ceo energy power conference -...

TRANSCRIPT

Barclays CEO Energy‐Power ConferenceSeptember 2017

Forward‐Looking & Other Cautionary Statements

The fol lowing presentation includes forward‐ looking statements. These statements relate to future events, such as anticipated revenues, earnings, business strategies, competit ive position or other aspects of our operations or operating results or the industries or markets in which we operate or participate in general, including our acquisit ion and acreage trading strategies, projections regarding our rig count and abil ity to work through our dril led but uncompleted well backlog, our expectations regarding our hedging program, our abil ity to dril l high value Merge wells that reduce leverage over t ime, our abil ity to enhance current spacing assumptions in Merge and Woodford, our abil ity to execute on our development plan in the Merge, including our dril l ing and leasing programs, projections regarding total production, average daily production, lease operating expenses, production taxes as a percentage of revenue, ad valorem taxes, cash G&A expenses and projected internal rates of return, and the results of our hedging program. Actual outcomes and results may differ material ly from what is expressed or forecast in such forward‐ looking statements. These statements are not guarantees of future performance and involve certain risks, uncertainties and assumptions that may prove to be incorrect and are diff icult to predict such as oil and gas prices; operational hazards and dril l ing risks; potential fai lure to achieve, and potential delays in achieving, expected reserves or production levels from existing and future oil and gas development projects; our abil ity to identify and consummate acquisit ions and other growth opportunities, including acreage trades; unsuccessful exploratory activit ies; unsuccessful acquisit ions; unexpected cost increases or technical diff iculties in constructing, maintaining or modifying company faci l it ies; potential l iabi l ity for remedial actions under existing or future environmental regulations or from pending or future l it igation; l imited access to capital or signif icantly higher cost of capital related to i l l iquidity or uncertainty in the domestic or international f inancial markets; an inabil ity to improve well spacing; general domestic and international economic and polit ical conditions, as well as changes in tax, environmental and other laws applicable to our business and other economic, business, competit ive and/or regulatory factors affecting our business generally as set forth in our f i l ings with the Securit ies and Exchange Commission (SEC). We caution you not to place undue rel iance on our forward‐ looking statements, which are only as of the date of this presentation or as otherwise indicated, and we expressly disclaim any responsibil ity for updating such information.

2

Jones Energy Overview

Note: Bonds, common and preferred share prices as of Sept 1, 2017.[1] Par value of $92mm ($50.00/share). 3

NYSE Ticker JONE

Common share price $1.08 Preferred share price [1] $26.00

Equity Market Cap ($mm)Common stock $106Preferred stock [1] 48

Total Equity market cap $154

Enterprise Value ($mm) ~$888

Common Stock Outstanding (mm)Class A 74.4Class B 23.7

Total common stock outstanding 98.1

Senior Unsecured Debt Outstanding ($mm)6.75% notes due 2022 $4099.25% notes due 2023 150

