplied by an in-house machine shop or another production department.

․ EPQ =2DSH×

p(p-d)

(where, p = production rates. d = demand rates)

- 10 -

■ Inventory Management System. [Task 304]

Order Point System. ■ Determining Order Point. ․ The greater the stability in usage or item demand, the easier it is to plan order timing. If an item has a wide variation in usage quantities, it is much more difficult to determine when the item's demand may create an out-of-stock situation.

․ Calculating Order point.

- 11 -

■ Inventory Management System. [Task 304]

Order Point System. ■ Safety Stock Determination. ․ Safety stock is intended to protect against uncertainty in supply and demand.

․ Safety stock Calculation.

1. SS = Sigma( σ) × safety factor (if LTI = FI)

2. SS = Sigma( σ) × LTIFI × safety factor (if LTI ≠ FI)

- 12 -

■ Inventory Management System. [Task 304]

Order Point System. ■ Fixed Time Systems (Cyclical Systems). ․ Time-based systems are designed so that each inventoried item is reviewed and reorders are placed after a predetermined time interval.

․ Orders are placed for each item equal to the difference between current inventory level and a predetermined maximum.

- 13 -

■ Inventory Management System. [Task 304]

Just-In-Time (JIT). ■ JIT Concepts. ․ JIT is an operations management philosophy of continuous improvement whose dual objectives are to reduce waste and reduce cycle time.

․ Waste is anything that does not add value for the customer. In general, reducing the various forms of waste will result in a reduction of inventories that are held to deal with the cause of the waste.

- 14 -

■ Inventory Management System. [Task 304]

Just-In-Time (JIT). ■ JIT Concepts and Purchasing. ․ Overproduction. Purchasing can reduce inventories by developing contract with regular releases to the supplier to eliminate receiving large orders. ․ Waiting. Reducing order processing time shorten leadtime, thus reducing the required inventory levels.

․ Transportation. Using local suppliers reduces the transit time for delivery.

- 15 -

■ Inventory Management System. [Task 304]

Just-In-Time (JIT). ■ JIT Concepts and Purchasing. ․ Processing. Through standardization it can reduce the number of part numbers, thereby reducing inventories.

․ Quality. Using early supplier involvement, supplier evaluation, supplier development, and certification, purchasing can improve the quality of goods coming into the organization, reducing the uncertainty of supply and lowering inventories.

- 16 -

■ Inventory Management System. [Task 304]

Just-In-Time (JIT). ■ Kanban Production. ․ A popular type of inventory control system is the use of 'Kanbans.' Loosely translated, kanban means "card" and is used to authorize the replacement of material as it is consumed.

․ The inventory level is controlled by setting the number of kanbans to be used in a process.

- 17 -

■ Inventory Management System. [Task 304]

Just-In-Time (JIT). ■ Kanban Production. ․ The kanban system works best when there is a relatively smooth flow in the operation and the demand is constant from day to day.

․ It also assumes that the process changeover time are relatively short, preferably less than ten minutes.

․ JIT Ⅱ Concept. This is an evolution of the traditional JIT practice, but include the presence in the purchaser's facility of a supplier representative responsible for scheduling and coordinating deliveries.