Corporate Snapshot

4

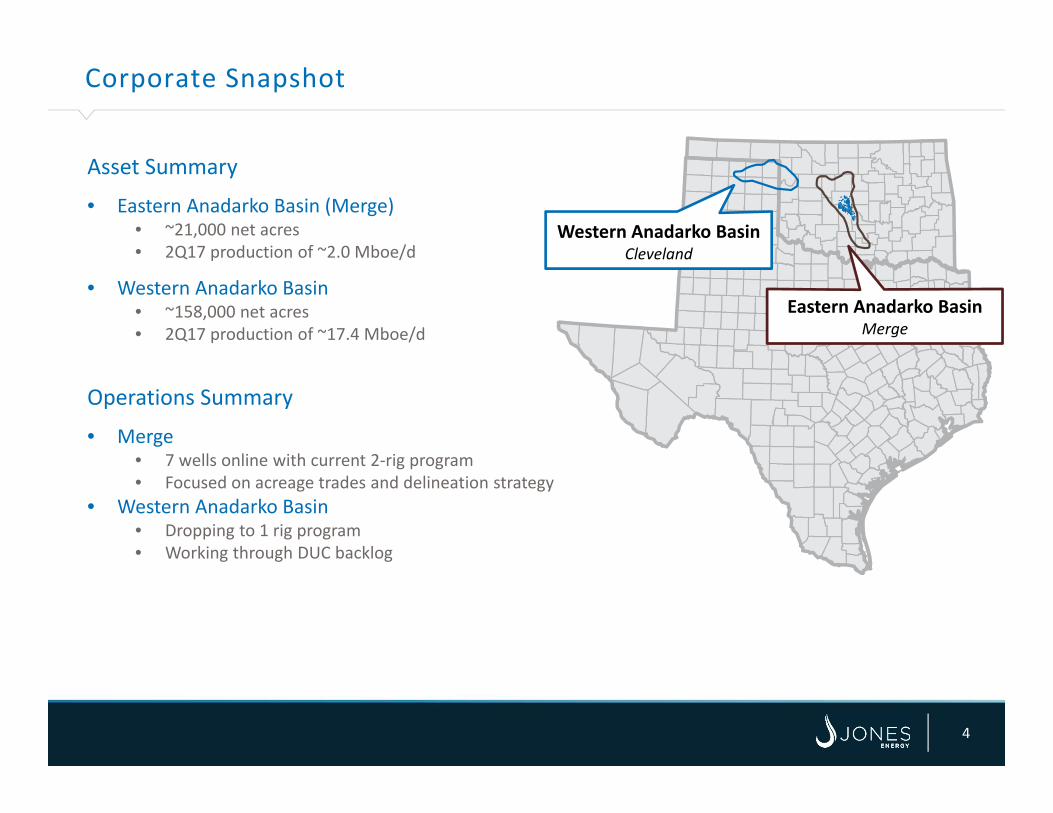

Asset Summary

• Eastern Anadarko Basin (Merge)• ~21,000 net acres• 2Q17 production of ~2.0 Mboe/d

• Western Anadarko Basin• ~158,000 net acres• 2Q17 production of ~17.4 Mboe/d

Operations Summary

• Merge• 7 wells online with current 2‐rig program • Focused on acreage trades and delineation strategy

• Western Anadarko Basin• Dropping to 1 rig program• Working through DUC backlog

Western Anadarko BasinCleveland

Eastern Anadarko BasinMerge

Financial Snapshot

5

Continue to manage the balance sheet and create financial flexibility• March 2017:

• Paid down revolver with $17.5 million from JEI to JEH via Class A stock dividend

• August 2017:

• Arkoma Woodford divestiture, sold for $65 million

• Proceeds used to pay down revolver

• Ongoing 2018/2019:

• Hedge unwinds bring forward value and pay down debt

• Undrawn revolver amount of $223 million[1]

• Working with lenders to create additional financial flexibility

• High PV Merge wells de‐lever the company over time

[1] As of August 31, 2017

What is the Merge Play?

Siluria

nDevon

ian

Mississippian

Blackjack Creek

Hunton

Chester/Caney

Springer Sands

AtokaMorrow

Cherokee

Oswego

Big Lime

Penn

sylvan

ian

Lower

Bois D’ Arc

Chimney Hill

Lower

Caney

Skinner

Prue

Anadarko Basin “Merge”Stratigraphic Column

Meramec

Osage/Sycamore

Woodford

Upper

Upper

Merge located between the STACK and the SCOOP within the Anadarko Basin

Key Points:• Unique and distinguishing

play characteristics• “Best of Both” attributes

including Meramec extension from STACK and Upper Woodford extension from SCOOP

• Multiple benches within proven productive zones

• Higher reservoir quality• Additional upside from

Hunton/Springer/etc.

JONE initial targets

STACK

NW STACK

MERGE

SCOOP

Mississippian Well

JONE Acreage

Woodford Well

Dewey Blaine

Caddo

Kiowa

Washita

Custer

Kingfisher

Grady

Comanche

Canadian

6

CLR Establishes SCOOP

2012‐13

2011 2011‐12

Merge Poised To Follow Similar Progression to SCOOP/STACK

7

NFX Identifies Meramec Potential While Pushing Woodford Up Dip

2015

Citizen Energy Gov. James well Establishes Meramec Potential In Merge

STACK Meramec AnnouncedInitial Delineation and development Focused North JONE Enters Merge

2016

Merge Consolidation, Delineation, and Development

CLR Drives Limit Of Meramec Production Down Dip In STACK & SCOOP

2017→

2016 Highlights: “Year of the Merge”

• JONE enters the Merge play, September 2016

• Meramec: aggressively moving westward into over pressured, higher GOR Osage & Meramec facies

• Woodford: tested different Woodford landing points and saw an increase in proppant loading

2017 To‐Date:

• Meramec: JONE begins delineation of 7 stacked, proven productive benches

• Woodford: JONE optimizes completion design. Offset operator density testing underway.

Jones AcreageWoodford Mississippian

STACK

MERGE

SCOOP

Grady

Caddo

CanadianOklahoma

Cleveland

McClain

Merge Upper Woodford Direct Extension of SCOOP

8

Upper Woodford flow unit extends northward across Merge originating from SCOOP.

• Landing points in the Woodford are defined by optimal rock properties.

• JONE has differentiated Upper and Lower Woodford landing points across position.

• Additional upside where both are present.

Ongoing completion optimization being driven by stage/cluster spacing and proppant loading.

JONE Acreage

Woodford Wells

Upper Woodford Thickness

Type Curve IP Range(Boe/d)

EUR Range(MBOE)

Oil%

Liquids%

Gross Locations

AFE Range($mm)

Woodford 600 –1,300

800 –2,000

25 –75%

55 –84% 1,833 $5.1 ‐ $5.8 Upper Woodford

Keys to Woodford Success: Frac Design Evolution

9

Initial Conclusions: Tighter stage spacing and greater proppant loading

driving well performance.GEN 3Today

GEN 2JONE enters the Merge

GEN 1Early Merge Drilling

GEN Proppant(lbs. / ft.)

Fluid Concentration(Bbls. /ft.)

Cluster Spacing(ft.)

Stage Spacing(ft.)

3 2,000 65 48 194

2 1,600 37 60 235

1 <1,500 ≥ 30 ≥ 60 ≥240

Merge Meramec Direct Extension of STACK

10

Continuation of Mississippian age (Meramec) reservoir from STACK

• Southern extent of position transitions to organic shale and limestone (Sycamore conventional reservoir)

• Play boundaries continually being pushed westward with additional delineation

• Net‐to‐gross pay is higher than STACK core.

Shale Dominated SCOOP Sycamore (Conventional)

Siltstone Dominated STACK Meramec (Unconventional)

Reservoir Qualifier

JONE AcreageUnconventionalConventional

Mississippian Wells

Type Curve

IP Range(Boe/d)

EUR Range(MBOE)

Oil%

Liquids%

Gross Locations

AFE Range ($mm)

Meramec 1,000 –1,500

950 –1,200

25 ‐50%

65 –75% 1,016 $5.4 ‐ $6.1

JONE Merge Position

1 Acreage closed and funded2 Net unrisked resource potential based on Company internal estimates

11

Merge Entry:September 2016

Today:September 2017

Net Acres: 16,9751 21,279

Operated Sections: 19 35

Total Sections: 219 235

Gross Loc.

Resource2(MMBoe)

Gross Loc.

Resource2(MMBoe)