- 18 -

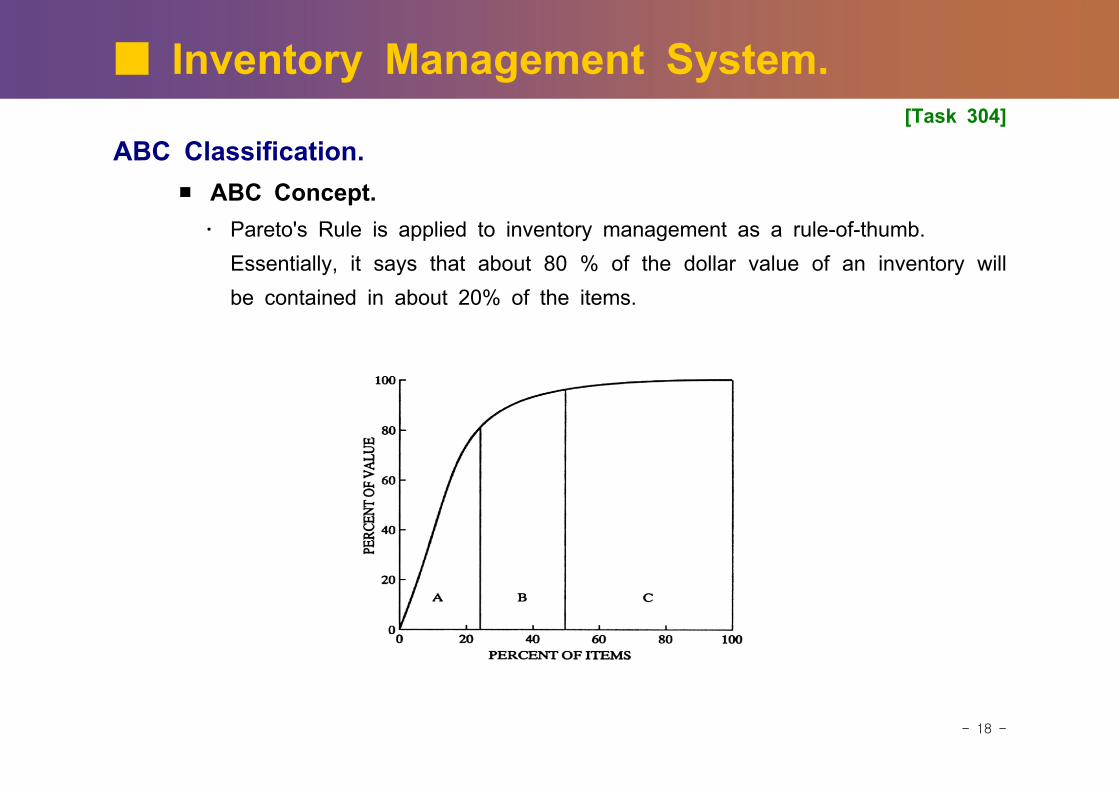

■ Inventory Management System. [Task 304]

ABC Classification. ■ ABC Concept. ․ Pareto's Rule is applied to inventory management as a rule-of-thumb. Essentially, it says that about 80 % of the dollar value of an inventory will be contained in about 20% of the items.

- 19 -

■ Inventory Management System. [Task 304]

ABC Classification. ■ ABC Concept. ․ ABC classification allow the manager to direct priorities for inventory control.

․ In general, higher turnover goals should be established for A and B items than for C items.

․ More control needs to be kept on A and B items, with low levels of safety stock. On the other hand, C items can be maintained with looser control but with higher amounts of safety stock.

․ In addition to other management procedures, ABC classifications used to design cycle counting schemes.

- 20 -

■ Inventory Management System. [Task 304]

Supplier Managed System. ■ Supplier Managed Inventory System ․ When business volumes is sufficient large, suppliers may operate an organization's supply or inventory storage facility using supplier personnel, under contract with the using organization.

․ Vendor Managed Inventory (VMI). VMI are inventories the supplier delivers to the work area or store and replenishes on a regular basis.

․ Consignment. Consignment inventories are inventories that are owned by the supplier.

․ Integrated Supply. The objective of an integrated supply relationship is to optimize, for both the purchaser and supplier, the labor and expense involved in the acquisition and possession of MRO products.

- 21 -

■ Inventory Management System. [Task 304]

Stores Management Systems. ■ Methods for Stores Management. ․ Open Stores. (or Point of Use) Inventory storage areas may be left open or kept close to the point of use for efficient user assess.

․ Closed Stores. (or Central Storage) Closed systems are used when close control and accounting of inventories are desirable. Goods enter inventory through a formal receiving process and leave through an authorized requisition or bill of materials.

․ Random Assess. (or Random location) In random assess systems, goods are stored without regard for commodity groupings. Instead, goods are stored in the next or nearest available space of suitable size.

- 22 -

■ Inventory Management System. [Task 304]

Inventory Performance. ■ Inventory Turnover Rate. ․ A convenient measure of how effectively inventories are being used is the inventory turns ratios.

Inventory Turnover = Annual cost of goods soldAverage inventory in dollars

■ Service Level. ․ Service level can be measured in a number of ways.

․ Order periods without a stockout, units supplied on time, operating days without a stockout, expediting expense, and number of production stoppage.

- 23 -

■ Inventory Management System. [Task 304]

Material Requirement Planning (MRP). ■ Material Requirement Planning. ․ MRP is a system of determining the quantity and timing of various materials and components required to produce a specified quantity of a finished product over a given period of time.

․ MRP Inputs : MPS, Bill of Materials, and Inventory Record.

․ Order Quantity ․ On-hand Balance․ Safety Stock ․ Allocated Qty ․ Lead-Time․ Low Level Code

: 50 units: 10: 0 : 0: 1 weeks: 0

Periods

1 2 3 4 5

A

Gross Requirements 25 0 15 20 30Scheduled Receipts 50Projected Available 10 35 35 20 0 20Net Requirements 30Planned Order Receipt 50Planned Order Release 50

- 24 -

■ Inventory Management System. [Task 304]

Distribution Requirement Planning (DRP). ■ Distribution Requirement Planning. ․ DRP optimizes planning for product distribution by determining time phased net requirements for distribution points.