Meramec 740 115 1,106 193

Woodford 1,375 215 1,833 271

Hunton 0 0 252 32

Springer 0 0 60 9

TOTAL 2,115 330 3,251 505

Producing Wells: 27 51

Net Production (Boe/d): 138 ~3,000

Merge Key Players and JONE Well Highlights

12

Gary 1H‐3601X7,249’ Lateral Length

Peak IP30: 699 Bo/d & 3,488 Mcf/d

Osborn 1H‐204,930’ Lateral Length

Peak IP30: 166 Bo/d & 2,620 Mcf/d

Lydia 1‐16H 4,795’ Lateral Length

Peak IP30: 436 Bo/d & 3,617 Mcf/d

Bomhoff 20‐12‐7 2H4,428’ Lateral Length

Peak IP30: 544 Bo/d & 4,777 Mcf/d

Huffman 2H‐30‐197,128’ Lateral Length

Peak IP30: 543 Bo/d & 3,114 Mcf/d

Rosemary 2H‐1‐367,506’ Lateral Length

Peak IP30: 1,023 Bo/d & 3,302 Mcf

Garrett 4‐11‐6 1H4,697’ Lateral Length

Peak IP24: 693 Bo/d & 2,344 Mcfd

Bomhoff 20‐12‐7 1H4,366’ Lateral Length

Peak IP30: 222 Bo/d & 3,015 Mcf/d

Toy Darrow 1H‐7‐68,128’ Lateral Length

Peak IP30: 315 Bo/d & 2,428 Mcf/d

Radcliff 1‐17H4,338’ Lateral Length

Peak IP30: 246 Bo/d & 1,776 Mcf/d

1

2

3

4

5 1 2

34

5

10

9

8

7

6

78

9

10

6

Merge dominated by STACK and SCOOP players

APACitizen/LINN CLR DVNEagle EnergyGPORJONE MRO NFXXEC

Meramec WellWoodford WellJONE OperatedJONE Non‐op

CANADIAN

OKLAHOMA

GRADY

CADDO

MC CLAIN

Production data are reported as actuals, not normalized.

OKLAHOMA

CADDO

CLEVELAND

MC CLAIN

CANADIAN

GRADY

Current Merge Rig Activity

13

Rigs by operator on the JONE Merge footprint

# of Rigs by Drilling Targets

Denotes JONE RigMeramec (6)Woodford (10)Hunton (3)Unknown (1)

Operator # of Rigs

Citizen Energy 3

NFX 3

JONE 2

LINN 2

XEC 2

89 Energy 1

APA 1

Casillas Petroleum 1

Chaparral Energy 1

EOG 1

Gaedeke Energy 1

Travis Peak Resources 1

Total 20

Rigs as of 8/31/2017. Source: Drillinginfo, IHS

Full Field Development on the Horizon

14

JONE Current Location InventoryPotential Upside Inventory (tests underway today)

1 Mile

TARGET

JONE Current

Assumption

Upside From

Industry

UPPER MERAMEC 4 8

LOWER MERAMEC 4 8

UPPER WOODFORD 8 8

LOWER WOODFORD 0 7

Per Section TOTAL 16 31

Density tests currently underway in both the Meramec and Woodford could significantly enhance current spacing assumptions.

Merge Development Plan

15Note:[1] Reliable technology areas (RTA); SEC mechanism for unconventional reserve booking. RTA data acquisition includes rock, fluids, and active/passive seismic.

2017

2018

2019

2020

2 rigs delineate acreage Secure leases Confirm optimal landing points

Potential to add additional rigs Continue delineation Optimize spacing, landing points, completion

Finalize spacing tests Prioritize landing points Optimize operations

Full scale development

Defined development areas of consistent geology [1]

Hydrocarbon phase Pressure gradient Landing point Drilling depth range

Multi‐year strategy to maximize resource value

JONE Acreage

RTA

Yukon

Tuttle

W. Minco

El Reno

E. Minco

49

13

2

40

12

520

5

10

15

20

25

30

35

40

45

50

A JONES(Last 9Wells)

JONES(All

Wells)

B C D E F

Average Drilling Da

ys per 15,00

0'

Operator

Average Drilling Days All Townships on JONE Footprint

Average Drilling Days Number of Wells

Driving Efficiencies in the Merge

16

JONE program advancing from delineation mode to first round optimization • Drill times for the last 9 wells decreased by ~30% over the first 4 wells• JONE wells now averaging less than 20 days drill time.• Reducing one day of drill time saves JONE ~$45K

~ 14% Faster

Well data has been normalized to measured depth of 15,000’ for comparison. Well data included 12 Merge townships. “Active Townships” includes all townships on JONE 2016‐2017 drill schedule. Operators included: CHK, Citizen, LINN, MRO, Travis Peak, and XEC

15

18

21

25 26

4

9

13

17

5

0

5

10

15

20

25

30

A JONES (Last 9Wells)

JONES (AllWells)

C D

Average Drilling Da

ys per 15,00

0'

Operator

Average Drilling Days Active Townships on JONE Footprint with > 3 Wells

Average Drilling Days Number of Wells

Upcoming Merge Catalysts

17

• Third Merge rig

• Long lateral drilling ‐ both 7,500’ and 10,000’ wells

• Specific bench testing

• Further completion optimization

• Pad drilling

• Density trials

• Gradual ramp in rigs

All in on the Merge!

APPENDIX

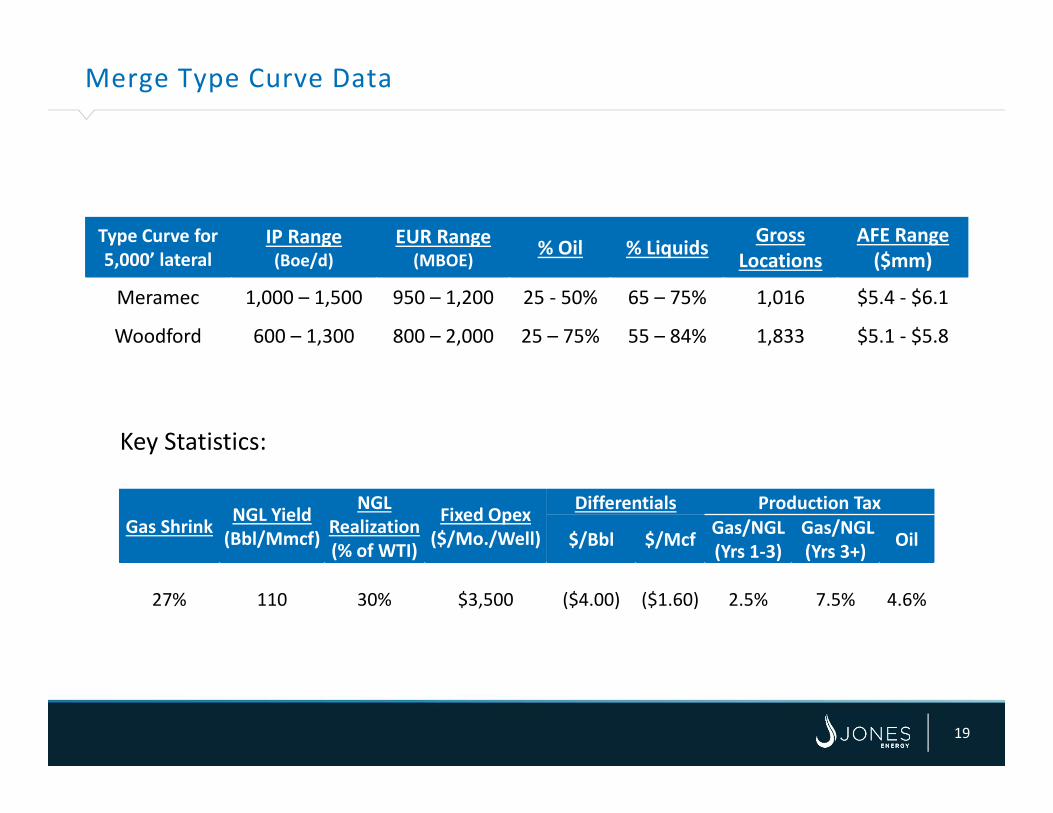

Merge Type Curve Data

19

Type Curve for 5,000’ lateral

IP Range(Boe/d)

EUR Range(MBOE)

% Oil % Liquids Gross Locations

AFE Range ($mm)

Meramec 1,000 – 1,500 950 – 1,200 25 ‐ 50% 65 – 75% 1,016 $5.4 ‐ $6.1

Woodford 600 – 1,300 800 – 2,000 25 – 75% 55 – 84% 1,833 $5.1 ‐ $5.8

Key Statistics:

Gas Shrink NGL Yield (Bbl/Mmcf)

NGL Realization (% of WTI)

Fixed Opex($/Mo./Well)

Differentials Production Tax

$/Bbl $/Mcf Gas/NGL (Yrs 1‐3)