- 25 -

■ Inventory Management System. [Task 304]

Enterprise Resource Planning (ERP). ■ Enterprise Resource Planning. ․ ERP is a term used to describe a variety of advanced MRPⅡ systems that integrate interfaces with customers, suppliers, and the global enterprise.

․ ERP provides a distributed application for planning, scheduling, and costing to the multiple layers of the organization, including work centers, plants, divisions, and the corporate organization.

- 26 -

■ Inventory Audit. [Task 304]

Inventory Valuation. ■ Accounting Valuation of Inventory. ․ Last-in, first-out (LIFO) In LIFO systems, the last goods received will be in the next issued. If the price of inventoried goods rises, higher reported expense and lower reported income for a given period will result.

․ First-in, first-out (FIFO) In FIFO systems, the oldest goods in inventory will be the next issued.

․ Average Cost in Storage. This method averages the cost per unit of an item in inventory by adding the value of goods received and those already on hand, and dividing that sum by the total number.

- 27 -

■ Inventory Audit. [Task 304]

Inventory Valuation. ■ Accounting Valuation of Inventory. ․ Lower of Cost or Market. Under this method, an organization is permitted to value inventory at its cost or fair market value, whichever is lower. Devaluing inventory when market value has fallen enables the organization to show the difference as an inventory adjustment and include it in the period expense as a cost-of-sale expense.

․ Retail Inventory Method. With this method the closing inventory value is determined by calculating the average relationship between the cost and retail values of merchandise available for sale during a period.

- 28 -

■ Financial Issues. [Task 305]

Inventory Cost. ■ Inventory Carrying Cost. ․ Finance Costs. Finance costs recognize that capital is required to finance the inventory.

․ Ownership Costs. Ownership costs are those associated with having material on hand. The two main components of ownership are insurance and taxes.

․ Overhead Costs. Overhead costs are costs associated with space, handling, and control.

․ Risk Costs. Risk costs are costs associated with having material on hand for a period of time. Examples include obsolescence, theft, damage, and shrinkage.

- 29 -

■ Financial Issues. [Task 305]

Inventory Cost. ■ Ordering Costs. ․ Ordering costs are the costs incurred to place an order with an external supplier. Ordering costs are incurred in the process of identifying suppliers and placing replenishment orders.

․ When the order is to be produced internally, the term "setup cost" is used in place of order cost. Setup costs may include direct setup labor, setup scrap, lost productivity and tooling costs.

- 30 -

■ Financial Issues. [Task 305]

Inventory Cost. ■ Stockout. ․ Stockout cost are the costs of not having the proper material on hand when it is needed. In general, stockout costs are among the hardest to measure because many organizations do not regularly collect this data.

․ Stockout cost can be divided into several categories, including extra production costs, extra transportation costs, extra clerical costs, costs of a lost customer, and lost revenue costs.

- 31 -

■ Financial Issues. [Task 305]

Other Financial Issues in Inventory Management. ■ Working Capital. ․ Working capital is defined as the current assets minus current liabilities. If too much of the organization's working capital is tied up in inventories, the organization's liquidity may be negatively affected.

■ Cash Flow. ․ If too many of an organization's assets are tied up in inventory, the organization may have an acceptable current ratio (current assets over current liabilities) but be cash poor. To obtain cash, the organization must turn the raw material and work-in-process inventory into finished goods that are then sold.

- 32 -

■ Financial Issues. [Task 305]

Other Financial Issues in Inventory Management. ■ Asset Turnover. ․ Asset turnover is calculated by dividing the cost of goods sold by the average value of the assets over a specific period. This is a measure of the productivity of the organization's assets.

․ Inventory affects this ratio because inventory is an asset. The higher the inventory, the greater the value of the asset and the lower the asset turnover ratio.

- 33 -

■ Financial Issues. [Task 305]

Other Financial Issues in Inventory Management. ■ Return On Investment (ROI). ․ ROI is a measure of return to the shareholder. ROI is calculated by dividing net profit by equity. It is the ratio of annual operating income to the total capital invested in the business.

․ As inventory increases, carrying costs such as interest costs, insurance, damage, and obsolescence increase, reducing profits and decreasing the return on investment.

- 34 -

■ Financial Issues. [Task 305]

Other Financial Issues in Inventory Management. ■ Commodity Speculation. ․ Commodity speculation involves purchasing quantities beyond normal or forecast usage (forward buying) in the belief that the price will go up and the organization will be able to sell the excess inventory at a substantial profit.

■ Exchange Rate Issue. ․ If the exchange rate moves in a direction favorable to the buyer, the purchase may consider forward buying to take advantage of the greater purchasing power of the dollar.

․ On the other hand, the purchaser would then scale back purchases, hoping for an exchange rate reversal.

- 35 -

■ Capacity Issue. [Task 305]

Capacity Issues in Inventory Management. ■ Seasonality. ․ The seasonal variation in usage of an item interacts with the capacity of the organization and the supplier's capacity to supply that item.

․ If it is undesirable to match production and purchasing levels with usage of an item, the organization may elect to build inventory during nonpeak periods to provide adequate material or product availability during peak periods.

■ Contingency Plans (e.g., disasters, strikes). ․ Inventories may be increased in anticipation of special events, such as threats of shortages caused by strikes, political instabilities, or natural disasters.

- 36 -

■ Capacity Issue. [Task 305]

Capacity Issues in Inventory Management. ■ Process Variation. ․ All process have variation. One of the functions of inventory is to provide protection against such variation. Purchasing needs to develop information on the natural variations of internal processes, as well as supplier production and delivery processes, in order to establish appropriate safety stocks and reorder points.

- 37 -

■ Sales & Marketing Related Issues. [Task 305]

Sales & Marketing Issues in Inventory Management. ■ Some Considerations. ․ New product introduction. Purchasing needs to be involved with marketing to ensure that the necessary raw materials, components, and/or products are available when production begins on a new product.

․ Product Discontinuance. Purchasing needs to be in contract with sales and engineering regarding the planned discontinuance of a product. The goal is to prevent the purchase of materials and components that are no longer needed by the organization.

․ Obsolescence. Purchasing has a responsibility to monitor the marketplace and work with internal departments to identify products and services being replaced with new technology or phased out by regulation.

- 38 -

■ Sales & Marketing Related Issues. [Task 305]

Sales & Marketing Issues in Inventory Management. ■ Some Considerations. ․ Promotional Activities. Marketing and supply management need to coordinate the availability of materials and products in anticipation of product promotions.

․ Forecasting Errors. Purchasing has a responsibility to work with internal customers and suppliers to identify the causes of forecast errors and to determine when a shift in operations, marketing, sales, customer demand, or other indicators may affect the need for a certain inventory level, restock level, or other inventory strategies.

․ Sales Plan Interface. Sales, production planning, and purchasing must work together to ensure compatibility between the sales plan and the supply plan.

- 39 -

Performance Check.

1. Which of the following seeks to transfer inventory responsibility to suppliers ? A. FIFO B. Dock to stock. C. Stockless buying D. Stores management systems.

2. All of the following are inventory control systems EXCEPT A. Order point. B. JIT C. TQM D. Cyclical.

3. For which of the following is the two bin inventory control system LEAST appropriate ? A. Low value items. B. High-value production materials. C. MRO supplies. D. Items with a short leadtime.

- 40 -

Performance Check.

4. In most organizations, safety stock is used to prevent stockouts when A. Materials is used sooner than expected. B. Leadtimes are met. C. Material arrives as scheduled. D. Inflation is increasing.

5. In ABC analysis, "C" item usually account for what percentage of the total dollar volume ? A. 5 - 10% B. 30 - 40% C. 50 - 60% D. 70 - 80%

6. Which of the following is NOT require to run an MRP systems ? A. Complete bill of materials. B. Sales forecast. C. Purchase price history. D. Current on-hand and on-order status.

- 41 -

Performance Check.

7. A purchaser is asked to calculate the raw material turnover rate for material on hand that day. Which of the following formula should the purchaser use ?

A. Yearly Sales (@ Selling Price)

Current Raw Material On Hand (@ Cost)

B. Current Raw Material On Hand (@ Selling Price)

Yearly Raw Material Usage (@ Cost)

C. Yearly Raw Material Usage (@ Cost)

Current Raw Material On Hand (@ Cost)

D. Current Raw Material On Hand (@ Cost)

Yearly Raw Material Usage (@ Cost)

- 42 -

Performance Check.

8. Which of the following would be considered a risk cost of inventory ? A. Insurance. B. Handling. C. Taxes. D. Obsolescence.

9. The two main components of the ownership costs of inventory are A. Space and handling. B. Insurance and taxes. C. Control and handling. D. Insurance and space.

10. The key to improving inventory performance is based on A. Managing the supplier base. B. Improving the organization's processes. C. Minimizing theft and damage. D. Maintaining sufficient safety stock.

- 43 -

Performance Check.

11. To maintain inventories of seasonal items, it is necessary to have a system that A. Forecasts usage and replenishment time. B. Considers overtime wages as production costs. C. Allows for shrinkage. D. Allows for alternate ordering quantities.

12. Extra transportation costs, as well as costs due to lost customers or lost profit margins, are example of A. Stockout costs. B. Ownership costs. C. Ordering costs. D. Risk costs.

- 44 -

Performance Check.

Solutions

1 2 3 4 5 6 7 8 9 10 11 12C C B A A C C D B B D A