Gas/NGL (Yrs 3+) Oil

27% 110 30% $3,500 ($4.00) ($1.60) 2.5% 7.5% 4.6%

2017 Guidance

20

Updated 2017E 3Q17ETotal Production (MMBoe) 7.6 – 8.0 1.8 – 1.9Average Daily Production (MBoe/d) 20.7 – 22.0 20.0 – 21.0Crude Oil (MBbl/d) 5.5 – 5.9 5.3 – 5.6Natural Gas (MMcf/d) 52 – 55.3 49.3 – 51.6NGLs (MBbl/d) 6.5 – 6.9 6.5 – 6.8

Lease Operating Expense ($mm) $40.0 – $45.0Production Taxes (% of Unhedged Revenue) * 4.5% – 5.5%Ad Valorem Taxes ($mm) * $2.7 – $3.0Cash G&A Expense ($mm) $23 – $25

Capital Expenditures ($mm)Merge JONE Operated D&C $83Merge Non‐Operated D&C and Other 17

Total Merge D&C $100Merge Leasing and Pooling 23

Total Merge Capital Expenditures $123Cleveland D&C $110Cleveland Leasing 5

Total Cleveland Capital Expenditures $115Other 12

Total Capital Expenditures $250

* Production and ad valorem taxes are included as one line item on the Company’s income statement.

Hedge Position

21[1] Swaps purchased to crystalize $15mm gainHedge position as of 9/1/2017

3Q17 4Q17 2017 2018 2019 2020Oil HedgesSwaps Sold (MBbl) 344 498 842 2,364 1,020 660 Price ($/Bbl) $62.78 $62.95 $62.88 $51.08 $50.04 $50.00

Swaps Sold (MBbl)[1] ‐ ‐ ‐ 294 ‐ ‐Price ($/Bbl) ‐ ‐ ‐ $78.58 ‐ ‐Offset Swaps Purchased (MBbl)[1] ‐ ‐ ‐ 294 ‐ ‐Price ($/Bbl) ‐ ‐ ‐ $46.79 ‐ ‐

Collars (MBbl) ‐ ‐ ‐ ‐ 810 ‐Floor ($/Bbl) ‐ ‐ ‐ ‐ $48.52 ‐Ceiling ($/Bbl) ‐ ‐ ‐ ‐ $59.64 ‐

Gas HedgesSwaps Sold (MMcf) 3,410 5,070 8,480 22,310 9,820 8,400 Price ($/Mcf) $3.72 $3.70 $3.71 $2.96 $2.83 $2.79

Swaps Sold (MMcf)[1] ‐ ‐ ‐ 3,930 ‐ ‐Price ($/Mcf) ‐ ‐ ‐ $4.27 ‐ ‐Offset Swaps Purchased (MMcf)[1] ‐ ‐ ‐ 3,930 ‐ ‐Price ($/Mcf) ‐ ‐ ‐ $2.81 ‐ ‐

Collars (MMcf) ‐ ‐ ‐ ‐ 11,890 ‐Floor ($/Mcf) ‐ ‐ ‐ ‐ $2.55 ‐Ceiling ($/Mcf) ‐ ‐ ‐ ‐ $3.19 ‐

NGL Swaps (MBbl)Ethane ‐ ‐ ‐ ‐ ‐ ‐Propane 154 227 381 850 ‐ ‐Iso Butane 16 24 40 120 ‐ ‐Butane 54 81 135 335 ‐ ‐Natural Gasoline 62 93 155 360 ‐ ‐Total NGLs 286 425 711 1,665 ‐ ‐

NGL Swap Prices ($/Gal)Ethane ‐ ‐ ‐ ‐ ‐ ‐Propane $0.47 $0.47 $0.47 0.57 ‐ ‐Iso Butane 0.57 0.57 0.57 0.72 ‐ ‐Butane 0.61 0.61 0.61 0.69 ‐ ‐Natural Gasoline 1.04 1.04 1.04 1.05 ‐ ‐

NGL Hedge Position Detail

22

3Q17 4Q17 2017 2018Mont Belvieu NGL Swaps (MBbl)Propane 20 30 50 60 Iso Butane ‐ ‐ ‐ ‐Butane 8 12 20 60 Natural Gasoline 8 12 20 60 MB NGLs 36 54 90 180

Mont Belvieu NGL Swap Prices ($/Gal)Propane $0.46 $0.46 $0.46 ‐Iso Butane ‐ ‐ ‐ ‐Butane 0.79 0.79 0.79 ‐Natural Gasoline 1.16 1.16 1.16 ‐

Conway NGL Swaps (MBbl)Propane 134 197 331 790 Iso Butane 16 24 40 120 Butane 46 69 115 275 Natural Gasoline 54 81 135 300 CW NGLs 250 371 621 1,485

Conway NGL Swap Prices ($/Gal)Propane $0.47 $0.47 $0.47 $0.57 Iso Butane 0.57 0.57 0.57 0.72 Butane 0.58 0.58 0.58 0.68 Natural Gasoline 1.02 1.02 1.02 1.05

Experienced Management Team

23

Eric Niccum(EVP & COO)

Joined Jones Energy in August 2011 23 years of industry experience Most recently Mid‐Continent Resource Manager and New Delivery Manager at BP for the Arkoma Woodford horizontal shale play Formerly Resource Manager at BP for the Anadarko Cleveland and Granite Wash horizontal drilling programs utilizing conventional and coil tubing drilling techniques Farmed‐out 28 Cleveland development wells to Jones in 2007‐2008 under an innovative cost cap deal structure Long history of field development at BP via horizontal drilling since 1995 Previously served various engineering and leadership roles in Louisiana and Deepwater Gulf of Mexico for BP / Amoco BS in Mechanical Engineering from Purdue University

Jonny Jones(Founder, Chairman & CEO)

Founded Jones Energy in 1988 33 years of industry experience focused in the US Mid‐Continent Formerly geologist with subsidiaries and affiliates of British Petroleum Active in the American Association of Petroleum Geologists and Independent Petroleum Association of America Served on the Advisory Council of the University of Oklahoma School of Geology and Geophysics and has been actively involved in fundraising efforts at the school Chairman of the U.S. Oil and Gas Association, immediate past Chairman of the Texas Oil & Gas Association Winner of Ernst & Young Entrepreneur of the Year 2012 Central Texas Award BS in Geology from the University of Oklahoma and an MA in Geology from the University of Texas

Mike McConnell(President)

Joined Jones Energy in 2004 33 years of industry experience Leads Jones Oklahoma City office Formerly CEO of the Generation and Production Group at Enron, CEO of Enron Global Markets LLC and President of Houston Pipe Line and Louisiana Resources Company Numerous other commercial positions in London and Houston Vice Chairman of the Independent Petroleum Association of America natural gas steering committee Past chairman of the Price Business School Board of Advisors for the University of Oklahoma BBA in Petroleum Land Management from the University of Oklahoma

Robert Brooks(EVP & CFO)

Joined Jones Energy in May 2013 25 years of industry experience Most recently Senior Managing Director and Head of Energy at Focus Capital Group Inc. / Whiteface Capital LLC Formerly served as Senior Managing Director and Head of U.S. Oil & Gas for Macquarie Capital Previously served as Principal at Bank of America Securities in the Global Energy and Power Group Prior to Bank of America, was Vice President in the Global Energy Group at Salomon Brothers BS in Mechanical Engineering from Massachusetts Institute of Technology, MS in Mechanical Engineering from Stanford, and MS in Management from Massachusetts Institute of Technology

Jeff Tanner(EVP – Geosciences)

Joined Jones Energy in September 2014 30 years of industry experience Most recently Vice President, Exploration for Southwestern Energy Formerly held a variety of leadership and technical positions for Laredo Petroleum, Cabot Oil and Gas, and Noble Energy Began career with Shell in Houston Member of the American Association of Petroleum Geologists and the Houston Geological Society B.S. in Geology from Texas A&M and an M.S. in Geology from the University of Houston

Corporate Structure

Jones Energy, Inc.

(NYSE: JONE)

Jones Energy Holdings, LLC(JEH LLC)

Class A Common Stock74.3 million shares

76% of voting power in Jones Energy, Inc.

24% of total common economic interest of JEH LLC

76% of total common economic interest of JEH LLC

Metalmark,Management

& Other Investors

PublicShareholders

Class B Common Stock23.7 million shares

24% of voting power in Jones Energy, Inc.

24